Palliative Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 165.27 Billion |

| Market Size (2031) | USD 244.01 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

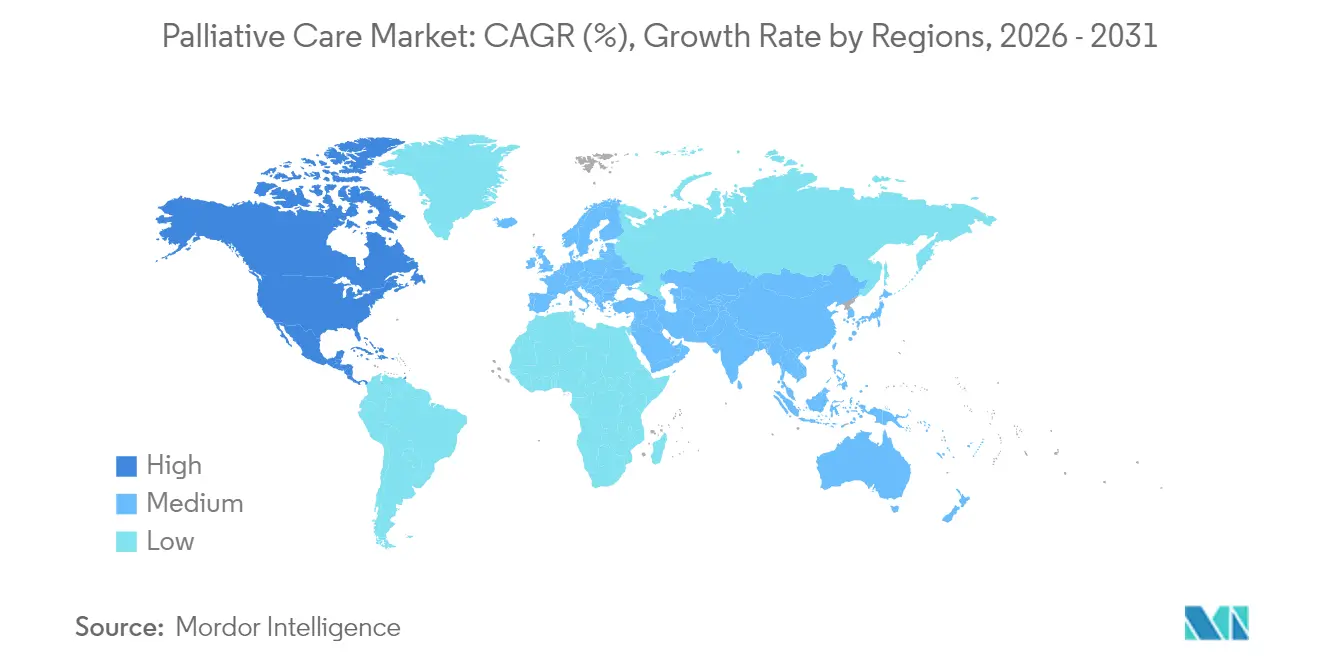

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Palliative Care Market Analysis by Mordor Intelligence

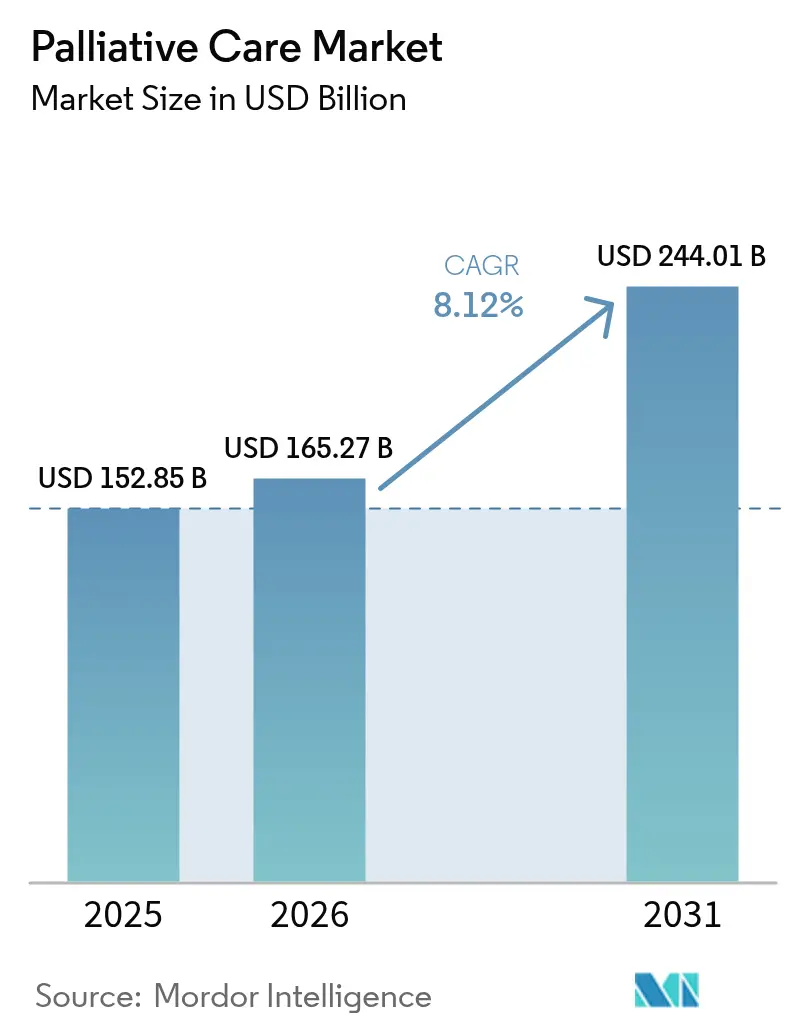

palliative care market size in 2026 is estimated at USD 165.27 billion, growing from 2025 value of USD 152.85 billion with 2031 projections showing USD 244.01 billion, growing at 8.12% CAGR over 2026-2031. Growth reflects demographic aging, surging chronic-disease prevalence, and shifting care models that prioritise quality-of-life outcomes. Cost-saving evidence from the Medicare Care Choices Model, which cut per-person spending by 13% while achieving 83% hospice uptake, has moved payers and providers to treat palliative care as mainstream rather than end-of-life support. Technology adds momentum: AI-enabled early-referral tools raised consultation rates by 8.5% without increasing overall visit volumes. Consolidation among home health and hospice operators further amplifies scale efficiencies, while reimbursement updates reward value-based delivery. Workforce shortages and high multi-disciplinary programme costs in low-income regions remain headwinds.

Key Report Takeaways

- By geography, North America led with 43.35% of the palliative care market share in 2025; Asia-Pacific is forecast to expand at an 10.98% CAGR to 2031.

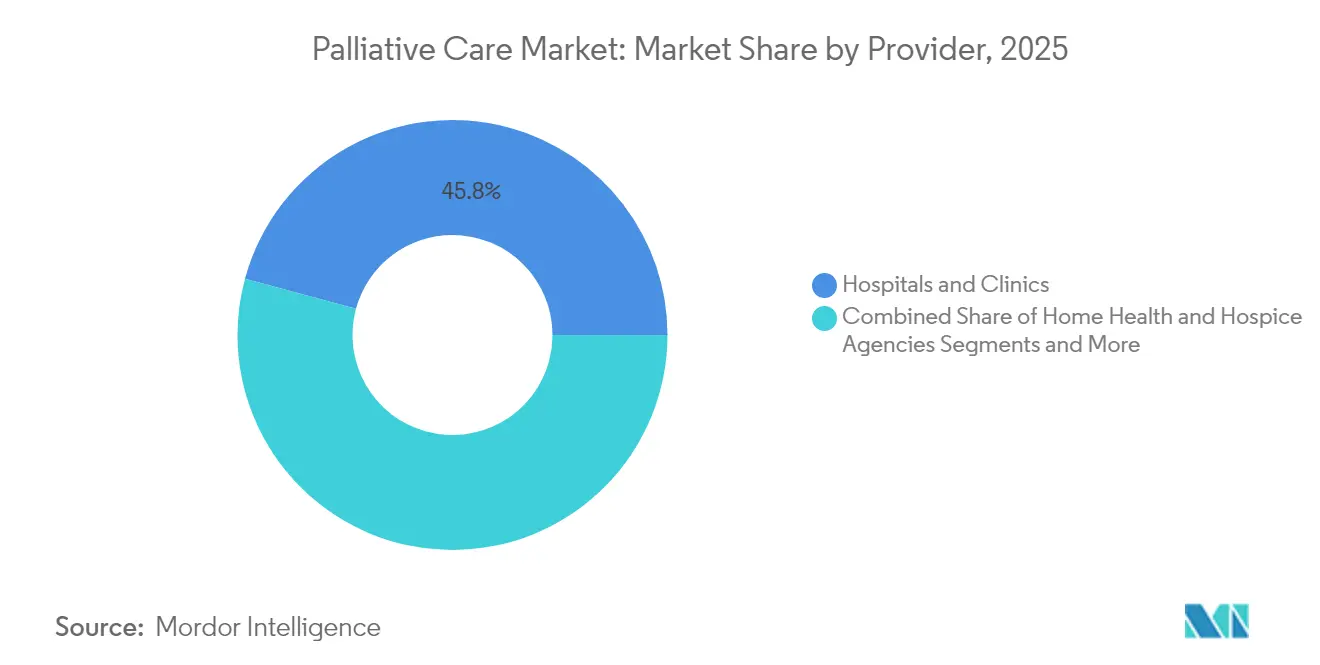

- By provider, hospitals and clinics held 45.78% of the palliative care market size in 2025, while home health and hospice agencies are advancing at a 9.18% CAGR through 2031.

- By care setting, routine home care accounted for 55.05% of the palliative care market share in 2025; tele-palliative and virtual care is projected to grow at a 9.92% CAGR to 2031.

- By service type, pain and symptom management represented 31.92% of the palliative care market size in 2025, whereas psychosocial and spiritual support is progressing at a 9.05% CAGR through 2031.

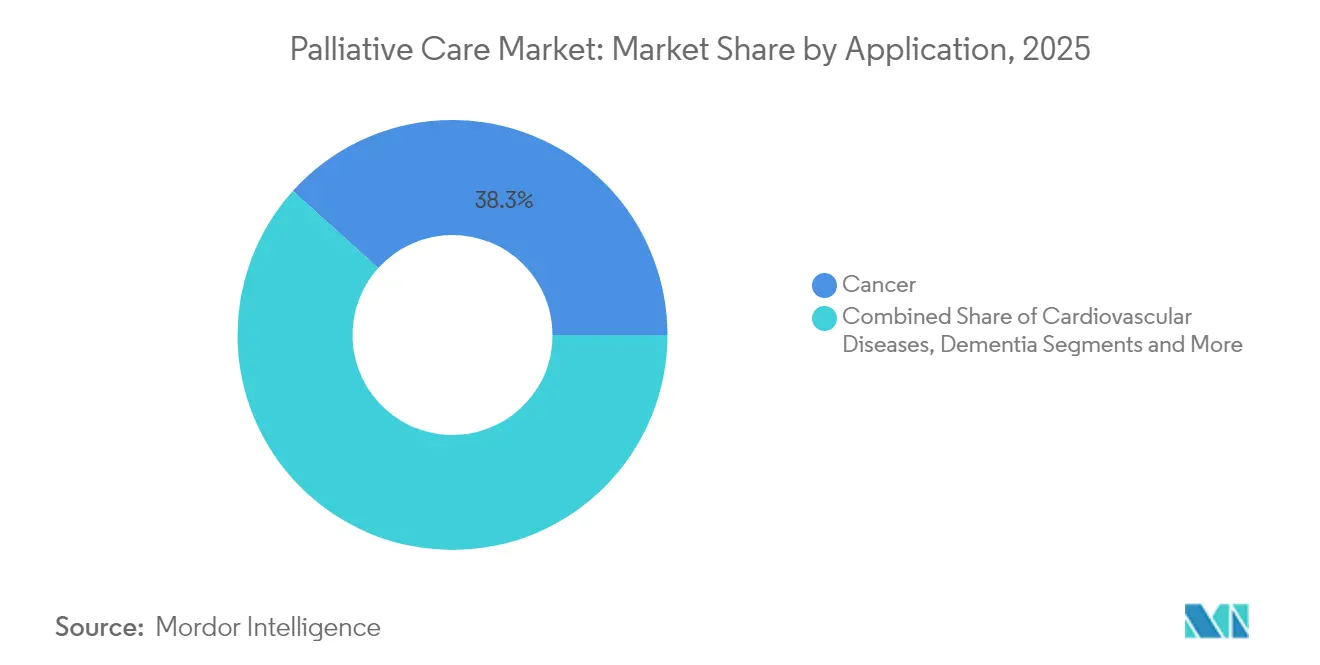

- By application, cancer maintained 38.32% of the palliative care market share in 2025; dementia and neuro-degenerative disorders are poised to increase at a 9.49% CAGR through 2031.

- By age group, adults commanded 84.10% of the palliative care market size in 2025, while paediatric and adolescent services are set to rise at a 9.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Palliative Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & rising chronic disease | +2.1% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Expansion of hospice & palliative centres | +1.8% | North America & APAC core; spill-over to MEA | Medium term (2-4 years) |

| Favourable reimbursement & value-based care | +1.4% | North America & EU; early adoption in Australia | Short term (≤ 2 years) |

| Integration into accreditation & quality | +1.2% | Global; led by North American regulators | Medium term (2-4 years) |

| AI-enabled early-referral algorithms | +0.9% | North America & EU; pilots in APAC | Short term (≤ 2 years) |

| Employer-funded serious-illness benefits | +0.7% | North America; emerging in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Rising Chronic Disease Burden

Worldwide, 48 million people are expected to die each year with serious health-related suffering by 2060, most in low- and middle-income nations [1]Katherine Sleeman, “Future Global Need for Palliative Care,” BMJ, bmj.com. Cancer incidence among those aged ≥65 is forecast to rise 70% by 2030, deepening demand for complex symptom control. Chinese studies report home-hospice patients scoring 115.7 on composite need scales, underscoring social and spiritual support gaps. In Europe, only 0.3% of older adults in Slovenia versus 30.4% in France die under palliative care, reflecting uneven capacity. Machine-learning frailty models predict palliative eligibility in elderly COPD patients with 92% accuracy, enabling earlier intervention.

Expansion of Hospice & Palliative Care Centers

Large operators are scaling; VITAS is entering 12 new US states as part of a multi-year build-out. Western Sydney’s new hospital-based unit illustrates similar capacity building in Australia. In Colombia, 504 palliative-care services now provide 1.8 facilities per 100,000 residents for primary care, yet specialised coverage averages only 0.4 per 100,000, highlighting urban–rural gaps. Cameroon counts 21 mainly faith-based organisations, but limited morphine supply and policy voids inhibit reach. Accreditation reinforces quality: the Joint Commission’s certification programme formalises interdisciplinary standards for inpatient units [2]Advanced Certification in Palliative Care,” Joint Commission, jointcommission.org .

Favourable Reimbursement & Value-Based-Care Incentives

Hospice payment rates climb 2.9% for fiscal-2025, adding USD 790 million to the payer pool. Each inpatient palliative consult reduces hospital costs by USD 1,310, a 13.6% saving that strengthens the business case. Home-health providers receive a 2.7% rate lift and recalibrated outlier payments in calendar-2025, supporting complex home-based cases. Alberta covers drugs, supplies and ambulances for registered palliative patients at no premium, showing provincial momentum. Quality reporting will tighten from October 2025 when the Hospice Outcomes and Patient Evaluation tool replaces legacy metrics.

Integration into Hospital Accreditation & Quality Metrics

The Joint Commission now measures pain screening, dyspnoea screening, goal-of-care discussions, and discharge documentation for certified programmes. Germany’s new specialist typology supports benchmarking across service models. Portugal identifies access inequity and coordination shortfalls, prompting indicator-based evaluations. In comparative audits, 20.5% of German nursing-home residents died in hospital versus 5.9% in the Netherlands, demonstrating metric impact on care location.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of multidisciplinary programs in LMICs | -1.6% | Sub-Saharan Africa, Latin America, South Asia | Long term (≥ 4 years) |

| Shortage of certified palliative specialists | -1.3% | Global, acute in rural North America & APAC | Medium term (2-4 years) |

| Opioid-stewardship regulations limiting pain protocols | -1.0% | North America & EU, emerging in APAC regulatory frameworks | Short term (≤ 2 years) |

| Cultural taboos delaying pediatric enrollment | -0.8% | APAC, MEA, Latin America with traditional family structures | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Multidisciplinary Programmes in LMICs

Cost-effectiveness studies show average monthly spend for home-based palliative care of USD 1,095 in the United States, USD 1,941 in Europe and USD 2,192 across Asian programmes, figures well beyond many low-income-country budgets. Zimbabwe’s need for cost-controlled home initiatives remains unmet despite compelling economic data. Latin American reviews cite accessibility, cultural perceptions and fragmented policy as persistent barriers. Training programmes for informal caregivers in Honduras were feasible but strained existing health budgets. A review of community-based models in Malawi, Uganda and Rwanda found evidence thin and funding unstable, limiting scalability.

Shortage of Certified Palliative Specialists

Healthcare executives rank workforce adequacy as their top 2025 risk, citing specialist scarcity. Pain-medicine fellowship applications have declined for five consecutive years, with widening gender disparity. In a US survey, 53.8% of advanced-practice nurses had five or fewer years’ palliative experience and 41% judged their formal education insufficient [3]Katherine Woltmann, “APRN Competencies,” Journal of Hospice & Palliative Nursing, journals.lww.com . Hybrid staffing models that pool social workers and chaplains between inpatient and home programmes are growing but remain resource constrained. The End-of-Life Nursing Education Consortium has trained 47,532 clinicians worldwide, yet demand continues to outpace supply. Rural communities lean on tele-health and expanded nursing scopes of practice, though cultural adaptation and paediatric cover remain obstacles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Provider: Hospitals Drive Volume While Home Agencies Capture Growth

Hospitals and clinics accounted for 45.78% of the palliative care market share in 2025 by virtue of established referral pathways and inpatient consult teams. Their programmes reduce average hospital costs, improve patient satisfaction, and operate as feeder channels to hospice services. Integration of AI-driven referral alerts is sharpening patient selection, enhancing financial returns and care quality. Home health and hospice agencies, while currently smaller, are forecast to post a 9.18% CAGR to 2031 as payment reforms shift incentives toward community settings. The palliative care market size for home-based providers benefits directly from a 2.7% uplift in the US Home Health Prospective Payment System, boosting margins for complex home visits.

Hospitals are leveraging interdisciplinary models to stabilise high-acuity patients then transition them to lower-cost venues. Leading systems have documented one avoidable admission per 1,000 resident-years in partner nursing homes after deploying dedicated palliative care teams. Home agencies are diversifying through mergers: Optum’s USD 3.3 billion Amedisys deal consolidates capabilities across 522 care sites, giving the buyer scale in 37 states. Community and faith-based NGOs continue to fill gaps in low-resource regions, as evidenced by Cameroon’s 21 grass-roots organisations that extend essential services where state coverage remains thin.

By Care Setting: Home Care Dominance Meets Virtual Innovation

Routine home care controlled 55.05% of the palliative care market in 2025, underscoring patient preference for familiar surroundings. Evidence shows each home-based plan of care can avert USD 10,000 annually in heart-failure costs by reducing hospitalisations. Tele-palliative and virtual visits represent the fastest-growing niche, with a projected 9.92% CAGR, as broadband penetration and remote-monitoring tools expand. Several large payers now reimburse video-based pain-management sessions at parity with in-office consultations, accelerating adoption.

In-patient settings remain crucial for complex symptom crises, yet many hospital teams now conduct an initial bedside evaluation then pivot to video follow-ups, minimising bed days. Out-patient clinics operate structured day programmes for infusion support and caregiver respite. Digital pilots such as Convoy-Pal have proven feasible among frail, multi-morbid seniors by combining asynchronous symptom tracking with scheduled nurse touchpoints. Wearable sensors tested in oncology wards successfully relayed continuous vital signs but require refinement in data fidelity before widespread roll-out.

By Service Type: Pain Management Leadership Faces Holistic Competition

Pain and symptom control held 31.92% of the palliative care market share in 2025, rooted in WHO analgesic ladder guidelines. German hospice audits found 89% adherence to stepwise protocols using drugs such as hydromorphone and pregabalin. Yet demand for psychosocial and spiritual interventions is climbing at a 9.05% CAGR as families seek emotional and existential support alongside pharmacologic relief. The palliative care market size for counselling services benefits from bundled payment pilots that reward holistic outcomes.

New e-health apps deliver real-time coaching on breathwork, guided imagery and medication titration. Physiotherapy, particularly respiratory therapy and gentle massage, is frequently prescribed but hampered by staff shortages and limited session time. Conversational AI agents help triage uncomplicated cases, escalating complex issues to human teams. Culturally tailored practice manuals have emerged for Korean American and Filipino American patients, emphasising values-based goal setting and family inclusion, broadening the service mix beyond Western norms.

By Application: Cancer Dominance Challenged by Neurological Growth

Cancer accounted for 38.32% of the palliative care market size in 2025, reflecting oncology’s early adoption of supportive care pathways. Predictive analytics within electronic health records now flag advanced cancer patients at risk of 12-month mortality with 0.861 AUROC, prompting earlier referrals and smoother transitions to hospice. Utilisation among metastatic breast-cancer cases climbed to 21% in 2024, though disparities persist for minority groups.

Dementia and other neuro-degenerative disorders are the fastest-rising application segment, set to grow 9.49% annually, driven by ageing populations and mounting caregiver burden. Japanese home-based studies show palliative sedation remains rare for non-cancer patients, suggesting under-served need. Chile projects overall palliative candidates will increase from 117,000 in 2021 to 209,000 by 2050, with non-cancer conditions driving the bulk of growth. Cardiovascular, respiratory, and renal failures follow closely, backed by evidence that palliative engagement is cost-neutral or cost-saving outside oncology as well.

By Age Group: Adult Focus Shifts Toward Pediatric Innovation

Adults represented 84.10% of the palliative care market share in 2025, consistent with chronic-disease prevalence in older cohorts. However, paediatric and adolescent services are advancing at a 9.29% CAGR as hospitals recognise unmet needs. Neonatal registries in Latin America cite trisomy 21 and complex congenital heart disease as leading diagnoses among infants receiving specialised palliation.

Early advance-care planning discussions improve alignment with family goals, yet cultural norms often delay conversations. Technology for home-based paediatric support raises questions of privacy, equitable access and role shifts within families. A four-theme model—child condition, service availability, parental capacity and overall family wellbeing—guides place-of-death decisions. Barriers to paediatric pain control include provider knowledge gaps and organisational inertia, while facilitators range from simulation training to family engagement and medication-delivery innovations.

Geography Analysis

North America commanded 43.35% of the palliative care market in 2025, propelled by Medicare coverage, extensive hospital consult services and active private-equity investment. US policy incentives such as a 2.9% hospice payment increase and quality-measure reporting strengthen financial sustainability. Canada’s provincial drug-and-transport coverage enhances cross-setting continuity, while employer-funded serious-illness benefits broaden access in commercial insurance lines. The palliative care market size for North America is further enlarged by consolidation, as large payers integrate home-health subsidiaries into coordinated networks.

Europe shows mature yet heterogeneous uptake. France records 30.4% of older adults receiving palliative services at end of life, whereas Slovenia remains at 0.3%. Germany’s typology project supports national benchmarking, and the Netherlands demonstrates low hospital-death rates after robust integration of home-based palliation. The European market’s steady 5.74% CAGR reflects alignment of accreditation standards, though specialist shortages in rural regions temper pace. Cross-border datasets fuel research and inform EU-level workforce planning initiatives.

Asia-Pacific is the fastest-expanding territory, expected to grow 10.98% through 2031 as demographic ageing accelerates and governments invest in hospice infrastructure. Japan refines non-cancer sedation protocols, while China pilots home-based models despite regulatory and cultural friction over family decision-making. Australia’s Western Sydney build-out exemplifies regional capital spend, and the Asia Pacific Hospice Palliative Care Network coordinates training and knowledge exchange. Market penetration remains uneven, especially in South-East Asia’s rural areas, but tele-health and NGO partnerships narrow some gaps.

Latin America is at an inflection point. Colombia now offers 1.8 primary palliative services per 100,000 residents yet struggles with geographic inequity; Amazonia and Orinoquia regions remain under-served. Chile projects doubling of serious-illness cases by 2050, and Brazil is rolling out national guidelines aimed at peri-urban clinics. Payment models remain largely fee-for-service, although Peru and Argentina are piloting bundled reimbursements tied to symptom-control metrics.

The Middle East and Africa face resource constraints. South Africa’s hospice network is sizeable but financing relies heavily on charitable donations. Zimbabwe evaluates cost-per-suffering-day averted, but scale-up is limited by drug availability. Nigeria and Kenya experiment with community-health-worker-led approaches, supported by international NGOs. Tele-palliative care via mobile platforms shows promise in remote desert and savannah regions, though connectivity and power stability issues persist.

Competitive Landscape

The palliative care market is moderately fragmented, yet consolidation is accelerating. UnitedHealth’s USD 3.3 billion acquisition of Amedisys places Optum at the vanguard of integrated home health and hospice services, reshaping competitive boundaries. Gentiva’s purchase of ProMedica’s home-health unit for USD 710 million signals continued private-equity interest in scale assets. Publicly reported quality scores show not-for-profit hospices outperforming for-profit and private-equity-backed peers, a reputational lever in hospital referral contracts.

Technology adoption is a key differentiator. Systems implementing AI-based referral algorithms reported an 8.5% increase in consults without raising staffing levels, enhancing return on investment. Start-ups in symptom-tracking, pain-app management and virtual support secure contracts with payers seeking outcome-based payment models. Established players partner with technology vendors to integrate wearables and remote monitoring into care pathways.

Regulatory compliance shapes risk profiles. Gentiva’s USD 19.4 million False Claims Act settlement underscores the cost of documentation lapses. Certified programmes must now meet Joint Commission metrics, prompting investment in data platforms capable of automated reporting. White-space remains in paediatric services, rural outreach and low-income-country expansion, where first movers can lock in referral relationships and build local brand equity.

Palliative Care Industry Leaders

Genesis Healthcare Corporation

VITAS Healthcare

Sunrise Senior Living LLC (Revera)

Amedisys

Lifepoint Health, Inc (Kindred Healthcare)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Center for Hospice Care expanded Kaleidoscope, its community-based programme, deploying interdisciplinary teams that deliver holistic services in patients’ homes.

- May 2024: Thyme Care named Dr Julia Frydman as its first Medical Director for palliative care, launching a virtual support service for cancer patients.

- March 2024: The United Nations Development Programme and the European Union supplied specialised vehicles to Ukrainian health facilities, strengthening mobile palliative capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the palliative care market as the total value of interdisciplinary medical, psychosocial, and spiritual services delivered across inpatient, outpatient, long-term-care, and home-based settings to patients with life-limiting illnesses. Revenues include professional fees, facility charges, hospice per-diem payments, and reimbursed tele-palliative visits recorded in 2025 global health accounts.

Scope Exclusion: Funeral services, bereavement counseling sold independently, and unlicensed volunteer care are not counted.

Segmentation Overview

- By Provider

- Hospitals & Clinics

- Nursing Homes & Skilled-Nursing Facilities

- Rehabilitation & Long-Term Care Centers

- Home Health & Hospice Agencies

- Community & NGO-run Centers

- By Care Setting

- In-patient Hospital

- Routine Home Care

- Out-patient / Day-care Clinics

- Tele-palliative / Virtual Care

- By Service Type

- Pain & Symptom Management

- Psychosocial & Spiritual Support

- Care Coordination & Case Management

- Bereavement & Family Support

- By Application

- Cancer

- Cardiovascular Diseases

- Chronic Respiratory Diseases (COPD, etc.)

- Dementia & Neuro-degenerative Disorders

- Renal & Hepatic Failure

- Other Life-limiting Conditions

- By Age Group

- Adult

- Pediatric & Adolescent

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed physicians directing hospital consult teams, executives at home-health operators, reimbursement specialists, and patient-advocacy leaders across North America, Europe, and Asia Pacific. Their insights helped validate prevalence-to-referral ratios, per-visit cost differentials, and likely technology adoption curves before we finalized our numbers.

Desk Research

Analysts first compiled service utilization and spend data from public sources such as WHO Global Health Expenditure Database, OECD Health Statistics, the National Hospice and Palliative Care Organization, CMS Medicare Cost Reports, and UN World Population Prospects. Company filings and investor decks, supported by D&B Hoovers screens, clarified provider mix and average reimbursement levels. Peer-reviewed journals (for example, Journal of Pain and Symptom Management) supplied evidence on referral timing and typical length of stay. The sources listed illustrate the breadth reviewed; many additional publications and databases informed gap checks and clarifications.

Market-Sizing & Forecasting

A top-down care-spend reconstruction starts with country inpatient and hospice expenditure, then allocates the palliative share by applying referral penetration and average length-of-service metrics. Selective bottom-up provider roll-ups (sampled occupied bed days multiplied by average per-diem or visit value) give a reasonableness check. Key variables embedded in the model include: 1) annual incidence of advanced cancer and other non-communicable diseases, 2) percentage of deaths receiving specialist palliation, 3) median length of stay by care setting, 4) nurse-to-patient staffing norms, and 5) average reimbursement per day or visit. Multivariate regression on aging rate, chronic-disease prevalence, and health-spend elasticity drives the 2026-2030 forecast, while scenario analysis adjusts for workforce shortages. Data gaps in low-income nations were bridged with proxy ratios from comparable economies, subsequently stress-tested during expert calls.

Data Validation & Update Cycle

Our outputs are tri-checked against independent mortality trends, insurer payout data, and historical hospice cost trajectories. Discrepancies trigger senior-analyst review and, if needed, a fresh expert call. The model refreshes annually, and material regulatory or reimbursement shifts prompt interim updates so clients always receive the latest vetted view.

Why Mordor's Palliative Care Baseline Earns Decision-Maker Trust

Published figures often diverge because firms differ on which care settings to include, the year chosen as baseline, and the rigor used to cross-verify input statistics.

Key gap drivers here stem from scope (home-based and tele-palliative inclusion), refresh cadence, and the depth at which unit economics are validated with frontline providers. Some estimates rely on outdated service-mix splits or extrapolate hospital data without reconciling the fast-growing community segment, whereas Mordor's analysts revisit both segments each year and adjust for currency shifts before final release.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 152.85 B (2025) | Mordor Intelligence | - |

| USD 137.80 B (2024) | Global Consultancy A | Earlier base year and exclusion of tele-palliative spend reduce value |

| USD 12.20 B (2021) | Regional Consultancy B | Counts hospital programs only and omits home hospice plus pediatric care |

| USD 8.40 B (2025) | Trade Journal C | Focuses on high-income countries and hospice services, not full palliative scope |

The comparison shows that when scope breadth, latest economic data, and yearly validation are combined, Mordor Intelligence delivers a balanced, transparent baseline that executives can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the current Palliative Care Market size?

The palliative care market is valued at USD 165.27 billion in 2026 with an 8.12% growth trajectory to 2031.

Who are the key players in Palliative Care Market?

Genesis Healthcare Corporation, VITAS Healthcare, Sunrise Senior Living LLC (Revera), Amedisys and Lifepoint Health, Inc (Kindred Healthcare) are the major companies operating in the Palliative Care Market.

Which is the fastest growing region in Palliative Care Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Palliative Care Market?

North America holds 43.35% of global revenue, driven by Medicare reimbursement and mature hospital consult programmes.

What is the main barrier to palliative care expansion in low-income countries?

High costs of multidisciplinary teams and limited drug availability hinder scale-up, reducing service penetration despite rising disease burden.

Page last updated on: