United States Long Term Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

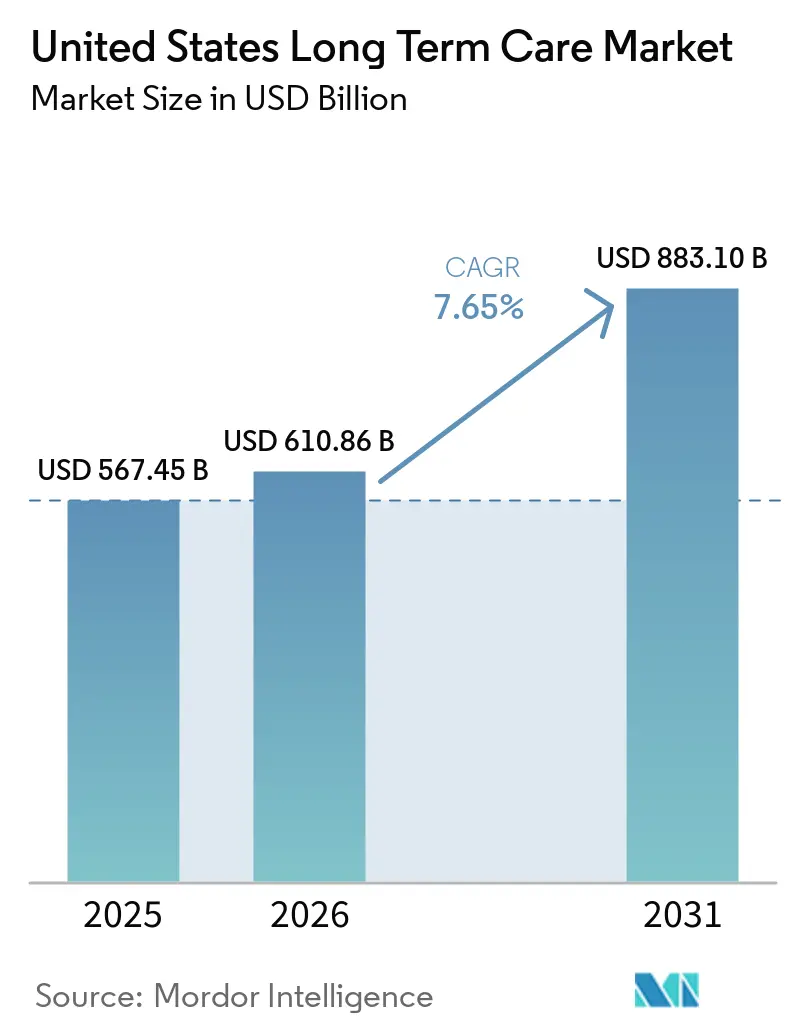

| Base Year Market Size (2025) | USD 567.45 Billion |

| Market Size (2026) | USD 610.86 Billion |

| Market Size (2031) | USD 883.10 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

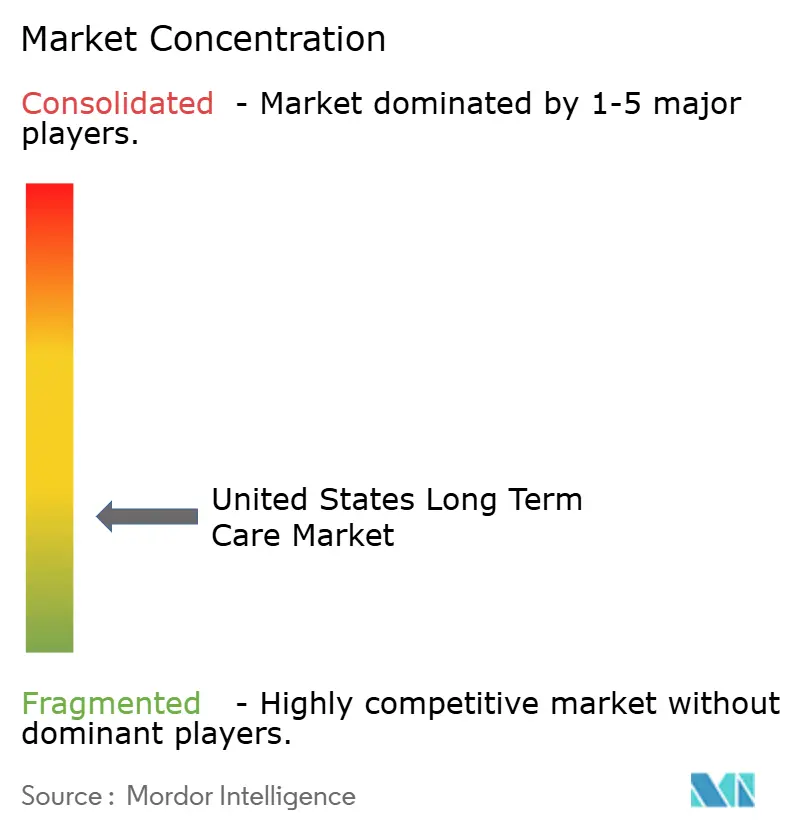

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Long Term Care Market Analysis by Mordor Intelligence

The United States Long Term Care Market size is projected to expand from USD 567.45 billion in 2025 and USD 610.86 billion in 2026 to USD 883.10 billion by 2031, registering a CAGR of 7.65% between 2026 to 2031.

In recent years, the aging population in the United States has grown significantly, increasing its share of the national demographic. This demographic shift has widened the gap between the demand for care and the available workforce, posing challenges for the United States (US) long-term care market. Public payer programs provide a stable reimbursement base, but policy changes are expected to impact Medicaid spending and access to services in several states. While the market remains fragmented, recent acquisitions and strategic moves by major players highlight the growing importance of scale, vertical integration, and disciplined acquisitions in shaping the competitive landscape. At the same time, the market faces a substantial number of projected job vacancies in direct care roles over the next decade. The reliance on immigrant labor remains critical, strengthening the case for technology-driven care models to enhance efficiency and safety in service delivery.

Key Report Takeaways

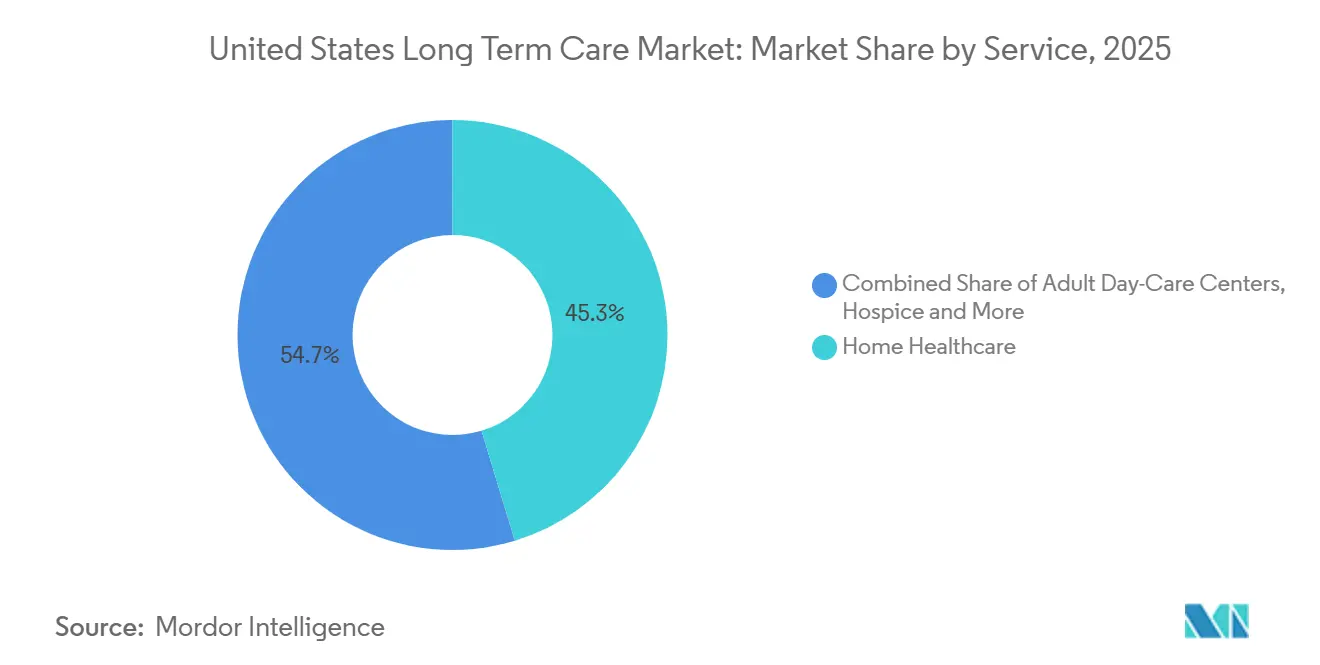

- By service, Home Healthcare held 45.31% of revenue in 2025, while Adult Day-Care Centers are projected to expand at a 9.38% CAGR through 2031.

- By payer, the Public payer segment held 56.24% of the United States long term care market size in 2025, while Managed-Care & Value-Based Contracts recorded the highest projected CAGR at 8.52% through 2031.

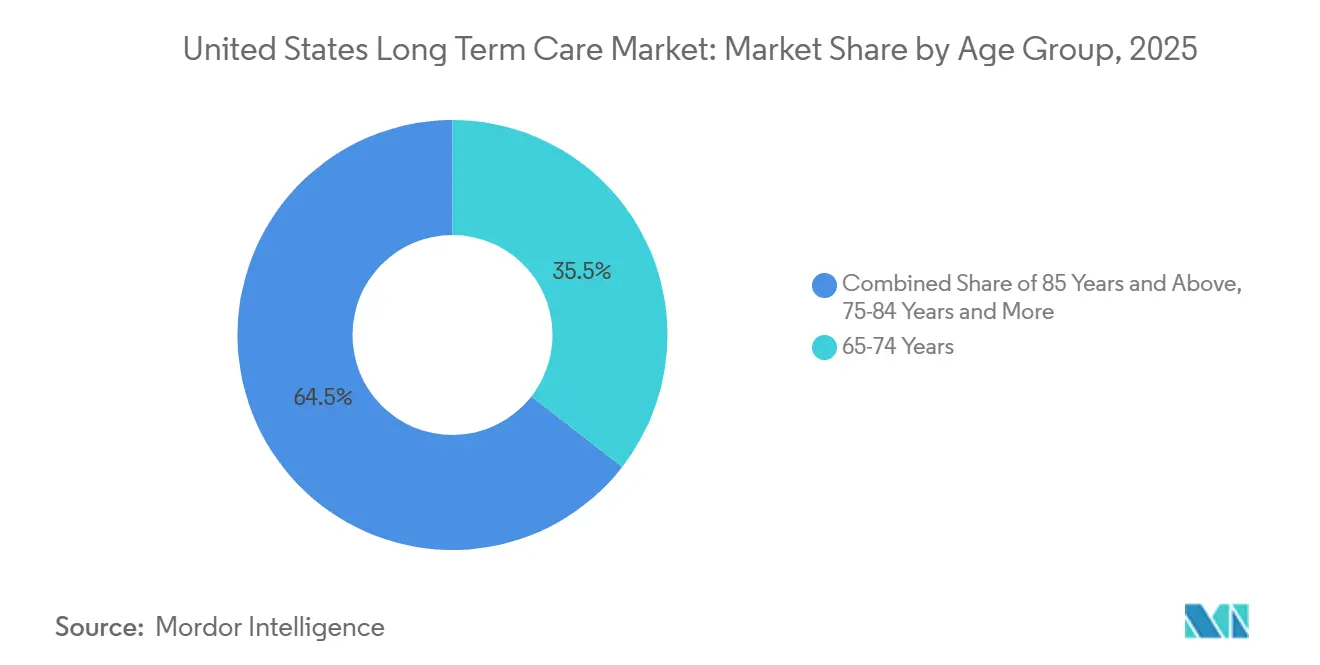

- By age group, the 65-74 Years cohort held 35.52% revenue share in 2025, while the 85 Years & Above cohort is forecast to grow at an 8.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Long Term Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Longevity | +2.2% | National, acute intensity in Florida, Arizona, South Carolina, and Sun Belt states | Long term (≥ 4 years) |

| Medicaid and Medicare HCBS Rebalancing | +1.5% | National, most pronounced in high-MLTSS states such as Tennessee, Texas, New Jersey, and New York | Medium term (2-4 years) |

| Aging-in-Place Preference | +1.3% | National, suburban and rural markets seeing accelerating home care demand | Long term (≥ 4 years) |

| Chronic Disease and Dementia Burden | +1.1% | National, above-average intensity in high-density 85+ states such as Florida, Pennsylvania, New York, and California | Long term (≥ 4 years) |

| Value-Based LTSS Contracting | +0.7% | National, early commercial gains in states running MLTSS programs | Medium term (2-4 years) |

| Immigrant Labor Access Sustaining Capacity | +0.5% | Florida, New York, New Jersey, and Massachusetts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Longevity Driving Structural Demand Expansion

The demographic base supporting the United States long term care market is expanding faster than most provider planning cycles and capital budgets can adjust. The population aged 65 and older reached 61.2 million in 2024, represented 18.0% of the U.S. population. By 2024, 11 states and nearly 45% of U.S. counties had more older adults than children, which shows how quickly this age shift has spread across local care markets[1]U.S. Census Bureau, “Older Adults Outnumber Children in 11 States, Nearly Half of Counties,” U.S. Census Bureau, census.gov. Brookings reported that nearly 1 in 5 adults aged 65 and older could not perform at least 1 activity of daily living, while the figure approached 2 in 5 among those aged 85 and older, which is a direct trigger for formal long term care use. As this aging pattern spreads across Sun Belt states and rural counties at the same time, the United States long term care market faces a location mismatch between existing facilities and the counties where demand is rising most quickly, and that gap will take years to close because development, licensing, and staffing all move slowly.

Medicaid and Medicare HCBS Rebalancing Reshaping Service Architecture

The shift from institutional care toward home and community-based care is now built into how the United States long term care market deploys funding, capacity, and care coordination. In 2023, 87% of 9.7 million Medicaid LTSS users received HCBS, and HCBS accounted for 63.8% of total LTSS spending of USD 228.6 billion, which confirms how far service delivery has already moved away from institutional models. All but 11 states used managed care for at least some home care delivery, and 26 states included 1915(c) waivers under managed care arrangements in 2025, up from 22 states in 2024, which shows that MLTSS adoption is still advancing. This policy direction is reinforcing demand for home care, adult day care, and other community-based formats while also changing how providers in the United States long term care market invest in documentation, network participation, and outcomes management. KFF projected that the 2025 reconciliation law will reduce federal Medicaid spending by USD 911 billion over 10 years, and because HCBS programs are optional, states may respond by tightening enrollment or lowering reimbursement if budget pressure deepens. CMS also finalized the 2028 HCBS Quality Measure Set with mandatory reporting beginning in fall 2026, which creates added compliance work that will weigh more heavily on smaller HCBS providers with limited technology infrastructure[2]Federal Register, “Medicaid Program, 2028 Medicaid Home and Community-Based Services Quality Measure Set,” Federal Register, thefederalregister.org.

Aging-in-Place Preference Creating Durable Uplift for Home-Based Services

Consumer preference for receiving care at home has moved beyond a lifestyle choice and has become a durable demand driver in the United States long term care market. Northwestern Mutual reported in October 2025 that 74% of Americans preferred in-home care in the event of a long-term care episode, while only 11% said they would choose a nursing home. Pew Research Center also reported in February 2026 that most older adults who live at home want to remain there as they age, even though many are not fully confident they will be able to do so. This preference supports a sustained shift toward home healthcare, adult day care, caregiver support, and home adaptation services rather than lower-acuity institutional placement. It also gives providers with strong scheduling systems, better caregiver continuity, and family communication tools a practical edge because families want care settings that preserve independence without losing supervision. As a result, aging in place is likely to keep lifting home-based volumes even when public reimbursement conditions become harder.

Chronic Disease and Dementia Burden Raising Per-Beneficiary Intensity

The sharpest rise in care intensity inside the United States long term care market is tied to chronic disease, dementia, and multi-morbidity in older beneficiaries. USC Schaeffer reported that 5.6 million Americans were living with dementia in 2025 and that the total societal economic burden reached USD 781 billion, including USD 232 billion in direct medical and long-term care expenditures. The same center reported that annual medical spending for Medicare fee-for-service beneficiaries with dementia averaged USD 44,700 in 2023, adjusted to 2025 dollars, and ranged from USD 57,700 in California to USD 31,500 in Montana. A 2025 Nature Medicine study found that more than 42% of Americans aged 55 and older will develop dementia during their lifetime, and annual new diagnoses are projected to rise from 514,000 in 2020 to nearly 1 million by 2060. This burden is raising acuity across home healthcare, assisted living, and adult day care, which means providers that build memory care programs, dementia-trained staff, and stronger caregiver support will be better positioned to capture long-duration demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Direct-Care Workforce Shortages | -1.5% | National, most severe in rural areas and states with limited HCBS waiver funding | Long term (≥ 4 years) |

| Wage Inflation and Reimbursement Lag | -1.1% | National, most severe in high cost-of-living states such as California, New York, and Massachusetts | Medium term (2-4 years) |

| Immigration Policy Tightening Caregiver Supply | -0.8% | Florida, Massachusetts, New York, and New Jersey | Short term (≤ 2 years) |

| Cyber and Privacy Risk in Connected Care | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Direct-Care Workforce Shortages Constraining Supply-Side Capacity

Workforce availability remains the clearest operating restraint across the United States long term care market because labor demand is growing faster than new worker supply. PHI projected 8.9 million direct-care job vacancies between 2024 and 2034, including roles created by growth, turnover, and labor force exits. PHI also reported that home care alone will face 6.1 million job openings by 2034, after the home care workforce expanded from 1.4 million in 2014 to 3.2 million in 2024. ANCOR reported in 2025 that 88% of community-based providers were experiencing moderate or severe staffing shortages, 62% had turned away referrals because of inadequate staffing, and 52% were considering additional program cuts if conditions did not improve. PHI further reported that the median hourly wage for home care workers was USD 16.77 in 2024, with 15% living below the poverty line and more than 40% living in low-income households, which shows that the constraint extends beyond pay and into job quality, career mobility, work hours, and benefits.

Wage Inflation and Reimbursement Lag Compressing Provider Margins

Margin pressure remains one of the most persistent growth restraints in the United States long term care market because labor costs move faster than public reimbursement updates. CareScout reported that the national median monthly cost of assisted living reached USD 6,200 in 2025, while a nursing home semi-private room reached USD 9,581 per month, which shows how quickly operating costs are feeding through to end pricing. KFF reported that 39 states raised HCBS rates in FY 2024 and 32 states did so in FY 2025, but the same policy environment now faces added pressure from the projected USD 911 billion federal Medicaid reduction over the next decade. KFF also noted that during the last major Medicaid funding reduction, 47 states cut home care spending and 40 states served fewer people, which gives current providers a clear historical reference for how rate pressure can translate into access cuts. Larger operators can offset part of this pressure through scale, stronger revenue cycle systems, and a more diversified payer mix, while providers that depend heavily on a single state Medicaid program remain more exposed to consolidation or exit. This gap in financial resilience is already shaping which companies can keep expanding capacity and which companies must slow growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Home Healthcare Anchors the Market While Adult Day Care Defines the Growth Frontier

Home Healthcare held 45.31% of the United States long term care market share in 2025, which reflects the strength of community-based delivery, public HCBS funding, and family preference for care at home. Richmond Fed reported in January 2026 that CMS programs reimburse more than 50% of total U.S. home health expenditures, and Medicaid accounted for nearly two-thirds of home care spending in 2023, which confirms the segment’s deep public funding base[3]Richmond Fed, “Home Health Care and Aging in Place,” Richmond Fed, richmondfed.org. Nursing Care and Assisted Living Facilities remained the next largest service groups, but they are moving in different directions within the United States long term care market. Nursing care faces gradual pressure in lower-acuity cases because more families prefer to delay institutional placement and use home-based services first. Assisted living is benefiting from seniors who need daily supervision but not full clinical intervention, and Brookdale management said average occupancy was tracking toward 90% in 2026, which signals steady demand recovery in that setting.

Adult Day-Care Centers are projected to grow at an 9.38% CAGR between 2026 and 2031 within the United States long term care market size. That pace stands 173 basis points above the overall market growth rate and reflects the segment’s role as a supervised bridge between home care and full institutional admission. CareScout reported that the national median daily rate for adult day health care was USD 95 in 2025, which supports its value case for families and public programs seeking lower-cost care intensity. The segment also fits closely with HCBS waiver structures and state efforts to prevent institutional admission, which supports continued demand as care continues to move into community settings across the United States long term care industry. Hospice remained smaller in revenue share, but it retained solid margin potential as the 85+ population expanded and palliative care acceptance broadened.

By Payer: Public Payer Dominance Faces Value-Based Disruption

The Public payer segment represented 56.24% of the United States long term care market size in 2025, which reflects Medicaid’s central role in LTSS and Medicare’s importance in post-acute skilled nursing and home health. This payer mix gives the United States long term care market a broad and durable funding base, even though policy shifts can quickly alter reimbursement conditions. KFF reported that Medicaid home care programs were serving more than 5.1 million beneficiaries annually in 2025, which shows the scale of public payer reach in community-based services. Out-of-pocket and self-funded spending, together with private insurance, remain more relevant for higher-income households that are bypassing public program waitlists or choosing extra service flexibility. Pew Research Center reported in February 2026 that only 21% of U.S. adults aged 65 and older held long-term care insurance, which leaves a wide coverage gap and supports demand for private-pay service bundles.

Managed-Care & Value-Based Contracts is the fastest-growing payer segment, with an 8.52% CAGR between 2026 and 2031. KFF reported that managed arrangements already reach a large share of home care delivery across states, especially in markets with MLTSS programs, which keeps moving reimbursement away from simple fee-for-service logic. This segment matters because it requires risk-adjusted patient attribution, timely functional assessment data, and outcomes reporting that many smaller operators still cannot support at scale. Providers with stronger technology platforms and cleaner clinical data are therefore better placed to secure these contracts and retain them over time. That dynamic suggests payer growth will continue to favor larger, better-instrumented operators rather than fragmented independent providers.

By Age Group: The 65-74 Cohort Defines Current Volume While the 85+ Cohort Defines Future Intensity

The 65-74 Years cohort held 35.52% of the United States long term care market share in 2025, making it the largest age-based demand pool by current volume. This cohort supports broad utilization through early functional assistance, chronic disease management, and strong participation in community-based care formats. Many beneficiaries in this group are still able to remain at home with moderate support, which keeps home healthcare and waiver-based services central to the care mix. The 30-64 Years and 0-29 Years groups represent a clinically different population that relies more heavily on disability-related HCBS waiver structures than on age-driven care demand. These younger age bands are smaller in revenue share, but their volumes tend to remain steadier because utilization is linked more to eligibility pathways and ongoing care needs than to demographic aging alone.

The 85 Years & Above cohort is projected to expand at an 8.28% CAGR between 2026 and 2031. That growth changes the acuity profile of the United States long term care market because frailty, dementia, and multi-morbidity rise sharply at the oldest ages. USC Schaeffer reported that dementia prevalence among Medicare fee-for-service beneficiaries aged 86 to 90 exceeded 25% in 2023 data, and combined medical and long-term care costs averaged USD 44,700 per person, rising to USD 54,500 for dual-eligible individuals. The 75-84 Years segment remains the transition zone where home healthcare and adult day care often reach peak use before beneficiaries move into higher-intensity settings. Providers that build relationships early in that transition are better positioned to retain beneficiaries as they move into the higher-acuity 85+ stage, where care complexity and revenue intensity are both materially higher.

Geography Analysis

The South and Southeast are the highest-intensity demand areas for the United States long term care market in 2026 because they combine fast population aging with active provider expansion. Florida remains a focal state because it has one of the densest older adult populations in the country and continues to attract hospice and home-based capacity investments. VITAS announced in May 2026 that it had expanded its hospice service footprint to 61 of Florida’s 67 counties, which shows how providers are targeting statewide coverage in high-demand aging markets. VITAS also broke ground in April 2026 on a new 14,000-square-foot inpatient hospice center in Port St. Lucie that is expected to open in 2027, which points to continued infrastructure buildout beyond routine service-line expansion. Texas is attracting large-scale capital as well, and The Ensign Group’s May 2026 transaction added 17 facilities, more than 2,000 skilled nursing beds, and 100 senior living units in the state, which signals confidence in its regulatory setting and long-run demand base.

The Northeast remains one of the most operationally demanding parts of the United States long term care market because care costs are high and managed home care penetration is deep. New York, New Jersey, Massachusetts, and Pennsylvania stand out for their reliance on managed structures in home and community-based services, which raises expectations around documentation, network participation, and performance reporting. Pennsylvania and Ohio also remain major skilled nursing corridors, which supports stable demand but keeps labor management and quality performance under constant pressure. Indiana is emerging as a Midwest growth pocket after Addus HomeCare entered the state in May 2026 through the acquisition of HomeCourt Home Care and a second comparable Indiana transaction tied to Medicaid rate improvement and waitlist reduction efforts.

The West shows where the United States long term care market is becoming most operationally complex because cost structures, dementia burden, and HCBS adoption are all elevated. California recorded the highest per-person annual medical spending for Medicare fee-for-service beneficiaries with dementia at USD 57,700, compared with USD 31,500 in Montana, which highlights how sharply revenue opportunity and care cost can vary across states. California, Michigan, and Washington added new day services coverage for intellectual and developmental disability waivers in 2025, which signals continued state support for broader community-based integration. Stronger aging-in-place preference, higher labor cost pressure, and more mature managed care frameworks make the West a useful signal for how service design and reimbursement expectations may evolve across the rest of the country.

Competitive Landscape

The United States long term care market remained structurally fragmented in 2026, and no single operator controlled more than a low-single-digit share of national revenue. Even so, consolidation is moving quickly across skilled nursing, home health, hospice, and adjacent community-based services. The Ensign Group offers one of the clearest examples of scale-led growth, after completing 71 acquisitions in 2025 and operating 395 healthcare operations across 17 states in 2026. Its Q1 2026 same-facility occupancy of 84.3%, quality outperformance of 22% to 31% against state and county peers, and quarterly revenue of USD 1.39 billion show how scale can improve staffing resilience, clinical performance, and financial execution. This pattern is raising the competitive bar in the United States long term care market because smaller regional operators are increasingly competing against larger systems with stronger labor, data, and reimbursement capabilities.

The UnitedHealth Group-Amedisys transaction, completed in August 2025 after DOJ-required divestitures to BrightSpring Health Services and The Pennant Group, brought a vertically integrated insurer-provider platform deeper into home health and hospice. That structure creates advantages in referral flow, data visibility, and care coordination that are difficult for pure-play providers to reproduce on their own. BrightSpring reported that the divested Amedisys and LHC Group assets added USD 79 million in Q1 2026 revenue, which shows how antitrust remedies can also accelerate scale for second-tier competitors. These transactions suggest that future share shifts in the United States long term care market are likely to come more from acquisition pipelines, asset transfers, and integration quality than from large waves of new independent entrants.

White space remains concentrated in rural HCBS access, dementia-focused care delivery, and the technology infrastructure needed to support value-based reimbursement. KFF reported that nearly 700,000 people remained on Medicaid HCBS waitlists nationally in 2025, which shows how much unmet demand still exists despite years of community-based policy expansion. VITAS is pursuing a certificate-of-need-led de novo strategy in Florida, and its December 2025 award followed by 2026 expansion activity shows how regulated entry can create durable local barriers in select states. Across the United States long term care market, the operators most likely to gain share are the ones combining disciplined acquisitions, selective de novo expansion, and stronger clinical data systems as public and managed care contracts become more demanding.

United States Long Term Care Industry Leaders

The Ensign Group

Brookdale Senior Living

VITAS Healthcare

Addus HomeCare

Sunrise Senior Living

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: VITAS Healthcare announced entry into Manatee County, Florida, bringing its hospice service footprint to 61 of Florida's 67 counties. The expansion reflects VITAS's CON-driven de novo strategy to reach approximately 88% of Florida's population, following a Certificate of Need award in December 2025.

- May 2026: Addus HomeCare completed its acquisition of HomeCourt Home Care in Fort Wayne, Indiana, annualized revenue of approximately USD 9.7 million, and entered into a second Indiana acquisition agreement of comparable size, marking the company's entry into a state with active Medicaid rate improvement and waitlist reduction efforts.

United States Long Term Care Market Report Scope

As per the scope of the report, long term care refers to a range of services and support provided over an extended period to individuals who have a chronic illness, disability, or other condition that impairs their ability to perform everyday activities independently. These services can include assistance with personal care, medical management, and daily living activities, and are typically provided in settings such as homes, nursing facilities, or assisted living communities.

The United States long-term care market is segmented by service into home healthcare, hospice services, nursing care services, assisted living facilities, and adult day-care centers. By payer, the market is categorized into public funding, private insurance plans, out-of-pocket payments, and managed-care & value-based contracts. Additionally, by age group, the segmentation includes 0-29 years, 30-64 years, 65-74 years, 75-84 years, and 85 years & above. For each segment, the market size and forecast are provided in terms of value (USD).

| Home Healthcare |

| Hospice |

| Nursing Care |

| Assisted Living Facilities |

| Adult Day-Care Centers |

| Public |

| Private Insurance |

| Out-of-Pocket / Self-Funded |

| Managed-Care & Value-Based Contracts |

| 0-29 Years |

| 30-64 Years |

| 65-74 Years |

| 75-84 Years |

| 85 Years & Above |

| By Service | Home Healthcare |

| Hospice | |

| Nursing Care | |

| Assisted Living Facilities | |

| Adult Day-Care Centers | |

| By Payer | Public |

| Private Insurance | |

| Out-of-Pocket / Self-Funded | |

| Managed-Care & Value-Based Contracts | |

| By Age Group | 0-29 Years |

| 30-64 Years | |

| 65-74 Years | |

| 75-84 Years | |

| 85 Years & Above |

Key Questions Answered in the Report

How large is the United States long term care sector in 2026?

The sector stands at USD 610.86 billion in 2026 and is projected to reach USD 883.10 billion by 2031, growing at a 7.65% CAGR over 2026-2031.

Which service category leads current revenue in the United States long term care space?

Home Healthcare leads with a 45.31% share in 2025, supported by strong aging-in-place preference and public HCBS funding.

Which service category is expanding the fastest through 2031?

Adult Day-Care Centers are projected to grow at a 9.38% CAGR through 2031, helped by their role as a lower-cost bridge between home care and institutional care.

Why do public payers matter so much in this space?

Public payers held 56.24% of revenue in 2025, and Medicaid alone serves more than 5.1 million home care beneficiaries annually, which makes government funding central to service access and provider economics.

Which age group will create the highest future care intensity?

The 85 Years & Above cohort is forecast to grow at an 8.28% CAGR through 2031, and this group carries the highest burden of dementia, frailty, and multi-morbidity.

What is the main operating challenge for providers through the forecast period?

Workforce supply is the clearest challenge, with 8.9 million projected direct-care job vacancies between 2024 and 2034 and broad evidence of staffing shortages across community-based providers.

Page last updated on: