United States Burn Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.38 Billion |

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 1.96 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

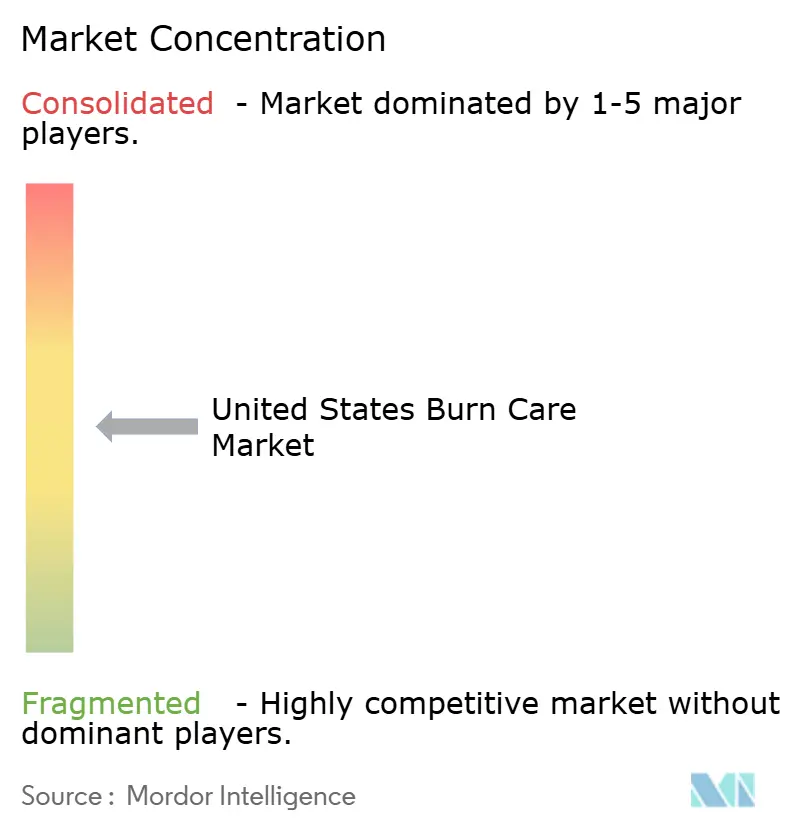

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Burn Care Market Analysis by Mordor Intelligence

The United States Burn Care Market size was valued at USD 1.38 billion in 2025 and is estimated to grow from USD 1.46 billion in 2026 to reach USD 1.96 billion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031).

The market covers advanced dressings, biologics and skin substitutes, negative pressure wound therapy, and traditional dressings used across hospitals, specialized burn centers, ambulatory surgery centers, and home-based recovery pathways. The clinical demand base remains durable because the American Burn Association recorded 32,993 burn-related admissions in 2024 and tracked 162,799 cumulative cases across 114 centers between 2020 and 2024. Product demand in the United States burn care market is shaped by a split injury pattern where flame and flash injuries account for 46% of burn-center admissions, while scalds represent 58% of pediatric cases, which supports broad use of antimicrobial and moisture-retentive dressings. The product mix is also moving toward higher-acuity care because lithium-ion battery fires are increasing severe injury risk, while federal preparedness programs are supporting domestic burn response capacity and advanced imaging adoption. The United States burn care market is still constrained by payment changes for skin substitutes, specialist staffing shortages, and rural access gaps, which makes teleburn and virtual follow-up an important part of long-term care delivery rather than an optional add-on.

Key Report Takeaways

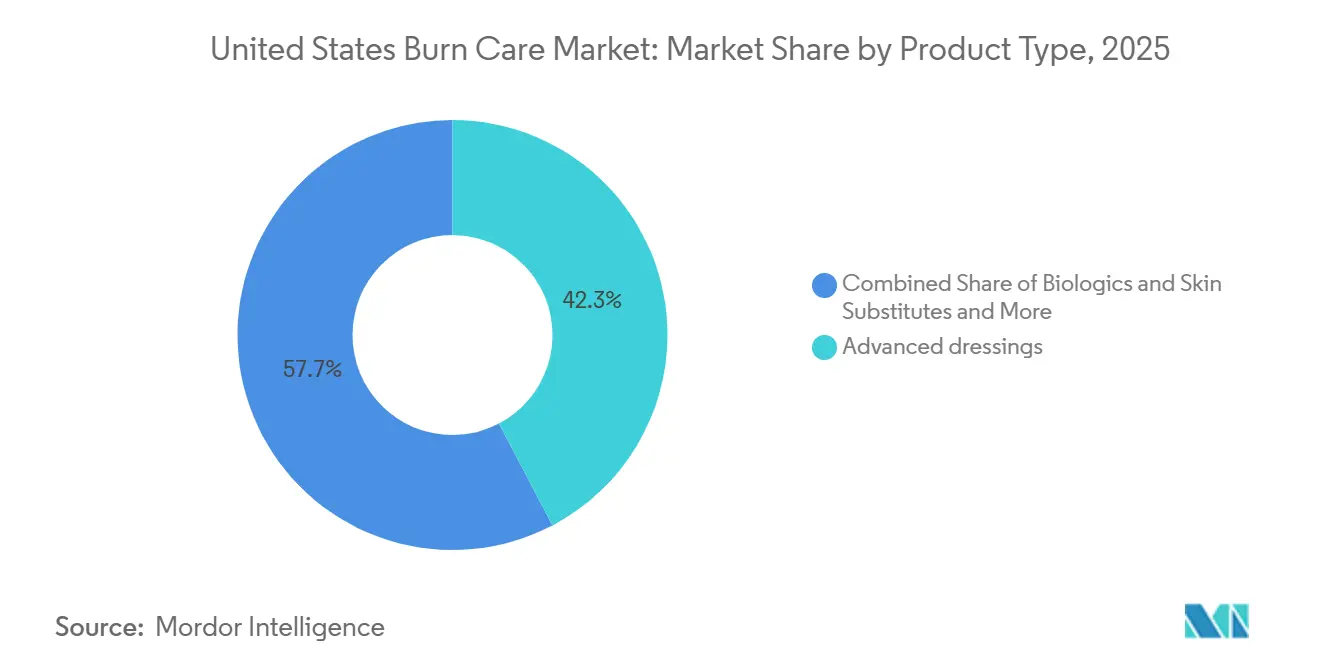

- By product type, advanced dressings accounted for 42.31% of the United States burn care market size in 2025, while biologics and skin substitutes are projected to expand at 8.38% CAGR through 2031.

- By burn depth, partial-thickness burns held 63.24% of the United States burn care market share in 2025, while full-thickness burns are forecast to grow at 7.52% CAGR through 2031.

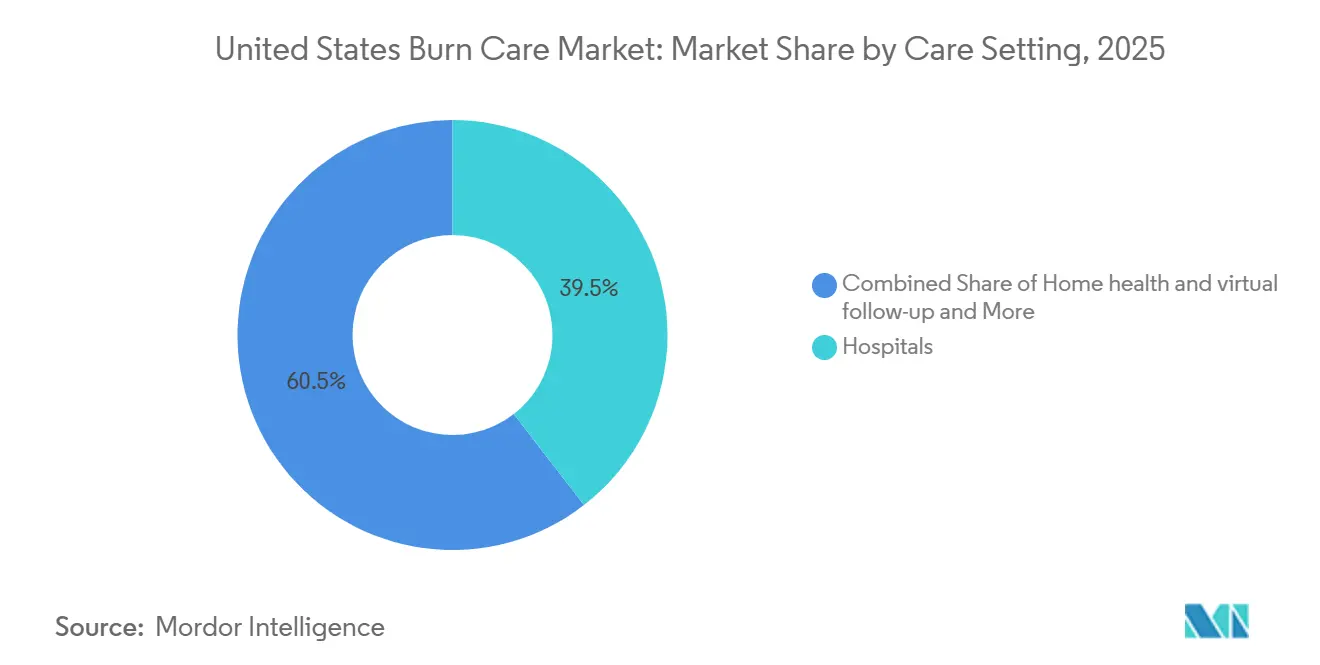

- By care setting, hospitals represented 39.52% of revenue in 2025, while home health and virtual follow-up are expected to advance at 7.25% CAGR through 2031.

- By burn etiology, thermal burns accounted for 38.24% of the United States burn care market size in 2025, while chemical burns are projected to grow at 6.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Burn Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High U.S. Burn Case Burden and Concentrated Referral Flows | +1.2% | National, with concentration in South Atlantic and Southern regions | Medium term (2-4 years) |

| Advanced Dressings, Grafts, and Biologics Adoption | +1.8% | National, highest uptake at ABA-verified burn centres in urban cores | Long term (≥ 4 years) |

| Burn-Centre Expansion and Outpatient Pathway Optimization | +0.9% | National, with early traction in Mid-Atlantic and Midwest hub markets | Medium term (2-4 years) |

| Teleburn Networks Closing Rural Access Gaps | +0.7% | National, with early gains in Southeast, rural Appalachia, and Mountain West | Medium term (2-4 years) |

| Lithium-Ion Battery Fires Increasing High-Acuity Cases | +0.6% | National, highest incidence in dense metro corridors with high e-mobility adoption | Short term (≤ 2 years) |

| BARDA-Backed Severe-Burn Preparedness and Domestic Capacity | +0.5% | National, stockpile and capacity investments centred on strategic federal sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High U.S. Burn Case Burden and Concentrated Referral Flows

The United States burn care market continues to benefit from a large and steady treatment base because the CDC-linked burn burden stands near 398,000 fire or burn-related injuries annually, while the American Burn Association reported that 29,165 cases required inpatient admission. Demand is not spread evenly across the country because 94 hospitals that each admit at least 100 burn encounters per year account for 81% of all inpatient burn admissions. This concentration creates dependable purchasing nodes where formulary access matters more than broad but shallow distribution coverage. The South Atlantic alone contributes 26% of inpatient burn admissions, which gives that region a larger role in infrastructure planning and supplier prioritization[1]American Burn Association, “Burn Incidence and Treatment in the United States,” American Burn Association, ameriburn.org. In the United States burn care market, product adoption is therefore tied closely to referral velocity through ABA-verified centers and high-volume hospitals. Manufacturers with direct access to these high-throughput institutions are better placed to secure repeat use across advanced dressings, grafts, and support therapies.

Advanced Dressings, Grafts, and Biologics Adoption

The United States burn care market is shifting toward care pathways that combine advanced dressings with biologics rather than treating the two categories as separate choices. Burn surgeons are using staged treatment protocols more often for full-thickness and deep partial-thickness injuries, which raises demand for dermal templates, graft-support products, and adjunct wound coverage. Integra LifeSciences presented real-world evidence from 985 cases and a 23-patient burn series across three conferences in April 2026, which shows that dermal regeneration templates are moving into routine institutional algorithms. At the same time, dressing volumes remain firm because formulary teams still favor a dressing-first approach for many partial-thickness wounds before escalating to higher-cost biologic products. Regulatory activity is reinforcing this trend because the FDA cleared AVITA Medical’s Cohealyx collagen-based dermal matrix and PermeaDerm biosynthetic wound matrix, while the FDA approved Abeona Therapeutics’ ZEVASKYN in April 2025, which signals that high-evidence products can still move forward. This combination of broader clinical acceptance and a higher evidence threshold keeps both advanced dressings and biologics in positive growth territory within the United States burn care market.

Burn-Centre Expansion and Outpatient Pathway Optimization

The United States burn care market is being reshaped by a stronger outpatient pathway for selected burn cases. Reimbursement changes that took effect in early 2026 pushed a larger share of skin-substitute procedures away from physician offices and mobile wound clinics and toward hospital outpatient wound centers. Hospitals that absorb this redirected volume gain more control over formulary standardization, product selection, and treatment economics. Burn centers are also widening same-day and short-stay pathways for superficial and partial-thickness injuries, supported by survivorship outcomes that improve clinician confidence around discharge planning. The American Burn Association reported a 97.6% survival rate in its 2025 summary, which supports continued movement toward recovery in lower-cost community settings when clinically appropriate. This shift supports the United States burn care market by expanding the role of outpatient wound centers without removing the need for specialized inpatient care in severe cases.

Teleburn Networks Closing Rural Access Gaps

The United States burn care market is also expanding through teleburn programs that bring specialist input to locations without nearby verified centers. Vanderbilt University Medical Center noted that the country sees close to 400,000 burn-related emergency department visits each year, while only 30,000 cases result in burn-center admissions. That gap leaves a large pool of patients managed in non-specialized settings where triage quality and follow-up discipline can vary widely. Vanderbilt’s teleburn model showed that virtual triage can reduce short-stay transfers and preserve inpatient capacity for higher-acuity cases that require complex wound products. Teleburn also creates structured image records and healing-path data that can support AI-based wound assessment over time. As these networks expand, the United States burn care market gains a larger outpatient treatment base for advanced dressings and supervised home protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Biologics and NPWT-Intensive Care Pathways | -1.1% | National, most acute for safety-net hospitals and rural facilities | Long term (≥ 4 years) |

| CMS 2026 Skin-Substitute Payment Reset | -1.6% | National, most acute in physician office and mobile clinic settings | Short term (≤ 2 years) |

| Rural Burn-Centre Access and Specialist Staffing Gaps | -0.8% | Rural and frontier areas, disproportionate impact in Mountain West and Appalachia | Medium term (2-4 years) |

| Higher Evidence and Regulatory Bar for Advanced Biologics | -0.7% | National, regulatory compliance concentrated at FDA CBER and CMS LCD levels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologics and NPWT-Intensive Care Pathways

The United States burn care market faces a clear adoption ceiling when treatment pathways depend heavily on biologics and NPWT. The American Burn Association reported that 29.1% of burn patients were covered by Medicaid and 10.2% were uninsured or self-paying, which limits the ability of many facilities to absorb expensive advanced therapies. NPWT-assisted graft preparation can add USD 1,000–3,000 per dressing change episode in inpatient care, which makes cost justification difficult in community hospitals without strong outcomes data. The payer mix becomes even more restrictive because 15.9% of burn-center patients are on Medicare and facilities now face tighter reimbursement for many skin substitutes. In response, manufacturers are leaning more heavily on real-world evidence such as Integra’s PriMatrix publications and Kerecis data on reduced hospital length of stay to support economic value discussions. These cost pressures slow the pace at which newer products can scale across the full United States burn care market.

CMS 2026 Skin-Substitute Payment Reset

The United States burn care market is also being constrained by the CMS payment reset that took effect on January 1, 2026. The rule reclassified most skin substitutes as incident-to supplies and replaced the ASP+6% model with a flat reimbursement rate near USD 127.28 per cm², which sharply reduced the economics that had supported rapid growth in office-based graft use. This reset is expected to reduce gross fee-for-service Medicare spending on skin-substitute services by USD 19.6 billion in 2026, and the change is already affecting contracting patterns in physician-office and mobile clinic channels. The rule also created a split between most skin substitutes and products licensed under Section 351 of the Public Health Service Act, which retain ASP+6% treatment and therefore hold a stronger commercial position. Organogenesis completed a rolling BLA submission for ReNu in April 2026, while Vericel continues to benefit from the orphan biologic position of NexoBrid, which shows how product strategy is shifting toward higher regulatory pathways. CMS has also intensified audit and documentation scrutiny, which adds another layer of channel friction for suppliers that depend on office-based applications[2]Frier Levitt, “The Impact of CMS’ Revised Billing Regulations for Skin Substitutes, Payment Mechanics, Compliance Priorities, and What Comes Next,” Frier Levitt, frierlevitt.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biologics Growth Pressures the Long-Standing Lead of Advanced Dressings

Advanced dressings held the leading position in the United States burn care market, accounting for 42.31% of revenue in 2025. Their lead reflects broad use across superficial, partial-thickness, and selected post-surgical wounds in hospitals, ambulatory settings, and home recovery programs. Antimicrobial silver dressings and foam dressings remain the most widely used formats because they address infection control and exudate management across a large patient pool. Smith+Nephew’s March 2026 launch of ALLEVYN COMPLETE CARE, which cited stronger exudate management performance than competing products, shows that innovation continues to support premium pricing in this tier.

Biologics and skin substitutes are the fastest-growing product segment in the United States burn care market, with an 8.38% CAGR expected from 2026 to 2031. This growth reflects stronger clinical use in full-thickness and complex deep partial-thickness injuries, along with a regulatory shift that now favors BLA-pathway products. Vericel reported that NexoBrid generated USD 12.0 million in burn care revenue in Q1 2026, up 91% year on year, and the company raised its full-year 2026 guidance to USD 44–48 million. Negative pressure wound therapy remains an important support layer in graft preparation and wound management, while traditional dressings still hold a cost-led role in facilities that cannot absorb higher biologic spending. The United States burn care market therefore shows a two-track product structure where advanced dressings preserve scale and biologics capture the fastest revenue growth.

By Burn Depth: Full-Thickness Injuries Increase Product Intensity and Surgical Need

Partial-thickness burns represented 63.24% in 2025, giving them the largest role in the United States burn care market by burn depth. This share follows the clinical pattern reported by the American Burn Association, where deep partial-thickness injuries requiring surgery but not prolonged ventilation made up 32% of hospital admissions, while the most extensive injuries requiring both surgery and ventilation accounted for only 4.4%. Foam, hydrocolloid, alginate, and other advanced dressings remain the backbone for these wounds because they support healing while limiting unnecessary escalation. Enzymatic debridement products such as NexoBrid are also gaining traction in deep partial-thickness care because they can remove eschar selectively without sacrificing viable tissue, a treatment approach reflected in recent clinical guidance.

Full-thickness burns are forecast to expand at a 7.52% CAGR from 2026 to 2031, making them the fastest-growing burn-depth category in the United States burn care market. Their growth matters because these injuries carry higher product complexity, heavier surgical use, and greater revenue per episode than superficial burns. PolyNovo’s NovoSorb BTM remains in a multicenter pivotal study at U.S. burn centers including Valleywise Health and LAC+USC, with estimated completion in December 2026, which could support wider use of synthetic matrices in excision-and-graft protocols. Superficial burns still contribute large case volume, but their lower treatment intensity limits their value contribution. This pattern keeps the United States burn care market anchored by partial-thickness prevalence while allowing full-thickness cases to drive product sophistication and premiumization.

By Care Setting: Hospital Systems Gain More Control as Home Follow-Up Expands

Hospitals held 39.52% of revenue in 2025, which made them the largest care-setting segment in the United States burn care market. Their position strengthened as reimbursement changes redirected skin-substitute procedures away from office-based and mobile providers and toward hospital outpatient wound centers. This gave hospital systems more influence over formulary decisions, contracting terms, and protocol standardization across inpatient and outpatient sites. Specialized burn centers and wound clinics remain the premium end of the treatment landscape because they handle the most complex cases and use the widest mix of biologics, NPWT, and staged reconstruction products.

Home health and virtual follow-up are forecast to grow at 7.25% CAGR from 2026 to 2031, which makes them the fastest-expanding care setting in the United States burn care market. The Vanderbilt teleburn program showed that virtual follow-up can reduce unnecessary transfers and maintain wound care adherence in rural populations. This growth also changes how products are packaged and supported because dressings used at home need simpler application steps and clearer patient instruction. Manufacturers are therefore adjusting the commercial model around education tools and home-compatible protocols rather than relying only on hospital-based product training. The United States burn care market is moving toward a more connected care pathway where hospitals retain control over complex episodes and home follow-up captures a larger share of recovery activity.

By Burn Etiology: Thermal Burns Hold the Largest Revenue Base While Chemical Burns Accelerate

Thermal burns accounted for 38.24% of revenue in 2025, which made them the largest etiology in the United States burn care market. Their lead reflects the broad mix of scalds, flame injuries, and contact burns that fall into this category and require different dressing and reconstruction protocols. The American Burn Association reported that flame and flash injuries represented 46% of burn-center admissions, while scalds were dominant in pediatric cases, which shapes product demand toward antimicrobial and non-adherent dressing systems. Electrical burns remain lower in case volume, but their greater tissue necrosis depth and ICU burden make them important contributors to NPWT and biologic use. Radiation and friction burns form a smaller share of treatment demand and are linked mainly to occupational and oncology-related settings.

Chemical burns are projected to grow at 6.83% CAGR from 2026 to 2031, which gives them the fastest etiology growth in the United States burn care market. This rise is tied to industrial expansion, occupational exposure events, and injuries related to corrosive materials in lithium-ion battery manufacturing and recycling. Chemical burns often require prolonged decontamination and extended dressing use before reconstruction decisions can be made, which increases treatment intensity despite a smaller base volume. The growth of lithium-ion cell production in states such as Nevada, Tennessee, and Michigan is widening the occupational health channel for burn care beyond traditional trauma pathways. This keeps thermal injuries at the center of volume demand while pushing chemical burns into a more visible commercial role.

Geography Analysis

The United States burn care market operates under one national regulatory and reimbursement framework, but regional differences in infrastructure and case burden remain pronounced. The South Atlantic census division accounted for 26% of national inpatient burn admissions, which was the highest share of any U.S. region[3]American Burn Association, “2025 Annual Burn Injury Summary Report,” American Burn Association, ameriburn.org. That regional concentration supports the largest cluster of ABA-verified burn centers and high-volume hospitals, which makes the Southeast the most important commercial zone for suppliers targeting institutional formulary adoption. The region also carries a heavier Medicaid mix, which increases cost pressure even as high treatment volume supports faster real-world evidence generation. This combination makes the South Atlantic a central testing ground for how hospital outpatient wound centers adjust product use under the 2026 reimbursement framework.

New England accounted for only 3% of national burn admissions, which puts it at the opposite end of the regional volume range. The Mid-Atlantic and Midwest remain important secondary hubs because they have strong academic medical center networks that participate in pivotal studies and influence evidence-based product adoption. Rural parts of Appalachia, the Mountain West, and the Great Plains face the deepest access gaps because distance from ABA-verified centers often overlaps with weaker broadband access and more limited telehealth capacity. Teleburn networks led by institutions such as Vanderbilt are helping extend specialist input into these underpenetrated areas, which can gradually widen the treatment base for advanced wound products.

The western United States, especially California, is becoming a technology-focused cluster within the United States burn care market. The region hosts AVITA Medical’s commercial activity and several important clinical trial sites tied to PolyNovo’s BTM study and related evaluations. California’s wildfire exposure creates periodic demand for mass-casualty-scale dressings, debridement tools, and federal preparedness support. States with growing lithium-ion battery manufacturing footprints, including Nevada, Tennessee, and Michigan, are also seeing a stronger overlap between occupational chemical and thermal burns and employer-linked care pathways.

Competitive Landscape

The United States burn care market shows moderate-to-high concentration in advanced dressings and NPWT, but it remains fragmented by indication, burn depth, and care setting. Large multinational suppliers such as Smith+Nephew, Mölnlycke Health Care, Solventum, and Coloplast compete on product breadth, contract reach, and clinical support rather than on a single dominant position across all categories. Smith+Nephew reinforced this posture through its December 2025 strategy update for advanced wound management and followed that with the March 2026 U.S. launch of ALLEVYN COMPLETE CARE. The company also signaled further portfolio expansion with the planned RENASYS EDGE tNPWT launch tied to EWMA 2026, which shows the level of product cadence needed to defend formulary positions.

The biologics and skin-substitute layer of the United States burn care market follows a different pattern because mid-tier specialists compete more on regulatory standing and outcome evidence than on manufacturing scale alone. AVITA Medical strengthened its preparedness role through a 10-year Project BioShield agreement with BARDA worth up to USD 25.5 million in April 2026, which links the company directly to federal severe-burn response capacity. Vericel continued to build commercial momentum around NexoBrid in 2026, supported by strong growth and the benefit of differentiated FDA status within the reimbursement environment. This tier is likely to favor companies that can support BLA-level evidence and navigate tighter payer scrutiny.

Two underdeveloped spaces still stand out in the United States burn care market. AI-supported wound triage remains early, but Spectral AI’s USD 149 million BARDA contract for DeepView burn imaging has already created a validation path across more than 30 burn centers. Home health and virtual follow-up also remain underserved because most current offerings are adapted from hospital use rather than designed for home application from the start. Kerecis added a differentiated position in April 2026 by reporting a 9.3-day reduction in hospital length of stay for severely burned patients treated with its intact fish-skin grafts. As the evidence bar rises and reimbursement remains selective, competition in the United States burn care market is moving toward stronger clinical proof, more targeted channel strategies, and tighter alignment with federal preparedness and hospital procurement systems.

United States Burn Care Industry Leaders

Smith+Nephew

Solventum Corporation

Mölnlycke Health Care

ConvaTec Group

Integra LifeSciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AVITA Medical announced a 10-year Project BioShield agreement with BARDA worth up to USD 25.5 million, covering RECELL deployment for burn mass-casualty incident preparedness, with annual access-maintenance fees of approximately USD 3.97 million and additional procurement options.

- March 2026: Smith+Nephew launched ALLEVYN COMPLETE CARE Foam Dressing in the United States, featuring proprietary five-layer construction with 55% greater reduction in wound strain relative to competitive products; the dressing addresses both chronic wound healing and pressure injury prevention.

United States Burn Care Market Report Scope

As per the scope of the report, burn care refers to the medical treatment and management of burns, which are injuries to the skin and underlying tissues caused by heat, chemicals, electricity, radiation, or friction. It involves assessing the severity of the burn, preventing infection, managing pain, and promoting healing to restore function and minimize complications.

The segmentation of the United States burn care market is categorized by product type, burn depth, care setting, and burn etiology. By product type, the market includes advanced dressings such as foam dressings, hydrocolloid dressings, hydrogel dressings, alginate dressings, antimicrobial silver dressings, collagen dressings, silicone contact layers, biologics and skin substitutes, negative pressure wound therapy, traditional dressings, and other product types. By burn depth, the market is segmented into superficial burns, partial-thickness burns, and full-thickness burns. By care setting, the segmentation includes hospitals, specialized burn centers and wound clinics, ambulatory surgery centers, home health and virtual follow-up, and other care settings. By burn etiology, the market is divided into thermal burns, electrical burns, chemical burns, and radiation and friction burns. For each segment, the market size and forecast are provided in terms of value (USD).

| Advanced Dressings | Foam Dressings |

| Hydrocolloid Dressings | |

| Hydrogel Dressings | |

| Alginate Dressings | |

| Antimicrobial Silver Dressings | |

| Collagen Dressings | |

| Silicone Contact Layers | |

| Biologics and Skin Substitutes | |

| Negative Pressure Wound Therapy | |

| Traditional Dressings | |

| Other Product Types |

| Superficial Burns |

| Partial-Thickness Burns |

| Full-Thickness Burns |

| Hospitals |

| Specialised Burn Centres and Wound Clinics |

| Ambulatory Surgery Centers |

| Home Health and Virtual Follow-up |

| Other Care Settings |

| Thermal Burns |

| Electrical Burns |

| Chemical Burns |

| Radiation and Friction Burns |

| By Product Type | Advanced Dressings | Foam Dressings |

| Hydrocolloid Dressings | ||

| Hydrogel Dressings | ||

| Alginate Dressings | ||

| Antimicrobial Silver Dressings | ||

| Collagen Dressings | ||

| Silicone Contact Layers | ||

| Biologics and Skin Substitutes | ||

| Negative Pressure Wound Therapy | ||

| Traditional Dressings | ||

| Other Product Types | ||

| By Burn Depth | Superficial Burns | |

| Partial-Thickness Burns | ||

| Full-Thickness Burns | ||

| By Care Setting | Hospitals | |

| Specialised Burn Centres and Wound Clinics | ||

| Ambulatory Surgery Centers | ||

| Home Health and Virtual Follow-up | ||

| Other Care Settings | ||

| By Burn Etiology | Thermal Burns | |

| Electrical Burns | ||

| Chemical Burns | ||

| Radiation and Friction Burns |

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for burn care in the United States?

The United States burn care market stands at USD 1.46 billion in 2026 and is projected to reach USD 1.96 billion by 2031 at a CAGR of 5.95%, supported by stable admission volumes, wider outpatient pathways, and stronger adoption of advanced products.

Which product category leads revenue today?

Advanced dressings led revenue with 42.31% in 2025 because they are used across the widest range of burn depths and care settings, including hospitals, ambulatory facilities, and supervised home care.

Which product segment is growing the fastest?

Biologics and skin substitutes are expanding the fastest at 8.38% CAGR through 2031 because severe and complex burns increasingly require biologic reconstruction, and reimbursement changes now favor higher-evidence products.

Which burn depth segment contributes the most demand?

Partial-thickness burns held 63.24% in 2025, which keeps them at the center of product volume demand, even though full-thickness burns are creating faster growth in biologics and surgical reconstruction.

How is care delivery shifting across treatment settings?

Hospitals remained the largest care setting with 39.52% of revenue in 2025, but home health and virtual follow-up are growing the fastest at 7.25% CAGR through 2031 as teleburn networks support outpatient recovery and rural follow-up.

What is changing competition among suppliers?

Competition is moving toward stronger clinical evidence, better hospital contract access, and closer alignment with federal preparedness programs, while AI imaging and home-optimized wound products remain less developed spaces.

Page last updated on: