Domiciliary Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

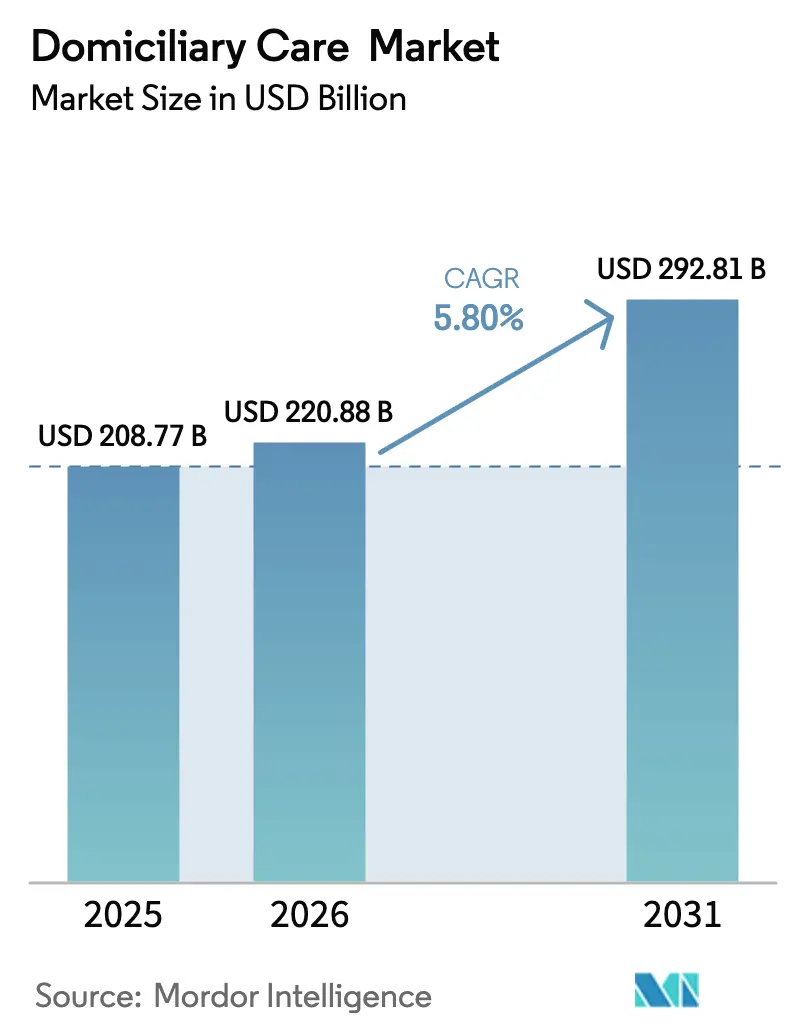

| Market Size (2026) | USD 220.88 Billion |

| Market Size (2031) | USD 292.81 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Domiciliary Care Market Analysis by Mordor Intelligence

The domiciliary care market size in 2026 is estimated at USD 220.88 billion, growing from 2025 value of USD 208.77 billion with 2031 projections showing USD 292.81 billion, growing at 5.80% CAGR over 2026-2031. This sustained growth reflects the structural migration of healthcare delivery from hospitals and nursing facilities to home settings, underpinned by demographic aging, payer cost-containment, and technology that now supports hospital-level acuity in the living room. Providers are capitalizing on the cost differential, with daily home care averaging USD 1,046 less than inpatient stays, while simultaneously lowering readmissions by 18% and mortality by 20%. As hospital-at-home programs mature, investors view the domiciliary care market as a primary rather than supplementary healthcare channel, giving rise to aggressive acquisition strategies by payers, hospital systems, and technology firms. Rapid adoption of remote patient monitoring (RPM) devices now used by 50 million Americans enables safe escalation of clinical complexity at home, further widening total addressable demand.

Key Report Takeaways

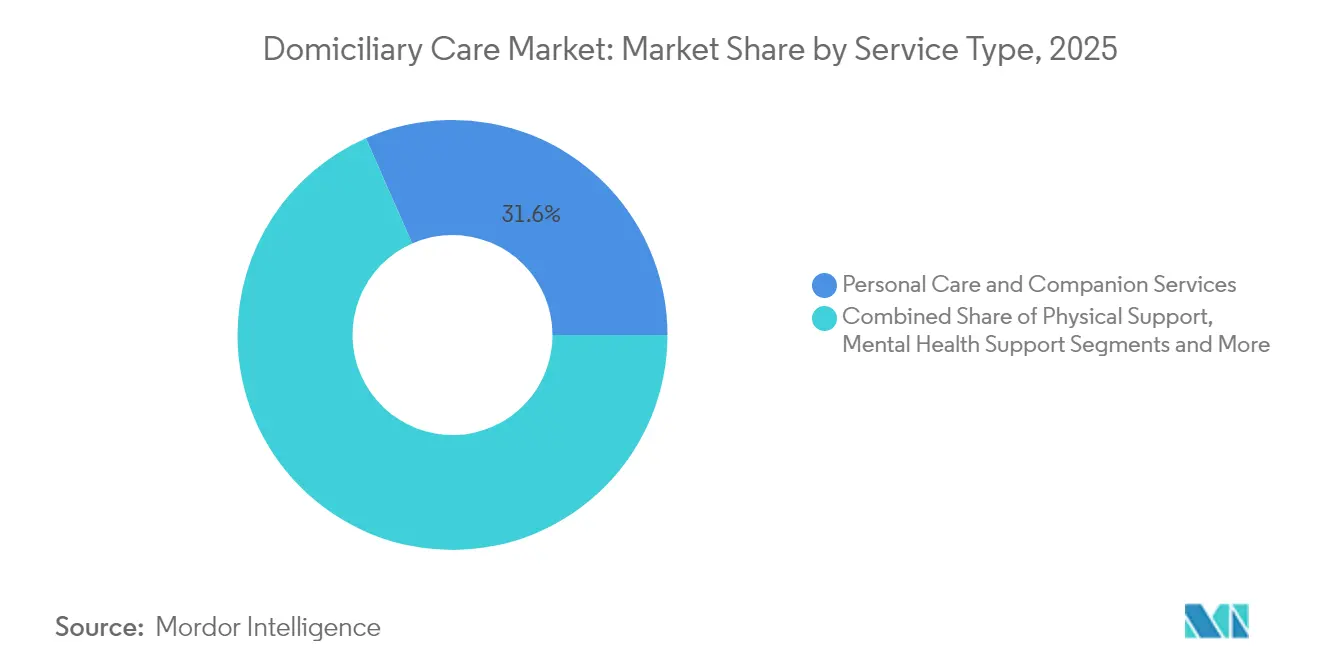

- By service type, personal care and companion services led with a 31.60% revenue share in 2025, while hospital-at-home acute-care services are projected to expand at a 6.75% CAGR to 2031.

- By care intensity, low-acuity personal care retained 56.10% of the domiciliary care market share in 2025; high-acuity hospital-at-home recorded the highest projected CAGR at 5.88% through 2031.

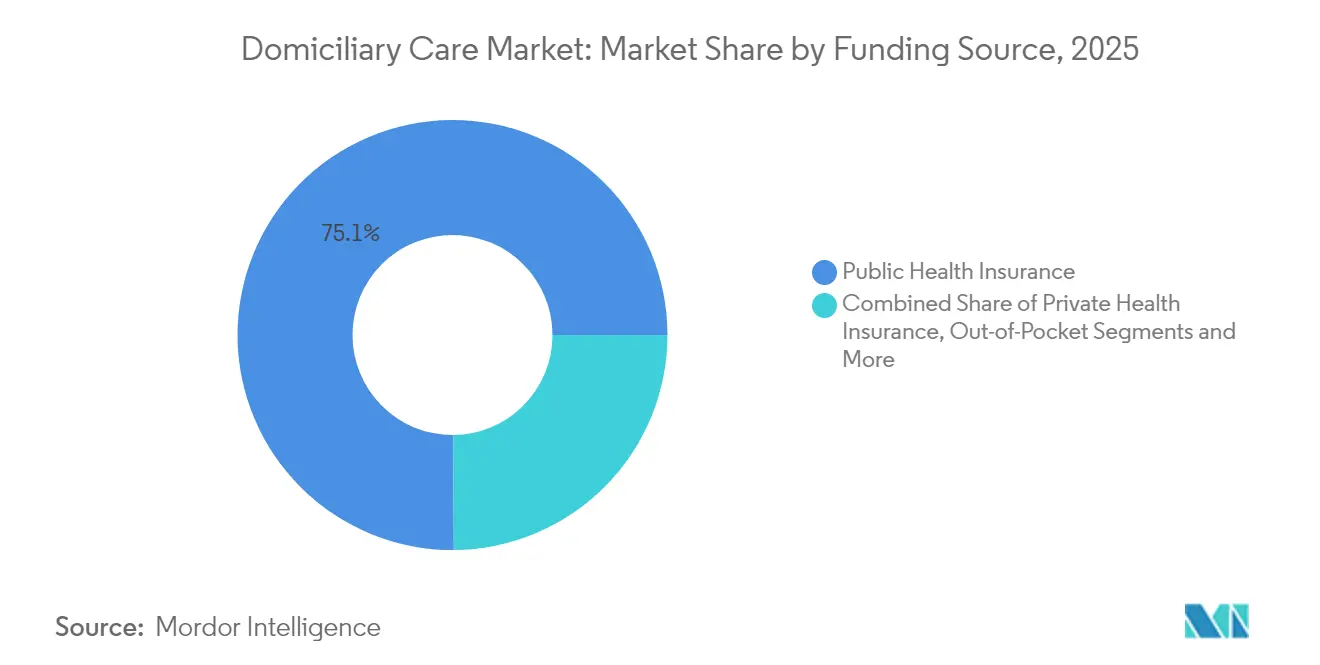

- By funding source, public health insurance/Medicare-type programs accounted for 75.10% of the domiciliary care market size in 2025, whereas long-term care insurance is forecast to grow at 7.25% CAGR between 2026-2031.

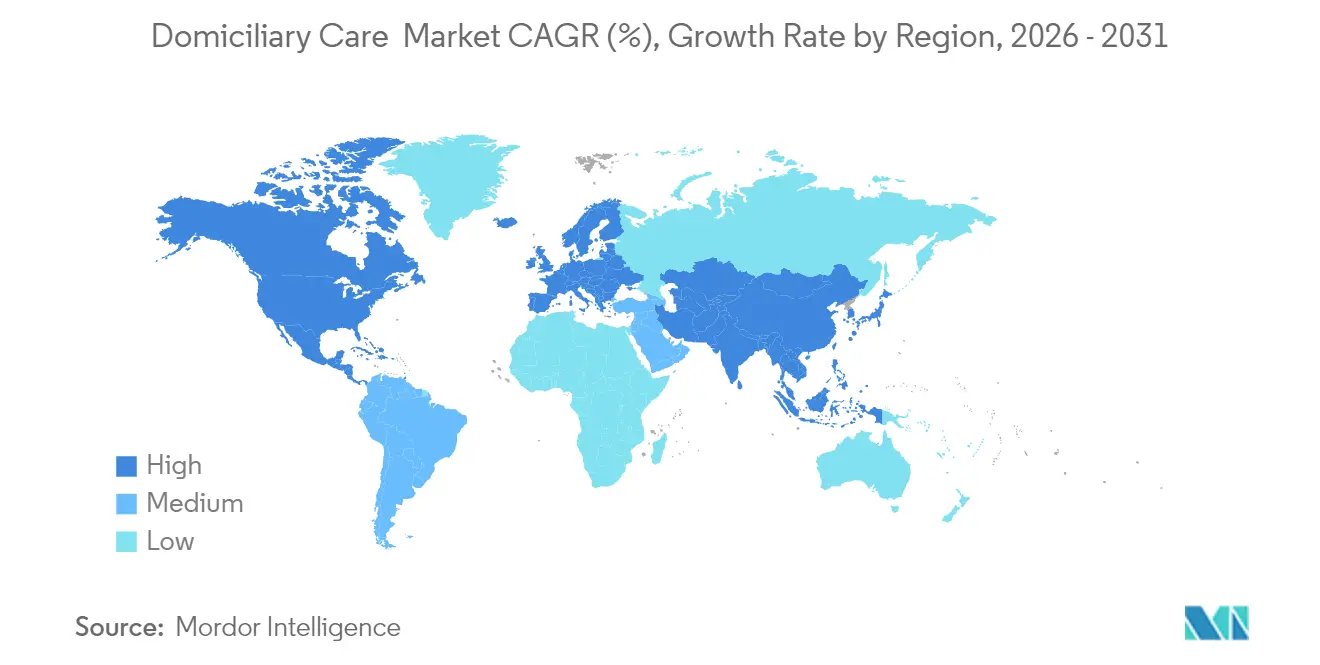

- By geography, North America dominated with 42.10% domiciliary care market share in 2025; Asia-Pacific is advancing at an 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Domiciliary Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population | +1.80% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Surge in chronic, long-term illnesses & disabilities | +1.50% | Developed markets worldwide | Medium term (2-4 years) |

| Cost advantage of home-based vs. institutional care | +1.20% | North America, EU, expanding APAC | Medium term (2-4 years) |

| Government reimbursement & policy tailwinds | +0.90% | North America, selective EU | Short term (≤ 2 years) |

| Expansion of hospital-at-home acute-care models | +0.70% | North America, pilots in EU & APAC | Medium term (2-4 years) |

| AI-driven RPM enables higher-acuity home care | +0.60% | North America, urban hubs globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population

The United States expects its 65-plus cohort to climb from 58 million in 2023 to 82 million by 2050, intensifying demand for longitudinal, home-based services that support aging in place. Nine out of ten older adults prefer remaining at home, prompting Medicare Advantage plans to purchase home health agencies and scale domiciliary networks. Asia-Pacific faces an equally acute demographic curve, giving rise to professional caregivers who complement traditional family support. Smart-home sensors and AI-enabled fall detection are proliferating as baseline infrastructure, widening clinical insight while respecting the elderly’s independence.

Surge in Chronic, Long-Term Illnesses & Disabilities

Chronic conditions afflict 129 million Americans and absorb 90% of national healthcare outlays, pushing payers toward settings that reduce emergency visits and inpatient volume.[1]Kyle J. Foreman, “Forecasting Life Expectancy and Mortality to 2050,” Institute for Health Metrics and Evaluation, ihme.washington.edu In-home multi-disciplinary teams have cut inpatient stays by 5.22% and emergency visits by 4.39% within a year, proving domiciliary efficacy in complex disease management. The shift drives an uptick in skilled nursing and rehab visits outside facility walls, encouraging investment in portable diagnostics and infusion therapies.

Cost Advantage of Home-Based vs. Institutional Care

At USD 783 per home-health day versus USD 1,829 in the hospital, the economic case sways both public and private payers. Hospital-at-home pilots show Medicare spending 20% less per episode while preserving or improving outcomes.[2]Centers for Medicare & Medicaid Services, “CMS Acute Hospital Care at Home,” cms.gov High-intensity home rehab has saved Medicare USD 17,123 within 90 days post-discharge, spotlighting a compelling ROI play for bundled-payment models.

Expansion of Hospital-at-Home Acute-Care Models

CMS has approved 378 hospitals for hospital-at-home programs, validating the model at scale.[3]American Hospital Association, “Hospital-at-Home Users and Outcomes,” aha.org Mass General Brigham’s 70-bed home hospital treats 50-60 daily patients, covering pneumonia, COPD, and post-operative care while posting lower 30-day readmissions than brick-and-mortar wards. Acute-care domiciliary episodes typically generate higher revenue per case, incentivizing cross-industry alliances between health systems and technology platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce Shortages & High Turnover of Skilled Caregivers | -1.40% | Global, particularly acute in North America and EU | Short term (≤ 2 years) |

| Fragmented Reimbursement & Licensing Rules in Emerging Markets | -0.80% | APAC, Latin America, selective EU markets | Medium term (2-4 years) |

| Rising Liability Insurance & Litigation Risk for Agencies | -0.60% | North America, expanding to developed markets globally | Medium term (2-4 years) |

| Cyber-Security Risks Tied to Connected Home-Care Devices | -0.40% | Global, concentrated in digitally advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Workforce Shortages & High Turnover of Skilled Caregivers

Turnover among US home-care aides has reached 80%, jeopardizing service continuity and forcing agencies to decline up to 25% of referrals. Low wages, limited career ladders, and emotionally taxing shifts deter retention. States like Michigan project a 170,000-worker gap this decade, triggering sign-on bonuses and preceptor programs aimed at the first 90 days on the job. Technology that automates documentation and routes clinicians efficiently is emerging as a non-cash retention lever.

Fragmented Reimbursement & Licensing Rules in Emerging Markets

Regulatory heterogeneity complicates APAC and Latin American expansion, where fee-for-service billing, limited home health codes, and variable professional licensure slow cross-border scaling. Even in the United States, CMS applied a -1.975% permanent adjustment to the 2025 payment base under PDGM, tempering top-line growth potential. Large operators absorb compliance overheads, whereas small regional providers struggle, accelerating consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hospital-at-Home Drives Premium Growth

Hospital-at-home services, though currently smaller in volume, are forecast to grow at 6.75% CAGR to 2031, outpacing every other line. CMS certification of 378 programs substantiates payer confidence while evidence shows lower mortality and fewer readmissions relative to inpatient wards. Personal care & companion services remain the volume anchor with a 31.60% share in 2025, yet face pricing pressure as commoditization sets in. Hospice and palliative demand rises in tandem with end-of-life preferences, and infusion therapy at home benefits from biologic drug innovation. AdventHealth’s January 2025 launch in Central Florida typifies hospital systems’ pivot to acute domiciliary capacity.

Broader service-mix evolution demonstrates a bifurcated landscape: low-skill, high-volume personal assistance versus high-skill, premium-priced medical episodes. Providers therefore pursue dual strategies—scale in foundational services for margin stability while capturing hospital-at-home upside through tech partnerships. The domiciliary care market continues to reward portfolio breadth that balances predictable companion hours with episodic, high-acuity interventions.

By Care Intensity: High-Acuity Segment Emerges Despite Low-Acuity Dominance

Low-acuity personal care captured 56.10% of the domiciliary care market share in 2025, illustrating the enduring necessity of daily-living assistance. Yet the high-acuity cohort is projected to expand at a 5.88% CAGR, reflecting policy allowances and technological capability. CMS reimburses hospital-at-home at roughly 80% of facility DRG rates, delivering budget relief while enabling physician oversight via tele-rounding. Intermediate skilled nursing continues to grow steadily as chronic multimorbidity rises. End-of-life care at home demonstrates both clinical efficacy and family satisfaction.

Escalation along the acuity curve intensifies requirements for 24/7 monitoring, rapid infusion logistics, and emergency escalation protocols. Scaling high-acuity services, therefore, necessitates robust command centers and interoperable EHR links. Mass General Brigham’s 70-bed program, the country’s largest, underscores operational feasibility at scale.

By Funding Source: Long-Term Care Insurance Gains Momentum

Public insurance sources, chiefly Medicare and Medicaid, financed 75.10% of the domiciliary care market size in 2025. Washington State’s long-term-care payroll tax mirrors a broader push to anticipate eldercare liabilities and traditional LTC policies disbursed USD 14 billion in 2023 benefits. Long-term care insurance as a funding source is forecast to rise 7.25% CAGR to 2031, buoyed by hybrid life/LTC products marketed through employers. Private health insurance penetration grows incrementally as commercial plans expand home-health riders, while out-of-pocket remains material among affluent households seeking concierge-level services.

Cost escalation plays a catalytic role as National median in-home caregiving expenses rose from USD 43,472 in 2012 to USD 75,504 in 2023, prompting consumers to hedge with insurance. Public-private interplay, therefore, defines future payment, with government programs anchoring basic entitlement and private mechanisms underwriting premiums or extended benefits.

Geography Analysis

North America retains leadership at 42.10% domiciliary care market share, sustained by CMS waivers and Medicare Advantage investments that normalize hospital-grade home episodes. The United States hosts all 378 CMS-approved hospital-at-home facilities, while Canada pilots community aging-in-place models and Mexico scales telehomecare through private insurers. Persistent 80% staff turnover, however, constrains capacity and inflates operating costs, emphasizing the need for workforce innovation. US adoption of RPM—involving 50 million device users—illustrates a technological bulwark reinforcing regional dominance.

Asia-Pacific represents the fastest-growing bloc, anticipated to log 8.55% CAGR through 2031. China’s domestic innovation mandates and Japan’s super-aged society spur local med-tech manufacturing, while India’s Make-in-India scheme cultivates portable diagnostic supply chains. Regulatory heterogeneity persists, though governments are steadily harmonizing home-health coding and telemedicine law to encourage private capital participation.

Europe continues gradual expansion via digital transformation agendas. Germany’s electronic patient record (ePA) rollout and hospital payment reform incentivize outpatient substitution . The EU-wide Health Technology Assessment framework primes cross-border reimbursement for digital therapeutics, while the United Kingdom advances Integrated Care Systems that budget for hospital avoidance. Workforce deficits—1 million vacant healthcare roles in 2024—require remote supervision tools and cross-training to sustain domiciliary scale.

Middle East & Africa and South America offer greenfield potential where hospital bed shortages and burgeoning elderly populations intersect. Yet patchy broadband, limited home-health licensure, and reimbursement uncertainty keep penetration low. Multinationals often adopt hub-and-spoke entry models, clustering services around metropolitan centers with private insurer footholds.

Competitive Landscape

Moderate fragmentation persists, though recent megadeals foreshadow tighter concentration. UnitedHealth’s USD 5.4 billion purchase of LHC Group in April 2024 and its pending USD 3.3 billion Amedisys merger highlight the payer appetite for vertical integration. The strategic goal is to control post-acute spending, enhance Medicare Advantage benefit portfolios, and leverage data insights for population management. The Department of Justice scrutiny illustrates antitrust sensitivities, yet the consolidation logic remains compelling.

Technology is the principal wedge for competitive differentiation. Mass General Brigham deploys Best Buy Current Health wearables for live streams of vitals, achieving 0.5% 30-day mortality in its home wards versus 1.2% systemwide inpatient average. Similarly, Hackensack Meridian leverages Medically Home’s logistics engine to combine in-person nursing with tele-rounding. AI predictive analytics shorten nurse drive time, optimizing labor deployment during a staffing crunch.

White-space opportunities abound in dementia care, post-hip-fracture rehab, and rural high-acuity care, where hospital deserts expand. Yet smaller regional operators such as Intrepid USA face bankruptcy after failing to absorb wage inflation and PDGM rate cuts. Investment theses now emphasize scale economics, proprietary tech, and diversified payer mix. The domiciliary care industry, therefore, trends toward national platforms augmented by local clinical affiliates, mirroring patterns seen in dialysis and ambulatory surgery decades earlier.

Domiciliary Care Industry Leaders

Amedisys Inc.

LHC Group (Optum)

BAYADA Home Health Care

CenterWell

Addus HomeCare Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AdventHealth launched its Hospital at Home program in Central Florida, providing hospital-level care with 24/7 monitoring and virtual consultations.

- December 2025: Addus HomeCare completed a USD 350 million purchase of Gentiva’s personal care operations, expanding across seven states.

- June 2025: Hackensack Meridian Health partnered with Medically Home to launch Hospital From Home across three hospitals.

- April 2024: SSM Health inaugurated Recovery Care at Home with Inbound Health, substituting skilled nursing stays.

Global Domiciliary Care Market Report Scope

As per the scope of the report, domiciliary care, also known as home care, provides compassionate support in the comfort of an individual's home. It includes a wide range of services provided by professional caregivers, helping individuals maintain their independence and live at home instead of relocating to a residential site or hospital. The domiciliary care market is segmented into service and geography. By service, the market is segmented into physical support, learning disability support, mental health support, support with memory and cognition, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers a value in USD for the above segments.

| Physical Support (ADL Assistance) |

| Learning Disability Support |

| Mental Health Support |

| Memory & Cognition Support |

| Personal Care & Companion Services |

| Skilled Nursing Care |

| Rehabilitation & Physiotherapy |

| Hospice & Palliative Care |

| Infusion Therapy At Home |

| Other Services |

| Low-Acuity Personal Care |

| Intermediate Skilled Nursing |

| High-Acuity Hospital-at-Home |

| End-of-Life / Palliative |

| Public Health Insurance |

| Private Health Insurance |

| Out-of-Pocket / Self-Pay |

| Charity & Non-Profit Sponsored |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Physical Support (ADL Assistance) | |

| Learning Disability Support | ||

| Mental Health Support | ||

| Memory & Cognition Support | ||

| Personal Care & Companion Services | ||

| Skilled Nursing Care | ||

| Rehabilitation & Physiotherapy | ||

| Hospice & Palliative Care | ||

| Infusion Therapy At Home | ||

| Other Services | ||

| By Care Intensity | Low-Acuity Personal Care | |

| Intermediate Skilled Nursing | ||

| High-Acuity Hospital-at-Home | ||

| End-of-Life / Palliative | ||

| By Funding Source | Public Health Insurance | |

| Private Health Insurance | ||

| Out-of-Pocket / Self-Pay | ||

| Charity & Non-Profit Sponsored | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current domiciliary care market size?

The domiciliary care market size is USD 220.88 billion in 2026 and is projected to reach USD 292.81 billion by 2031.

Which segment is growing fastest within domiciliary services?

Hospital-at-home acute-care services lead growth with a 6.75% CAGR through 2031, supported by CMS reimbursement and technology that enables hospital-level acuity at home.

Why is North America the largest regional market?

North America holds 42.10% market share due to well-established reimbursement frameworks, 378 CMS-approved hospital-at-home programs, and widespread RPM adoption.

How are workforce shortages affecting providers?

Turnover reaches 80%, forcing agencies to decline up to a quarter of new clients and spurring investment in retention programs and automation.

What funding sources dominate domiciliary care?

Public insurance programs such as Medicare and Medicaid finance 75.10% of spending, though long-term care insurance is the fastest-growing private funding stream.

Page last updated on: