Post-Acute Care (PAC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.97 Trillion |

| Market Size (2031) | USD 1.35 Trillion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

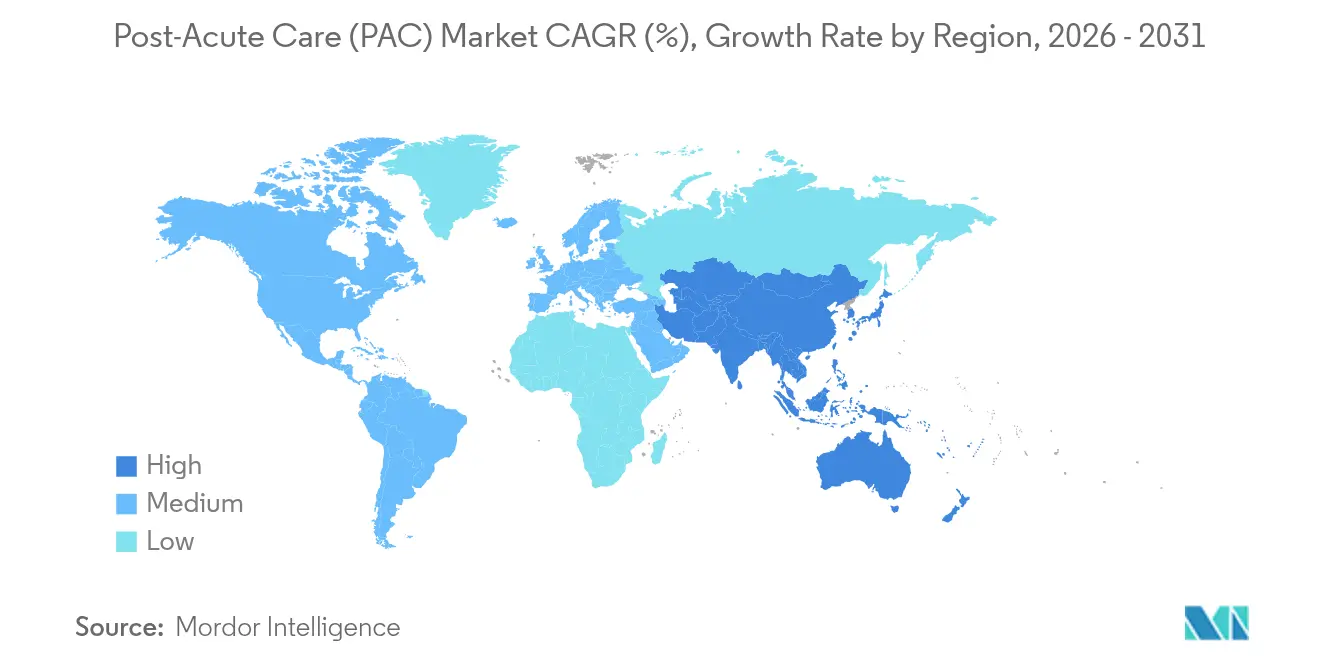

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

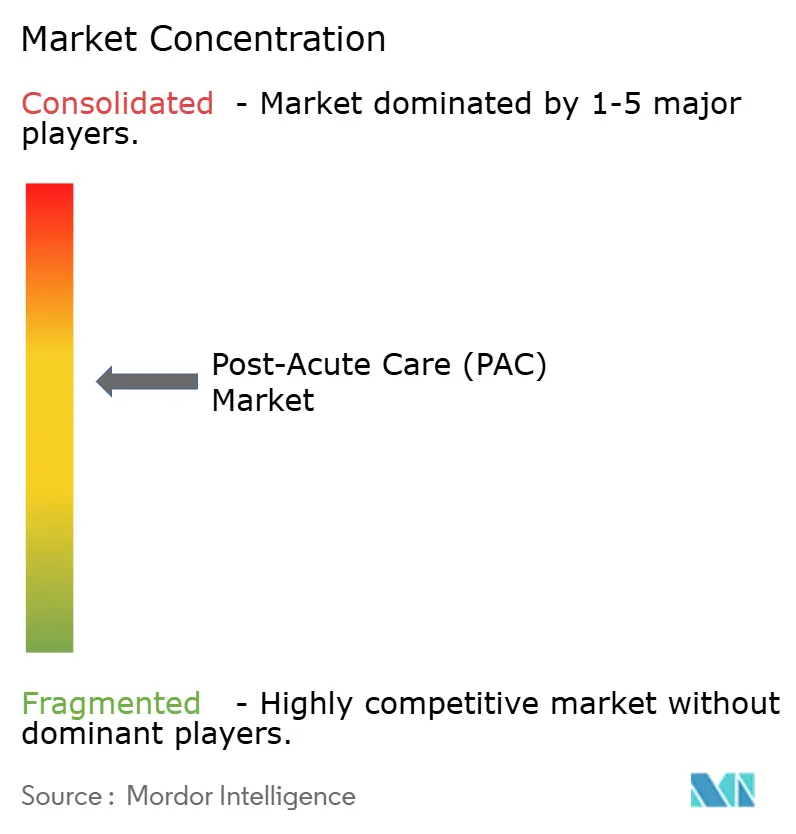

| Market Concentration | Medium |

Major Players-market---MP.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Post-Acute Care (PAC) Market Analysis by Mordor Intelligence

post-acute care market size in 2026 is estimated at USD 0.97 trillion, growing from 2025 value of USD 0.91 trillion with 2031 projections showing USD 1.35 trillion, growing at 6.82% CAGR over 2026-2031. Demographic aging, chronic disease prevalence, and payer incentives that reward lower readmission rates collectively reinforce steady demand. Technology-enabled home care, remote monitoring, and data-driven triage are re-shaping service mix allocations, while Medicare Advantage network optimization channels more cases toward providers that excel on outcomes [1]Centers for Medicare & Medicaid Services, “National Health Expenditure Projections,” cms.gov . Market participants that harmonize analytics, workforce flexibility, and cross-setting coordination are positioned to capture the next phase of growth in the post-acute care market. Capacity constraints inside institutional settings, persistent caregiving labor shortages, and emerging quality metrics widen the opportunity for digital platforms, AI-supported rehabilitation, and home-based acute-level services. Regulatory momentum—from the Acute Hospital Care at Home waiver to expanded SNF value-based purchasing rules—continues to steer capital away from legacy bricks-and-mortar toward scalable hybrid models that blend onsite and virtual interventions.

Key Report Takeaways

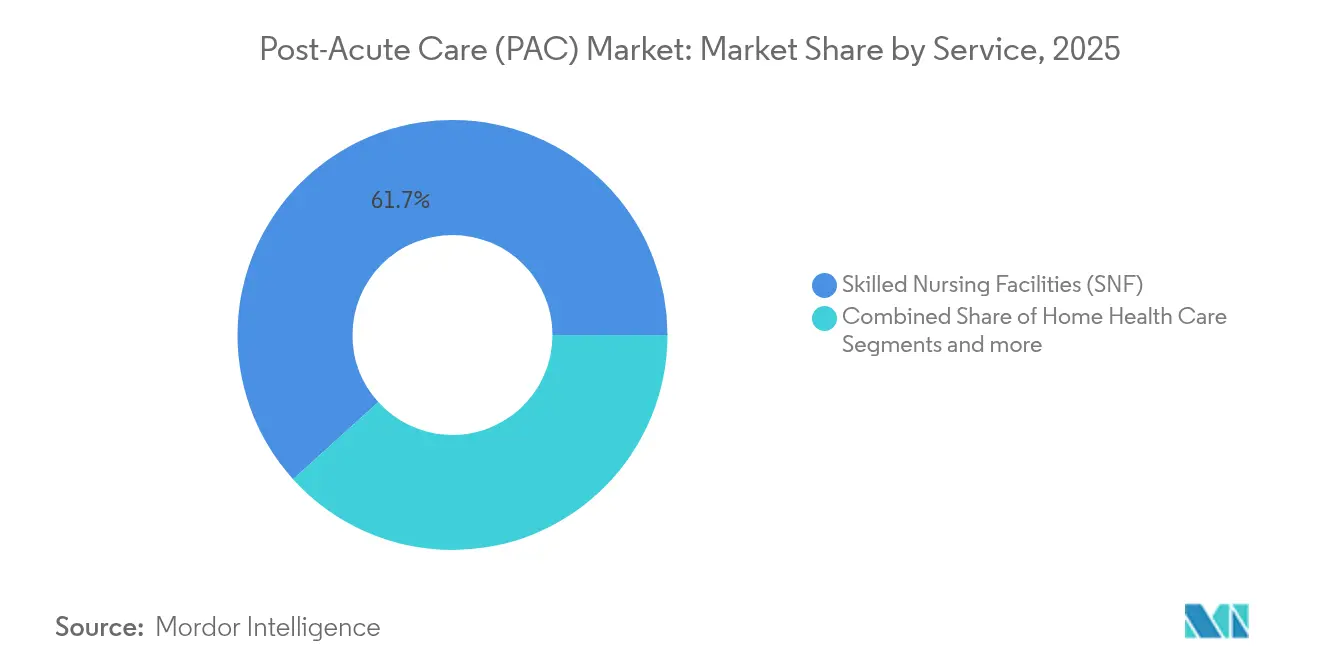

- By service, skilled nursing facilities held 61.70% of post-acute care market share in 2025, while home health care is forecast to expand at a 7.30% CAGR through 2031.

- By patient type, the elderly cohort accounted for 60.75% of the post-acute care market size in 2025; the adult segment records the fastest growth at 7.32% CAGR.

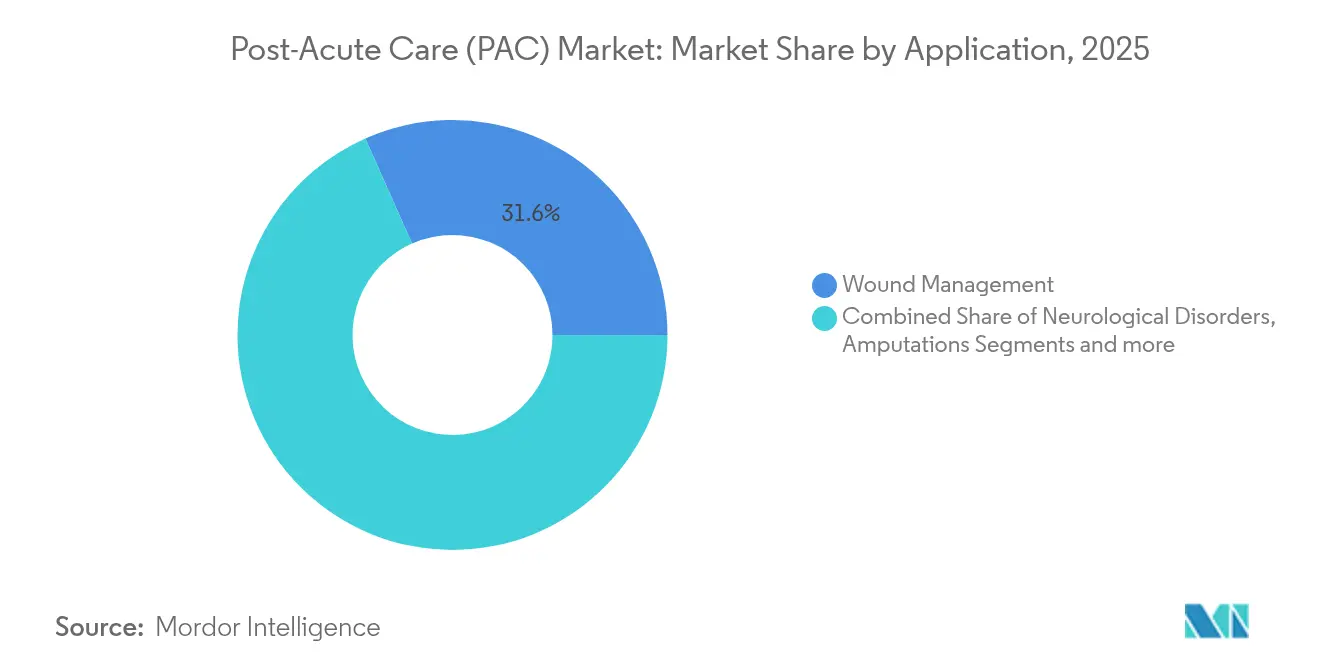

- By application, wound management dominated with 31.64% revenue share in 2025; neurological disorders rehabilitation is set to grow at a 7.41% CAGR to 2031.

- By setting, institution-based care retained 67.10% share of the post-acute care market size in 2025, yet home-based services are advancing at a 7.50% CAGR.

- By geography, North America led with 40.95% revenue share in 2025, while Asia-Pacific is the fastest-growing region at a 7.60% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Post-Acute Care (PAC) Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.8% | Global—notably North America & Europe | Long term (≥ 4 years) |

| Growing geriatric population | +2.1% | Global—highest in Asia-Pacific & North America | Long term (≥ 4 years) |

| Shift to home-based hospital-at-home models | +1.2% | North America & EU; extending to Asia-Pacific | Medium term (2-4 years) |

| Medicare Advantage network analytics | +0.9% | Primarily North America | Medium term (2-4 years) |

| Early hospital discharge trends | +0.7% | Global—led by North America & EU | Short term (≤ 2 years) |

| AI-enabled remote rehab devices | +0.8% | Developed markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Chronic conditions now dictate a larger share of post-acute episodes, and neurological indications drive the fastest application growth at 7.66% CAGR to 2030. Stroke rehabilitation increasingly integrates closed-loop robotics that pair motion sensing with neuromuscular stimulation to personalize therapy [2]Honggang Wang, "Closed-loop rehabilitation of upper-limb dyskinesia after stroke: from natural motion to neuronal microfluidics," Journal of NeuroEngineering and Rehabilitation, jneuroengrehab.biomedcentral.com. Hospice utilization for neurological patients has risen faster than overall Medicare enrollment, reflecting longer average stays and the complexity of end-stage management. Providers that deploy multidisciplinary teams alongside sensor-based progress tracking can shorten recovery windows and reduce readmissions. At the same time, payers tighten episodic bundles, pressing facilities to demonstrate functional gains within constrained payment windows.

Growing Geriatric Population

Population aging accelerates demand for skilled nursing, hospice, and allied home services, especially in Asia-Pacific and North America where the cohort aged 65+ rises sharply. Institutional bed growth lags behind demand, prompting governments to pilot Programs of All-Inclusive Care for the Elderly (PACE) that unify medical and social services under capitated payments. Providers that master geriatric assessment, fall prevention, and polypharmacy management gain a performance edge in value-based networks. The demographic surge also intensifies the need for culturally competent caregivers and remote family engagement platforms that sustain continuity when relatives live far from patients [3]Rangraze Imran, "A systematic review on the efficacy of artificial intelligence in geriatric healthcare: a critical analysis of current literature," BMC Geriatrics, bmcgeriatr.biomedcentral.com.

Shift to Home-Based “Hospital-at-Home” PAC Models

CMS’s Acute Hospital Care at Home waiver shows lower 30-day mortality and reduced per-episode spending versus inpatient care across 366 hospitals in 39 states. Health systems such as Mass General Brigham target transferring 10% of eligible medical admissions to home, supported by mobile phlebotomy, remote vital signs, and rapid-response nursing teams. As commercial payers mirror the waiver’s billing codes, technology vendors that integrate logistics, telemetry, and documentation APIs gain traction. Sustainability hinges on congressional renewal of the waiver and scalable workforce models that staff nurses, paramedics, and virtualists around the clock.

Medicare Advantage Network Optimization & Analytics Uptake

CMS has finalized a 4.33% payment increase for Medicare Advantage plans in 2026, translating to more than USD 21 billion in additional funds. Plans respond by tightening preferred-provider panels and embedding predictive analytics that flag members at readmission risk. Skilled nursing facilities now face quality measures tracking staff turnover and nursing hours per resident day; facilities able to evidence strong scores gain higher steerage volumes. Home health agencies equipped with Bluetooth-enabled devices and care-pathway dashboards increasingly occupy the downstream slot in an optimized network, edging out peers that cannot quantify outcomes.

Restraints Impact Analysis of Post-Acute Care (PAC) Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement uncertainty & rate cuts | -1.4% | Highest in North America | Short term (≤ 2 years) |

| Workforce shortages & caregiver turnover | -1.1% | Acute in developed markets | Medium term (2-4 years) |

| Payer data-reporting penalties | -0.6% | North America & EU | Medium term (2-4 years) |

| Pull-back of private capital for SNF upgrades | -0.8% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement Uncertainty & Rate Cuts

The 2025 Medicare Physician Fee Schedule lowers conversion factors by 2.83% to USD 32.35, squeezing outpatient rehab margins while therapy threshold increases raise beneficiary cost-sharing. Site-neutral payment rules now apply to long-term acute-care hospital discharges that fall outside specific clinical criteria, undermining the economics of extended-stay settings. Skittish investors defer capital projects in skilled nursing as Washington deliberates further risk-adjustment tweaks. Many operators respond by expanding high-acuity home programs that escape facility-specific rate shocks.

Workforce Shortages & High Caregiver Turnover

More than 100,000 direct-care positions remain unfilled in U.S. post-acute settings, and turnover rates have become a star metric in SNF value-based purchasing. Lower staffing correlates with penalties and market exclusion from preferred MA networks. Pandemic-era emergency funds stabilized wages only temporarily; long-run solutions center on apprenticeship ladders, loan-forgiveness packages, and task-sharing with tele-supervised assistants. AI-enabled scheduling optimizers and documentation automation reduce administrative load, yet cannot fully substitute for bedside presence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Post-Acute Care (PAC) Market Segment Analysis

By Service:

Home Health Drives Institutional TransformationHome health’s 7.30% CAGR through 2031 outpaces every other modality even though skilled nursing facilities commanded 61.70% revenue in 2025. The post-acute care market rewards agencies that combine remote monitoring with rapid-response nursing to manage higher-acuity patients at home. The CMS Acute Hospital Care at Home program validates the clinical safety of shifting select DRGs outside the hospital. While inpatient rehabilitation hospitals benefit from a 2.6% payment update and new social-risk quality metrics, long-term acute-care hospitals confront site-neutral rate pressures that erode legacy margins. Outpatient rehab clinics face a reimbursement haircut under the 2025 Physician Fee Schedule, whereas hospice providers enjoy a 2.9% uplift alongside longer average lengths of stay. Overall, the post-acute care market increasingly hinges on cross-setting partnerships that allow seamless escalation or de-escalation without unnecessary readmissions.

Institutional operators that adopt hybrid staffing—blending in-person clinicians with virtualists—can flex capacity and keep census levels stable. Conversely, facilities slow to integrate analytics and home-transition workflows risk referral leakage to tech-forward agencies. Capital now gravitates toward asset-light models, decentralized logistics, and cloud-based care management systems. The competitive frontier lies in demonstrating how each visit, whether virtual or physical, measurably advances functional status within bundled payment windows.

By Patient Type:

Adult Segment Accelerates Beyond DemographicsAdults record the fastest growth—7.32% CAGR—despite the elderly segment controlling the largest share of revenue. Workplace injuries, early-onset chronic diseases, and expanded insurance coverage for rehabilitation drive higher adult utilization. The post-acute care market size for adults is projected to widen as employers emphasize return-to-work programs and as value-based payers subsidize preventive rehab to deter costly complications. Tele-rehab platforms that gamify therapy sessions resonate with tech-savvy adults, supporting adherence and remote progress tracking.

Children and neonates remain the smallest share but see rising acuity as pediatric post-intensive-care syndrome protocols spread. Tele-consults connect pediatric intensivists to rural hospitals, mitigating specialist shortages and avoiding transfers. For geriatric patients, fall prevention, medication reconciliation, and dementia-specific behavior plans dominate care plans. Providers agile enough to tailor protocols by age and diagnosis capture diversified revenue streams and hedge against demographic shifts.

By Application:

Neurological Disorders Drive Innovation AdoptionNeurological rehabilitation’s 7.41% CAGR stems from breakthroughs in exoskeletons, VR-guided motor retraining, and AI-driven dosing of electrical stimulation. Closed-loop systems adjust resistance in real time to maintain engagement and avoid plateauing. Meanwhile, wound management sustains its 31.64% revenue lead through smart dressings containing fluorescent nanosensors that detect infection and trigger care alerts. Amputation rehab evolves with multi-articulating prosthetics and myoelectric control strategies that require specialized training programs.

Musculoskeletal and cardiopulmonary rehab gain from app-based adherence trackers, yet their growth trails neuro because payers increasingly differentiate payments based on objective functional gains—metrics more readily captured by sensor-rich neuro devices. Providers that invest in interoperability, evidence generation, and clinician training for these tools advance their bargaining position with both payers and integrated delivery systems.

By Setting Type:

Home-Based Care Redefines Service DeliveryHome-based models grow at 7.50% CAGR, challenging institution-based incumbents that held 67.10% of revenue in 2025. The post-acute care market sees home-based episodes reimbursed at lower cost, with comparable or superior outcomes when supported by IoT vitals, nurse call centers, and pharmacy couriers. Community-based PACE sites expand in many states, blending adult day services with on-demand physician access under capitated contracts. Remote patient monitoring uses AI to triage alerts, allowing scarce clinicians to focus on high-risk deviations.

For facilities, the imperative is to extend their brand into the home via joint ventures or de-novo agencies. Operators that integrate wearable data into electronic health records create closed-loop feedback and fulfill new payer reporting requirements. Conversely, those tethered to real estate-heavy footprints face occupancy volatility and rising labor costs that compress margins.

Geography Analysis

North America Post-Acute Care (PAC) Market

North America accounts for 40.95% of global revenue, propelled by Medicare policy stability, mature referral networks, and broad EHR adoption. The Acute Hospital Care at Home waiver demonstrates viability for acute-level home episodes, and a 4.33% Medicare Advantage rate hike in 2026 incentivizes further network optimization. Yet the region wrestles with more than 100,000 unfilled caregiver roles, spurring investment in documentation automation and task-sharing to preserve quality scores.

APAC Post-Acute Care (PAC) Market

Asia-Pacific posts the fastest regional CAGR at 7.60%, underpinned by rapid demographic aging and accelerating health-system modernization. Governments pilot bundled payment models and subsidize telehealth investments to offset bed shortages. Urban middle-class populations embrace consumer health tech, enabling agencies to leapfrog straight to virtual case management. Nevertheless, workforce training variability and fragmented regulations can hamper cross-border expansion.

EMEA and LATAM Post-Acute Care (PAC) Market

Europe maintains steady growth as national health systems recalibrate discharge pathways to clear inpatient backlogs. SNF equivalents see pressure to report staffing ratios and infection-control metrics. Eastern European markets open new opportunities for technology exporters as they digitize rehabilitation clinics. Meanwhile, Latin America, the Middle East, and Africa present emerging potential but hinge on economic stability, insurance penetration, and basic infrastructure upgrades such as broadband connectivity and supply-chain cold chains for biologics.

Competitive Landscape

Consolidation intensifies as vertically integrated payers and health systems target seamless episode control. UnitedHealth Group closed its USD 5.4 billion purchase of LHC Group and seeks clearance to acquire Amedisys for USD 3.3 billion, a deal that would command roughly 10% of U.S. home health volume. Data interoperability between Optum analytics and home-health field staff aims to reduce readmissions and elevate Star Ratings. The move pressures regional independents to join alliances or specialize in niche therapies such as complex wound care.

Encompass Health operates 161 inpatient rehab hospitals across 37 states and plans 6-10 new facilities annually plus bed expansions through 2027. The company partners with not-for-profit systems to secure referral pipelines, while investing in predictive modeling that schedules therapy minutes to peak patient energy levels. The Ensign Group continues a roll-up strategy, adding five facilities in April 2025 to reach 343 operations, leveraging centralized back-office functions to boost EBITDAR.

Private-equity ownership now covers an estimated single-digit share of U.S. nursing homes; studies associate these locations with lower quality ratings and higher fines, prompting legislators to consider stricter transparency rules. Technology vendors such as Current Health and Biofourmis form partnerships with hospital-at-home operators to supply wearable kits and analytics that quantify patient stability. Competitive advantage hinges on demonstrable outcome improvement, payer-aligned reporting, and workforce practices that keep turnover below industry medians.

Post-Acute Care (PAC) Industry Leaders

-

Kindred Healthcare

-

LHC Group

-

Genesis Healthcare

-

Brookdale Senior Living Inc.

-

Amedisys Inc .

- *Disclaimer: Major Players sorted in no particular order

Post-Acute Care (PAC) Market Companies Covered in this Report

- Amedisys Inc.

- LHC Group (Optum)

- Encompass Health Corp.

- Brookdale Senior Living Inc.

- Genesis HealthCare

- Kindred Healthcare (ScionHealth)

- Select Medical

- AccentCare Inc.

- Aveanna Healthcare

- Vitas Healthcare

- naviHealth (Optum)

- CareCentrix (Elevance Health)

- AdventHealth

- HCR ManorCare

- Sonida Senior Living

- Trilogy Health Services

- ProMedica Senior Care

- National HealthCare Corp.

- Lifepoint Rehabilitation

- Brookdale Hospice

- Interim HealthCare

Recent Industry Developments in Post-Acute Care (PAC) Market

- May 2025: UnitedHealth and Amedisys agreed to divest selected home health and hospice sites to BrightSpring and Pennant Group to address DOJ antitrust concerns tied to their USD 3.3 billion merger.

- April 2025: The Ensign Group acquired five new facilities, expanding its portfolio to 343 operations and signaling continued consolidation in senior care.

- January 2025: Baptist Health entered a joint venture with Alternate Solutions Health Network to scale home-health services across Kentucky, Indiana, and Illinois.

- January 2025: AdventHealth launched a Hospital at Home program in Central Florida, enabling acute-level care with daily in-person visits and 24/7 virtual oversight.

Global Post-Acute Care (PAC) Market Report Scope

As per the scope of the report, post-acute care refers to a range of healthcare services and support provided to individuals recovering from an acute illness, injury, or surgery. It focuses on helping patients regain their functional abilities, improve their quality of life, and transition back to their home or community setting. Post-acute care is a critical component of the healthcare continuum, providing specialized medical and rehabilitative services to individuals who require continued care after being discharged from a hospital.

The post-acute care market is segmented into services, patient type, application, and geography. By services, the market is segmented into skilled nursing facilities, inpatient rehabilitation facilities, long-term acute care hospitals, home health care, and other services. By patient type, the market is segmented into elderly, adult, and other patient types. By application, the market is segmented into amputations, wound management, brain injury and spinal cord injury, neurological disorders, and other applications. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizes and forecasts were made based on value (USD).

Segmentation Overview

| Skilled Nursing Facilities (SNF) |

| Inpatient Rehabilitation Facilities (IRF) |

| Long-term Acute Care Hospitals (LTACH) |

| Home Health Care |

| Assisted Living Facilities |

| Out-patient Rehabilitation Clinics |

| Palliative & Hospice Care Facilities |

| Others |

| Elderly |

| Adults |

| Children and Neonates |

| Amputations |

| Wound Management |

| Brain and Spinal Cord Injury |

| Neurological Disorders |

| Other Applications |

| Institution-Based |

| Home-Based |

| Community-Based |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Skilled Nursing Facilities (SNF) | |

| Inpatient Rehabilitation Facilities (IRF) | ||

| Long-term Acute Care Hospitals (LTACH) | ||

| Home Health Care | ||

| Assisted Living Facilities | ||

| Out-patient Rehabilitation Clinics | ||

| Palliative & Hospice Care Facilities | ||

| Others | ||

| By Patient Type | Elderly | |

| Adults | ||

| Children and Neonates | ||

| By Application | Amputations | |

| Wound Management | ||

| Brain and Spinal Cord Injury | ||

| Neurological Disorders | ||

| Other Applications | ||

| By Setting Type | Institution-Based | |

| Home-Based | ||

| Community-Based | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the post-acute care market in 2031?

The post-acute care market size is forecast to reach USD 1.35 trillion by 2031.

Which service segment is growing the fastest?

Home health care records the highest growth, expanding at a 7.30% CAGR through 2031 as hospital-at-home models scale.

Why is neurological rehabilitation gaining momentum?

Advances in robotics, virtual reality, and AI-guided stimulation deliver measurable functional gains, driving a 7.41% CAGR in this application.

Which region offers the most rapid growth opportunity?

Asia-Pacific is expected to grow at a 7.60% CAGR, driven by rapid population aging and health-system modernization.

How are workforce shortages being addressed?

Providers deploy tele-supervised assistants, AI-enabled documentation tools, and apprenticeship programs to mitigate the impact of over 100,000 unfilled caregiver roles.

What impact will the Medicare Advantage rate increase have on providers?

The 4.33% payment uplift in 2026 incentivizes network optimization, rewarding facilities that can document superior outcomes and lower readmissions.

Page last updated on: