Wheatgrass Product Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

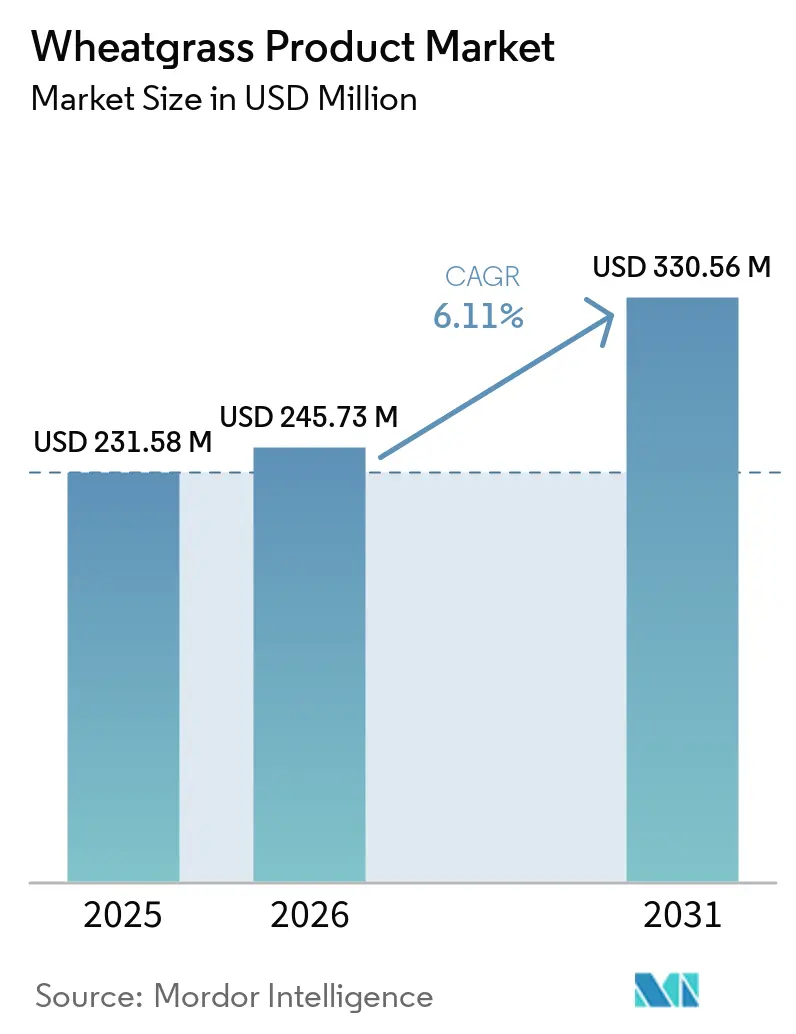

| Market Size (2026) | USD 245.73 Million |

| Market Size (2031) | USD 330.56 Million |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wheatgrass Product Market Analysis by Mordor Intelligence

The wheatgrass products market size is expected to grow from USD 231.58 million in 2025 to USD 245.73 million in 2026 and is forecast to reach USD 330.56 million by 2031 at 6.11% CAGR over 2026-2031. This growth is primarily fueled by an increasing consumer preference for plant-based wellness routines that emphasize immunity enhancement and detoxification as part of everyday health practices. Wheatgrass products, available in various formats such as powder, juice, and pills, have transitioned from being exclusive to niche health-food stores to becoming widely available in mainstream retail outlets and e-commerce platforms. The demand for organic labeling has further strengthened, as it not only justifies premium pricing but also enhances consumer trust in brands. Among the product formats, pills are gaining popularity due to their convenience, while powders continue to dominate retail shelves because of their versatility in recipes and lower cost per serving. Geographically, North America remains the largest market for wheatgrass products. However, the Asia-Pacific region is experiencing rapid growth, supported by increasing penetration of dietary supplements, a growing adoption of vegan diets, and the implementation of favorable food-safety regulations.

Key Report Takeaways

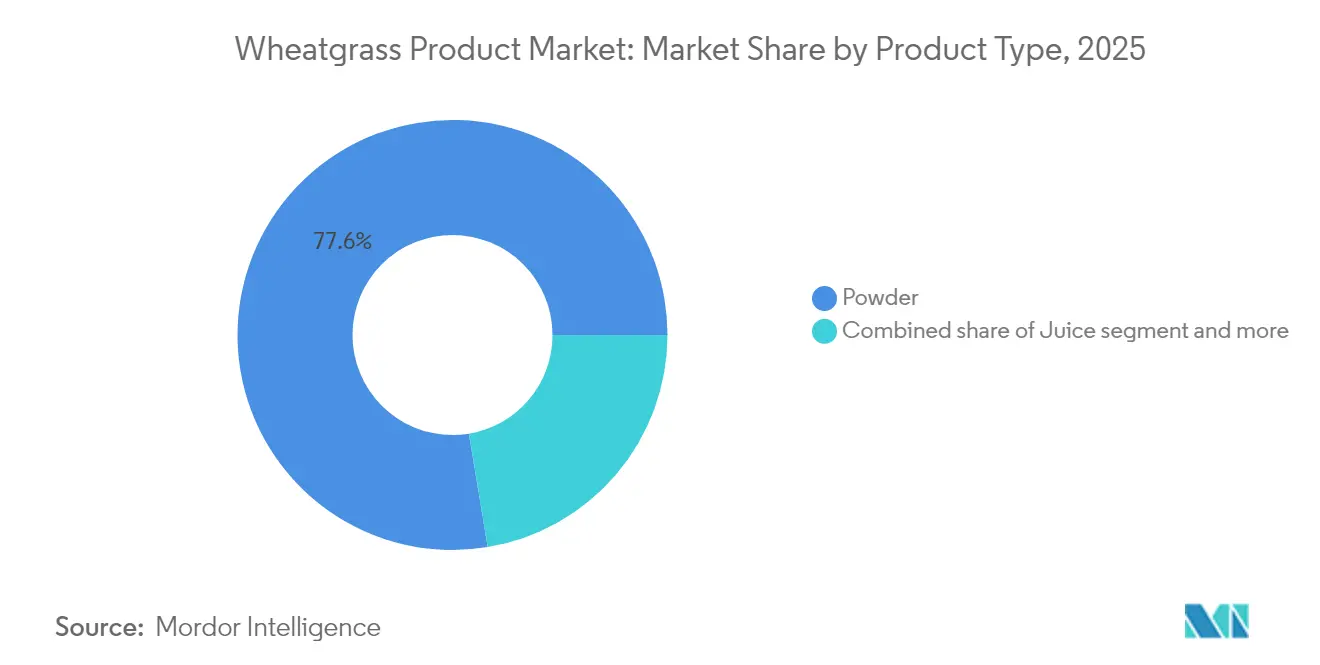

- By product type, powder held 77.62% of the wheatgrass products market share in 2025; pills are rising at a 7.18% CAGR through 2031.

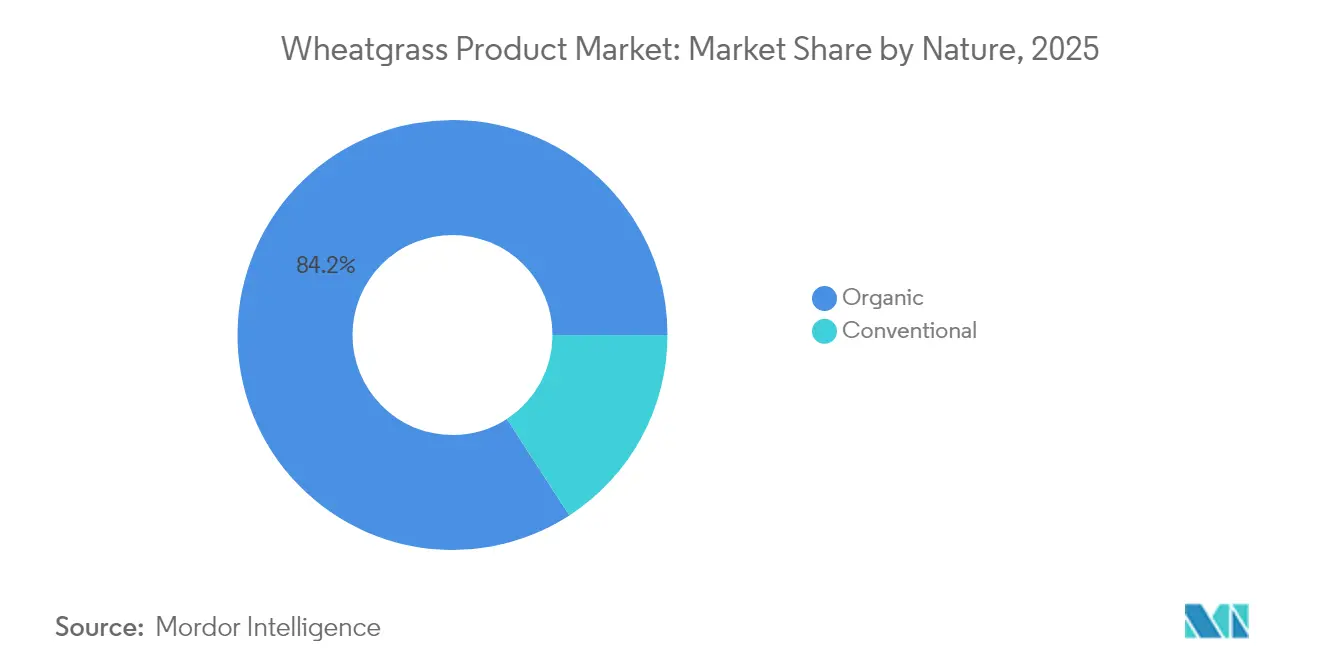

- By nature, organic accounted for 84.15% of the wheatgrass products market size in 2025 and is advancing at a 7.62% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 35.12% of sales in 2025, while online retail is forecast to expand at an 7.71% CAGR to 2031.

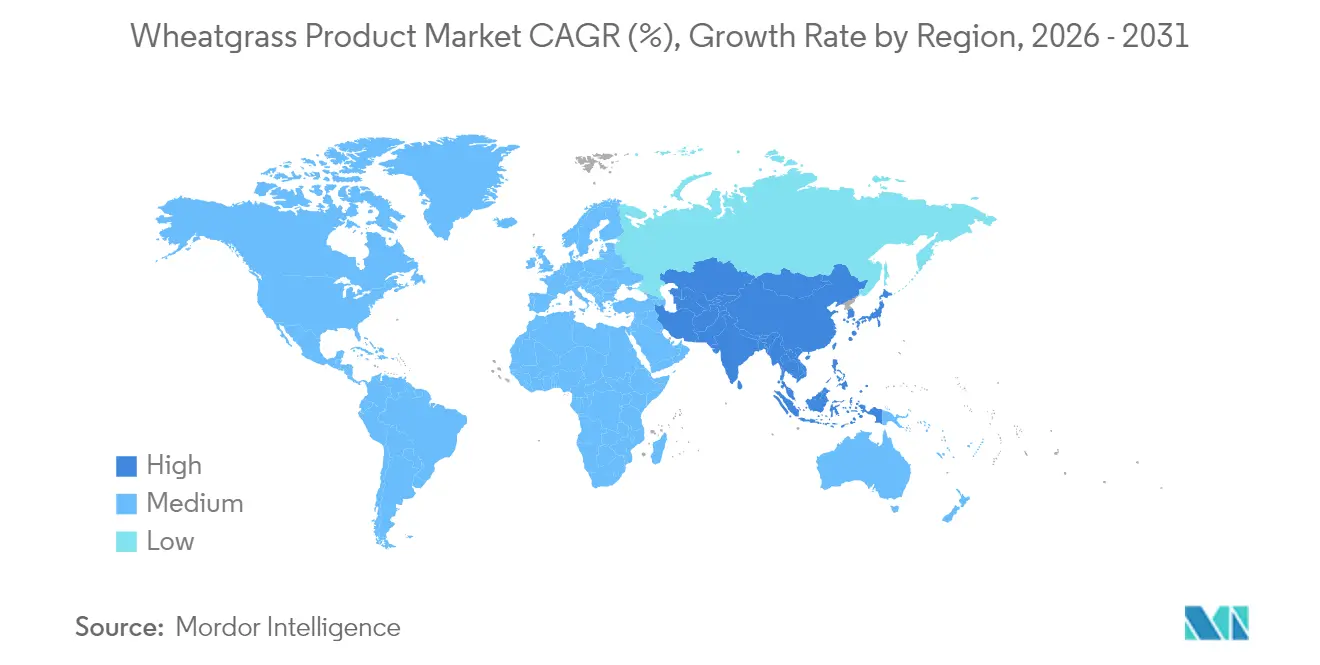

- By geography, North America generated 54.88% of 2025 revenue, whereas Asia-Pacific is forecast to register the fastest 7.21% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wheatgrass Product Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural detox and immunity supplements | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing prevalence of chronic illnesses | +0.9% | Global, particularly acute in North America, Europe, and emerging Asia | Long term (≥ 4 years) |

| Growing popularity of detoxification and immunity-boosting trends | +0.8% | North America, Europe, urban India and China | Short term (≤ 2 years) |

| Surge in plant-based, vegan, and vegetarian diets favoring nutrient-rich superfoods | +1.1% | Global, led by North America and Europe, accelerating in Asia-Pacific | Medium term (2-4 years) |

| Advancements in regenerative farming and processing technologies | +0.7% | North America, Europe, with adoption spreading to Brazil and India | Long term (≥ 4 years) |

| Personalised-nutrition apps recommending wheatgrass | +0.5% | Urban markets in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for natural detox and immunity supplements

In the aftermath of the pandemic, consumers have increasingly integrated immunity-boosting and detoxification practices into their daily wellness routines. This behavioral shift has driven a sustained demand for botanical supplements, which are now perceived as preventive health measures rather than reactive remedies. Among these, wheatgrass has gained attention due to its high chlorophyll content and antioxidant properties, which resonate strongly with detoxification narratives. However, it is important to highlight that the clinical evidence supporting these claims remains limited, primarily stemming from small-scale trials. In India, the nutraceuticals sector mirrors this global trend, experiencing significant growth as households frequently consume vitamins, minerals, and herbal supplements, often without consulting healthcare professionals. This shift from treatment-oriented to preventive consumption patterns is particularly evident in urban markets, where consumers are increasingly prioritizing proactive health management. The structural demand for such products is expected to stabilize over the medium term, as the process of habit formation and the establishment of repeat purchase cycles typically takes 2-4 years to solidify across various demographic groups.

Increasing prevalence of chronic illnesses

The global rise in chronic diseases positions wheatgrass as a nutrient-dense option, particularly for individuals managing diabetes, cardiovascular conditions, and obesity. For example, the World Health Organization (WHO) states that cardiovascular diseases (CVDs) account for over 42.5% of annual deaths in Europe in 2024, making them the leading cause of disability and premature death in the region[1]Source: World Health Organization (WHO), "Cardiovascular diseases kill 10 000 people", who.int. The USDA's 2024 guidelines for vegan diets emphasize the necessity of supplements such as vitamin B12, vitamin D, calcium, iron, and DHA/EPA. This is especially important for individuals on plant-based diets, commonly adopted by chronic disease patients, to meet their Dietary Reference Intakes. Iron requirements, in particular, are 1.8 times higher due to the lower bioavailability of non-heme iron. Wheatgrass, rich in vitamins A, C, E, and essential minerals, is increasingly marketed as a solution to address these nutritional gaps. However, its efficacy compared to targeted supplementation remains under-researched. While the long-term nature of chronic disease management ensures consistent demand, the market penetration of wheatgrass depends on clinical validation and endorsements from healthcare professionals, support that remains limited compared to established interventions like omega-3 or vitamin D.

Surge in plant-based, vegan, and vegetarian diets favoring nutrient-rich superfoods

As the global trend shifts increasingly towards plant-based diets, wheatgrass is experiencing significant growth in adoption. According to the Good Food Institute, in 2024, around 40% of adults in Germany and the UK plan to increase their plant-based food consumption[2]Source: The Good Food Institute, "State of the Industry 2024", gfi.org. Health reasons account for 48% of this shift, while environmental concerns represent 29%, and animal welfare considerations comprise 25%. Wheatgrass, known for its clean-label attributes, vegan compatibility, and gluten-free nature, is well-suited for incorporation into functional beverages and superfood powders. The plant-extract market is projected to grow at a robust CAGR of 12.4% through 2030, driven by a growing consumer preference for food-derived phytonutrients and supported by clinical research validating the efficacy of bioactive compounds. In India, the functional beverages segment has emerged as the largest contributor within the broader nutraceuticals market. However, wheatgrass faces notable challenges in the medium term due to intense competition from alternatives such as moringa, spirulina, and chlorella. These substitutes offer comparable nutrient profiles and are often perceived as more palatable by consumers. Additionally, the increasing popularity of multi-ingredient superfood blends, where wheatgrass is typically one of 5-10 components, diminishes the ability of single-ingredient products to stand out in the market and maintain strong pricing power.

Advancements in regenerative farming and processing technologies

While innovations in perennial wheat cultivation and regenerative agriculture are successfully cutting input costs and minimizing environmental impacts, their adoption on a commercial scale has been limited. Processing methods like freeze-drying and cold-press juicing are now addressing past quality issues of wheatgrass products by preserving their enzymatic activity and nutrient density. According to the OECD-FAO Agricultural Outlook 2024-2033, real cereal prices are expected to see modest declines, and fertilizer costs are set to ease from their 2022 peaks. This trend could alleviate some input-cost pressures for wheatgrass growers. Yet, compliance with organic certification standards, such as the USDA's 7 CFR Part 205 and similar regulations in Europe and India, continues to impose significant costs. These costs are especially burdensome for smaller producers. The future success of these technologies hinges on achieving better yields and matching costs with conventional methods, a goal that remains over four years away from widespread realization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong earthy taste limits repeat purchase | -0.6% | Global, particularly acute in North America and Europe where flavor expectations are high | Short term (≤ 2 years) |

| High production costs associated with organic cultivation and quality preservation | -0.8% | Global, with greatest impact in North America and Europe due to labor costs and certification overhead | Medium term (2-4 years) |

| Intense competition from other superfoods | -0.5% | Global, with moringa and spirulina competition most intense in North America and urban Asia | Medium term (2-4 years) |

| Stringent regulatory requirements for health claims | -0.4% | Europe (EFSA), North America (FDA), with emerging complexity in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong earthy taste limits repeat purchase

Wheatgrass's grassy and bitter flavor profile continues to act as a significant deterrent for first-time users, while also limiting repeat purchase rates, making sensory acceptance the primary obstacle to its mainstream adoption. To address this challenge, the industry has implemented various strategies, including flavor masking through encapsulation, blending wheatgrass with naturally sweeter ingredients such as pineapple or apple in juice formulations, and introducing gummy formats that completely eliminate the need to taste the product. Amazing Grass's upcoming launch of "Amazing Greens Mood Blend" in March 2024 highlights a dual approach of flavor innovation and functional positioning to overcome this barrier. Although consumer surveys consistently identify taste as the leading reason for discontinuation, the industry's continuous advancements in formulation are steadily reducing this gap and improving consumer acceptance.

High production costs associated with organic cultivation and quality preservation

Harvesting organic wheatgrass is labor-intensive and requires stringent pest management without synthetic inputs. Additionally, cold-chain logistics are essential for fresh juice products. These factors collectively elevate production costs by 30-50% compared to conventional methods. Obtaining USDA organic certification, as stipulated under 7 CFR Part 205, involves a three-year transition period, meticulous record-keeping, and annual inspections, posing challenges for newcomers. Juice products grapple with a short shelf life, necessitating capital-intensive methods like high-pressure processing or flash-freezing. While the OECD-FAO outlook hints at easing fertilizer costs from 2022 peaks, organic producers remain tethered to compost and biological inputs, missing out on this trend. Such structural cost challenges squeeze profit margins, making it tough to compete on price with spirulina or moringa. The latter enjoys an edge, thanks to established cultivation infrastructure in cost-effective regions. The medium-term outlook remains challenging, as achieving cost parity hinges on either significant yield breakthroughs or elusive scale economies for many producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pills Gain Ground Despite Powder Dominance

In 2025, powder products accounted for 77.62% of the market share, highlighting their adaptability in smoothies, shakes, and functional beverages. Their popularity is further supported by lower per-dose costs compared to encapsulated formats. However, pills, comprising tablets and capsules, are experiencing significant growth, expanding at a 7.18% CAGR through 2031. This growth, the fastest among product types, is driven by their convenience, precise dosing, and ability to eliminate taste barriers. Urban consumers, particularly those with busy schedules and individuals managing chronic conditions, find pills especially appealing. They value the consistent dosing pills offer over the flexibility of preparation. On the other hand, the juice segment, the smallest in the market, faces challenges such as a short shelf life and the need for cold-chain logistics. Nonetheless, there is niche demand in juice bars and wellness centers, where the fresh-pressed appeal commands premium pricing.

Encapsulation technology is advancing rapidly. Manufacturers are increasingly adopting enteric coatings to enhance bioavailability and reduce gastric discomfort, directly addressing past concerns about wheatgrass's digestive effects. At the same time, the broader dietary supplements market is shifting toward gummy and chewable formats. While powder's dominance is expected to continue through 2031, supported by established supply chains and simpler manufacturing processes, a convergence in growth rates between pills and powders by the end of the decade could indicate pills' successful mainstream adoption. Regulatory frameworks, such as Japan's Food with Function Claims system, which requires clinical evidence for health claims, favor standardized pill formats. This preference for variable-composition powders could accelerate the shift toward pills in Asian markets.

By Nature: Organic Certification as Competitive Moat

In 2025, organic wheatgrass accounted for a significant 84.15% of the market share and is projected to grow at a strong 7.62% CAGR through 2031. This growth not only surpasses that of conventional variants but also establishes organic certification as a key factor for premium market positioning. Consumers are increasingly willing to pay a 20-30% premium for organic labels due to concerns over pesticide residues and heavy-metal contamination, issues that have long affected non-certified herbal supplements. In 2022, FSSAI's Ayurveda Aahara regulations required herbal products in India to comply with Good Agricultural and Collection Practice (GACP). This regulation has effectively raised quality standards, favoring established organic producers. Additionally, Europe's micronutrient inadequacy crisis, impacting 40% of its population for essential vitamins, has driven higher demand for certified, traceable supplements. In fragmented markets, organic labels have become reliable indicators of quality.

Conventional wheatgrass is becoming less relevant, with its appeal limited to price-sensitive segments. Retail buyers are increasingly demanding organic certification for shelf placement. The USDA's three-year transition period for organic certification serves as both a protective barrier for incumbent producers and a constraint on supply flexibility during demand surges. While India's abundant agricultural resources and cost-effective labor make it a potential low-cost organic supplier, challenges such as insufficient cold storage and processing infrastructure limit its export capabilities. The similar growth rates of organic products and the overall market indicate a gradual replacement of conventional products, a trend likely to accelerate as regulatory oversight becomes stricter.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

In 2025, supermarkets and hypermarkets represented 35.12% of total sales, benefiting from foot traffic and impulse buying. However, online retail stores are growing at the fastest rate among all channels, with an 7.71% CAGR projected through 2031. This growth is driven by subscription models, personalized recommendations, and a wide product assortment. Increasing internet penetration further supports the expansion of online retail. As of 2024, 5.5 billion people, or 68% of the global population, were internet users, according to the International Telecommunication Union. At the same time, direct-to-consumer brands are bypassing traditional retail by leveraging Instagram and YouTube influencers to encourage trials and using subscription models to maximize customer lifetime value.

Specialty stores, such as health-food outlets and juice bars, are losing market share as their assortment advantages decline and price competition intensifies. Convenience stores and other channels remain minor players, constrained by limited shelf space and a weak consumer association with wellness products. While brick-and-mortar stores still account for 94% of India's nutraceutical sales, the trend is shifting toward online platforms. This shift is particularly evident as quick-commerce services like Blinkit and Zepto expand their product ranges to include supplements. However, regulatory compliance for online sales, including accurate labeling and adverse-event reporting, remains inconsistent across markets, creating challenges for platforms and brands.

Geography Analysis

North America held a leading 54.88% share of global revenues 2025, driven by high per-capita supplement spending, a well-developed retail infrastructure, and strong consumer awareness of superfoods. While Canada and Mexico contribute smaller shares, Mexico's expanding middle class and wellness trends indicate untapped potential. The FDA's regulation of dietary supplements under the 1994 DSHEA provides a more permissive regulatory environment compared to Europe. However, increasing scrutiny of heavy-metal contamination in herbal products is raising quality standards. Although the region's mature market status suggests slower growth, innovation in functional beverages and gummy formats could help maintain momentum.

Asia-Pacific is the fastest-growing region, with a projected 7.21% CAGR through 2031. This growth is primarily driven by India's USD 8 billion nutraceuticals market, which is expanding at an annual rate of 11%, and China's increasing health awareness. India's widespread micronutrient deficiencies and rising household supplement adoption create a significant market opportunity. Additionally, the FSSAI's 2022 Ayurveda Aahara regulations provide a clear framework for wheatgrass products as functional foods. Japan's functional food market, valued at USD 30-40 billion, offers strong potential. Its notification-based Food with Function Claims system, which has approved over 1,700 products, is more accessible than the stricter FOSHU pathway. Meanwhile, China's updated 2024 health-food filing rules maintain positive-ingredient lists, requiring specific approvals for wheatgrass. This creates both entry barriers and quality assurance. Although Australia and New Zealand contribute smaller shares, their strong preference for organic and clean-label products aligns well with wheatgrass positioning. However, the region's growth is challenged by price sensitivity, fragmented regulations, and competition from traditional herbal remedies like Ayurvedic and TCM formulations.

Europe, South America, and the Middle East and Africa collectively represent the remaining market share. Europe demonstrates strong demand, primarily due to micronutrient inadequacies. However, EFSA's stringent health-claim substantiation requirements under Directive 2002/46/EC pose compliance challenges. At the same time, these strict measures help differentiate approved products in competitive markets. Germany, the United Kingdom, and France lead consumption, with organic and vegan certifications being key purchase drivers. South America, still in its early stages, shows potential in Brazil and Argentina due to their agricultural capacity and growing wellness trends. However, infrastructure gaps and import tariffs hinder market growth. The Middle East and Africa are slowly emerging, with the UAE and South Africa leading adoption among affluent urban consumers. Nevertheless, underdeveloped regulatory frameworks and fragmented distribution networks remain obstacles. These regions collectively offer long-term opportunities, dependent on infrastructure investments and regulatory harmonization.

Competitive Landscape

The wheatgrass products market exhibits moderate concentration. Established supplement multinationals, including NOW Foods, Glanbia's Amazing Grass, and Nestlé's Garden of Life, dominate the wheatgrass products market, leveraging their scale, retail ties, and brand strength to secure a notable combined market share. Competing fiercely, regional specialists like Pines International and Navitas Organics, along with Indian players such as Kapiva, Organic India, and Jivo Wellness, utilize Ayurvedic positioning, local supply-chain benefits, and direct-to-consumer strategies to sidestep traditional retail markups.

There are untapped opportunities in integrating personalized nutrition, collaborating with coffee and smoothie chains on functional beverages, and introducing gummy formats to overcome taste challenges. To stay ahead, companies are channeling investments into product innovation, emphasizing value-added ingredients. A favored strategy for gaining market traction involves expanding production capacities and distribution networks. Key market players encompass Pines International Inc., Nestlé S.A., Glanbia plc, NOW Foods, and Naturya Limited, among others.

Disruptors on the rise include direct-to-consumer brands harnessing influencer marketing and subscription models to cultivate loyalty sans retail middlemen. Additionally, private-label products from e-commerce giants like Amazon and iHerb are making waves, offering prices 20-30% lower than established brands. Leaders in the sector are turning to freeze-drying and cold-press extraction techniques to maintain nutrient density. They're also prioritizing GACP compliance and third-party testing, setting themselves apart in a market often marred by adulteration issues. The 2022 introduction of India's FSSAI Ayurveda Aahara regulations enforces formulation and safety standards, benefiting players with robust compliance frameworks. As suppliers of moringa and spirulina venture into multi-ingredient superfood blends, the competitive landscape intensifies, diluting wheatgrass's unique standing. In response, companies are undertaking clinical trials to validate health claims, forging alliances with functional beverage brands, and broadening their reach into the rapidly evolving regulatory landscape of high-growth Asia-Pacific markets.

Wheatgrass Product Industry Leaders

-

Pines International Inc.

-

Nestlé S.A.

-

Glanbia plc

-

NOW Foods

-

Naturya Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Pines International Inc. unveiled its latest offering: Wheatgrass Capsules. These capsules are promoted as a user-friendly supplement designed to enhance immunity and energy levels.

- April 2024: Amazing Grass, a brand under Glanbia, introduced "Amazing Greens Mood Blend," a wheatgrass-based superfood powder designed to support mental wellness and manage stress. This launch marks the brand's entry into the functional mood-support market.

Global Wheatgrass Product Market Report Scope

| Juice |

| Powder |

| Pills (Tablets and Capsules) |

| Organic |

| Conventional |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Juice | |

| Powder | ||

| Pills (Tablets and Capsules) | ||

| By Nature | Organic | |

| Conventional | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the wheatgrass products market in 2026?

The wheatgrass products market size is USD 245.73 million in 2026.

What is the expected CAGR for wheatgrass products through 2031?

Revenue is forecast to grow at a 6.11% CAGR between 2026 and 2031.

Which product format leads current sales?

Powder leads, holding 77.62% of 2025 sales value.

Why is organic wheatgrass outpacing conventional?

Consumers pay premiums for pesticide-free assurance, lifting organic to 84.15% share in 2025.

Page last updated on: