Dry-Packaged Scallops Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

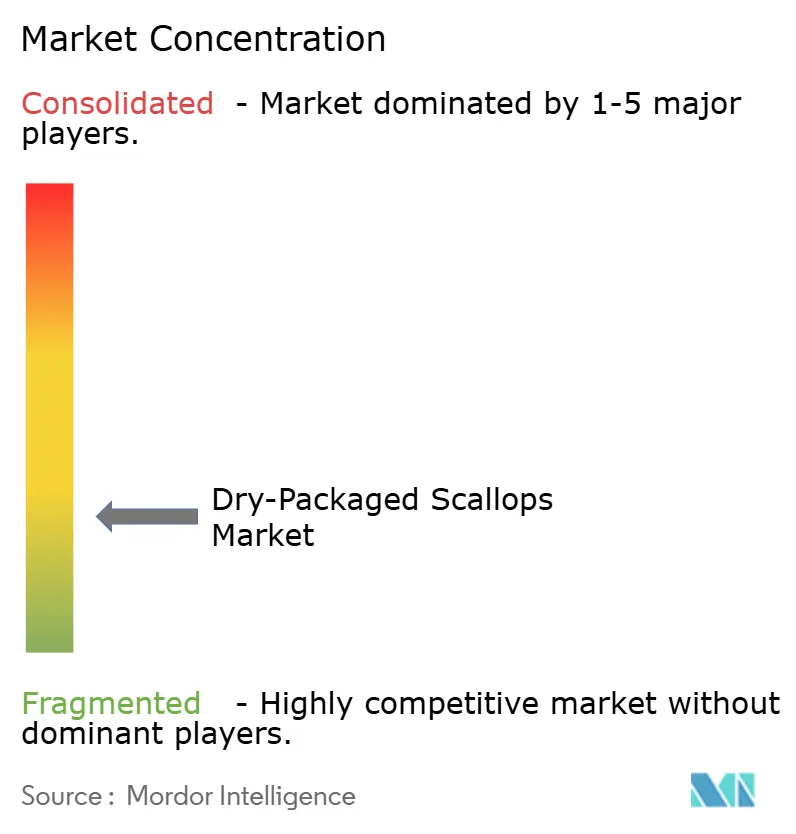

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dry-Packaged Scallops Market Analysis by Mordor Intelligence

The dry-packed scallops market size is expected to grow from USD 2.76 billion in 2025 to USD 2.87 billion in 2026 and is forecast to reach USD 3.51 billion by 2031 at 4.11% CAGR over 2026-2031. This growth is driven by a surge in consumer demand for chemical-free seafood, strong regulatory backing for sustainable harvesting, and consistent investments in advanced freezing and dry-pack technologies. The widening customer base is bolstered by premium positioning in food service, an increase in MSC-certified quotas, and innovative products that boast extended shelf lives. However, fragmented supply chains and quota-driven landings are keeping prices elevated. The market sees moderate competitive intensity, but this, coupled with supply-side constraints and changing label requirements, is nudging processors towards vertical integration, the adoption of cryogenic freezing, and a shift to value-added formats to safeguard their margins. As food-safety oversight tightens, processors emphasizing traceability and sustainability are securing long-term contracts with both retailers and institutional buyers. While the dry-packed scallops market reaps benefits from the clean-label trend, some channels' price sensitivity might dampen volume growth during cyclical supply shortages.

Key Report Takeaways

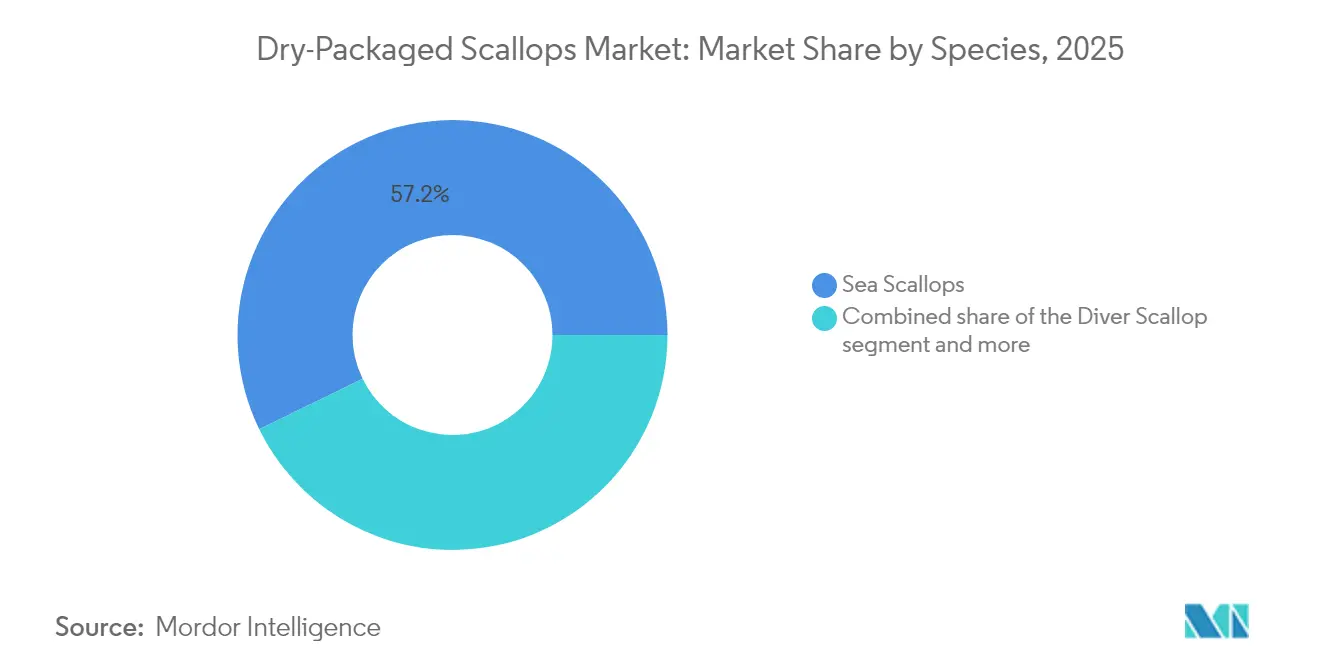

- By species, sea scallops led with 57.22% revenue share in 2025; diver scallops are forecast to expand at a 6.15% CAGR through 2031.

- By form, frozen products accounted for 45.96% of revenue in 2025; dried scallops are projected to grow at a 6.63% CAGR through 2031.

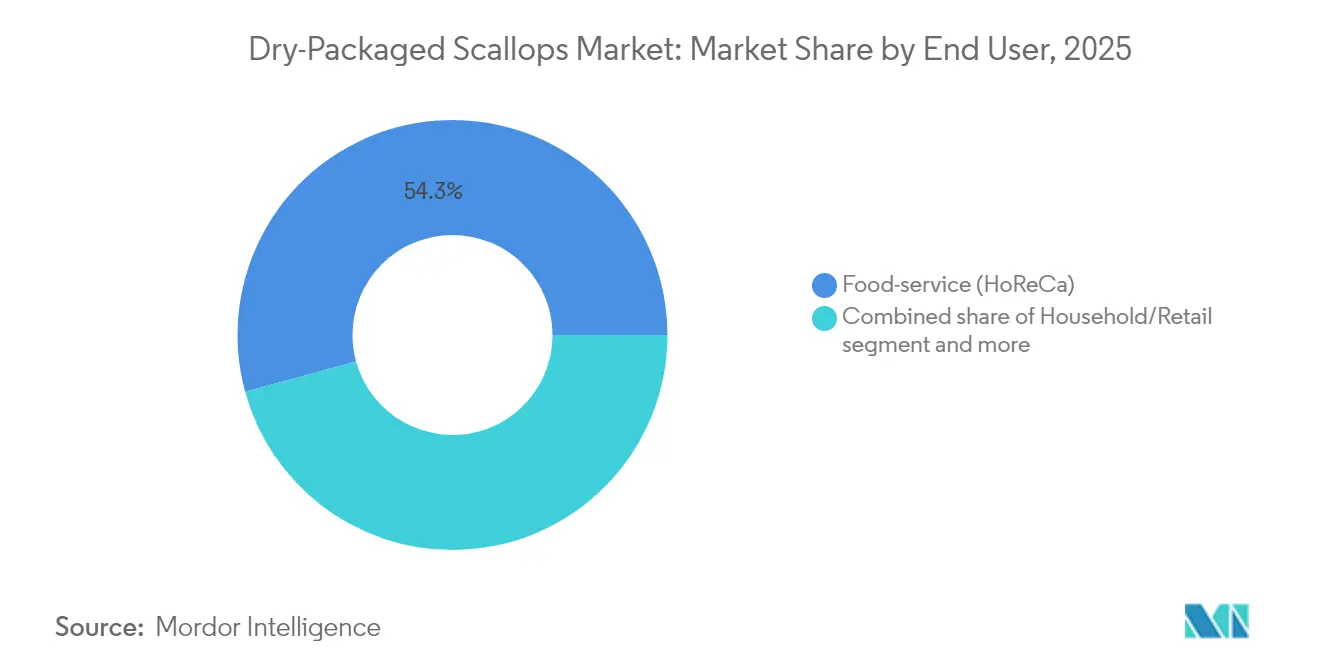

- By end user, the food-service segment held 54.25% of value in 2025; the household/retail channel is set to advance at a 5.61% CAGR to 2031.

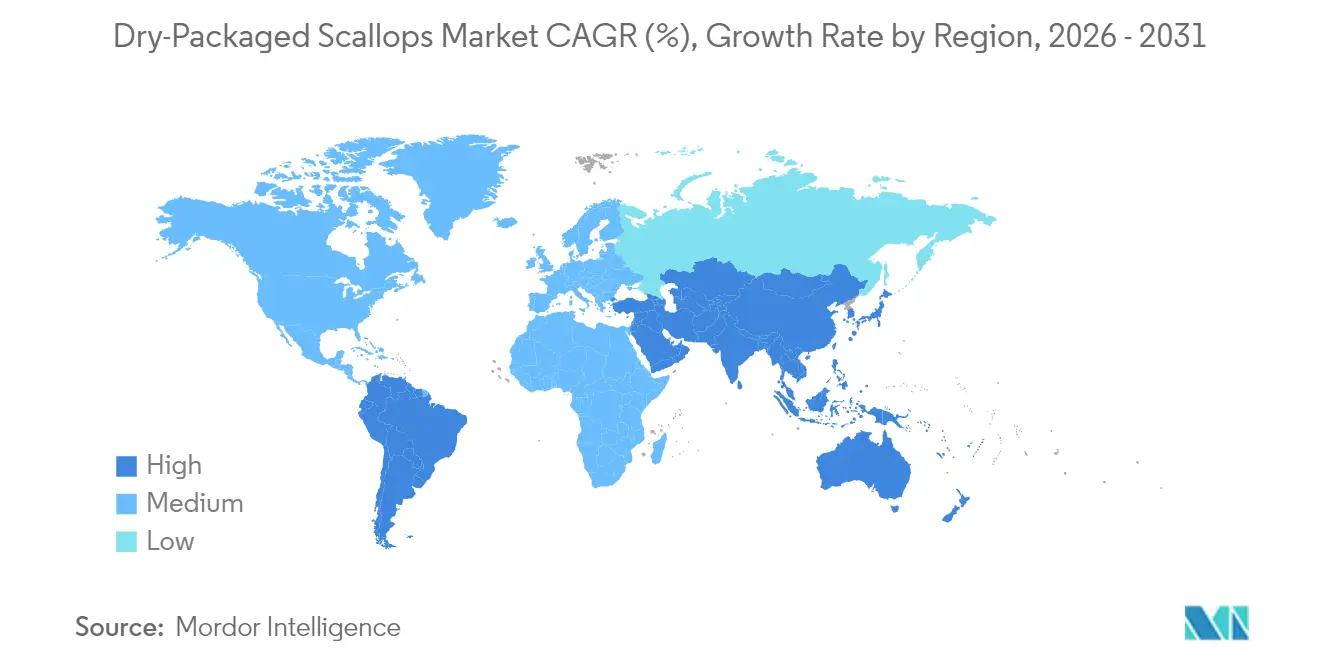

- By geography, North America commanded a 33.10% share in 2025; Asia-Pacific is expected to post the fastest growth at a 5.30% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dry-Packaged Scallops Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for chemical-free "dry" seafood | +0.8% | Global, with premium penetration in North America and Europe | Medium term (2-4 years) |

| Premium price realisation in food-service segment | +0.6% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of MSC-certified Atlantic sea-scallop quotas | +0.4% | North America primary, spill-over to export markets | Long term (≥ 4 years) |

| Product innovation in processing and freezing techniques | +0.5% | Global, led by North American and European processors | Medium term (2-4 years) |

| Advances in freezing and dry-pack technology | +0.3% | Developed markets initially, technology transfer to emerging regions | Long term (≥ 4 years) |

| Product diversification: Value-added scallops | +0.4% | North America and Europe, selective penetration in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising preference for chemical-free "dry" seafood

As health consciousness and culinary sophistication rise, consumers are increasingly favoring natural, unprocessed seafood, especially in premium markets. Dry-packed scallops, in particular, are fetching notable price premiums over their chemically treated counterparts. Chefs, especially in restaurants, are drawn to dry-packed scallops not just for their superior flavor but also for their enhanced searing capabilities. Global Seafoods highlights that these scallops boast greater culinary versatility, with chefs lauding their authentic taste and cooking attributes. This trend is especially strong in North America and Europe, where regulations promote transparent labeling, helping consumers discern processing methods. The Interstate Shellfish Sanitation Conference underscores the significance of proper scallop handling and storage, bolstering the premium status of dry-packed products. As food service operators increasingly champion sustainability and natural processing, the market for chemical-free products is rapidly expanding. This movement resonates with the broader clean-label trend in the food industry, indicating a lasting shift beyond just premium segments.

Premium price realisation in food-service segment

Despite supply constraints, U10 scallops are now commanding prices nearly USD 20 higher than those of last year's levels, thanks to their strategic positioning as premium menu items in food service establishments. This pricing power not only underscores the scallops' scarcity value but also highlights a quality differentiation. Restaurants are capitalizing on the superior culinary properties of dry-packed products, justifying their premium positioning, as reported by Seafood News[1]Source: Seafood News, “U10 Scallop Prices,” seafoodnews.com. Operators in the HoReCa sector note that dry-packed scallops not only differentiate their menus but also bolster higher check averages. This is especially true in fine dining venues, where the origin and preparation of a dish significantly shape customer perceptions. Maine's burgeoning scallop aquaculture industry is riding this wave. Organizations like NOAA Sea Grant are actively promoting both farmed and wild scallops through culinary education programs, spotlighting their quality attributes, as highlighted by the World Aquaculture Society. The food service industry's readiness to shoulder these elevated costs underscores the strategic importance of premium ingredients in the fiercely competitive restaurant landscape. Yet, there's a growing pushback against ongoing price hikes, hinting at potential demand elasticity limits that might temper future price gains, according to Undercurrent News.

Expansion of MSC-certified Atlantic sea-scallop quotas

As the US Atlantic sea scallop fishery retains its Marine Stewardship Council (MSC) certification, quota allocations are rising to meet market demand. NOAA Fisheries has projected landings of 18 million pounds for 2025. Under Framework 39, annual quotas have been boosted to 675,563 pounds, and once off-limits areas are now reopened. This certification offers a competitive edge in markets, especially in Europe, where sustainability credentials play a pivotal role in procurement choices. Fisheries holding the MSC certification showcase their commitment to responsible resource management, employing science-based quotas and habitat protection, ensuring the industry's long-term viability. With expanded quotas, processors can grow their operations while upholding sustainability pledges, alleviating supply constraints that have historically driven up market prices. The MSC certification not only bolsters market access but also aids in premium positioning, as sustainability increasingly sways purchasing choices in both institutional and retail sectors. Yet, it's essential to note that quota management is tethered to biological assessments and environmental factors, introducing supply variability that can sway market stability.

Product innovation in processing and freezing techniques

Innovations in liquid nitrogen quick-freezing and cryogenic systems are transforming scallop preservation, offering enhanced product characteristics over traditional methods. Research from Virginia Tech highlights that cryogenically frozen scallops boast notably lower thaw loss rates: a 4-hour cryogenic process results in a 2.41% thaw loss, while a 24-hour method sees a 4.21% loss[2]Source: Virginia Tech, “Quality of Cryogenically Frozen Sea Scallops,” vt.edu. These advancements empower processors to uphold product quality during prolonged storage, ensuring the texture and nutritional attributes of premium dry-packed products remain intact. The swift freezing rates of liquid nitrogen applications in aquatic products curtail ice crystal formation, bolstering overall product integrity, as noted by the Food Science of Animal Products. Further processing innovations introduce automated ear-hanging equipment in aquaculture, nearly doubling production capacity and slashing labor costs by 43% compared to traditional lantern net culture. Merging advanced freezing technologies with dry-pack processing not only amplifies quality but also bolsters premium market positioning and broadens distribution reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -0.3% | Global, with varying compliance costs by region | Short term (≤ 2 years) |

| Volatile raw material supply and price fluctuations | -0.5% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Short shelf life for premium fresh dry-packed products | -0.2% | Global, with higher impact in distant markets | Medium term (2-4 years) |

| Limited processing infrastructure in emerging markets | -0.3% | Asia-Pacific and developing regions primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety and labeling regulations

Regulatory compliance requirements impose substantial operational costs and complexity on dry-packed scallop processors. The FDA's Fish and Fishery Products Hazards and Controls guidance mandates the implementation of comprehensive hazard identification and control systems, requiring processors to establish robust monitoring protocols. Recent updates to FDA guidelines have expanded post-harvest treatment requirements and pathogen control measures, particularly for shellfish products that require specific handling procedures[3]Source: U.S. FDA, “Fish and Fishery Products Hazards and Controls,” fda.gov. NOAA's Seafood Inspection Program regulations, which took effect in January 2025, establish standardized procedures that require significant investment in compliance. Additionally, Mandatory Country of Origin Labeling (COOL) requirements increase administrative responsibilities and potential penalties for mislabeling, especially for imported products. The regulatory environment creates operational advantages for established processors with dedicated quality assurance resources, while smaller operators face potential barriers to market entry. These regulations, however, support product quality and authenticity verification, contributing to industry-wide value enhancement.

Volatile raw material supply and price fluctuations

Supply chain disruptions and seasonal variations create persistent cost pressures, affecting profitability and market stability in the scallop industry. According to NOAA Fisheries, regulatory measures, including the Northern Gulf of Maine closure until April 2026, have reduced market supply volumes and increased price volatility. The ban on Japanese seafood imports by China has significantly altered global trade patterns, leading to supply chain instability. As Japan's scallop exports to China decreased to zero in 2024, producers have redirected their supply to other markets, including the United States and Vietnam, resulting in pricing pressures in these regions. The Seafood News reports that the Atlantic sea scallop market faces ongoing supply constraints, characterized by reduced landings and a shortage of larger scallops. These factors maintain historically high price levels, affecting market demand. Processors face challenges in maintaining profit margins due to fluctuating raw material costs and fixed operational expenses. The perishable nature of scallops further complicates the situation by limiting inventory management options and increasing vulnerability to short-term price fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species: Sea Scallops Dominate Through Size and Culinary Versatility

In 2025, sea scallops dominated the market with a 57.22% share, thanks to their larger size, better meat yield, and well-established Atlantic supply chains. Meanwhile, diver scallops are the fastest-growing segment, boasting a 6.15% CAGR through 2031, thanks to their premium positioning and sustainable harvesting methods. The commercial viability and processing efficiency of sea scallops are evident, with the Atlantic sea scallop fishery raking in USD 478 million from 31.6 million pounds of landings in 2022, as reported by NOAA Fisheries. Bay scallops, valued for their sweet flavor and seasonal availability, hold a niche position. They fetch premium prices during peak harvests, especially in northeastern U.S. markets. According to the Interstate Shellfish Sanitation Conference, bay scallops are celebrated for their delicate taste, while sea scallops stand out as the largest and most commercially available option.

Diver scallops are witnessing rapid growth, thanks to their hand-harvested nature and minimal environmental impact. This appeals to sustainability-minded consumers and upscale restaurants seeking unique menu options. Geographic production patterns influence species segmentation: sea scallops thrive in North American waters, while diver scallops are sourced from select coastal regions with ideal diving conditions. Processing methods differ by species: sea scallops benefit from mechanized shucking, whereas diver scallops undergo labor-intensive handling, reinforcing their premium status. Regulatory frameworks also shape the species mix, with MSC certification programs endorsing sustainable harvesting across various scallop types.

By Form: Frozen Products Lead Through Extended Availability

In 2025, frozen scallops dominated the market, capturing a 45.96% share, thanks to their extended shelf life and year-round availability. Meanwhile, dried scallops, buoyed by Asian culinary traditions and a premium stance in specialty markets, emerge as the fastest-growing segment, boasting a 6.63% CAGR. Technological strides in Individual Quick Freezing (IQF) and cryogenic processing bolster the frozen segment, ensuring product quality and enabling global distribution beyond seasonal harvests. Lund's Fisheries' USD 2 million investment in advanced tunnel freezer technology underscores the confidence in the frozen segment's capabilities and demand, as highlighted by National Fisherman.

Fresh-chilled products command a premium in local and regional arenas, where swift distribution ensures top-notch quality, catering especially to upscale restaurants and niche retailers. The segmentation by form underscores varied value propositions: frozen products excel in operational ease and cost-effectiveness, while fresh offerings, with their enhanced culinary attributes, fetch higher margins. Dried scallops carve out a niche, holding deep cultural resonance in Asian cuisines, serving dual roles as core ingredients and flavor enhancers in age-old recipes. Recent innovations in drying technologies for aquatic products highlight the importance of environmental control in maintaining sensory and nutritional quality. The uptick in dried products reflects the growing Asian diaspora and the West's increasing adoption of Asian culinary methods, often featuring dried seafood ingredients.

By End User: Food Service Drives Premium Market Development

In 2025, the food service segment captured a dominant 54.25% market share, leveraging premium pricing and menu differentiation to elevate dry-packed scallops as signature ingredients. Meanwhile, the household/retail segment emerged as the fastest-growing, boasting a 5.61% CAGR, driven by rising consumer sophistication and a surge in home cooking. The food service's stronghold underscores its ability to command premium prices for high-quality ingredients. Restaurants are harnessing the superior searing and flavor profiles of dry-packed scallops to craft unique menu items. Highlighting the industry's commitment, Maine's culinary exchange programs, backed by NOAA Sea Grant, are actively promoting both farmed and wild scallops through chef education and tech transfer, as noted by the World Aquaculture Society.

Food processing and industrial sectors consistently demand reliable quality and supply. They often turn to frozen forms, which are well-suited for large-scale production and offer extended storage. The household retail segment is experiencing a surge, driven by heightened consumer awareness of premium seafood and growing confidence in home cooking, which is being bolstered by online resources and cooking classes. High Liner Foods, in a Q2 2025 report, credited improved retail performance to a later Lent timing and robust retail sales, signaling a positive consumer market trend, as highlighted by Seafood News. The segmentation nuances are evident: while food service leans towards bulk packaging, retail emphasizes consumer-friendly portions and transparent labeling, detailing product attributes and preparation guidance.

Geography Analysis

North America held a 33.10% market share in 2025, driven by established Atlantic sea scallop fisheries, robust processing infrastructure, and comprehensive regulatory frameworks. The region's integrated supply chains connect harvesting operations with processing facilities and distribution networks, serving both domestic and export markets efficiently. NOAA's management of the Atlantic sea scallop fishery includes quota allocations of 18 million pounds for 2025 and area management through Framework 39. In Canada, industry consolidation continues, as evidenced by Ocean Choice International's USD 200 million scallop quota sale to three companies in Nova Scotia. However, seasonal closures and quota limitations create supply constraints, affecting pricing and market stability.

Europe's mature market is characterized by established trade relationships and stringent sustainability requirements. The European Union's imports of live, fresh, or chilled scallops reached USD 79.4 million in 2021, with the United Kingdom as the primary supplier at USD 75.2 million, followed by the United States and Norway. MSC certification requirements influence market dynamics, benefiting certified suppliers. EU scallop production reached 45,985 tonnes in 2021, with France contributing 91% of regional production. Post-Brexit, the UK maintains its position as a significant supplier, despite new regulatory requirements affecting market access.

Asia-Pacific demonstrates the highest growth rate at 5.30% CAGR through 2031, supported by increased seafood consumption and expanding middle-class populations. Regional trade patterns shifted after China's ban on Japanese seafood imports, with Japan redirecting exports to markets including the United States and Vietnam, where Japanese scallop imports increased by 771% in 2024. The region focuses on aquaculture development, with Japan working to reduce dependence on Chinese processing. Infrastructure limitations and quality control requirements remain key challenges for accessing premium market segments. South America and Middle East & Africa present growth opportunities despite current infrastructure limitations. In the Middle East, the UAE exported USD 12,160 worth of scallops in 2023, primarily to Saudi Arabia. Saudi Arabia's seafood market is expected to grow from USD 0.98 billion in 2024 to USD 1.23 billion by 2033, supported by Vision 2030 initiatives. Both regions require significant infrastructure investment and market development to expand their presence in premium scallop segments.

Regulatory Landscape

Dry-packaged scallops trade is shaped by overlapping food-safety, labeling, and import certification regimes that increase compliance requirements for processors and exporters. In the United States, FDA oversight focuses on the Fish and Fishery Products Hazards and Controls guidance and seafood market-name and labeling controls through the FDA Seafood List (updated on a semi-annual cycle). FSMA traceability recordkeeping also adds documentation obligations for seafood supply chains. Separately, NOAA Fisheries supports exporters with European Union certification requirements and guidance on the documentation needed for EU market access.

In Europe, official controls for bivalve molluscs are being updated through implementing acts that affect both production-area monitoring and import certificates. Commission Implementing Regulation (EU) 2026/1406 (26 June 2026) amends sanitary survey requirements for classifying and monitoring production and relaying areas for live bivalve molluscs under Regulation (EU) 2019/627, which affects upstream controls that determine product eligibility and documentation. Commission Implementing Regulation (EU) 2026/1305 (11 June 2026) amends Regulation (EU) 2020/1641 on official certificate requirements for imports of bivalve molluscs from the United States and includes a transitional period running until 3 December 2026, creating a defined deadline for US-origin consignments and their certifying and record systems.

Competitive Landscape

The dry-packed scallops industry exhibits moderate fragmentation. Leading players, including Sea Watch International and Pacific Seafood Group, utilize vertical integration, covering everything from harvesting quotas to processing plants and nationwide distribution. These companies invest in cryogenic tunnel freezers and automated grading lines, ensuring texture preservation and reduced labor costs, all while securing long-term contracts with food service providers. Meanwhile, medium-sized firms carve out niches by emphasizing regional specialties, often sourcing diver scallops and collaborating with chefs to weave in stories of provenance.

Strategic investments highlight a strong belief in technology-driven scaling. Lund’s Fisheries, for instance, enhanced its hourly capacity by investing USD 2 million in a tunnel freezer, leading to greater throughput efficiency and energy savings. In 2024, Northern Wind expanded its horizons by acquiring a regional supplier, gaining access to MSC-certified raw materials and broadening its private-label offerings for retail chains. Clearwater Seafoods, under First Nations ownership, showcases the increasing involvement of Indigenous communities in managing quotas and making value-chain decisions, adding a socio-economic layer to the competitive landscape.

Innovation is steering towards convenience and sustainability. Aquamar has tapped into the trend with its ready-to-eat tender strips, catering to the meal-kit and snacking markets. Simultaneously, processors are experimenting with blockchain traceability to meet the stringent demands of institutional procurement audits. Noteworthy disruptors are emerging, such as aquaculture ventures in Maine utilizing ear-hanging gear for enhanced adductor yields, and Norwegian companies harnessing AI-driven underwater vision for selective harvesting. As processors vie for premium shelf space and menu placements, their success hinges on access to capital, compliance expertise, and robust marketing strategies.

Dry-Packaged Scallops Industry Leaders

Sea Watch International

Clearwater Seafoods

Pacific Seafood Group

High Liner Foods

Northern Wind

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are centered on compliance-ready, shelf-life-extending formats and packaging lines that help maintain dry-pack quality over longer distribution distances and under tighter audit requirements. Active and barrier packaging that manage in-pack moisture and inhibit bacterial growth, combined with automated inspection steps (X-ray, metal detection, and checkweighing) in co-packing operations, gives processors leverage with premium retail and institutional buyers that expect consistent specifications and documentation. This direction is reinforced by tightening documentation and certification regimes, including FSMA traceability requirements in the United States and updated EU import certificate rules with a transitional window to 3 December 2026 for US bivalve mollusc consignments.

Value-added processing is another growth route where dry-pack attributes can be carried into new consumption occasions, including scallop-based snacks and convenience items. Equipment and process innovation, such as automated handling and low-temperature or vacuum processing approaches, are aimed at preserving texture and limiting quality loss during storage. On the supply side, constraint conditions in core wild fisheries, including quota-managed landings (NOAA Fisheries projected 18 million pounds of US Atlantic sea scallop landings for 2025) and area-based restrictions (including the Northern Gulf of Maine closure until April 2026), make yield management, cold-chain control, and vertical integration more relevant for stabilizing input quality and supporting premium pricing across food service and retail channels.

Recent Industry Developments

- June 2026: Clearwater Seafoods completed the sale of its Argentine subsidiary Glaciar Pesquera, including scallop fishing operations, to Grupo Newsan. The divestment reshapes Clearwater Seafoods' geographic footprint and reallocates scallop supply and processing capabilities away from Argentina toward its core operating focus.

- May 2026: Premium Brands Holdings noted the completion of the transaction involving Clearwater Seafoods. The ownership structure and integration under a larger seafood platform strengthens the ability to coordinate procurement, processing, and distribution across cold-chain seafood categories relevant to dry-packed scallops.

- December 2024: Northern Wind completed the acquisition of a scallop supplier to expand its product offerings and secure access to raw material aligned with premium sourcing needs. The move supported broader private-label and retail-facing programs by tightening control over supply and provenance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from dry-packaged scallops sold through retail and foodservice channels, where the product is packaged for sale and positioned as a dry-packed scallop offering.

Scope exclusions: We exclude wet-packed or chemically treated scallops, as well as fresh and frozen scallops that are not marketed and sold as dry-packaged products.

Segmentation Overview

- By Species

- Sea Scallops

- Bay Scallops

- Diver Scallops

- By Form

- Fresh-Chilled

- Frozen

- Dried

- By End User

- Food-service (HoReCa)

- Food Processing/Industrial

- Household/ Retail

- By Geography

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Spain

- Poland

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Australia

- Singapore

- Thailand

- Rest of Asia-Pacific

- South America

- Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map supply availability, trade signals, and price movement that impact dry-packaged scallops, and then translate those signals into sizing inputs. Public datasets, such as UN Comtrade trade statistics, FAO fisheries and aquaculture data, NOAA fisheries landings summaries, and national customs or statistical offices in large importing countries, helped us understand import dependency and consumption direction.

We also reviewed company filings and investor presentations from seafood processors and distributors, along with foodservice and retail category articles from reputable press and association websites. For cross-checking, we selectively used paid subscriptions for company financials and intelligence, shipment-level import and export records, and patent databases covering seafood processing and packaging, where it helped confirm processing trends and shelf-stable product claims. The sources listed above are illustrative only, and many other public and paid references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on validating what portion of scallop trade and consumption is actually sold as dry-packaged, and how pricing differs by pack style, grade, and route to market. We spoke with processors, importers, distributors, and category managers, and then used those inputs to confirm conversion factors, typical price ranges, and channel splits across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 42% |

| Mid tier: 54% | Functional/Unit leaders: 28% | EMEA: 32% |

| Smaller Players: 14% | Managers: 59% | Americas: 26% |

Market-Sizing & Forecasting

The market was sized using a top-down build that starts from scallop supply and trade signals, and then reconstructs the addressable demand pool for dry-packaged formats by applying share and price assumptions. To keep the totals realistic, we corroborated results with selective bottom-up checks, such as sampled average selling price (ASP) by pack format multiplied by estimated volume moving through key channels, and then adjusted where gaps appeared.

Inputs used in the model included, in an illustrative way, scallop import volumes and values in major consuming countries, domestic landing and aquaculture output trends, dry-pack price premiums versus comparable formats, the share of sales moving through retail versus foodservice, and packaging and processing changes that influence shelf life and handling. When a variable was not consistently available for a country, a proxy was used from a close peer market and then refined using interview feedback.

For forecasting, we relied on scenario analysis anchored to expected supply conditions, trade normalization, and consumption patterns, and then stress-tested it against price sensitivity shared by participants. Growth paths were kept consistent with observed seasonality and procurement cycles, which helped avoid unrealistic jumps in volume or ASP over the forecast period.

Data Validation & Update Cycle

Validation was done through multiple checks so that one single source did not decide the final number. We compared model outputs against independent signals, such as import value trends, reported category growth in key markets, and expected production and harvest movements, and then reviewed any abnormal swings before sign-off.

Where the first pass showed large variances by region or channel, assumptions were revisited and respondents were re-contacted to confirm whether a real market change had occurred or whether a definition mismatch was driving the gap. The report is refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the most current view available at the time of release.

Mordor Intelligence's Dry Packaged Scallops Market Size Compared With Other Published Estimates

Published numbers for dry-packaged scallops do not always line up because the product boundary is easy to stretch into broader scallop formats, and because some studies mix different time horizons and pricing assumptions. Differences also come from how researchers treat trade values, channel markups, and whether they apply conservative or aggressive growth paths when supply swings.

The table shows a wide spread that mainly tracks scope choices and how pricing is handled. In Mordor Intelligence's model, the value is counted only for scallops sold as dry-packaged offerings, rather than folding in adjacent wet-packed or general dried scallop categories. Other gaps often appear when a study uses a longer forecast window with faster assumed ASP progression, or when it relies on trade-value totals without separating re-exports, processing margins, and retail markups in a consistent way.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.76 B (2025) | |

| Global Publisher A | USD 2.51 B (2025) | Uses an earlier base-year structure and may apply a narrower channel treatment that undercounts premium dry-pack positioning, which can reduce the value captured in the same year. |

| Category Study B | USD 0.31 B (2023) | Focuses on dried scallops as a product category with end-use splits, which is narrower than dry-packaged scallops sold across modern retail and foodservice, and it also uses a different base year. |

Taken together, the comparison points to two practical drivers of differences, which are what is included as dry-packaged and how prices and channels are translated into revenue. By keeping the scope clear and tying assumptions back to trade signals, supply context, and interview-confirmed price ranges, the estimate stays traceable to repeatable steps rather than one-off assumptions.

Key Questions Answered in the Report

What is the current value of the dry-packed scallops market?

The dry-packed scallops market is valued at USD 2.87 billion in 2026 and is forecast to reach USD 3.51 billion by 2031.

Which region leads global consumption?

North America leads, supplying 33.10% of global sales due to advanced processing and strong regulatory frameworks.

Which species dominates supply?

Sea scallops dominate with 57.22% market share thanks to high meat yield and established Atlantic fisheries.

Why are dry-packed scallops preferred in restaurants?

Chefs favor them for chemical-free processing that allows superior caramelization and consistent flavor profiles.

How is sustainability addressed in the sector?

MSC certification, quota management, and traceability programs ensure responsible harvesting and bolster consumer trust.

Page last updated on: