United States Creatine Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

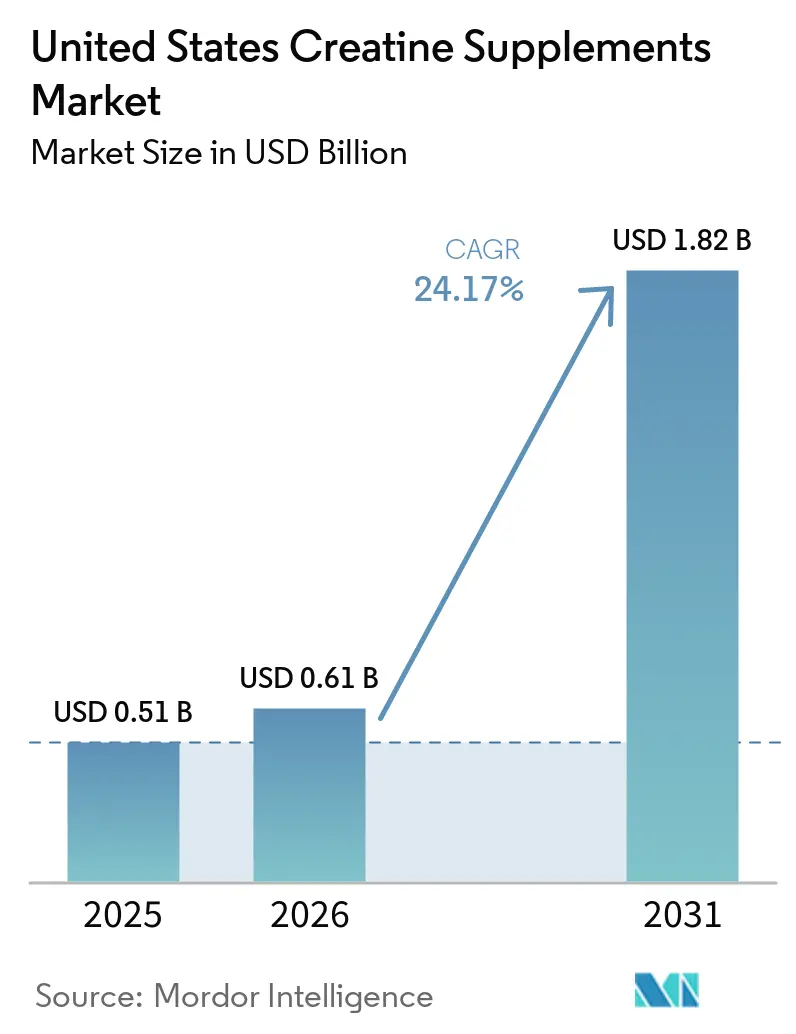

| Base Year Market Size (2025) | USD 0.51 Billion |

| Market Size (2026) | USD 0.61 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 24.17% CAGR |

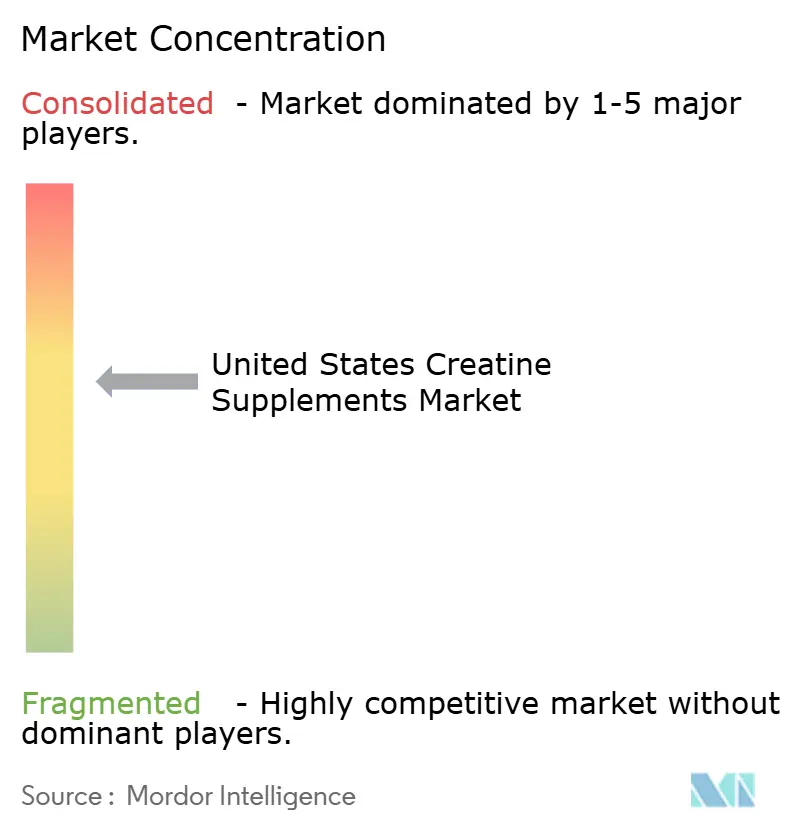

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Creatine Supplements Market Analysis by Mordor Intelligence

The United States creatine supplements market size was valued at USD 0.51 billion in 2025 and estimated to grow from USD 0.61 billion in 2026 to reach USD 1.82 billion by 2031, at a CAGR of 24.2% during the forecast period 2026 to 2031. The market is expanding as creatine moves beyond its traditional athlete-focused positioning and gains adoption among regular gym users, active older adults, and consumers seeking convenient daily performance support. Stronger clinical validation related to lean mass, strength, and cognition is also broadening the product’s relevance in healthy aging and practitioner-led wellness settings. Format innovation is attracting first-time users who prefer gummies, chewables, capsules, or ready-to-consume options over bulk powder, although powder continues to account for a major share of category volume. Search-led purchasing behavior, direct online comparison, and rising demand for clean labeling, verified purity, and consistent dosing are also shaping the market. Competitive opportunities remain attractive; however, price pressure from commodity products, quality concerns in novel formats, and tighter scrutiny of health claims continue to raise execution standards across the United States creatine supplements market.

Key Report Takeaways

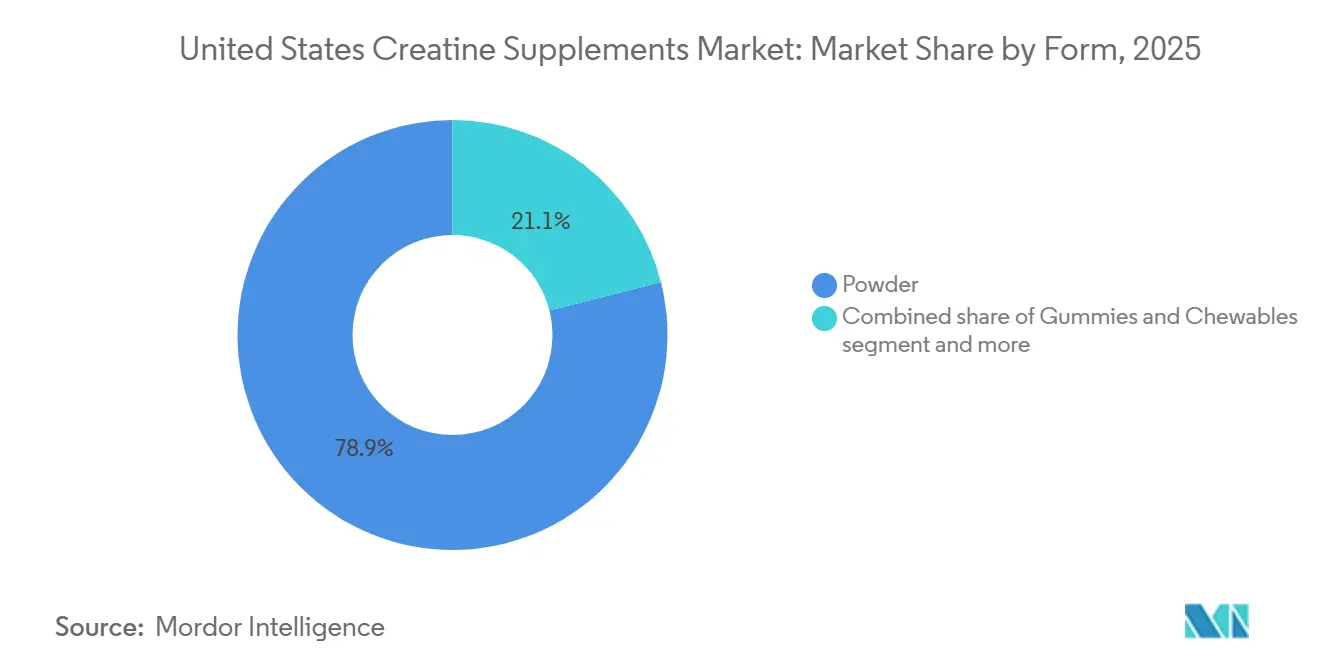

- By form, powder held 78.94% of revenue in 2025, while gummies and chewables are projected to record the fastest growth at 26.96% through 2031.

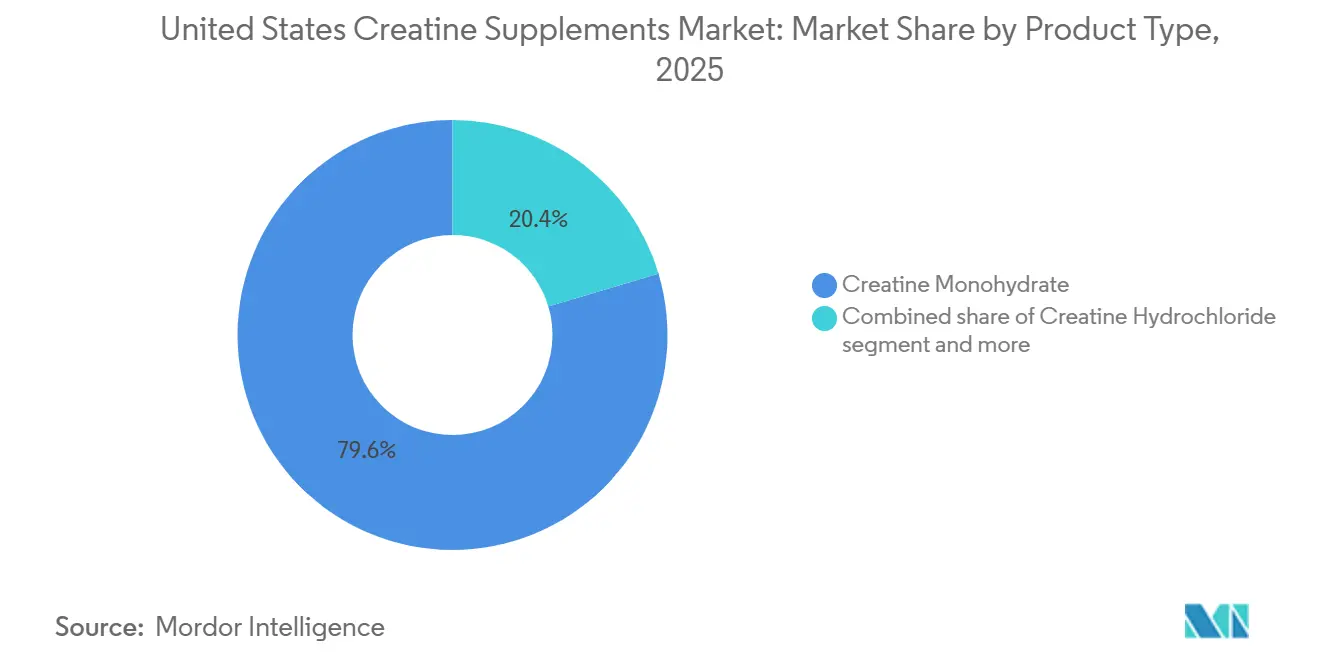

- By product type, creatine monohydrate accounted for 79.62% of revenue in 2025, while creatine hydrochloride is forecast to expand at the highest CAGR of 25.01% through 2031.

- By distribution channel, online retail captured 52.13% of revenue in 2025 and is also the fastest-growing channel with a projected CAGR of 26.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Creatine Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Fitness and Strength Training Demand | +6.2% | National, with the highest density in Sun Belt and Pacific Coast metros | Short term (≤ 2 years) |

| Expanding Sports Nutrition Consumer Base | +4.8% | National, concentrated in urban and suburban markets | Medium term (2–4 years) |

| E-Commerce and Direct-to-Consumer Channels | +4.5% | National, with outsized gains in digitally connected Millennial and Gen Z markets | Short term (≤ 2 years) |

| Third-Party Testing and Labeling Transparency | +2.1% | National, with a premium skew in the Northeast and West Coast markets | Medium term (2–4 years) |

| Creatine Use in Active Aging Population | +3.0% | National, with early gains in retirement-concentration states (Florida, Arizona, California) | Long term (≥ 4 years) |

| Single-Serve, Gummy, and Novel Delivery Formats | +2.4% | National, with Gen Z and female consumer crossover concentrated in metro areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising fitness and strength training demand

The Health & Fitness Association (HFA) expects a record 81 million Americans to hold a fitness facility membership in 2025, representing a 5.2% year-over-year increase and the highest penetration in US history. Gen Z adults (18–24) are expected to record the highest membership rate at 35.5%[1]Source: Health & Fitness Association, “Title Not Provided In The Supplied Draft,” Health & Fitness Association, healthandfitness.org. According to the HFA, free weight usage, the equipment category most directly linked to creatine’s performance rationale, has grown faster than any other equipment segment since 2021. This trend is more consequential than aggregate membership figures suggest, as repeat creatine purchases closely correlate with sustained resistance training, creating a stickier revenue base than intermittent sports-seasonal demand. A secondary mechanism worth tracking is the gym floor’s role as a recommendation channel. HFA data indicate that the practitioner channel, which includes gyms and health clubs, is expected to account for 9.3% of the United States supplement sales in 2025, up from approximately 4% in 2021. This increase illustrates how the in-facility experience continues to influence purchasing decisions. The Sports & Fitness Industry Association (SFIA) also confirmed that 247.1 million Americans participated in at least one sport or fitness activity in 2024, representing 80% of the population and creating the broadest active consumer base ever recorded[2]Source: Sports & Fitness Industry Association, “Title Not Provided In The Supplied Draft,” Sports & Fitness Industry Association, sfia.org.

Expanding sports nutrition consumer base beyond athletes

In 2025, lifestyle users, women, older adults, and recreational exercisers are expected to form the fastest-growing cohort in sports nutrition, rather than competitive athletes. This demographic shift is structurally more durable than any single product trend. According to the Health & Fitness Association, the Healthy Aging focus area within the United States supplements is projected to grow by 14.3% in 2025, outpacing every other health orientation. Sports nutrition is also expected to grow by 8% and displace general health as the largest wellness focus segment. Clinical evidence linking creatine to cognitive function, sarcopenia mitigation, and bone density has repositioned the ingredient scientifically, enabling brands to target multiple consumer archetypes without changing formulations and reducing the product’s exposure to fitness trend cycles. A 2025 narrative review indicates that creatine supplementation, when combined with exercise, improves muscle strength, lean body mass, functional capacity, and cognitive outcomes in older adults, particularly memory, processing speed, and executive function. Health practitioner networks continue to communicate this evidence base, steadily unlocking a consumer segment that has historically remained outside sports nutrition revenue models.

E-commerce and direct-to-consumer channel acceleration

E-commerce is expected to account for a majority share of the United States supplement sales in 2025 and become the leading distribution channel by 2028, structurally favoring creatine’s evidence-driven, search-first purchase journey. TikTok Shop is forecast to post 71% year-over-year growth in supplement sales for the period ending January 2026, generating approximately USD 1 billion in supplement transactions and representing 3% of total United States supplement sales. This channel disproportionately benefits creatine’s highly visual, socially validated use case. Moreover, the supplement category generates approximately USD 20 billion in Amazon sales annually, growing by roughly 21% year-over-year, compared to approximately 6% in measured retail. This velocity gap rewards brands that invest in the digital shelf. A less-discussed implication is that DTC platforms support subscription model development: approximately 1 in 4 regular supplement users now receive at least one product through a monthly subscription, improving predictability and reducing category exit rates.

Creatine use in active aging population

Clinical evidence supporting creatine monohydrate use among older adults has expanded enough to serve as a structurally independent demand driver, separate from traditional sports nutrition tailwinds. A 2025 pilot trial published in Alzheimer's & Dementia found that 20 grams per day of creatine monohydrate increased total brain creatine by 11% (p < 0.001) and improved global and fluid cognition in 20 patients with Alzheimer's disease over eight weeks. A concurrent Springer Nature study confirmed that creatine supplementation combined with resistance training reduced bone resorption markers by 27%, compared with a 13% increase in the placebo group, a finding with direct implications for the USD multi-billion osteoporosis management market. Notably, a majority of the United States adults aged 65 and older consumed less than 0.95 grams per day of dietary creatine in 2025, well below maintenance thresholds, creating a measurable and addressable supplementation deficit. A 26-week clinical trial registered at ClinicalTrials.gov is evaluating creatine and resistance training in adults with mild cognitive impairment, suggesting that practitioner-recommended purchases from this cohort could increase as the evidence base strengthens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Misinformation and Consumer Concerns | -1.4% | National, highest in female and 45+ demographics | Short term (≤ 2 years) |

| Regulatory Scrutiny on Claims | -1.1% | National, FTC, and FDA jurisdiction across all channels | Medium term (2–4 years) |

| Price Compression from Private Label | -1.7% | National, strongest in mass-market and e-commerce channels | Short term (≤ 2 years) |

| Ingredient Authenticity and Adulteration | -1.2% | National, concentrated in gummy and novel format segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Safety misinformation and consumer concerns

Despite creatine monohydrate’s FDA GRAS (Generally Recognized as Safe) designation and a 2025 safety analysis covering 32 studies and 1,232 participants, which found no significant differences in side effects among older adults, persistent social media misinformation about kidney stress, hair loss, and illegal performance enhancement continues to suppress first-time buyer conversion[3]Source: U.S. Food and Drug Administration, “Title Not Provided In The Supplied Draft,” U.S. Food and Drug Administration, fda.gov. This challenge remains asymmetric, as negative claims spread faster than corrections on short-form video platforms, creating latent churn risk among female and older consumer segments, the demographics most critical to the market’s next growth phase. Third-party certification programs, such as NSF Certified for Sport, recognized by USADA and endorsed by major professional leagues, including the NFL and NBA, and Informed Sport, which tests every batch against more than 285 banned substances, provide credibility bridges for hesitant buyers. These programs improve purchase intent, but uneven certification awareness across demographics and the compliance investment required limit adoption among smaller, price-competitive brands.

Ingredient authenticity and adulteration in novel formats

Gummies and chewables, the fastest-growing format, face the most significant quality verification challenges, creating reputational exposure that could affect the broader creatine supplements category if product failures gain mainstream attention. Independent laboratory testing by SuppCo in 2025 found that 4 of the 6 top-selling creatine gummies on Amazon failed identity and potency standards, with 2 products containing no detectable creatine. Even products that passed showed measurable creatinine degradation, a quality marker of inadequate formulation stability. A 2025 peer-reviewed study using HPLC spectroscopy on 149 commercial creatine samples identified 32 adulterated products, confirming that the quality gap extends beyond gummies. Under DSHEA (21 CFR Part 111), manufacturers must verify ingredient identity and test for impurities, including dicyandiamide (DCD), dihydrotriazine (DHT), and creatinine. However, enforcement remains post-market and reactive rather than pre-sale. Brands that secure and communicate batch-level third-party verification through NSF or USP certification can defend a price premium in this environment, while the systemic quality gap continues to weaken category trust among cautious first-time buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Commands the Market While Novel Formats Redefine Entry Points

Creatine supplements in powder form are expected to hold a 78.94% share in 2025, reflecting decades of practitioner and consumer familiarity with bulk powder dosing conventions. However, this dominance masks the structural pressure building beneath the category. Gummies and chewables are projected to be the fastest-growing form, with a CAGR of 26.96% from 2026 to 2031. Growth is driven by the format’s ability to attract non-traditional buyers, including women, casual fitness participants, and older adults, who often avoid powders due to mixing requirements and chalky texture. Capsules and tablets remain the preferred format for clinical and practitioner-recommended use, while liquid creatine continues to face stability challenges, as creatine degrades into creatinine in aqueous solutions. TSI Group’s expected 2025 launch of OptiCreatine, a processing technology for stable gummy, chewable, effervescent, and RTD formulations, addresses this constraint and is likely to drive manufacturer investment across liquid and gummy categories through the forecast period.

The key strategic implication of this format shift is that powder’s dominance represents both a volume floor and a margin ceiling. Glanbia’s development of encapsulated creatine monohydrate, which offers superior dispersibility in water and stability through ultra-high-temperature processing and enables gummy and gel applications, indicates that market leaders no longer view format innovation as peripheral. The gummy format failure rate documented in independent testing in 2025 is expected to create a quality bifurcation. Brands with rigorous manufacturing protocols and certified supply chains are likely to command premium pricing, while lower-quality entrants may face regulatory and reputational risks. The “Other Forms” category, including RTD beverages, protein bars, and functional food integration, is positioned as the next frontier. Jimmybar! Functional Foods is expected to introduce a creatine protein bar with 5 grams of creatine and 20 grams of protein in late 2025, while KA-EX plans to launch a ready-to-drink Creatine EAA+ Booster in the United States in 2026.

By Product Type: Monohydrate Anchors Trust While Hydrochloride Grows on Differentiation

Product type segmentation shows a market anchored by scientific consensus. Creatine monohydrate is expected to hold a 79.62% share in 2025, supported by more than three decades of peer-reviewed validation as the most studied and cost-effective form of creatine supplementation. No competing form has demonstrated superiority in clinical trials. Creatine hydrochloride (HCl) is projected to be the fastest-growing product type, with a CAGR of 25.01% from 2026 to 2031. It is gaining traction due to marketing claims of enhanced solubility and reduced bloating at lower doses, although peer-reviewed literature has not established its superiority over monohydrate in clinical outcomes. Buffered creatine, commonly marketed as Kre-Alkalyn, holds a niche premium position based on claims of greater stability and reduced conversion to creatinine at physiological pH. It appeals to users who experienced gastrointestinal discomfort with monohydrate at loading doses. Other product types, including creatine ethyl ester, creatine nitrate, and combination stacks, serve the formulation differentiation segment, where novelty and superior bioavailability claims provide short-term marketing advantages.

A supply chain dynamic is reshaping competitive conditions upstream of the product type segmentation. Alzchem Group, whose Creapure brand is the most widely recognized high-purity creatine monohydrate ingredient globally, reported EBITDA growth from EUR 62 million in 2021 to EUR 116.5 million in 2025. The company is investing EUR 120 million (approximately USD 133 million) to build a new production facility in Germany, expected to come online in late 2027. Alzchem Group confirmed that creatine demand tripled over two years, prompting it to prioritize existing customers while delaying new business. This constraint gives Creapure-certified brands a procurement advantage during the current demand surge. In parallel, new precision-grade ingredient suppliers, including Jenerise (Cr. 01 with a 99.96% assay) and Qura Creatine BV, entered the market in 2026 to address quality and supply concentration risks, as an estimated 84% of the global creatine supply originates from China.

By Distribution Channel: Online Retail Leads and Reshapes the Competitive Terrain

Online retail is expected to account for 52.13% of US creatine supplement sales in 2025 and remain the fastest-growing channel, with a projected CAGR of 26.51% from 2026 to 2031. This dual dominance reflects the category’s shift from gym-floor recommendations to digital discovery. The concentration extends beyond channel preference: e-commerce platforms, particularly Amazon, generate real-time consumer data that brands can use for algorithm optimization, subscription model conversion, and competitive pricing responses in ways physical retail cannot replicate. TikTok Shop is projected to represent approximately 3% of total United States supplement sales for the period ending January 2026, generating an estimated USD 1 billion in supplement revenue with 71% year-over-year growth. This trend shows how social commerce now functions as a parallel discovery-to-purchase funnel. Create Wellness, with 100 million gummies sold to date primarily through DTC and Amazon before its planned October 2025 Target launch, demonstrates how digitally native creatine brands can achieve significant sales velocity before entering mass retail.

Other distribution channels indicate a market undergoing structural evolution. Specialty stores continue to serve performance-focused buyers willing to pay premium prices. This channel remains stable, although growth is slow as buyers increasingly shift toward omnichannel purchasing. Pharmacy and drug stores are becoming a higher-stakes channel for creatine as clinical health claims gain mainstream traction and aging consumers bring the category into wellness retail alongside vitamins and minerals. Hypermarkets and supermarkets serve mainstream and value-seeking buyers. Private-label penetration is highest in this channel, as retailer brands priced 30–40% below branded products compete directly in commodity formats. Online retail’s trajectory toward eventual channel leadership aligns with broader United States supplement distribution trends. The mass market’s share is expected to nearly double from 14% in 2020 to 27.1% in 2025, with e-commerce close behind, confirming that supplement purchasing has shifted decisively away from specialty-only channels.

Geography Analysis

The United States creatine supplements market operates as a single national market, but regional demand patterns continue to influence adoption rates, channel mix, and acceptance of premium products. The West Coast, led by California, remains an important testing ground, as it combines high gym density, health-oriented consumer behavior, and strong openness to certified or premium supplement formats. The Northeast also plays a significant role, as the New York City, Boston, and Philadelphia corridors support strong direct-to-consumer adoption and a higher willingness to pay for clinical-grade quality cues. These two regions help drive early product discovery and trial, which can later scale into broader national distribution.

The Sun Belt states, especially Texas, Florida, Georgia, and Arizona, represent a strong growth zone within the United States creatine supplements market, supported by population inflows, expanding fitness infrastructure, and year-round outdoor activity. This demand base is especially relevant for creatine, as repeat use often aligns with consistent training habits rather than short seasonal participation. According to the Health and Fitness Association, adults aged 65 and older are expected to post the strongest year-over-year membership growth, at 8.6% in 2025, strengthening the case for aging-related demand in states with large retiree populations. Florida and Arizona stand out because they combine a high concentration of older residents with a growing wellness culture that can support both practitioner-guided and self-directed creatine use. The Midwest remains important as a value-driven volume market, where accessible price points, mass retail presence, and trust in established brands can matter more than novelty.

Regional differences also influence how brands should position themselves across the United States creatine supplements market. Premium certifications and science-led messaging are likely to resonate more in coastal urban markets, where consumers are more inclined to compare labels and seek practitioner or research validation. In the Sun Belt, convenient formats and broad retail availability can be especially effective, as the buyer base is expanding across both younger fitness users and older active adults. In the Midwest, a balanced offering that combines quality reassurance with practical pricing may provide the strongest route to scale within the United States creatine supplements market.

Competitive Landscape

The United States creatine supplements market is moderately fragmented, with established multi-brand companies competing with digital specialists, premium clinical brands, and newer convenience-led entrants. Glanbia Performance Nutrition stands out among the larger players. The company has stated that Optimum Nutrition holds the No. 1 creatine brand position in the United States and the United Kingdom. This scale matters because broad distribution, manufacturing depth, and long-standing brand recognition continue to influence purchasing decisions in a category where consumers often repurchase the same product over extended periods. At the same time, fragmentation remains high enough for smaller brands to gain share by offering a clearer value proposition around purity, transparency, or format relevance.

Strategic behavior across the United States creatine supplements market is dividing into distinct lanes. Legacy companies are using wide channel coverage, established shelf access, and recognizable product architecture to defend share across powder and mainstream formats. Transparent Labs and NutraBio Labs are competing through cleaner labels, formulation transparency, and premium positioning that support higher pricing in segments where trust is a key purchase driver. Thorne HealthTech has developed a more clinical route by emphasizing practitioner distribution and NSF-certified positioning, which helps the company bridge performance nutrition and broader health-focused supplementation. These strategies indicate that no single formula is winning the United States creatine supplements market, as buyers differ in whether they prioritize cost efficiency, certification, clinician trust, or convenience.

The clearest white space remains in women-focused positioning, cognition-oriented messaging that stays within substantiated evidence, and stable, ready-to-consume applications. Brands that can combine convenience with reliable quality should be better positioned than those that rely only on flavor or novelty. Private-label sellers continue to pressure the lower end of the category, particularly in commodity powder, forcing branded suppliers to sharpen either value or differentiation. Overall, the United States creatine supplements market is moving toward a more visible split between basic low-cost products and premium, science-backed offerings.

United States Creatine Supplements Industry Leaders

Glanbia PLC

Optimum Nutrition

MuscleTech

GNC Holdings, LLC

NutraBio Labs, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Elysium Health launched Creatine+, a longevity-focused creatine system combining creatine monohydrate with complementary compounds targeting strength, recovery, and cognition in aging adults. The launch marked Elysium's entry into the sports nutrition supplements segment, reflecting the category's mainstreaming into the broader longevity wellness market.

- May 2026: Alzchem Group announced an investment of EUR 120 million (approximately USD 133 million) to construct a new Creapure creatine production facility in Germany, scheduled to come online in late 2027. The investment was triggered by global creatine demand tripling over two years, a supply shortage that has led Alzchem to prioritize existing customers while turning away new orders.

- April 2026: Optimum Nutrition (Glanbia Performance Nutrition) expanded its US portfolio with Creatine Gummies in pineapple and blue raspberry flavors, delivering 5 grams of creatine monohydrate per 3-gummy serving. The product is available at select retailers nationwide and on OptimumNutrition.com, priced at USD 39.99 for 35 servings.

United States Creatine Supplements Market Report Scope

Creatine is a natural compound made from amino acids that supplies energy to your muscle cells. As a dietary supplement, it is used to boost athletic performance, increase muscle mass, and improve strength during short bursts of high-intensity exercise. The United States creatine supplements market is segmented by form, product type, and distribution channel. By form, the market is segmented into powder, liquid, capsules and tablets, gummies and chewables, and other forms. By product type, the market is segmented into creatine monohydrate, creatine hydrochloride, buffered creatine, and other types. By distribution channel, the market is segmented into hypermarkets and supermarkets, pharmacy and drug stores, specialty stores, online retail, and other channels. The Market Forecasts are Provided in Terms of Value (USD).

| Powder |

| Liquid |

| Capsules and Tablets |

| Gummies and Chewables |

| Other Forms |

| Creatine Monohydrate |

| Creatine Hydrochloride |

| Buffered Creatine |

| Other Product Types |

| Hypermarkets and Supermarkets |

| Pharmacy and Drug Stores |

| Specialty Stores |

| Online Retail |

| Other Distribution Channels |

| Form | Powder |

| Liquid | |

| Capsules and Tablets | |

| Gummies and Chewables | |

| Other Forms | |

| Product Type | Creatine Monohydrate |

| Creatine Hydrochloride | |

| Buffered Creatine | |

| Other Product Types | |

| Distribution Channel | Hypermarkets and Supermarkets |

| Pharmacy and Drug Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is driving demand for creatine supplements in the United States?

Demand is being supported by wider fitness participation, stronger clinical validation, and more convenient delivery formats. The category is projected to rise from USD 0.62 billion in 2026 to USD 1.82 billion by 2031 at a 24.17% CAGR.

Which product form leads sales today?

Powder remains the leading form with a 78.94% revenue share in 2025, mainly because it is familiar, cost-efficient, and widely accepted by repeat users.

Which form is growing the fastest?

Gummies and chewables are the fastest-growing form, with a projected 26.97% CAGR through 2031, because they reduce mixing effort and appeal to mainstream users.

Why does creatine monohydrate still dominate?

Creatine monohydrate held 79.62% of revenue in 2025 because it has the strongest research base, broad familiarity, and a long record of use in strength and body composition support.

Page last updated on: