Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

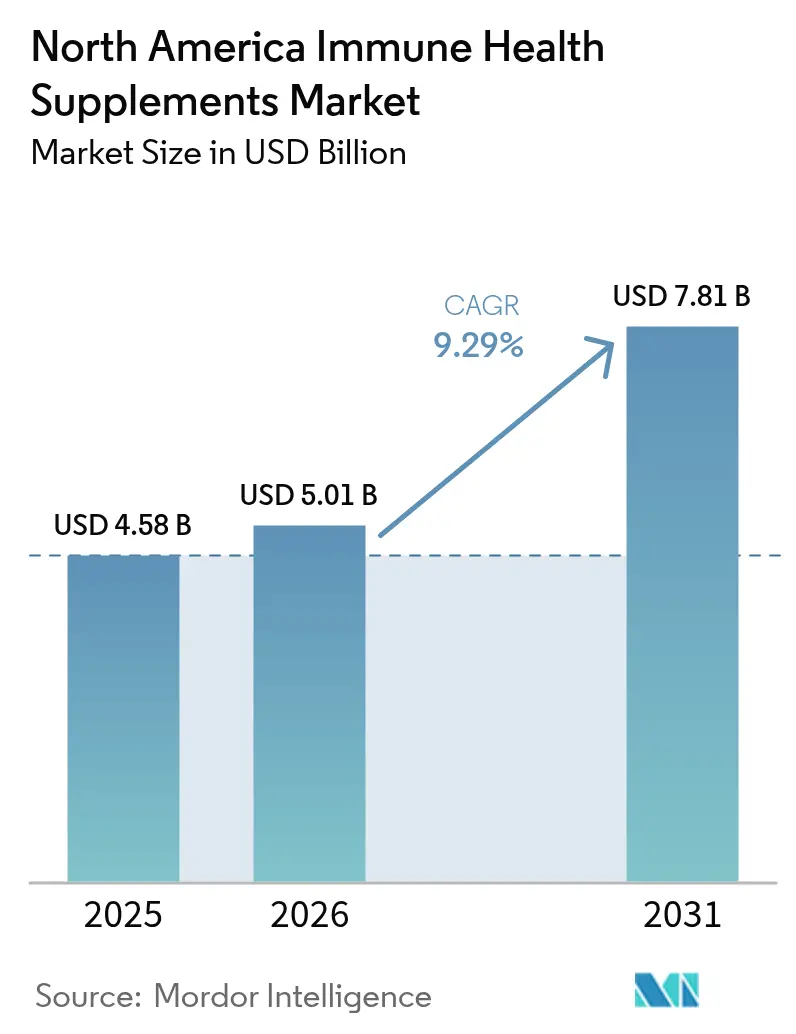

| Base Year Market Size (2025) | USD 4.58 Billion |

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 7.81 Billion |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

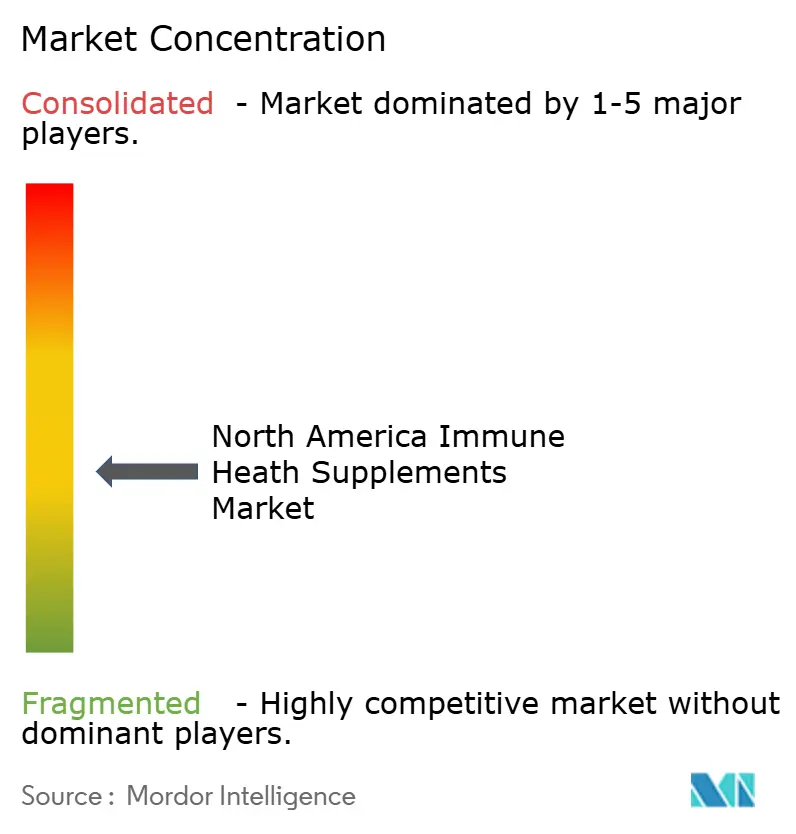

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Immune Health Supplements Market Analysis by Mordor Intelligence

The North America immune health supplements market size was valued at USD 4.58 billion in 2025 and estimated to grow from USD 5.01 billion in 2026 to reach USD 7.81 billion by 2031, at a CAGR of 9.29% during the forecast period (2026-2031). An emphasis on preventive healthcare and wellness heavily influenced North America's dietary supplements market. While vitamins and minerals dominated the product landscape, probiotics emerged as a rapidly growing segment, fueled by heightened consumer awareness of gut and immune health. Probiotics, in particular, gained traction due to their perceived benefits in improving digestion, enhancing immunity, and addressing specific health concerns like irritable bowel syndrome (IBS). Tablets held the top spot in product format, but gummies surged in popularity, thanks to their palatable taste and ease of consumption. Gummies appealed to a broader demographic, including children and adults, who preferred a more enjoyable alternative to traditional pills. Specialty and health stores remained the go-to sales channels, yet online platforms saw a swift rise, capitalizing on convenience and data-driven customization. The U.S. commanded the largest market share, but Mexico surfaced as a notable growth hotspot. Factors like an aging population, a rise in chronic conditions, and a demand for premium, bioavailable products bolstered the market's expansion.

Key Report Takeaways

- By product type, vitamins and minerals led with 31.48% the 2025 share; probiotics represent the fastest segment with a 9.42% CAGR to 2031.

- By form, tablets captured 30.55% of the 2025 share, while gummies are set to grow at an 10.44% CAGR over the forecast period.

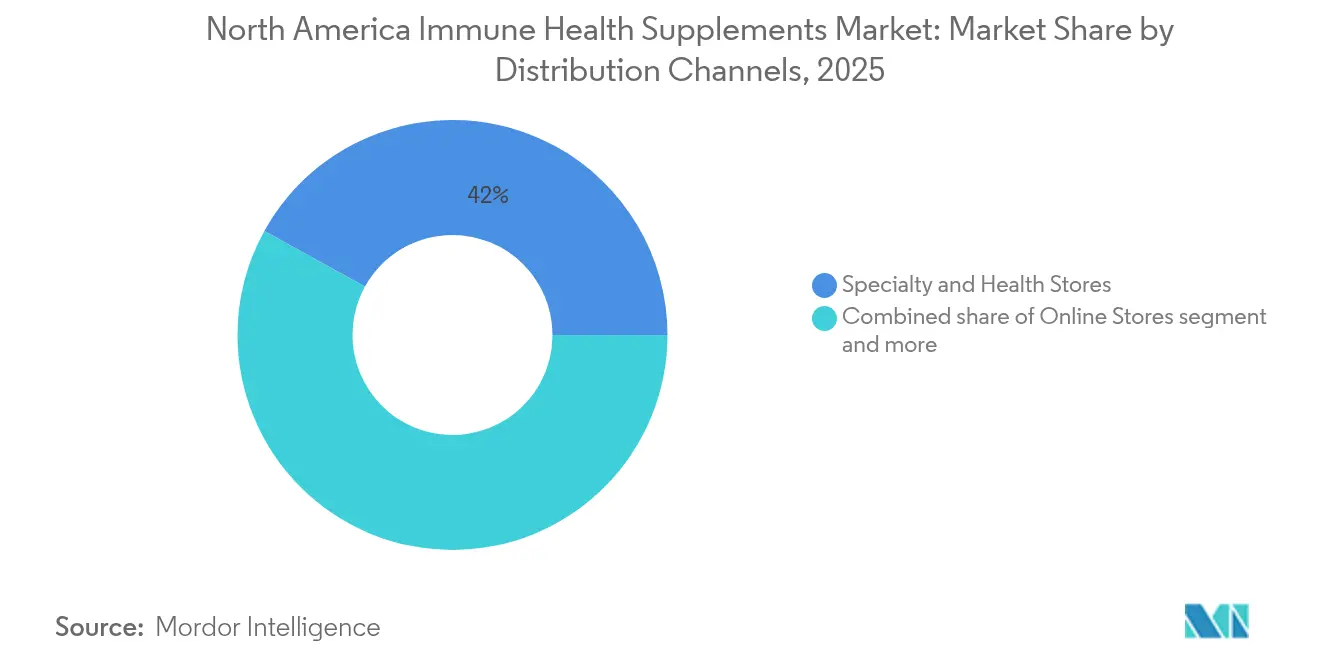

- By distribution channel, specialty and health stores held 41.96% of the 2025 share, whereas online retail is expected to rise at a 10.08% CAGR through 2031.

- By geography, the United States dominated with 78.65% of the 2025 share, whereas Mexico is projected to expand at an 10.86% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Immune Health Supplements Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preventive healthcare trends strengthen immune supplement market | +2.1% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Growing demand for vitamin D supplements among elderly for bone health | +1.8% | United States, Canada | Medium term (2-4 years) |

| Rising chronic disease rates | +1.5% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Increased use of E-commerce and DTC brands | +1.4% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Product innovation and use of functional ingredients | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Supportive regulatory landscape | +0.9% | United States, Canada, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preventive Healthcare Trends Strengthen Immune Supplement Market

The prevalence of chronic conditions among US adults reached 76.4% in 2023, according to the Centers for Disease Control and Prevention, reflecting an upward trend from previous years [1]Source: Centers for Disease Control and Prevention, “Multiple Chronic Conditions Among Adults,” cdc.gov. Among young adults aged 18-34, chronic condition rates increased from 52.5% to 59.5% between 2013-2023, leading this demographic to seek immune support products. The rising health consciousness has prompted consumers to take proactive measures in managing their well-being through dietary supplements and preventive healthcare solutions. With chronic diseases contributing USD 4.5 trillion to annual healthcare costs, consumers are increasingly adopting preventive health measures through supplements to potentially reduce their long-term medical expenses. This shift in health management approach is particularly notable among Millennials, who recognize the connection between gut health and overall wellness. Their growing awareness has accelerated the demand for multifunctional products that combine immune support with mental health and digestive benefits, reflecting a more holistic approach to health maintenance.

Growing Demand for Vitamin D Supplements Among Elderly for Bone Health

According to Health Canada data from 2024, approximately 19% of Canadians have insufficient vitamin D levels for optimal bone health. Vitamin D supplementation addresses bone integrity and immune function concerns in elderly populations, particularly those over 65 years of age [2]Source: Canada Gazette, "Marketing Authorization for Vitamin D in Yogurt and Kefir: SOR/2024 88, "gazette.gc.ca. The Food and Drug Administration reported in 2024 that over 10 million Americans have osteoporosis, with the highest prevalence among postmenopausal women. The demand for vitamin D supplements stems from multiple factors, including age-related bone density loss, hormonal changes during menopause, interactions with prescription medications, reduced outdoor activity, and dietary insufficiencies. Geographic variations in vitamin D deficiency rates across northern latitudes create significant market opportunities, particularly in Canada, where limited seasonal light exposure between October and March necessitates consistent year-round supplementation to maintain adequate vitamin D levels.

Rising Chronic Disease Rates

As consumers increasingly turn to immune health supplements alongside traditional medical treatments, the demand for these products remains strong, driven by the rising prevalence of chronic diseases. Data from the Centers for Disease Control and Prevention reveals a notable uptick: the percentage of young adults grappling with multiple chronic conditions surged from 21.8% in 2013 to 27.1% in 2023. This shift has broadened the market's focus, extending its reach beyond just elderly consumers. With chronic diseases placing a significant strain on healthcare systems, many consumers are proactively seeking preventive measures. Immune supplements, believed to mitigate infection risks and bolster overall health, have become a popular choice. These supplements are increasingly viewed as a complementary approach to managing health, particularly for individuals aiming to reduce dependency on conventional treatments. Furthermore, scientific studies linking immune function to effective chronic disease management bolster the perception that these supplements offer benefits that transcend mere nutrition.

Increased Use of E-Commerce and DTC Brands

Digital channels enable personalized marketing that addresses specific immune health concerns, allowing brands to build direct relationships with consumers and gather usage data for product development. The data collected helps companies understand consumer preferences, track purchasing patterns, and identify emerging trends in immune health products. E-commerce growth benefits smaller brands that can compete against established companies through digital marketing and subscription models, which provide consistent revenue. The digital marketplace also allows these brands to test new products and marketing strategies with minimal investment. However, the online environment increases regulatory oversight, as FDA warning letters frequently target companies making unsubstantiated immune health claims through digital platforms. This heightened scrutiny requires companies to carefully review their marketing materials and product claims. This regulatory focus creates advantages for companies with strong compliance programs and evidence-based marketing, as they can maintain consumer trust while avoiding potential penalties and reputational damage.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent labeling and health claims | -1.8% | United States, Canada, Mexico | Medium term (2-4 years) |

| High market competition | -1.2% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Risk of overconsumption and side effects | -0.9% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Availability of alternative supplements | -0.7% | United States, Canada, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Labeling and Health Claims

The complex regulatory landscape across North America creates significant compliance challenges that affect market growth and innovation in the immune supplements industry. The FDA's revised "healthy" claim requirements, implemented in December 2024, establish strict nutritional criteria that many immune supplements struggle to meet [3]Source: Food and Drug Administration, “Dietary Supplement Enforcement Report 2024,” fda.gov. The FDA's structure/function claim regulations require manufacturers to provide substantiation while avoiding disease-related terminology that could classify products as unapproved drugs. Health Canada's Natural Health Products Regulations further complicate pan-North American distribution by requiring Natural Product Numbers (NPNs), which demand comprehensive safety and efficacy documentation. Small companies without dedicated compliance departments face a disproportionate burden, which can restrict market diversity. In Mexico, COFEPRIS regulations mandate front-of-pack warning labels for products exceeding specific nutrient thresholds, which may influence consumer perceptions of immune supplements with higher vitamin content. These regulatory frameworks create market entry barriers that favor established companies with existing compliance systems while potentially limiting innovation from new market entrants.

High Market Competition

The immune health supplements market shows intense competition and limited pricing flexibility. The market includes multinational corporations, regional companies, and direct-to-consumer brands, each with distinct competitive strengths. Major retailers' private label products create additional price competition, especially in basic vitamin categories where product differentiation is minimal. Competition extends beyond traditional supplement manufacturers as immune health claims appear across various product categories, including functional foods. Companies with research capabilities gain competitive advantages through clinical studies that validate immune health benefits, though these studies increase development costs significantly. The rise in digital marketing expenses, particularly for direct-to-consumer brands building market presence, further impacts profitability as companies compete across multiple online platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vitamins and Minerals Lead, with Strong Growth in Probiotics

The vitamins and minerals segment dominated the North America immune health supplements market in 2025, accounting for 31.48% of revenue, driven by physician acceptance and comprehensive nutritional benefits. The probiotics segment is projected to grow at a 9.42% CAGR, gaining prominence as research advances in gut-immune system interactions. New probiotic strains, including Faecalibacterium duncaniae and Bacteroides dorei, demonstrate the industry's shift toward targeted immunity benefits. The market continues to evolve with the introduction of postbiotics and synbiotics in the "Others" category. Technical advances in microencapsulation technology improve probiotic survival rates in the digestive system, while liposomal delivery systems enhance vitamin absorption. The market supports premium pricing for products with strong scientific validation.

The market structure features strategic partnerships between ingredient suppliers, contract manufacturers, and finished-product companies. For example, Cargill's EpiCor postbiotic is now available in multiple product formats, including gummies, capsules, and powders, through various partnerships. Botanical extracts maintain a stable market presence among consumers seeking natural immunity solutions, while omega-3 products combine cardiovascular and immune health benefits. While probiotics demonstrate the highest growth rate, ongoing innovation across categories ensures vitamins remain fundamental to the North America immune health supplements market through 2030.

By Form: Gummies Revolutionize Supplement Delivery

Tablets hold a dominant 30.55% market share in 2025, driven by their cost-effectiveness, stability, and precise dosing capabilities that resonate with traditional supplement users. The gummies segment is growing at an 10.44% CAGR, supported by consumer preferences for palatable delivery formats and new technologies enabling reduced-sugar formulations. Capsules and softgels maintain their market position through effective ingredient protection and consumer association with pharmaceutical-grade quality. Powders attract consumers seeking flexible dosing options and quick dissolution, especially among protein-focused demographics.

Cold-set gelation technology has emerged as an energy-efficient manufacturing method for gummies, improving product quality and shelf life. Vegan gummy formulations meet the increasing demand for plant-based options by using alternative gelling agents that deliver consistent texture and stability. The "Others" category encompasses delivery formats such as functional beverages, chewable tablets, and sublingual formulations that offer enhanced bioavailability. Manufacturing processes now integrate HACCP guidelines while facilitating natural ingredient incorporation to meet consumer demand for clean-label products.

By Distribution Channel: Specialty Stores Lead Market Share While E-commerce Shows Rapid Growth

Specialty and health stores hold a 41.96% market share in 2025, driven by their ability to provide expert consultation and curated product selections that enhance consumer confidence in immune health purchases. The online retail segment is growing at 10.08% CAGR, supported by direct-to-consumer brands and subscription models that provide reliable product availability. While supermarkets and hypermarkets offer extensive consumer reach, they struggle with immune health product education and premium positioning. Pharmacies represent another significant distribution channel, benefiting from their proximity to healthcare providers and established consumer trust.

NOW Foods launched brick-and-mortar exclusive product sizes in March 2024, introducing 20 supplement formulations specifically for independent retailers to differentiate from online competitors. The growth in e-commerce enables targeted marketing and subscription services, with companies using consumer data to enhance product recommendations and customer retention. However, online platforms face heightened regulatory oversight regarding health claims, necessitating comprehensive compliance measures to prevent FDA enforcement. An omnichannel presence has become crucial as consumers conduct online research before making in-store purchases, particularly for premium immune health products where professional guidance provides additional value.

Geography Analysis

The United States anchored 78.65% of 2025 sales within the North America immune health supplements market, owing to high discretionary income, a mature retail ecosystem, and prolific clinical research that validates new actives. Chronic conditions afflict more than three-quarters of adults, sustaining year-round demand for immune fortification. The FDA supplies clear guidance on good manufacturing practice, which raises baseline quality and cements consumer confidence, allowing premium lines to flourish.

Canada contributes steady expansion as Health Canada’s Natural Health Products Regulations enforce strong safety standards yet offer a clear licensing roadmap. Natural product numbers serve as visible trust marks on pack, driving consumer purchase intent. National latitude-induced vitamin D deficiency shapes product portfolios toward higher dosing and fortified functional foods. Temporary exemptions from plain-language labeling rules until 2028 give firms breathing room to update packs without interrupting supply.

Mexico is the breakout territory, poised for an 10.86% CAGR. Rising middle-class affluence lifts supplemental spending, and COFEPRIS modernization expedites product registrations. Front-of-pack nutrient warnings may appear onerous, yet brands that formulate below critical thresholds gain a competitive halo. Geographic proximity to U.S. manufacturing hubs keeps logistics costs in check, while cultural openness to herbal remedies allows hybrid formulations that blend botanicals with clinical-grade micronutrients. Collectively, distinct regulatory and socioeconomic conditions across the three countries ensure that no single go-to-market blueprint suffices. Brands must localize compliance, messaging, and retail strategy to capture the full potential of the North America immune health supplements market size through 2030.

Competitive Landscape

The North American immune health supplements market exhibits moderate fragmentation, creating a competitive environment where established pharmaceutical players like Bayer AG and Pfizer Inc. compete alongside specialized nutrition companies such as Herbalife Nutrition Ltd. and Amway Corp. This diverse competitive landscape drives innovation across multiple dimensions, including ingredient science, delivery technologies, and consumer engagement strategies.

The market's competitive dynamics are increasingly shaped by scientific differentiation rather than merely marketing claims, with companies investing in clinical validation to substantiate efficacy. This science-driven approach is exemplified by Lallemand Health Solutions' distribution agreement with Kirin Holdings for Immuse, a postbiotic containing heat-inactivated Lactococcus lactis that has been validated through 15 clinical studies demonstrating enhanced immune responses in May 2025. Strategic consolidation continues to reshape the competitive landscape, with the May 2025 acquisition of The Vitamin Shoppe by Kingswood Capital Management and Performance Investment Partners highlighting the value of established retail distribution networks combined with digital capabilities.

White-space opportunities exist in personalized immune support solutions, with over half of consumers expressing interest in genetic testing for nutrition guidance, indicating untapped potential for tailored formulations that address individual risk factors and health goals. Technological innovation represents another competitive frontier, with advances in delivery systems like lipid nanoparticles (LNPs) demonstrating potential to enhance the bioavailability and efficacy of immune ingredients, creating differentiation opportunities for companies that can successfully commercialize these technologies.

North America Immune Health Supplements Industry Leaders

-

Pfizer Inc.

-

Bayer AG

-

Herbalife Nutrition Inc.

-

Amway Corporation

-

Nestle SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Pharmavite, LLC, a subsidiary of Otsuka Pharmaceutical Co., Ltd. (Otsuka), opened a new facility called "Pharmavite New Albany" in Ohio, United States. The facility specializes in manufacturing gummy supplements under Pharmavite's Nature Made® brand.

- March 2025: The Vitamin Shoppe launched GLP-1 Support from Whole Health Rx by The Vitamin Shoppe, a line of dietary supplements designed to address the nutritional needs of individuals using GLP-1 medications for weight management.

- December 2024: Nature's Bounty introduced its Plant-Based Omega-3 dietary supplement, a vegetarian alternative to traditional fish oil. The supplement sources EPA and DHA omega-3s directly from algae, providing a plant-based solution for consumers seeking omega-3 benefits. The product aims to support heart health, maintain healthy skin, and promote proper joint function, making it suitable for individuals following plant-based diets or those who prefer non-fish sources of omega-3s.

- October 2024: Ultisana, a nutraceutical brand established in Central America, launched in the U.S. market. The company, which has served healthcare practitioners in Central America, introduces three products: COGNIFORTE, DIABERINE, and STAMINA. These supplements focus on cognitive function, metabolic health, and stress management.

North America Immune Health Supplements Market Report Scope

Immune health supplements are the products that are consumed by all age groups to protect themselves from diseases and stay healthy.

The North American immune health supplements market is segmented by product type, form, distribution channel, and geography. Based on the product type, the market is segmented into vitamins & minerals, herbal/botanical extracts, probiotics, omega-3 fatty acids, and others. Based on the form, the market is segmented into soft gels & capsules, tablets, gummies, powders, and others. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, specialty & health stores, online retail, and others. Based on geography, the study provides an analysis of the immune supplements market in the United States, Canada, Mexico, and the Rest of North America. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Vitamins and Minerals |

| Herbal/Botanical Extracts |

| Probiotics |

| Omega-3 Fatty Acids |

| Others |

By Form

| Capsules and Softgels |

| Tablets |

| Gummies |

| Powders |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Stores |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Vitamins and Minerals |

| Herbal/Botanical Extracts | |

| Probiotics | |

| Omega-3 Fatty Acids | |

| Others | |

| By Form | Capsules and Softgels |

| Tablets | |

| Gummies | |

| Powders | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty and Health Stores | |

| Online Stores | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current size of the North America immune health supplements market?

The market stands at USD 5.01 billion in 2026 and is projected to climb to USD 7.81 billion by 2031.

Which country contributes the largest share to regional sales?

The United States holds 78.65% of 2025 market share, reflecting mature retail infrastructure and high consumer spending.

Which product category is growing fastest?

Probiotics are forecast to advance at a 9.42% CAGR between 2026-2031, outpacing vitamins and minerals.

Why are gummies gaining popularity?

Gummies combine palatable taste with advanced gelation technology, driving an 10.44% CAGR from 2026 onward while maintaining functional efficacy.

Page last updated on: