Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

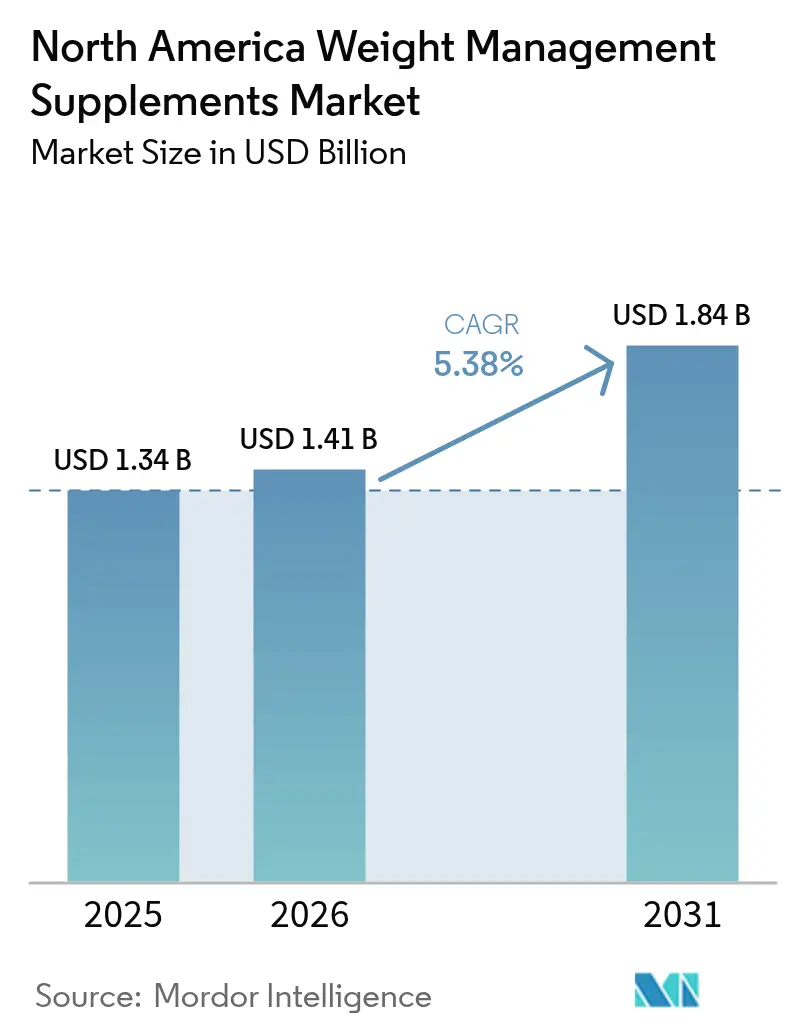

| Base Year Market Size (2025) | USD 1.34 Billion |

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.84 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Weight Management Supplements Market Analysis by Mordor Intelligence

The North America weight management supplements market size in 2026 is estimated at USD 1.41 billion, growing from 2025 value of USD 1.34 billion with 2031 projections showing USD 1.84 billion, growing at 5.38% CAGR over 2026-2031. This trajectory reflects a recalibration rather than acceleration, as the weight management supplements market contends with the disruptive entry of GLP-1 receptor agonists. Semaglutide prescriptions alone reached 5.6 million Americans in 2023 and are projected to climb to 24 million by 2035, fundamentally reshaping demand for traditional thermogenic and appetite-suppression formulations [1]Source: National Institutes of Health, "Know Your Blood Pressure Numbers", nih.gov. Obesity prevalence above 40% in U.S. adults remains the structural demand driver, yet purchase decisions now favor clinically documented ingredients, partly because FDA enforcement has removed several products with unverifiable claims [2]Source: CDC (Centers for Disease Control and Prevention), "Obesity Prevalence", cdc.gov. Capsules and tablets still dominate, but gummies are accelerating, supported by low-sugar technologies that improve compliance. Channel power is shifting as specialty health-store closures coincide with a surge in direct-to-consumer online sales, driven by Amazon’s third-party testing rules that reward certified suppliers. Thus, the North American weight management supplements market is growing due to persistent obesity rates above 40% in adults and increasing consumer preference for clinically proven ingredients, as FDA enforcement removes products with unverifiable claims. Additionally, the rise of GLP-1 receptor agonists, innovations like low-sugar gummies, and the shift toward online direct-to-consumer channels are reshaping demand and fueling market expansion.

Key Report Takeaways

- By product type, vitamins and minerals captured 30.62% of the weight management supplements market share in 2025, while amino acids are forecast to grow at a 7.04% CAGR through 2031.

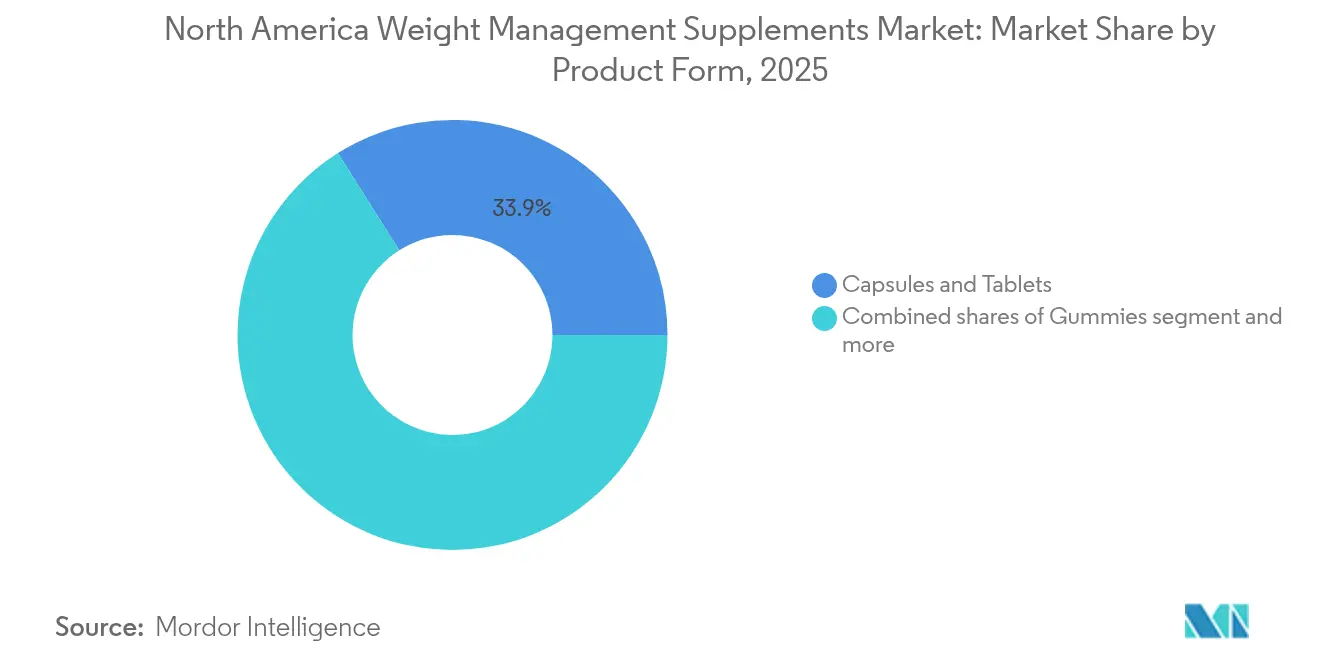

- By product form, capsules and tablets led with a 33.94% share of the weight management supplements market size in 2025, whereas gummies are advancing at a 6.55% CAGR to 2031.

- By distribution channel, health and wellness stores held 45.38% revenue share in 2025, yet online retail is expanding at a 5.62% CAGR through 2031.

- By geography, the United States commanded 77.58% of 2025 revenue, and Canada represents the fastest-growing territory at a 5.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Weight Management Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity and chronic disease prevalence | +1.8% | United States, Canada | Long term (≥ 4 years) |

| Growing health and wellness consciousness | +1.3% | United States, Canada | Medium term (2-4 years) |

| Demand for natural, plant-based supplement formulations | +0.9% | United States, Canada, with stronger traction in urban coastal markets | Medium term (2-4 years) |

| Popularity of powders and convenient supplement formats | +0.7% | United States, Canada | Short term (≤ 2 years) |

| Ease of access via offline and online retail channels | +0.8% | United States, Canada | Short term (≤ 2 years) |

| Innovation and new formulation launches are boosting interest | +0.6% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Obesity and Chronic-Disease Prevalence

Obesity rates in North America have reached crisis proportions, with a significant number of US adults classified as obese in the 2021-2023 NHANES (National Health and Nutrition Examination Survey) survey, and Canada reporting 29.5% obesity prevalence according to the Centers for Disease Control and Prevention. The 40-59 age cohort exhibits the highest obesity rates, creating a demographic bulge that will sustain demand through 2030 as this population seeks metabolic interventions. Chronic conditions linked to obesity, type 2 diabetes, cardiovascular disease, and non-alcoholic fatty liver disease are driving the majority of US consumers to actively pursue weight-loss strategies, yet the strategic shift lies in their preference for evidence-based supplements over proprietary blends. The FDA's December 2024 finalization of the "healthy" nutrient-content claim rule, effective in 2028, will further legitimize supplements that meet specific micronutrient thresholds, creating a regulatory moat for compliant formulations[3]Source: U.S. Food and Drug Administration, "7 Months Reform", fda.gov. Projections indicate that obesity prevalence will continue rising through 2050, ensuring a sustained addressable market, but the competitive advantage will accrue to brands that can substantiate metabolic benefits through clinical endpoints rather than anecdotal testimonials.

Growing Health and Wellness Consciousness

Consumer health consciousness has evolved from a preference for "clean" or "natural" labels to a demand for clinically substantiated efficacy, a shift catalyzed by the visibility of GLP-1 drugs and their dramatic weight-loss outcomes. Survey data reveal that 67% of supplement users want personalized formulations tailored to their metabolic profiles, and 67% of regular users consume supplements 24 or more days per month, indicating high adherence when products deliver perceived value according to the National Institutes of Health. This behavioral pattern favors subscription models and direct-to-consumer brands that can offer customization and transparency. The Vitamin Shoppe's June 2024 launch of Whole Health Rx, a telehealth platform prescribing GLP-1 drugs alongside complementary supplements, exemplifies how retailers are positioning themselves as holistic wellness advisors rather than transactional vendors. The strategic implication is that weight management supplements are increasingly bundled with broader wellness ecosystems, genetic testing, continuous glucose monitors, and digital coaching, making standalone product sales less defensible. Brands that cannot integrate into these ecosystems risk commoditization.

Demand for Natural, Plant-Based Supplement Formulations

Plant-based supplement formulations are capturing share as consumers associate botanical ingredients with lower side-effect profiles, though this perception is not always supported by clinical evidence. Green tea extract (EGCG) and caffeine-based botanicals dominate the thermogenic segment, while adaptogenic herbs like ashwagandha are being positioned for stress-related weight gain. However, the FDA issued multiple warning letters in 2024 targeting botanical weight-loss products with unsubstantiated claims or adulteration, creating a credibility gap that benefits vertically integrated brands with in-house testing. The plant-based trend is also evident in protein powders, where pea, soy, and rice proteins are growing faster than whey, driven by environmental and ethical considerations. The strategic opportunity lies in hybrid formulations that combine plant-based proteins with amino acids like L-carnitine or CLA, offering both the "clean" positioning consumers seek and the metabolic mechanisms they need. Brands that can navigate FDA scrutiny while maintaining botanical authenticity will capture the premium segment, which tolerates higher price points for perceived safety.

Innovation and New Formulation Launches Boosting Interest

Innovation in weight management supplements is concentrating around three vectors: GLP-1 complementary formulations, low-sugar gummy technologies, and ready-to-drink convenience formats. Berberine, a botanical compound with glucose-lowering properties, surged 89.8% in sales as consumers sought a "natural" alternative to metformin, while MCT oil grew 42.7% as a ketogenic adjunct. Gummy manufacturers are deploying Gelita's Soluform technology and allulose-based sweeteners to deliver metabolism-boosting actives in formats that adults prefer over pills, addressing the compliance gap that undermines efficacy. Ready-to-drink protein shakes grew in 2024, driven by on-the-go consumption and the perception that liquid formats offer faster absorption. The FDA's February 2024 launch of the New Dietary Ingredient (NDI) Directory and March 2024 final guidance on NDI notification procedures are raising the bar for novel ingredients, favoring companies with regulatory affairs teams capable of navigating premarket submissions. The competitive insight is that innovation is no longer about ingredient novelty, but about delivery-system optimization and regulatory compliance; brands that can combine both will command pricing power.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulatory scrutiny and safety compliance requirements | -0.9% | United States, Canada | Short term (≤ 2 years) |

| Widespread adulteration and counterfeit supplement risk | -0.6% | United States, Canada, with a higher incidence in online channels | Short term (≤ 2 years) |

| Increasing preference for whole foods over supplements | -0.4% | United States, Canada, concentrated in health-conscious urban demographics | Medium term (2-4 years) |

| High cost of premium or specialty supplements | -0.5% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Regulatory Scrutiny and Safety Compliance Requirements

Regulatory intensity escalated sharply in 2024, with the FDA finalizing NDI notification guidance in March and launching the NDI Directory in February, creating a transparent but burdensome pathway for novel ingredients. Health Canada's updated Natural Health Products Regulations impose stricter labeling and substantiation requirements, raising compliance costs that disproportionately affect smaller brands lacking regulatory infrastructure. New York's Assembly Bill A5610, effective April 22, 2024, restricts minors' access to weight-loss and muscle-building supplements, mandating age verification and staff training that increase operational friction for both brick-and-mortar and online retailers. The Council for Responsible Nutrition (CRN) and Natural Products Association (NPA) filed lawsuits challenging the law, but the precedent signals potential federal action. The strategic implication is that regulatory compliance is becoming a competitive moat: brands that invest in quality systems and third-party verification will capture share from non-compliant competitors, but the cost burden will compress margins for mid-tier players.

Widespread Adulteration and Counterfeit Supplement Risk

Adulteration remains a persistent threat, with the FDA issuing warning letters in 2024 targeting weight-loss supplements spiked with undeclared pharmaceutical ingredients like sibutramine and phenolphthalein. Health Canada conducted seizures of unauthorized products, particularly those marketed online with exaggerated claims. The economic incentive for adulteration is high: adding pharmaceutical actives delivers rapid weight loss that consumers attribute to the supplement, generating repeat purchases before adverse events surface. This dynamic erodes trust in the entire category, particularly for botanical formulations where ingredient identity and potency are harder to verify than synthetic vitamins. Third-party certification by NSF International, USP, or Informed Choice is becoming a de facto requirement for premium positioning, but only some of brands carry such seals due to cost and testing burdens. The strategic opportunity lies in transparency: brands that publish certificates of analysis, conduct batch-level testing, and use blockchain for supply-chain traceability can command price premiums from risk-averse consumers. However, the counterfeit problem is worsening in online channels, where marketplace dynamics favor low-cost sellers over verified brands, creating a race-to-the-bottom that undermines category growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Amino Acids Drive Fastest Expansion

Amino acids are the fastest-growing product segment at a 7.04% CAGR from 2026 to 2031, outpacing the overall market as consumers seek muscle-preserving formulations to counteract the lean-mass loss associated with GLP-1 drugs and caloric restriction. L-carnitine, which facilitates fatty acid transport into mitochondria, and conjugated linoleic acid (CLA), which modulates body composition, are the primary drivers, with clinical evidence supporting modest but measurable effects on fat oxidation. Branched-chain amino acids (BCAAs) are also gaining traction as consumers recognize that weight loss without muscle preservation leads to metabolic slowdown. Vitamins and minerals held the largest share at 30.62% in 2025, anchored by chromium picolinate for glucose metabolism, B-complex vitamins for energy production, and vitamin D for its inverse association with obesity, according to the Centers for Disease Control and Prevention. However, this segment faces commoditization pressure as these ingredients are widely available in multivitamins and fortified foods, limiting differentiation.

Botanicals occupy a middle position, with green tea extract (EGCG) and garcinia cambogia (hydroxycitric acid) delivering thermogenic and appetite-suppression mechanisms, but the segment is constrained by FDA enforcement targeting unsubstantiated claims and adulteration risks. The "Others" category, which includes fiber supplements, probiotics, and emerging compounds like berberine, is experiencing volatility: berberine surged 89.8% in 2024 as a "natural metformin" alternative, while traditional fiber products face competition from whole-food sources. The strategic insight is that product-type preferences are fragmenting along efficacy expectations, consumers willing to pay premium prices gravitate toward amino acids with clinical backing, while price-sensitive buyers remain in the vitamins-and-minerals segment. Brands that can straddle both tiers through tiered product lines will maximize the addressable market.

By Product Form: Gummies Capture Compliance-Driven Growth

Capsules and tablets dominated with 33.94% of market share in 2025, reflecting their cost efficiency, stability, and ability to deliver high-potency actives in compact doses. This format remains the default for amino acids and botanical extracts where dosing precision matters. Yet gummies are the fastest-growing format at a 6.55% CAGR through 2031, driven by adult adoption and the recognition that compliance, not potency, is the primary determinant of real-world efficacy. Adults now represent the core gummy consumer base, a reversal from the pediatric origins of the format, and manufacturers are responding with low-sugar innovations using allulose, stevia, and Gelita's Soluform technology that enables higher active loads without compromising texture. Metabolism-boosting gummies containing green tea extract, caffeine, or apple cider vinegar are proliferating, though clinical evidence for these formulations is limited compared to capsule equivalents.

Powders, which include protein powders and meal replacements, are experiencing bifurcated demand: traditional weight-loss shakes are declining, but protein powders grew in 2024 as GLP-1 users sought to prevent muscle wasting. The "Others" category, encompassing liquids, soft gels, and effervescent tablets, remains niche but is growing in specific use cases like pre-workout thermogenics. The strategic takeaway is that format innovation is now a primary axis of competition: brands that can deliver clinically relevant doses in consumer-preferred formats will outperform those constrained by traditional delivery systems. However, gummy manufacturers must navigate the tension between palatability and efficacy, as high active loads often compromise taste and texture.

By Distribution Channel: Online Retail Reshapes Channel Economics

Health and wellness stores commanded 45.38% of market share in 2025, but this dominance is eroding as the channel grapples with structural headwinds. GNC closed approximately 900 mall-based stores, and its Q2 2024 US and Canada revenue fell 8% to USD 476.1 million, reflecting traffic declines and competition from e-commerce. However, GNC's December 2024 partnership with Walmart to place products in 4,000+ stores and its April 2024 launch of GLP-1 support sections in all 2,300+ US stores illustrate a strategic pivot toward mass-market distribution and pharmaceutical adjacency. These moves suggest that specialty retailers are repositioning from product sellers to solution providers, leveraging their credibility to capture higher-margin services.

Online retail is the fastest-growing channel at a 5.62% CAGR from 2026 to 2031, propelled by direct-to-consumer brands, Amazon's dominance, and subscription models that lock in recurring revenue. iHerb generated USD 2.4 billion in net sales in 2024 and expanded into Albertsons and Amazon UK/Australia in January 2025, demonstrating the scalability of pure-play e-commerce models. Amazon's 2024 third-party testing requirements are consolidating the channel around verified brands, raising barriers to entry but enhancing consumer trust. Supermarkets and hypermarkets, while holding a smaller share, benefit from impulse purchases and the ability to cross-sell weight management supplements alongside functional foods. The strategic insight is that channel parity is emerging: by 2025-2026, natural/specialty, e-commerce, and mass market will hold roughly equal shares, forcing brands to adopt omnichannel strategies or risk losing visibility.

Geography Analysis

The United States dominates with 77.58% of market share in 2025, a concentration driven by high obesity prevalence, strong consumer spending on wellness, and a mature regulatory framework that, despite its complexity, provides clarity for compliant brands according to the Centers for Disease Control and Prevention. Regional variations within the US are notable: urban coastal markets exhibit stronger demand for plant-based and premium formulations, while heartland regions prioritize value and efficacy over ingredient sourcing. The strategic opportunity lies in geographic segmentation; brands that tailor formulations and messaging to regional preferences can capture share from one-size-fits-all competitors.

Canada is the fastest-growing geography at a 5.93% CAGR from 2026 to 2031, despite holding a smaller absolute market size. This growth is fueled by a 29.5% obesity rate, rising health consciousness, and Health Canada's updated Natural Health Products Regulations in 2024 that, while raising compliance burdens, enhance consumer trust in certified products. Canadian consumers exhibit a stronger preference for natural and plant-based formulations compared to their US counterparts, creating opportunities for botanical and adaptogenic supplements. The regulatory environment is also more favorable to certain claims: Health Canada's pre-approval system for health claims allows compliant brands to differentiate on efficacy in ways that US brands cannot without triggering FDA enforcement. The strategic implication is that Canada rewards brands willing to invest in local regulatory compliance and tailored formulations, but the smaller market size limits the return on investment for all but the largest players.

The rest of North America, encompassing Mexico and Central American markets, remains a minor contributor but exhibits nascent growth as obesity rates rise and middle-class expansion increases discretionary spending on wellness. However, regulatory fragmentation, lower per-capita incomes, and weaker enforcement against counterfeit products create barriers to entry for premium brands. The strategic focus for most companies remains the US-Canada duopoly, where regulatory clarity, purchasing power, and distribution infrastructure justify investment. Brands seeking geographic diversification are more likely to look toward Western Europe or Asia-Pacific than to expand within North America beyond the US and Canada.

Competitive Landscape

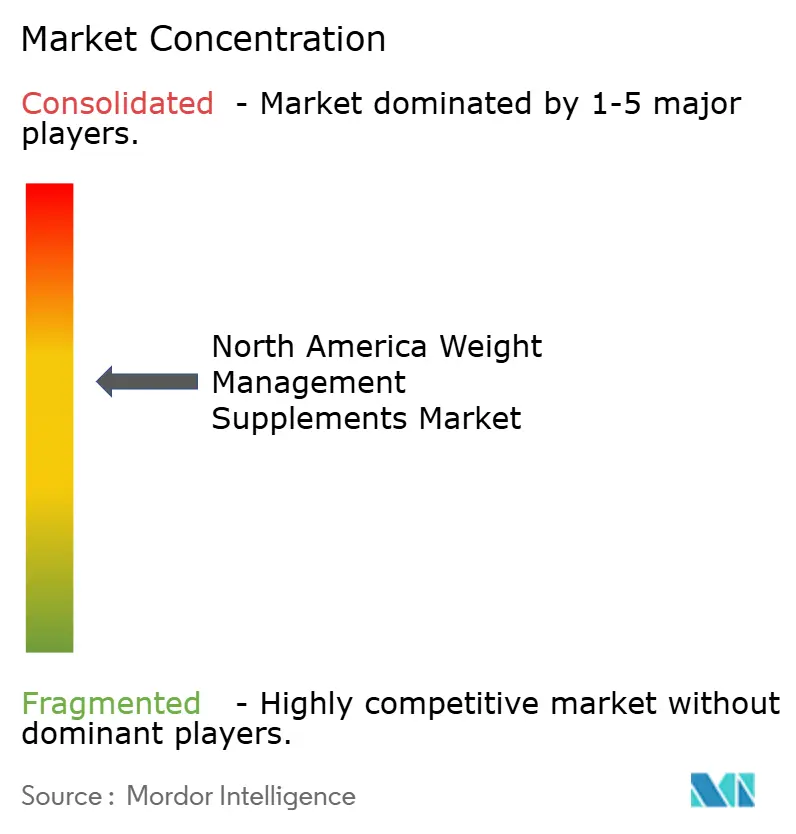

The North America weight management supplements market exhibits moderate concentration, as compliance costs and third-party certification requirements favor scaled players with regulatory infrastructure, while leaving room for specialized disruptors. Established brands like Abbott, Glanbia, and Herbalife leverage clinical credibility, distribution scale, and brand equity, yet face margin pressure from direct-to-consumer entrants that bypass intermediaries and capture customer data for personalized offerings.

Glanbia's Performance Nutrition segment is demonstrating that protein-powder incumbents are successfully pivoting toward GLP-1 complementary formulations. Conversely, Herbalife's North America sales fell 13.4% year-over-year to USD 265.1 million in Q3 2024, reflecting challenges in its multi-level marketing model as consumers shift toward transparent, science-backed brands. The strategic pattern is clear: brands that can substantiate efficacy through clinical endpoints and navigate regulatory complexity are gaining share, while those reliant on proprietary blends and testimonial-based marketing are losing ground. Opportunities are emerging at the intersection of pharmaceutical weight loss and nutritional supplementation.

Technology is becoming a competitive differentiator: Amazon's third-party testing mandates, implemented in 2024, are consolidating the e-commerce channel around brands that can afford NSF International or USP certification, effectively creating a quality moat. Emerging disruptors are leveraging subscription models, genetic testing, and continuous glucose monitors to offer personalized formulations that command premium pricing. The FDA's December 2024 finalization of the "healthy" nutrient-content claim rule, effective in 2028, will further advantage brands with formulations that meet specific micronutrient thresholds, creating a regulatory moat for compliant products. The competitive insight is that the market is bifurcating into a premium tier characterized by clinical validation, third-party certification, and integrated wellness ecosystems, and a value tier where price-sensitive consumers accept lower efficacy in exchange for affordability.

North America Weight Management Supplements Industry Leaders

-

Abbott.

-

NOW® Foods

-

Herbalife Nutrition Ltd.

-

Glanbia PLC

-

Amway

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Vitanergy Health US Inc., a women-led dietary supplement company based in the United States, announced the launch of three new products formulated to support women's daily nutritional needs: Vitanergy D3 Multivitamin Gummy, Vitanergy B Complex Gummy with Folate, and Rejuvenate and Glow 4-in-1 Capsule. These products became available on Amazon, Walmart Marketplace, Flaire.com, and Vitanergy.com. They were formulated with high-quality ingredients and manufactured in the USA.

- July 2025: Herbalife Nutrition company launched MultiBurn™: a multi‑action dietary supplement built on clinically studied botanical extracts (Moro blood orange extract “Morosil”, hibiscus + lemon verbena “Metabolaid”, red chili pepper + fenugreek “Capsifen”), plus caffeine and chromium, targeting fat reduction, metabolic health, and energy expenditure in the United States.

- March 2025: The Vitamin Shoppe introduced GLP-1 Support from Whole Health Rx: a line of supplements formulated for users of GLP-1 medications (protein, fiber, probiotics/synbiotics, multivitamins, all‑in‑one nutrient powders) to address nutrient gaps from appetite suppression and reduced food intake in the United States.

North America Weight Management Supplements Market Report Scope

The weight management supplements market is segmented by product type, product form, distribution channel, and geography. By product type, the market is segmented into vitamins and minerals, botanicals, amino acids, and others. By product form, the market is segmented into powder, capsules and tablets, gummies, and others. By distribution channel, the market is segmented into hypermarkets/supermarkets, health and wellness stores, online retail stores, and more. By geography, the market is segmented into the United States, Canada, and more. the market forecasts are provided in terms of value (USD).

By Product Type

| Vitamins and Minerals |

| Botanicals |

| Amino Acids |

| Others |

Product Form

| Powder |

| Capsules and Tablets |

| Gummies |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Wellness Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Rest of North America |

| By Product Type | Vitamins and Minerals |

| Botanicals | |

| Amino Acids | |

| Others | |

| Product Form | Powder |

| Capsules and Tablets | |

| Gummies | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Wellness Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

How large will North America spending on weight-control supplements be in 2031?

The weight management supplements market size is projected at USD 1.84 billion by 2031, reflecting a 5.38% CAGR from 2026.

Which product form is growing fastest among adult users?

Gummies lead with a 6.55% CAGR as low-sugar technologies increase palatability and daily-dose compliance.

How are GLP-1 drugs affecting supplement demand?

They shift buying toward protein powders and amino-acid blends that preserve muscle mass, while standalone fat burners decline.

What sales channel shows the highest forward growth?

Online retail expands at a 5.62% CAGR, aided by Amazon’s testing mandates and subscription models.

Page last updated on: