Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 25.64 Billion |

| Market Size (2031) | USD 38.07 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Dietary Supplements Market Analysis by Mordor Intelligence

The European dietary supplements market size is valued at USD 25.64 billion in 2026 and is forecast to reach USD 38.07 billion by 2031, expanding at an 8.23% CAGR. This growth is driven by several key factors, including an aging population, an increasing gap in micronutrient intake, and the implementation of clear regulatory policies under Directive 2002/46/EC, which collectively sustain long-term demand. Additionally, the expansion of online retail channels, the introduction of innovative supplement formats, and the rising trend of personalized nutrition are further broadening the market's consumer base. Vitamins and minerals continue to dominate as the leading segment, supported by national campaigns aimed at reducing deficiencies and promoting daily supplementation. However, the fastest growth in volume is observed in gummies and subscription-based e-commerce models, which cater to evolving consumer preferences for convenience and novelty. Despite the challenges posed by fragmented country-level regulations that complicate product registration and labeling, pharmacies in countries like Italy and Germany remain trusted distribution channels, particularly for clinically focused brands. Efforts to suppress counterfeit products and the European Food Safety Authority's (EFSA) stricter reviews of health claims may temper overall market growth. However, these measures also create opportunities for companies that can demonstrate the authenticity of their ingredients and provide clinical evidence of their products' efficacy, thereby gaining a competitive edge in the market.

Key Report Takeaways

- By product type, vitamins and minerals led with 51.31% European dietary supplements market share in 2025; the same segment is projected to grow at a 10.57% CAGR through 2031.

- By form, tablets commanded 27.85% of the European dietary supplements market size in 2025, yet gummies represent the fastest-rising format with a 9.21% CAGR to 2031.

- By consumer group, women captured 34.01% of consumption in 2025, while children’s products recorded the highest forecast CAGR at 9.84% through 2031.

- By health application, immunity enhancement held 22.13% share of the European dietary supplements market size in 2025, whereas skin, hair, and nail care is advancing at a 9.67% CAGR to 2031.

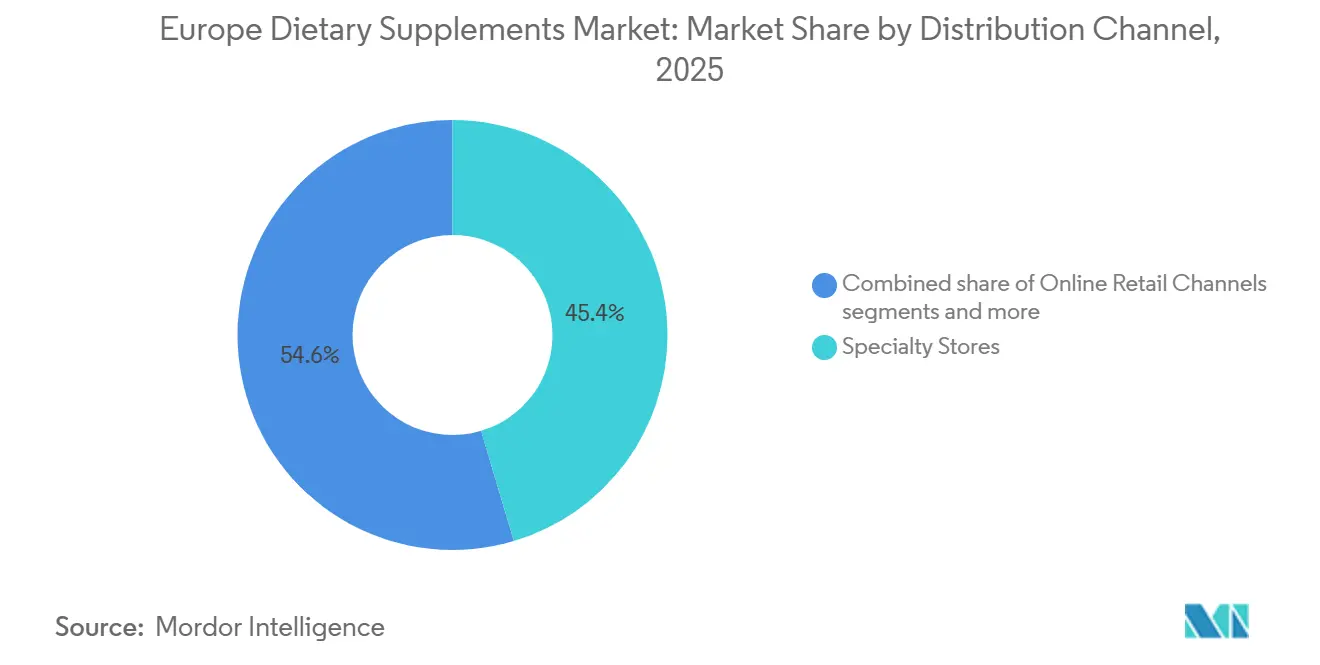

- By distribution channel, specialty stores accounted for 45.38% revenue share in 2025; online retail is the quickest-growing route with a 9.11% CAGR through 2031.

- By geography, Italy contributed 21.16% to regional value in 2025, but the United Kingdom posts the highest projected CAGR at 12.21% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Dietary Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preventive healthcare trends driving regular supplement consumption | +1.8% | Pan-European, strongest in Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Supplements targeting women consumers fueling growth | +1.5% | Italy, France, United Kingdom, Spain | Short term (≤ 2 years) |

| Consumers' inclination towards clean-label and natural supplements | +1.2% | Germany, Austria, Nordics, spillover to Western Europe | Medium term (2-4 years) |

| Europe's aging population boosts demand for age-related supplements | +1.6% | Italy, Germany, France, Poland | Long term (≥ 4 years) |

| Growing popularity of sports nutrition and fitness trends drives supplement use among younger consumers | +1.0% | United Kingdom, Germany, France, Netherlands | Short term (≤ 2 years) |

| E-commerce expansion makes supplements more accessible and promotes market growth | +1.3% | United Kingdom, Germany, France, Benelux, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preventive healthcare trends are driving regular supplement consumption

European health systems dedicate a smaller share of their total health expenditure to preventive measures. Consequently, consumers are increasingly relying on self-directed supplementation to address this gap. This trend is particularly prominent in markets with high out-of-pocket healthcare expenses and prolonged waiting times for specialist care, where supplements are perceived as a convenient alternative to pharmaceuticals. The European Commission's 2024 State of Health in the European Union report revealed that 23% of adults aged 65 and older are at risk of malnutrition [1]Source: OECD (Organisation for Economic Co-operation and Development), "Health at a Glance: Europe 2024", oecd.org. This risk is fueling greater demand for fortified multivitamins and protein supplements. National initiatives, such as the United Kingdom's vitamin D supplementation guidance for at-risk groups, are both legitimizing regular supplement use and positioning preventive nutrition as an essential public health measure. Furthermore, Germany's Federal Institute for Risk Assessment has issued updated tolerable upper intake levels for micronutrients. These evidence-based dosing guidelines aim to reduce consumer concerns about long-term supplementation.

Supplements targeting women consumers fueling growth

Women's health supplements have shifted their focus from solely prenatal care to addressing a broader range of concerns, including menopause, hormonal balance, skin elasticity, and bone density, areas often neglected by pharmaceutical companies. Highlighting the growing investor interest in the menopause supplement market, Venture Life Group acquired Health and Her Limited for GBP 7.5 million (USD 9.5 million) in October 2024. This market stands out due to its longer treatment durations and higher per-capita spending compared to general wellness products. In 2025, the European Medicines Agency clarified labeling requirements for botanical substances in menopause products, reducing regulatory uncertainties for manufacturers. Additionally, France's ANSES approved specific health claims for calcium and vitamin D in postmenopausal women, setting a precedent likely to be followed by other European Union member states. Furthermore, women's demand for clean-label formulations and transparent sourcing is driving progress in organic certification and third-party testing protocols.

Europe's aging population boosts demand for age-related supplements

The demographic shift in Europe is driving demand for supplements that address age-related health concerns, as the population aged 65 and above is projected to reach 30% by 2050, according to the Centre for the Promotion of Imports from Developing Countries[2]Source: CBI Centre for the Promotion of Imports from Developing Countries, “Which Trends Offer Opportunities on the European Market for Natural Ingredients for Health Products,” CBI, cbi.eu . According to the data from Eurostat, Italy has the highest older population in Europe, with around 24.30% as of 2024[3]Source: Eurostat, “Eurostat Data Browser,” European Commission, ec.europa.eu . The aging population is driving increased demand for supplements that support bone and joint health, cognitive function, and cardiovascular well-being. Bayer's Berocca Mind, launched in November 2024, features Spanish sage extract and aims to combat age-related memory decline. Positioned as a gentler alternative to prescription nootropics, these cognitive health supplements boast fewer side effects. With Poland's population aging swiftly and supplement usage still in its infancy, brands adept at maneuvering through the nation's pharmacy-dominated distribution landscape stand to gain significantly.

Consumers' inclination towards clean-label and natural supplements

In Germany and Austria, where "naturkost" retail channels benefit from premium pricing and strong consumer loyalty, the demand for clean-label products is transforming formulation strategies. The European Food Safety Authority, in its 2024 assessment, highlighted safety concerns regarding 13 botanical substances, including St. John's wort, holy basil, and turmeric. This has accelerated the industry's shift toward ingredients that are both well-characterized and clinically validated. Manufacturers are responding by replacing synthetic excipients with plant-based alternatives and implementing blockchain-enabled systems to verify ingredient authenticity. Adulteration remains a significant challenge; studies published in 2024 reported the highest contamination rates in supplements such as ginkgo, black cohosh, and turmeric. As a result, retailers like Holland and Barrett have introduced DNA barcoding for these high-risk products. Additionally, the EU's Novel Foods Regulation requires detailed safety dossiers for certain botanicals, particularly those without a significant consumption history before 1997, a threshold that many traditional Ayurvedic and Chinese herbs fail to meet unless sponsors invest in toxicology studies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of counterfeit products hampering growth | -0.9% | Pan-European, acute in online channels across United Kingdom, Germany, France | Short term (≤ 2 years) |

| Scientific skepticism reduces consumer trust in unproven products | -0.7% | Germany, Netherlands, Nordics, spillover to Western Europe | Medium term (2-4 years) |

| Strict regulations limit health claims on supplements | -0.6% | European Union wide, particularly stringent in France (ANSES), Germany | Long term (≥ 4 years) |

| Growing preference for natural food-based nutrition reduces reliance on supplements | -0.5% | Germany, Austria, Netherlands, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Presence of counterfeit products hampering the growth

Counterfeit supplements significantly undermine consumer trust and pose a serious risk to the reputations of legitimate manufacturers, particularly when adverse incidents occur. Online platforms, with third-party sellers on sites like Amazon and eBay, have emerged as major distribution channels for counterfeit products. Among these, weight-loss, bodybuilding, and sexual-enhancement supplements are the most frequently adulterated categories. To combat this issue, premium brands are increasingly adopting advanced authentication technologies such as blockchain-enabled traceability and DNA barcoding. However, the high costs associated with implementing these technologies remain a substantial barrier for smaller manufacturers. In response to these challenges, the European Commission has proposed extending pharmaceutical serialization requirements to high-risk supplement categories by 2025. While this initiative could help address the issue, industry groups have expressed concerns about the financial burden it may place on small and medium-sized enterprises (SMEs) in terms of compliance costs.

Scientific skepticism reduces consumer trust in unproven products

Germany's Federal Institute for Risk Assessment and France's ANSES have expressed concerns about the efficacy of certain botanical supplements, particularly those lacking evidence from randomized controlled trials. Under EFSA's framework, the suspension of health claims for probiotics, where the term "probiotic" is classified as a health claim, has created labeling challenges, leading to consumer confusion and hindering marketing differentiation. Ashwagandha, a widely used adaptogen in Ayurvedic medicine, is banned in several European Union markets due to concerns over hepatotoxicity. This regulatory caution highlights broader skepticism toward traditional botanicals that do not meet the safety dossier requirements under the Novel Foods Regulation. Manufacturers are addressing this by investing in clinical trials and publishing peer-reviewed studies. However, the delay between initiating studies and publishing results places evidence-based brands at a disadvantage compared to competitors making unverified claims in less-regulated markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vitamins and Minerals Lead Innovation

In 2025, vitamins and minerals dominated the market with a 51.31% share, and projections indicate an annual growth rate of 10.57% through 2031. This growth is largely attributed to heightened awareness campaigns about deficiencies and innovative bioavailability formulations. A case in point is DSM-Firmenich's April 2024 green light for calcidiol monohydrate, a vitamin D variant boasting enhanced absorption for the elderly. This move underscores the innovative momentum propelling this segment's dominance. Meanwhile, herbal supplements grapple with challenges. The EFSA's 2024 assessment flagged safety issues in 13 botanical substances, including turmeric and St. John's wort. This revelation has spurred reformulation initiatives and a more vigilant approach to ingredient sourcing. On another front, proteins and amino acids ride the wave of sports nutrition's popularity. Fatty acids, especially omega-3s, enjoy steady demand from consumers prioritizing cardiovascular health. Enzymes, though a niche, find their primary application in digestive health, catering to issues like lactose intolerance and pancreatic insufficiency.

The segment's expansion is anchored in the widespread prevalence of micronutrient deficiencies. For instance, vitamin D shortages are a concern for many Europeans, and iron deficiency anemia poses a significant challenge, especially for women of reproductive age. National supplementation initiatives, such as the United Kingdom's recommendations for vulnerable groups, bolster the legitimacy of routine vitamin consumption, ensuring a consistent demand. Postbiotics, which are metabolites from probiotic fermentation, are carving out a niche. They offer a potential solution to the regulatory ban on "probiotic" health claims. Manufacturers are now marketing these as innovative functional foods, stepping away from the traditional supplement label. The European Food Safety Authority, through its stringent health claims evaluation process under Regulation 1924/2006, guarantees that only robustly supported claims reach the public. However, this meticulous approach can stifle innovation and tends to benefit established players with the financial muscle to back clinical trials.

By Form: Gummies Disrupt Traditional Tablets

Tablets accounted for 27.85% of the market in 2025. However, gummies are the fastest-growing format, with an annual growth rate of 9.21% projected through 2031. This growth is driven by benefits such as taste masking, convenience, and their appeal to both pediatric and geriatric populations. Bayer's introduction of Berocca Multi-Action Gummies in the United Kingdom in December 2023, followed by a broader rollout in 2024, highlights how established brands are leveraging format innovation to meet rising demand. Advances in starchless depositing and pectin-based formulations have enabled the production of sugar-free gummies that comply with clean-label standards, addressing concerns about dental health and glycemic impact. Capsules and softgels remain popular for oil-soluble nutrients, such as omega-3s and fat-soluble vitamins, as gelatin or vegetarian shells protect these ingredients from oxidation. In sports nutrition, powders are preferred for their dose flexibility and rapid dissolution, while liquids cater to individuals with swallowing difficulties or those seeking faster absorption.

The growing preference for gummies reflects a broader consumer trend toward products that resemble confectionery rather than medicine, reducing psychological barriers to daily supplementation. However, gummies face formulation challenges; heat-sensitive nutrients like probiotics and certain vitamins can degrade during manufacturing, limiting the format's applicability. Regulatory scrutiny is also increasing, with some member states proposing restrictions on marketing gummies to children due to concerns about overconsumption. Tablets and capsules, supported by established manufacturing infrastructure and lower per-unit costs, continue to dominate in price-sensitive segments. The European Commission's ongoing review of food supplement labeling requirements may lead to standardized dosing guidelines, which could influence format choices, particularly for nutrients with narrow therapeutic windows.

By Consumer Group: Children's Supplements Surge

Women constituted 34.01% of the demand in 2025, driven by specialized formulations targeting menopause, bone health, prenatal nutrition, and skin elasticity. Children's supplements, supported by parental concerns over micronutrient adequacy and the growing acceptance of early-life supplementation, are expanding at an annual rate of 9.84% through 2031, the fastest among all consumer groups. Gummy formats dominate the pediatric market, with vitamin D, omega-3, and multivitamin products leading sales. Although men's supplements hold a smaller market share, they are gaining popularity in sports nutrition and prostate health, with brands utilizing digital marketing to connect with younger male consumers.

In 2025, the European Medicines Agency clarified labeling requirements for botanical substances in menopause products, reducing regulatory challenges for manufacturers. France's ANSES approved health claims for calcium and vitamin D in postmenopausal women, setting a precedent that other European Union member states are following. Northern and Western Europe, characterized by higher disposable incomes and greater health awareness, are the key growth regions for children's supplements. In Italy, the pediatric supplement market benefits from the pharmacy channel, where trusted pharmacists play a crucial role in recommending products to parents. However, the segment faces challenges, including concerns about supplement dependency and the medicalization of childhood, particularly in regions with strong public health systems that emphasize whole-food nutrition.

By Health Application: Skin and Hair Care Accelerates

Immunity enhancement accounted for 22.13% of the market in 2025, reflecting the ongoing demand driven by the aftermath of the COVID-19 pandemic and recurring seasonal respiratory illnesses. Supplements for skin, hair, and nails are expected to grow at an annual rate of 9.67% through 2031. This growth is attributed to the rising popularity of collagen peptides, biotin, and antioxidant formulations, as consumers increasingly seek beauty-from-within solutions. In January 2026, Haleon launched Centrum Multibiotics, a product combining gut health and general wellness benefits. This highlights a trend where manufacturers are blending traditional health applications to address cross-category demand. Europe's aging population continues to drive demand for bone and joint health supplements, with calcium, vitamin D, and glucosamine formulations maintaining steady popularity. However, energy and weight management products are facing increased regulatory scrutiny due to safety concerns associated with certain stimulants and appetite suppressants.

Gastrointestinal and gut health applications are experiencing growth fueled by innovation. For instance, the next-generation probiotic Akkermansia muciniphila received novel food approval in 2024. Additionally, postbiotics are emerging as a strategic alternative to navigate the regulatory ban on "probiotic" health claims. Cardiovascular health supplements, led by omega-3 fatty acids and plant sterols, continue to see stable demand but are now competing with functional foods fortified with the same ingredients. Diabetes management supplements remain a niche segment, constrained by the European Food Safety Authority's (EFSA) strict health claim regulations and the reluctance of physicians to recommend non-pharmaceutical options. Cognitive and mental health supplements are gaining momentum, as demonstrated by Bayer's November 2024 launch of Berocca Mind, which features Spanish sage extract designed to support memory and combat age-related cognitive decline. Meanwhile, eye health supplements, primarily containing lutein and zeaxanthin, are benefiting from growing concerns over increased screen time and blue-light exposure.

By Distribution Channel: Online Retail Narrows the Gap

Specialty stores captured 45.38% of the distribution market in 2025, underscoring their role as trusted advisors with curated product selections. In Germany, Italy, and France, pharmacy channels take the lead, bolstered by regulatory frameworks that treat supplements akin to pharmaceutical products, emphasizing the need for professional guidance. Online retail channels are on an upward trajectory, growing at an annual rate of 9.11% through 2031. This surge is fueled by subscription models, direct-to-consumer brands, and the allure of home delivery. While supermarkets and hypermarkets act as gateways for mainstream multivitamin brands, they find it challenging to match the depth of product assortment and the level of expert consultation offered by other channels.

Direct selling continues to hold its ground in markets like France and Italy. Here, network marketing thrives on personal relationships and in-home demonstrations. Yet, this channel grapples with challenges, facing regulatory scrutiny over income claims and a wave of consumer skepticism regarding multi-level marketing structures. Boots, a prominent pharmacy retailer in the United Kingdom, has broadened its supplement range, forging exclusive partnerships, notably with Haleon for the Centrum Multivitamins line. Online channels, while lucrative, harbor the highest risk of counterfeits. In response, platforms are rolling out authentication protocols and rigorously vetting third-party sellers. A 2025 proposal from the European Commission aims to broaden pharmaceutical serialization mandates to encompass high-risk supplement categories. If enacted, this could significantly alter online distribution dynamics, especially by raising compliance costs for smaller sellers.

Geography Analysis

Italy accounted for 21.16% of the market in 2025, driven by a pharmacy-centric distribution model that establishes supplements as essential health interventions rather than optional wellness products. Germany's market relies heavily on naturkost retail channels, with pharmacies maintaining a dominant role. France's ANSES enforces strict pre-market safety assessments, which, while slowing innovation, strengthen consumer trust. This regulatory environment benefits established brands capable of managing complex dossier requirements. The United Kingdom, with an anticipated annual growth rate of 12.21% through 2031, is the fastest-growing market among its peers. This growth is primarily due to post-Brexit regulatory independence, enabling the MHRA to deviate from European Union standards and accelerate novel ingredient approvals. Spain's market continues to grow steadily, supported by Mediterranean dietary habits that emphasize micronutrient gaps and a pharmacy channel that inspires consumer confidence.

Russia's supplement market experiences volatility due to geopolitical tensions and currency fluctuations. However, domestic manufacturers are gaining market share as Western brands exit. Sweden reflects Nordic preferences for evidence-based, minimalist formulations, with consumers favoring single-nutrient supplements over complex multivitamin blends. Belgium and the Netherlands benefit from high disposable incomes and strong health awareness, with online retail penetration surpassing the European average. Poland's rapidly aging population and historically low supplement penetration offer significant growth potential for brands that can navigate the country's pharmacy-focused distribution model and price-sensitive consumer base.

Smaller European markets, such as Portugal, Greece, and the Baltics, exhibit diverse regulatory and distribution frameworks, necessitating localized market-entry strategies. Germany's Federal Institute for Risk Assessment has introduced updated tolerable upper intake levels for micronutrients, providing consumers with science-based dosing guidelines that reduce concerns about long-term supplementation. Italy's aging population and strong trust in pharmacy channels drive sustained demand for supplements targeting bone health, cardiovascular health, and cognitive function. The European Food Safety Authority, under Regulation 1924/2006, oversees health claims, ensuring only well-supported claims reach consumers. However, this rigorous process slows innovation and favors established players with the resources to fund clinical trials.

Regulatory Landscape

In the European Union, food supplements are regulated as foods under Directive 2002/46/EC, which sets harmonized rules for vitamins and minerals, while Regulation (EC) No 1925/2006 governs the addition of vitamins, minerals, and certain other substances to foods. Safety and bioavailability assessments for new nutrient sources route through the European Food Safety Authority (EFSA), with the European Commission managing authorization decisions and Member States retaining some country-level implementation differences that affect notifications and enforcement.

For market access and ongoing compliance, labeling must identify the product as a "food supplement" and include daily portion guidance, warnings not to exceed the recommended dose, a statement that supplements do not substitute a varied diet, and a keep-out-of-reach-of-children warning, while disease prevention or treatment claims are prohibited. EFSA also updates procedural requirements that shape dossier readiness, including its January 2025 updated administrative guidance for applications on new nutrient sources (applicable to submissions from 1 February 2025) under the EU Transparency Regulation (EU) 2019/1381, which increases expectations on data completeness and public-facing submissions.

Competitive Landscape

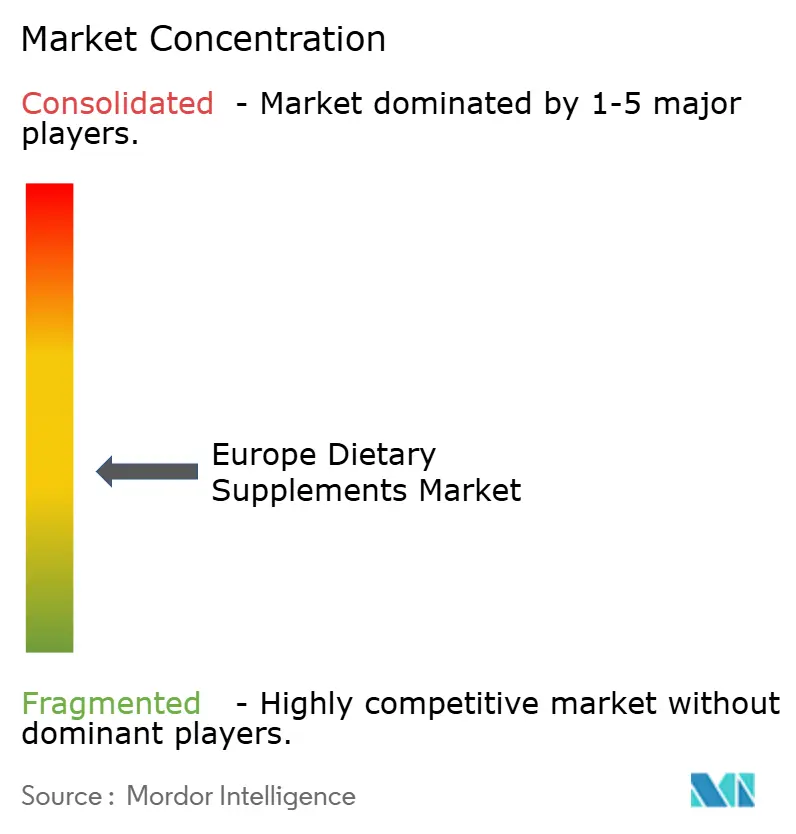

The European Dietary Supplements market is moderately fragmented. Multinational companies capitalize on economies of scale for procurement and regulatory compliance, while smaller, digitally-focused brands gain a competitive edge by quickly adapting formulas based on consumer feedback. Increased competition in the probiotics and beauty supplement segments has driven established firms to acquire specialized companies, strengthening their ingredient portfolios. This trend highlights a strategic shift in acquisitions, emphasizing both brand value and technological capabilities.

Furthermore, companies are increasingly adopting AI-driven assessment tools to offer personalized nutrition services. These tools generate critical consumer insights, which are then used to market vitamins and functional foods more effectively. By shifting to direct-to-consumer models, companies are reducing their dependence on traditional retail channels. This approach not only improves profit margins but also fosters stronger customer loyalty by delivering tailored solutions directly to consumers.

Emerging disruptors include suppliers of postbiotic ingredients and developers of next-generation probiotics. For instance, some are advancing formulations of Akkermansia muciniphila, supported by the strain's novel food approval in 2024. Smaller players are challenging incumbents by focusing on niche markets, such as menopause supplements, pediatric gummies, and sports nutrition for women and leveraging influencer marketing to build brand equity without relying on traditional advertising. DSM-Firmenich's April 2024 authorization for calcidiol monohydrate illustrates how ingredient innovation can establish strong competitive advantages, as the more bioavailable vitamin D form commands premium pricing and requires specialized manufacturing capabilities. Regulatory compliance remains a critical competitive factor, with the European Food Safety Authority's health claims process (Regulation 1924/2006) favoring brands that invest in clinical trials and thorough dossier preparation. Companies losing ground include those dependent on botanical ingredients, such as ashwagandha and St. John's wort, which are under safety scrutiny, and brands struggling to authenticate their supply chains amid growing concerns over counterfeits.

Europe Dietary Supplements Industry Leaders

-

Bayer AG

-

Haleon PLC

-

Sanofi S.A.

-

Vitabiotics Ltd.

-

Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory standardization work creates a portfolio opportunity in Europe as the European Commission plans to start a public consultation in Q3 2026 on harmonized Maximum Permitted Levels (MPLs) for vitamins and minerals in supplements and fortified foods. Because MPLs vary by Member State today, harmonization supports pan-European SKUs with more consistent dosing and claims-ready labeling, while also pushing higher-dose products toward compliance-friendly strengths and formats (including gummies and tailored daily packs) that suit pharmacy and online channels.

Novel food and evidence-led ingredient pipelines also remain a differentiation route as EFSA continues to publish safety conclusions that can unlock new supplement claims and formats under Regulation (EU) 2015/2283. Examples include EFSA's May 2026 positive safety opinion for beta-nicotinamide mononucleotide (NMN) at a daily intake of 300 mg, and EFSA NDA Panel conclusions in December 2025 that supported safe use levels for egg membrane collagen peptides (up to 500 mg/day) and specified-use astaxanthin novel food ingredients. These updates reinforce the commercial advantage for companies that can fund dossiers, align labeling early, and scale clinically substantiated positioning across multiple European markets.

Recent Industry Developments

- June 2026: Haleon was reported as a strategic bidder for Thorne, a US dietary supplement company, signaling ongoing interest among large consumer health players in expanding supplements capabilities through acquisition. The move highlights the value placed on established premium brands and science-led platforms that can be leveraged across pharmacy and digital channels.

- September 2025: Bayer launched Supradyn Mom and Supradyn Naturals Calcium+ in India, expanding its prenatal and maternal nutrition supplement portfolio with a focus on targeted life-stage needs. The rollout reinforces multinational players' emphasis on specialized formulations that can be adapted across markets where micronutrient supplementation is supported by public health guidance.

- October 2024: Oriflame Spain introduced a personalized nutrition supplement solution under its Wellosophy brand, extending beyond standard packs into more tailored regimens. The launch supports the shift toward individualized supplement plans, which aligns with subscription-based e-commerce and data-driven product selection strategies used across Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers finished dietary supplement products sold across Europe for oral consumption, including common formats like tablets, capsules, gummies, powders, and liquids. Values are counted as manufacturer-level revenues for supplements consumed to complement daily diets.

Scope exclusions: We exclude functional foods and prescription nutraceutical products, and we do not count adjacent meal-replacement or sports-performance powders when they are positioned as food-style nutrition.

Segmentation Overview

-

By Product Type

- Vitamins and Minerals

- Enzymes

- Herbal Supplements

- Proteins and Amino Acids

- Fatty Acids

- Probiotics

- Other Product Types

-

By Form

- Tablets

- Capsules and Softgels

- Powders

- Gummies

- Liquids

- Other Forms

-

By Consumer Group

- Men

- Women

- Kids/Children

-

By Health Application

- General Health and Wellness

- Bone and Joint Health

- Energy and Weight Management

- Gastrointestinal and Gut Health

- Immunity Enhancement

- Cardiovascular Health

- Diabetes Management

- Cognitive and Mental Health

- Skin, Hair and Nail Care

- Eye Health

- Other Health Applications

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Channels

- Direct Selling

- Other Distribution Channels

-

By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by aligning the Europe boundary, the product definition, and the regulatory context so the sizing does not mix food, medicine, and supplements. Public sources were used to ground the rules and health-claim constraints, such as the European Commission framework for food supplements, EFSA opinions on permitted claims, and national competent authority guidance where it clarifies labeling and maximum levels.

To build the demand backdrop, we relied on public health and population signals such as Eurostat demographic tables, WHO and OECD health statistics, and customs or trade summaries when cross-border flows were relevant. We also reviewed company annual reports, investor presentations, and credible press for pricing direction, channel shifts (pharmacy versus online), and portfolio mix changes, and then supported this with selective paid subscriptions for company financials, patents, and news. These sources are illustrative and not exhaustive, and many additional public documents were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how supplements are priced and sold across major European markets, and on confirming what is truly counted as a dietary supplement versus nearby nutraceutical and wellness items. We spoke with a mix of brand owners, contract manufacturers, ingredient suppliers, distributors, pharmacy-channel stakeholders, and online-led sellers across APAC, EMEA, and the Americas to test assumptions on mix, margins, and the pace of format shifts (for example, gummies).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | |

| Mid tier: 55% | Functional/Unit leaders: 33% | |

| Smaller Players: 17% | Managers: 54% |

Market-Sizing & Forecasting

The core model uses top-down logic where population by country, age mix, and category participation rates are translated into a supplement demand pool, then converted into value using typical consumption frequency and price points by format. To keep the result realistic, we corroborate totals with selective bottom-up checks, including sampled brand and channel price benchmarks, supplier and distributor channel checks, and a reasonableness roll-up using reported supplement revenue ranges from public filings.

Key inputs for this market include adult and elderly population counts, health-claim and compliance tightening that changes product availability, the pharmacy share versus online share, observed format shifts (capsules and tablets versus gummies and liquids), and the mix between vitamins and minerals versus botanicals and specialty products. Where bottom-up evidence is incomplete for smaller countries or niche formats, gaps are handled using conservative participation and price assumptions that are cross-checked with interview feedback before being carried into the final total.

For forecasting, we mainly use scenario analysis supported by a light multivariate regression on indicators such as aging rates, consumer health spending direction, and channel penetration. The final growth path is adjusted after primary conversations confirm whether price inflation, promotional intensity, and mix shift are expected to be the bigger drivers in the next cycle.

Data Validation & Update Cycle

Validation is done through multiple passes where our estimates are compared against independent signals, and then the biggest variances are investigated before sign-off. Checks include year-to-year growth sanity, country share stability, price and mix plausibility by format, and alignment with regulatory events that would reasonably slow or accelerate launches.

If material gaps are found, we re-contact relevant interviewees to confirm whether the change is real or caused by a definition mismatch. Reports are refreshed annually, and interim updates are made when large events occur, such as major regulatory shifts or abrupt pricing swings. Before delivery, an analyst completes a fresh pass to ensure the model reflects the latest public information and consistent assumptions.

Mordor Intelligence's Europe Dietary Supplement Market Size Compared With Other Published Estimates

It is normal to see different market values for Europe dietary supplements because studies do not always count the same products, channels, and countries, even when the titles look similar. The year used as the starting point, the currency treatment, and whether values are measured at manufacturer revenue or retail spending can also move the final number.

By tracking manufacturer-level revenues and refresh cadence across countries, Mordor Intelligence keeps the Europe dietary supplement total tied to finished supplement products and avoids mixing in functional foods or prescription-like nutraceuticals, which is a common boundary issue in this space.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.64 B (2026) | |

| Industry Database A | USD 37.61 B (2024) | Uses an earlier base year and a broader segmentation set that can pull in adjacent wellness and nutrition functions, and it is not always clear if values are retail-level or manufacturer-level across all countries. |

| Trade Journal B | USD 26.60 B (2024) | Counts by a different time window and may apply category groupings that blend specialty nutrition types with supplements, which can shift totals when gummies, powders, and application-led groupings are priced differently. |

Across the three numbers, the spread is mainly explained by definition edges, the year chosen for the headline value, and how pricing is applied across formats and channels. Our approach keeps the steps repeatable because the same demand indicators and pricing logic are applied country by country, and then rechecked against real-world channel signals before the final total is locked.

Key Questions Answered in the Report

What is the projected value of the Europe dietary supplements market in 2031?

It is forecast to reach USD 38.07 billion by 2031 based on an 8.23% CAGR.

Which product type currently leads sales across Europe?

Vitamins and minerals hold 51.31% share, making them the region’s dominant segment.

Which consumer group is growing fastest?

Children’s supplements are advancing at a 9.84% CAGR, outpacing all other cohorts.

Why are gummies gaining popularity over tablets?

Flavor masking, convenience, and format novelty drive a 9.21% CAGR for gummies, especially among kids and seniors.

Page last updated on: