United States Meat Extract Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

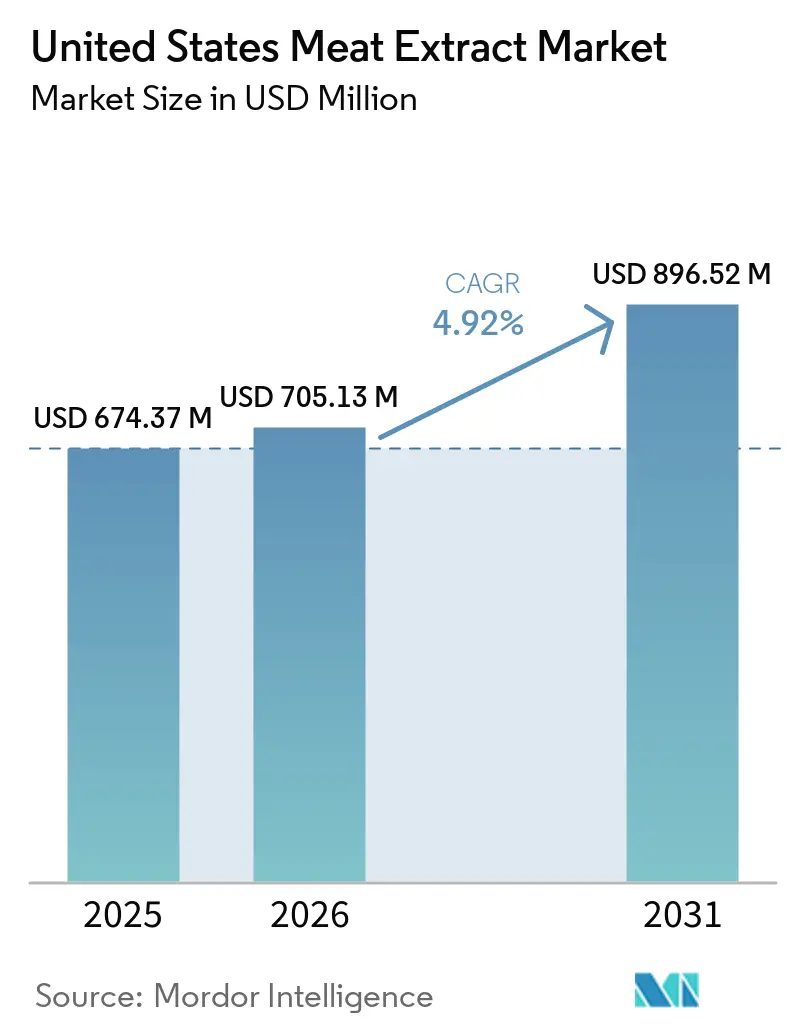

| Base Year Market Size (2025) | USD 674.37 Million |

| Market Size (2026) | USD 705.13 Million |

| Market Size (2031) | USD 896.52 Million |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

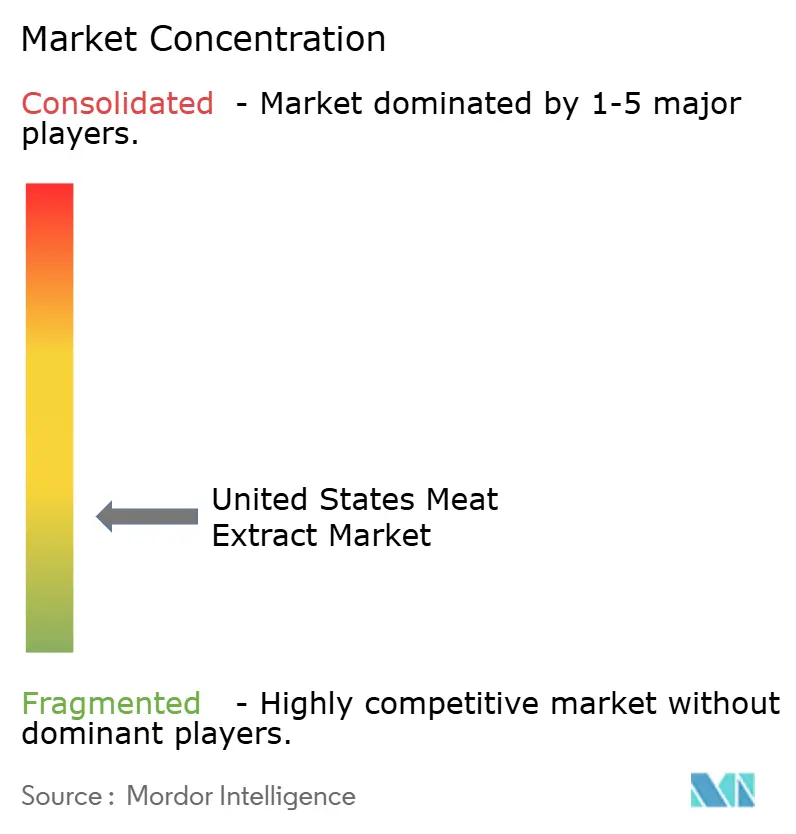

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Meat Extract Market Analysis by Mordor Intelligence

The United States meat extract market size is expected to grow from USD 674.37 million in 2025 to USD 705.13 million in 2026 and is forecast to reach USD 896.52 million by 2031 at 4.92% CAGR over 2026-2031. In the United States, the meat extract market is experiencing significant growth, driven by shifting consumer food preferences and advancements in scientific applications. This growth is supported by increasing demand for convenience and processed food products, the need for consistent flavor profiles across foodservice chains, and the expanding application of meat extracts in biotechnology, where they play a critical role in supporting culture media and the development of cultivated protein. According to the United States Department of Agriculture Economic Research Service, the per capita availability of red meat and poultry in the United States is projected to reach 227 pounds by 2026[1]Source: United States Department of Agriculture Economic Research Service, "Per capita availability of red meat and poultry projected higher in 2025 and 2026," ers.usda.gov. This anticipated availability ensures that United States producers maintain a steady supply of raw materials, providing a competitive advantage in terms of cost efficiency and traceability over regions such as Europe and the Asia-Pacific, which rely heavily on imports. Simultaneously, clean-label reformulation trends are reinforcing the importance of meat extracts as natural umami flavor enhancers, aligning with consumer demand for transparent, non-genetically modified organism flavor solutions. Collectively, these factors position meat extracts as a pivotal component bridging traditional culinary applications with cutting-edge protein innovation.

Key Report Takeaways

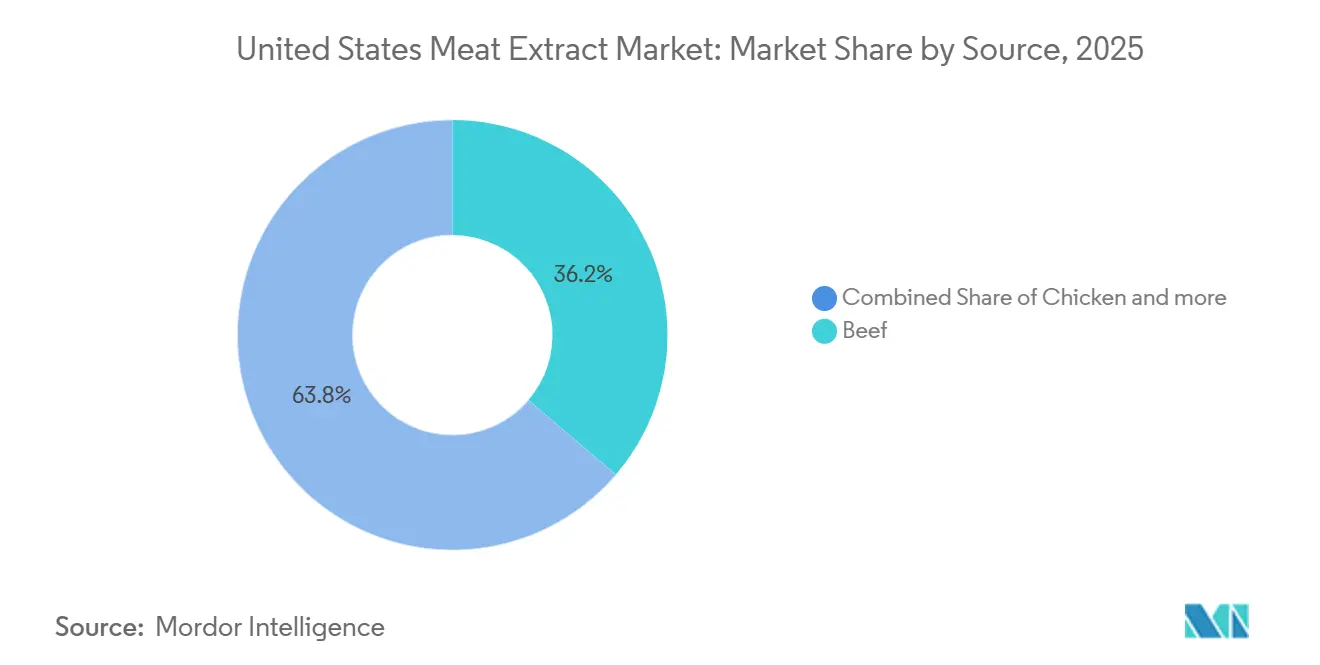

- By source, beef led the United States meat extract market with a share of 36.24% in 2025, while chicken is anticipated to register the fastest CAGR of 6.13% during 2026-2031.

- By form, powder retained 45.75% share in 2025, whereas liquid concentrate is forecast to expand at a 6.87% CAGR through 2031.

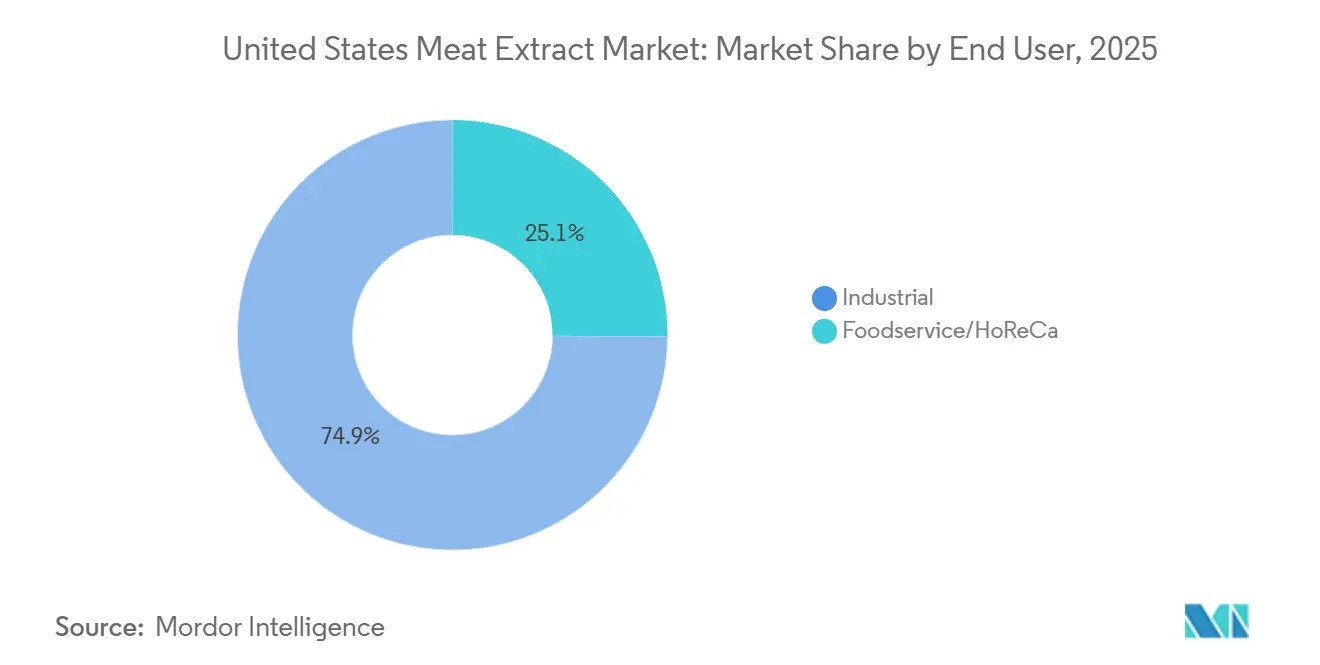

- By end user, industrial held 74.89% of 2025 revenue, but foodservice/HoReCa is expected to grow fastest at 7.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Meat Extract Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Busy lifestyles fuel consumption of convenience and ready-to-eat foods | +1.1% | National, concentrated in high-density metros (Northeast, West Coast, Sunbelt) | Short term (≤ 2 years) |

| Protein-centric wellness trends reinforce demand for meat-derived ingredients | +0.9% | National, strongest in fitness-oriented markets (West Coast, Southeast) | Medium term (2-4 years) |

| Growth of foodservice chains seeking consistent flavor profiles | +1.1% | National, led by Sunbelt and Mountain West markets with high QSR density | Short term (≤ 2 years) |

| Premium pet nutrition movement elevates use of meat-based flavor ingredients | +0.7% | National, premium adoption highest in Northeast and Pacific Northwest | Medium term (2-4 years) |

| Robust life sciences and research activities strengthen demand for culture media | +0.8% | National, concentrated in biotech hubs (Boston, San Francisco Bay Area, Research Triangle) | Long term (≥ 4 years) |

| Consumer preference for rich umami experiences boosts meat extract applications | +0.6% | National, with early gains in multicultural urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Busy lifestyles fuel consumption of convenience and ready-to-eat foods

As households in the United States increasingly prioritize convenience, the meat extract market is experiencing significant growth. This transition toward ready-to-eat and heat-and-serve products has amplified the demand for standardized flavor bases, primarily derived from meat extracts. According to the National Restaurant Association’s 2025 State of the Restaurant Industry report, United States foodservice sales are projected to reach USD 1.5 trillion by 2025, highlighting the substantial market opportunity[2]Source: National Restaurant Association, "Restaurant Industry Poised for Growth in 2025," restaurant.org. The rise of off-premises dining, including delivery, takeout, and drive-through services, is driving the need for shelf-stable, portion-controlled formats tailored for commercial kitchens. Simultaneously, the expansion of meal kit services and industrial soup production is placing dual pressure on suppliers to procure, compelling them to develop certified, application-specific product grades. These market dynamics underscore the critical role of meat extracts in meeting the evolving demands of modern food innovation.

Protein-centric wellness trends reinforce demand for meat-derived ingredients

The United States meat extract market is undergoing significant transformation, driven by the increasing adoption of protein-focused dietary trends such as the paleo diet, ketogenic diet, and high-protein dietary frameworks. These trends are normalizing the inclusion of meat-derived ingredients in packaged food products, which traditionally relied on synthetic flavoring agents. According to the International Food Information Council (IFIC), high-protein diets and mindful eating emerged as the most prevalent dietary patterns in the United States in 2025, with 23 percent and 19 percent of survey respondents, respectively, adhering to these practices[3]Source: International Food Information Council (IFIC), "2025 IFIC Food & Health Survey," ific.org. Meat extracts, known for their concentrated amino acid and glutamate profiles, align seamlessly with the functional nutrition narrative, enabling premium positioning within retail channels. Beyond their conventional culinary applications, these extracts are increasingly utilized in sports nutrition and meal replacement products, where they serve as authentic protein sources that comply with regulatory labeling requirements. This diversification into wellness-oriented applications not only broadens demand but also enhances the value proposition for producers, as consumers increasingly prefer natural and recognizable protein sources over processed alternatives. As a result, meat extracts are strategically positioned at the intersection of flavor, functionality, and health, reinforcing their relevance across both everyday dietary consumption and specialized nutrition categories.

Growth of foodservice chains seeking consistent flavor profiles

In the United States, the expansion of foodservice chains is significantly driving the demand for meat extracts. Foodservice operators are focused on delivering consistent flavor profiles across their extensive networks of quick-service restaurants (QSRs) and fast-casual dining establishments. By utilizing liquid concentrates and paste formats, these operators can standardize their offerings, reducing reliance on the variability of fresh-stock preparations and inconsistent kitchen skills. This approach ensures uniform taste while optimizing operational efficiency. According to the National Restaurant Association, the United States foodservice sector added over 200,000 net new jobs in 2025. This growth in operational capacity directly translates into increased procurement of meat extracts. Additionally, the rise of cloud kitchens and ghost-kitchen networks further accelerates this trend. These high-throughput operational models depend heavily on standardized inputs that integrate seamlessly with automated dispensing systems. Collectively, these developments emphasize the critical importance of flavor consistency in the modern foodservice industry, positioning meat extracts as indispensable tools for efficiently scaling menus and meeting diverse consumer expectations.

Premium pet nutrition movement elevates use of meat-based flavor ingredients

In the United States, the premium pet nutrition trend is driving significant changes in the meat extract market. As the humanization of pets continues to grow, there is an increasing demand for high-quality, meat-based flavor ingredients. Pet food manufacturers are now prioritizing human-grade or United States Department of Agriculture (USDA)-inspected protein inputs, which has raised the quality standards for commercially viable extracts and reduced opportunities for lower-specification suppliers. This shift allows producers of chicken and pork extracts catering to the pet food segment to also penetrate the human food market. This dual-market strategy enhances operational efficiency and justifies investments in regulatory compliance. As a result, meat extracts are gaining recognition not only as reliable flavor enhancers but also as functional protein sources, highlighting their importance in both pet nutrition and human food innovation. Additionally, this trend strengthens consumer confidence in product transparency, with traceability and inspection standards becoming critical factors in purchasing decisions. Overall, this movement positions meat extracts within a premium market segment, where quality assurance and cross-category versatility are key drivers of long-term growth potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating consumer shift toward plant-based and flexitarian diets | −0.5% | National, most pronounced in Pacific Coast and Northeast metros | Medium term (2-4 years) |

| Volatility in livestock and raw material prices | −0.4% | National; amplified in regions dependent on single-source protein (e.g., Midwest beef belt) | Short term (≤ 2 years) |

| Recurring avian influenza and livestock disease outbreaks | −0.5% | National, concentrated in major poultry-producing states (Iowa, Indiana, Ohio, Texas) | Short term (≤ 2 years) |

| Stringent food safety and regulatory compliance requirements | −0.3% | National, with heightened compliance costs in states with stricter labeling standards | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Accelerating consumer shift toward plant-based and flexitarian diets

In the United States, the meat extract market is encountering challenges due to the increasing consumer transition toward plant-based and flexitarian diets. This trend is reducing the market's reliance on animal-derived ingredients, particularly in retail categories such as soups, seasonings, and snack coatings. Although plant-based meat alternatives have not yet become direct substitutes, a more significant challenge arises from the growing investments in yeast extracts and fermentation-derived umami compounds. These alternatives replicate the depth of flavor without necessitating animal-based labeling. This indirect competition exerts pressure on profit margins and necessitates that meat extract producers differentiate themselves through authentic flavor profiles, verified protein content, and transparent clean-label declarations. As the flexitarian movement continues to influence product innovation, it will be crucial for meat extract suppliers to emphasize the natural origin and nutritional value of their products to retain buyer preference in the face of these evolving alternatives.

Recurring avian influenza and livestock disease outbreaks

In the United States meat extract market, recurring outbreaks of avian influenza and other livestock diseases present significant challenges, disrupting raw material supply pipelines and creating volatility within supply chains. Poultry extract production is particularly impacted, as disease outbreaks reduce flock sizes and restrict access to critical feedstock. The recent spillover of avian influenza into dairy cattle further emphasizes the systemic risk of cross-species disease transmission, raising concerns about concurrent disruptions to both poultry and bovine raw material sources. The turkey extract supply chain is especially vulnerable; the United States Department of Agriculture (USDA) livestock outlook for 2025 projects a loss of approximately 2 million turkeys due to Highly Pathogenic Avian Influenza (HPAI). This exacerbates constraints in an already niche raw-material segment and drives turkey prices significantly higher than those in the broader meat category. These challenges highlight the critical need for resilience strategies. Producers are increasingly adopting multi-species sourcing and geographic diversification to ensure supply continuity. Additionally, industrial buyers are placing greater emphasis on supply chain security and traceability, making robust risk management practices a key differentiator in fostering long-term supplier relationships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Beef Anchors Volume While Chicken Reshapes the Growth Curve

In 2025, beef solidified its position as the cornerstone of the United States meat extract market, commanding a 36.24% share. Its dominance is largely attributed to its integral role in soups, bouillons, and seasoning blends. Rich in glutamates, beef imparts a unique umami depth, cementing its status in traditional cooking. However, while beef leads the market, its supremacy is challenged by supply limitations and evolving consumer preferences. These changes are prompting industrial formulators to explore alternative sources. Although beef remains the primary driver of extract demand, its growth trajectory is slower compared to emerging sources, indicating a potential gradual decline in dominance as buyers evaluate authenticity alongside cost and availability considerations.

Conversely, chicken is emerging as the fastest-growing segment in the market, with a projected CAGR of 6.13% from 2026 to 2031. Its subtle flavor profile aligns well with lighter broths and Asian-inspired dishes, while its lower fat content enhances its appeal for nutraceutical and functional food applications. With abundant feedstock availability and widespread consumer acceptance, chicken extracts are increasingly favored across both culinary and wellness markets. This growth trajectory positions chicken as a critical driver of future market expansion, enabling producers to capitalize on rising demand across diverse categories while reinforcing beef's established role in the market.

By Form: Powder Leads on Volume, Liquid Concentrate Leads on Trajectory

In 2025, powder dominates the United States meat extract market, holding a 45.75% market share. This dominance is attributed to its shelf stability, cost-efficient transportation, and compatibility with dry-mix seasoning and instant noodle production lines, where controlling moisture levels is critical. Powder's established role in large-scale manufacturing reinforces its position as the cornerstone of extract demand. Concurrently, advancements in enzymatic hydrolysis are enhancing paste formats by introducing differentiated peptide fractions, which provide more complex and nuanced flavor profiles. These innovations enable manufacturers to justify premium pricing.

On the other hand, liquid concentrate is redefining the market trajectory as the fastest-growing form segment, with a CAGR of 6.87% forecasted for the period 2026–2031. Its growing appeal lies in its operational efficiencies, such as eliminating the need for reconstitution, integrating smoothly into automated dispensing systems, and reducing errors in high-throughput production environments. These features make liquid concentrate the preferred choice for national restaurant chains, ghost kitchen networks, and centralized production facilities that prioritize consistency across multiple locations. The segment's growth reflects a broader procurement trend toward continuous liquid systems, positioning liquid concentrate as a strategic driver of future market expansion.

By End User: Industrial Dominates, Foodservice Momentum Quickens

In 2025, industrial end users dominate the United States meat extract market, holding a substantial 74.89% share. This segment caters to a diverse array of applications, including soups, bouillons, and sauces, as well as ready meals, instant noodles, and snack seasonings. Additionally, it plays a pivotal role in nutraceuticals, baby food, pet food, and even biotechnology culture media. The segment's dominance is underscored by its wide-ranging demand, spanning both mainstream and niche products. Notably, pet food and biotechnology have emerged as influential sub-segments. The pet food industry is driving a trend toward premiumization, emphasizing authentic protein sourcing in its nutrition claims. Meanwhile, in biotechnology, there is a pronounced focus on standardized nitrogen content and traceability in growth media formulations. Collectively, these varied industrial applications solidify the segment's position as the largest and most stable demand driver, ensuring consistent procurement volumes and enduring relevance.

On the other hand, the foodservice sector, which includes Hotels, Restaurants, and Catering (HoReCa), is witnessing the fastest growth, projected to advance at a 7.01% CAGR from 2026 to 2031. This surge is largely attributed to a structural shift toward culinary outsourcing. National restaurant chains, cloud kitchens, and catering operators are increasingly turning to extract-based flavor systems, ensuring consistency across their outlets. Within this realm, liquid and specialty extracts hold particular value, seamlessly integrating into automated dispensing systems and catering to diverse, multicultural menu profiles. Furthermore, hotels and event caterers are expanding their demand for fish and niche extracts, aligning with evolving guest expectations. This rapid expansion positions the foodservice sector as the most dynamic segment, reshaping procurement strategies and presenting suppliers with lucrative opportunities to enhance demand through diverse portfolios and flavor-matching expertise.

Geography Analysis

High per capita meat consumption, a robust food-processing infrastructure, and an advanced foodservice economy bolster the United States' leadership in the meat extract market. This leadership is further solidified by the United States Department of Agriculture (USDA) and Food and Drug Administration (FDA) protocols, ensuring quality assurance and enhancing the competitive edge of domestic producers. For buyers in industrial and life sciences sectors, traceability and certification are paramount, making United States-origin extracts the top choice. The combination of a plentiful raw material supply and stringent regulations lays a strong foundation for large-scale, cost-competitive production, cementing the country's pivotal role in the region.

Regional consumption patterns reveal a diverse landscape. The Midwest and South lead in industrial extract usage, thanks to a concentration of soup, bouillon, and snack manufacturers. Meanwhile, the West Coast and Northeast are witnessing a surge in demand for premium and specialty extracts, buoyed by biotechnology hubs and diverse foodservice operators. Sunbelt states like Texas, Florida, and Arizona, with their rapidly expanding foodservice capacities, are translating population growth into heightened demand for liquid and paste concentrates. These regional trends showcase a harmonious coexistence of industrial scale and premium niches, presenting producers with opportunities to cater to both volume-driven and specialty markets.

However, supply-side challenges, such as recurring avian influenza outbreaks, create vulnerabilities, especially in poultry-producing states like the Upper Midwest and South. This underscores the need for diversification and resilient sourcing strategies. On an international note, trade flows between the United States and Mexico introduce another layer of demand. Collectively, these dynamics highlight United States intricate landscape, where scale, compliance, and adaptability are key to sustained competitiveness.

Competitive Landscape

In the United States meat extract market, competition is intense and fragmented. Global corporations such as Kerry Group and Symrise, recognized for their proprietary processing technologies, compete across multiple categories. At the same time, specialty ingredient companies like Essentia Protein Solutions and Proliant Health & Biologicals establish their competitive edge by focusing on specification precision, United States Department of Agriculture (USDA) certification, and traceability. As buyers in premium pet food and life sciences increasingly prioritize documented assays, microbial controls, and technical support, the competitive emphasis is shifting from price-per-kilogram to compliance and co-development.

A significant market opportunity exists at the intersection of culture-media-grade and conventional food-grade procurement. Only a limited number of suppliers possess the infrastructure to simultaneously serve both biopharmaceutical and food-industrial clients. However, those that do achieve dual-channel premium margins create a competitive advantage that is challenging for others to replicate. Global players are also expanding into traditional meat extract markets through adjacent technologies. For example, Kerry’s fermentation-based savory product portfolio and Ajinomoto’s taste-enhancement platforms demonstrate how major flavor companies are diversifying into alternatives that reduce the differentiation potential for generic-grade extracts. This trend highlights that innovation, rather than scale alone, will drive competitive advantage in the coming years.

Smaller regional competitors, such as Basic Food Flavors and Nikken Foods USA, remain effective in localized markets by offering customization and faster turnaround times than global corporations can typically provide. Their agility enables them to secure contracts in foodservice and industrial niches where responsiveness is more critical than global reach. Consequently, the competitive landscape is defined by a combination of global scale, specialized precision, and regional agility. Success increasingly depends on compliance credibility, advancements in adjacent technologies, and the ability to co-develop applications with buyers across a wide range of end-use categories.

United States Meat Extract Industry Leaders

-

Essentia Protein Solutions

-

International Dehydrated Foods, Inc.

-

Givaudan

-

Kerry Group

-

Nikken Foods USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Ajinomoto expanded its food solutions and savory ingredients operations by investing in biotechnology-based ingredient platforms. This initiative supported the development of advanced meat extracts and flavor-enhancing ingredients designed for United States food manufacturers.

- October 2025: Givaudan, a global leader in Taste and Wellbeing, announced the commencement of construction for its advanced liquids production facility in Reading, Ohio. This development reinforced the company's ongoing commitment to the North American market. The new facility, designed to complement Givaudan's existing operations, represented an initial investment of CHF 187 million (USD 215 million). Covering 24,000 square meters, the site was situated on a reserved land area exceeding 100,000 square meters, ensuring capacity for future expansion.

- May 2025: At the International Frankfurt Meat Industry Exhibition (IFFA) 2025, Essentia Protein Solutions launched its "Bring Back the Joy of Meat" campaign. The initiative highlighted how functional animal proteins, renowned for their gelling, binding, and emulsification properties, could effectively replace synthetic additives in the reformulation of processed meat products.

United States Meat Extract Market Report Scope

Meat extract is a concentrated substance derived from meat, typically beef or chicken, that captures the savory, umami-rich essence of meat in a shelf-stable form. It is widely used in cooking, food manufacturing, and microbiology laboratories as both a flavor enhancer and a nutrient source.

The United States meat extract market is segmented based on source, form, and end user. By source, the market is segmented into beef, pork, chicken, fish, turkey, and other sources. By form, the market is segmented into powder, paste, liquid concentrate, and other forms. By end users, the market is segmented into foodservice/HoReCa and industrial. The market forecasts are provided in terms of value (USD) and volume (tons).

| Beef |

| Pork |

| Chicken |

| Fish |

| Turkey |

| Other Sources |

| Powder |

| Paste |

| Liquid Concentrate |

| Other Forms |

| Foodservice/HoReCa | |

| Industrial | Soups and Bouillons |

| Sauces and Dressings | |

| Ready Meal and Instant Noodles | |

| Snack and Seasonings | |

| Nutraceuticals and Dietary Supplements | |

| Baby Food | |

| Pet Food | |

| Biotechnology and Culture Media | |

| Other Industries |

| By Source | Beef | |

| Pork | ||

| Chicken | ||

| Fish | ||

| Turkey | ||

| Other Sources | ||

| Form | Powder | |

| Paste | ||

| Liquid Concentrate | ||

| Other Forms | ||

| End User | Foodservice/HoReCa | |

| Industrial | Soups and Bouillons | |

| Sauces and Dressings | ||

| Ready Meal and Instant Noodles | ||

| Snack and Seasonings | ||

| Nutraceuticals and Dietary Supplements | ||

| Baby Food | ||

| Pet Food | ||

| Biotechnology and Culture Media | ||

| Other Industries | ||

Key Questions Answered in the Report

What is the current size of the United States meat extract market?

The United States meat extract market was valued at USD 674.37 million in 2025 and is projected to reach USD 896.52 million by 2031, growing at a CAGR of 4.92% between 2026 and 2031.

Which source segment dominates the market?

Beef is the largest source segment, holding a 36.24% share in 2025. Its entrenched role in soups, bouillons, and seasoning formulations ensures it remains the anchor category despite gradual diversification toward other proteins.

Which form leads the market in 2025?

Powder is the largest form segment, accounting for 45.75% of the market in 2025. Its shelf stability, cost efficiency, and compatibility with dry-mix manufacturing lines secure its dominance in high-volume industrial applications.

Which end-user segment dominates the market?

Industrial users lead the market, holding a 74.89% share in 2025. This includes applications in soups, sauces, ready meals, instant noodles, pet food, and biotechnology culture media, where extract demand is embedded in large-scale production.

Which end-user segment is growing the fastest?

Foodservice/HoReCa is the fastest-growing end-user segment, advancing at a CAGR of 7.01% from 2026–2031. Growth is driven by restaurant chains, cloud kitchens, and catering operators seeking standardized flavor systems for consistency across outlets.

Page last updated on: