Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

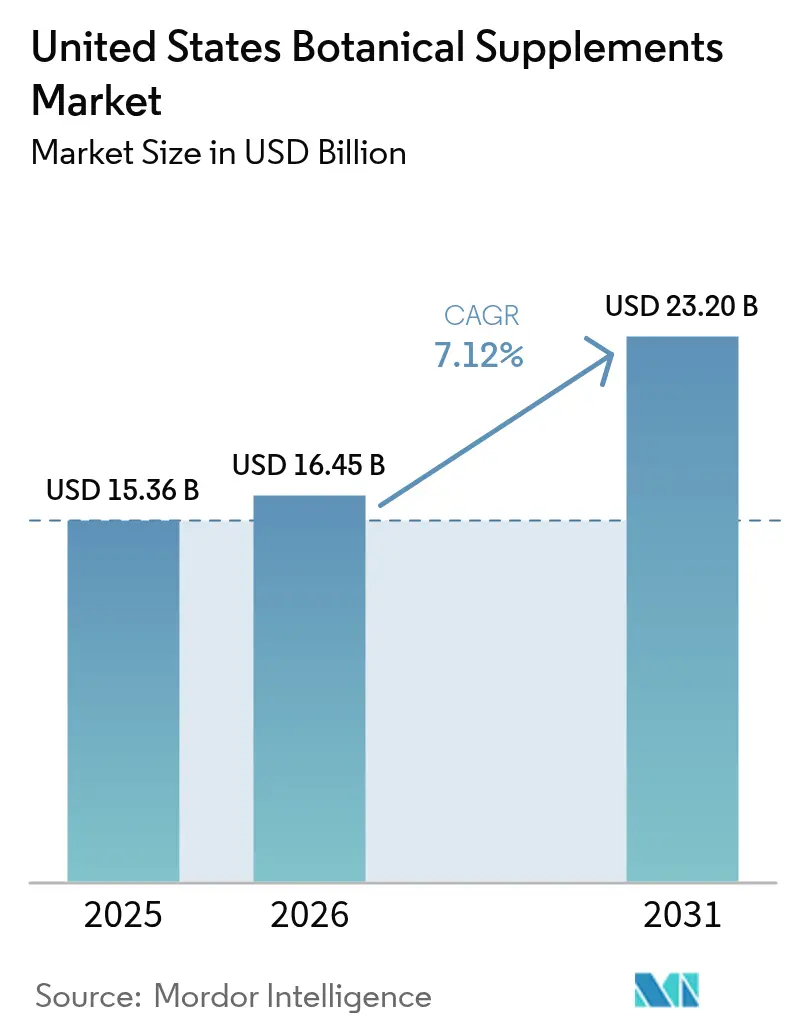

| Base Year Market Size (2025) | USD 15.36 Billion |

| Market Size (2026) | USD 16.45 Billion |

| Market Size (2031) | USD 23.2 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

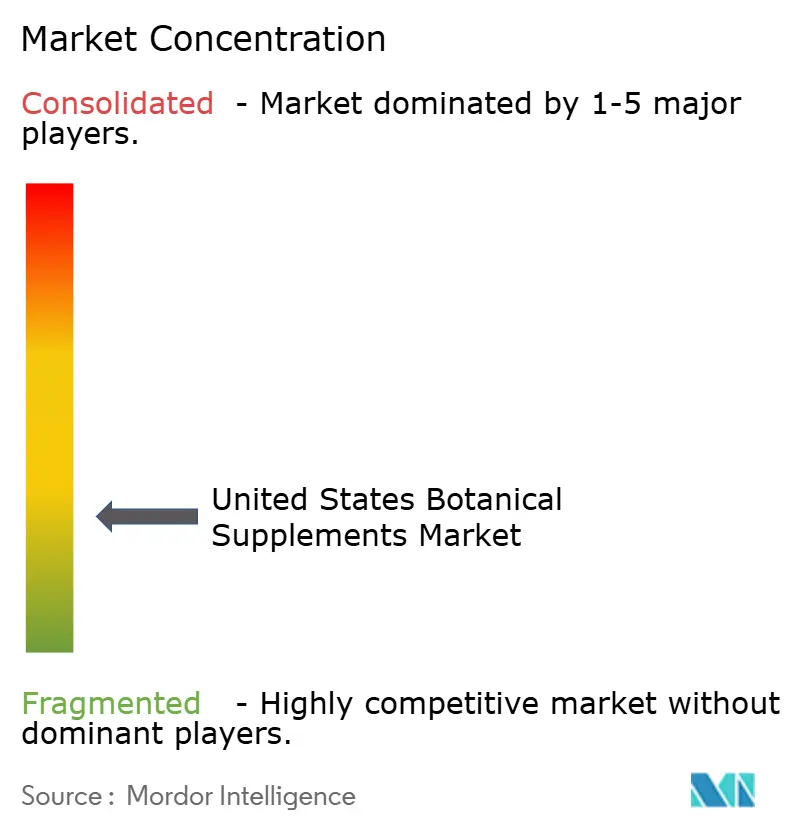

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Botanical Supplements Market Analysis by Mordor Intelligence

The United States botanical supplements market size is expected to grow from USD 15.36 billion in 2025 to USD 16.45 billion in 2026 and is forecast to reach USD 23.2 billion by 2031 at 7.12% CAGR over 2026-2031. The market growth is driven by increased consumer confidence in scientifically validated plant-based therapeutics, expanded clinical research supporting ingredients like ashwagandha and curcumin, and enhanced regulatory oversight. Consumer preferences are shifting toward products that combine traditional botanical knowledge with scientific validation, influenced by wellness trends and social media. The FDA's guidelines on New Dietary Ingredient notifications and the Botanical Drug Pathway have strengthened quality standards while establishing credibility for companies with comprehensive quality control systems[1]Source: Food and Drug Administration, “New Dietary Ingredient Notifications Draft Guidance,” fda.gov. The supply chain challenges for imported botanical materials have highlighted the advantages of vertically integrated companies that can ensure product authenticity and potency.

Key Report Takeaways

- By form, tablets led with 33.74% of the United States botanicals market share in 2025, while gummies and chews are forecast to expand at a 8.88% CAGR through 2031.

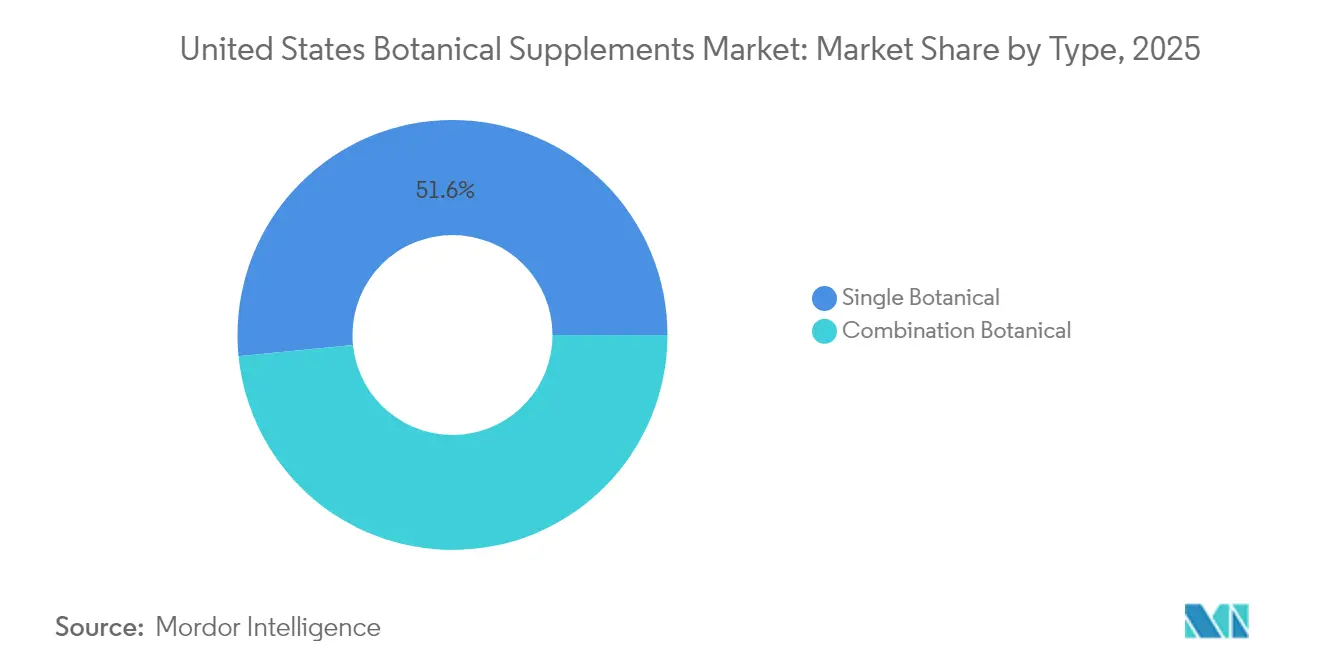

- By type, single botanicals accounted for 51.58% of the United States botanicals market size in 2025, whereas combination botanicals are projected to grow at an 8.63% CAGR to 2031.

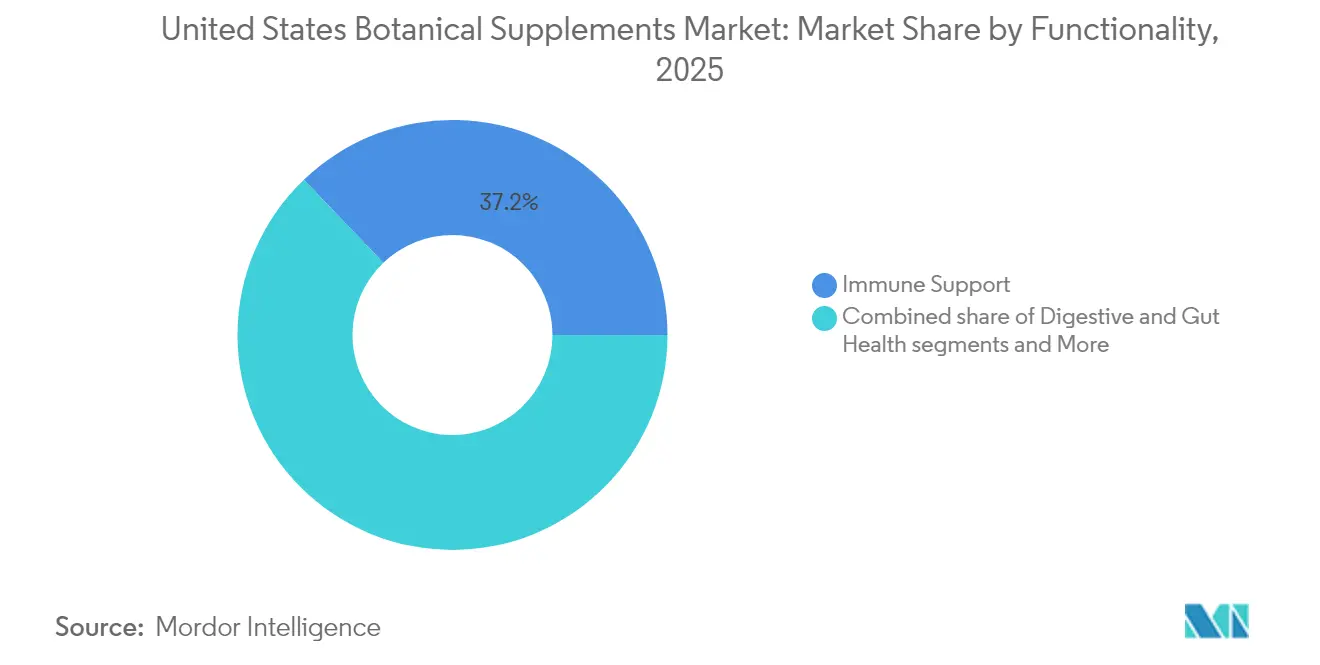

- By functionality, immune support captured 37.15% of the United States botanicals market size in 2025, and stress-sleep-cognitive health is advancing at an 8.05% CAGR to 2031.

- By distribution channel, specialty and health stores held 35.66% revenue share in 2025; online retail records the fastest projected CAGR at 7.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Botanical Supplements Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing consumer interest in holistic wellness approaches and traditional medicinal practices | +1.8% | National, with concentration in health-conscious metropolitan areas | Medium term (2-4 years) |

| Endorsement of herbal products by public figures and social media influencers | +0.9% | National, with higher impact in younger demographics | Short term (≤ 2 years) |

| Consumer preference shifting toward plant-based ingredients as alternatives to synthetic compounds | +1.5% | National, with premium market concentration in coastal regions | Long term (≥ 4 years) |

| Expanding elderly demographic seeks natural alternatives for managing chronic health conditions | +1.2% | National, with concentration in aging population centers | Long term (≥ 4 years) |

| Scientific research and clinical studies demonstrate the effectiveness of botanical ingredients | +1.1% | National, with institutional adoption in healthcare systems | Medium term (2-4 years) |

| Enhanced Regulatory Oversight and FDA Support for Botanical Ingredient Standards | +1.0% | National, with emphasis on regions housing major supplement manufacturers and research institutions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer interest in holistic wellness approaches and traditional medicinal practices

The integration of traditional medicine with modern wellness practices is driving significant demand for botanical supplements, as consumers increasingly seek alternatives to conventional healthcare approaches. According to the Council for Responsible Nutrition Survey 2023, 74% of adults in the United States use dietary supplements[2]Source: Council for Responsible Nutrition, "2023 CRN Consumer Survey on Dietary Supplements", www.crnusa.org. Companies are incorporating centuries-old Ayurvedic and Chinese medicine principles while adhering to stringent modern quality standards and safety protocols, enabling them to position products in premium market segments. Rising disposable income levels in health-conscious urban areas continue to support market expansion, while FDA recognition of botanical drugs strengthens their credibility and acceptance among healthcare professionals. Companies that effectively demonstrate product authenticity through transparent sourcing practices, documented supply chains, and scientifically proven effectiveness gain better retail shelf placement and enhanced online visibility across digital commerce platforms and social media channels.

Endorsement of herbal products by public figures and social media influencers

Social media is driving the mainstream adoption of botanical products, particularly among younger consumers who value peer recommendations over traditional medical advice. Influencer endorsements on social platforms have increased product awareness and sales, with platforms like Instagram and TikTok becoming primary channels. This trend presents both opportunities and challenges, as regulators increase their scrutiny of health claims made on social media. The FDA's monitoring of supplement marketing has intensified, requiring companies to implement comprehensive compliance protocols. Companies that effectively balance influencer partnerships with FDA compliance requirements gain competitive advantages through established legal frameworks and transparent marketing practices. Celebrity endorsements have notably increased the popularity of premium botanical products, such as functional gummies, which offer both social media appeal and ease of use. The influence-driven market segment remains volatile, with product demand shifting based on trending health topics rather than established clinical evidence, creating uncertainty in long-term market stability and consumer retention.

Consumer preference shifting toward plant-based ingredients as alternatives to synthetic compounds

The growing preference for plant-based products has expanded into the supplements market, as consumers thoroughly examine ingredient sources, production methods, and supply chain transparency. This trend drives significant advancements in botanical extraction technologies and increases demand for formulations with minimal synthetic additives. Companies are adopting improved extraction methods, including supercritical CO2 extraction and ultrasound-assisted techniques, that maintain bioactive compounds without chemical solvents to address consumer demands for processing purity. Organic certification, sustainable sourcing practices, and fair trade partnerships have become key market differentiators, with consumers accepting higher prices for botanicals meeting stringent environmental and ethical criteria. The plant-based trend also increases interest in traditional medicine botanicals from regions like Asia, Africa, and South America, creating opportunities for companies that effectively introduce and educate consumers about these ingredients through detailed documentation, scientific validation, and transparent sourcing information.

Expanding elderly demographic seeks natural alternatives for managing chronic health conditions

The United States' aging population drives demand for botanical supplements addressing age-related health concerns with minimal side effects compared to conventional pharmaceuticals. According to the United States Census Bureau, the population aged 65 and over increased by 9.4% from 2020 to 2023, reaching approximately 59.2 million people nationally[3]Source: United States Census Bureau, "Older Population Grew in Nearly All U.S. Metro Areas", census.gov. This growth occurred across all U.S. metropolitan areas, except Eagle Pass, Texas. Older consumers seek botanical supplements supporting cognitive function, memory enhancement, mental clarity, joint health, mobility, flexibility, and immune system maintenance. This demand has expanded product development in these categories. Healthcare providers increasingly accept botanical supplements as complementary treatments for chronic conditions and overall health maintenance, enhancing their credibility among older adults who previously used only prescription medications. This demographic's disposable income and emphasis on preventive healthcare have encouraged the development of premium botanical products targeting specific age-related conditions, including inflammation, bone density, and cardiovascular health. Manufacturers are also creating new delivery formats, including liquid extracts, easy-to-swallow capsules, sublingual drops, and powder formulations, to address the physical limitations and preferences of elderly consumers who struggle with traditional supplement forms.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Risk of contamination and adulteration in raw botanicals hinders growth | -1.3% | National, with higher impact on imported botanical supply chains | Short term (≤ 2 years) |

| Seasonal and regional variability affects raw botanical supply | -0.8% | National, with concentration in agricultural regions | Medium term (2-4 years) |

| Presence of counterfeit products restricts growth | -0.7% | National, with higher impact in online retail channels | Short term (≤ 2 years) |

| Competition from alternative supplements hinders growth | -0.9% | National, with concentration in urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Risk of contamination and adulteration in raw botanicals hinders growth

Quality control challenges in botanical supply chains create significant barriers to market expansion, as contamination and adulteration issues affect consumer confidence and regulatory compliance. The industry faces systemic quality concerns, particularly regarding botanical extract overdilution, where manufacturers use excessive excipients and resell spent biomass. With FDA inspections covering only 5% of known dietary supplement facilities annually, enforcement gaps allow substandard products to enter the market. Botanicals sourced from regions with limited quality control infrastructure face higher contamination risks, requiring companies to make substantial investments in testing and verification systems. Growing consumer awareness of adulteration issues has increased demand for third-party certifications and transparent supply chain documentation, benefiting companies with comprehensive quality assurance programs. In response, the industry is adopting new authentication technologies, such as DNA barcoding and spectroscopic analysis, which increase operational costs but enable product differentiation.

Seasonal and regional variability affects raw botanical supply

Climate-dependent botanical harvests create supply chain volatility, constraining market growth and increasing pricing uncertainty for manufacturers and consumers. Supply disruptions in key botanicals demonstrate this vulnerability, as seen in the 2024 ginger production decline in Peru that created global supply gaps and affected product availability across multiple regions. Climate change intensifies these challenges, with research showing potential disruption of natural pollination processes, such as the risk of vanilla plants becoming separated from their pollinators, which could significantly impact future production capabilities and market stability. The seasonal variability particularly affects single botanical products, which lack ingredient substitution options when primary sources become scarce, leading to increased production costs and potential market shortages. Companies are addressing these challenges by diversifying their sourcing locations across different geographical regions and implementing vertical integration strategies to gain better control over their supply chains, though these approaches require substantial capital investment and long-term planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Single Botanicals Dominate Despite Combination Growth

Single botanicals account for 51.58% of the United States botanicals market in 2025, as consumers increasingly gravitate toward products with transparent and easily understandable benefit statements. Extensive scientific research and clinical validation supporting key ingredients like ashwagandha, elderberry, and turmeric continue to drive consistent consumer repurchases. While combination products represent a smaller market share, they are projected to grow at an 8.63% CAGR by offering comprehensive adaptogenic blends that simultaneously address multiple health concerns, including stress management, digestive wellness, and immune system support in single formulations.

Single-ingredient products provide manufacturers with streamlined FDA compliance processes compared to multi-component formulations, which must navigate more complex notification requirements and regulatory frameworks. However, combination formulas enable retailers to enhance sales performance through strategically positioned multi-benefit products and potentially higher average order values in the United States botanicals market. Manufacturers develop sophisticated targeted combinations such as ashwagandha with L-theanine and magnesium for comprehensive stress management, or curcumin with Boswellia for complete joint support, effectively addressing consumers' increasingly complex and interconnected health concerns.

By Form: Tablets Lead While Gummies Transform Delivery

Tablets account for 33.74% of the United States botanicals market share in 2025, driven by their cost efficiency and precise dosing capabilities. The tablet format offers manufacturers significant advantages in production scalability and shelf stability. They remain the primary format for curcumin and herbal extracts that require standardized high-milligram doses, particularly for ingredients sensitive to moisture and oxidation. The gummies and chews segment is experiencing rapid growth at a 8.88% CAGR through 2031, as manufacturers address bioavailability challenges and reduce sugar content while maintaining palatability and consumer appeal.

Advancements in gummy production incorporate pectin bases, vegan colorants, and microencapsulated active ingredients that maintain stability during high-temperature manufacturing processes. These technological improvements enable better nutrient retention and enhanced absorption rates. Capsules and softgels maintain their market position through features such as odor-masking coatings and immediate-release shells, offering superior protection for volatile compounds and oils. Powder formats attract fitness enthusiasts who incorporate adaptogens into their smoothies, providing flexibility in serving size and blend customization. The diverse range of delivery formats in the United States botanicals market accommodates various consumer preferences and daily routines, from convenience-oriented users to those seeking specific therapeutic benefits.

By Functionality: Immune Support Leads as Stress Management Accelerates

Immune products accounted for 37.15% of the United States botanicals market size in 2025, driven by increased consumer health awareness following COVID-19. The category prominently features elderberry, echinacea, and beta-glucan formulations, with elderberry demonstrating particular market strength. An MDPI meta-analysis validated elderberry's effectiveness in reducing respiratory infection duration through enhanced immune response mechanisms and decreased inflammatory markers. Consumer demand for these immune-supporting botanicals continues to rise, particularly in supplement and functional food applications.

The stress-sleep-cognitive health segment is projected to grow at 8.05% CAGR, supported by comprehensive workplace wellness programs and burnout prevention initiatives across industries. Ashwagandha is the main ingredient in mood supplements, with clinical studies documenting its significant cortisol reduction benefits and stress-alleviating properties. Research indicates improved sleep quality and reduced anxiety levels among regular users. Digestive health supplements combining probiotics with traditional botanicals like peppermint or ginger are expanding their presence in mainstream grocery retail channels. This expansion includes new product formats such as gummies and beverages, increasing consumer accessibility and driving sustained growth in the United States botanicals market.

By Distribution Channel: Specialty Stores Anchor While E-commerce Surges

Specialty and health stores accounted for 35.66% of revenue in 2025 through their highly trained staff and carefully selected product assortments that build consumer trust in high-potency botanical products. These brick-and-mortar retailers strengthen customer loyalty by conducting comprehensive live seminars and educational workshops on botanical benefits, therapeutic applications, and proper usage guidelines. Online sales are projected to grow at a 7.74% CAGR through 2031 as consumers increasingly prefer the convenience of doorstep delivery, detailed product information, and verified customer reviews.

Amazon's 2024 policy requiring Certificates of Analysis for supplements eliminates substandard sellers while benefiting established brands that invest in rigorous quality testing and compliance measures. Direct-to-consumer websites gather extensive first-party consumer data and combine subscription services with personalized wellness coaching programs. While mass supermarkets maintain their presence in entry-level botanicals, they continue to lose market share in premium and clinically validated segments of the United States botanicals market due to limited product expertise and specialized inventory.

Geography Analysis

Urban coastal areas, with their affluent populations and concentrated wellness retailers, are fueling a surge in botanical spending. Notably, California and New York, together, rake in almost a third of the country's specialty store revenue. These states prominently feature innovative functional beverages infused with adaptogens, which are gaining popularity for their stress-relieving and health-boosting properties. The dense network of wellness-focused retailers in these regions further supports the growth of premium botanical products.

As online education and telehealth endorsements boost botanical awareness, Midwestern and Southern states emerge as prime expansion territories. While Texans and Floridians embrace elderberry syrups for colds and turmeric capsules for joint health, they exhibit a heightened price sensitivity compared to their coastal counterparts. However, increasing consumer literacy about the benefits of botanicals in these regions is gradually driving demand, presenting significant opportunities for market players to expand their footprint.

State-specific regulatory intricacies come into play, with Utah and Colorado adding extra registration layers, inflating compliance costs. These additional requirements often necessitate higher investments in regulatory expertise and documentation. Manufacturers strategically set up production near New Jersey and Wisconsin's established pharmaceutical hubs, tapping into their advanced analytical labs and skilled workforce to streamline operations. As logistics improve and e-commerce deepens, regional availability gaps shrink, enabling broader access to botanical products. This trend is accelerating the growth and adoption of the U.S. botanicals market across diverse regions.

Competitive Landscape

The United States botanicals market is fragmented, creating significant opportunities for market consolidation and the development of specialized niche products. Prominent players in the market include Amway Corporation, Herbalife International of America Inc., Harbin Pharmaceutical Group, and Nestle S.A. Major companies such as Otsuka Pharmaceutical Co., Ltd, and Nestle S.A. maintain their market positions through extensive distribution networks, established brand presence, and substantial retail footprints. Meanwhile, newer companies differentiate themselves through innovations in ingredient sourcing, advanced product formulations, enhanced delivery formats, and comprehensive scientific validation processes.

The market's competitive dynamics are continuously evolving as pharmaceutical companies enter through strategic acquisitions and partnerships, bringing substantial financial resources, advanced research capabilities, and extensive regulatory expertise. Companies now compete primarily on quality assurance and supply chain transparency, investing heavily in vertical integration strategies and sophisticated testing technologies to minimize contamination risks and ensure product consistency. The integration of advanced technologies, including artificial intelligence for comprehensive safety monitoring and blockchain systems for end-to-end supply chain verification, is fundamentally reshaping competitive advantages through enhanced consumer trust and stringent regulatory compliance.

Additionally, direct-to-consumer business models enable smaller companies to effectively compete with established brands by offering highly specialized products, customized formulations, and personalized customer experiences that extend beyond traditional retail capabilities. This shift in distribution strategy has created new opportunities for market penetration and customer engagement.

United States Botanical Supplements Industry Leaders

-

Amway Corporation

-

Herbalife International of America, Inc.

-

Harbin Pharmaceutical Group

-

Nestlé S.A (Nature's Bounty)

-

NOW Foods (NOW Health Group, Inc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: VIVAZEN introduced its latest offering: Botanical Gummies. These gummies provide a delicious and convenient means to bolster energy, enhance focus, promote relaxation, and uplift mood. Each product is crafted with active botanical ingredients, ensuring a delightful taste without any unpleasant aftertaste.

- January 2025: iHerb expanded its digital presence by launching a storefront on the Albertsons Companies platform in the United States. This expansion allows iHerb to access a broader customer base through Albertsons' retail network, offering consumers access to iHerb's product portfolio via the Albertsons digital marketplace.

- December 2024: Himalaya Wellness, a herbal and plant-based supplements and personal care brand, has introduced a new 28-count PartySmart bottle. The expanded packaging format for their herbal formula provides customers with greater flexibility for home storage, social gatherings, and family sharing.

- February 2024: Herbalife introduced nutrition companion product combinations in the United States, designed for individuals using GLP-1 weight-loss medications. The company offers these products in both Classic and Vegan variants.

United States Botanical Supplements Market Report Scope

The United States botanical supplements market is segmented by form into powdered supplements, capsules and tablets, and other forms. The market is also segmented by distribution channel into supermarket/hypermarket, pharmacies/ drug stores, online retail stores, and other distribution channels.

By Type

| Single Botanical | Turmeric |

| Cannabidiol | |

| Mushrooms | |

| Ashwagandha | |

| Psyllium | |

| Elderberry | |

| Apple Cider Vinegar | |

| Cranberry | |

| Others | |

| Combination Botanical |

By Form

| Tablets |

| Capsules/Softgels |

| Gummies and Chews |

| Powders |

| Others |

By Functionality/Health Benefits

| Digestive and Gut Health |

| Stress, Sleep and Cognitive Health |

| Immune Support |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retailers |

| Other Distribution Channels |

| By Type | Single Botanical | Turmeric |

| Cannabidiol | ||

| Mushrooms | ||

| Ashwagandha | ||

| Psyllium | ||

| Elderberry | ||

| Apple Cider Vinegar | ||

| Cranberry | ||

| Others | ||

| Combination Botanical | ||

| By Form | Tablets | |

| Capsules/Softgels | ||

| Gummies and Chews | ||

| Powders | ||

| Others | ||

| By Functionality/Health Benefits | Digestive and Gut Health | |

| Stress, Sleep and Cognitive Health | ||

| Immune Support | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Health Stores | ||

| Online Retailers | ||

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current value of the United States botanicals market?

The market reached USD 16.45 billion in 2026 and is forecast to rise to USD 23.2 billion by 2031.

Which form factor leads sales today?

Tablets hold the largest share at 33.74% of United States botanicals market share, favored for dose accuracy.

Why are gummies growing so quickly?

Gummies post a 8.88% CAGR because they combine flavor, convenience, and social media appeal while now delivering clinically relevant doses.

Which functionality segment is expanding the fastest?

Stress-sleep-cognitive health products lead growth at an 8.05% CAGR as workplace wellness and mental health awareness rise.

Page last updated on: