Mental Health Clinical Trials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

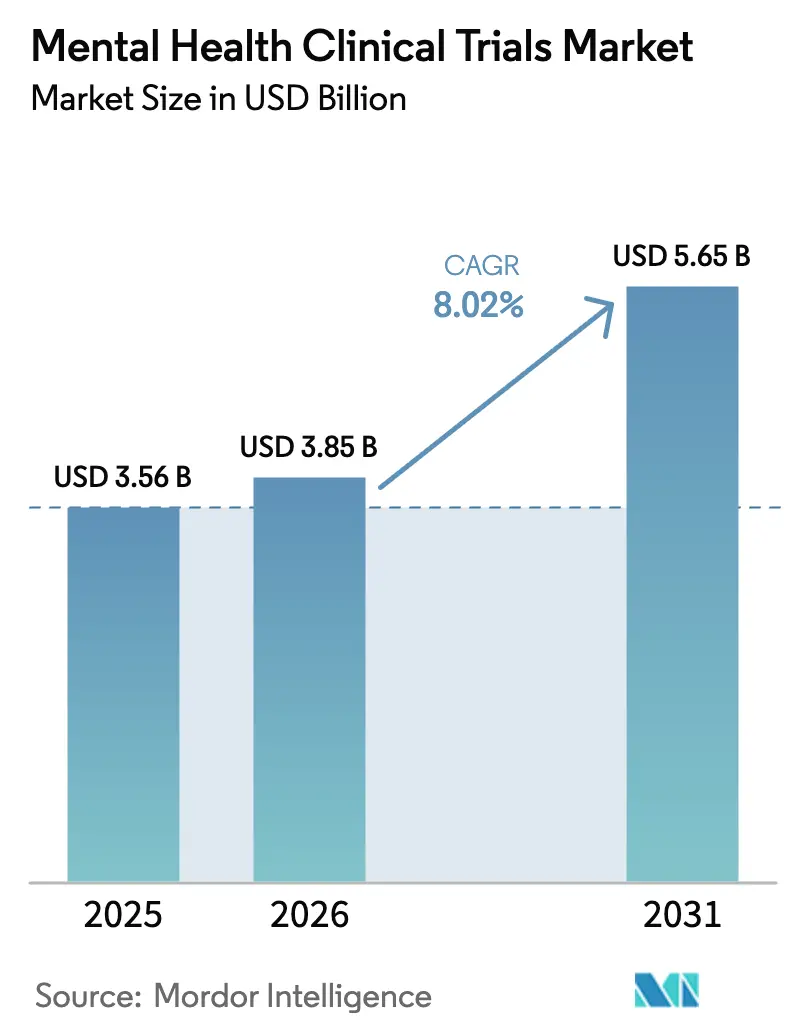

| Market Size (2026) | USD 3.85 Billion |

| Market Size (2031) | USD 5.65 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

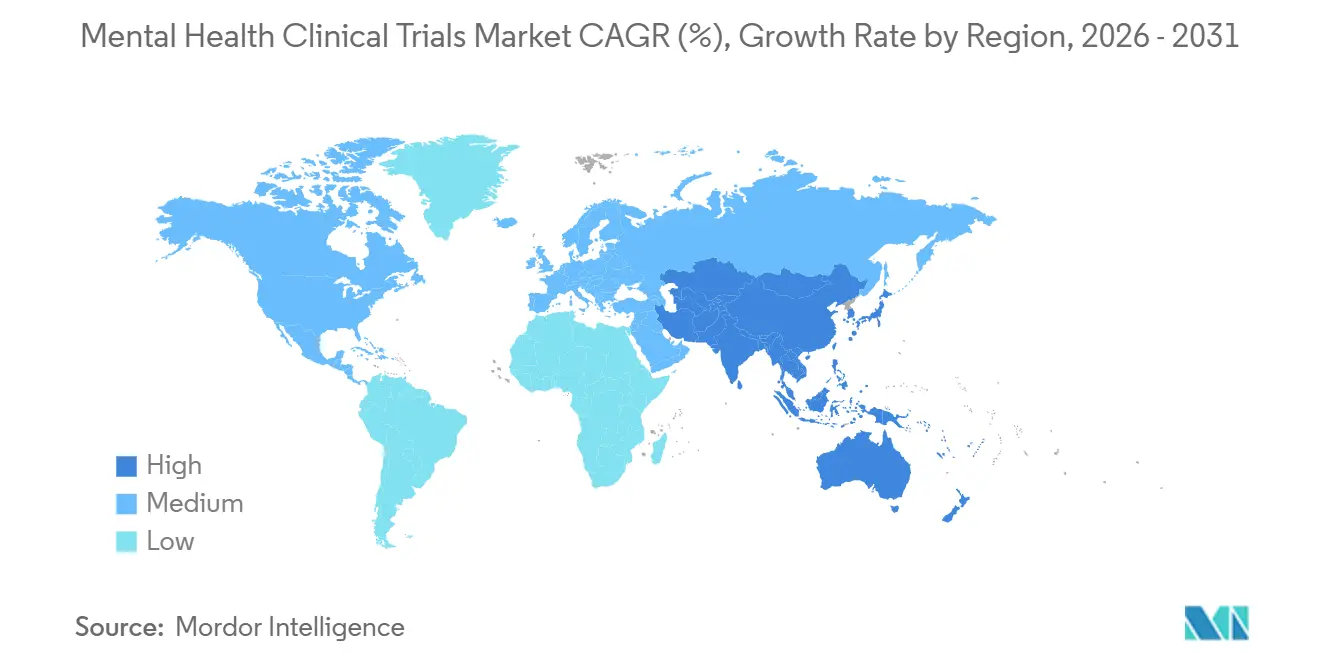

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

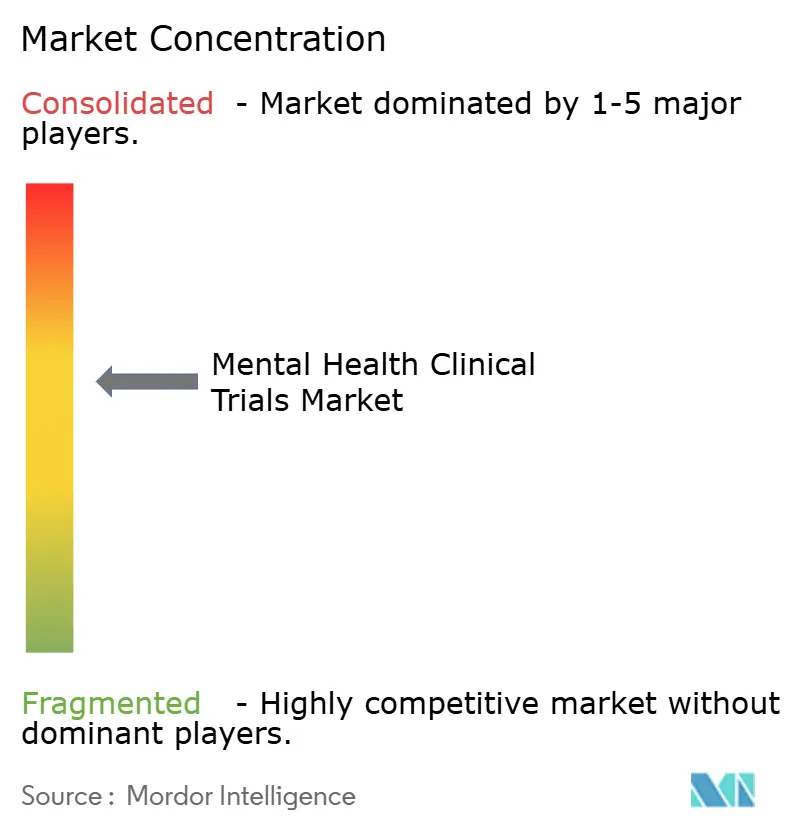

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mental Health Clinical Trials Market Analysis by Mordor Intelligence

The mental health clinical trials market size is projected to expand from USD 3.56 billion in 2025 and USD 3.85 billion in 2026 to USD 5.65 billion by 2031, registering a CAGR of 8.02% between 2026 to 2031. Sponsor appetite for adaptive platform protocols, the U.S. Food and Drug Administration’s (FDA) fast-track designations for novel mechanisms, and employer demand for evidence-based well-being benefits are converging to accelerate cycle times and expand indication breadth. Breakthrough approvals—such as Bristol Myers Squibb’s muscarinic-modulator Cobenfy—and regulatory rejections—such as the FDA’s August 2024 decision on MDMA for post-traumatic stress disorder—signal that regulators will green-light differentiated science while still requiring reproducible safety profiles. Venture funding for psychedelic programs, decentralized trial guidance that legitimizes telehealth assessments, and NIH’s USD 2.9 billion mental-health budget continue to widen the pipeline. Meanwhile, dropout rates averaging 30% in depression and 40% in schizophrenia inflate per-patient costs, forcing sponsors to over-enroll and adopt AI-driven retention interventions.

Key Report Takeaways

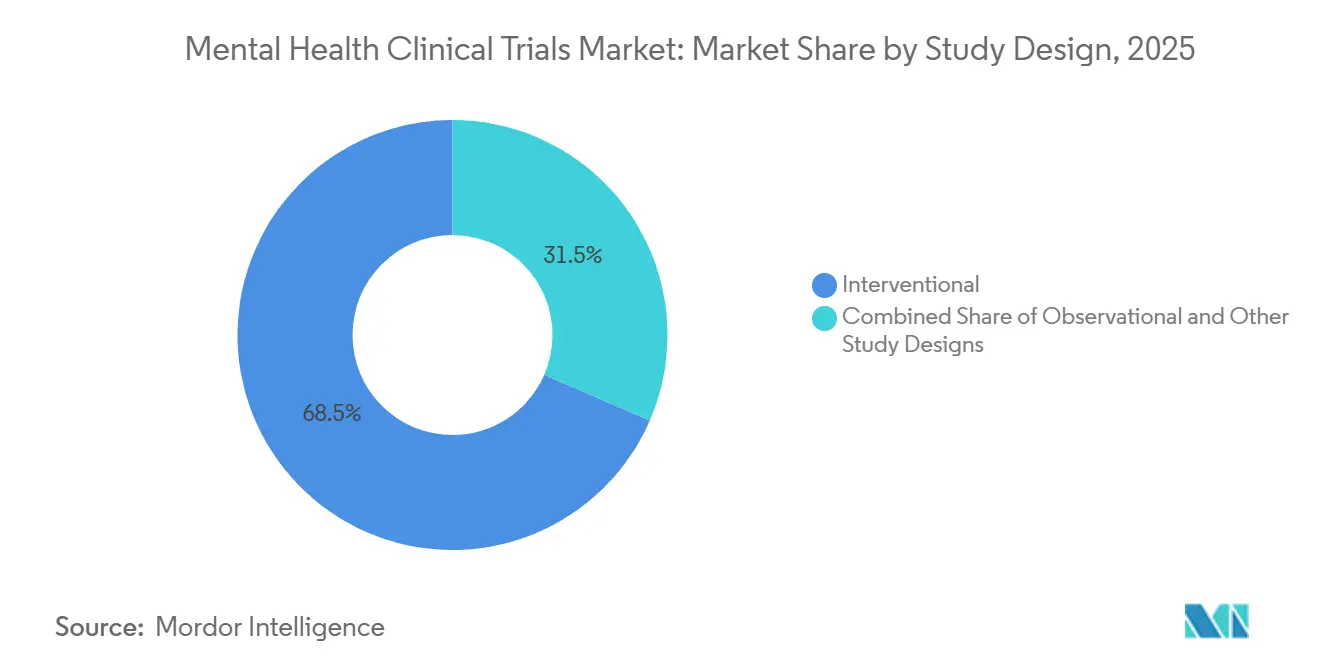

- By study design, interventional protocols led with 68.54% of the mental health clinical trials market share in 2025; observational studies are forecast to expand at an 11.25% CAGR through 2031.

- By phase, Phase III retained a 37.44% share of the mental health clinical trials market size in 2025, while Phase II is projected to grow at a 10.65% CAGR to 2031.

- By disorder, depression accounted for 25.15% of 2025 activity, whereas schizophrenia trials are advancing at a 10.82% CAGR through 2031.

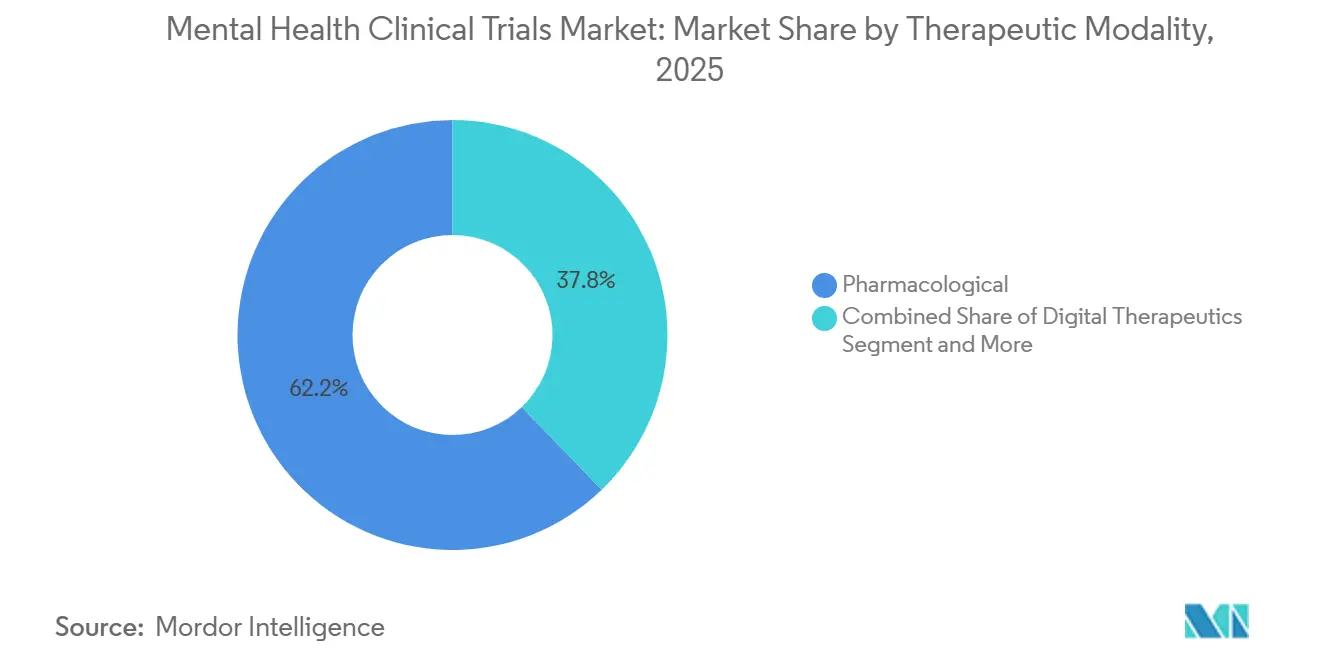

- By therapeutic modality, pharmacological approaches held 62.23% of 2025 revenue; digital therapeutics are scaling at a 12.42% CAGR following multiple FDA clearances.

- By sponsor, pharmaceutical and biopharmaceutical companies commanded 54.45% in 2025, while venture-backed biotechs are expanding at an 11.12% CAGR on the strength of USD 1.8 billion psychedelic financing.

- By trial setting, site-based formats still dominated with 70.63% share in 2025, yet decentralized models are climbing at a 10.22% CAGR as wearables reduce visit burden.

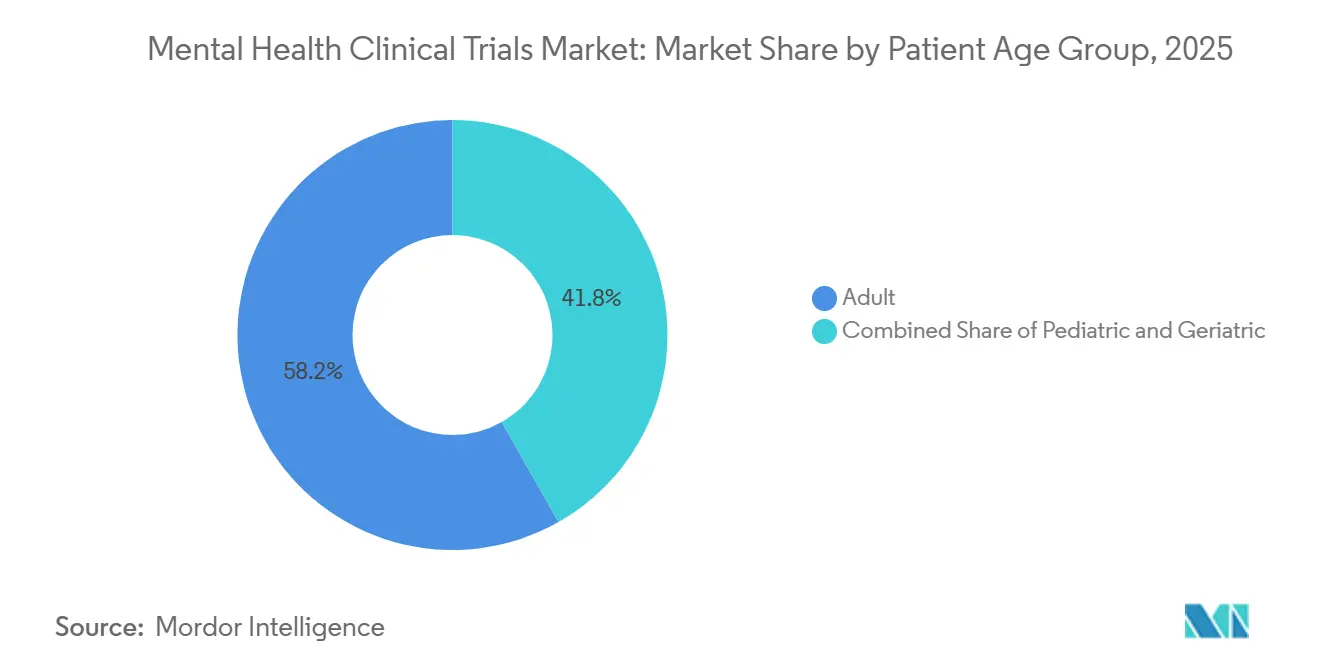

- By age group, adults represented 58.23% of 2025 enrollment; pediatric cohorts are growing at a 9.12% CAGR following 2024 FDA draft guidance on pediatric investigation plans.

- By geography, North America captured 45.13% share in 2025, while Asia-Pacific is the fastest-growing region at a 13.01% CAGR through 2031 on the back of China’s regulatory reforms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mental Health Clinical Trials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of mental-health conditions | +2.1% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| Growth in pharma & biotech R&D budgets | +1.8% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Adoption of decentralized & digital trial models | +1.5% | North America & EU lead, spill-over to APAC | Medium term (2-4 years) |

| Venture funding for psychedelic-assisted therapies | +1.2% | North America, Europe, Australia | Short term (≤ 2 years) |

| AI-enabled patient stratification boosts enrollment | +1.0% | North America, select EU markets | Medium term (2-4 years) |

| Employer-sponsored well-being benefits spur demand | +0.6% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Mental-Health Conditions

WHO estimated 280 million people living with depression and 301 million with anxiety in 2024, a 25% rise since 2019, expanding the addressable patient pool for the mental health clinical trials market. Governments responded; the NIH increased its dedicated budget to USD 2.9 billion in fiscal 2025, an annual jump of 12%, to fuel biomarker-rich studies that parse responder phenotypes. Sponsors embed neuroimaging and cytokine panels into Phase II designs to meet payer and regulator demands for precision evidence. The broader epidemiological burden—USD 280 billion in lost U.S. productivity—creates urgency among employers that ultimately fund insurance premiums. These converging factors lift enrollment rates and sustain high trial starts.

Growth in Pharma & Biotech R&D Budgets

Eli Lilly’s USD 9.3 billion 2024 R&D spend earmarked 18% for neuroscience, up four points year-on-year[1]Eli Lilly and Company, “Full-Year 2024 Results,” investor.lilly.com. Biogen redeployed USD 2.1 billion toward depression and schizophrenia programs after Alzheimer’s launch cash flows stabilized. Heavier wallets fund adaptive platform trials that collapse Phase II and III, shaving up to two years off timelines under the FDA’s Complex Innovative Designs pathway. Project Optimus principles around dose-optimization have spilled into psychiatry, encouraging lower, tolerable regimens that cut attrition by double digits. Larger R&D envelopes thus amplify both the quantity and sophistication of trials.

Adoption of Decentralized & Digital Trial Models

March 2024 FDA guidance legitimized telehealth assessments, provided inter-rater reliability exceeds 0.80, lowering geographic barriers for the mental health clinical trials market. IQVIA disclosed that 38% of its psychiatric portfolio used at least one decentralized element by Q4 2024, up from 22% in 2023[2]IQVIA Holdings, “Q4 2024 Earnings Call Transcript,” iqvia.com. Cost savings reach USD 3,000-5,000 per patient by eliminating site overhead, but remote ratings show 15% higher score variance, prompting algorithmic quality checks. Hybrid designs, blending quarterly in-clinic visits with monthly telehealth, now represent a pragmatic compromise embraced by sponsors and regulators alike.

Venture Funding for Psychedelic-Assisted Therapies

Psychedelic start-ups attracted USD 1.8 billion across 47 deals in 2024, sustaining a pipeline of psilocybin, DMT, and MDMA analogs despite an FDA complete-response letter to Lykos’ PTSD filing. Compass Pathways’ USD 150 million Series C underscores investor willingness to fund 300-patient Phase III trials that incorporate active-placebo blinding to meet heightened evidentiary bars. The capital influx accelerates enrollment in high-dose and micro-dose arms, broadening mechanistic readouts and, ultimately, filing velocity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited mental-health literacy in emerging markets | -0.8% | APAC excl. Japan & Australia, MENA, South America | Long term (≥ 4 years) |

| Scarcity of pediatric populations for ethical recruitment | -0.9% | Global, acute in U.S. & EU | Medium term (2-4 years) |

| High drop-out rates due to long therapy timelines | -1.4% | Global, acute in U.S. & EU | Medium term (2-4 years) |

| Reimbursement uncertainty for novel neuro-therapeutics | -1.1% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Drop-Out Rates Due to Long Therapy Timelines

A Lancet Psychiatry meta-analysis covering 127 studies showed 30% attrition by week 12 for depression and 40% by week 26 for schizophrenia, inflating per-patient costs by USD 8,000-12,000. Sponsors now over-enroll by roughly 25% to preserve statistical power, yet this escalates budgets and prolongs recruitment. CROs such as Fortrea embed nurse-led retention programs—weekly text or phone outreach—that trimmed dropout by 12 percentage points in a 2024 pilot but add USD 2,500 per enrollee. Regulators have not mandated retention plans, but reviewer queries increasingly scrutinize whether completers reflect the intended population. Persistent attrition remains the costliest operational hurdle for sponsors.

Reimbursement Uncertainty for Novel Neuro-Therapeutics

Digital therapeutics priced above USD 500 monthly risk exclusion from formularies unless supported by real-world cost-offset data, a lesson underscored by Pear Therapeutics’ 2023 bankruptcy. Neuromodulation devices costing USD 15,000-25,000 secured Medicare coverage yet face patchy Medicaid uptake, limiting access in low-income cohorts. Sponsors now stratify Phase III designs by payer type to generate targeted health-economic outcomes, increasing complexity and adding 6-9 months to timelines. Financing this dual-endpoint burden is particularly challenging for cash-constrained biotechs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Study Design: Observational Protocols Gain Traction

Interventional trials commanded 68.54% of the mental health clinical trials market in 2025, but observational studies are on track to post an 11.25% CAGR to 2031 as payers prioritize real-world evidence for coverage talks. Observational registries leverage propensity-score matching to control confounding, allowing data to support label expansions without the logistical weight of randomized controls.

Interventional designs remain regulators’ gold standard, yet they confront recruitment fatigue among treatment-resistant patients wary of placebo arms. IQVIA’s 4,200-patient depression registry delivered data 2 × faster than comparable RCTs, highlighting speed advantages that lure sponsors seeking post-approval safety confirmations.

By Phase: Phase II Adaptive Platforms Accelerate Timelines

Phase III absorbed 37.44% of 2025 expenditure, reflecting its pivotal-evidence mandate, while Phase II platforms are expanding at a 10.65% CAGR, exploiting seamless progression rules under FDA draft guidance. Mental health clinical trials market size for Phase II initiatives is projected to expand at pace as Bayesian algorithms shift allocation toward effective doses mid-trial.

Compass Pathways completed a 233-patient psilocybin Phase IIb in 14 months using adaptive randomization, versus a typical 28-month traditional design, illustrating the timeline dividends now attracting large pharma co-development deals[3]Compass Pathways, “Investor Presentation Q1 2025,” compasspathways.com.

By Disorder: Schizophrenia Trials Benefit from Novel Mechanisms

Depression retained 25.15% share in 2025, yet schizophrenia protocol starts are climbing at a 10.82% CAGR, fueled by Bristol Myers Squibb’s 2024 muscarinic approval that sidesteps dopamine side effects. Muscarinic follow-ons across eight Phase II programs highlight how one green-light can reorder pipeline focus.

Inflammation-linked depression subtypes respond 40% better to IL-6 blockade, spurring immunomodulator repurposing studies that could further fragment the indication into biomarker-defined niches. This precision trend increases trial complexity but improves effect-size detection.

By Therapeutic Modality: Digital Therapeutics Scale Rapidly

Pharmacologics held 62.23% share in 2025, yet digital therapeutics’ 12.42% CAGR signals a shift toward software-based care as the FDA cleared Sleepio for chronic insomnia and multiple CBT apps for substance use. Mental health clinical trials market share for digital tools is further buoyed by 40% commercial-payer coverage rates achieved within 12 months of clearance.

Apps avoid pharmacokinetic safety reviews, shortening development to 3-4 years versus 8-10 years for small molecules. A JAMA Network Open study found app-based CBT sustained 60% of symptom gains at 12-month follow-up, outperforming face-to-face therapy durability.

By Sponsor: Venture-Backed Biotechs Drive Innovation

Pharma and large biopharma owned 54.45% of 2025 activity, yet venture-backed biotechs are compounding at an 11.12% CAGR as mental health clinical trials market entrants receive outsized funding for first-in-class assets.

Biotechs target underserved pediatric anxiety and geriatric depression niches ignored by diversified pharmas. Compass Pathways’ single-asset focus exemplifies venture willingness to back concentrated risk that could rebase standard-of-care if Phase III succeeds.

By Trial Setting: Decentralized Models Reduce Geographic Barriers

Site-based approaches controlled 70.63% in 2025, yet decentralized formats grow at 10.22% as telehealth lowers travel friction, boosting the mental health clinical trials market’s rural reach. Lindus Health’s 320-patient virtual depression study enrolled across 38 states in nine months—geographic breadth a traditional model would achieve only with 200 sites.

Variance in remote rating scores persists, but algorithmic anomaly detection and mandatory calibration sessions keep data within acceptable error margins, preserving regulatory confidence.

By Patient Age Group: Pediatric Trials Navigate Ethical Complexity

Adults covered 58.23% of 2025 enrollment, yet pediatric cohorts are expanding at 9.12% CAGR after FDA draft guidance made pediatric investigation plans obligatory for all CNS-active agents. Mental health clinical trials market size associated with pediatric studies remains modest because assent refusal rates can cut eligible pools by 20 percentage points.

Sponsors must supply age-appropriate formulations and perform pharmacokinetic tests in children as young as six, driving unit costs 30-50% above adult trials. Nonetheless, policy momentum is pushing sponsors to front-load pediatric data rather than defer until post-approval.

Geography Analysis

North America controlled 45.13% of 2025 spending, supported by NIH’s USD 2.9 billion allocation and FDA openness to adaptive and decentralized designs. Canada’s expedited psilocybin exemptions and Mexico’s 30-40% lower per-patient costs diversify site selection while maintaining robust oversight.

Europe ranks second; the EMA’s 2024 clinical-trial regulation harmonized approvals, halving median start-up times to six months, while the UK’s MHRA fast-track allows conditional marketing based on Phase IIb data, incentivizing sponsors to lodge European programs early.

Asia-Pacific is the growth engine, posting a 13.01% CAGR through 2031 as China authorizes foreign Phase I work and Japan reimburses digital therapeutics that meet head-to-head non-inferiority criteria. India’s ultra-low costs entice biotechs, though stigma slows enrollment in rural zones. Australia’s TGA permits for psychedelic studies and South Korea’s smartphone-based phenotyping labs enhance regional specialization.

Competitive Landscape

The top five CROs, IQVIA, ICON, Fortrea, Parexel, and others, collectively run a substantial share of psychiatric enrollment, yet the mental health clinical trials industry remains only moderately consolidated. Technology-led challengers such as Lindus Health and Elligo Health Research capture contracts requiring fully virtual delivery or AI patient-matching algorithms.

IQVIA holds three patents covering dropout-risk AI that proactively flags disengaging participants, a feature winning multiyear preferred-provider deals. ICON cut enrollment timelines by 30% in 2025 via EHR-scraping algorithms, signaling that data science now rivals site networks as a buying criterion.

Specialist CROs lean on decentralized expertise: Medpace’s wearable collaboration inserts cardiac and sleep measures as exploratory endpoints, broadening datasets without extra visits. White-space is richest in pediatric psychiatry, geriatric depression, and rare disorders like trichotillomania, where top CROs lack turnkey playbooks and smaller providers can differentiate on agility.

Mental Health Clinical Trials Industry Leaders

IQVIA Inc.

Parexel International Corporation

Caidya

Fortrea Holdings Inc.

ICON plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Boehringer Ingelheim and Click Therapeutics reported the Phase III CONVOKE study met its primary endpoint, marking one of the first pivotal successes for a prescription digital therapeutic in schizophrenia.

- July 2025: atai Life Sciences and Beckley Psytech announced positive Phase 2b topline results for intranasal mebufotenin (BPL-003) in treatment-resistant depression.

Global Mental Health Clinical Trials Market Report Scope

As per the scope of the report, mental health clinical trials investigate methods to prevent, detect, or treat various diseases and conditions, playing a pivotal role in advancing comprehension and treatment of mental health disorders.

The segmentation of the mental health clinical trials market is categorized by study design, phase, disorder, therapeutic modality, sponsor, trial setting, patient age group, and geography. By study design, the market is segmented into interventional, observational, and expanded-access/other designs. By phase, it is divided into Phase I, Phase II, Phase III, and Phase IV. By disorder, the segmentation includes anxiety disorders, depression, schizophrenia, bipolar disorder, post-traumatic stress disorder (PTSD), substance-use disorders, and other disorders. By therapeutic modality, the categories include pharmacological, digital therapeutics, psychedelic-assisted, and neuromodulation. By sponsor, the market is segmented into pharmaceutical and biopharmaceutical companies, MedTech and digital-therapeutic companies, government and academic institutes, and venture-backed biotech/non-profits. By trial setting, the segmentation includes site-based traditional, decentralized/virtual, and hybrid. By patient age group, the market is divided into pediatric (0-17 years), adult (18-64 years), and geriatric (65+ years). By geography, the segmentation covers North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Interventional |

| Observational |

| Expanded-access / Other designs |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Anxiety Disorders |

| Depression |

| Schizophrenia |

| Bipolar Disorder |

| Post-Traumatic Stress Disorder (PTSD) |

| Substance-Use Disorders |

| Other Disorders |

| Pharmacological |

| Digital Therapeutics |

| Psychedelic-assisted |

| Neuromodulation |

| Pharmaceutical & Biopharmaceutical Companies |

| MedTech & Digital-Therapeutic Companies |

| Government & Academic Institutes |

| Venture-backed Biotech / Non-Profits |

| Site-based Traditional |

| Decentralized / Virtual |

| Hybrid |

| Pediatric (0-17 yrs) |

| Adult (18-64 yrs) |

| Geriatric (65+ yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Study Design | Interventional | |

| Observational | ||

| Expanded-access / Other designs | ||

| By Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Disorder | Anxiety Disorders | |

| Depression | ||

| Schizophrenia | ||

| Bipolar Disorder | ||

| Post-Traumatic Stress Disorder (PTSD) | ||

| Substance-Use Disorders | ||

| Other Disorders | ||

| By Therapeutic Modality | Pharmacological | |

| Digital Therapeutics | ||

| Psychedelic-assisted | ||

| Neuromodulation | ||

| By Sponsor | Pharmaceutical & Biopharmaceutical Companies | |

| MedTech & Digital-Therapeutic Companies | ||

| Government & Academic Institutes | ||

| Venture-backed Biotech / Non-Profits | ||

| By Trial Setting | Site-based Traditional | |

| Decentralized / Virtual | ||

| Hybrid | ||

| By Patient Age Group | Pediatric (0-17 yrs) | |

| Adult (18-64 yrs) | ||

| Geriatric (65+ yrs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the mental health clinical trials market be by 2031?

It is projected to reach USD 5.65 billion, reflecting an 8.02% CAGR from 2026 to 2031.

Which study design is growing fastest?

Observational registries are advancing at an 11.25% CAGR as payers demand real-world evidence.

What region shows the quickest expansion pace?

Asia-Pacific leads with a projected 13.01% CAGR through 2031, driven by Chinese and Japanese regulatory reforms.

Why are decentralized trials gaining traction?

FDA guidance allowing telepsychiatry reduces travel burden and lowers per-patient costs by USD 3,000-5,000.

Which therapeutic modality outpaces others in growth?

Digital therapeutics are scaling at a 12.42% CAGR following multiple FDA clearances and growing payer coverage.

Page last updated on: