Decentralized Clinical Trials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

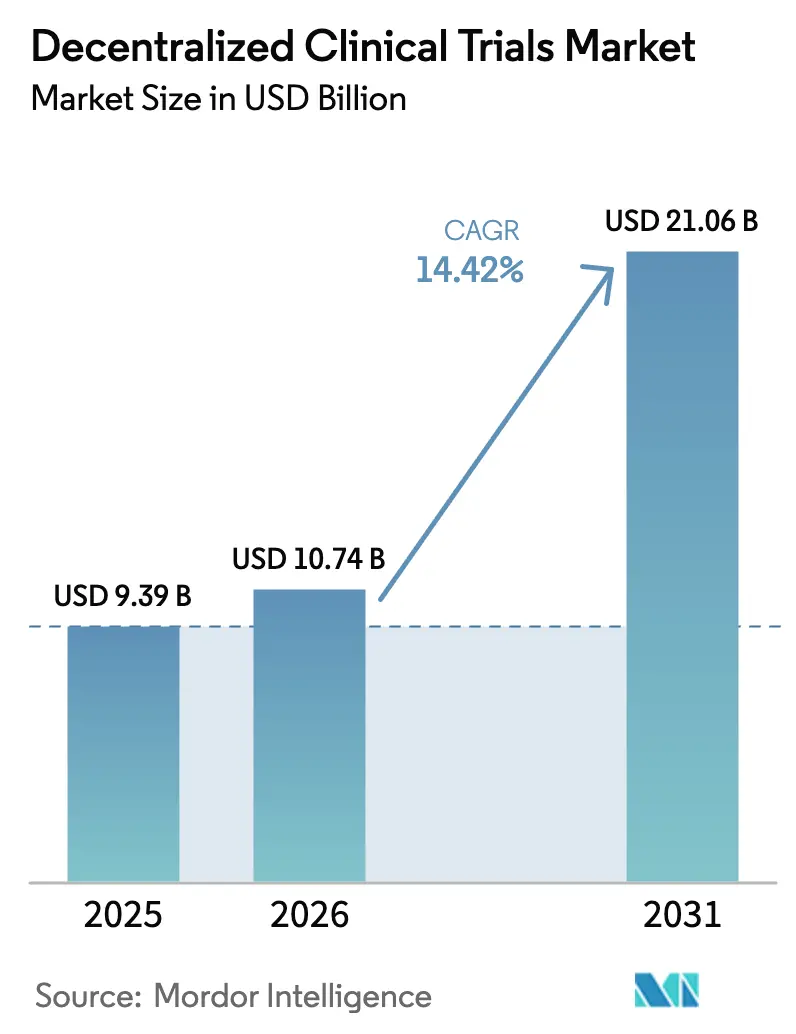

| Market Size (2026) | USD 10.74 Billion |

| Market Size (2031) | USD 21.06 Billion |

| Growth Rate (2026 - 2031) | 14.42% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decentralized Clinical Trials Market Analysis by Mordor Intelligence

Decentralized clinical trials market size in 2026 is estimated at USD 10.74 billion, growing from 2025 value of USD 9.39 billion with 2031 projections showing USD 21.06 billion, growing at 14.42% CAGR over 2026-2031. This growth reflects the decisive shift from site-centric research to technology-enabled, patient-centric models that widen access and improve data integrity. FDA’s September 2024 finalized guidance and the April 2024 launch of the Center for Clinical Trial Innovation provide regulatory clarity, encouraging adoption of telehealth visits, remote monitoring, and local care networks. Rising investment in 5G, wearables, and AI analytics further accelerates adoption, while public-private collaborations such as BARDA–Walgreens deliver large-scale infrastructure that extends reach to underserved communities HHS. Cloud-native platforms dominate as the backbone of trial operations; however, hybrid and app-centric solutions gain traction by offering flexible, patient-friendly interfaces. Moderate market fragmentation persists as CROs acquire digital capabilities and pure-play DCT specialists attract funding, but consolidation is gathering pace through high-value acquisitions and platform partnerships.

Key Report Takeaways

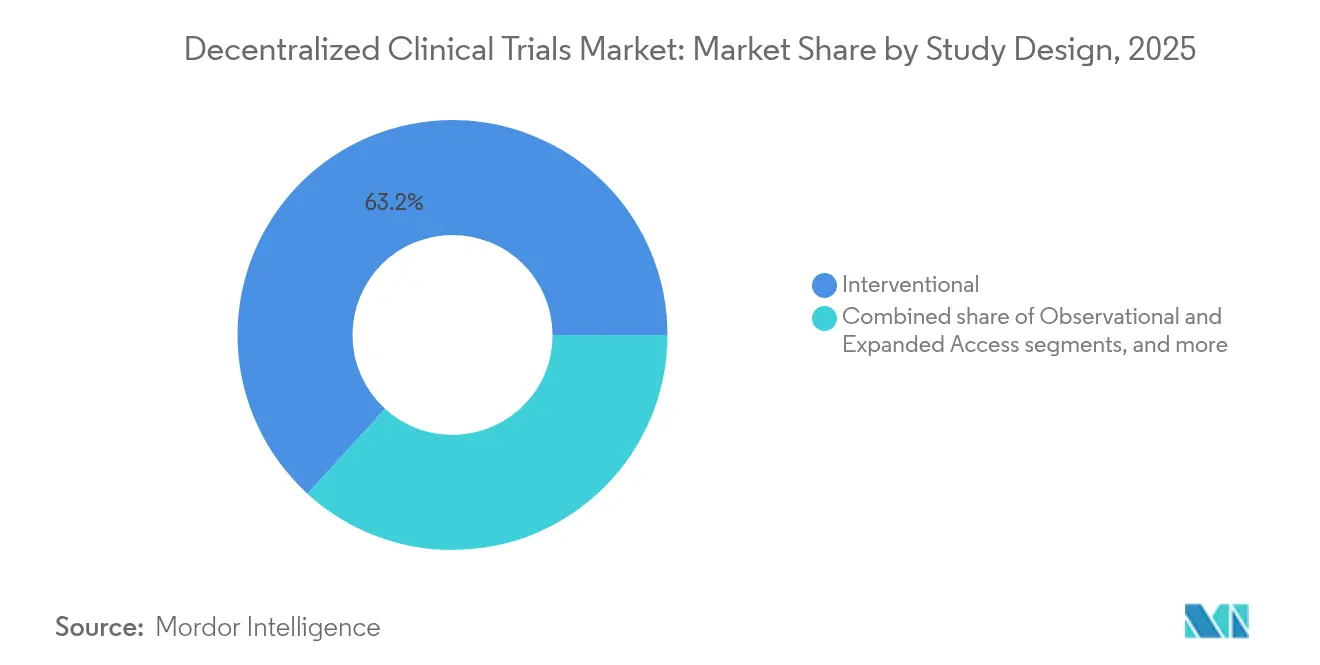

- By study design, interventional trials led with 63.21% revenue share in 2025, while expanded-access trials are advancing at a 15.89% CAGR to 2031.

- By component, cloud platforms captured 57.64% of the decentralized clinical trials market share in 2025; hybrid/app-centric solutions are forecast to expand at 16.48% CAGR through 2031.

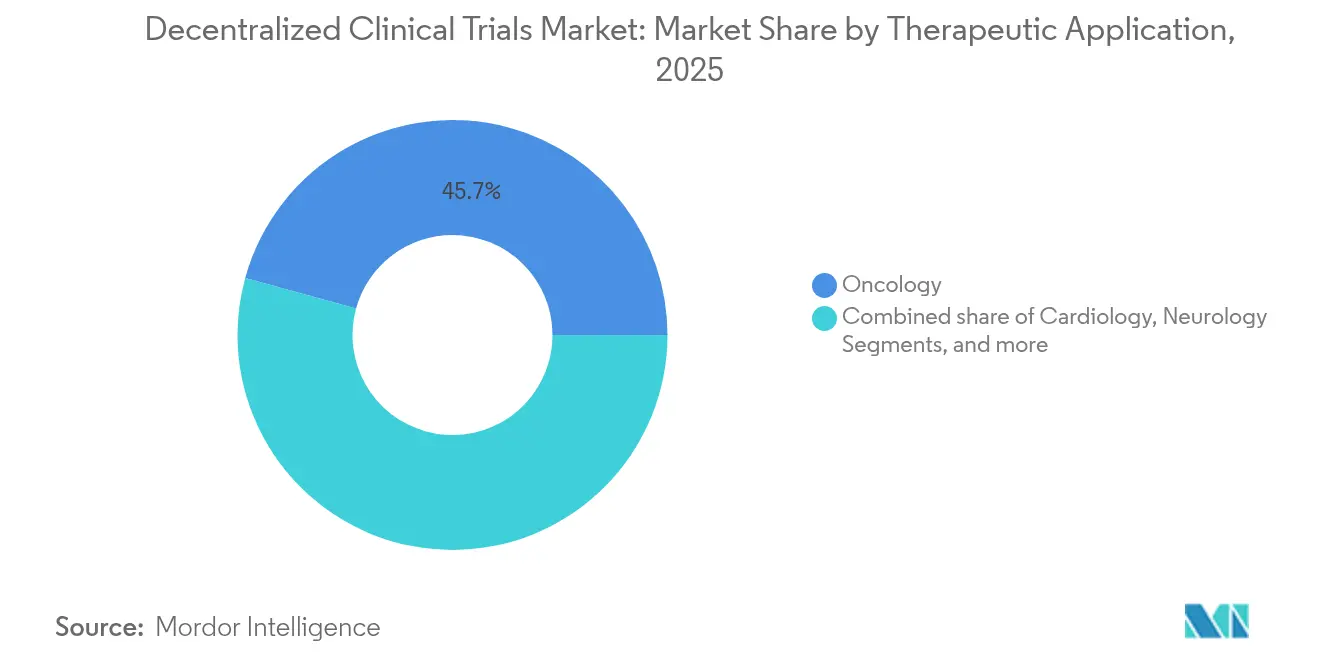

- By therapeutic application, oncology accounted for 45.72% share of the decentralized clinical trials market size in 2025; neurology is projected to grow at 16.02% CAGR through 2031.

- By end-user, pharmaceutical and biotech sponsors held 56.98% share in 2025, while medical device manufacturers record the fastest growth at 16.87% CAGR.

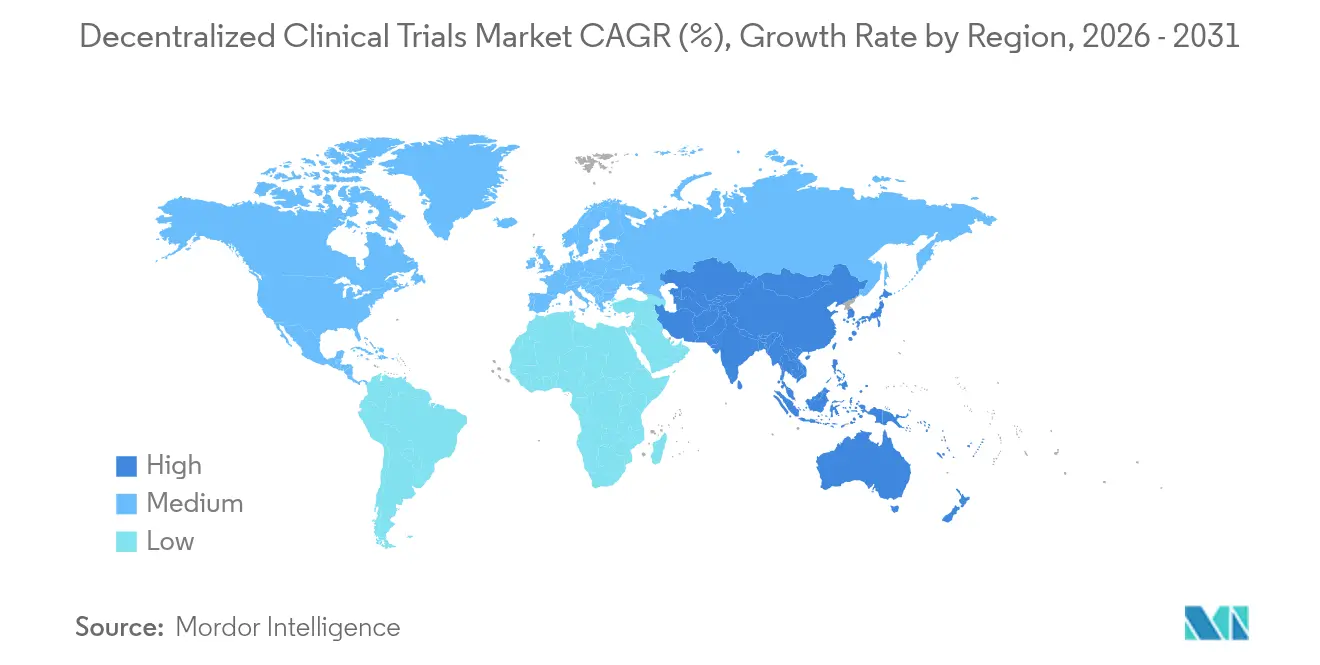

- By geography, North America dominated with 48.12% share in 2025; Asia-Pacific is the fastest-growing region at 15.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Decentralized Clinical Trials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of telehealth and remote patient monitoring infrastructure | +2.8% | Global (North America & Europe lead) | Medium term (2-4 years) |

| Demonstrated efficiency gains and accelerated study timelines | +2.1% | Global, especially US & EU | Short term (≤ 2 years) |

| Strengthening global regulatory endorsement for decentralized trial models | +1.9% | North America & Europe, emerging APAC | Medium term (2-4 years) |

| Proliferation of connected wearable and biosensor technologies | +1.6% | Global, high in developed markets | Long term (≥ 4 years) |

| Emergence of AI-powered synthetic control arms and predictive analytics | +1.4% | North America & Europe | Long term (≥ 4 years) |

| Adoption of blockchain-based consent and data integrity solutions | +0.8% | Global, early in advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Telehealth and Remote Patient Monitoring Infrastructure

Telehealth usage surged during the pandemic and remains a mainstay of care delivery, providing the foundation for large-scale decentralized trials. Remote monitoring programs such as the Utah initiative reduced A1C from 9.73% to 7.81% and lowered systolic blood pressure by 7.8 mm Hg, illustrating clinical benefit. Medicare now reimburses remote monitoring codes, creating a viable revenue stream for providers[1]Center for Telehealth & e-Law, “Medicare Remote Monitoring Reimbursement,” ctel.org. Combined with ubiquitous 5G and lower-cost wearables, sponsors can capture continuous biometric data while minimizing site visits. AI-driven analytics turn raw signals into actionable insights, triggering automated alerts that speed medical interventions. Rural and underserved communities, historically excluded from trials, gain unprecedented access through home-based data collection and local clinician support.

Strengthening Global Regulatory Endorsement for Decentralized Trial Models

The FDA’s 2024 guidance details telehealth visits, local HCP use, and digital data acceptance, eliminating ambiguity that previously hindered investment[2]Food and Drug Administration, “Decentralized Clinical Trials Guidance,” fda.gov. Parallel updates from ICH E6(R3) and EMA harmonize expectations across key markets. Singapore’s HSA and Australia’s TGA issue streamlined review pathways, supporting multi-regional scalability. FDA’s timeline to embed AI in all centers by mid-2025 signals openness to advanced analytics in protocol design and review. Clearer rules quell compliance concerns and give sponsors confidence to negotiate long-term contracts with platform vendors.

Proliferation of Connected Wearable and Biosensor Technologies

Medical-grade wearables—from Masimo pulse oximeters to Vivalink’s multi-parameter patches—unlock continuous, objective endpoints at population scale. Twenty percent of Medable-enabled trials already embed sensor feeds to supplement eCOA data. A 3,000-patient atrial fibrillation study demonstrated feasibility of remote vitals capture across large cohorts. IQVIA’s Connected Devices service curates and validates gadgets, accelerating device selection and deployment. Passive data capture reduces participant burden and elevates data density, enhancing statistical power while supporting real-time safety monitoring.

Emergence of AI-Powered Synthetic Control Arms and Predictive Analytics

Phesi’s Trial Accelerator Version 2 houses profiles for 132 million patients and 400,000 cohorts, enabling trial planners to forecast enrollment and optimize inclusion criteria[3]Phesi, “Trial Accelerator V2 Launch,” phesi.com. Synthetic control arms mitigate ethical issues around placebo exposure in oncology and rare diseases, cutting recruitment demands and timeline risk. Novotech anticipates AI managing half of trial data tasks by 2025, shrinking cycle times by 20%. FDA’s February 2025 draft guidance on AI credibility assessment offers a path to regulatory acceptance, prompting rapid pilot deployments among leading sponsors.

Adoption of Blockchain-Based Consent and Data Integrity Solutions

METORY—a blockchain dynamic-consent system—achieved 95.7% consent completion and 90.8% drug-adherence rates in a multicenter trial. Intel and ConsenSys Health’s federated architecture protects patient privacy while enabling cross-institutional analytics. A Health Canada-approved sub-study proved private permissioned blockchains can secure longitudinal trial data. Pfizer’s investment in VitaDAO highlights pharmaceutical interest in distributed research governance models, hinting at future decentralized funding ecosystems.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of harmonized international data governance frameworks | -1.8% | Global, particularly impacting multi-regional trials | Medium term (2-4 years) |

| Escalating cybersecurity and privacy compliance risks | -1.2% | Global, with stricter requirements in EU and emerging in APAC | Short term (≤ 2 years) |

| Technology access gaps among older and underserved patient cohorts | Not quantified | Rural areas and low-income regions across all continents | Medium term (2-4 years) |

| Unresolved reimbursement and logistics challenges for home-based specimen collection | Not quantified | North America and Europe primarily, with growing relevance in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Harmonized International Data Governance Frameworks

Sponsors juggling GDPR, HIPAA, and Asia-Pacific localization rules often build parallel infrastructures, eroding the scale advantage of global DCT platforms. FDA’s April 2025 request for comment on data standards underscores persistent uncertainty that delays multi-regional protocols. KPMG’s 2024 survey flags data sovereignty as a top-three concern for life-science executives. Divergent privacy statutes in China and India necessitate on-shore servers and fragmented data pipelines, elevating cost and operational complexity. Without harmonization, sponsors prioritize regional rollouts over truly global trial designs, dampening the decentralized clinical trials market’s long-term upside.

Escalating Cybersecurity and Privacy Compliance Risks

Healthcare endures 1,426 cyberattacks per week, 86% higher than other sectors, and DCTs broaden the threat surface through home networks and personal devices. FDA’s October 2024 electronic-systems guidance mandates audit trails and risk-based validation, adding compliance overhead. Investors now scrutinize cyber posture in due diligence, and adverse headlines can erode sponsor trust. AI and ML models create new attack vectors via adversarial inputs; hardening these pipelines requires scarce specialist skillsets. Heightened vigilance raises security spending and may slow adoption among smaller sponsors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Study Design: Interventional Trials Drive Market Leadership

Interventional studies held 63.21% share of the decentralized clinical trials market in 2025, reflecting alignment between structured protocols and remote-first data capture. Their dominance is reinforced by FDA guidance encouraging pragmatic, randomized designs within routine practice. Sponsors value the ability to embed telemedicine visits and remote safety labs that trim site burden and speed enrollment. Expanded-access protocols, while smaller, grow 15.89% CAGR as patient-advocacy groups lobby for early treatment availability. Observational studies benefit from streamlined real-world data capture but lack the IP-linked budgets driving interventional uptake.

The decentralized clinical trials industry increasingly leverages AI-powered synthetic control arms, reducing placebo exposure and ethical concerns in oncology. Flatiron Health’s automated EHR feeds illustrate how pragmatic frameworks blur lines between interventional and observational categories. Regulatory acceptance accelerates migration of late-phase trials to decentralized models, further entrenching interventional leadership. Yet patient-centricity and diversity imperatives ensure continued investment in expanded-access and community-based observational designs.

By Component: Cloud Platforms Dominate While Hybrid Solutions Accelerate

Cloud platforms accounted for 57.64% of the decentralized clinical trials market share in 2025, underpinning secure multi-stakeholder access, auditability, and scalable analytics. Enterprise sponsors prefer validated, 21 CFR Part 11-compliant environments that integrate EDC, eCOA, and randomization in a single stack. Hybrid and app-centric platforms are expanding 16.48% CAGR as user experience becomes a differentiator; BYOD strategies reduce device logistics and improve retention. Web-based portals remain relevant for investigator workflows but increasingly converge with mobile frameworks.

Medable’s Google Cloud Marketplace presence exemplifies how hyperscale clouds expedite global rollouts while offering regional data residency options. eCOA+ libraries accelerate study build and shorten first-patient-in timelines. WCG’s ClinSphere combines participant engagement with consent management, demonstrating the hybrid trajectory. As sponsors extend trials to aging populations, intuitive mobile interfaces and offline functionality will influence platform selection and propel growth in hybrid architectures.

By Therapeutic Application: Oncology Leadership Meets Neurology Innovation

Oncology controlled 45.72% of the decentralized clinical trials market size in 2025, anchored by high unmet need and patient-burden concerns. Frequent assessments and toxicity monitoring make remote data capture invaluable, while precision-medicine trials benefit from rapid genomic screening and tele-oncology follow-up. Neurology, expanding at 16.02% CAGR, leverages wearables for gait, sleep, and cognitive metrics that were previously infeasible in site-centric models. Cardiology and respiratory segments adopt continuous vitals monitoring, whereas rare-disease programs find DCTs essential for reaching dispersed cohorts.

The myeloMATCH platform run by Thermo Fisher and NCI spans 2,200 sites and channels genomic insights into trial matching, a milestone for oncology decentralization. Lindus Health’s Oura-enabled ME/CFS study showcases neurology’s potential for fully virtual protocols with high retention. Real-time patient-reported outcomes deepen safety insights, and synthetic control constructs expedite efficacy comparisons, fueling uptake across therapeutic areas.

By End-User: Pharma Dominance Challenged by Device Innovation

Pharma and biotech companies controlled 56.98% of the decentralized clinical trials market in 2025, driven by R&D intensity and patent-lifecycle pressures. These sponsors integrate DCT workflows to compress timelines and meet diversity targets mandated by regulators. Medical-device manufacturers, however, are the fastest-growing constituency at 16.87% CAGR as wearable validation and post-market surveillance align naturally with remote monitoring. CROs partner across segments, providing technology and services that shorten adoption curves. Academic institutes pilot novel methodologies that later cascade into industry practice.

Oracle Health Sciences’ feasibility-assessment modules and real-time recruitment tools exemplify the infrastructure catering to pharmaceutical sponsors. The Q-Centrix research network illustrates hospitals’ pivot toward data-powered trial participation. Device firms deploy connected sensors that feed continuous efficacy endpoints, critical for reimbursement evidence. Competitive tension around digital IP and analytics capabilities will shape vendor selection across all end-user groups.

Geography Analysis

North America held 48.12% of the decentralized clinical trials market in 2025, buoyed by robust telehealth reimbursement, FDA guidance, and deep venture capital flows. Walgreens’ BARDA contract leverages 9,000 pharmacy locations to reach underrepresented communities, setting a precedent for retail-based trial ecosystems. Canada’s coordinated data standards enable efficient cross-province studies, while Mexico’s telecommunication reforms support low-cost remote monitoring deployments.

Asia-Pacific records the fastest 15.32% CAGR to 2031, propelled by 30–40% cost advantages and agile regulatory pathways. Japan’s digital-health drive targets a 7.29% CAGR through 2028, harnessing 5G and an aging demographic. China’s regulatory reforms slashed IND review times, fueling a surge in domestic trial initiations toward 26.5% of global total by 2020. Singapore and Australia publish DCT guidelines that harmonize with ICH and FDA principles, facilitating multi-regional protocols. Novotech’s acquisition of US CRO NCGS signals APAC players’ intent to marry cost leadership with FDA-facing expertise.

Europe, a mature adopter, benefits from EMA guidance that aligns with GDPR, enabling cross-border trials within the bloc. The merger of OCT Clinical and palleos healthcare creates a 300 million-person coverage network across Central & Eastern Europe, expanding site options for sponsors. Middle East & Africa and South America remain nascent but promising; rising smartphone penetration and supportive e-health policies lay groundwork for future decentralized clinical trials market expansion.

Competitive Landscape

Market structure remains moderately fragmented as established CROs integrate digital tools and specialized vendors scale niche offerings. IQVIA operates 500+ active decentralized studies across 75 countries, using proprietary connected-device libraries and global logistics assets to manage end-to-end execution. Medidata’s platform, under Dassault Systèmes, layers virtual-site management and eConsent onto its EDC backbone, making it a one-stop environment for sponsors seeking data continuity. Thermo Fisher Scientific combines CDMO services with clinical research outsourcing, evidenced by its USD 17.4 billion PPD acquisition, to provide molecule-to-market capabilities that embed DCT options from early development onward.

Pure-play innovators differentiate on patient engagement. Science 37’s Metasite model mobilizes local HCPs and telemedicine physicians to reduce participant travel. Obvio Health employs gamified smartphone tasks to lift compliance rates across maternal-health studies. AI-centric disrupters such as Phesi and Grove AI turn large-scale patient data into predictive enrollment tools that cut screening waste. Consolidation is accelerating; PCM Trials’ acquisition of EmVenio and Thermo Fisher’s new Accelerator services illustrate the drive toward vertically integrated offerings that promise speed and data integrity.

Vendor selection increasingly hinges on cybersecurity credentials and cross-border data governance. Firms with ISO 27001 certification and zero-trust architectures win multi-regional bids. Strategic partnerships with hyperscale clouds and medical-device OEMs strengthen ecosystem stickiness, positioning leading platforms to capture disproportionate share as enterprise sponsors standardize on preferred vendors.

Decentralized Clinical Trials Industry Leaders

IQVIA Inc.

ICON plc

Thermo Fisher Scientific, Inc.

Labcorp Drug Development

Dassault Systèmes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FDA launched Elsa, a generative-AI tool to streamline protocol review, hinting at faster DCT clearances.

- February 2025: Allucent secured a 5-year BARDA contract to bolster decentralized operations under its D-COHRe program.

- January 2025: Lindus Health raised USD 55 million to scale its virtual-trial platform.

- January 2025: Phesi released Trial Accelerator V2, expanding to 132 million patient profiles and 400,000 cohorts for predictive enrollment.

- January 2025: Medable partnered with Google Cloud and Masimo to embed cloud scalability and medical-grade wearables in DCT workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis counts every technology and service dollar that enables patients, investigators, or monitors to carry out trial tasks remotely, including cloud platforms, eConsent, connected wearables, home nursing, and direct-to-patient logistics across all phases, study designs, and therapy areas worldwide.

Scope exclusion: generic telehealth software and routine courier runs not tied to a regulated trial protocol remain outside the model.

Segmentation Overview

- By Study Design

- Interventional

- Observational

- Expanded Access

- By Component

- Cloud-Based Platforms

- Web-Based Platforms

- Hybrid / App-Centric Platforms

- By Therapeutic Application

- Oncology

- Cardiology

- Neurology

- Respiratory

- Other Therapeutic Applications

- By End-User

- Pharmaceutical & Biotech Sponsors

- Medical-Device Manufacturers

- Contract Research Organisations (CROs)

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and surveys with CRO operations heads, decentralized-platform product managers, site nurses, and payer policy leads across North America, Europe, and Asia ground rule-of-thumb prices, hybrid uptake rates, and compliance hurdles.

Desk Research

Mordor desk analysts collect granular trial start counts, enrollment sizes, and device shipment volumes from FDA and EMA registries, ClinicalTrials.gov, customs codes, and filings by listed CROs, then enrich these with adoption ratios, cost curves, and regulatory timelines reported by DIA, DTRA, and leading journals. Select paid repositories such as Dow Jones Factiva, D&B Hoovers, and Questel close company revenue and patent gaps, while many additional open sources round out assumptions.

Market-Sizing & Forecasting

We begin with a top-down pool built from global trial counts multiplied by weighted remote visit numbers and average spend per visit. We then stress test totals with supplier roll-ups on biosensor kits and platform licenses. Key drivers modeled include oncology share of remote protocols, median kit price, broadband reach, and timing of new FDA guidance. Forecasts to 2030 use multivariate regression blended with scenario analysis to capture regulatory or cost shocks, and any missing micro data is bridged through conservative proxies from adjacent study types; only after those cross checks converge do we release the final market value.

Data Validation & Update Cycle

Outputs pass anomaly screens against external indicators, receive double analyst review, and trigger expert rechecks when variance thresholds emerge. Reports refresh each year and can update mid-cycle after landmark rules or major technology breakthroughs.

Why Mordor's Decentralized Clinical Trials Baseline Earns Decision-Maker Confidence

Published figures often diverge because firms choose different scopes, price ladders, and refresh cadences. Mordor's disciplined variable set keeps our baseline steady yet responsive when facts change.

Most gaps appear when other publishers omit hybrid trials, apply one flat visit cost worldwide, or freeze currency at contract date, while Mordor rolls quarterly exchange rates, region specific cost ladders, and phase by phase adoption curves into the model.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.39 B | Mordor Intelligence | |

| USD 8.77 B | Global Consultancy A | Hybrid designs excluded |

| USD 8.66 B | Industry Research Publisher B | Only North America and Europe counted |

| USD 8.80 B | Regional Analytics Firm C | Static device prices and FX |

This comparison shows that Mordor's cross checked scope, live cost inputs, and scheduled refresh cadence deliver a transparent, balanced baseline that planners can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the decentralized clinical trials market?

The decentralized clinical trials market stands at USD 10.74 billion in 2026 and is projected to reach USD 21.06 billion by 2031.

Which region leads the decentralized clinical trials market?

North America commands 48.12% market share, driven by strong telehealth infrastructure and supportive FDA guidance.

Which study design is most common in decentralized clinical trials?

Advarra, Thermo Fisher Scientific Inc, IQVIA Inc, Medidata and Clario are the major companies operating in the Decentralized Clinical Trials Market.

Which is the fastest growing region in Decentralized Clinical Trials Market?

Interventional trials dominate with 63.21% share, reflecting their compatibility with remote monitoring and structured endpoints.

How fast is the Asia-Pacific market growing?

Asia-Pacific is the fastest-growing region, forecast to expand at a 15.32% CAGR through 2031 due to cost advantages and streamlined regulations.

Which technology platforms hold the largest share?

Cloud-based platforms lead with 57.64% of decentralized clinical trials market share, thanks to scalability and compliance capabilities.

What is the greatest restraint facing decentralized clinical trials?

The lack of harmonized international data governance increases complexity and cost for multi-regional trials, dampening adoption momentum.

Page last updated on: