Trauma Care Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.76 Billion |

| Market Size (2031) | USD 29.88 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

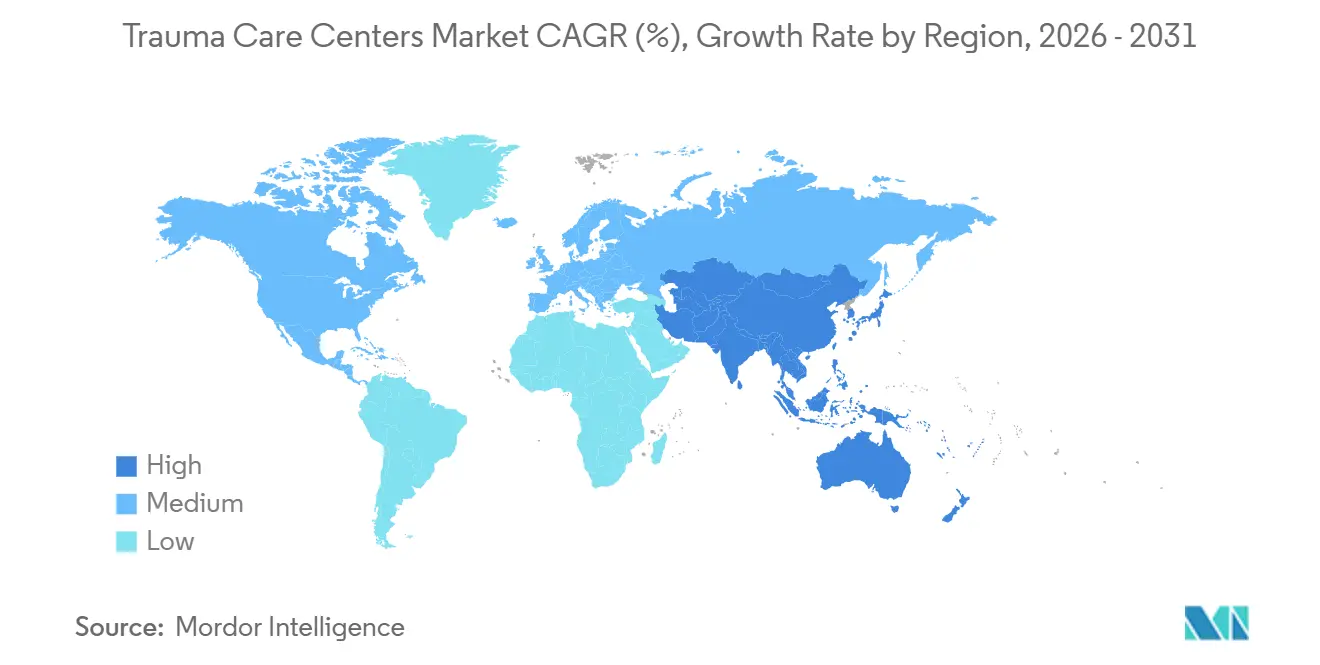

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

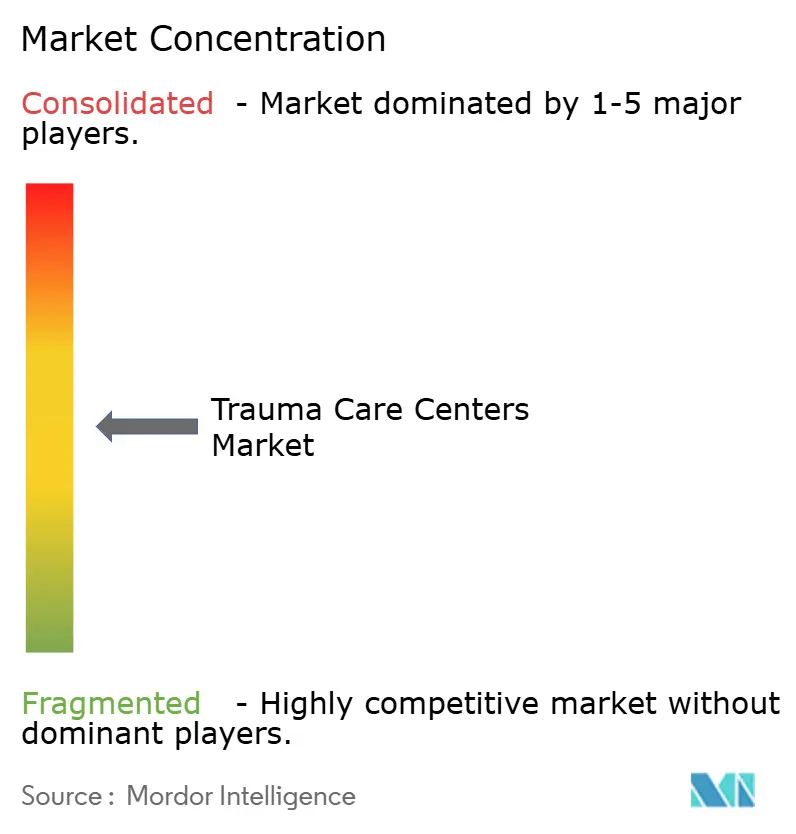

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trauma Care Centers Market Analysis by Mordor Intelligence

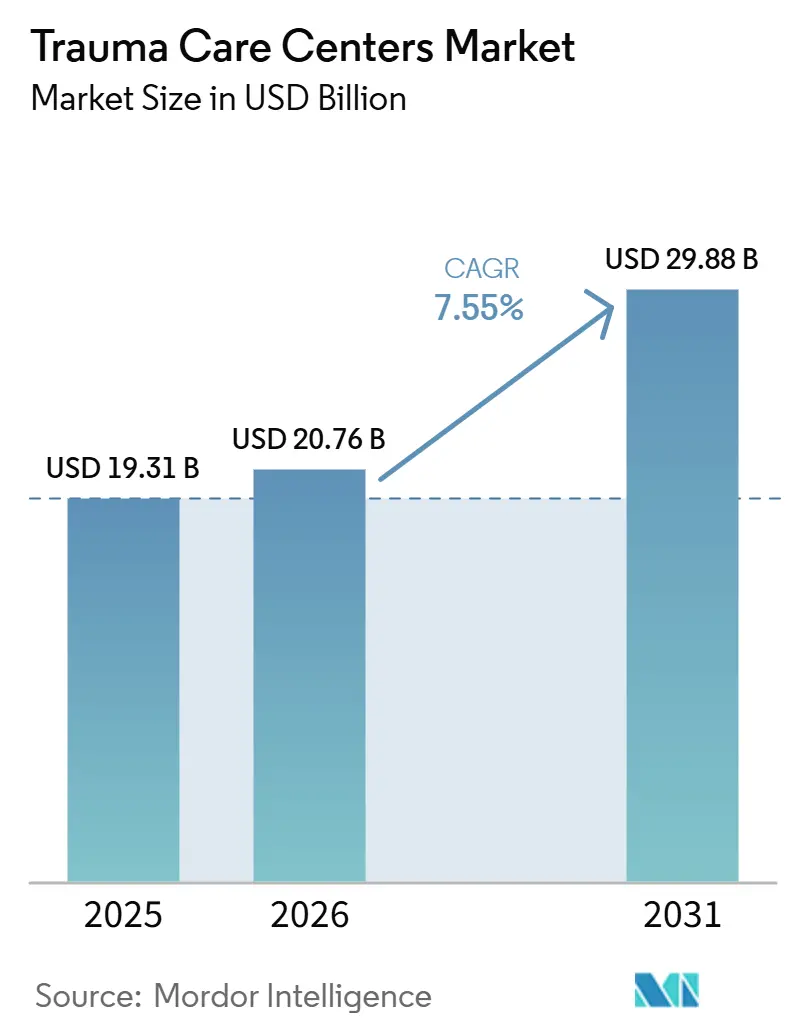

The Trauma Care Centers Market size is projected to expand from USD 19.31 billion in 2025 and USD 20.76 billion in 2026 to USD 29.88 billion by 2031, registering a CAGR of 7.55% between 2026 to 2031.

The trauma care centers market is being supported by the steady rise in severe road injury cases, the higher fall burden in older adults, and the wider use of AI-supported triage and imaging workflows in emergency settings. North America remained the largest regional base in 2025 because it combines a dense trauma center footprint with mature verification and referral structures, which helps large systems maintain high-acuity readiness at scale. Asia-Pacific is set to expand faster as public systems and hospital operators continue building regional trauma pathways, referral links, and stabilization capacity across fast-growing injury corridors. Competitive advantage in the trauma care centers market continues to favor integrated health systems and academic operators that can absorb readiness costs, support designation upgrades, and invest in data connectivity. Expansion decisions across the trauma care centers market are still shaped by surgeon shortages, high fixed readiness spending, and persistent EMS-to-hospital interoperability gaps that can slow throughput and raise operating pressure.

Key Report Takeaways

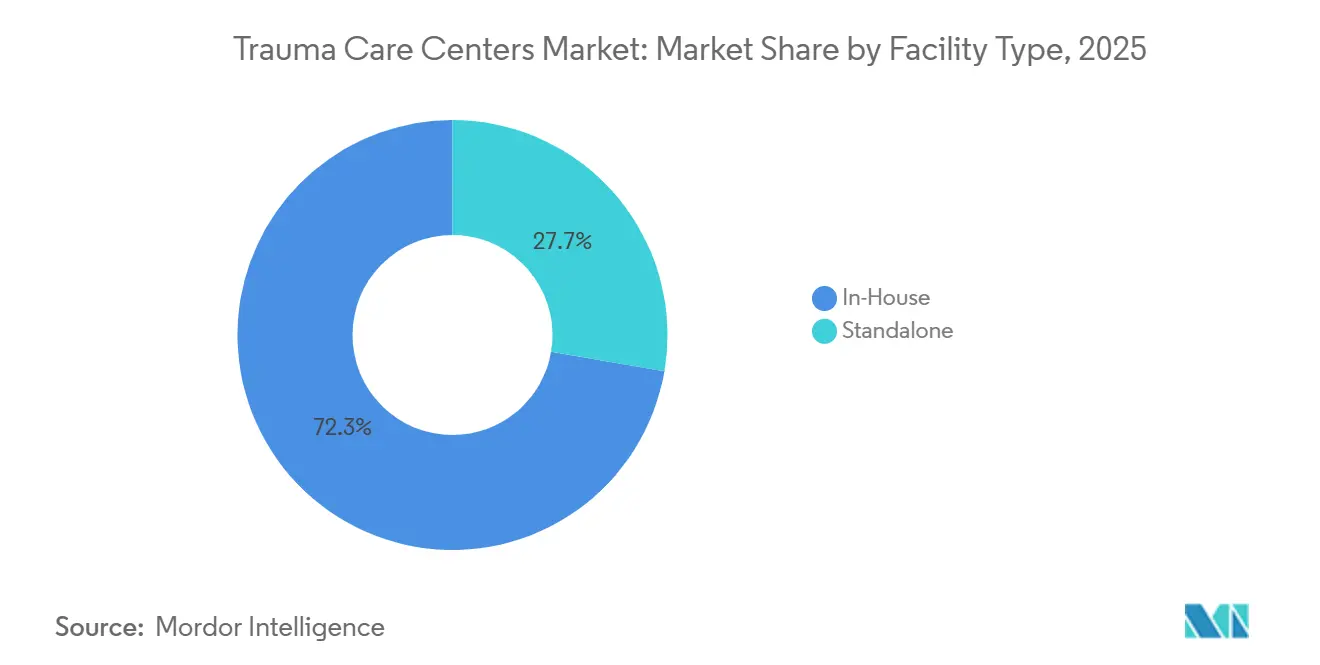

- By facility type, in-house facilities held 72.31% of trauma care centers market share in 2025, while standalone centers are forecast to grow at an 8.38% CAGR through 2031.

- By trauma type, falls led with a 35.24% revenue share in 2025, while traffic-related injuries are projected to expand at an 8.52% CAGR through 2031.

- By service type, outpatient services accounted for 56.26% share in 2025, while inpatient services are forecast to grow at an 8.55% CAGR through 2031.

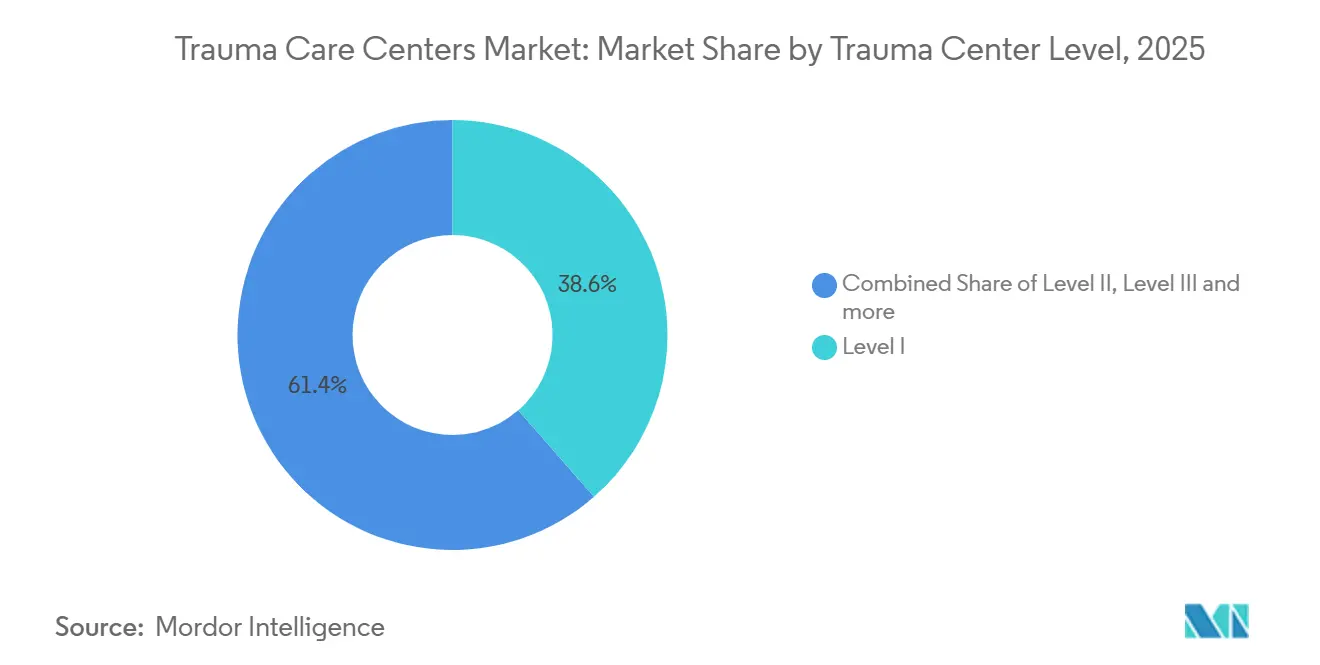

- By trauma center level, Level I centers held 38.56% share in 2025, while Level V centers are expected to record the fastest growth at a 9.65% CAGR through 2031.

- By patient age group, adults aged 18 to 64 years held 48.33% share in 2025, while the geriatric segment is projected to expand at a 9.15% CAGR through 2031.

- By mode of admission, ambulance-based admissions captured 36.52% share in 2025, while air medical transport is forecast to grow at a 9.25% CAGR through 2031.

- By geography, North America accounted for 36.61% share of the trauma care centers market size in 2025, while Asia-Pacific is projected to expand at an 8.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Trauma Care Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Road Traffic Injuries and Polytrauma Caseloads | +1.8% | Global, concentrated in APAC, MEA, and South America | Medium term (2-4 years) |

| Aging Population With Higher Fall and Fragility Injury Burden | +1.6% | North America, Europe, Japan, Australia | Long term (≥ 4 years) |

| Expansion of Regionalized Trauma Networks and Referral Pathways | +1.2% | APAC and MEA core, mature gains in North America and EU | Medium term (2-4 years) |

| Adoption of AI-Enabled Triage and Imaging Workflows | +1.0% | North America and EU core, spill-over to APAC | Short term (≤ 2 years) |

| Post-Acute Rehabilitation Integration Improving Survival and Throughput | +0.7% | North America, EU | Medium term (2-4 years) |

| Trauma Resilience Planning in Urban Mobility, Mass-Casualty, and Disaster Preparedness | +0.6% | Global, with early gains in North America and EU urban corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Road Traffic Injuries and Polytrauma Caseloads

The trauma care centers market continues to benefit from the sheer scale of road injury volumes worldwide. The World Health Organization estimated 1.19 million road traffic deaths each year, with 20 million to 50 million additional non-fatal injuries, which keeps trauma systems under sustained pressure. The financial effect comes less from fatalities and more from survivors with complex polytrauma who need resuscitation, surgery, imaging, and extended critical care. Powered 2-wheel and 3-wheel vehicles account for a large share of fatalities, which leaves motorcycle-heavy transport corridors in South and Southeast Asia with a deep unmet need for organized trauma pathways. Evidence published in 2025 also showed that coordinated regional operations models can support daily trauma demand and mass-casualty readiness at the same time, which improves the case for network investment across the trauma care centers market.

Aging Population With Higher Fall and Fragility Injury Burden

The trauma care centers market is also being pushed upward by the growing older adult population and its higher injury intensity. The CDC reported that more than 14 million older Americans, or 1 in 4, experienced falls each year, which keeps fracture, pelvic injury, and traumatic brain injury volumes high in mature care systems[1]Centers for Disease Control and Prevention, “Older Adult Falls Data,” CDC, cdc.gov. Spending on non-fatal falls among older adults reached USD 50 billion in the United States, which shows why geriatric trauma now carries both volume and cost weight for providers. The older population in the United States is projected to reach 74 million by 2030, which points to a larger future base for inpatient recovery and rehabilitation demand. The American College of Surgeons also updated traumatic brain injury guidance to include early rehabilitation expectations, which makes geriatric trauma more central to how the trauma care centers market organizes clinical pathways.

Adoption of AI-Enabled Triage and Imaging Workflows

The trauma care centers market is moving from AI pilot activity toward real clinical deployment in triage and imaging. A 2025 multi-institutional and multi-national validation study published in Nature Communications showed a prehospital AI model that could score mortality risk in real time and was already active in trauma care settings. In emergency imaging, AI-based prioritization of non-contrast head CT scans for hemorrhage, mass effect, and fracture showed faster diagnostic handling in work presented at ECR 2026[2]ECR 2026, “AI Triage of Non-Contrast Head CT Scans in the ER, Prioritizing Reports for Intracranial Hemorrhage, Mass Effect, and Fracture,” European Congress of Radiology, epos.myesr.org. At the same time, a 2026 study in European Radiology Experimental found that discretionary AI use does not consistently improve radiologist sensitivity, which means workflow design matters as much as software quality. That raises the real deployment cost in the trauma care centers market because operators must fund process change, clinician training, and data integration rather than software licenses alone.

Expansion of Regionalized Trauma Networks and Referral Pathways

The trauma care centers market is increasingly being organized around hub-and-spoke design rather than isolated high-acuity campuses. This model links field triage, community stabilization, and inter-facility transfer so that top-tier centers are not overloaded with cases that could be managed downstream. The 2026 equity analysis in JAMA Network Open found that simple trauma center proliferation does not automatically improve access or mortality in proportion to site count, which strengthens the case for coordinated network design. Public systems in Asia and other developing regions are responding by building broader trauma pathways instead of relying only on tertiary expansion. That approach supports wider catchment coverage and lowers bottlenecks at referral hubs, which should remain an important growth lever for the trauma care centers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Board-Certified Trauma Surgeons and Specialized Critical Care Staff | -1.5% | North America and EU, nascent in APAC | Long term (≥ 4 years) |

| High Capital Intensity for Level I and Level II Trauma Readiness | -1.2% | Global, most acute in North America and EU | Medium term (2-4 years) |

| Uneven Reimbursement for Readiness Costs and Uncompensated Trauma Volume | -0.9% | North America, secondary in MEA and South America | Medium term (2-4 years) |

| Interoperability Gaps Across EMS, ED, Imaging, and Transfer Networks | -0.6% | Global, with systemic gaps in APAC and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage Of Board-Certified Trauma Surgeons And Specialized Critical Care Staff

The most persistent operating constraint in the trauma care centers market remains the shortage of surgeons and specialized staff. The Association of American Medical Colleges projected a shortfall of 10,000 to 19,900 surgeons by 2036, which directly limits staffing depth for centers that need continuous attending coverage. A 2025 EAST multicenter study found measurable acute care surgeon shortfalls across U.S. facilities when workload benchmarks were applied, which confirms that the gap is already visible in operating practice. The age mix of the workforce adds more pressure because a large share of surgeons are already near retirement age[3]American College of Surgeons, “Surgeon Shortage Calls for Action,” ACS Bulletin, facs.org. Since Level I and Level II verification depends on 24/7 attending coverage, the trauma care centers market cannot solve this problem with capital spending alone.

High Capital Intensity For Level I And Level II Trauma Readiness

Capital intensity remains a major brake on expansion across the trauma care centers market. Georgia Trauma Commission data for CY2024 showed average annual readiness costs of USD 10.1 million for Level I centers and USD 4.9 million for Level II centers, which highlights the cost of keeping surgical capability available at all times. Large infrastructure projects reinforce that burden, with Harborview Medical Center pursuing a USD 1.74 billion upgrade program to maintain designation-grade capability. Georgia’s FY2024 trauma report also noted that centers received only 7% of actual readiness costs in state funding, which leaves a wide operating gap for many providers. This funding mismatch continues to favor larger systems that can cross-subsidize readiness and absorb compliance costs more effectively than smaller standalone operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: In-House Scale Enables Clinical Continuity

In-house trauma facilities held 72.31% share in 2025, which made them the dominant operating model across the trauma care centers market. Their lead reflects the practical value of shared operating rooms, blood banks, imaging departments, and post-acute beds inside a broader hospital campus. That shared platform lowers the incremental cost of trauma readiness and supports better continuity between emergency treatment, surgery, and recovery. It also gives hospital groups more flexibility when they need to balance trauma demand against other acute care service lines.

Cross-departmental subsidization remains a major reason these facilities stay ahead because trauma readiness costs can be spread across a wider patient base. Standalone centers are still forecast to grow at an 8.38% CAGR through 2031, showing that purpose-built models are gaining traction in specific urban and peri-urban corridors. They are especially relevant where public hospital campuses are overcrowded and private operators see room to serve insured trauma volumes more directly. A 2025 study on trauma network expansion found that well-placed standalone units near rural communities can improve access without the full cost of building a complete hospital campus.

By Trauma Type: Falls Anchor Revenue, Motor Vehicle Injuries Accelerate

Falls accounted for 35.24% share in 2025, which kept them at the center of the trauma care centers market by revenue. This pattern is tied to the high incidence of hip fractures, pelvic injuries, and traumatic brain injuries among people aged 65 years and above. In mature health systems, these patients often need longer inpatient care and higher rehabilitation support than many younger cohorts. That makes falls both a large-volume and high-resource category for trauma operators.

Traffic-related injuries are projected to grow at an 8.52% CAGR through 2031, which makes them the fastest-growing trauma type. Continued motorization in low-income and middle-income regions, especially where powered 2-wheel transport is common, is keeping severe crash exposure elevated. Brain injury remains a smaller segment by volume but it consumes disproportionate ICU, neurosurgical, and neurorehabilitation capacity. Burn injury is also smaller by volume, yet it requires highly specialized wound care and clinical infrastructure that many general trauma wards cannot provide. Taken together, these patterns show that the trauma care centers market depends on a balanced case mix where large-volume falls support revenue while high-acuity traffic, brain, and burn cases drive capability investment.

By Service Type: Inpatient Complexity Drives Forward Investment

Outpatient services represented 56.26% of revenue in 2025, which shows that a large share of the trauma care centers market still comes from fractures, lacerations, and concussions that do not require admission. This segment benefits from throughput, lower length of stay, and wider accessibility within general emergency settings. It also gives providers a steady base of trauma-related encounters without the full staffing intensity of complex inpatient care. Even so, outpatient scale does not remove the need for strong inpatient back-up when acuity changes quickly.

Inpatient services are projected to grow at an 8.55% CAGR through 2031, which makes them the fastest-growing service type. Surviving trauma patients are presenting with more clinical complexity, which increases demand for sequential operations, critical care teams, and longer monitored stays. Rehabilitation is also moving closer to the center of care design because ACS guidance has raised expectations around timely rehabilitation planning and delivery. A 2026 meta-analysis on traumatic brain injury rehabilitation in intensive care found improved mobility scores at ICU discharge for patients receiving early rehabilitation, which supports earlier integration in the care pathway. As a result, the trauma care centers market is shifting service investment toward inpatient pathways that combine acute care and functional recovery more closely.

By Trauma Center Level: Level I Concentration and Level V Frontier Growth

Level I centers held 38.56% share of the trauma care centers market size in 2025, which reflects their concentration of the most complex and highest-revenue admissions. These centers anchor regional referral systems and carry the broadest mix of surgical, critical care, research, and teaching capabilities. Severe polytrauma, major vascular injury, and high-acuity traumatic brain injury tend to concentrate in this tier. That concentration keeps Level I centers central to revenue capture even when other designation levels expand faster.

Level II centers continue to serve wide community catchments and provide strong neurosurgical and orthopedic coverage, while still transferring selected cases upstream when needed. Level V centers are forecast to grow at a 9.65% CAGR through 2031 as health systems push triage and stabilization deeper into peri-urban and rural locations. This model improves time to assessment and referral without requiring the full capital and staffing profile of a Level I buildout. Lakeland Regional Health’s elevation to Florida’s 12th Level I trauma center in June 2026 also showed how systems move through staged designation upgrades over time. Level III and Level IV centers remain important middle tiers because they give the trauma care centers market a scalable base for regional network growth.

By Patient Age Group: Geriatric Complexity Redefines Operating Models

Adults aged 18 to 64 years held 48.33% share in 2025, which kept them as the largest patient group in the trauma care centers market. Their volume is tied to occupational injury, road crashes, and interpersonal violence that remain concentrated in working-age populations. This cohort supports steady admission flow across emergency, orthopedic, and surgical trauma pathways. It also keeps many urban trauma centers heavily exposed to labor-force and commuter injury patterns.

The geriatric segment is projected to grow at a 9.15% CAGR through 2031, which makes it the fastest-growing age group. Higher fall incidence, fragility fractures, longer stays, and greater rehabilitation referral needs are all shifting resource use toward older patients. That shift changes staffing needs because trauma teams increasingly need orthogeriatric coordination, longer discharge planning, and closer links to rehabilitation providers. Pediatric trauma remains the smallest age cohort by volume, yet it still demands premium institutional commitment and strict care standards. Northwell Health’s Cohen Children’s Medical Center earned its fourth ACS reverification as a Level 1 pediatric trauma center in September 2025, which illustrates the long-term investment needed in this part of the trauma care centers market.

By Mode of Admission: Air Transport Infrastructure Reshapes Catchment Economics

Ambulance-based admissions held 36.52% share in 2025, which kept ground EMS as the largest intake channel across the trauma care centers market. This reflects the continued dominance of urban and suburban transport patterns where road transfer times remain clinically workable. Ground ambulance pathways also integrate more easily with existing emergency department operations and regional dispatch systems. That makes them the default access route for a wide range of trauma acuity levels.

Air medical transport is forecast to grow at a 9.25% CAGR through 2031, which makes it the fastest-growing admission mode. Expansion is being supported by rural trauma network growth, new helipad capacity, and hospital efforts to widen the effective catchment radius for severe injury cases. HCA Houston Healthcare Kingwood’s USD 111 million expansion approved in 2025 included 2 rooftop helipads, 60 beds, and an expanded emergency department, which linked transport infrastructure to higher-level trauma ambitions. Walk-in and direct admissions still account for lower-acuity cases, while inter-hospital transfers remain essential for rural communities that rely on referral to Level I and Level II centers. Higher operating standards under FAA Part 135 and related night operations requirements are also pushing fleet investment toward larger health systems and specialized operators.

Geography Analysis

North America held 36.61% share in 2025, which kept it as the largest regional position in the trauma care centers market. The region benefits from one of the densest networks of designated trauma facilities and from established reimbursement structures tied to Medicare and Medicaid. The United States is still adding designation depth, with Lakeland Regional Health elevated to Florida’s 12th Level I trauma center in June 2026 and Cleveland Clinic pursuing Level I status at its main campus after securing a USD 50 million grant in March 2026. Workforce shortages and readiness funding gaps remain the region’s main structural limits, which continues to support consolidation toward large integrated systems.

Europe remains divided between mature western systems and central and eastern markets that are still expanding infrastructure. Austria’s AUVA Traumazentrum Brigittenau completed its modular expansion in mid-2026, while the broader Trauma-Campus Wien model will integrate acute and rehabilitation services under one structure from 2027. Germany added more capacity through a EUR 1.7 billion (USD 1.9 billion) investment in the northern campus expansion of Universitätsklinikum Würzburg and through the opening of Klinikum Bielefeld’s new emergency and intensive care center in June 2026. Norway’s BEST program met its founding goal in 2025, making team training compulsory across hospitals in the national trauma plan and reinforcing quality standardization as a regional benchmark.

Asia-Pacific is projected to grow at an 8.15% CAGR through 2031, making it the fastest-growing regional block in the trauma care centers market. That growth is supported by large population exposure, persistent road injury burdens, and wider public investment in trauma infrastructure and referral pathways. Governments and hospital operators across the region are expanding stabilization capacity, transfer coordination, and rehabilitation support to relieve pressure on tertiary facilities. Middle East and Africa remain smaller but are growing as GCC states incorporate trauma capacity into national healthcare transformation programs. South America also remains smaller, with Brazil leading urban trauma system investment and South Africa supporting gradual modernization that can widen future regional designation capacity.

Competitive Landscape

The trauma care centers market is moderately consolidated at the top tier, with large integrated systems holding clear advantages in designation breadth, capital access, and operational data depth. HCA Healthcare operates more than 105 trauma centers in the United States and treats more than 176,000 patients annually, which gives it the broadest visible trauma footprint among large commercial operators. That scale helps HCA feed outcome data into state agencies and national trauma repositories, which strengthens internal quality loops and supports future designation strategy. Academic systems such as Mayo Clinic, Johns Hopkins, Stanford Health Care, and Cleveland Clinic compete more through referral depth, research standing, and prestige around high-acuity care.

Cleveland Clinic’s January 2026 announcement that it is pursuing a Level I trauma center at its main campus shows how research-led systems use designation upgrades to deepen referral economics. Mid-market operators in the trauma care centers market are also expanding, though they are doing it more through targeted approvals and level upgrades than through broad greenfield building. CommonSpirit Health’s Level III designation for Saint Joseph London is one example of how systems add regional trauma credibility through selective capability expansion. Ascension’s state approval for a USD 20.6 million freestanding emergency department in Fairview in May 2026 shows the same emphasis on network reach and front-end emergency access.

Technology is becoming a stronger competitive divider across the trauma care centers market. Prehospital AI mortality prediction tools, validated in 2025, favor systems that already have stronger EMS data integration and faster triage feedback loops. The American Hospital Association reported in 2026 that Carilion Clinic’s interoperability link between ImageTrend Elite and Epic delivered more than 20,000 electronic EMS reports in its first year, which improved emergency department readiness and shortened EMS turnaround time. White-space opportunities remain in geriatric co-management programs, rural Level IV and Level V expansion, and earlier rehabilitation integration that ACS guidance increasingly expects. A 2026 JAMA Network Open study also warned that adding centers without proportionate mortality improvement may attract tighter scrutiny, which could push competition toward outcome proof rather than simple facility count growth.

Trauma Care Centers Industry Leaders

HCA Healthcare, Inc.

Tenet Healthcare Corporation

Ascension Health Alliance

CommonSpirit Health

Mayo Foundation for Medical Education and Research

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: India’s Bastar district announced that a new trauma center would soon open as part of a broader healthcare infrastructure upgrade in Chhattisgarh, aiming to improve access to emergency care in one of the country’s most underserved regions.

- June 2026: Lakeland Regional Health Medical Center received a Level I trauma center designation from the Florida Department of Health, making it the 12th such center in Florida. The center serves more than 4,400 patients annually and is expected to reduce transfer pressures on Level I centers in Tampa, Orlando, and Gainesville.

Global Trauma Care Centers Market Report Scope

As per the scope of the report, trauma care centers are specialized medical facilities equipped and staffed to provide comprehensive emergency care for patients suffering from traumatic injuries. These centers are designated based on their ability to deliver timely, multidisciplinary treatment, including resuscitation, surgery, critical care, and rehabilitation, aimed at improving survival rates and functional outcomes for trauma patients.

The trauma care centers market is segmented by facility type into in-house and standalone; by trauma type into falls, traffic-related injuries, stab, wound, and cut injuries, burn injuries, and brain injuries; by service type into outpatient, inpatient, and rehabilitation; by trauma center level into level I, level II, level III, level IV, and level V; by patient age group into adult, pediatric, and geriatric; by mode of admission into ambulance-based, walk-in and direct admission, air medical transport, and inter-hospital transfers; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| In-House |

| Standalone |

| Falls |

| Traffic-Related Injuries |

| Stab, Wound, and Cut Injuries |

| Burn Injury |

| Brain Injury |

| Outpatient |

| Inpatient |

| Rehabilitation |

| Level I |

| Level II |

| Level III |

| Level IV |

| Level V |

| Adult |

| Pediatric |

| Geriatric |

| Ambulance-Based |

| Walk-In and Direct Admission |

| Air Medical Transport |

| Inter-Hospital Transfers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Facility Type | In-House | |

| Standalone | ||

| By Trauma Type | Falls | |

| Traffic-Related Injuries | ||

| Stab, Wound, and Cut Injuries | ||

| Burn Injury | ||

| Brain Injury | ||

| By Service Type | Outpatient | |

| Inpatient | ||

| Rehabilitation | ||

| By Trauma Center Level | Level I | |

| Level II | ||

| Level III | ||

| Level IV | ||

| Level V | ||

| By Patient Age Group | Adult | |

| Pediatric | ||

| Geriatric | ||

| By Mode of Admission | Ambulance-Based | |

| Walk-In and Direct Admission | ||

| Air Medical Transport | ||

| Inter-Hospital Transfers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the trauma care centers sector?

The trauma care centers market size stands at USD 20.76 billion in 2026 and is forecast to reach USD 29.88 billion by 2031 at a 7.55% CAGR.

Which region leads trauma care center demand today?

North America held the largest regional share at 36.61% in 2025, supported by a dense trauma center network and mature reimbursement structures.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at an 8.15% CAGR through 2031, driven by population scale, road injury burden, and expanding trauma infrastructure.

Which service line is expanding the fastest in trauma care delivery?

Inpatient services are forecast to grow at an 8.55% CAGR through 2031 as surviving trauma patients need longer stays, critical care, and rehabilitation support.

Which patient group is reshaping care models the most?

Geriatric patients are projected to grow at a 9.15% CAGR through 2031, and their higher rates of falls, fragility fractures, and rehabilitation needs are changing staffing and pathway design.

What is the biggest operational challenge for providers?

The most persistent challenge is workforce scarcity, especially trauma surgeons and specialized critical care staff, along with high readiness costs for Level I and Level II centers.

Page last updated on: