Surgical Wound Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.30 Billion |

| Market Size (2031) | USD 21.20 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

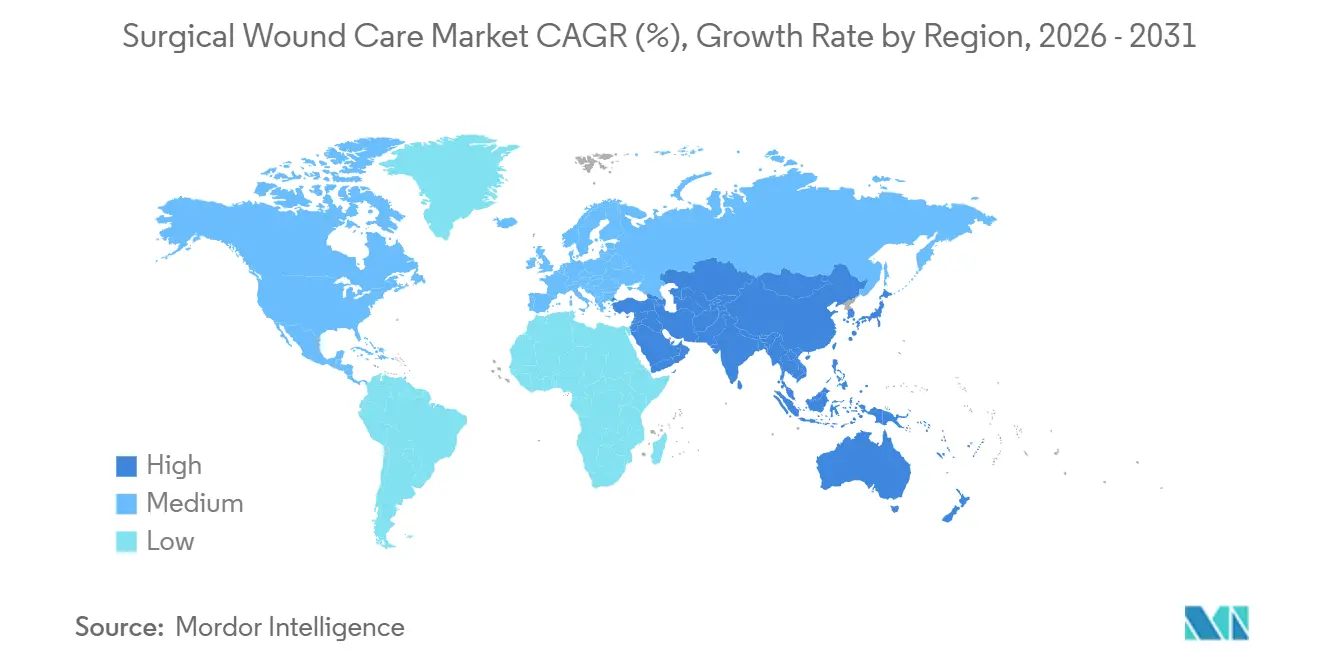

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Wound Care Market Analysis by Mordor Intelligence

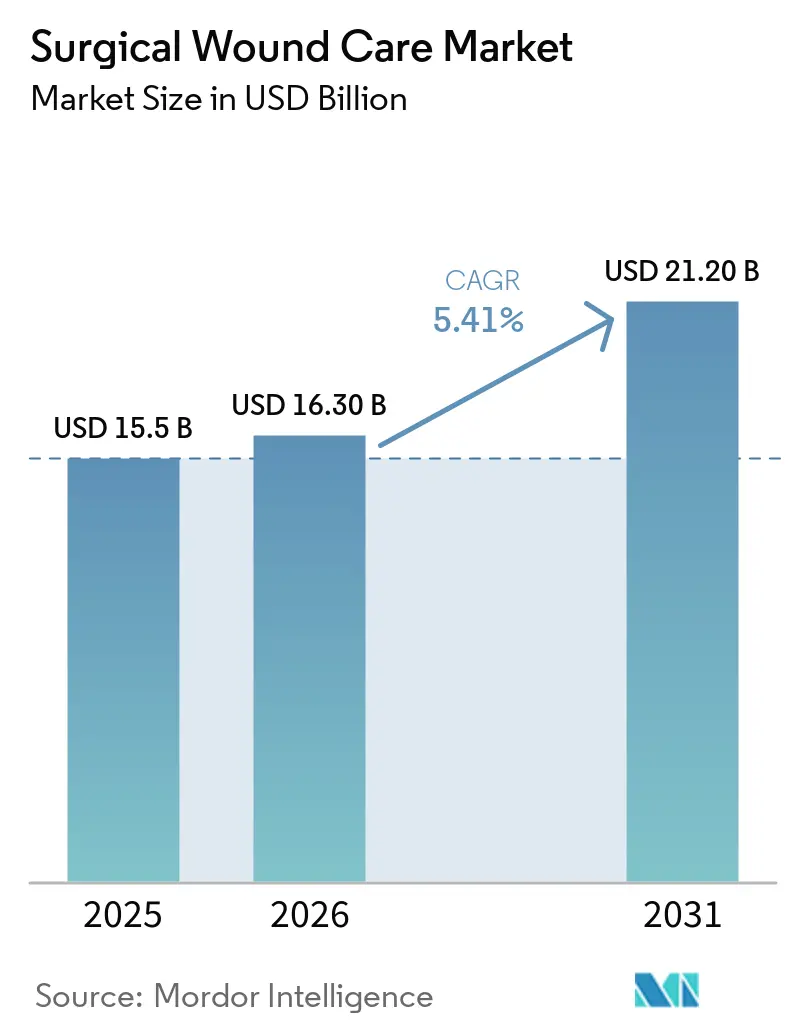

The Surgical Wound Care Market size is expected to increase from USD 15.5 billion in 2025 to USD 16.30 billion in 2026 and reach USD 21.20 billion by 2031, growing at a CAGR of 5.41% over 2026-2031.

Structural shifts in reimbursement, site-of-service migration, and rapid digitization are significantly transforming value creation, surpassing the impact of procedural volume growth. Hospital groups are complementing these changes with AI-enabled remote-monitoring platforms, reducing in-person visits by 30-40% and expanding the addressable base for data-driven postoperative care. Advancements in antimicrobial sutures, bioactive dressings, and peptide-based barriers continue to differentiate premium products, while the shift toward ambulatory surgical centers (ASCs) is driving increased demand for single-use, pre-packaged closure kits.

Key Report Takeaways

- By wound type, chronic wounds led with 59.80% revenue share in 2025; the segment is forecast to advance at a 5.91% CAGR through 2031.

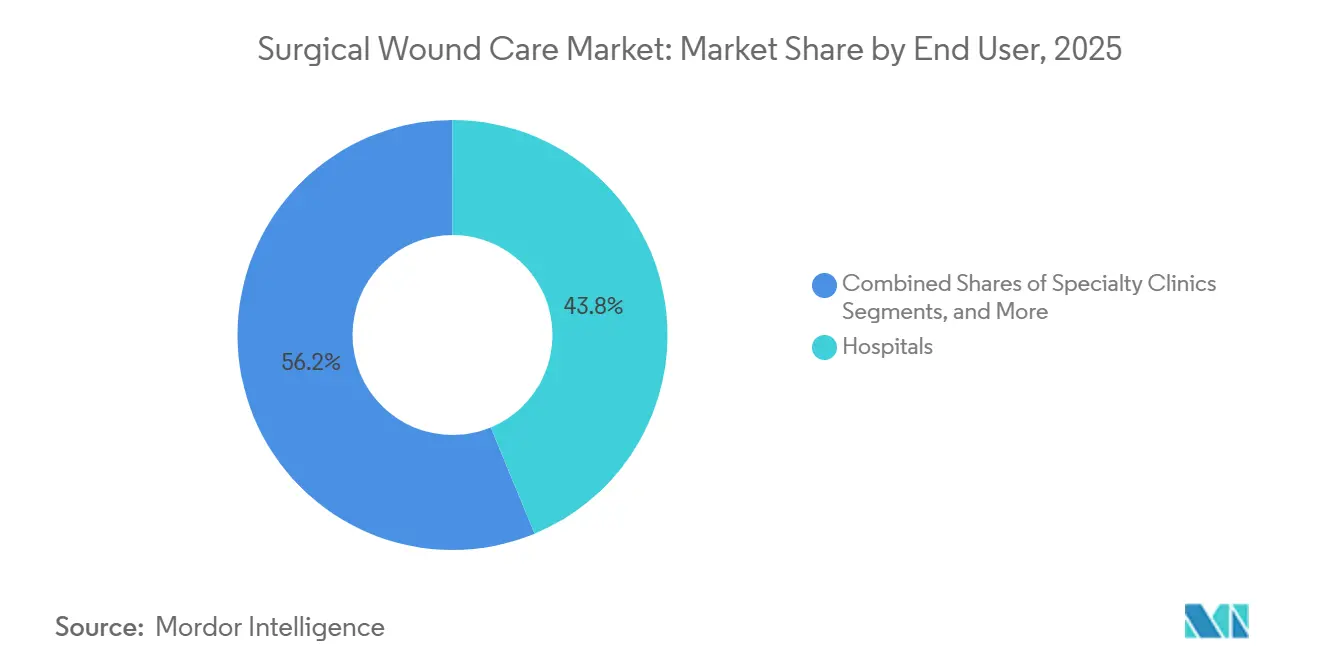

- By end user, hospitals held 43.76% of the surgical wound care market share in 2025, while ASCs are poised for the fastest growth at a 5.76% CAGR between 2026 and 2031.

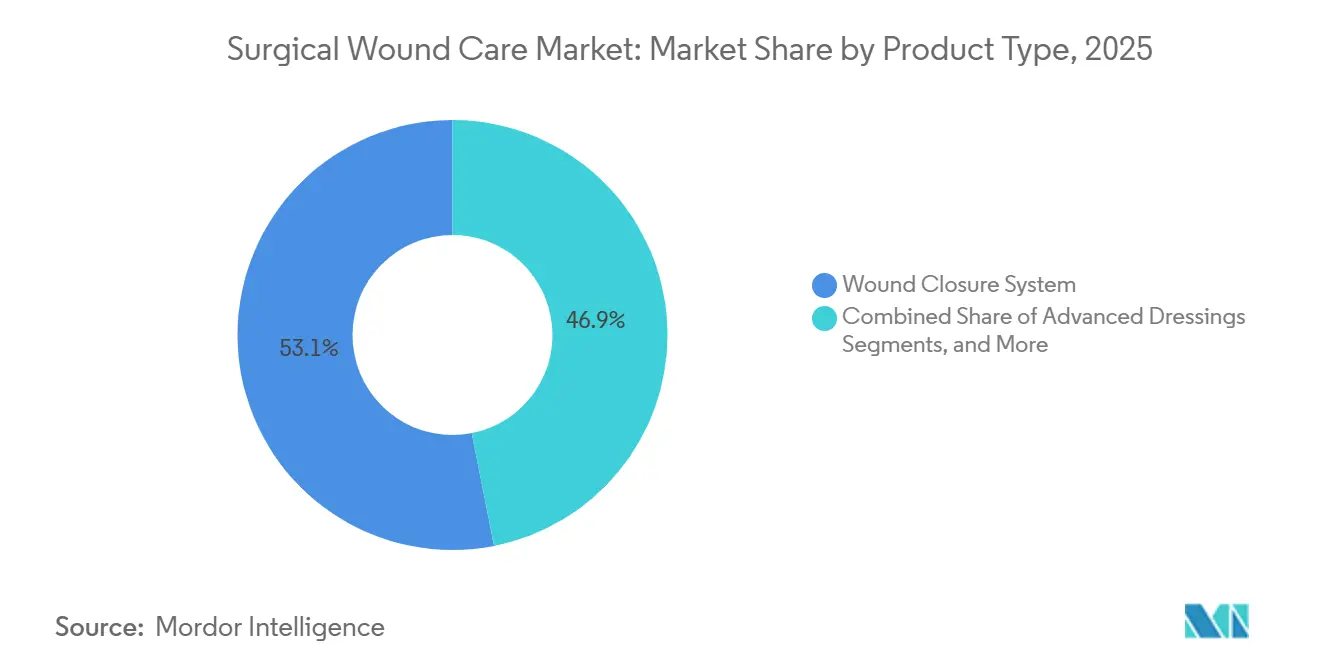

- By product category, wound-closure systems captured 53.10% of the surgical wound care market size in 2025 and remain integral across surgical specialties.

- By geography, North America captured 41.98% share in 2025, although Asia-Pacific is pacing the global field at 5.86% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Surgical Wound Care Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing adoption of minimally invasive surgical procedures | +0.9% | Global, led by North America & Europe | Medium term (2–4 years) |

| Rising prevalence of chronic diseases requiring surgical interventions | +1.2% | Global, acute in Asia-Pacific & North America | Long term (≥4 years) |

| Increasing volume of ambulatory surgeries | +0.8% | North America & Europe | Short term (≤2 years) |

| Technological advancements in antimicrobial sutures & dressings | +1.0% | Global | Medium term (2–4 years) |

| Surge in surgical site infections prompting preventive care | +0.7% | Global, pronounced in LMICs | Short term (≤2 years) |

| Shift to outpatient wound centers integrated with AI-enabled remote monitoring | +0.6% | North America, early adoption in Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Minimally Invasive Surgical Procedures

Robotic and laparoscopic techniques are increasingly being adopted due to their ability to minimize incision sizes, reduce tissue trauma, and shorten hospital stays. These advancements have led to a decline in the use of traditional gauze while driving demand for barbed sutures, tissue adhesives, and thin antimicrobial films. This shift has also contributed to a reduction in infection rates, with robotic procedures showing a 1.2% infection rate compared to 4.7% for open hysterectomies. Smaller wounds are shifting postoperative care to outpatient or home settings, where telehealth monitoring enhances adherence and reduces readmission risks. In response, manufacturers are expanding their product portfolios to include self-adhering antimicrobial dressings designed for delicate tissue planes and robotic workflows.

Rising Prevalence of Chronic Diseases Requiring Surgical Interventions

The increasing prevalence of chronic conditions such as diabetes, obesity, and peripheral vascular disease is complicating surgical wound management and prolonging healing times. Diabetic foot ulcers affect 6.3% of the population, with a lifetime risk of 34%, contributing to approximately 1 million diabetes-related amputations annually.[1]U.S. Centers for Medicare & Medicaid Services, “CMS Finalizes 2026 Medicare Payment Policies,” CMS.gov In the United States, direct treatment costs range between USD 9-13 billion annually, with 80% of amputations preceded by a foot ulcer. Although guidelines recommend maintaining peri-operative HbA1c levels at 8% and intra-operative glucose levels between 100-180 mg/dL by 2026, compliance challenges in community hospitals continue to result in higher infection rates. These challenges are driving the development of advanced solutions such as bioactive collagen matrices, peptide-infused barriers, and growth-factor-laden foams, which aim to stimulate stalled angiogenesis and accelerate the inflammatory phase.

Increasing Volume of Ambulatory Surgeries

Ambulatory surgical centers (ASCs) performed over 60 million procedures across 12,007 facilities in the United States in 2025. The segment is projected to reach USD 80.60 billion by 2035, growing at a CAGR of 6.30%. To support this growth, 560 new codes were added to the ASC covered-procedures list for 2026, along with a 2.6% increase in the payment conversion factor.[2]: U.S. Food and Drug Administration, “De Novo Clearance for Amferia Peptide-Based Wound Dressing,” fda.gov This shift is enabling the transfer of suitable orthopedic, gastrointestinal, and low-risk cardiovascular cases from high-cost inpatient settings to more cost-effective ASCs. ASCs are increasingly adopting single-use kits that streamline turnover and reduce inventory costs, driving the demand for integrated suture-stapler devices and self-adhering antimicrobial dressings that align with rapid case cycles.

Technological Advancements in Antimicrobial Sutures & Dressings

Recent regulatory developments highlight a shift from passive barriers to active biochemical interventions in wound care. In February 2026, a peptide-based dressing received regulatory clearance, marking the introduction of a synthetic antimicrobial peptide platform for incisional use. Additionally, an antimicrobial irrigation solution was approved for intraoperative use in January 2026, complementing existing topical regimens. Research conducted in 2025 demonstrated that dual-drug sutures containing chlorhexidine and dexamethasone reduced colorectal infection rates by 42% compared to uncoated sutures. These innovations are gaining traction, particularly among diabetic and immunocompromised patients.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost of advanced surgical wound care products | -0.5% | Global, acute in emerging markets | Medium term (2–4 years) |

| Reimbursement challenges in emerging economies | -0.4% | Asia-Pacific, Middle East & Africa, South America | Long term (≥4 years) |

| Sterile supply-chain disruptions due to geopolitical conflicts | -0.3% | Global, pronounced in Europe & Middle East | Short term (≤2 years) |

| Growing preference for non-surgical treatment alternatives | -0.2% | North America & Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Costs Hinder Adoption of Advanced Surgical Wound Care Products

Premium closures and bioactive dressings are priced 3-10 times higher than standard gauze and nylon sutures, limiting their adoption in cost-sensitive regions. Newly introduced antimicrobial-peptide dressings are sold at USD 15-25 per 10×10 cm sheet, compared to USD 2-4 for traditional foams. Negative-pressure wound-therapy (NPWT) systems, such as AOTI’s NEXA, require an upfront investment of USD 1,500-3,000, excluding disposables, which discourages adoption in resource-constrained hospitals. Supply-chain disruptions in 2025 caused a 50% increase in the cost of polymer and aluminum inputs in India, driving up overall device prices. As a result, budget-constrained facilities often resort to basic care, leading to persistently high infection rates.

Emerging Economies Face Reimbursement Hurdles

In emerging markets, public-sector insurance programs typically cover only basic dressings, leaving patients to bear the cost of advanced options. In India, the PM-JAY scheme provides annual coverage of up to INR 500,000 (USD 6,000), but utilization is concentrated in six states and private centers, where out-of-pocket expenses frequently exceed the coverage limit. In 2024, the cesarean-section rate in urban India reached 32.3%, compared to 17.6% in rural areas, highlighting significant disparities in access. Similarly, insurers in Latin America and Africa limit reimbursements to basic gauze and tape, slowing the adoption of advanced peptide dressings and antimicrobial foams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Closure Systems Anchor Revenue, Advanced Dressings Lead Innovation

In 2025, wound-closure systems, considered essential in surgeries, accounted for 53.10% of the surgical wound care market size. In March 2026, Smith+Nephew introduced ALLEVYN COMPLETE CARE, a product designed to manage high-exudate wounds by combining silicone contact layers with superabsorbent foam cores. Advanced dressings, enhanced by antimicrobial peptides, collagen matrices, and smart foams, are projected to grow at the fastest rate of 5.83% CAGR through 2031. ConvaTec’s AQUACEL Ag Foam continues to gain traction in burn units, while Freudenberg’s Tacnera is increasingly used for pressure ulcer prevention in long-term care settings.

Surgical sealants and hemostats are becoming more relevant in minimally invasive and robotic procedures, where suture placement can be challenging. In February 2026, Baxter launched Hemopatch, designed for rapid hemostasis in cardiovascular and hepatobiliary applications. Grifols’ VISTASEAL expanded its pediatric labeling in October 2024, addressing congenital heart surgeries.

By Wound Type: Chronic Wounds Dominate, Driven by Diabetes and Aging

Chronic wounds held 59.80% of the surgical wound care market share in 2025 and are expected to grow at a rate of 5.91% through 2031. In the United States, diabetic foot ulcers, which account for 80% of lower-limb amputations, incur annual costs of USD 9-13 billion. Pressure and venous leg ulcers remain prevalent among aging and immobile populations. Acute wounds benefit from advancements in perioperative care, with infection rates for robotic hysterectomies in the United Kingdom at 1.2%, compared to 4.7% for open surgeries.

By End User: Hospitals Lead, ASCs Surge on Payment Tailwinds

In 2025, hospitals captured 43.76% of the revenue, driven by their ability to handle complex cases and provide intensive chronic-wound services. The ASC segment is forecast to grow at a rate of 5.76% from 2026-2031, supported by reimbursement increases and the addition of 560 new ASC-eligible procedures. Orthopedics accounts for approximately 30.22% of ASC volume, with cardiology and gastroenterology also experiencing growth. Following the implementation of flat-rate skin-substitute payments, which removed an anticipated USD 19.6 billion from the 2026 spend, specialty wound clinics are consolidating or affiliating with hospitals.

Geography Analysis

In 2025, North America accounted for 41.98% of the revenue, driven by ASC expansion, high per-capita spending, and a robust payer infrastructure in the United States. Reimbursement reforms are driving clinic consolidation and reinforcing hospital dominance, while also creating opportunities for AI-enabled home monitoring solutions. Canada and Mexico contribute smaller shares but are experiencing growth due to aging populations and increasing diabetes prevalence.

Asia-Pacific is projected to achieve a 5.86% CAGR from 2026 to 2031, supported by rising surgical volumes, new insurance initiatives, and infrastructure investments in China, India, and Japan. India’s PM-JAY scheme, despite its coverage limitations, is expanding procedural access, although the private sector continues to dominate. Japan, where 28% of the population is aged 65 or older, is scaling up pressure ulcer prevention and chronic wound care programs. South Korea and Australia are deploying AI-integrated imaging solutions to enhance healthcare delivery.

Europe maintains steady growth due to universal healthcare coverage. However, supply chain disruptions caused by geopolitical tensions are increasing device costs, prompting providers to explore regional sourcing strategies. The Middle East & Africa and South America, despite facing reimbursement challenges, are seeing incremental growth through private hospitals catering to medical tourism and expatriate communities.

Competitive Landscape

The surgical wound care market is moderately fragmented. The top players, Smith+Nephew, Mölnlycke, ConvaTec, and Johnson & Johnson (Ethicon), collectively account for approximately 40-45% of the market share. ConvaTec, through its Accelerate strategy announced in April 2026, aims to achieve high-single-digit growth by integrating AQUACEL Ag Foam with its digital adherence platforms. 3M is leveraging its V.A.C. NPWT expertise to introduce lighter, battery-efficient pumps designed for home use. Mölnlycke has committed EUR 115 million (USD 135 million) to expand its foam-dressing production capacity in its Maine facility by 30% by 2027. Baxter’s Hemopatch and Grifols’ extended VISTASEAL labeling underscore the intensifying competition in the sealants segment. Additionally, start-ups are focusing on AI-enabled imaging and peptide-based dressings, often licensing their technologies to established players for scaling operations.

Competition is intensifying in the home-based NPWT segment, with the FDA approving AOTI’s NEXA in August 2024, Cork Medical’s Versa in 2025, and Alleva Medical’s extriCARE 1000 in October 2025. Integrated device-software solutions are becoming a standard requirement as payers increasingly tie reimbursements to documented healing outcomes and reduced hospital readmissions.

Surgical Wound Care Industry Leaders

Mölnlycke Health Care

B. Braun SE

Baxter International Inc.

coloplast a/s

convatec group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Smith+Nephew launched ALLEVYN COMPLETE CARE multi-layer foam dressing for high-exudate wounds.

- February 2026: FDA granted De Novo clearance to Amferia’s peptide-based dressing, the first synthetic antimicrobial peptide platform for surgical incisions.

- February 2026: Baxter introduced Hemopatch collagen hemostat for cardiovascular and hepatobiliary applications.

- February 2026: Dynarex rolled out Dürma+ portable NPWT system with smartphone connectivity.

- June 2025: Mölnlycke announced a EUR 115 million expansion of its Brunswick, Maine, plant to boost foam-dressing capacity.

Global Surgical Wound Care Market Report Scope

As per the scope of the report, surgical wound care is the specialized, aseptic management of incisions made during surgery, designed to promote healing, prevent infections, and manage complications. It involves cleaning, dressing changes, and monitoring for infection. Key actions include washing hands, inspecting for drainage or redness, changing dressings, and showering after a specified time.

The segmentation of the surgical wound care market is based on product type, wound type, end user, and geography. By product type, the market is segmented into traditional products, advanced dressings, sutures & stapling devices, surgical sealants & glues, hemostats, and anti-infective agents. By wound type, the market is segmented into acute wounds, incisional wounds, traumatic wounds, chronic wounds, diabetic foot ulcers, pressure ulcers, and venous leg ulcers. By end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and home healthcare. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Wound Closure System |

| Advanced Dressings |

| Sutures & Stapling Devices |

| Surgical Sealants & Glues |

| Hemostats |

| Anti-infective Agents |

| Acute Wounds | Incisional Wounds |

| Traumatic Wounds | |

| Chronic Wounds | Diabetic Foot Ulcers |

| Pressure Ulcers | |

| Venous Leg Ulcers |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Home Healthcare |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wound Closure System | |

| Advanced Dressings | ||

| Sutures & Stapling Devices | ||

| Surgical Sealants & Glues | ||

| Hemostats | ||

| Anti-infective Agents | ||

| By Wound Type | Acute Wounds | Incisional Wounds |

| Traumatic Wounds | ||

| Chronic Wounds | Diabetic Foot Ulcers | |

| Pressure Ulcers | ||

| Venous Leg Ulcers | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Home Healthcare | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Surgical wound care market CAGR to 2031?

The surgical wound care market is projected to expand at a 5.41% CAGR from 2026-2031.

Which product category leads revenue?

Wound-closure systems hold 53.10% revenue share, underlining their indispensable role in every surgical specialty.

Fastest-growing segment by end user?

Ambulatory surgical centers are forecast to advance at a 5.76% CAGR through 2031 as CMS reimbursement encourages site-of-care migration.

Region with highest growth potential?

Asia-Pacific is expected to post the quickest 5.86% CAGR to 2031, buoyed by rising surgical volumes and insurance expansion.

Key driver shaping product innovation?

Regulatory approvals for antimicrobial peptide dressings and dual-drug sutures are steering the market toward active infection-control technologies.

Page last updated on: