Complete Blood Count Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

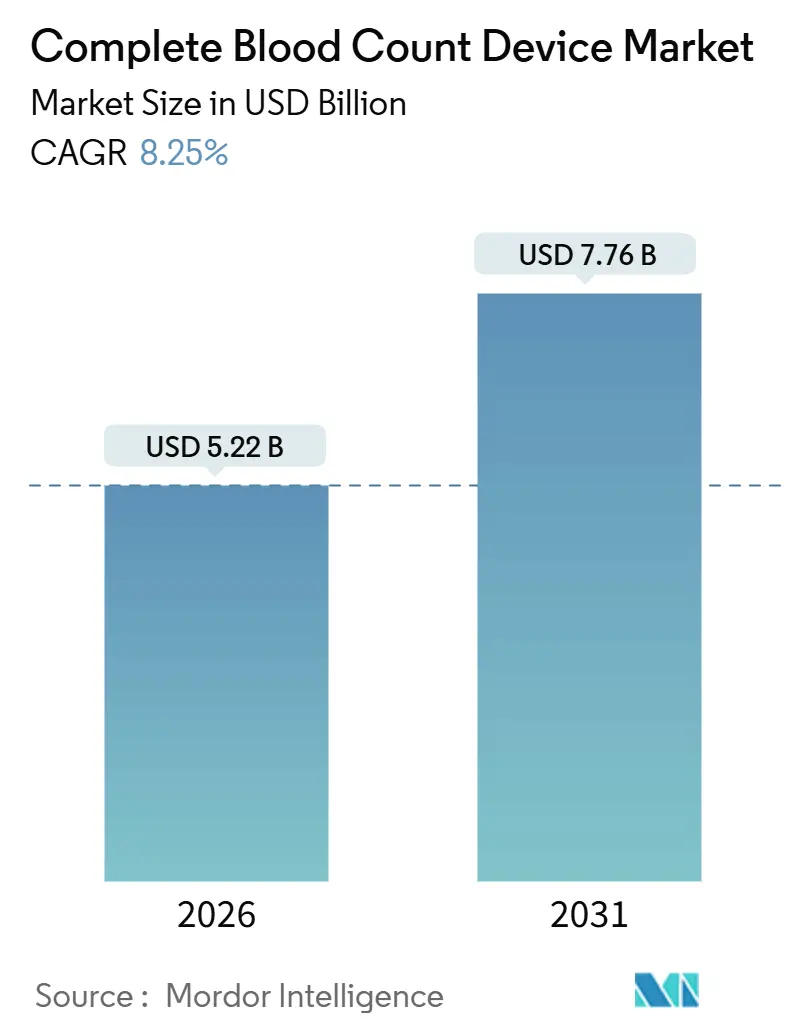

| Market Size (2026) | USD 5.22 Billion |

| Market Size (2031) | USD 7.76 Billion |

| Growth Rate (2026 - 2031) | 8.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Complete Blood Count Device Market Analysis by Mordor Intelligence

The Complete Blood Count Device Market size is estimated at USD 5.22 billion in 2026, and is expected to reach USD 7.76 billion by 2031, at a CAGR of 8.25% during the forecast period (2026-2031).

This expansion is underpinned by rising chemotherapy-related neutropenia monitoring protocols, rapid integration of artificial intelligence (AI) into differential counting, and national incentives that localize manufacturing to lower logistics risk. Mandatory post-chemotherapy CBC testing, typically scheduled 7–12 days after infusion, is pushing weekly sample volumes higher in oncology clinics. AI-enabled cell classifiers now flag immature granulocytes with up to 98% accuracy, easing pressure on over-extended laboratory scientists. Meanwhile, India’s USD 1.4 billion Production-Linked Incentive (PLI) program and similar measures in China are catalyzing regional production hubs that shorten supply chains and lower import duties.[1]Invest India, “Production Linked Incentive Schemes in India,” investindia.gov.in Even so, a 2.5% Medicare reimbursement cut for automated hemograms implemented in 2025 has compressed margins at independent laboratories and accelerated their acquisition by health-system networks.

Key Report Takeaways

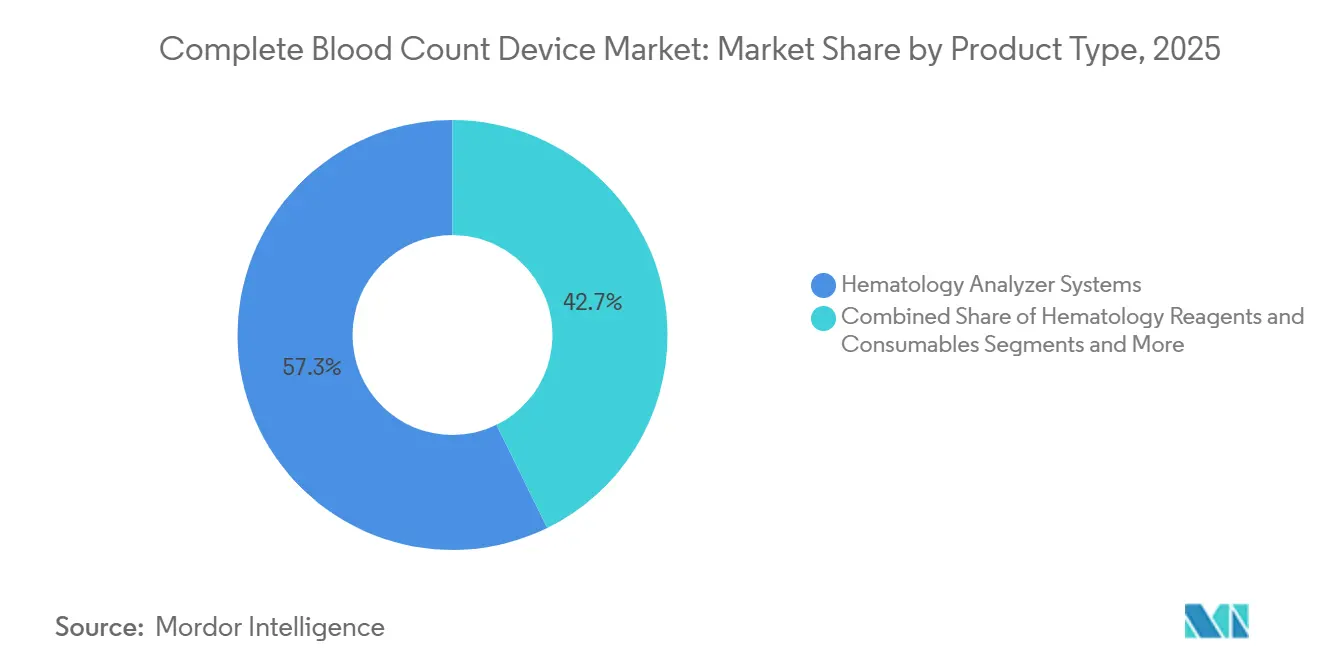

- By product type, hematology analyzer systems led with 57.26% revenue share in 2025; slide stainers and peripheral equipment are forecast to expand at an 11.63% CAGR to 2031.

- By modality, benchtop analyzers held 51.72% of the complete blood count device market share in 2025, while point-of-care and portable analyzers are projected to grow at 12.68% through 2031.

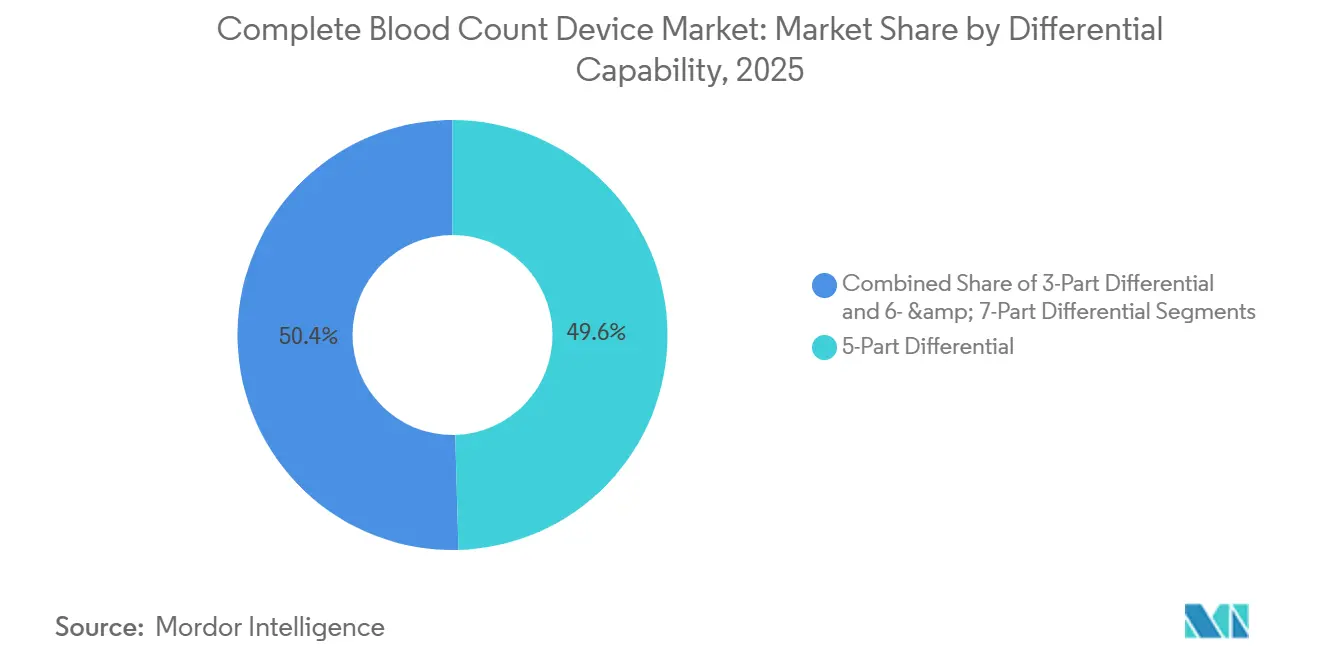

- By differential capability, 5-part systems accounted for a 49.56% share of the complete blood count device market size in 2025, whereas 6- and 7-part platforms are advancing at a 12.23% CAGR through 2031.

- By end user, hospitals captured 49.74% revenue share in 2025; blood banks and transfusion centers are set to expand at an 11.32% CAGR to 2031.

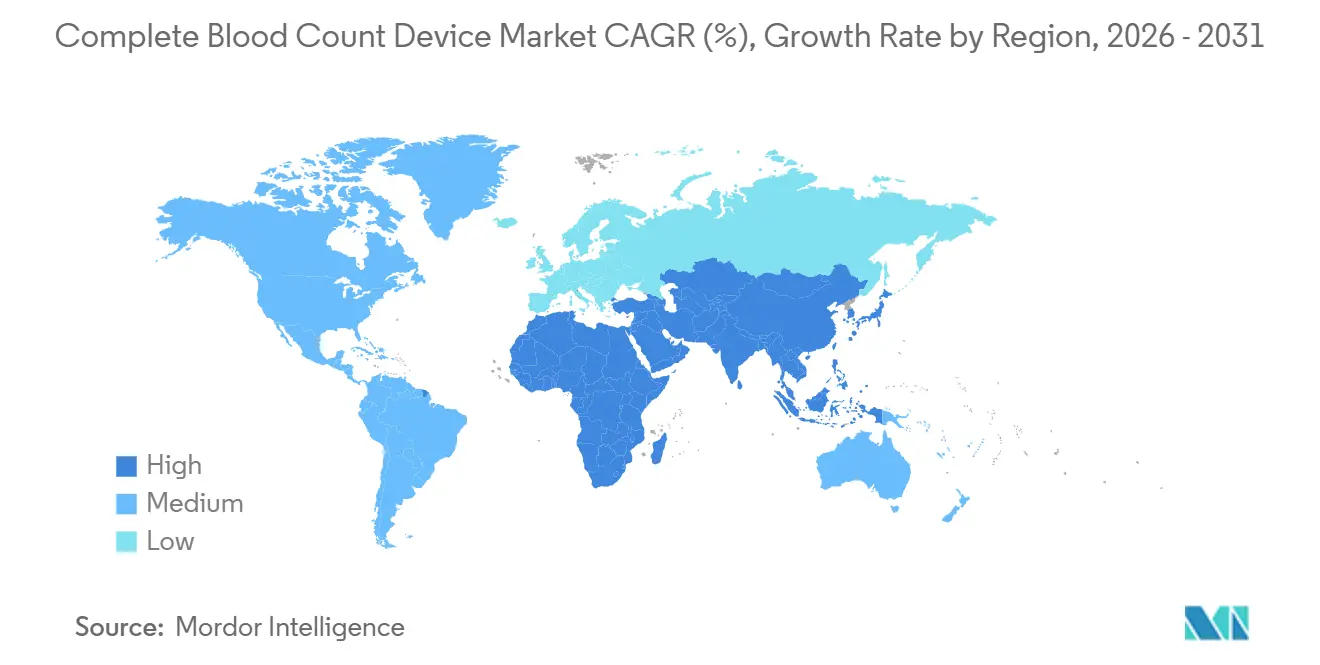

- By region, North America led with 48.13% revenue share in 2025, but Asia-Pacific is forecast to register the fastest 10.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Complete Blood Count Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded Access to Point-of-Care Hematology Testing | +1.8% | Global, early gains in rural North America and APAC | Medium term (2-4 years) |

| Integration of AI-Based Differential Counting | +2.1% | North America and EU, spill-over to APAC | Short term (≤2 years) |

| Rising Oncology Incidence & Chemo-Therapy Monitoring | +1.5% | Global | Long term (≥4 years) |

| Aging Population in Emerging Markets | +1.3% | APAC core, spill-over to MEA and South America | Long term (≥4 years) |

| Regulatory Push for Preventive Screening Programs | +0.9% | EU, China, India | Medium term (2-4 years) |

| Supply-Chain Localization Incentives | +0.7% | India, China, select South American markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration of AI-Based Differential Counting

Artificial intelligence now automates white blood cell identification with sensitivities exceeding 95% for immature granulocytes, slashing manual review workloads. Sysmex’s DI-60 digital morphology analyzer pre-classifies 400 cells per slide in under two minutes and highlights blasts for technologist confirmation.[2]Sysmex Corporation, “DI-60 Digital Cell Morphology Analyzer,” sysmex.com Siemens Healthineers embedded image-based infectious disease screening into the Atellica HEMA 570 and 580 platforms in 2024 after training on 1.2 million annotated cells. Beckman Coulter’s FDA-cleared Monocyte Distribution Width biomarker exploits impedance data to stratify sepsis risk four hours sooner than conventional approaches. Although slide-stain volumes fall inside high-throughput laboratories, AI expansion boosts demand for digital microscopy systems that pair seamlessly with hematology analyzers. ISO 15189 compliance requires each lab to validate algorithm performance against manual differentials, often extending adoption timelines by up to nine months.

Expanded Access to Point-of-Care Hematology Testing

Point-of-care (POC) analyzers are migrating from emergency rooms to pharmacies and primary clinics following CLIA-waived clearances. EKF Diagnostics gained FDA approval for the DiaSpect hemoglobin meter in September 2025, letting pharmacists screen anemia during medication reviews. Sysmex’s XW-100 runs an eight-parameter CBC from a 10 µL capillary sample in two minutes, fitting pediatric and geriatric needs. Roche’s 4.2 kg cobas m 511 operates on battery power for mobile clinics in sub-Saharan Africa and rural India. Despite identical Medicare reimbursement of USD 10.87 regardless of test venue, decentralized settings value the rapid turnaround that avoids sample transport delays. A two-tier market is forming, with high-throughput benchtop analyzers supporting central labs while compact devices handle time-critical decisions in decentralized care.

Rising Oncology Incidence & Chemo-Therapy Monitoring

National Comprehensive Cancer Network guidelines issued in 2024 mandate CBC monitoring 7–12 days after cytotoxic infusion to spot neutropenia below 1,000 cells/µL, elevating recurring testing volumes in oncology centers.[3]National Comprehensive Cancer Network, “Hematologic Toxicities, Version 1.2024,” National Comprehensive Cancer Network, nccn.orgThe American Cancer Society counted 2 million new U.S. cancer diagnoses in 2024, 70% of whom required serial CBCs every two to three weeks. Mindray’s BC-7500 CRP analyzer combines five-part differentials with C-reactive protein to distinguish infection from tumor inflammation in a single run. Neutropenic fever triggers 60,000 hospitalizations annually in the United States at a median USD 19,000 per stay, motivating payers to reimburse point-of-care CBC testing that averts emergency visits. Regulatory classifications still treat oncology-specific analyzers the same as general devices, so manufacturers cannot expedite clearances despite distinct clinical workflows.

Aging Population in Emerging Markets

Asia-Pacific’s population aged 65+ will climb from 395 million in 2024 to 844 million by 2050, doubling chronic disease prevalence and routine hematology demand. India’s elderly cohort is set to reach 14.9% by 2050, increasing benchtop analyzer usage in secondary and tertiary hospitals that manage anemia and kidney-related disorders. China’s health authority mandated annual exams for citizens 65+ in 2024, adding 140 million tests per year and reinforcing domestic supplier preferences such as Mindray. Latin American public systems face budget constraints, favoring reagent-rental models that delay capital outlay but lock in long-term reagent contracts. Ultimately, fast-growing elderly populations lift reagent consumption faster than new instrument placements, tilting value toward consumable vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment & Maintenance Cost | -0.8% | Global, acute in South America and MEA | Short term (≤2 years) |

| Data Integration & Interoperability Issues | -0.6% | North America and EU | Medium term (2-4 years) |

| Shortage of Skilled Laboratory Technicians | -0.5% | Global, acute in rural North America and APAC | Long term (≥4 years) |

| Declining Reimbursement for Routine Blood Tests | -0.9% | United States, spill-over to EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Declining Reimbursement for Routine Blood Tests

Medicare trimmed automated hemogram reimbursement by 2.5% for 2025, dropping rates from USD 11.15 to USD 10.87 and shrinking independent lab margins that already range between 8% and 12%. The American Clinical Laboratory Association notes cumulative cuts of 15% since 2018, pushing labs into volume-based reagent contracts that bind them to single vendors for up to seven years. Quest Diagnostics and Labcorp performed 380 million hematology tests in 2024 and can absorb lower pricing, but small regional chains are exiting the service or selling to hospital systems. European payers often shadow Medicare trends, extending downward price pressure globally. The result is a bifurcated landscape in which high-volume labs automate aggressively while low-volume sites outsource testing.

Data Integration & Interoperability Issues

generated by modern analyzers, forcing middleware purchases that add USD 15,000–25,000 in annual fees. The Integrating the Healthcare Enterprise group published a FHIR-based Laboratory Analytical Workflow profile in 2024, yet adoption remains below 20% across installed devices. Vendor-specific data managers such as Siemens’ Atellica Data Manager or Beckman’s Remisol Advance improve connectivity but create vendor lock-in. Sysmex’s Extended IPU sends critical values to clinician smartphones in real time, but only within its own ecosystem. ISO 15189 accreditation demands documented verification of every interface, adding three to six months to analyzer switch-overs and discouraging labs from adopting multivendor fleets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Analyzers Anchor Revenue, Stainers Capture Growth

Hematology analyzer systems generated 57.26% of 2025 revenue, reflecting widespread replacement of seven-year-old instruments with AI-ready models, while slide stainers and peripheral gear are pacing the complete blood count device market at an 11.63% CAGR toward 2031. Premium analyzers list between USD 150,000 and USD 300,000, yet lifetime reagent income accounts for 60–70% of total value. Slide stainers have re-emerged thanks to integrated digital morphology offerings that archive slides for remote pathologist review, fueling double-digit growth. Closed-system analyzers from Siemens and Beckman use barcode-protected reagents that block third-party supplies, whereas Horiba’s Yumizen line operates as an open system for cost-sensitive labs. The reagent-first revenue model explains why consumables manufacturers aggressively court high-volume laboratories, even in flat instrument-placement years.

The reagent and consumable business benefits each time testing volumes rise—whether due to oncology protocols or expanded preventive screening—so vendors prioritize assay menu extensions that lift per-sample revenue. Peripheral automation, including robotic sample handlers, is equally hot; Roche’s cobas connection modules route tubes between hematology and chemistry benches, eliminating 80% of manual touches and lowering error rates. FDA 510(k) filings now require reagent performance data across broad hematocrit ranges, lengthening development cycles but also raising barriers to entry for latecomers.

By Modality: Benchtop Dominance Challenged by Portable Surge

Benchtop analyzers retained a 51.72% share in 2025 and remain essential inside high-throughput core laboratories that process 500–2,000 samples daily. However, portable and point-of-care systems are expanding at 12.68% through 2031, the fastest modality growth, as emergency departments, rural clinics, and pharmacies value two-minute turnaround times over sheer throughput. Abbott’s cartridge-based i-STAT delivers eight-parameter CBCs in handheld form, while Sysmex’s XW-100 serves physician offices performing fewer than 50 daily tests. Benchtop vendors have responded by introducing modular footprints such as Siemens’ Atellica HEMA 520–580 series, allowing laboratories to add capacity in 20-sample-per-hour increments.

Automated workcells that marry hematology, coagulation, and urinalysis onto one conveyor belt are proliferating at reference laboratories aiming to slash labor costs by up to 40%. CLIA classifications still restrict portable analyzers to waived or moderate-complexity tasks, limiting their diagnostic scope, yet their sheer convenience is reshaping purchase priorities for outpatient networks.

By Differential Capability: Advanced Counts Drive Premium Tier

Five-part differential analyzers controlled 49.56% of revenue in 2025, but six- and seven-part platforms are scaling at 12.23% as clinicians increasingly rely on immature granulocyte and nucleated red blood cell data to flag sepsis and bone marrow recovery. Siemens’ Atellica HEMA 580 offers built-in immature granulocyte measurement that emergency physicians employ for rapid sepsis triage. Sysmex’s fluorescence cytometry-based XN-Series quantifies nucleated red cells used in diagnosing myelodysplastic syndromes. Meanwhile, 3-part systems are gradually disappearing as reimbursement models and clinical guidelines incentivize richer data.

Novel biomarkers extracted from existing hardware extend analyzer lifespans. Beckman’s Monocyte Distribution Width, cleared in 2023, illustrates this software-led value extraction. Cost-sensitive markets still deploy Horiba’s sub-USD 30,000 systems that offer five-part capability without immature granulocyte counts. ISO 15189 validations of advanced differentials require at least 100 paired microscopic reviews per lab, slowing but not stopping upgrades.

By End User: Hospitals Lead, Blood Banks Accelerate

Hospitals consumed 49.74% of devices in 2025, driven by inpatient and emergency testing volumes that can top 500 CBCs per day in tertiary centers. Blood banks and transfusion services, although smaller, are rising at an 11.32% CAGR thanks to American Association of Blood Banks mandates requiring hemoglobin verification within 24 hours of transfusion. Diagnostic laboratories remain the second-largest segment and invest heavily in automated workcells that cut labor costs by a third. Research institutes and pharmaceutical CROs, while niche, demand open data architectures for machine-learning projects, prompting vendors to release software development kits.

Hospitals are consolidating outpatient satellite labs into centralized, 24-hour core facilities, installing portable analyzers in clinics only where immediate results alter care plans. Blood banks prefer compact benchtop units that handle 60 samples hourly yet occupy minimal floor space, such as Horiba’s Yumizen H550 and Boule’s Medonic range. Veterinary and pharma research users look for analyzers that accept species-specific reagents. Because FDA 510(k) pathways for each configuration average nine months, most manufacturers release modular software options rather than hardware revisions.

Geography Analysis

North America dominated with 48.13% of 2025 revenue due to high test volumes and rapid hospital consolidation, yet reimbursement cuts and staff shortages temper growth. Sysmex generated JPY 225.6 billion (USD 1.5 billion) from hematology in fiscal 2024, with 35% stemming from North America. Canada and Mexico are expanding pharmacy-based screening after Health Canada cleared EKF’s DiaSpect in October 2025. The American Society for Clinical Pathology reported an 11% technologist vacancy in 2023, spurring adoption of fully automated workcells from Roche and Beckman Coulter that minimize manual touchpoints. Stringent CLIA and FDA rules add 12–18 months to U.S. product launches compared with less-regulated regions.

Asia-Pacific is pacing the complete blood count device market at a 10.53% CAGR through 2031, propelled by China’s mandate for annual senior health exams that alone create 140 million extra tests each year. Mindray booked RMB 20.15 billion (USD 2.77 billion) in first-half 2024 revenue, underscoring domestic supplier momentum. India’s PLI program grants duty exemptions that lure Siemens and Abbott to local assembly facilities. Japan, with 29.1% of its population over 65 in 2024, sustains demand for municipal screening programs where Nihon Kohden’s Celltac holds 40% share. South Korea and Australia integrate Scopio Labs’ digital morphology to offset pathologist shortages.

Europe ranked third in 2025, though the European Union Medical Device Regulation prolonged Class IIb hematology analyzer certifications by eight months, delaying launches at Roche and Horiba. Siemens Healthineers earned EUR 11.8 billion in diagnostics revenue in fiscal 2024, buoyed by Atellica HEMA placements in Germany and France. Middle East & Africa grows moderately; Roche’s battery-powered cobas m 511 finds utility in off-grid clinics. South America adopts reagent-rental models to sidestep upfront capital, with Horiba and Boule gaining traction. GCC countries channel health-transformation funds into high-throughput workcells from Sysmex and Beckman to equip new reference labs.

Competitive Landscape

The complete blood count device market shows moderate concentration, yet reagent consumables remain fragmented because proprietary chemistries lock users into long contracts that stretch 70% of lifetime revenue. Sysmex alone posted USD 1.5 billion hematology sales in fiscal 2024, evidencing its dominance. Siemens’ Atellica HEMA 580, launched in 2024, embeds AI-driven infectious screening to directly counter Sysmex’s XN-Series in academic centers. Beckman’s Monocyte Distribution Width strategy extends installed platform life without large capital outlays.

White-space opportunity lies in CLIA-waived settings: EKF’s DiaSpect and Sysmex’s XW-100 allow pharmacies and urgent-care centers to conduct CBCs inexpensively. Mindray and Horiba win share in emerging markets by offering open-system analyzers that accept third-party reagents, lowering five-year ownership cost by 25–35%. Scopio Labs and PixCell Medical partner with Siemens and Beckman to integrate digital morphology, adding value without replacing analyzers. ISO 15189’s strict validation rules favor incumbents that already maintain robust quality systems, raising hurdles for startups.

Complete Blood Count Device Industry Leaders

Sysmex Corporation

Siemens Healthineers AG

Abbott Laboratories

Danaher

Shenzhen Mindray Medical International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Truvian received FDA 510(k) clearance for TruVerus, the first multimodal benchtop instrument delivering a broad menu of routine blood results.

- May 2025: CytoChip secured FDA clearance and CLIA waiver for its handheld CBC analyzer, preparing for U.S. launch.

- March 2025: Abbott debuted a portable whole-blood concussion test in the United Kingdom.

Global Complete Blood Count Device Market Report Scope

A Complete Blood Count (CBC) device, is a laboratory instrument that quickly measures and analyzes blood's cellular components, including red blood cells, white blood cells, platelets, and hemoglobin levels, using technologies like electrical impedance or laser flow cytometry.

The Complete Blood Count Device Market Report is segmented by Product Type, Modality, Differential Capability, End User, and Geography. By Product Type, the market is segmented into Hematology Analyzer Systems, Hematology Reagents & Consumables, and Slide Stainers & Peripheral Equipment. By Modality, the market is segmented into Benchtop Analyzers, Point-of-Care/Portable Analyzers, and Automated Integrated Workcells. By Differential Capability, the market is segmented into 3-Part, 5-Part, and 6- & 7-Part Differential. By End User, the market is segmented into Hospitals, Diagnostic Laboratories, Blood Banks & Transfusion Centers, Research & Academic Institutes, and Other End Users. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. he market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Hematology Analyzer Systems |

| Hematology Reagents & Consumables |

| Slide Stainers & Peripheral Equipment |

| Benchtop Analyzers |

| Point-of-Care / Portable Analyzers |

| Automated Integrated Workcells |

| 3-Part Differential |

| 5-Part Differential |

| 6- & 7-Part Differential |

| Hospitals |

| Diagnostic Laboratories |

| Blood Banks & Transfusion Centers |

| Research & Academic Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hematology Analyzer Systems | |

| Hematology Reagents & Consumables | ||

| Slide Stainers & Peripheral Equipment | ||

| By Modality | Benchtop Analyzers | |

| Point-of-Care / Portable Analyzers | ||

| Automated Integrated Workcells | ||

| By Differential Capability | 3-Part Differential | |

| 5-Part Differential | ||

| 6- & 7-Part Differential | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Blood Banks & Transfusion Centers | ||

| Research & Academic Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the complete blood count device market in 2026?

The complete blood count device market size stands at USD 5.22 billion in 2026.

What is the forecast CAGR for complete blood count devices through 2031?

The market is projected to grow at an 8.25% CAGR between 2026 and 2031.

Which product category is growing fastest?

Slide stainers and peripheral equipment are advancing at an 11.63% CAGR to 2031.

Why are point-of-care CBC analyzers gaining traction?

CLIA-waived clearances and demand for two-minute turnaround times are propelling portable analyzers in pharmacies and rural clinics.

Which region will expand the quickest?

Asia-Pacific is forecast to register the fastest 10.53% CAGR through 2031, driven by aging populations and government-mandated screening programs.

Page last updated on: