Blood Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

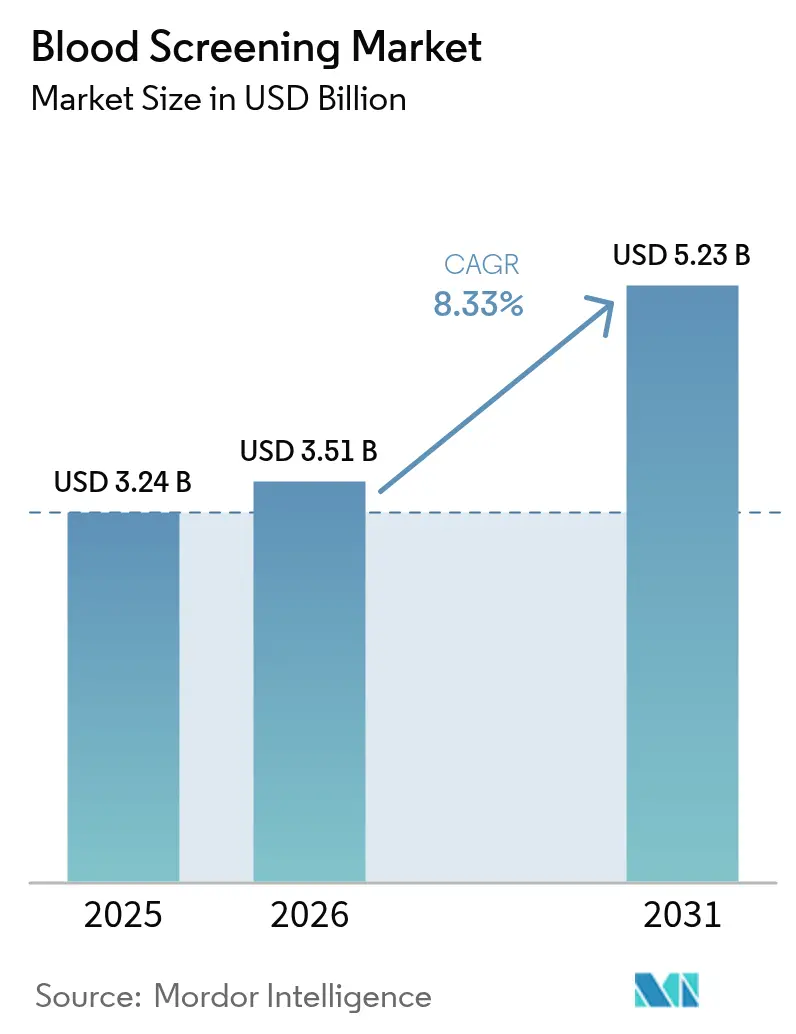

| Market Size (2026) | USD 3.51 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 8.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Screening Market Analysis by Mordor Intelligence

blood screening market size in 2026 is estimated at USD 3.51 billion, growing from 2025 value of USD 3.24 billion with 2031 projections showing USD 5.23 billion, growing at 8.33% CAGR over 2026-2031. Growth is propelled by regulatory reforms that emphasize individual donor risk assessment, rapid adoption of automation, and the steady rebound in global donations. Wider use of multiplex nucleic-acid testing, the arrival of point-of-care molecular platforms, and expanding inventory-management algorithms are streamlining operations while improving pathogen detection. Meanwhile, cost pressures linked to compliance with evolving Laboratory Developed Test (LDT) rules are driving hospitals and blood banks to invest in integrated solutions that lower per-unit testing costs. Finally, pathogen-reduction technologies are starting to complement conventional screening, prompting incumbents to rethink R&D priorities and partnerships.

Key Report Takeaways

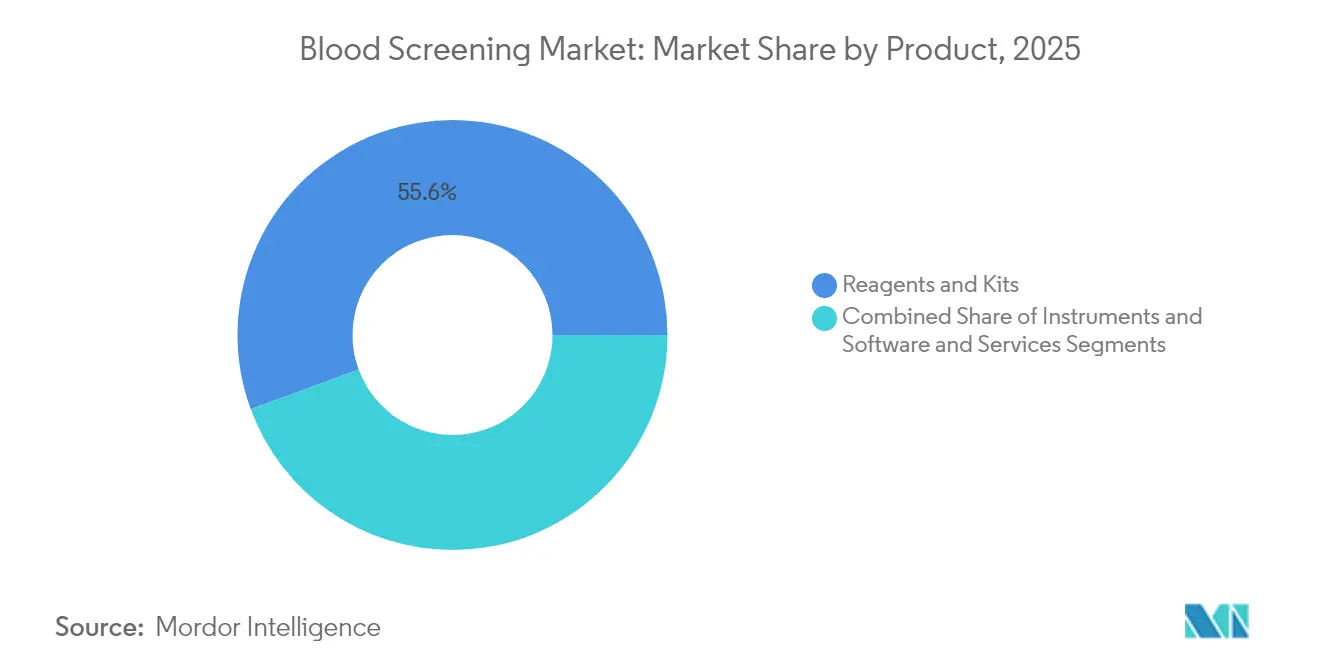

- By product, reagents and kits led with 55.62% of blood screening market share in 2025; instruments are projected to grow at a 9.78% CAGR to 2031.

- By technology, NAT held 41.88% revenue share in 2025, while next-generation sequencing is forecast to advance at an 11.02% CAGR through 2031.

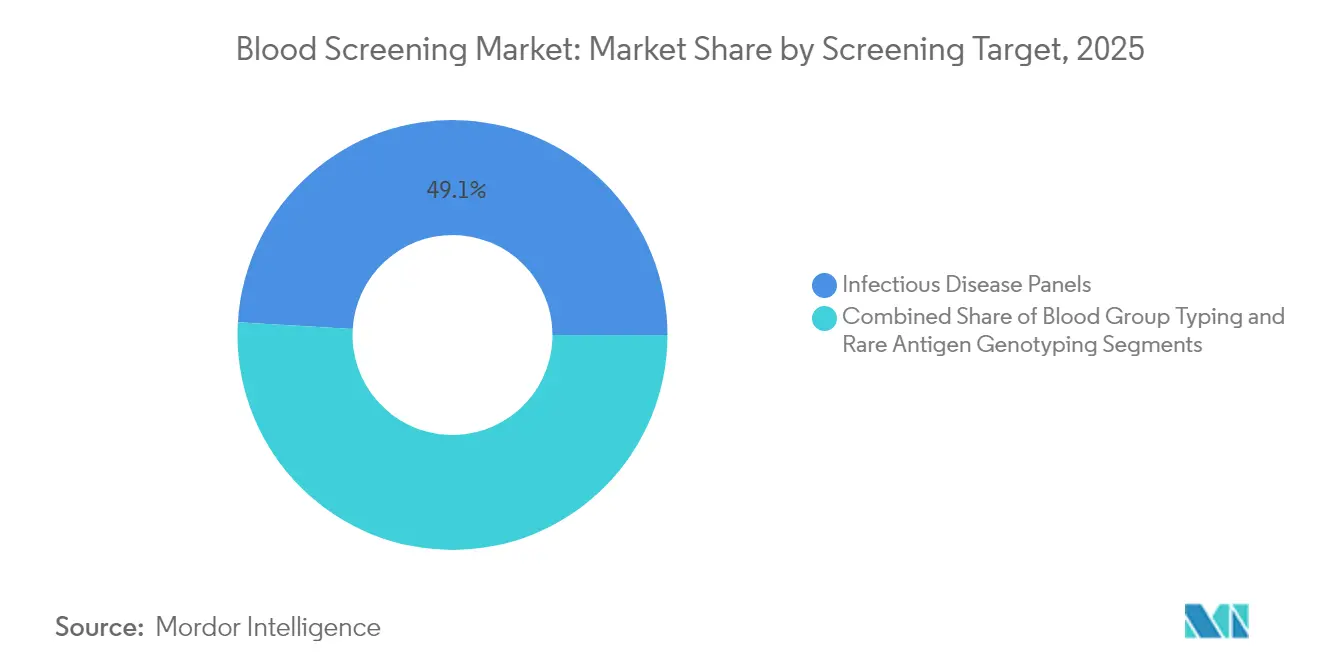

- By screening target, infectious-disease panels dominated with 49.05% share of the blood screening market size in 2025 and are set to expand at a 12.12% CAGR by 2031.

- By end-user, blood banks accounted for 58.15% of the blood screening market size in 2025, whereas clinical laboratories will register a 10.22% CAGR to 2031.

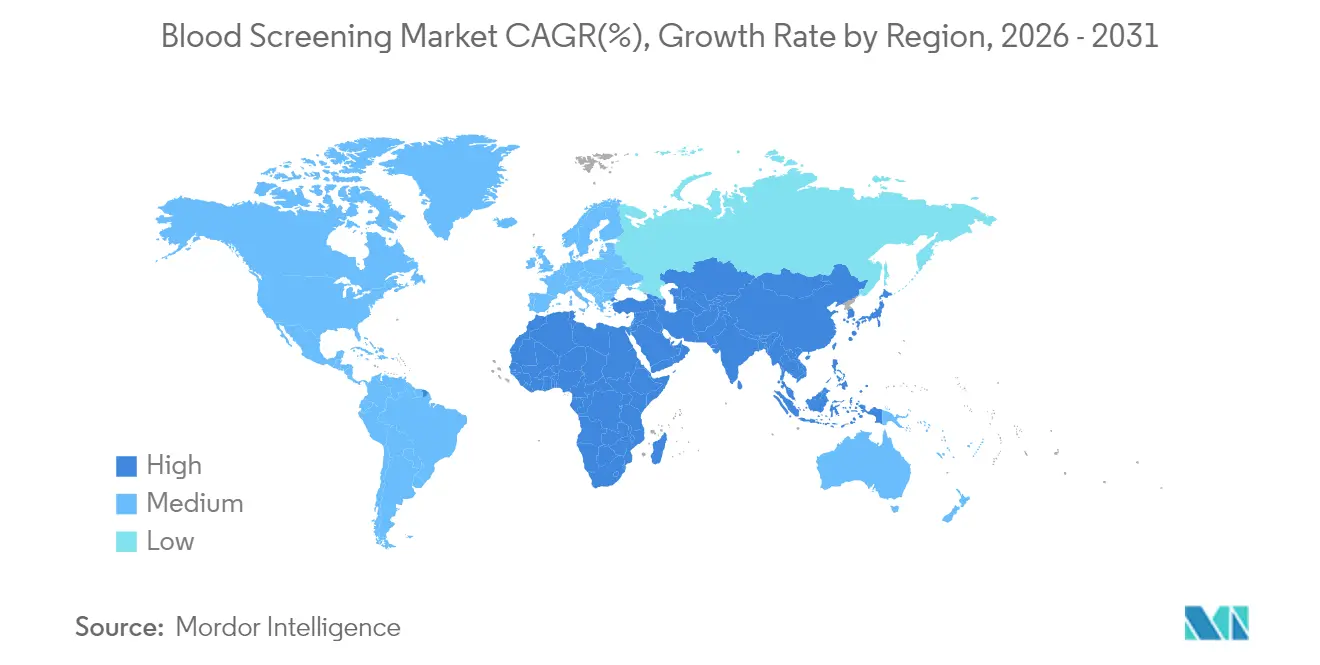

- By geography, North America commanded 35.10% of the blood screening market share in 2025; Asia-Pacific is the fastest-growing region at 9.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Blood Screening Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Blood Donations Leading To Increased Transfusion Screenings | +1.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Increasing Prevalence Of Transfusion-Transmissible Infections | +1.8% | Global, particularly APAC and MEA regions | Long term (≥ 4 years) |

| Stringent Regulatory Guidelines For Blood Safety | +0.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Technological Advancement In Blood Screening Methods | +1.5% | Global, led by North America and developed APAC markets | Medium term (2-4 years) |

| Rising Awareness For Blood Transmitted Infections And Increasing Number Of Blood Banks | +1.1% | Global, with accelerated growth in emerging markets | Long term (≥ 4 years) |

| AI-Driven Inventory Optimisation Platforms In Blood Banks | +0.7% | North America & EU, early adoption in urban APAC centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising blood donations leading to higher transfusion screenings

Group-donation campaigns, such as China’s 2025 initiative that rewards repeat donors, are reversing the pandemic dip in supply and creating fresh demand for scalable screening. A parallel shift by the United States Food and Drug Administration (FDA) to risk-based donor assessment removes categorical deferrals for men who have sex with men, enlarging the eligible pool while increasing the complexity of per-unit screening.[1]U.S. Food and Drug Administration, “Laboratory Developed Tests Regulatory Impact Analysis,” fda.gov Together, higher volumes and donor diversity are encouraging blood establishments to adopt fully automated assays and robotics so that throughput rises without compromising sensitivity.

Greater prevalence of transfusion-transmissible infections

The Centers for Disease Control and Prevention (CDC) issued a 2025 alert after 13 million dengue cases occurred in the Americas during 2024, more than twice the prior year.[2]Centers for Disease Control and Prevention, “Ongoing Risk of Dengue Virus Infections,” cdc.govConcurrent West Nile outbreaks in Bulgaria and isolated monkeypox transmissions through platelet products underline the need for multiplex assays that go beyond the HIV-HBV-HCV triad. Rapid expansion of such panels has lifted demand for NAT reagents that can screen for emerging flaviviruses, orthopoxviruses, and region-specific pathogens within one workflow.

Stricter regulatory guidelines for blood safety

The new European Regulation (EU) 2024/1938 sets harmonized oversight standards effective 2027, while updated FDA guidance for blood establishments focuses on donor qualification, platelet collection and hepatitis B procedures.[3]AABB, “AI and Data Sciences in Blood Banking,” aabb.org These rules accelerate investment in quality-management systems, automated documentation, and validated screening platforms. Vendors able to provide turnkey compliance features and audit-ready software modules gain a competitive edge.

Technological advances in screening methods

FDA approval of the cobas Malaria NAT test—the first molecular assay cleared for U.S. donors—illustrates regulators’ openness to high-sensitivity molecular diagnostics. Portable systems, such as Dragonfly, now deliver 96.1% orthopoxvirus sensitivity in under 40 minutes, making near-patient molecular testing viable. At the same time, metagenomic sequencing detects 74.0% of sepsis pathogens versus 41.1% by culture, offering a blueprint for future integrated blood-bank workflows.

Restraints Impact Analysis of Blood Screening Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Consumable Cost For Screening | -1.4% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Limited Skilled Workforce And Laboratory Infrastructure | -1.1% | APAC, MEA, and rural regions globally | Long term (≥ 4 years) |

| Competition From Pathogen-Reduction Technologies | -0.8% | North America & EU, expanding to developed APAC | Medium term (2-4 years) |

| Reagent Supply-Chain Disruptions (Geo-Politics & Cold-Chain) | -0.9% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital and consumable costs

Compliance with the newly finalized LDT rule will cost the U.S. screening sector an estimated USD 566 million to USD 3.56 billion each year, according to FDA modelling. Emerging economies struggle even more because NAT platforms require significant upfront spending and high-grade cold-chain reagents. Although microfluidic chips have driven per-test costs down to USD 9.5, overall affordability remains a challenge for smaller blood centres.

Limited skilled workforce and lab infrastructure

Expertise in molecular diagnostics is scarce outside tier-one hospitals. Rural Asia-Pacific labs face difficulties staffing technologists trained to run real-time PCR, interpret mNGS data, or maintain closed-system robotics. Without targeted training and tele-mentoring, decentralization may stall.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Blood Screening Market Segment Analysis

By Product:

Reagents anchor revenue while smart instruments reshape workflowsReagents and kits retained 55.62% of blood screening market share in 2025 due to recurring demand for NAT, immunoassay and confirmatory components. Their dominance is reinforced by batch-specific regulatory validation that locks in proprietary formulations. The instruments category is expanding at 9.78% CAGR as laboratories upgrade to fully automated NAT workcells and next-generation immunoassay analyzers that integrate robotic pipetting, bar-code tracking and LIS connectivity.

A surge in AI-enabled middleware is also notable; OneBlood’s deployment cut inventory levels by 40%, proving the operational value of real-time analytics. Software & services revenues therefore accelerate as blood banks seek predictive dashboards and automated deviation reporting, a trend likely to outpace reagent growth beyond 2028. Meanwhile, the emergence of portable molecular diagnostic devices, typified by the Dragonfly platform, suggests that decentralized testing could further fragment the instruments sub-segment over the long term.

By Technology:

NAT leads today, NGS rises fastestNAT maintained a robust 41.88% share of the blood screening market in 2025 as its capacity to detect viral nucleic acids during window periods remains unmatched for HIV-1/2, HBV and HCV. Nevertheless, next-generation sequencing is scaling quickly at an 11.02% CAGR. mNGS can uncover unexpected pathogens, pinpoint co-infections and support genomic surveillance during outbreaks, evidenced by a 74.0% detection rate in sepsis studies.

Traditional enzyme immunoassays (ELISA/CLIA) still dominate in lower-resource settings because of lower instrumentation costs and simpler workflows. Rapid tests fill emergency needs but struggle with sensitivity versus NAT. Western blot retains a niche for confirmatory HIV workups. As AI tools mine large molecular datasets, labs may unify NAT and NGS within a common informatics layer, eventually blurring the boundaries between technologies.

By Screening Target:

Infectious-disease panels outpace all other categoriesInfectious-disease panels accounted for 49.05% of revenue in 2025 and will grow at a 12.12% CAGR through 2031. Dengue’s surge to 13 million cases in the Americas during 2024 drove immediate demand for flavivirus NAT panels. Widening West Nile and Zika footprints similarly elevate the need for multiplex assays.

Blood-group typing continues to be indispensable for compatibility, while rare-antigen genotyping serves complex transfusion cases, especially in multi-ethnic populations. Roche’s cobas Malaria test, cleared in 2024, broadens screening for travelers and immigrants from endemic areas. Taken together, these advances reinforce the case for syndromic panels capable of processing multiple targets in a single run, streamlining both cost and logistics.

By End-User:

Blood banks remain central, clinical labs race aheadBlood banks processed 58.15% of global donations in 2025, reflecting their integrative role in collection, testing, processing and distribution. Yet testing decentralization is accelerating: clinical laboratories will expand at 10.22% CAGR to 2031 as hospital networks outsource specialty NAT and mNGS work to reference labs equipped with high-throughput sequencers.

University Hospitals Blood Bank recorded a 7% rise in samples and activated 323 massive-transfusion protocols in 2024, illustrating the growing testing burden on tertiary centers. Private-sector consolidation is also reshaping the end-user landscape, highlighted by Quest Diagnostics’ USD 985 million purchase of LifeLabs to extend advanced diagnostics into Canada. Plasma-fractionation facilities continue to demand stringent viral clearance, sustaining high-specificity NAT reagent consumption.

Geography Analysis

North America Blood Screening Market

North America held 35.10% of the blood screening market in 2025. The FDA’s risk-based donor eligibility guidance, AI-assisted inventory management, and ongoing implementation of LDT oversight collectively maintain the region’s technology edge. Canada’s diagnostics sector expanded after Quest Diagnostics took full control of LifeLabs, deepening molecular-testing capacity and cross-border sample logistics. Meanwhile, Mexico is improving rural donation infrastructure, which lifts demand for mid-tier immunoassay analyzers.

APAC Blood Screening Market

Asia-Pacific is the growth engine, projected at a 9.86% CAGR to 2031. Japan’s 2025 hemoglobin-vesicle trial—the world’s first artificial-blood clinical study—could eventually reduce dependence on donor supply and lengthen storage life to two years at room temperature. India’s Quick Vitals facial-scan platform delivers non-invasive hemogram readouts within a minute and is being piloted in public hospitals, underscoring the region’s openness to disruptive diagnostics. China’s national carrier rate of 8.95% for thalassemia points to substantial prenatal and donor screening volume, while ongoing group-donation campaigns expand collection points in second-tier cities.

Europe Blood Screening Market

Europe shows steady progress under Regulation (EU) 2024/1938, which pools oversight across member states and allocates funds for crisis readiness. Germany and France are trial-ling pathogen-reduced platelets alongside traditional screening, whereas Bulgaria’s West Nile outbreak prompted expanded NAT panels at regional blood bank. The regulation’s unified guidance will streamline vendor approvals, encouraging pan-European platform standardization.

Competitive Landscape

Major suppliers—Roche, Abbott, Grifols and bioMérieux—pursue end-to-end platforms rather than stand-alone tests. Roche gained first-mover status with FDA-approved malaria NAT, while bioMérieux’s EUR 111 million SpinChip purchase strengthens the firm’s 10-minute, point-of-care portfolio. Grifols is doubling investment in its NAT business to ward off competition from emergent NGS-based services.

The arrival of pathogen-reduction technologies heightens rivalry by offering an alternative safety layer that could eventually trim the number of individual assays per donation. At the same time, AI-driven middleware and cloud inventory platforms invite non-traditional players from the software sector into the blood screening industry, intensifying competition for data ownership.

Regulatory hurdles may consolidate the market: mandated LDT submissions and hefty post-market surveillance fees could marginalize small independent labs, pushing them toward alliances or acquisition. Simultaneously, emerging manufacturers in India and China are scaling reagent production for domestic use, signaling a potential shift in global supply dynamics within five years.

Blood Screening Industry Leaders

F. Hoffmann-La Roche Ltd.

Grifols

bioMérieux

Bio-Rad Laboratories, Inc.

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Blood Screening Market Companies Covered in this Report

- Roche

- Grifols

- Abbott Laboratories

- bioMérieux

- Bio-Rad Laboratories

- Beckton Dickinson

- Danaher

- DiaSorin

- Siemens Healthineers

- Thermo Fisher Scientific

- Ortho Clinical Diagnostics

- Revvity

- Hologic

- QIAGEN

- Illumina

- GRAIL, Inc

- Immucor

- Meril Life Sciences

- Mindray

- Sysmex

Recent Industry Developments in Blood Screening Market

- May 2025: Roche introduced the Elecsys PRO-C3 test, a rapid assay that detects liver fibrosis in 18 minutes and lowers dependence on invasive biopsies.

- March 2025: Japan began the first human trial of artificial blood based on hemoglobin vesicles that store for two years at ambient temperature without blood-group matching.

- February 2025: Roche won FDA 510(k) clearance for the Tina-quant Lp(a) Gen.2 test, the first U.S. blood assay to report Lp(a) in molar units.

- January 2025: bioMérieux finalized its acquisition of SpinChip Diagnostics, adding a handheld immunoassay platform that delivers whole-blood results in 10 minutes.

Blood Screening Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the blood-screening market as all laboratory tests performed on donated whole blood, packed cells, platelets, and plasma that aim to detect infectious markers before transfusion; it captures revenue from reagents, instruments, and dedicated software used within licensed blood banks, hospital transfusion units, and plasma-fractionation centers worldwide.

Scope exclusion: point-of-care glucose, hematology, and blood-typing analyzers are not counted.

Segments Covered in This Report

- By Product

- Reagents & Kits

- NAT Reagents and Kits

- Immunoassay Reagents and Kits

- Other Reagents and Kits (WB, Rapid, WB)

- Instruments

- Automated NAT Systems

- Immunoassay Analysers (ELISA/CLIA)

- Point-of-Care Molecular Devices

- Software & Services

- Reagents & Kits

- By Technology

- Nucleic Acid Amplification Test (NAT)

- TMA

- Real-time PCR

- Immunoassay

- ELISA

- CLIA / EIA

- Rapid Tests (Lateral-flow)

- Next-Generation Sequencing (NGS)

- Western Blotting

- Emerging Point-of-Care Molecular Tests

- Nucleic Acid Amplification Test (NAT)

- By Screening Target

- Infectious Disease Panels

- HIV

- HBV

- HCV

- Emerging Pathogens (Zika, WNV, Dengue)

- Blood Group Typing

- Rare Antigen Genotyping

- Infectious Disease Panels

- By End-User

- Blood Banks

- Hospitals

- Clinical Laboratories

- Plasma Fractionation Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed transfusion-medicine directors, regional blood-bank supervisors, reagent distributors, and regulatory auditors across North America, Europe, Asia-Pacific, and Latin America. Conversations clarified real-world NAT penetration, typical reagent run rates, capital amortization periods, and the pace at which next-generation sequencing kits move from validation to routine use, helping us fine-tune desk-derived assumptions.

Desk Research

We began with exhaustive reviews of public datasets such as WHO's Global Database on Blood Safety, US FDA device registrations, the European Centre for Disease Prevention weekly TTI bulletins, and national hemovigilance reports. We then overlaid insights from trade associations (AABB, EBA) and customs shipment records that show reagent volumes crossing major ports. Annual reports and 10-Ks from key IVD suppliers, along with clinical-trial registries that flag upcoming screening technologies, supplied cost and adoption clues. Subscription tools within Mordor's paid stack, D&B Hoovers for company financials, and Questel for patent intensity added depth where public numbers thinned. This list is illustrative; numerous additional open and paid sources fed the evidence pool.

Market-Sizing & Forecasting

A top-down reconstruction used annual units of donated blood and average tests per unit to frame demand, which we calibrated against historical reagent import values. Selected bottom-up checks, sampled supplier shipments and hospital procurement data, validated totals. Key variables in the model include: 1) number of whole-blood donations, 2) mandatory TTI panels per jurisdiction, 3) reagent average selling prices, 4) instrument installation base growth, 5) NAT penetration rate, and 6) regulatory compliance deadlines. A multivariate regression links these drivers to revenue, and an ARIMA overlay smooths short-term volatility. Gaps in country-level donor data were bridged by applying region-specific donation rates confirmed during interviews.

Data Validation & Update Cycle

Outputs pass three checks: variance against historical import statistics, cross-comparison with independent donation data, and an internal peer review. Reports refresh every twelve months, with interim revisions triggered by material events such as new mandatory screening guidelines or disruptive test approvals. Before each client delivery, an analyst performs a fresh verification pass.

How Mordor Intelligence's Blood Screening Market Size Compares to Other Published Estimates

Published estimates frequently diverge because analysts pick differing product bundles, price bases, and refresh cadences.

Key gap drivers include narrower scopes that drop software service revenue, older currency conversions, or aggressive bundling of ancillary diagnostic assays that inflate totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.24 B (2025) | Mordor Intelligence | - |

| USD 3.40 B (2024) | Global Consultancy A | Excludes software & services, applies uniform 2019-2024 ASP uplift |

| USD 2.40 B (2023) | Industry Association B | NAT-only scope and 2023 USD baseline left un-escalated |

| USD 4.20 B (2025) | Specialty Research Firm C | Bundles manual blood-testing kits and point-of-care devices |

Taken together, the comparison shows how Mordor's disciplined scope, fresher baseline year, and dual-path validation yield a balanced, transparent figure that decision-makers can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current size of the blood screening market?

The blood screening market size stands at USD 3.51 billion in 2026 and is projected to reach USD 5.23 billion by 2031.

Which product segment generates the highest revenue?

Reagents and kits hold the largest share at 55.62% in 2025, thanks to recurring demand for NAT and immunoassay consumables.

Which region shows the fastest growth?

Asia-Pacific is forecast to grow at 9.86% CAGR through 2031, fueled by technological leapfrogging in Japan, India and China.

How are new regulations affecting the market?

FDA LDT rules and EU Regulation 2024/1938 tighten oversight, raising compliance costs but driving adoption of fully validated, automated platforms.

What technological trend is set to disrupt current workflows?

Next-generation sequencing and AI-enabled inventory systems are poised to streamline multi-pathogen detection and reduce reagent wastage.

Will pathogen-reduction systems replace traditional screening?

Adoption is rising, yet most blood banks still combine reduction with nucleic-acid testing to meet stringent safety margins.

Page last updated on: