Blood And Blood Components Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.20 Billion |

| Market Size (2031) | USD 22.20 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood And Blood Components Market Analysis by Mordor Intelligence

The Blood And Blood Components Market size is expected to grow from USD 16.30 billion in 2025 to USD 17.20 billion in 2026 and is forecast to reach USD 22.20 billion by 2031 at 5.29% CAGR over 2026-2031.

Steady demand stems from complex surgical procedures, CAR-T programs that intensify platelet use, and trauma protocols that require immediate access to red blood cells, plasma, and cryoprecipitate. Regulatory acceptance of cold-stored platelets up to 14 days, national rollouts of blood-group genotyping, and automation in apheresis collections are helping suppliers address chronic shortages and reduce wastage. At the same time, Patient Blood Management (PBM) programs have lowered allogeneic transfusion rates by as much as 60%, tempering growth in mature hospitals. Shrinking donor pools in high-income economies, as spelled out by the American Red Cross shortage declaration in 2024, continue to pressure inventories despite expanded eligibility criteria[1]American Red Cross, “National Blood Shortage,” redcross.org.

Key Report Takeaways

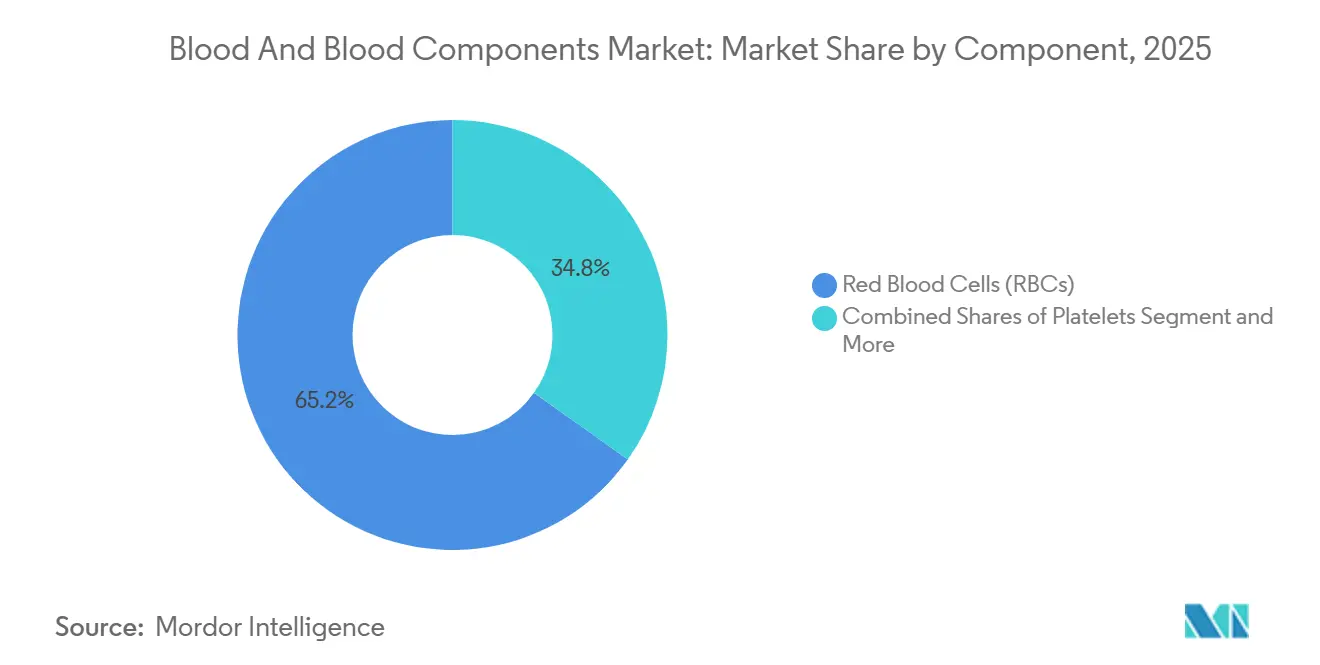

- By component, red blood cells led with 65.18% of the blood and blood components market share in 2025, while platelets are projected to advance at a 6.50% CAGR through 2031.

- By collection method, whole-blood-derived components accounted for 72.18% share of the blood and blood components market size in 2025; apheresis collections are forecast to expand at a 6.92% CAGR to 2031.

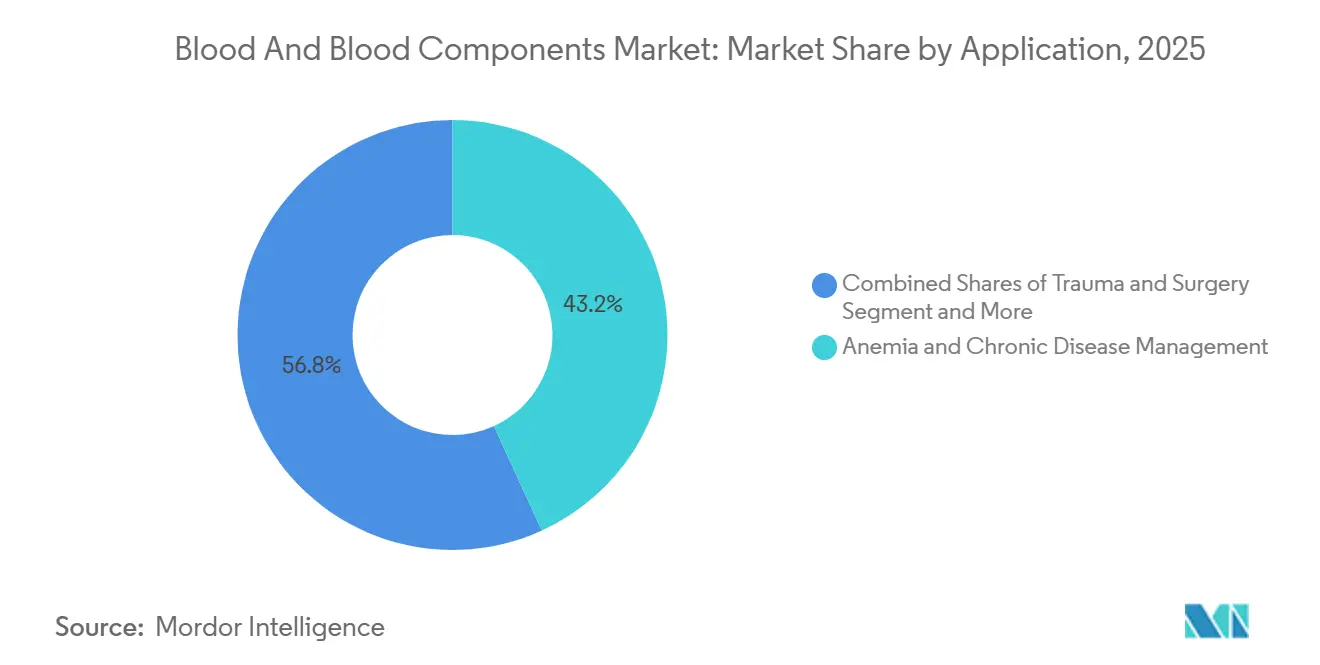

- By application, anemia and chronic disease management captured 43.18% revenue in 2025, whereas cancer treatment and hemato-oncology support are progressing at a 6.76% CAGR to 2031.

- By end user, hospitals controlled 68.19% revenue in 2025, yet ambulatory surgical centers are growing at a 6.55% CAGR through 2031.

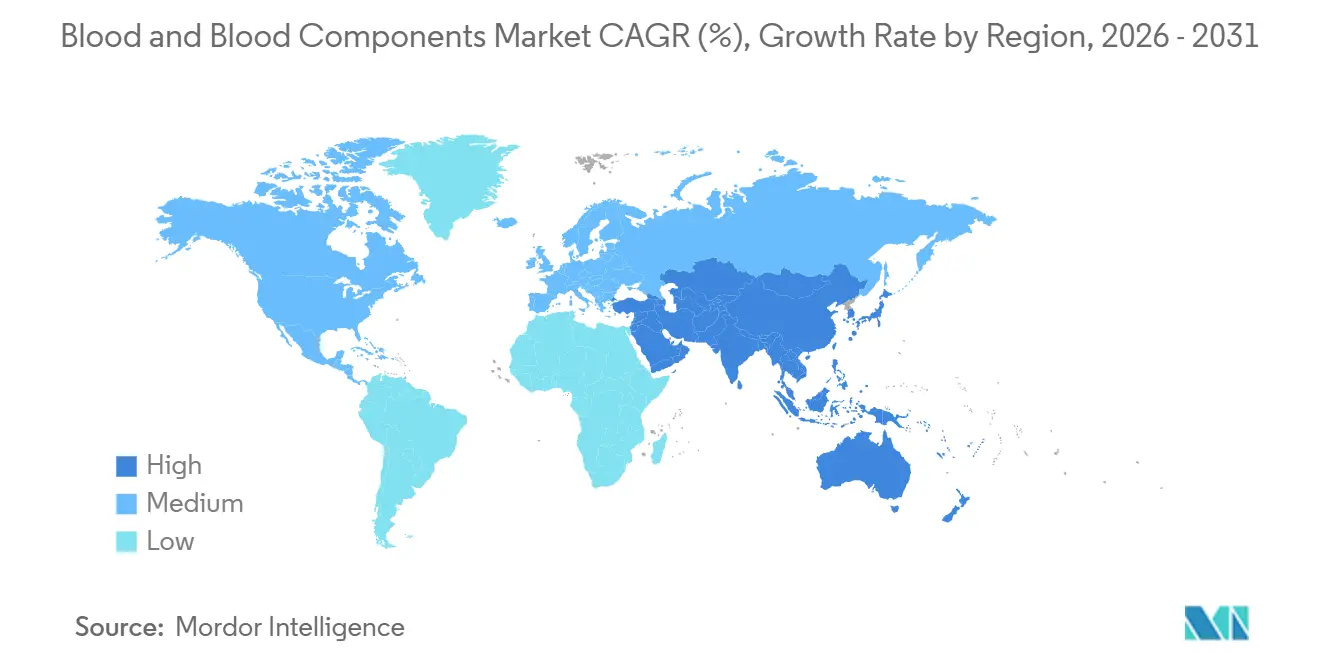

- By geography, North America contributed 36.19% revenue in 2025; Asia-Pacific is set to register the fastest 6.81% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blood And Blood Components Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical volumes in complex specialties | +0.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Oncology-induced anemia and thrombocytopenia support | +0.7% | North America, Europe, China, Japan | Medium term (2-4 years) |

| Trauma and road-injury burden are elevating emergency transfusions | +0.5% | Middle East & Africa, South America, rural Asia-Pacific | Short term (≤ 2 years) |

| Aging populations are increasing perioperative transfusion intensity | +0.6% | North America, Europe, Japan, Australia | Long term (≥ 4 years) |

| Regulatory acceptance of cold-stored platelets up to 14 days | +0.4% | United States, Canada, Scandinavia | Medium term (2-4 years) |

| National rollouts of blood-group genotyping | +0.3% | United Kingdom, United States pilot centers, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes in Complex Specialties

Outpatient procedures in the United States are expected to climb 21% during 2025 to 2035, illustrating the shift toward ambulatory care. Complex oncologic resections and robotic-assisted orthopedic cases still mandate cross-matched red cells and platelets on standby, sustaining hospital inventories. Satellite blood depots are proliferating near large ambulatory surgical centers, yet decentralized stock elevates cold-chain overheads and demands real-time visibility. FDA Current Good Tissue Practice and AABB standards oblige these centers to document transfusion protocols, adding compliance costs that only large systems can easily absorb.

Oncology-Induced Anemia and Thrombocytopenia Support

CAR-T and high-dose chemotherapy produce severe cytopenias in 10-25% of treatment cycles, triggering prophylactic platelet transfusions below 10,000/μL as guided by ASCO and ASH[2]National Cancer Institute, “Bleeding & Bruising,” cancer.gov. Hospitals are adopting pathogen-reduction platforms such as INTERCEPT, cleared by the FDA in 2025, to extend shelf life and curb bacterial contamination. As survival improves, each patient requires more transfusions over a longer horizon, reinforcing steady growth for the blood and blood components market.

Trauma and Road-Injury Burden Elevating Emergency Transfusions

Trauma-induced coagulopathy affects up to 35% of severely injured patients, necessitating 1:1:1 resuscitation ratios endorsed by the WHO. The FDA’s 2023 guidance on cold-stored platelets enables prehospital deployment in rural ambulances, military field hospitals, and disaster caches[3]U.S. Food and Drug Administration, “Guidance for Cold-Stored Platelets,” fda.gov. The CHIPS trial, now enrolling, may extend permissible storage to 21 days, a potential game-changer for low-resource trauma networks.

Aging Populations Increasing Perioperative Transfusion Intensity

Adults ≥ 65 years old present higher baseline anemia and polypharmacy, which elevate transfusion probability during orthopedic and cardiac operations. Japan, where citizens ≥ 65 represent 29% of the population, has intensified donor-recruitment campaigns to offset waning participation among younger cohorts. Adults ≥ 65 years old present higher baseline anemia and polypharmacy, which elevate transfusion probability during orthopedic and cardiac operations. Japan, where citizens ≥ 65 represent 29% of the population, has intensified donor-recruitment campaigns to offset waning participation among younger cohorts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient Blood Management reducing allogeneic transfusions | -0.9% | North America, Europe, Australia, and urban Asia-Pacific | Short term (≤ 2 years) |

| Shrinking donor pools and seasonal shortages | -0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Platelet bacterial-contamination controls add cost | -0.3% | Global, strictest in North America & Europe | Short term (≤ 2 years) |

| Ethnic donor-matching gaps for rare phenotypes | -0.2% | North America, Europe, and diverse urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patient Blood Management Reducing Allogeneic Transfusions

PBM bundles preoperative anemia correction, intraoperative cell salvage, and restrictive thresholds have cut red-cell use by up to 60% and reduced mortality odds to 0.33 in German multicenter studies. Joint Commission standards now oblige hospitals to audit transfusion appropriateness, compressing demand even as surgical complexity climbs.

Shrinking Donor Pools and Seasonal Shortages

The American Red Cross reported a 40% decline in teen and young-adult donors over two decades. Japan mirrors the trend as its population ages; older donors now outnumber younger contributors. Mobile drives and social-media campaigns restored only single-digit growth in first-time donors, leaving inventory gaps during holidays that inflate procurement costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platelets Gain Share Despite RBC Dominance

Red blood cells generated 65.18% of 2025 revenue, yet platelets are on track for a 6.50% CAGR to 2031 as CAR-T and intensified chemotherapy expand thrombocytopenia cases. Plasma and cryoprecipitate continue to support coagulation-factor replacement in massive transfusion protocols, but pathogen-reduction systems are shifting the mix toward higher-margin, longer-shelf-life platelet products. INTERCEPT’s 2025 FDA authorization is emblematic of technology’s role in this shift.

Whole-blood-derived platelets remain critical across regions with limited apheresis capacity, yet stringent bacterial-contamination rules now add USD 50-100 to per-unit costs, nudging hospitals toward safer, pretreated supplies. Plasma fractionation investments, EUR 160 million by Grifols in Barcelona, underline a tilt toward derivatives with stronger margins.

By Collection Method: Apheresis Automation Drives Yield Gains

Whole-blood collections captured 72.18% of 2025 revenue thanks to entrenched mobile drives, but apheresis is heading for a 6.92% CAGR through 2031. Fresenius Kabi’s Aurora Xi software, cleared in 2025, raised plasma yield by 88 mL per donation, illustrating the incremental productivity that sustains apheresis growth.

Mobile collection remains indispensable for rural outreach, yet suppliers are exiting low-margin businesses. Haemonetics sold its whole-blood assets to GVS for USD 67.1 million in 2025 to focus on plasma and platelet automation. China’s updated 2024 guidelines similarly prioritize automated, pathogen-reduced collections, securing momentum for apheresis in Asia-Pacific.

By Application: Hemato-Oncology Support Outpaces Traditional Indications

Anemia and chronic disease management held 43.18% revenue in 2025, but cancer treatment and hemato-oncology support should clock a 6.76% CAGR through 2031 as durable CAR-T responses lengthen transfusion dependence. Massive transfusion in trauma continues to rely on 1:1:1 protocols, while the adoption of viscoelastic testing in obstetric hemorrhage sustains cryoprecipitate use.

Geographic concentration varies; trauma protocols dominate in the Middle East & Africa, whereas hemato-oncology peaks in North America, Europe, and urban China. WHO guidance on postpartum hemorrhage, including tranexamic acid and cryoprecipitate, widens demand in lower-income regions.

By End User: Ambulatory Centers Capture Outpatient Shift

Hospitals retained 68.19% revenue in 2025 because only they maintain 24/7 blood banks capable of emergency release. Ambulatory surgical centers, however, are growing at 6.55% a year as minimally invasive procedures accelerate. This decentralization forces blood centers to set up satellite depots, inflating logistics costs and requiring digital inventory platforms compliant with AABB traceability rules.

Standalone blood centers such as Vitalant consolidated operations in 2024-2025 to cushion PBM-driven volume drops. ASC operators now invest in transfusion-preparedness training and cross-matching protocols, acknowledging the limits of “low-risk” elective surgery models.

Geography Analysis

North America contributed 36.19% of global revenue in 2025, maintaining the largest blood and blood components market share. The U.S. FDA guidance in 2023 that permits 14-day cold storage of platelets lets trauma centers place inventory closer to remote highways and emergency medical services. This regulatory flexibility reduces wastage from expired units and supports steady growth even as Patient Blood Management programs restrain red-cell demand in urban hospitals. Persistent donor shortages remain a structural challenge, highlighted by the American Red Cross declaration of a national shortage in January 2024.

Asia-Pacific is forecast to log a 6.81% CAGR through 2031, the fastest among all regions within the blood and blood components market. China’s hospital capacity boost, coupled with a USD 2.4 billion CAR-T segment that is expanding at 28.9% annually, lifts platelet demand and accelerates adoption of apheresis automation. Japan’s aging population, where citizens over 65 already exceed 29%, forces the Japanese Red Cross to run targeted youth campaigns and pilot extended eligibility criteria to stabilize donations. Regional regulators are still evaluating pathogen-reduction and genotyping protocols pioneered in the West, creating a patchwork of standards that suppliers must navigate to unlock the full Asia-Pacific opportunity

Europe shows steady but slower expansion as national blood services roll out large-scale genotyping that cut alloimmunization in sickle-cell cohorts by up to 90%. Even so, summer vacations and year-end holidays still depress donor turnout by 15-20%, prompting elective-surgery cancellations and inter-country unit transfers within the European Union. Middle East and Africa as well as South America face higher trauma burdens and fragmented collection networks, driving hospitals to prioritize O-negative stocks and adopt cold-stored platelet protocols endorsed by the WHO.

Competitive Landscape

Global supply is moderately fragmented. Haemonetics, Grifols, Terumo BCT, and Fresenius Kabi together held a significant portion of 2025 revenue, each leveraging automation or pathogen reduction to differentiate. Haemonetics’ USD 67.1 million divestiture of whole-blood assets signals a pivot to higher-margin plasma and platelet solutions, while Fresenius Kabi’s Aurora Xi software raised plasma yields by 11.5% through adaptive nomograms. Grifols committed EUR 160 million to Barcelona fractionation and opened a 73,541 ft² San Diego facility in 2025 to bolster rare-RBC inventory. Terumo BCT’s Reveos automated separator, installed at The Blood Center in New Orleans, illustrates ongoing investments in labor-saving devices.

Smaller innovators such as Cerus focus on pathogen-reduction; INTERCEPT’s 2025 platelet expansion positions the firm for hospitals prioritizing safety over cost. Competitive intensity now revolves around integrated workflows that combine leukoreduction, pathogen reduction, and cold-storage compatibility, with ISO 9001 and AABB accreditation increasingly required in tenders.

Blood And Blood Components Industry Leaders

Haemonetics Corporation

Grifols, S.A.

Terumo BCT, Inc.

Fresenius Kabi

Baxter International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Grifols secured a USD 2 billion revolving credit facility to fund plasma-collection expansion in North America and Europe.

- November 2025: Cerus received FDA clearance for an expanded INTERCEPT platelet indication, extending shelf life while mitigating bacterial risk.

- November 2025: Fresenius Kabi completed U.S. rollout of Aurora Xi 2.0, boosting average plasma yield by 88 mL per donation.

Global Blood And Blood Components Market Report Scope

As per the scope of the report, whole blood is a vital fluid composed of approximately 55% plasma, a nutrient-rich liquid, and 45% formed elements, which include red blood cells, white blood cells, and platelets. Red blood cells (erythrocytes) use hemoglobin to transport oxygen to tissues, while white blood cells (leukocytes) serve as the primary defense within the immune system to fight infection. Platelets (thrombocytes) are essential for coagulation, working to stop bleeding at injury sites, while the plasma itself acts as a medium to transport hormones, electrolytes, and waste products throughout the body to maintain homeostasis.

The blood and blood components market is segmented by components, collection method, application, end user, and geography. Based on components, the market is segmented into red blood cells (RBCs), platelets (Apheresis-derived, whole-blood-derived), plasma (FFP/FP24), and cryoprecipitate/cryo-reduced plasma. By collection method, the market is segmented into apheresis collections and whole-blood-derived Components. By applications, the market is segmented into trauma & surgery, cancer treatment / hemato-oncology support, anemia and chronic disease management, obstetrics & gynecology / postpartum hemorrhage. By end users, the market is segmented into hospitals, standalone/regional blood centers, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Red Blood Cells (RBCs) |

| Platelets (Apheresis-derived, Whole-blood-derived) |

| Plasma (FFP/FP24) |

| Cryoprecipitate/Cryo Reduced Plasma |

| Apheresis Collections |

| Whole-blood-derived Components |

| Trauma & Surgery |

| Cancer Treatment / Hemato-oncology Support |

| Anemia and Chronic Disease Management |

| Obstetrics & Gynecology / Postpartum Hemorrhage |

| Hospitals |

| Standalone/Regional Blood Centers |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Red Blood Cells (RBCs) | |

| Platelets (Apheresis-derived, Whole-blood-derived) | ||

| Plasma (FFP/FP24) | ||

| Cryoprecipitate/Cryo Reduced Plasma | ||

| By Collection Method | Apheresis Collections | |

| Whole-blood-derived Components | ||

| By Application | Trauma & Surgery | |

| Cancer Treatment / Hemato-oncology Support | ||

| Anemia and Chronic Disease Management | ||

| Obstetrics & Gynecology / Postpartum Hemorrhage | ||

| By End User | Hospitals | |

| Standalone/Regional Blood Centers | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the blood and blood components market?

The blood and blood components market size reached USD 17.2 billion in 2026 and is projected at USD 22.2 billion by 2031.

How fast will platelet demand grow through 2031?

Platelet revenue is expected to rise at a 6.50% CAGR through 2031 as CAR-T and intensive chemotherapy increase thrombocytopenia incidence.

Which region will post the quickest gains?

Asia-Pacific should record a 6.81% CAGR through 2031 due to hospital expansions in China and India’s push toward a USD 50 billion medical-device sector.

How are Patient Blood Management programs affecting transfusion volumes?

Comprehensive PBM adoption has reduced allogeneic red-cell use by up to 60% in leading hospitals, curbing near-term volume growth.

Page last updated on: