United States Antiseptic And Disinfectant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

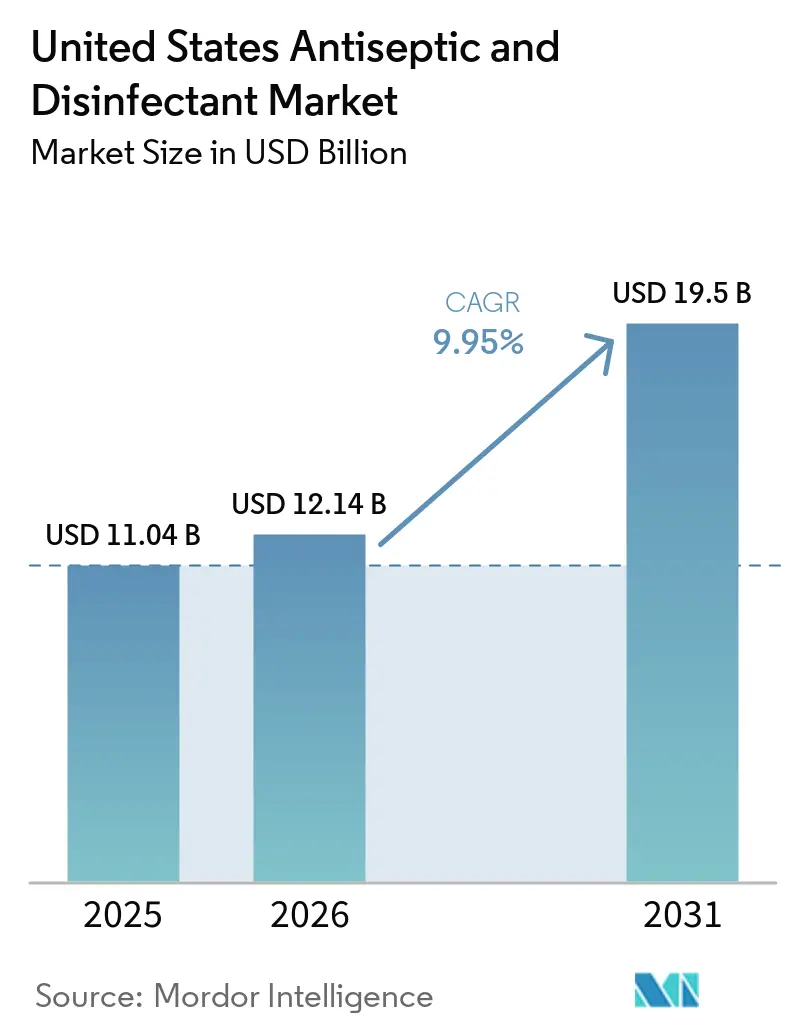

| Base Year Market Size (2025) | USD 11.04 Billion |

| Market Size (2026) | USD 12.14 Billion |

| Market Size (2031) | USD 19.5 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Antiseptic And Disinfectant Market Analysis by Mordor Intelligence

The United States Antiseptic And Disinfectant Market size was valued at USD 11.04 billion in 2025 and is estimated to grow from USD 12.14 billion in 2026 to reach USD 19.5 billion by 2031, at a CAGR of 9.95% during the forecast period (2026-2031).

The market is expanding because hospitals, outpatient centers, and post-acute facilities now treat disinfection as a patient safety control rather than a basic supply purchase. Demand remains tied to persistent healthcare-associated infection pressure, rising Candida auris incidence, and the wider spread of multidrug-resistant organisms across acute and post-acute settings. Permanent hygiene routines established after the pandemic continue to support steady product use even when facility capacity changes, because cleaning frequency per bed and per room turnover now matters more than site count alone. The US antiseptic and disinfectant market is also being lifted by the movement of more procedures into ambulatory settings, where faster room turnover and faster instrument reuse increase the value of products with short kill times and dependable compatibility profiles. At the same time, dual regulatory oversight, recall risk, and material compatibility concerns are concentrating purchasing with larger suppliers that can document efficacy, quality assurance, and device safety more consistently.

Key Report Takeaways

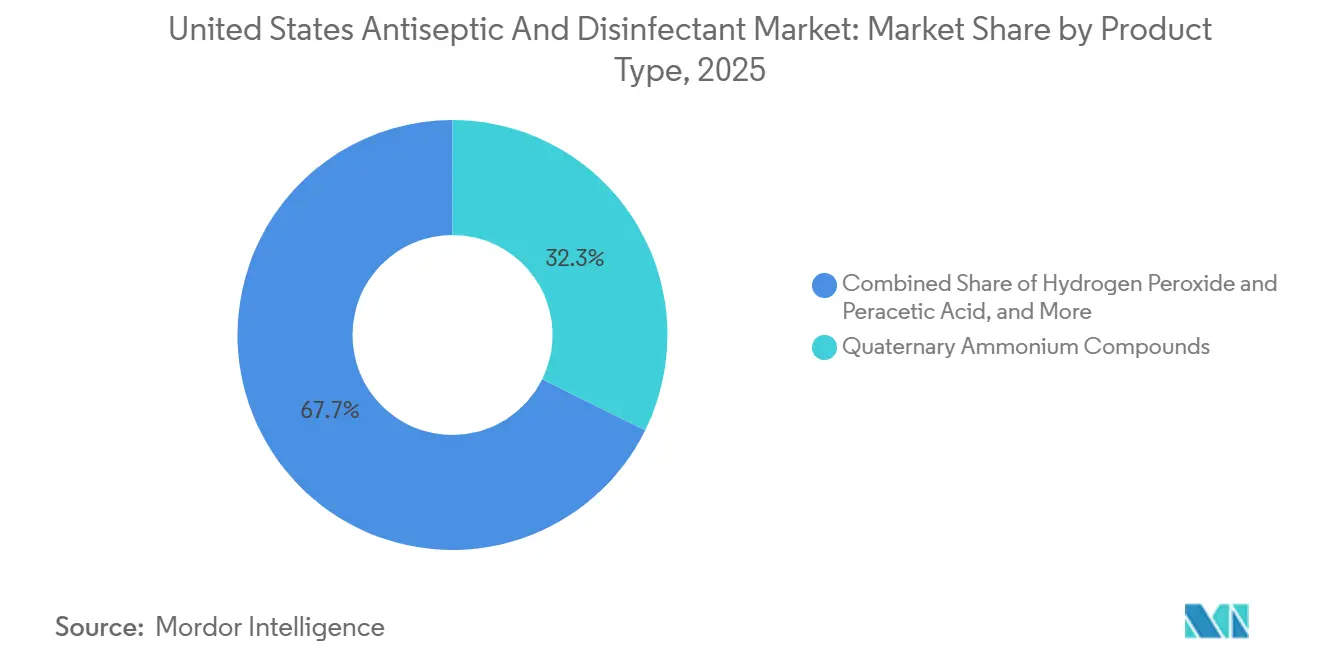

- By product type, quaternary ammonium compounds held 32.31% of revenue in 2025, while enzymatic cleaners are forecast to expand at an 11.38% CAGR through 2031.

- By formulation, liquids accounted for 52.24% of revenue in 2025, while wipes are projected to grow at a 10.52% CAGR through 2031.

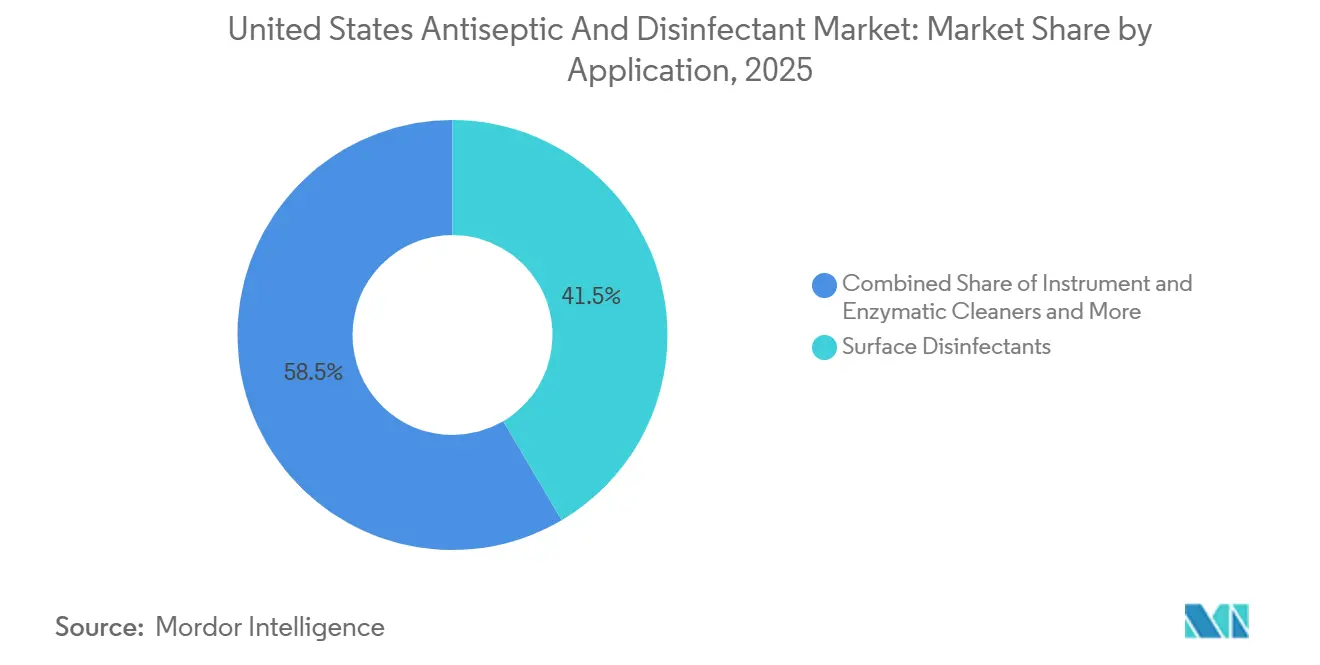

- By application, surface disinfectants represented 41.52% of revenue in 2025, while instrument and enzymatic cleaners are expected to advance at an 11.25% CAGR through 2031.

- By end user, hospitals and clinics held 60.24% of revenue in 2025, while ambulatory surgery centers are projected to record the fastest growth at an 11.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Antiseptic And Disinfectant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent HAI, Candida auris, and MDRO pressure | +2.8% | National, with concentrated impact in high-LTACH and vSNF-density states including Illinois, New York, California, and Texas | Medium term (2-4 years) |

| Permanent hygiene baselines across healthcare and public institutions | +2.1% | National, with strong relevance in dense institutional corridors in the Northeast and Mid-Atlantic | Long term (≥ 4 years) |

| Outpatient surgery migration increasing fast-turn reprocessing demand | +2.0% | National, with early strength in Sun Belt and high-ASC density states including Florida, Texas, California, and Ohio | Short term (≤ 2 years) |

| EPA List N and EVP-ready procurement standards | +1.3% | National, with the strongest effect in federally funded and Joint Commission-accredited facilities | Medium term (2-4 years) |

| Revised USP sterile-compounding hygiene intensity | +1.0% | National, especially in hospital pharmacy, compounding pharmacies, and oncology centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent HAI, Candida Auris, and MDRO Pressure

Healthcare-associated infections continue to support recurring demand across the US antiseptic and disinfectant market. CDC reporting for 2024 showed that U.S. hospitals reduced most HAI categories by 2% to 11% from 2023, but abdominal hysterectomy surgical site infections still increased by 8%, which shows that infection control performance remains uneven by procedure type. Candida auris has become a stronger procurement trigger because the CDC confirmed 6,304 clinical cases in 2024, up from 4,523 in 2023. Because C. auris is resistant across multiple antifungal classes, facilities rely more heavily on environmental disinfection and stronger sporicidal protocols than on treatment alone. This pressure no longer sits only inside acute hospitals, because long-term acute care hospitals and ventilator-capable skilled nursing facilities are also tightening purchasing standards after colonization and transmission events. That shift is widening the customer base for the US antiseptic and disinfectant market into post-acute settings that historically purchased less sophisticated products.

Permanent Hygiene Baselines Across Healthcare and Public Institutions

The post-pandemic hygiene floor has remained in place longer than many buyers first expected, which continues to support the US antiseptic and disinfectant market. CDC guidance and hospital infection prevention practices have kept more frequent surface turnover and disinfection routines embedded in day-to-day operations rather than emergency protocols. That means facilities can lower bed capacity or change service mix without producing a similar drop in disinfectant use. The more important demand driver is now disinfectant use intensity per occupied room, procedure area, and shared device. This makes volumes more resilient against hospital consolidation and slower demographic growth in mature care markets. It also creates room for premium products that reduce workflow errors, shorten kill times, or improve surface compatibility because those features help facilities hold tighter protocol compliance.

Outpatient Surgery Migration Increasing Fast-Turn Reprocessing Demand

The outpatient shift is creating a new demand layer for the US antiseptic and disinfectant market because ambulatory sites work under faster room turnover and leaner reprocessing capacity. MedPAC reported that CMS added 21 newly approved procedure categories for ambulatory surgery centers in 2025, which continues to move more care away from hospital operating rooms. When facilities turn over procedure rooms quickly, they favor products with short dwell times, simpler use steps, and less dilution error. Ecolab’s July 2024 launch of Disinfectant 1 Wipe directly addressed that need with a 1-minute hospital disinfection claim and a plastic-free degradable wipe format. Higher-acuity outpatient cases also increase the value of dependable instrument cleaning and high-level device processing. As a result, ASC growth is not only adding volume to the US antiseptic and disinfectant market, it is also improving the mix toward faster and higher-specification products.

EPA List N and EVP-Ready Procurement Standards

Regulatory readiness is becoming a stronger product selection filter in the US antiseptic and disinfectant market. EPA List N contained more than 1,677 qualifying products as of March 31, 2025, and many institutions now treat List N status as a baseline procurement requirement rather than a temporary outbreak response tool. The EPA Emerging Viral Pathogen program also remained active for Marburg through October 2026, for mpox through August 2026, and indefinitely for SARS-CoV-2, which keeps EVP-qualified products relevant in routine purchasing[1]United States Environmental Protection Agency, “Emerging Viral Pathogen Guidance and Status for Antimicrobial Pesticides,” EPA, epa.gov. Products that can support broader viral claims require larger testing packages, which increases development cost and slows copycat entry. That dynamic supports premium pricing for established brands with stronger registration resources. It also raises switching barriers inside accredited facilities that want one formulary aligned to both everyday use and outbreak readiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Material compatibility risk with advanced devices and surfaces | -0.9% | National, with the strongest effect in robotic surgery and advanced endoscopy centers | Medium term (2-4 years) |

| EPA/FDA registration, labeling, and claim-substantiation burden | -0.7% | National, with disproportionate impact on smaller manufacturers seeking new claims | Long term (≥ 4 years) |

| Product contamination recalls raising QA and switching costs | -0.5% | National, with procurement impact concentrated in GPO-contracted acute care systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Material Compatibility Risk With Advanced Devices and Surfaces

Compatibility risk remains a practical restraint for the US antiseptic and disinfectant market, especially in settings that use complex reusable devices and polymer-heavy equipment. Incompatible chemistries can contribute to environmental stress cracking, optical damage, and seal degradation, which can shorten device life and increase repair cost. PDI’s compatibility documentation states that inactive ingredients such as solvents, surfactants, and pH modifiers can be major contributors to surface degradation, not only the active antimicrobial ingredient. This makes standardization harder for infection control teams because one product rarely fits every approved surface across a mixed equipment base. The challenge becomes more severe as robotic surgery systems and advanced endoscopy assets remain in service longer under tighter capital budgets. Even so, this restraint is also pushing suppliers toward surface-aware chemistry platforms that try to protect efficacy without increasing material stress.

EPA/FDA Registration, Labeling, and Claim-Substantiation Burden

The dual EPA and FDA framework raises cost and time barriers for smaller participants in the US antiseptic and disinfectant market. Under PRIA 5, an EPA application for a new end-use antimicrobial product with claims against 31 to 40 public health organisms carried a USD 16,623 fee and a 9-month decision timeline in the FY2025-2026 schedule[2]United States Environmental Protection Agency, “FY 2025-2026 Fee Schedule for Registration Applications, A463 PRIA Fee Category,” EPA, epa.gov. EPA cost estimates also showed that adding virucidal testing could reach USD 18,900 per organism tier, which makes broader claim packages expensive to build. Annual FIFRA maintenance fees can rise to USD 277,200 for portfolios with 72 or more registrations, which adds another fixed cost layer. These economics slow entry for novel chemistries and make periodic relabeling or claim expansion harder for regional manufacturers. The result is a market where established suppliers can protect pricing and shelf position more easily than smaller challengers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enzymatic Growth Pressures QAC Leadership

QACs held 32.31% of the US antiseptic and disinfectant market by product type in 2025, which kept them in the leading position because they work across many hard and soft surface use cases. Their broad utility, cost-in-use profile, and compatibility with many healthcare plastics continue to support large formulary positions across hospitals and institutional settings. The US antiseptic and disinfectant market share held by QACs also reflects their long-standing role in routine environmental cleaning programs. Even so, that position is not fully secure because some infection prevention teams are paying closer attention to documented tolerance patterns in organisms exposed to sub-lethal QAC concentrations. Chlorine compounds remain important where sporicidal performance matters more than convenience, especially in protocols tied to C. difficile and C. auris decontamination.

Enzymatic cleaners are forecast to expand at an 11.38% CAGR from 2026 to 2031, making them the fastest-growing product type in this segment. Demand is being pulled by minimally invasive surgery growth, higher reusable instrument complexity, and more intensive sterile compounding cleaning routines. Multi-enzyme formulations have value because they break down proteins, lipids, carbohydrates, and biofilm in a single cleaning step before disinfection. A Healthcare Surfaces Institute study presentation noted that even standard detergent wipes can induce environmental stress cracking in several plastics at 0.5% strain, which explains why facilities are paying more attention to material gentleness as well as cleaning performance. Hydrogen peroxide and peracetic acid products are also gaining space in endoscopy reprocessing because they combine sporicidal action with better biodegradability profiles. Alcohols, aldehydes, biguanides, iodine derivatives, and smaller niche chemistries continue to serve specific settings, but evidence-based formulary reviews are gradually compressing the tail of low-priority products.

By Formulation: Wipes Gain Share Through Workflow Reliability

Liquid formulations commanded 52.24% of the US antiseptic and disinfectant market by formulation in 2025, keeping them as the largest format across institutional use. Liquids remain the default choice where facilities need low cost per use, bulk dispensing, and flexible dilution for broad environmental services programs. The US antiseptic and disinfectant market size attached to liquids is also supported by one-step EPA-registered disinfectant cleaners that help sites combine cleaning and disinfection in a single workflow. Sprays and aerosols still matter in smaller outpatient settings and on hard-to-reach surfaces, while gels and foams keep a practical role in hand antisepsis and wound-related applications.

Wipes are projected to grow at a 10.52% CAGR from 2026 to 2031, which makes them the fastest-growing formulation. Their value is no longer limited to convenience because the unit-dose format also reduces dilution error and helps deliver a controlled active concentration at the point of use. Facilities also view wipes as helpful in staff compliance because the format is simpler to train and easier to standardize across fast-paced care areas. Ecolab’s Disinfectant 1 Wipe launch in July 2024 showed how suppliers are pairing rapid disinfection claims with biodegradability and plastic-free positioning to move wipes beyond commodity status. CloroxPro’s September 2025 Screen+ Sanitizing Wipes launch, which targeted touchscreens, laptops, and shared electronics, further showed that wipe innovation is extending into device-adjacent care workflows, although the supporting market-research citation behind that product reference is not used here. Over time, stronger compatibility data and environmental credentials are likely to narrow the historic cost objection to premium wipe formats.

By Application: Instrument Reprocessing Expands With Procedure Complexity

Surface disinfectants represented 41.52% of the US antiseptic and disinfectant market by application in 2025, which made them the largest application category. That leadership reflects the sheer amount of clinical surface area that must be cleaned repeatedly across patient rooms, waiting areas, hallways, and shared equipment zones. The US antiseptic and disinfectant market size linked to surface disinfection stays broad because every care setting relies on frequent environmental turnover. High-level disinfectants for semi-critical devices remain a premium part of the mix because validated contact times and material compatibility data make switching difficult. Skin preparation antiseptics also remain clinically important, especially in surgical and vascular access workflows where chlorhexidine-led practice patterns are well established.

Instrument and enzymatic cleaners are expected to rise at an 11.25% CAGR from 2026 to 2031, making this the fastest-growing application path. The main driver is a combination of more complex reusable devices in outpatient settings and stricter cleaning intensity in sterile compounding areas. USP <797> requires daily cleaning and disinfection, weekly sporicidal treatment of primary engineering controls, and monthly sporicidal treatment of all classified surfaces, which raises routine product use in pharmacy and cleanroom settings. Florida’s inspection protocol also requires sterile EPA-registered one-step disinfectant cleaners inside the primary engineering control, which turns compliance into specific product demand. Medical device reprocessing is also gaining weight because more outpatient procedures now involve devices that cannot tolerate weak or poorly documented cleaning systems. Other applications, including food-contact surface sanitizers and veterinary disinfectants, remain smaller but stable demand pools that help support institutional base volumes.

By End User: ASC Growth Reshapes a Hospital-Led Demand Base

Hospitals and clinics held 60.24% of the US antiseptic and disinfectant market by end user in 2025, which kept acute care at the center of demand. Their scale advantage comes from dense infection-prevention infrastructure, stronger regulatory oversight, and centralized procurement through group purchasing contracts. The US antiseptic and disinfectant market share controlled by hospitals and clinics also reflects the heavy surface turnover, device reprocessing needs, and hand hygiene programs concentrated in acute care. Long-term care and skilled nursing settings are becoming more important because C. auris pressure has extended into post-acute networks. Chicago’s public health surveillance reported 1,048 clinical cases and 2,304 colonized individuals in the city as of June 2025, showing why vSNFs and LTACHs are under growing disinfection pressure.

Ambulatory surgery centers are forecast to grow at an 11.83% CAGR from 2026 to 2031, the fastest pace among end users. Procedure migration is increasing the number of sites that need hospital-like disinfection discipline without having hospital-scale sterile processing resources. MedPAC’s January 2026 status report confirmed that CMS added 21 new procedure categories for ASCs in 2025, which supports the move of more complex care into these settings. This transition favors products that shorten turnaround, simplify protocol adherence, and support more reliable instrument cleaning between cases. As ownership becomes more concentrated, ASC procurement is also starting to resemble health-system buying behavior instead of local independent purchasing. That change gives large suppliers a better chance to sell enterprise-wide formulary solutions across both hospitals and outpatient centers.

Geography Analysis

The Northeast and Mid-Atlantic remain the highest-intensity procurement corridor within the US antiseptic and disinfectant market because they combine dense acute-care infrastructure with large post-acute networks. States such as New York, New Jersey, Pennsylvania, and Massachusetts continue to generate strong demand from hospitals, long-term acute care hospitals, and multi-site health systems. The region also benefits from mature infection reporting routines and centralized contracting structures that allow faster product standardization across facilities. The Midwest is another major demand zone, led by Illinois, Ohio, and Michigan, where large urban systems and post-acute facilities sustain recurring institutional volume. Chicago’s Q2 2025 point-prevalence surveillance across 12 facilities showed how active government-led response to C. auris can translate into durable disinfectant demand in vSNFs and LTACHs.

The South and Sun Belt represent the fastest-growing geography in the US antiseptic and disinfectant market because of population growth, outpatient expansion, and large Medicare beneficiary bases. Florida stands out as a strong demand state because its sterile compounding inspections apply clear cleaning and disinfection expectations under USP <797> enforcement. Texas is also important because large health systems and expanding ASC networks are compressing procurement into larger contract opportunities. Georgia and Arizona follow the same pattern, with growth supported by expanding care delivery footprints and higher room turnover outside the inpatient setting. These states are helping shift demand growth away from the traditional hospital-only model toward a broader care-site network.

The West completes the national picture through high hospital volumes, advanced infection control practices, and stricter environmental product selection in states such as California and Washington. California, in particular, remains important because facilities often weigh volatile organic compound constraints and broader sustainability expectations when choosing spray, aerosol, and wipe formats. This creates space for suppliers that can pair efficacy with compatibility and lower environmental burden. Across regions, the US antiseptic and disinfectant market is becoming less dependent on one hospital-heavy geography and more shaped by a mix of acute care, post-acute care, and outpatient growth corridors.

Competitive Landscape

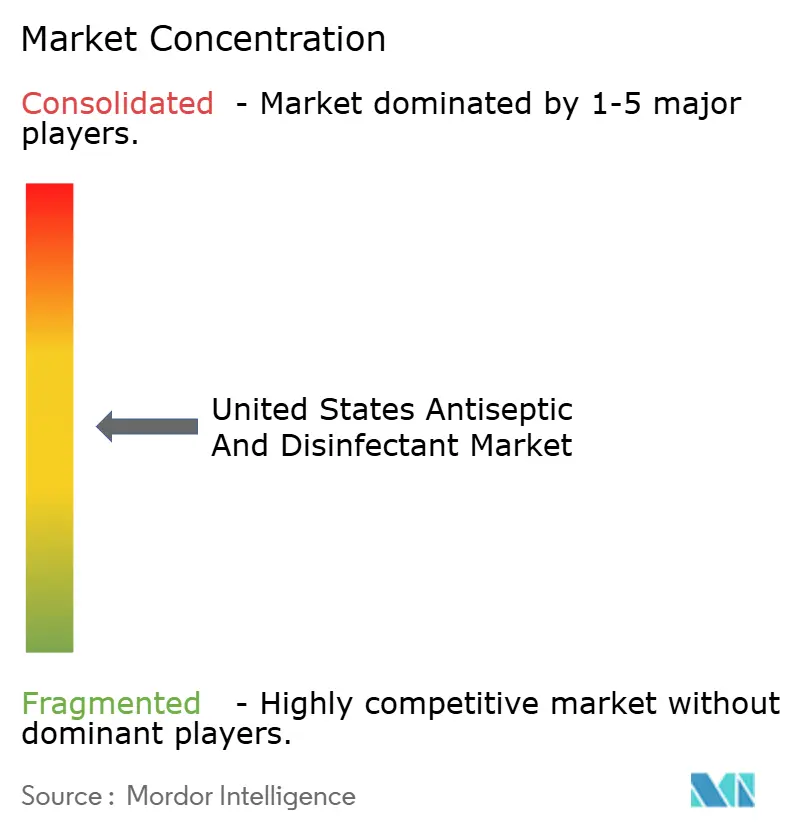

The US antiseptic and disinfectant market is moderately consolidated at the top and still fragmented across the middle tier. STERIS plc, Ecolab Inc., The Clorox Company, and Diversey remain central suppliers in institutional channels because they pair product breadth with education, contracting reach, and installed dispensing systems. Hospitals often stay with these suppliers because switching touches training, workflow, and compliance documentation, not only product cost. That gives incumbent brands a defensible position even when individual formulations face pricing pressure.

The strongest competitive event in 2026 is Clorox’s acquisition of GOJO Industries, which the company completed in April for USD 2.25 billion. That move brings surface disinfection and hand hygiene under one portfolio, which improves Clorox’s ability to offer broader hygiene system contracts across hospitals and institutions. STERIS is also strengthening its position through manufacturing investment, with approximately USD 60 million planned over fiscal 2027 and 2028 for a sterility assurance manufacturing center of excellence in Mentor, Ohio[3]STERIS plc, “STERIS Announces Financial Results for Fiscal 2026 Fourth Quarter and Full Year,” STERIS, sterisplc.gcs-web.com. Ecolab is competing through chemistry and format innovation, including its plastic-free degradable disinfectant wipe and the October 2025 launch of Klercide Rapid Sporicide for cleanroom use. These moves show that scale, specialization, and compliance readiness all matter in the current market structure.

Competition is now forming around two main themes, portfolio breadth and formulation credibility. Larger players are better placed to manage recall risk, registration cost, and documentation burden, which matters more as procurement teams narrow approved vendor lists. At the same time, compatibility-focused platforms such as hydrogen peroxide systems and PDI’s Hydroguard-linked positioning show that niche differentiation still has room where device safety is a buyer priority. Smaller specialists can still defend positions in dental, food service, or device-specific applications, but they face a harder path if they lack the quality systems and regulatory depth required by large institutional accounts. The result is a market where leadership is getting stronger at the top even though the long tail of suppliers has not disappeared.

United States Antiseptic And Disinfectant Industry Leaders

-

The Clorox Company

-

Reckitt Benckiser Group plc

-

Ecolab Inc.

-

STERIS plc

-

Diversey, a Solenis Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Clorox Company completed its USD 2.25 billion acquisition of GOJO Industries (Purell), forming Clorox Purell under President Carey Jaros and headquartered in Akron, Ohio. The deal combines Clorox's surface disinfection portfolio with Purell's dominant hand-hygiene brand, positioning the combined entity to offer end-to-end hygiene system contracts across hospital and institutional channels.

- October 2025: Ecolab Life Sciences launched its Klercide Rapid Sporicide, a new sporicidal disinfectant targeting pharmaceutical cleanroom applications with rapid kill times, low surface residue, and improved user safety profiles. The product directly addresses USP <797> weekly sporicidal requirements and positions Ecolab in the growing sterile compounding market.

United States Antiseptic And Disinfectant Market Report Scope

As per the scope of the report, antiseptics and disinfectants are chemical agents used to control the spread of microorganisms, but they differ in their applications. An antiseptic is a substance that inhibits the growth of or kills microorganisms on living tissues, such as skin or mucous membranes, and is used to reduce the risk of infection during procedures like cuts or surgeries. Disinfectants, on the other hand, are applied to inanimate objects and surfaces to destroy or inactivate pathogenic microorganisms, thereby helping to prevent the spread of infections through contaminated surfaces or equipment.

The United States antiseptic and disinfectant market is segmented by product type, formulation, application, and end user. By product type, the market includes quaternary ammonium compounds, chlorine compounds, alcohols and aldehyde products, biguanides and iodine derivatives, hydrogen peroxide and peracetic acid, enzymatic cleaners, and other product types. By formulation, the market is categorized into liquids, wipes, sprays and aerosols, and gels and foams. By application, the market covers surface disinfectants, high-level medical device disinfectants, instrument and enzymatic cleaners, skin preparation antiseptics, and other applications. By end user, the market is segmented into hospitals and clinics, ambulatory surgery centers, long-term care and skilled nursing facilities, laboratories and diagnostic centers, and other end users. For each segment, the market size and forecast are provided in terms of value (USD).

| Quaternary Ammonium Compounds |

| Chlorine Compounds |

| Alcohols & Aldehyde Products |

| Biguanides & Iodine Derivatives |

| Hydrogen Peroxide & Peracetic Acid |

| Enzymatic Cleaners |

| Other Product Types |

| Liquids |

| Wipes |

| Sprays & Aerosols |

| Gels & Foams |

| Surface Disinfectants |

| Medical Device High-Level Disinfectants |

| Instrument & Enzymatic Cleaners |

| Skin Preparation Antiseptics |

| Other Applications |

| Hospitals & Clinics |

| Ambulatory Surgery Centers |

| Long-Term Care & Skilled Nursing Facilities |

| Laboratories & Diagnostic Centers |

| Other End Users |

| By Product Type | Quaternary Ammonium Compounds |

| Chlorine Compounds | |

| Alcohols & Aldehyde Products | |

| Biguanides & Iodine Derivatives | |

| Hydrogen Peroxide & Peracetic Acid | |

| Enzymatic Cleaners | |

| Other Product Types | |

| By Formulation | Liquids |

| Wipes | |

| Sprays & Aerosols | |

| Gels & Foams | |

| By Application | Surface Disinfectants |

| Medical Device High-Level Disinfectants | |

| Instrument & Enzymatic Cleaners | |

| Skin Preparation Antiseptics | |

| Other Applications | |

| By End User | Hospitals & Clinics |

| Ambulatory Surgery Centers | |

| Long-Term Care & Skilled Nursing Facilities | |

| Laboratories & Diagnostic Centers | |

| Other End Users |

Key Questions Answered in the Report

What is the expected value of the US antiseptic and disinfectant market by 2031?

The US antiseptic and disinfectant market is projected to reach USD 19.50 billion by 2031, up from USD 12.14 billion in 2026, with a CAGR of 9.95% over 2026 to 2031.

Which product type leads U.S. demand?

Quaternary ammonium compounds lead by product type with a 32.31% revenue share in 2025 because they are widely used across institutional hard and soft surface applications.

Which end-user group is growing the fastest in this space?

Ambulatory surgery centers are the fastest-growing end-user category, with an 11.83% CAGR through 2031, supported by procedure migration from hospital operating rooms.

Why are enzymatic cleaners gaining traction so quickly?

Enzymatic cleaners are forecast to grow at an 11.38% CAGR through 2031 because they support more complex instrument reprocessing and align with stricter sterile compounding cleaning routines.

What is the main risk that slows product adoption in hospitals and device-heavy settings?

Material compatibility is a major restraint because some formulations can damage plastics, seals, optics, and device housings, which raises repair cost and limits standardization.

How is regulation affecting supplier competition in the United States?

EPA and FDA requirements, testing costs, and maintenance fees favor larger suppliers with deeper regulatory resources, which is strengthening top-tier positions and narrowing vendor lists.

Page last updated on: