Medical Nonwoven Disposables Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

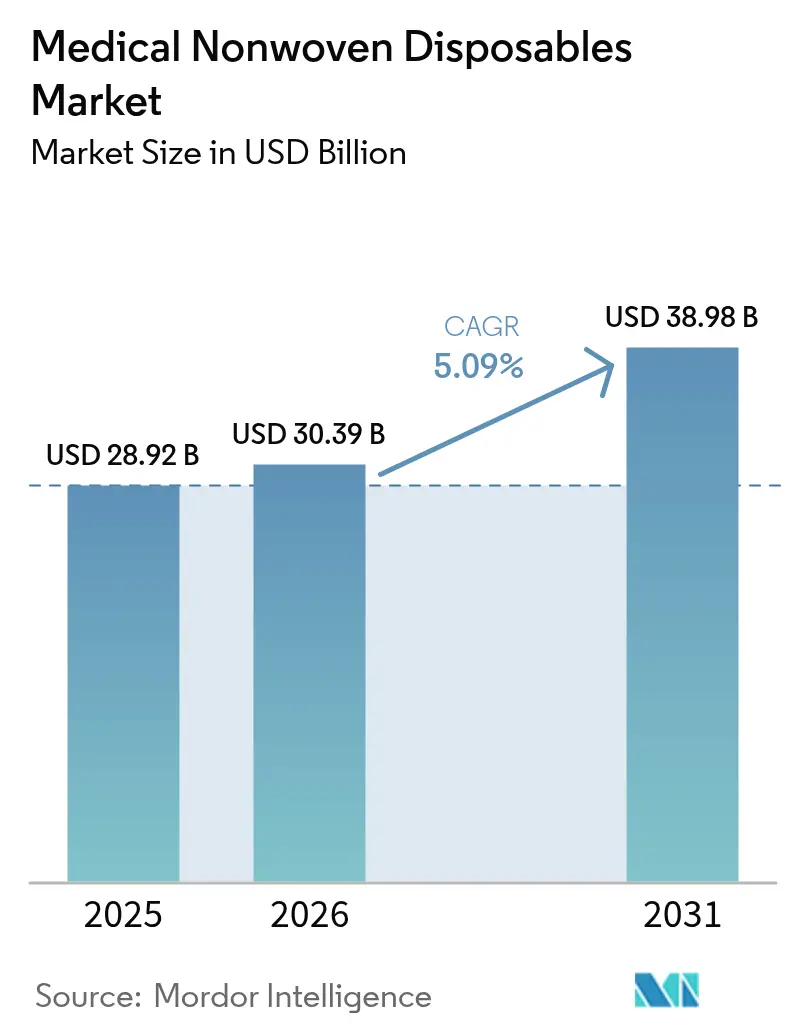

| Market Size (2026) | USD 30.39 Billion |

| Market Size (2031) | USD 38.98 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

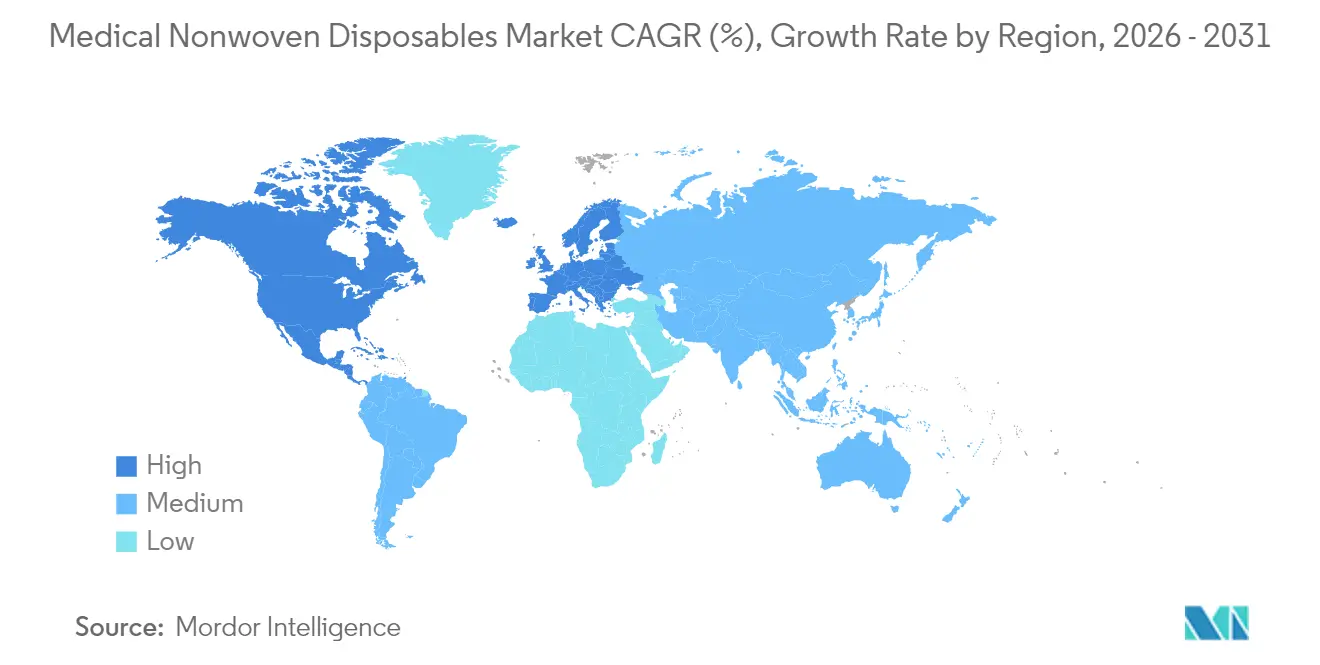

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

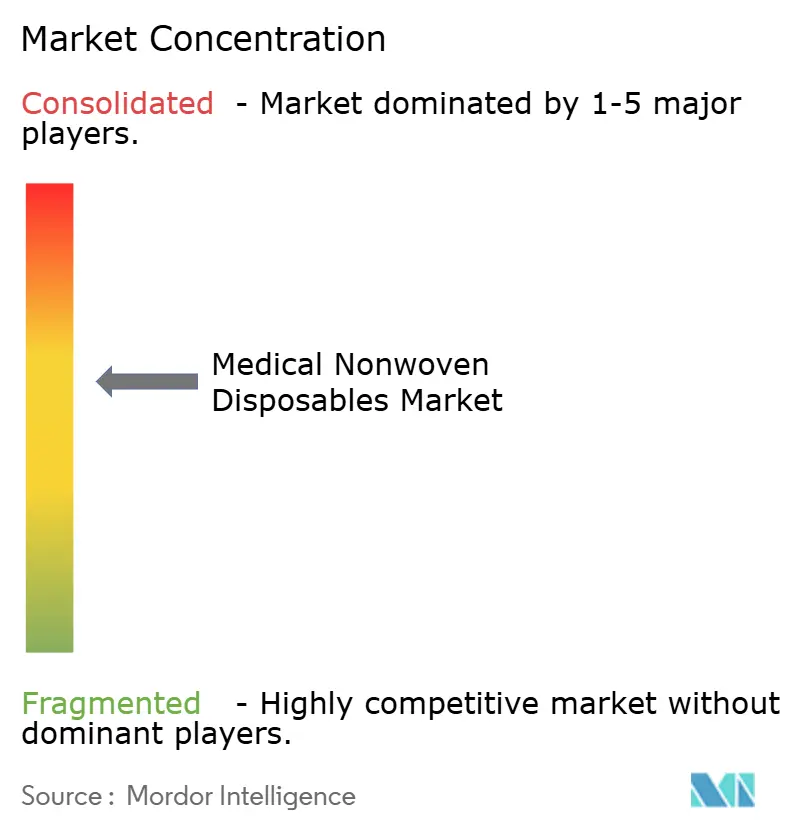

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Nonwoven Disposables Market Analysis by Mordor Intelligence

Medical Nonwoven Disposables Market size market size in 2026 is estimated at USD 30.39 billion, growing from 2025 value of USD 28.92 billion with 2031 projections showing USD 38.98 billion, growing at 5.09% CAGR over 2026-2031.

Rising demand for infection-barrier products, widespread adoption of disposable surgical apparel, and steady demographic shifts toward older populations continue to underpin volume growth. Product innovation, including breathable composites and antimicrobial finishes, enables premium pricing while helping hospitals comply with increasingly stringent infection-control protocols. Capital expenditure on domestic personal protective equipment (PPE) capacity in the United States, Europe, and selected Asia-Pacific markets enhances supply resilience, but cost pressure persists as polypropylene resin prices fluctuate. Sustainability imperatives are gradually redirecting investment toward biodegradable spunbond substrates, yet polypropylene remains indispensable due to its proven sterility performance and well-established regulatory track record. Competitive intensity remains moderate; leading suppliers use backward integration and proprietary barrier technologies to protect margins in a market that still rewards scale and reliability.

Key Report Takeaways

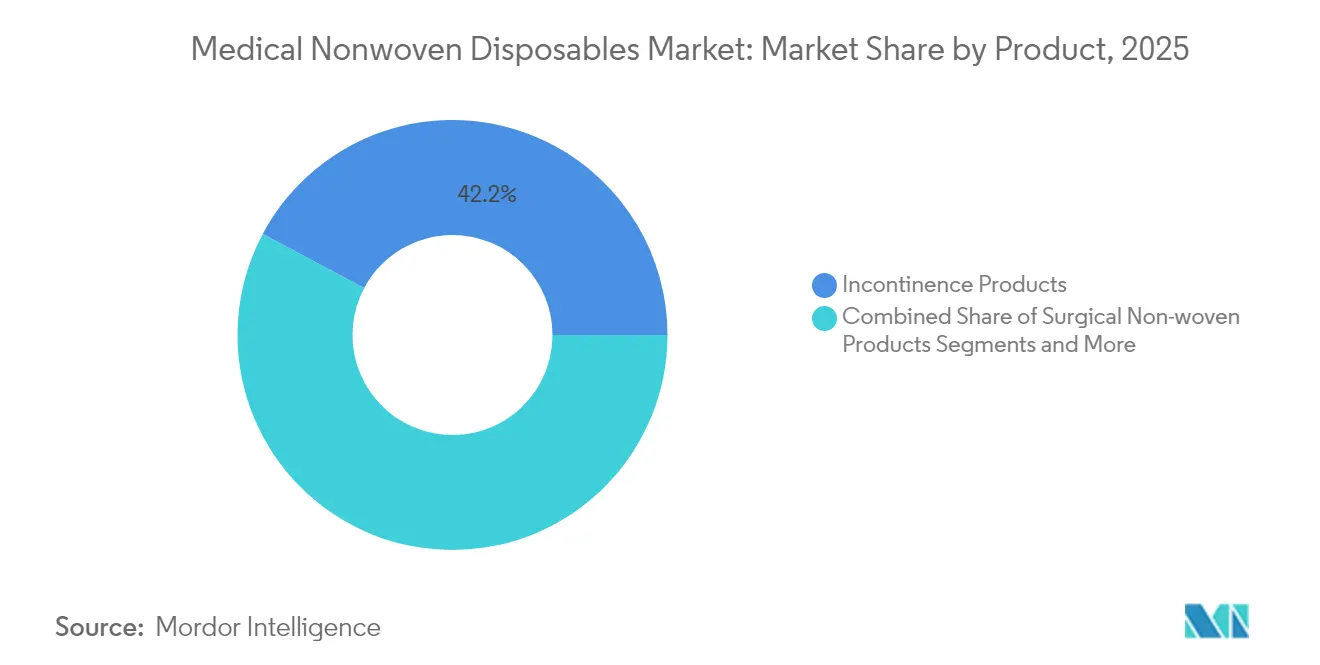

- By product category, incontinence products led with 42.21% revenue share in 2025; advanced wound dressings are forecast to expand at a 5.68% CAGR through 2031.

- By material, polypropylene spunbond held 47.62% of the medical nonwovens disposables market share in 2025, while biodegradable alternatives are projected to grow at a 5.55% CAGR through 2031.

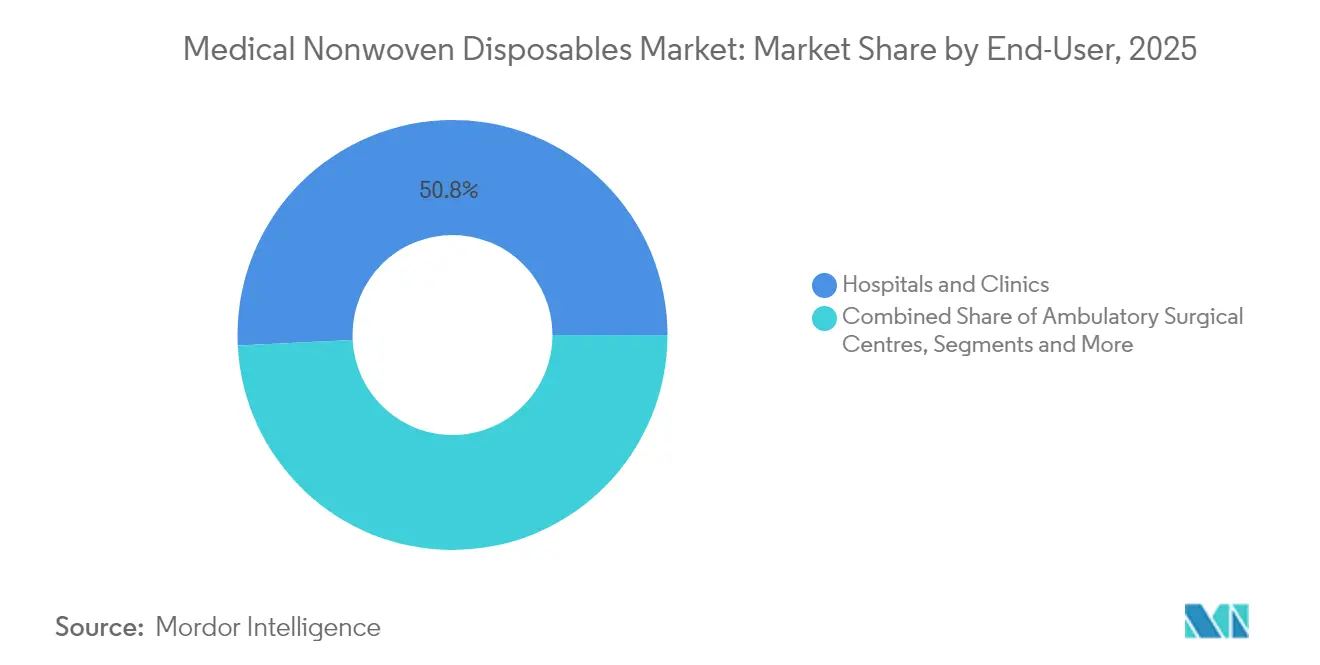

- By end-user, hospitals and clinics accounted for 50.78% share of the medical nonwovens disposables market size in 2025 and ambulatory surgical centers are advancing at a 5.92% CAGR through 2031.

- By distribution channel, hospital pharmacies led with 45.71% revenue share in 2025; online pharmacies are expected to rise at a 6.04% CAGR over 2026-2031.

- By geography, North America captured 39.83% of the medical nonwovens disposables market share in 2025 and Asia-Pacific is set to grow at a 6.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Nonwoven Disposables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Global Geriatric Population | +1.2% | Global, with highest concentration in North America, Europe, and Japan | Long term (≥ 4 years) |

| Rising Incidence Of Hospital-Acquired Infections | +0.8% | Global, particularly acute in developing healthcare systems | Medium term (2-4 years) |

| Expanding Surgical Volumes In Emerging Economies | +0.9% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Stringent Infection-Control Guidelines In Outpatient Settings | +0.6% | North America, Europe, with spillover to APAC | Short term (≤ 2 years) |

| Surging Adoption Of Antimicrobial-Impregnated Spun-Melt Nonwovens | +0.7% | Global, led by advanced healthcare markets | Medium term (2-4 years) |

| Government Subsidies For Domestic PPE & Medical Textile Manufacturing | +0.5% | United States, European Union, select APAC countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Global Geriatric Population

People aged 60 and older already exceed 310 million in China alone, a figure that is driving long-term demand for adult absorbent products and advanced wound dressings [1]LBX Pharmacy Chain, “2024 Annual Report,” LBX Pharmacy Chain, lbxpharmacy.cn. Chronic wound prevalence rises sharply with age, compelling both hospitals and home-health services to maintain higher inventories of breathable, skin-friendly nonwoven dressings. Long-term care facilities are expanding worldwide, and each bed translates directly into recurring demand for disposable bedding protectors and underpads. Clinical studies link aging to higher rates of frailty, malnutrition, and device-related infections, further reinforcing institutional reliance on sterile single-use drapes and gowns[2]Agency for Healthcare Research and Quality, “Prevention of Healthcare-Associated Infections,” AHRQ, ahrq.gov. Together these demographic pressures create a predictable, multi-year baseline for the medical nonwovens disposables market.

Rising Incidence of Hospital-Acquired Infections

Healthcare-associated infections cost U.S. hospitals USD 35.7–45 billion every year, with analysts estimating that 70% of cases can be prevented through better barrier materials and workflow controls. Hospital procurement teams therefore prioritize nonwovens that incorporate fluid-impervious layers and embedded antimicrobial chemistries. Audit-and-feedback programs increasingly measure compliance at the material level, reinforcing the link between product choice and reimbursement. Advanced gauze dressings infused with silver ions or cationic additives have demonstrated significant reductions in surgical-site infection rates, validating premium pricing for such solutions. Regulators in Europe and the United States now require performance data on microbial strike-through resistance, accelerating replacement of legacy cotton packs with engineered composites. The result is steady, price-supported uptake of higher-margin antimicrobial nonwoven SKUs.

Expanding Surgical Volumes in Emerging Economies

Ambulatory and inpatient procedure counts continue to rise across Asia-Pacific and parts of Latin America as public and private insurers broaden coverage. Medicare data show ambulatory surgical centers treating 3.3 million beneficiaries in 2022, underscoring how outpatient facilities translate into incremental consumption of single-use gowns, caps, and shoe covers. Providers in resource-constrained settings prefer disposable SMS packs that balance cost and protection, creating export opportunities for large-scale converters in China and India. Government stimulus programs aimed at upgrading provincial hospitals further lift demand for sterile surgical drapes. With minimally invasive surgery gaining traction, thinner, breathable drape films that resist alcohol-based prep solutions have become a key product differentiator. These trends collectively sustain above-average growth for procedure-driven subsegments of themedical nonwovens disposables market.

Stringent Infection-Control Guidelines in Outpatient Settings

The U.S. Food and Drug Administration will fully align its Quality Management System Regulation with ISO 13485:2016 in February 2026, imposing uniform design-control and traceability rules on surgical apparel manufacturers. Non-sterile isolation gowns now fall under Class II rules that require documented fluid-barrier performance, while surgical drapes are regulated under 21 CFR 878.4370 with similar test mandates. Outpatient surgical centers must meet these standards without on-site sterilization capacity, so they rely heavily on pre-packaged, terminally sterile nonwoven kits. Ethylene-oxide compatibility has therefore become a critical material attribute, steering converters toward polypropylene-rich structures that tolerate repeated sterilant exposure. Compliance deadlines and audit risk drive near-term procurement spikes for certified products, reinforcing volume forecasts for high-specification nonwovens.

Surging Adoption of Antimicrobial-Impregnated Spun-Melt Nonwovens

Hospitals now treat antimicrobial finishing as a first-line defense rather than an optional upgrade. Spun-melt composites that disperse zinc or copper additives through the fiber matrix inhibit gram-positive and gram-negative bacterial growth, extending safe wearing time for gowns and masks. Field data confirm lower colony-forming unit counts on treated drapes compared with untreated polypropylene, supporting formulary inclusion for specific antimicrobial brands. Global demand is most pronounced in heightened-risk procedures such as orthopedic implant surgery, where infection can double patient length of stay. Because additive masterbatches integrate seamlessly into existing melt lines, suppliers scale output quickly, translating material science advances directly into higher revenue for the medical nonwovens disposables market.

Government Subsidies for Domestic PPE Manufacturing

The Make PPE in America Act commits federal agencies to source selected protective products from domestic factories for at least five years, providing clear volume signals to U.S. converters [3]White House Office of Management and Budget, “Notice About Demand Forecast for PPE,” whitehouse.archives.gov. The Department of Homeland Security has mirrored this stance in its acquisition regulations, effectively guaranteeing baseline orders through 2029. Similar programs in the European Union reserve procurement quotas for within-bloc producers. These policy moves give vertically integrated players predictable cash flow to justify multimillion-dollar spunbond line investments. Capital formation reinforces supply resilience, shortens lead times, and enhances the global competitiveness of local suppliers, all of which support steady expansion of the medical nonwovens disposables market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Concerns Over Polypropylene-Based Waste | -0.9% | Global, with highest regulatory pressure in Europe and California | Long term (≥ 4 years) |

| Shift Toward Reusable Robotic & Laparoscopic Procedures | -0.6% | North America, Europe, advanced APAC markets | Medium term (2-4 years) |

| Volatility In Polypropylene Resin Pricing Due To Capacity Rationalisation | -0.7% | Global supply chain impact, acute in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Slow Clinical Acceptance Of Biopolymer Nonwovens Owing To Cost | -0.4% | Cost-sensitive markets in emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns Over Polypropylene-Based Waste

Life-cycle studies undertaken during the COVID-19 pandemic recorded steep increases in nonwoven waste volumes, highlighting landfill pressure and carbon footprints associated with single-use PPE. Regulators in the European Union and the state of California now explore extended-producer-responsibility schemes that could raise compliance costs for disposable products. Hospitals in urban centers have started piloting closed-loop collection for sterilizable textile alternatives, potentially eroding demand for low-value SMS gowns. Brands counter by introducing polylactic-acid (PLA) spunbond that degrades 95% within 90 days under commercial composting conditions, yet price premiums and limited sterilization data inhibit rapid substitution. Unless cost parity is achieved, sustainability will remain a headwind that modestly tempers the long-run CAGR of the medical nonwovens disposables market.

Shift Toward Reusable Robotic and Laparoscopic Procedures

Growth in minimally invasive surgery reduces the field size and fluid exposure area, enabling some facilities to substitute hard-surface drape accessories for disposable fabric kits. Reusable powered air-purifying respirator programs in large health systems lower annual mask burn rates by up to 90% and can save millions of dollars over a five-year depreciation cycle. While procedure volumes still rise, the per-case consumption of standard drapes and gowns can fall, pressuring unit sales. Suppliers respond with slimmed-down procedural packs tailored for robotic platforms, but market expansion remains slower than for open-surgery products. This dynamic introduces moderate, segment-specific drag on overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Demographic-Driven Dominance of Incontinence Lines

The incontinence segment held 42.21% of the medical nonwovens disposables market share in 2025. Consistent consumer uptake of adult briefs, underpads, and gender-specific liners underscores how stigma reduction campaigns and discreet product designs convert latent need into active purchasing. Manufacturers have boosted fluff-free core absorption and skin-contact softness, attributes that attract long-term-care operators and retail buyers alike. Disposable adult underwear volumes are rising in supermarkets and e-commerce channels, aided by plus-size SKUs that fit waistlines up to 95 inches.

Advanced wound dressings are the fastest-growing product cluster with a 5.68% CAGR as electrospun nanofiber scaffolds mimic extracellular matrix and foster moist-healing environments. Self-adhesive bioresorbable patches that integrate antibacterial agents and controlled-release growth factors shorten dressing change intervals, easing nursing workloads and lowering infection risk. Surgical packs remain a bedrock category, with procedure count growth offsetting modest pack optimization initiatives. Collectively, these trends ensure the medical nonwovens disposables market size continues to benefit from both volume-driven staples and value-added specialized dressings.

By Material: Polypropylene Rules but Green Alternatives Accelerate

Polypropylene spunbond represented 47.62% of the 2025 medical nonwovens disposables market size due to its favorable cost-to-performance ratio and straightforward compliance path. SMS and SMMS laminates blend spunbond strength with melt-blown filtration to meet high-stress surgical applications, and capacity additions in the United States and Vietnam are calibrated for healthcare volumes. Melt-blown webs maintain critical importance for N95-class respirators, with governments stockpiling media to hedge against future respiratory outbreaks.

Biopolymer and natural-fiber substrates posted the highest growth at 5.55% CAGR. PLA fibers from corn starch or sugarcane deliver hypoallergenic performance and moisture wicking for next-generation feminine hygiene pads. Start-ups leverage agricultural waste streams such as pineapple leaf and bagasse to spin biodegradable pulps into absorbent cores, a development that reduces fossil-carbon content while supporting rural economies. Although volumes remain small, price premiums have started to narrow as line speeds climb, setting the stage for broader adoption over the forecast period.

By End-User: Hospitals Anchor Demand, Outpatient Sites Surge

Hospitals and clinics absorbed 50.78% of the medical nonwovens disposables market size in 2025. They drive bulk orders for sterile surgical gowns, drapes, and shoe covers, often through multi-year tenders that favor integrated suppliers. Quality-linked reimbursement models encourage acute-care facilities to specify higher-grade barrier fabrics to curb infection penalties.

Ambulatory surgical centers posted the fastest growth at 5.92% CAGR as insurers steer low-risk procedures away from costlier hospital operating rooms. ASCs prefer all-in-one procedure kits that accelerate room turnover and simplify inventory. Home-healthcare use is also on the rise; disposable bed protectors and low-adherent dressings enable safe self-care in aging-at-home settings, further widening the customer base for the medical nonwovens disposables market.

By Distribution Channel: Digital Disruption Gains Traction

Hospital pharmacies held 45.71% revenue share in 2025 as integrated supply chains keep high-value inventory within arm’s reach of surgical suites. Group-purchasing organizations negotiate multi-facility contracts that lock in volume and price for as long as five years, ensuring predictable offtake for converters.

Online pharmacies achieved a 6.04% CAGR, benefiting from an e-commerce boom that lifted global healthcare retail sales to USD 309.62 billion in 2022 and could top USD 732.3 billion by 2027. Direct-to-consumer shipping of incontinence and wound-care SKUs bypasses store shelves, cutting handling costs while enhancing privacy for buyers. B2B platforms now match clinics with vetted suppliers, indicating that digital channels will carve a steadily larger slice of the medical nonwovens disposables market.

Geography Analysis

North America contributed 39.83% to 2025 revenue thanks to advanced infection-control standards, high procedure intensity, and federal incentives that channel PPE contracts to domestic mills. U.S. manufacturers committed over USD 290 million to new lines after federal demand forecasts guaranteed order visibility, though domestic unit costs remain above Asian benchmarks. Canada focuses on provincial stockpiles for pandemic resilience, further supporting regional utilization of premium nonwovens.

Asia-Pacific is forecast to post the fastest 6.42% CAGR through 2031 as governments expand universal health coverage and build surgical infrastructure. China commands significant export volume in wound dressings and packs, leveraging economies of scale and improving quality systems to hold global share. India, Indonesia, and Vietnam combine low labor costs with rising local consumption, prompting multinationals to establish joint ventures for closer-to-market production. Japan and South Korea sustain demand for high-specification drapes in robotic surgery, underpinning value growth.

Europe registers steady expansion on the back of stringent environmental mandates that stimulate early adoption of biodegradable spunbond fabrics. Extended-producer-responsibility rules set phased recycling targets for medical disposables, nudging procurement toward certified compostable gowns in Nordic hospitals. Eastern European facilities absorb niche contract manufacturing as Western EU converters focus on sustainable specialty lines.

The Middle East & Africa and South America together account for a modest but rising contribution to the medical nonwovens disposables market. Investment in flagship hospitals and national health-insurance schemes in Saudi Arabia, the United Arab Emirates, Brazil, and Chile create demand for disposable procedure packs, even though macro-economic volatility sometimes delays public tenders.

Competitive Landscape

The market shows moderate concentration; the top five suppliers control roughly 45% of global revenue. Kimberly-Clark announced USD 2 billion in North American expansion to shorten lead times and fortify its hospital portfolio. Berry Global invests in multilayer melt-blown capabilities that integrate electrostatic charging at the line, improving filtration while cutting secondary processing steps.

Freudenberg reported EUR 604.4 million in R&D expenditure for 2024 and continues to push low-basis-weight composites for advanced wound dressings. Asian challenger Magnera boosted spunbond width to 6.6 meters, enabling high-output PPE fabric runs that serve both export and domestic markets.

Mergers and acquisitions focus on niche technology pick-ups: Alkegen attracted fresh capital for its high-temperature specialty fibers, and specialty converters in Germany acquired nanofiber start-ups to secure sensor-ready wound-care platforms. Competition centers on barrier performance, sustainability credentials, and guaranteed on-time delivery, factors that collectively shape buyer preference in the medical nonwovens disposables market.

Medical Nonwoven Disposables Industry Leaders

Unicharm Corporation

Kimberly-Clark Corporation

Georgia-Pacific LLC

Cardinal Health, Inc.

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Seattle-based Singletto won FDA clearance for methylene-blue-infused face masks that deactivate pathogens on contact, offering an extra layer of protection for healthcare workers.

- August 2024: Manjushree Spntek introduced Hightex hybrid nonwovens for chemotherapy gowns with superior resistance to cytotoxic drug permeation.

- June 2024: Principle Business Enterprises added a 3XL size to its Tranquility disposable underwear range, featuring a higher-rising waist panel and extended side seams for plus-size users.

- May 2024: Medicare Hygiene Limited entered the cosmetics space with Earthika compostable wet wipes, expanding beyond its core bandage and surgical disposables portfolio.

Global Medical Nonwoven Disposables Market Report Scope

Nonwoven medical disposables are crucial products in the field of healthcare. Medical disposables have surpassed medical items made from woven fabrics in terms of popularity, providing a more hygienic alternative that effectively helps prevent contamination and infections. Nonwoven disposables can provide material with particular characteristics, such as absorbency, resilience, softness, strength, and elasticity.

The Medical Nonwoven Disposable Market is Segmented by Product (Incontinence Products and Surgical Nonwoven Products), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Other Distribution Channels), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally.

| Incontinence Products | Adult Diapers |

| Feminine Hygiene Pads | |

| Infant Diapers | |

| Surgical Non-woven Products | Surgical Gowns |

| Surgical Drapes & Packs | |

| Face Masks, Caps & Shoe Covers | |

| Advanced Wound Dressings | |

| Personal Protective Equipment (PPE) |

| Polypropylene Spunbond |

| Melt-blown |

| SMS/SMMS Composites |

| Air-laid Pulp |

| Biodegradable/Biopolymer Nonwovens |

| Hospitals & Clinics |

| Ambulatory Surgical Centres |

| Long-term Care Facilities |

| Home-healthcare Settings |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Incontinence Products | Adult Diapers |

| Feminine Hygiene Pads | ||

| Infant Diapers | ||

| Surgical Non-woven Products | Surgical Gowns | |

| Surgical Drapes & Packs | ||

| Face Masks, Caps & Shoe Covers | ||

| Advanced Wound Dressings | ||

| Personal Protective Equipment (PPE) | ||

| By Material | Polypropylene Spunbond | |

| Melt-blown | ||

| SMS/SMMS Composites | ||

| Air-laid Pulp | ||

| Biodegradable/Biopolymer Nonwovens | ||

| By End-user | Hospitals & Clinics | |

| Ambulatory Surgical Centres | ||

| Long-term Care Facilities | ||

| Home-healthcare Settings | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Medical Nonwoven Disposables Market size in 2026?

The medical nonwovens disposables market size stands at USD 30.39 billion in 2026, with a projected 5.09% CAGR to 2031.

Who are the key players in Medical Nonwoven Disposables Market?

Unicharm Corporation, Kimberly-Clark Corporation, Georgia-Pacific LLC, Cardinal Health, Inc. and Medtronic PLC are the major companies operating in the Medical Nonwoven Disposables Market.

Which is the fastest growing region in Medical Nonwoven Disposables Market?

Asia-Pacific is forecast to post the highest 6.42% CAGR over 2026-2031.

Why are antimicrobial nonwovens gaining traction?

Hospitals link these fabrics to measurable infection-rate reductions, supporting premium adoption.

Page last updated on: