Antimicrobial Hospital Curtains Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.60 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

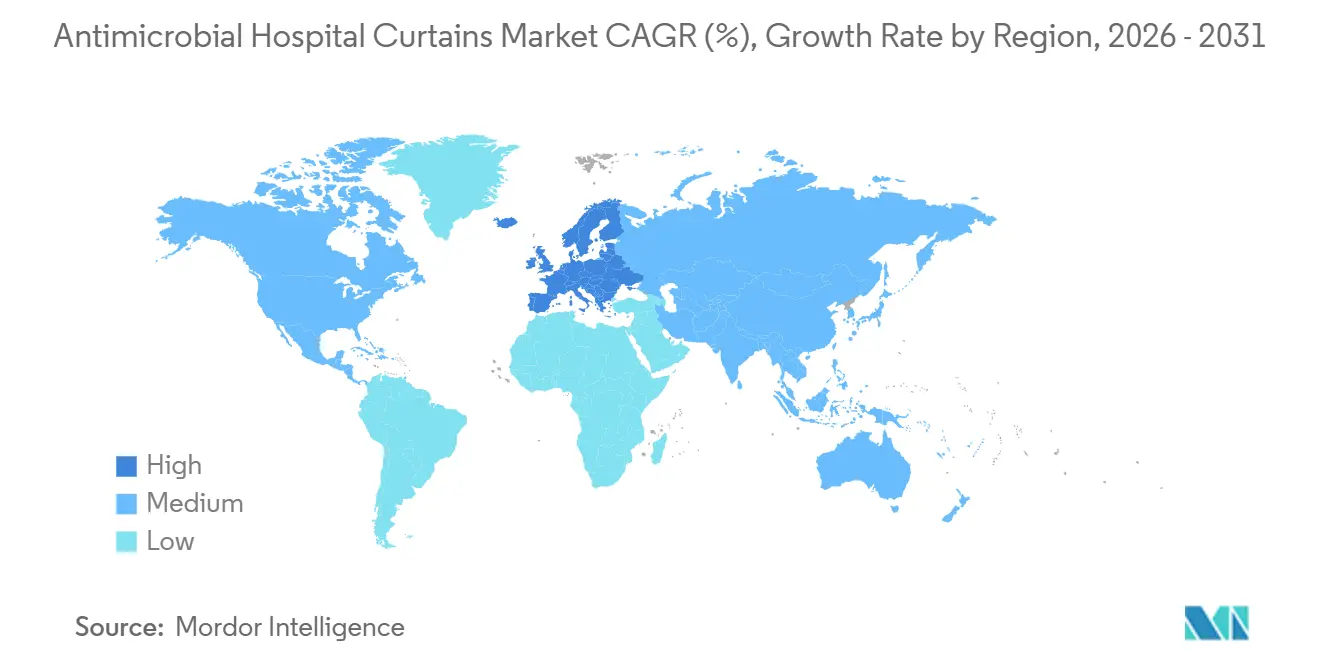

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

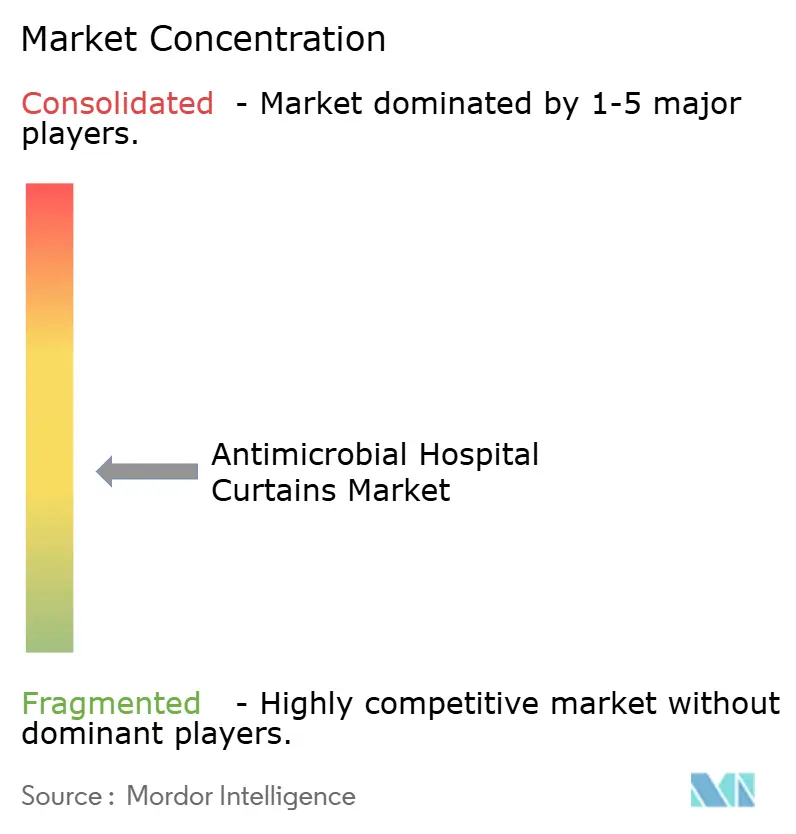

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antimicrobial Hospital Curtains Market Analysis by Mordor Intelligence

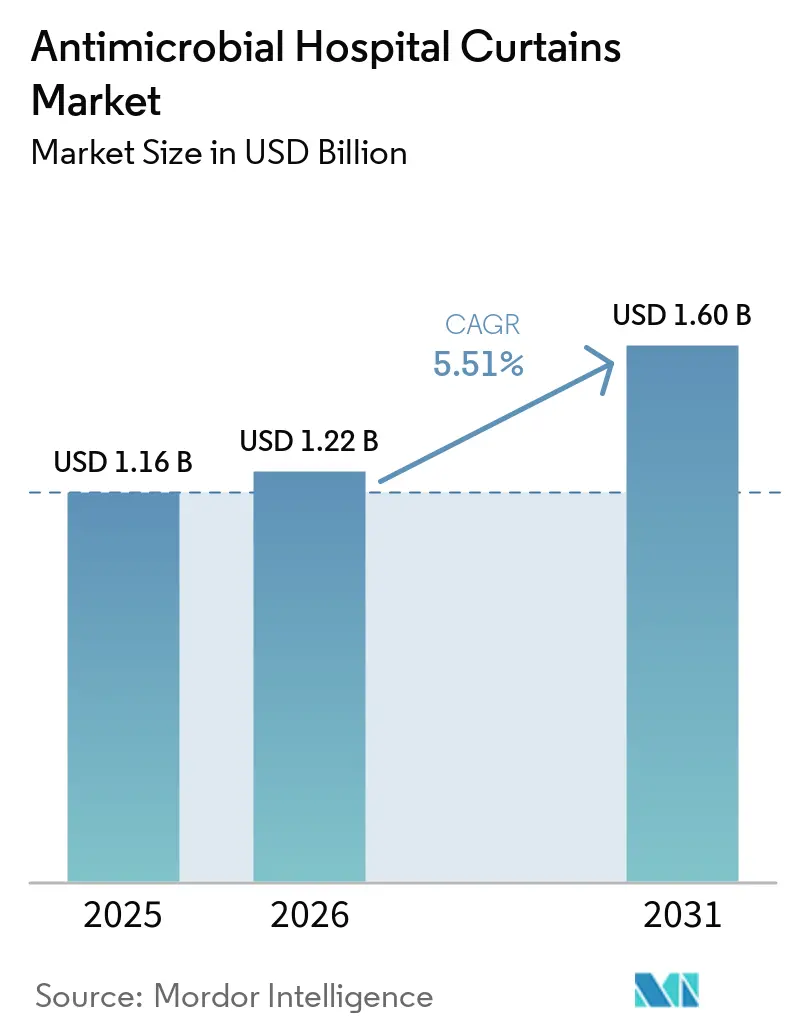

The Antimicrobial Hospital Curtains Market size is projected to be USD 1.16 billion in 2025, USD 1.22 billion in 2026, and reach USD 1.60 billion by 2031, growing at a CAGR of 5.51% from 2026 to 2031.

Heightened public reporting of healthcare-associated infections, reimbursement penalties tied to infection metrics, and the transition from voluntary to mandatory environmental hygiene protocols are the primary forces driving this trajectory[1]Centers for Disease Control and Prevention, “Healthcare-Associated Infections Data Portal,” cdc.gov. Hospitals continue to rationalize spending by prioritizing products that meet both flame-resistance (NFPA 701) and antimicrobial-efficacy standards (ISO 20743), while outpatient facilities accelerate purchases as procedures shift from hospital outpatient departments. Suppliers that pair treated fabrics with digital replacement-tracking systems enjoy a compliance premium because documentation reduces audit preparation time under Joint Commission inspections. Asia-Pacific leads demand on the back of hospital-bed expansion in China and India, but Europe offers the fastest growth due to the European Union Biocidal Products Regulation (BPR) and circular-economy mandates that steer procurement away from low-documentation imports.

Key Report Takeaways

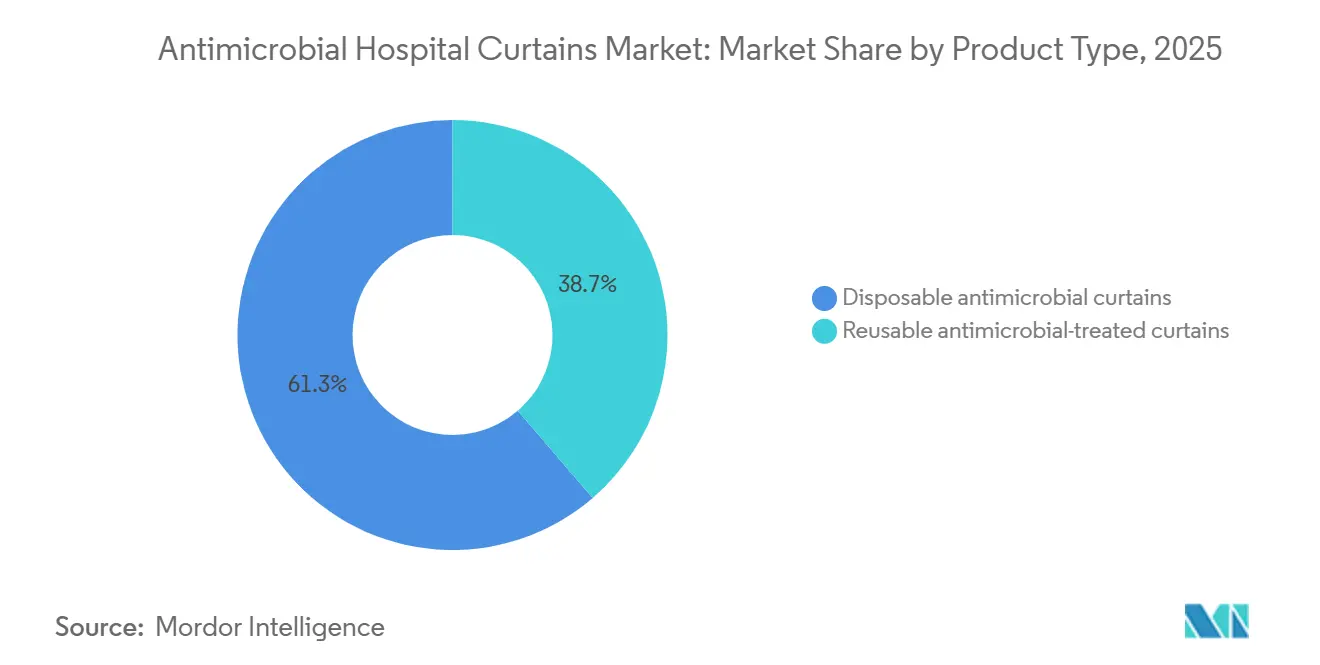

- By product type, disposable antimicrobial curtains held 61.30% of the antimicrobial hospital curtains market share in 2025, whereas reusable antimicrobial-treated curtains are projected to post the fastest CAGR at 6.18% through 2031.

- By end user, hospitals accounted for 65.60% of revenue in 2025; ambulatory surgical centers are forecast to expand at a 5.86% CAGR between 2026 and 2031.

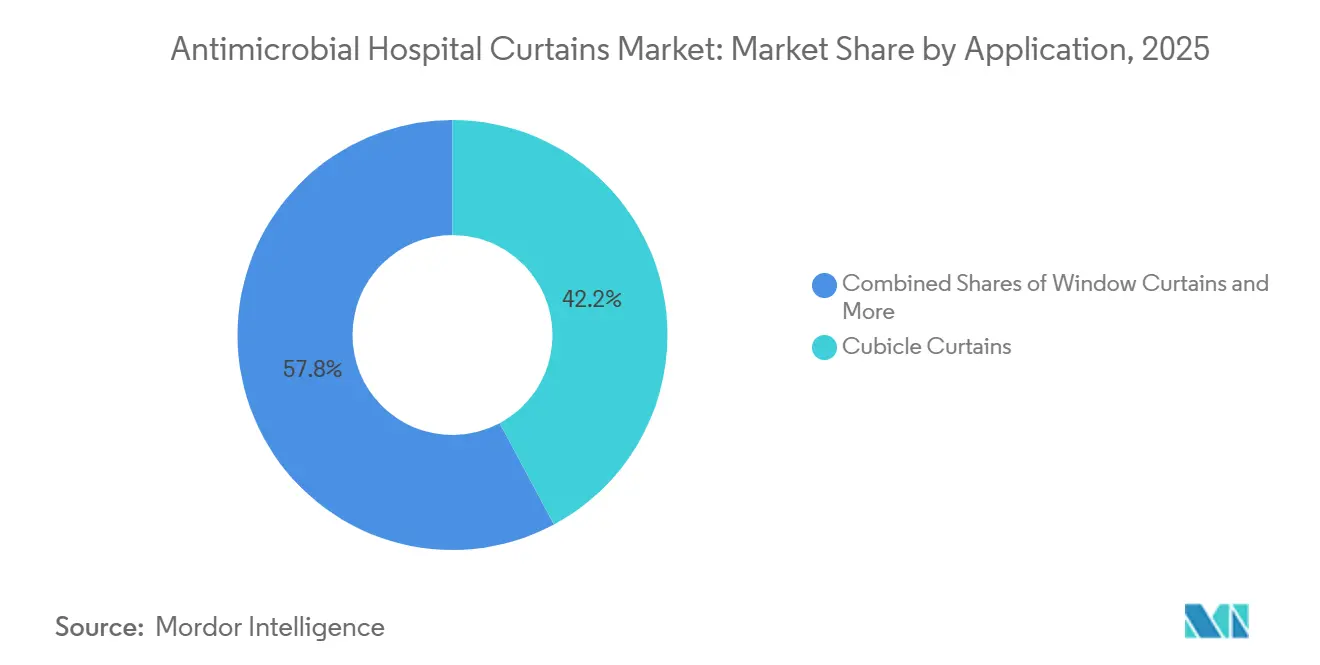

- By Applications, cubicle curtains accounted for 42.18% market share in 2025, whereas room divider curtains are forecasted to expand at a 6.13% CAGR through 2031.

- By material, the polypropylene led the market with 58.18% market share in 2025, and is expected to grow with 6.25% CAGR by 2031.

- By geography, Asia-Pacific accounted for 38.73% of global revenues in 2025, while Europe is poised to deliver the highest regional CAGR of 5.75% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antimicrobial Hospital Curtains Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HAI reduction and infection-control mandates elevate demand for treated privacy textiles | +1.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Shift to disposable antimicrobial PP curtains for rapid changeovers and lower laundry/labor cost | +0.9% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Built-in antimicrobial technologies (silver ions, quats) integrated into PP/polyester curtains | +0.8% | Global; premium uptake in North America and Europe | Long term (≥ 4 years) |

| North America compliance frameworks (NFPA 701, IPC audits) sustain premium adoption | +0.6% | United States and Canada | Long term (≥ 4 years) |

| EU BPR treated-article rules steer procurement to compliant actives/labels | +0.5% | Europe, spillover to Middle East & Africa | Medium term (2-4 years) |

| Ladderless snap-on/hookless systems improve EVS safety and room turnover | +0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

HAI Reduction and Infection-Control Mandates Elevate Demand for Treated Privacy Textiles

Hospitals reported that 1 in 31 patients experiences at least one healthcare-associated infection each day; 70% of such cases are preventable through robust protocols. Privacy curtains rank among the most frequently touched surfaces, and a 2024 randomized study from Hong Kong found that multidrug-resistant organisms colonized untreated curtains within 5 days, compared with 138 days for quaternary-ammonium-treated fabrics[2]V.C.C. Cheng et al., “Antimicrobial Curtains in Healthcare Settings,” ncbi.nlm.nih.gov. Reimbursement penalties under the Hospital-Acquired Condition Reduction Program amplify the economic stakes, moving antimicrobial procurement from discretionary to strategic spending. In the United Kingdom, the National Health Service’s “Bare Below the Elbows” policy and COVID-19-era cleaning guidelines elevated environmental hygiene discussions to the board level.

Shift to Disposable Antimicrobial PP Curtains for Rapid Changeovers and Lower Laundry/Labor Cost

Geisinger Health System’s 2024 operational audit found that hookless disposable curtains reduced changeout time to under 2 minutes, saved 7,000 environmental services hours, and eliminated laundry costs, resulting in higher HCAHPS scores. Australian lifecycle analysis validated that disposables become economically superior when replacement intervals fall below 90 days, a threshold increasingly mandated in infection-control policies. Labor shortages in North America and Asia-Pacific amplify this calculus, catalyzing a rapid pivot toward single-use polypropylene curtains. Although disposables dominate revenue today, the segment’s mature growth profile suggests a leveling off as sustainability pressures gain momentum.

Built-in Antimicrobial Technologies (Silver Ions, Quats) Integrated into PP/Polyester Curtains

The United States Patent and Trademark Office cleared SINTX Technologies’ silicon-nitride fabric claims in 2025, demonstrating market appetite for chemistries that curb leaching and cytotoxicity concerns associated with legacy silver-ion formulations. ICP Medical’s RFID-enabled Rapid Refresh Armor curtain embeds AEM 5700 antimicrobial treatment, maintaining≥log-3 bacterial reduction across 50 laundry cycles. Scientific Reports confirmed quaternary-ammonium coatings achieve 99.9% kill within one minute, yet Europe-wide implementation hinges on BPR compliance and label transparency.

North America Compliance Frameworks (NFPA 701, IPC Audits) Sustain Premium Adoption

The NFPA 701 flammability standard couples with Joint Commission audits to create a two-gate approval process, consolidating share among vendors that can demonstrate dual compliance. Standard Textile’s CubeControl platform automates traceability, shortening audit preparation and reinforcing demand for integrated data systems. CMS Conditions of Participation require environmental-hygiene documentation, nudging procurement toward suppliers offering end-to-end digital records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints and TCO skepticism for premium antimicrobial curtains | -0.8% | Global; highest in publicly funded systems | Short term (≤ 2 years) |

| Waste and sustainability pressure on single-use PP curtains | -0.6% | Europe and North America | Medium term (2-4 years) |

| Substitution by hard-surface privacy screens in high-risk areas | -0.4% | North America and Europe | Medium term (2-4 years) |

| Regulatory scrutiny of antimicrobial claims (BPR/EPA) slows launches | -0.3% | Global; strictest in Europe and United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints and TCO Skepticism for Premium Antimicrobial Curtains

APIC and The Leapfrog Group warned in 2025 that proposed USD 800 billion Medicaid cuts could force U.S. health systems to trim infection-prevention staffing by 25%, eroding willingness to pay 20-50% premiums for treated fabrics[3]Association for Professionals in Infection Control and Epidemiology, “Joint Statement on IPC Staffing Cuts,” apic.org. Historic surveys noted that infection-control budgets resisted prior austerity waves, yet the combination of Medicaid reductions and terminated NIH grants introduces unprecedented strain. When curtain replacements occur every 30 days, regardless of antimicrobial efficacy, procurement managers pivot to the lowest fire-safe, compliant option.

Waste and Sustainability Pressure on Single-Use PP Curtains

The European Union CEMTex program (2025-2029) allocates EUR 1.74 million to circular medical textiles, highlighting privacy curtains as a priority waste stream. California’s SB 707 extends producer responsibility to textiles, while the UK “Design for Life” roadmap forecasts a 56% reduction in carbon emissions from switching from single-use devices to reusables. Hard-surface screens such as Silentia claim 10-year lifespans and 1-3-year payback periods, framing disposables as environmentally negligent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reusables Gain Despite Disposables’ Dominance

Disposable curtains commanded 61.30% of the antimicrobial hospital curtains market share in 2025, driven by rapid turnover requirements and the freedom from laundry infrastructure. Yet reusable antimicrobial-treated curtains are projected to grow at a 5.98% CAGR, due to circular-economy mandates and new non-leaching chemistries that maintain efficacy through 100 wash cycles. Geisinger’s operational audit underscored disposables’ labor savings, but Europe’s Waste Directive and California’s SB 707 narrow their long-term viability. AHRQ’s 2024 evidence-mapping protocol on reprocessed versus single-use devices may tilt U.S. policy toward reusables if environmental data corroborate cost advantages.

Reusable’s growth hinges on infrastructure: a 2025 Journal of Cleaner Production study for the National Health Service cited gaps in sterilization capacity and entrenched supply habits as obstacles. Nevertheless, vendor innovation, hookless tracks, snap-off panels, RFID-driven hang-time tracking, lowers changeout friction, incentivizing hospitals to reconsider long-life fabrics. As a result, the Antimicrobial hospital curtains market size for reusable formats is forecast to increase in tandem with extended producer responsibility laws across key states and EU member nations.

By End User: ASCs Drive Growth as Procedures Migrate Outpatient

Hospitals accounted for 65.60% of revenue in 2025, reflecting their sheer bed volume and regulatory exposure. Ambulatory surgical centers, however, are expanding at a 5.86% CAGR, mirroring procedural migration catalyzed by CMS payment reforms and patient preference for same-day discharge. Disposable curtains dominate this segment because facilities rarely maintain on-site laundries, and ladder-free mounting systems introduced by PRVC Systems in 2025 dovetail with rapid case turnover.

Clinics and long-term care facilities trail in uptake, but recent surges in methicillin-resistant Staphylococcus aureus infections in UK long-term care settings are reshaping risk assessments and procurement priorities. As accreditation bodies such as AAAHC and AAAASF tighten documentation requirements, even smaller outpatient sites are now implementing electronic curtain-tracking tools, driving incremental growth in the Antimicrobial hospital curtains market.

By Application: Room Dividers Capture Flex-Capacity Demand

The room divider curtains segment is projected to expand at a 6.13% CAGR from 2026 to 2031, the fastest trajectory among application categories within the healthcare curtains market size. Hospitals and ambulatory surgical centers increasingly favor these modular partitions because they let staff transform general wards into isolation bays or multi-acuity pods without capital-intensive construction, a capability that became standard practice after COVID-19 institutionalized surge-capacity planning. Demand also benefits from the smaller footprints of new outpatient facilities, where pre-operative, procedure, and recovery zones must coexist in flexible, open layouts. Disposable snap-off panel systems introduced by Standard Textile in 2025 enable environmental-services teams to replace only soiled sections, trimming labor and material waste in high-turnover areas.

Cubicle curtains retained a sizable 42.18% share of the healthcare curtains market share in 2025, underscoring their entrenched role around patient beds, yet their growth pace lags as penetration nears saturation in developed regions. Window curtains continue to lose relevance because new hospital designs integrate blinds, electrochromic glass, or privacy films that eliminate fabric maintenance and associated infection-control risks.

By Material: Polypropylene’s Dual Dominance Defies Sustainability Headwinds

Polypropylene held a 58.18% slice of the healthcare curtains market share in 2025 and is on track to expand at a 6.25% CAGR between 2026 and 2031, giving the segment a rare combination of scale and speed inside the broader healthcare curtains market size. This growth persists even as Europe’s CEMTex initiative and California’s SB 707 law tighten rules on single-use plastics, because hospitals keep prioritizing low total cost of ownership over circular-economy goals. Geisinger Health System showed why in 2024 when it reported that disposable polypropylene curtains eliminated laundry spend and freed 7,000 environmental-services labor hours in one year.

Geography Analysis

Asia-Pacific generated 38.73% of global revenue in 2025, led by China’s 9.93 million hospital beds and 10.3 billion outpatient visits, both up double digits year over year. India’s bed stock must climb by 1.3 million by 2030 to meet demand, further solidifying the region’s volume advantage. Although hospitals in China and India prioritize cost-effective formulations, Singapore, South Korea, and Japan allocate capital budgets for RFID-enabled curtain systems consistent with their smart-hospital roadmaps.

Europe is projected to log the fastest regional growth at a 5.75% CAGR, driven by strict BPR enforcement, ISO 20743 efficacy testing, and waste-reduction directives that reward compliant suppliers. Germany and the Nordic nations impose the highest documentation thresholds, funneling orders toward established European manufacturers with full dossiers, while Southern Europe admits lower-cost imports under lighter oversight. The region’s uptake of hard-surface screens in ICUs accelerates pressure on fabric-based suppliers to innovate, but, in parallel, raises overall spend on privacy solutions.

North America ranked second in 2025 share, buoyed by NFPA 701 requirements and Hospital-Acquired Condition Reduction Program penalties that tighten infection-prevention budgets toward compliance-ready offerings. Yet looming Medicaid cuts and a USD 240 million reduction in Hospital Preparedness Program funding temper future growth, contributing to a modest regional CAGR below the global average. Canada’s publicly funded model shows slower adoption, while Mexico’s private hospital groups import EU-certified curtains to satisfy Joint Commission International accreditation.

Competitive Landscape

The antimicrobial hospital curtains market remains moderately fragmented. North American incumbents, Standard Textile, Medline Industries, and Cube Care Company, secure large contracts by bundling fire-safety and antimicrobial certifications with digital compliance dashboards. Standard Textile’s 2024 AMY hookless curtain and 2025 snap-off panels reduce environmental-services labor, strengthening retention in tertiary centers. Medline’s CurtainMaster suite ties RFID tags to electronic health records, positioning data services as a differentiator rather than relying solely on fabric specifications.

Disruptive entrants rely on material science. SINTX Technologies’ silicon-nitride fabric claims non-leaching antipathogenic performance, addressing concerns about silver-ion resistance and potentially redrawing supplier shortlists in premium segments. ICP Medical embeds AEM 5700 treatment within Rapid Refresh Armor curtains, validated by Scientific Reports for immediate log-3 bacterial reduction, meeting fast-kill benchmarks in critical care.

Hard-surface privacy-screen firms such as Silentia and KwickScreen capitalize on evidence of eight-fold lower bacterial counts versus fabric, leveraging 10-year life cycles and 1-3-year payback periods to penetrate intensive care budgets. Emerging European manufacturers craft circular-ready reusable curtains to satisfy Waste Directive mandates, while Asian suppliers court price-sensitive markets, sustaining a coexistence of high-documentation and low-documentation tiers within the Antimicrobial hospital curtains industry.

Antimicrobial Hospital Curtains Industry Leaders

Standard Textile Co., Inc.

Medline Industries

Cube Care Company

EcoMed Curtains

Hygenica Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: SINTX Technologies received USPTO allowance for silicon-nitride antipathogenic fabrics, targeting a USD 30 billion addressable antimicrobial-textile space.

- January 2025: PRVC Systems debuted ladder-free sustainable curtains aimed at ambulatory surgical centers seeking rapid changeouts without laundry infrastructure.

Global Antimicrobial Hospital Curtains Market Report Scope

As per the scope of the report, antimicrobial hospital curtains are specialized medical textiles treated with agents that inhibit or kill harmful microorganisms, such as bacteria, viruses, and fungi, on their surfaces. Unlike standard cotton or polyester curtains, which can rapidly become reservoirs for pathogens such as MRSA or VRE, antimicrobial versions use technologies such as silver ions, copper-based compounds, or quaternary ammonium compounds (QACs) to disrupt microbial cell membranes and prevent colonization.

The antimicrobial hospital curtains market is segmented by product type, end users, application, material, and geography. By product type, the market is segmented into disposable antimicrobial curtains and reusable antimicrobial-treated curtains. By end users, the market is segmented into hospitals, ambulatory surgical centers, clinics & long-term care facilities. By applications, the market is segmented into cubicle curtains, window curtains, room divider curtains, and others. By material, the market is segmented into polypropylene, polyester, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Disposable antimicrobial curtains |

| Reusable antimicrobial-treated curtains |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics & Long-term Care Facilities |

| Cubicle Curtains |

| Window Curtains |

| Room Divider Curtains |

| Others |

| Polypropylene |

| Polyester |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Disposable antimicrobial curtains | |

| Reusable antimicrobial-treated curtains | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics & Long-term Care Facilities | ||

| By Application | Cubicle Curtains | |

| Window Curtains | ||

| Room Divider Curtains | ||

| Others | ||

| By Material | Polypropylene | |

| Polyester | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is demand for antimicrobial hospital curtains growing?

Global revenue is projected to rise at a 5.51% CAGR from 2026-2031, moving the antimicrobial hospital curtains market size from USD 1.2 billion to USD 1.6 billion.

Which product format is gaining share in Europe?

Reusable antimicrobial-treated curtains are growing fast because EU waste regulations penalize single-use polypropylene disposables.

Why are ambulatory surgical centers important to suppliers?

ASCs show the highest end-user CAGR of 5.86% through 2031, as procedural shifts require rapid-turnover solutions that favor disposable or ladder-free curtains.

What technologies differentiate premium suppliers?

RFID tags integrated into curtains enable automated hang-time tracking and compliance reporting demanded during Joint Commission inspections.

Page last updated on: