Medical Device Cleaning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

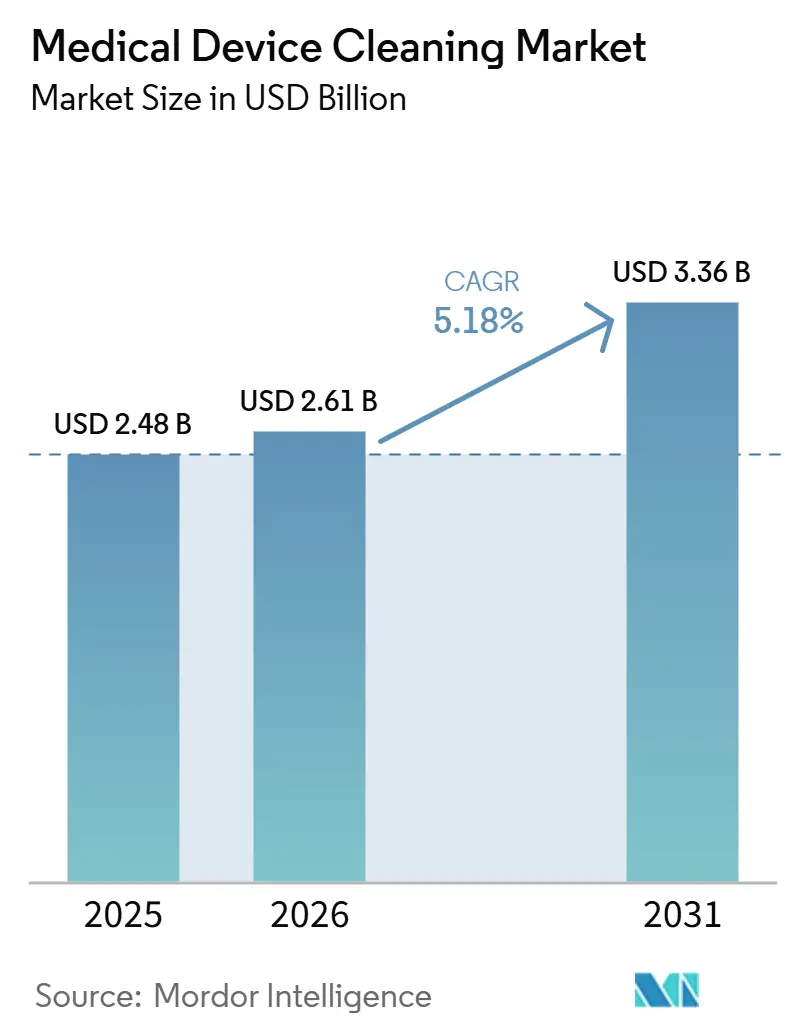

| Market Size (2026) | USD 2.61 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

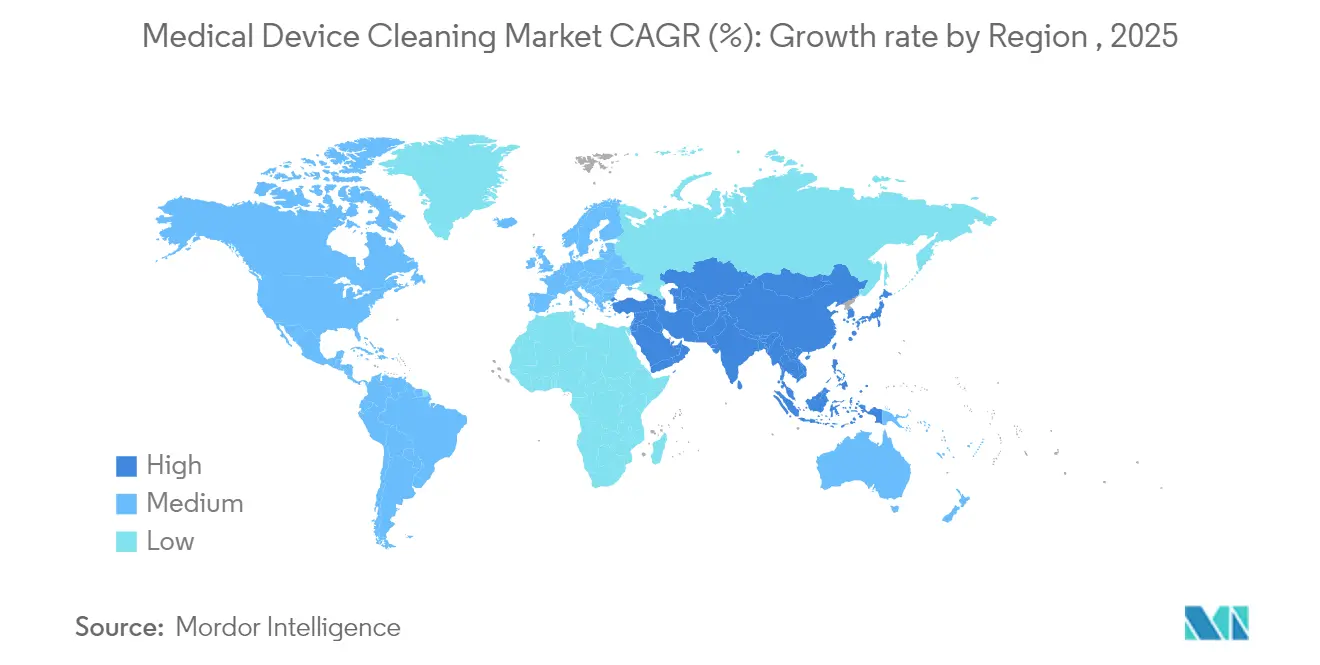

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device Cleaning Market Analysis by Mordor Intelligence

The medical device cleaning market size was valued at USD 2.48 billion in 2025 and estimated to grow from USD 2.61 billion in 2026 to reach USD 3.36 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031). Growth reflects healthcare providers’ heightened infection‐prevention focus as roughly 1 in 31 U.S. in-patients acquires a hospital-associated infection (HAI) during admission[1]Source: Centers for Disease Control and Prevention, “2023 National and State HAI Progress Report,” cdc.gov . Tighter oversight, including the U.S. FDA’s updated reprocessing guidance and the European Union’s Medical Device Regulation 2017/745, requires documented cleaning validation for every reusable device, creating predictable demand for proven chemistries and automated washer-disinfectors. Manufacturers are also capitalizing on surgical-volume growth, the rise of outpatient facilities, and digital monitoring that links cleaning cycles to real-time compliance dashboards. Investment in low-temperature enzyme-based detergents is accelerating as facilities transition away from ethylene oxide sterilization amid emission scrutiny.

Key Report Takeaways

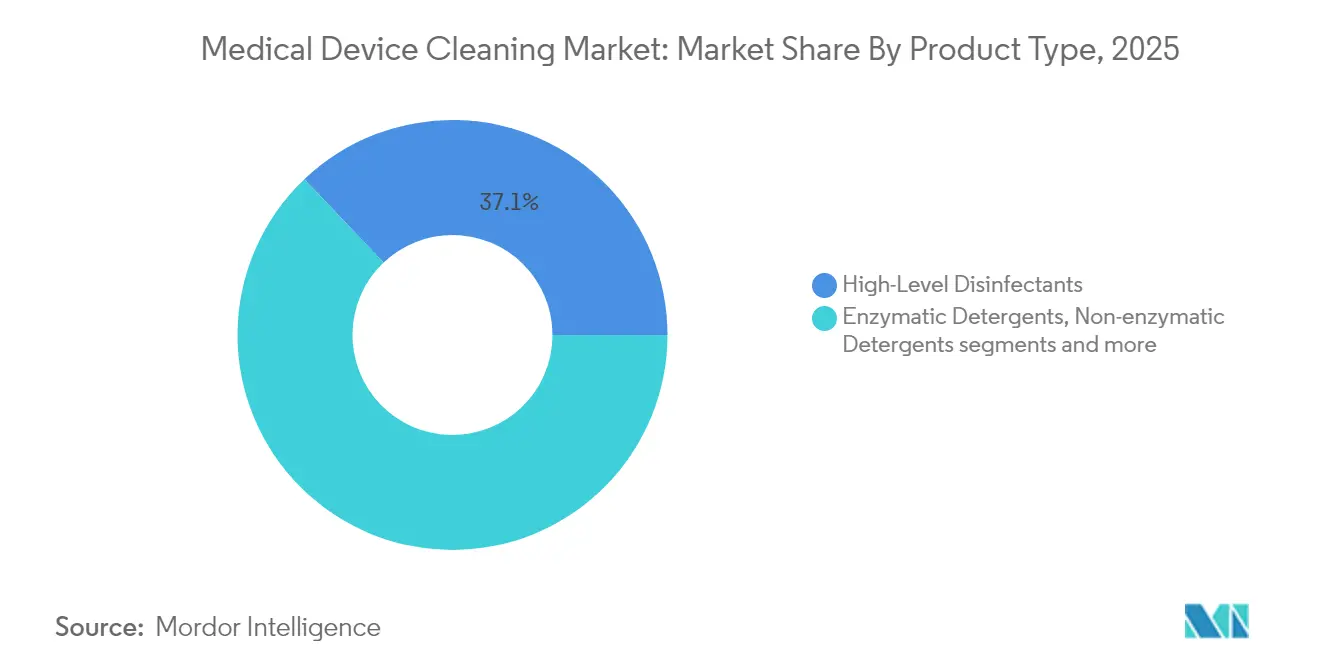

- By product type, High-Level Disinfectants held 37.10% of 2025 revenue, whereas Enzymatic Detergents are projected to expand at 6.63% CAGR to 2031.

- By cleaning process, Automated Washer-Disinfectors led with 40.85% revenue share in 2025; UV/Ozone/Emerging Technologies are expected to grow at 7.42% CAGR through 2031.

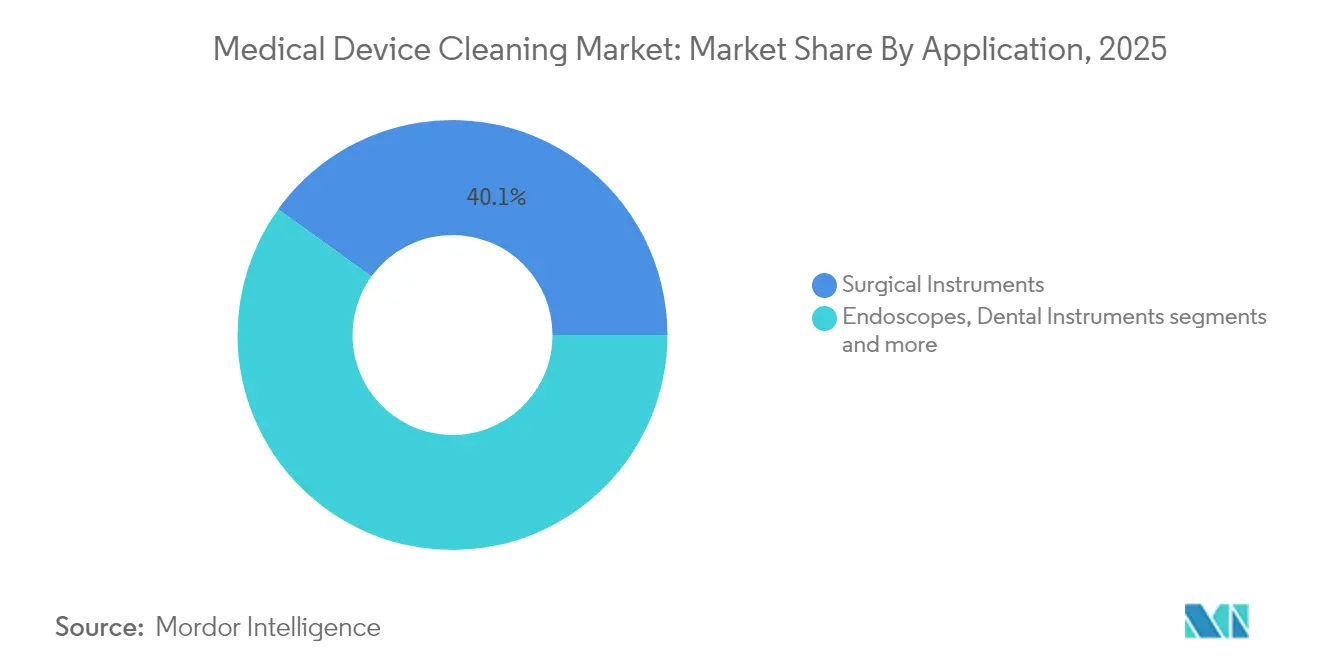

- By application, Surgical Instruments accounted for 40.05% of the medical device cleaning market share in 2025, while Endoscopes are forecast to rise at 6.91% CAGR to 2031.

- By geography, North America commanded 42.80% revenue in 2025; Asia-Pacific is poised for the fastest growth at 7.74% CAGR between 2026-2031.

- By end-user, Hospitals contributed 45.20% of 2025 revenue, with Ambulatory Surgical Centers advancing at 7.21% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Device Cleaning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hospital-acquired infections (HAIs) | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Stringent global reprocessing regulations (FDA, MDR, ISO-17664) | +1.0% | Global, led by North America & EU regulatory frameworks | Long term (≥ 4 years) |

| Growth in surgical & endoscopic procedure volumes | +0.8% | Global, with APAC showing strongest procedural growth | Medium term (2-4 years) |

| IoT-enabled washer-disinfectors for real-time compliance analytics | +0.6% | North America & Europe early adoption, APAC following | Long term (≥ 4 years) |

| Shift to enzyme-based, low-temperature detergents extending device life | +0.5% | Global, with premium markets leading adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hospital-Acquired Infections (HAIs)

HAIs add an estimated USD 25 billion-USD 45 billion to U.S. healthcare costs yearly. Although 2023 CDC data show double-digit declines in several device-associated infections, persistent bloodstream and endoscope-linked outbreaks have kept pressure on facilities to upgrade cleaning protocols. European surveillance recorded 7.1% HAI prevalence across 28 member states, equal to 4.3 million affected patients each year [2]Source: European Centre for Disease Prevention and Control, “Point Prevalence Survey of HAIs 2022-2023,” ecdc.europa.eu . Multidrug-resistant organisms such as carbapenem-resistant Klebsiella pneumoniae require extended contact times and multi-enzyme detergents that break down protective biofilms. This epidemiological environment is accelerating demand for validated chemistries and automated washer-disinfectors that deliver repeatable, trackable cycles.

Stringent Global Reprocessing Regulations (FDA, MDR, ISO 17664)

The U.S. FDA now demands full cleaning validation data for high-risk reusable devices, including bronchoscopes and laparoscopic instruments. MDR 2017/745 classifies standalone cleaning systems as medical devices and mandates Unique Device Identification to guarantee traceability across the cleaning life-cycle. ISO 17664 requires manufacturers to describe exact detergent type, temperature and contact time, pushing hospitals toward branded chemistries aligned with device instructions. Automated systems that reduce operator variability have become the preferred route to regulatory confidence, particularly in high-volume surgical centers.

Growth in Surgical & Endoscopic Procedure Volumes

Ambulatory surgical centers (ASCs) handled 3.3 million Medicare beneficiaries in 2022, a figure projected to grow another 22% over the next decade. Increased adoption of minimally invasive techniques multiplies endoscope usage; flexible endoscopes can contain more than 15 channels, each needing individual flushing and brushing. Robotic surgery adds to cleaning complexity because articulated wrist instruments must be disassembled and cleaned within two hours to avoid soil fixation, compelling investment in point-of-use enzymatic sprays and automated endoscope reprocessors. Vendors that combine chemistry, washer-disinfectors and consumable kits are gaining share among procedure-intense facilities.

IoT-Enabled Washer-Disinfectors for Real-Time Compliance Analytics

Connected washer-disinfectors transmit temperature, detergent concentration and cycle completion data to cloud dashboards, meeting 2024 Joint Commission requirements for electronic documentation. Platforms such as Diversey’s Internet of Clean use sensor analytics to flag deviations that could void a sterilization load, avoiding costly recalls. Early adopters reduced manual recordkeeping steps from 15 to 10 and halved overall processing time for robotic instruments. Predictive maintenance algorithms triggered by vibration or temperature anomalies are lowering unplanned downtime in central sterile departments, further justifying capital expenditure on connected systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & opex of automated reprocessors | -0.7% | Global, with higher impact in price-sensitive emerging markets | Medium term (2-4 years) |

| Rising adoption of disposable single-use devices | -0.5% | North America & Europe leading, with cost pressures driving adoption | Long term (≥ 4 years) |

| Supply-chain bottlenecks for specialty enzymes & surfactants | -0.4% | Global, with highest impact in regions dependent on imported chemicals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex & Opex of Automated Reprocessors

State-of-the-art washer-disinfectors cost USD 100,000-USD 300,000, while annual service contracts add 8%-12% of purchase price. Smaller hospitals and ASCs often struggle to justify this outlay, especially when staffing shortages already stretch operating budgets. Component inflation and freight surcharges have pushed supply-chain expenses close to 20% of revenue for many equipment makers, translating into higher list prices for buyers. As a workaround, vendors are rolling out subscription and leasing models that bundle chemistry, service and analytics in a per-cycle fee, but acceptance in price-sensitive markets remains limited.

Rising Adoption of Disposable Single-Use Devices

Single-use endoscopes and laparoscopic instruments eliminate reprocessing risk, shrinking the addressable base for cleaning equipment. Yet life-cycle studies show that regulated reprocessing cuts environmental impact by 43% and lowers direct device costs by nearly 50%. European policymakers are debating extended producer responsibility rules that could penalize unnecessary disposables, encouraging hospitals to maintain reusable portfolios where clinically justified. Sustainability pledges by large health systems are therefore expected to temper the long-term shift toward disposables, preserving demand for validated cleaning solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enzymatic Detergents Gain Momentum

High-Level Disinfectants captured 37.10% of the medical device cleaning market in 2025 as they deliver proven sporicidal activity for semi-critical devices. Enzymatic Detergents, however, are forecast to record a 6.63% CAGR, the fastest within the category, because multi-enzyme blends dissolve protein, lipid and carbohydrate soils lodged in intricate lumens. Chlorine-dioxide formulations are also expanding due to broad-spectrum efficacy with lower material corrosion, while non-enzymatic detergents remain the low-cost staple for routine trays. Manufacturers are introducing pH-neutral blends that maintain potency across variable water quality, improving compatibility with delicate polymer-based instruments.

The medical device cleaning market size for Enzymatic Detergents is projected to advance steadily as facilities retire legacy alkaline agents that cannot break down resilient biofilms formed by carbapenem-resistant organisms. Uptake is particularly strong in ophthalmology, orthopedics and robotic surgery suites where instrument longevity is critical. User-friendly dosing pumps and color-changing test strips ensure correct concentration, reducing technician training burden. Despite ocular-procedure concerns over toxic anterior segment syndrome, recent peer-review findings indicate that thorough rinsing mitigates risk, supporting broader adoption in outpatient surgical centers.

By Cleaning Process: Automation Drives Compliance

Automated Washer-Disinfectors led the 2025 revenues with 40.85% share, reflecting industry confidence in repeatable thermal and chemical parameters. UV/Ozone/Emerging Technologies are expected to clock 7.42% CAGR as facilities seek low-temperature methods that sidestep ethylene oxide bottlenecks. Far-UVC 222 nm ceiling fixtures now operate continuously in occupied spaces, trimming downtime between cases. Plasma and vaporized-hydrogen-peroxide units are capturing demand for heat-sensitive plastics.

The medical device cleaning market size tied to automated platforms is expanding as internet-connected units verify each load against ISO 17664-specified cycles. Conversely, manual cleaning persists in low-resource environments but shows declining share as audit failures highlight variability risks. New ductless ethylene oxide scrubbers that achieve 99% destruction efficiency are reopening sterilization lines idled by emission limits, ensuring that washer-disinfectors remain the upstream workhorse.

By Application: Endoscopes Propel Growth

Surgical Instruments generated 40.05% of 2025 revenue, reflecting their universal presence across every operating room. Endoscopes, though, are projected to grow at 6.91% CAGR because their complex multi-channel design necessitates specialized detergents and automated reprocessors. Regulatory advisories mandating tight linkages between scope models and validated cleaning parameters have driven hospitals to replace legacy manual workflows.

The medical device cleaning market share for endoscope reprocessing systems is rising fastest in large urban hospitals that run back-to-back gastroenterology lists. Innovations such as single-use protective sheaths and enzyme-based pre-clean sprays are reducing bedside turnaround time, while no-rinse detergent chemistries cut water usage by 25 liters per cycle. Surgical-instrument cleaning, meanwhile, is being refined through point-of-use gel sprays that prevent soil desiccation during transport to central sterile.

By End-User: ASCs Accelerate Demand

Hospitals retained 45.20% revenue share in 2025 thanks to their broad procedural spectrum and embedded sterile processing departments. Ambulatory Surgical Centers, however, are forecast to deliver 7.21% CAGR through 2031 as payers steer outpatient migration to curb costs. Space-constrained ASCs favor compact tabletop washers that finish cycles in under 20 minutes, ensuring instrumentation is ready for afternoon lists without overstocking trays.

As ASC networks proliferate, multi-site operators negotiate regional service contracts that bundle chemistry, preventive maintenance and remote monitoring, guaranteeing compliance without on-staff biomedical engineers. Specialty clinics and dental practices continue to adopt ultrasonic baths paired with chemistries optimized for resin-bonded burs and handpieces, creating a long-tail opportunity for niche suppliers.

Geography Analysis

The medical device cleaning market is moderately consolidated as strategic acquisitions reshape competitive dynamics. STERIS, Getinge and Ecolab remain the reference suppliers due to broad portfolios spanning chemistries, washer-disinfectors and service contracts. Medline’s USD 950 million purchase of Ecolab’s surgical solutions business in 2024 instantly broadened its consumables range and expanded access to European operating rooms. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification and filtration division in 2025 extends its reach into validated chemistries and membrane-based cleaning adjuncts.

Competition centers on automation, sensor integration and regulatory documentation. Getinge is rolling out vision-guided loading robots that cut operator touches by 30%, while Tristel leverages chlorine-dioxide chemistry registered in 38 countries to offer wipe-based high-level disinfection for niche scopes. Smaller innovators such as Sonata Scientific target emission-control niches with ductless EtO destruction units, easing pressure on sterilization capacity. Because no single customer accounts for more than 10% of STERIS revenue, demand remains fragmented and open to specialized entrants that address robotic instruments, ophthalmic scopes or plasma sterilization accessories.

Price competition is limited at the premium end, but mid-tier Asian suppliers are moving up-market with washer-disinfectors featuring basic IoT dashboards. Global service footprints, rapid part availability and operator training packages therefore differentiate incumbents. Partnerships between detergent formulators and equipment OEMs are tightening as hospitals prefer one-stop procurement that simplifies validation paperwork and warranty liability.

Competitive Landscape

The medical device cleaning market is moderately consolidated as strategic acquisitions reshape competitive dynamics. STERIS, Getinge and Ecolab remain the reference suppliers due to broad portfolios spanning chemistries, washer-disinfectors and service contracts. Medline’s USD 950 million purchase of Ecolab’s surgical solutions business in 2024 instantly broadened its consumables range and expanded access to European operating rooms. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification and filtration division in 2025 extends its reach into validated chemistries and membrane-based cleaning adjuncts.

Competition centers on automation, sensor integration and regulatory documentation. Getinge is rolling out vision-guided loading robots that cut operator touches by 30%, while Tristel leverages chlorine-dioxide chemistry registered in 38 countries to offer wipe-based high-level disinfection for niche scopes. Smaller innovators such as Sonata Scientific target emission-control niches with ductless EtO destruction units, easing pressure on sterilization capacity. Because no single customer accounts for more than 10% of STERIS revenue, demand remains fragmented and open to specialized entrants that address robotic instruments, ophthalmic scopes or plasma sterilization accessories.

Price competition is limited at the premium end, but mid-tier Asian suppliers are moving up-market with washer-disinfectors featuring basic IoT dashboards. Global service footprints, rapid part availability and operator training packages therefore differentiate incumbents. Partnerships between detergent formulators and equipment OEMs are tightening as hospitals prefer one-stop procurement that simplifies validation paperwork and warranty liability.

Medical Device Cleaning Industry Leaders

Steris PLC.

GAMA Healthcare Ltd

Ecolab Inc.

Hartmann Group

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sonata Scientific introduced the Helios MP500 stand-alone EtO emission-control system achieving 99% destruction efficiency

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s purification and filtration unit for USD 4.1 billion, adding high-purity cleaning capabilities to its healthcare portfolio

- July 2025: Ecolab launched Disinfectant 1 Wipe, the first EPA-registered 100% plastic-free hospital disinfectant wipe with 1-minute kill claims

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical device cleaning market as the revenue generated from products and equipment that remove bioburden from reusable medical devices before high-level disinfection or sterilization. The definition spans enzymatic and non-enzymatic detergents, manual and automated washer-disinfectors, ultrasonic systems, and related validation indicators that are sold to healthcare providers and reprocessing service companies worldwide; yet it excludes single-use device reprocessing and bulk chemical disinfectant supply chains.

Consumable disinfectant chemicals sold for general surface sanitation and terminal sterilization services are not included in this sizing.

Segmentation Overview

- By Product Type

- Enzymatic Detergents

- Non-enzymatic Detergents

- High-Level Disinfectants

- Lubricants & Rust Inhibitors

- Other Cleaning Chemicals

- By Cleaning Process

- Manual Cleaning

- Automated Washer–Disinfectors

- Automated Endoscope Reprocessors (AERs)

- UV / Ozone / Emerging Technologies

- By Application / Device Type

- Surgical Instruments

- Endoscopes

- Dental Instruments

- Ultrasound & Probes

- Others

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics & Dental Practices

- Diagnostic & Research Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with sterile processing managers, infection-control nurses, washer-disinfector OEM reps, and regional regulators across North America, Europe, and Asia helped us validate installed base ratios, cycle frequencies, and price dispersion that secondary sources could not capture.

Desk Research

We began with public domain datasets maintained by agencies such as the US FDA (device classification and recall notices), the CDC National Healthcare Safety Network, the European CDC, and Japan's PMDA, which quantify procedure volumes and infection-control mandates. Trade bodies, for example, the Association for the Advancement of Medical Instrumentation and the International Association of Healthcare Central Service Material Management, provided recommended practice updates that signal technology adoption. Company 10-Ks, investor decks, customs statistics, and hospital procurement portals added shipment counts and average selling prices that grounded early estimates. We also drew selectively on D&B Hoovers for company financial splits and Dow Jones Factiva for deal flow. The source list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction uses global surgical and endoscopic procedure counts, equipment reprocessing ratios, and average detergent usage to derive a demand pool, which is then balanced with sampled ASP × volume roll-ups from leading suppliers for bottom-up credibility. Key variables modeled include procedure growth, hospital bed additions, washer-disinfector replacement cycles, regulatory compliance deadlines, detergent concentration shifts, and exchange-rate movements. Multivariate regression aligns historical market value with these drivers and projects the 2025-2030 outlook, while scenario analysis stress-tests high and low HAI incidence paths.

Data Validation & Update Cycle

Outputs pass three rounds of analyst review, anomaly checks against independent indicators, and expert callbacks. The model refreshes annually, with interim updates triggered by material recalls, large mergers, or new reprocessing guidelines.

Building Confidence in Our Medical Device Cleaning Baseline

Published values often diverge because firms select different product baskets, price bases, and refresh cadences.

According to Mordor Intelligence, our disciplined scope and yearly recalibration keep figures decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.48 B (2025) | Mordor Intelligence | - |

| USD 2.3 B (2022) | Global Consultancy A | Uses hospital detergents only, no equipment revenue, five-year refresh cycle |

| USD 23.4 B (2023) | Trade Journal B | Bundles surface disinfection chemicals and sterilizers; applies list prices without regional ASP calibration |

These comparisons show that Mordor's carefully bounded scope and variable-level cross-checks yield a balanced, transparent baseline that stakeholders can replicate and trust.

Key Questions Answered in the Report

What is the current value of the medical device cleaning market?

The market stands at USD 2.61 billion in 2026 and is projected to reach USD 3.36 billion by 2031 at a 5.18% CAGR.

Which product category leads revenue?

High-Level Disinfectants hold 37.10% of 2025 revenue, reflecting their broad sporicidal efficacy.

Why are enzymatic detergents growing so quickly?

Multi-enzyme blends effectively dissolve biofilms in complex lumens, driving a 6.63% CAGR through 2031.

Which region shows the strongest growth?

Asia-Pacific is forecast to expand at 7.74% CAGR on the back of expanding procedure volumes and regulatory upgrades.

How do IoT-enabled washer-disinfectors benefit hospitals?

They offer real-time monitoring, automated documentation and predictive maintenance that streamline compliance and reduce downtime.

Page last updated on: