Endoscope Washer Disinfector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

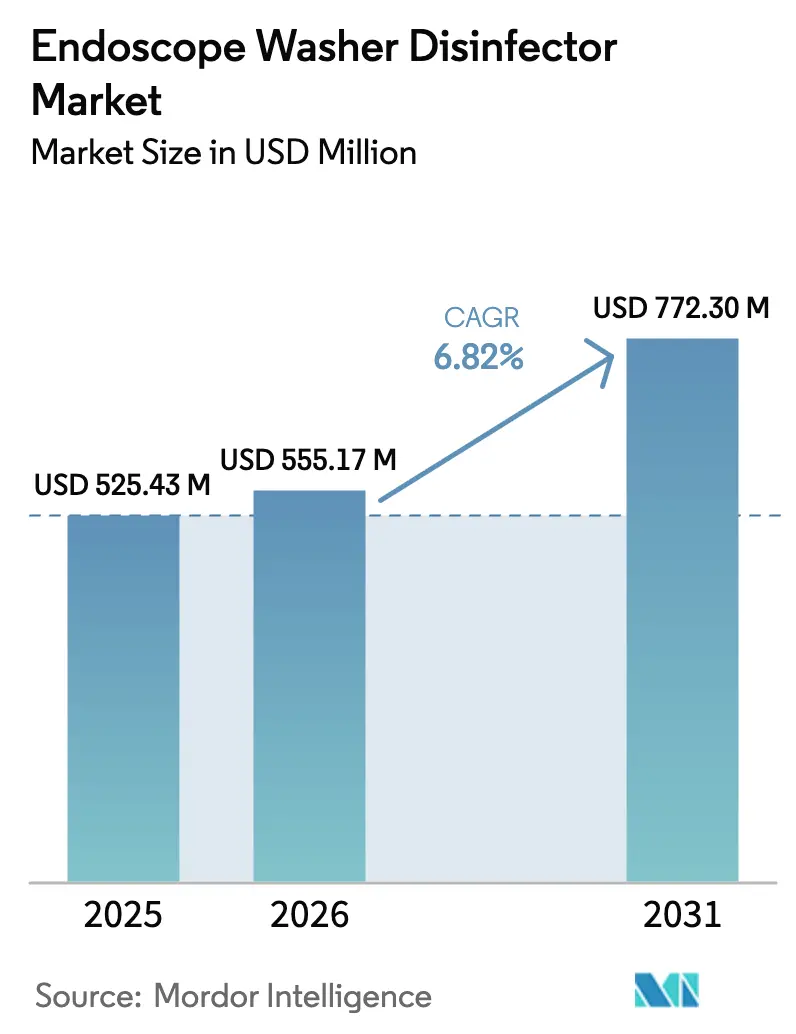

| Market Size (2026) | USD 555.17 Million |

| Market Size (2031) | USD 772.30 Million |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

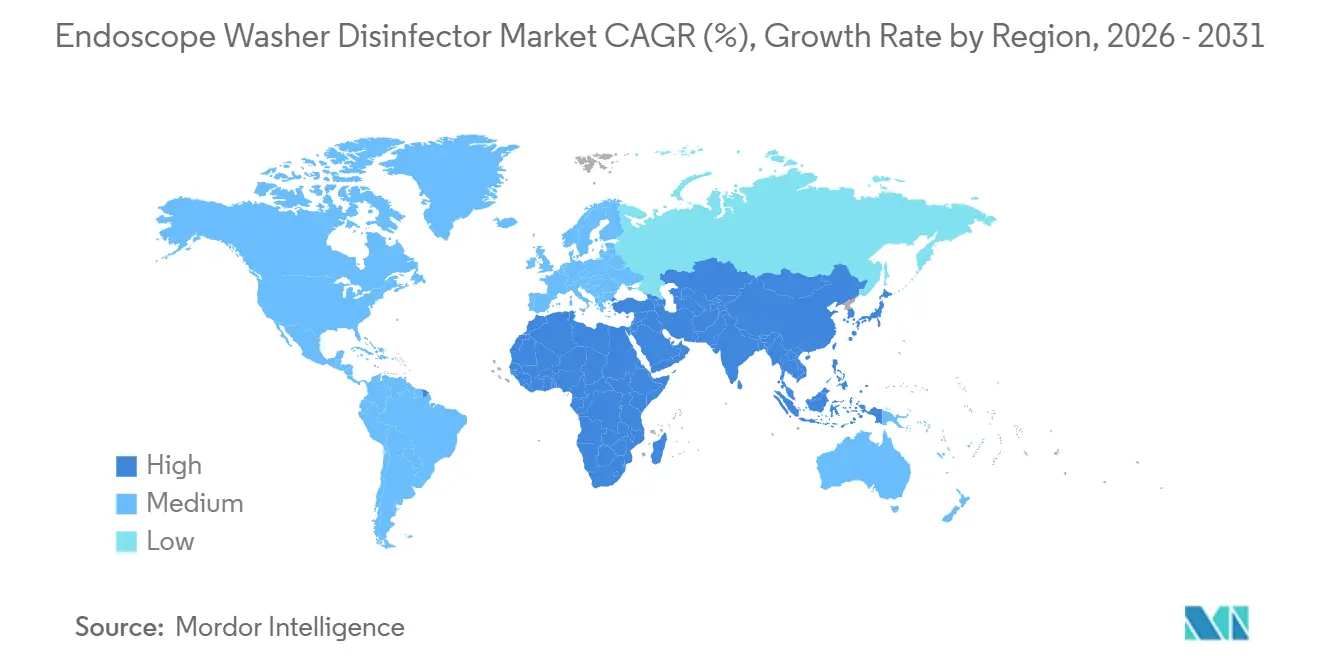

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoscope Washer Disinfector Market Analysis by Mordor Intelligence

The Endoscope Washer Disinfector Market size was valued at USD 525.43 million in 2025 and is estimated to grow from USD 555.17 million in 2026 to reach USD 772.30 million by 2031, at a CAGR of 6.82% during the forecast period (2026-2031).

Aging reprocessing infrastructure left behind when hospitals deferred capital spending between 2020 and 2023 is now being replaced amid tougher infection-control rules and a return to full procedural volumes.[1]American Hospital Association, “2024 Costs of Caring: Hospital Financial Pressures,” AHA, aha.org Automated washer-disinfectors already command 69.35% of revenue, yet multi-chamber designs are set to grow fastest at 9.38% as ambulatory surgery centers (ASCs) adopt high-throughput layouts for mixed endoscope inventories. Flexible-scope demand, driven by gastroenterology and pulmonology, represented 59.77% of compatibility-based sales in 2025 and will continue to outpace rigid scopes as screening guidelines widen and minimally invasive therapies expand. While hospitals maintained a 62.44% share in 2025, ASC purchases are rising 8.89% annually after 357 complex endoscopic procedures won outpatient reimbursement status in 2025.[2]Centers for Medicare & Medicaid Services, “CY 2025 Medicare Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment System Final Rule,” CMS, cms.gov Geographically, North America contributed 34.77% of 2025 revenue, yet Asia-Pacific leads growth at 9.01% as India alone funds 34,000 new acute-care beds by 2029.

Key Report Takeaways

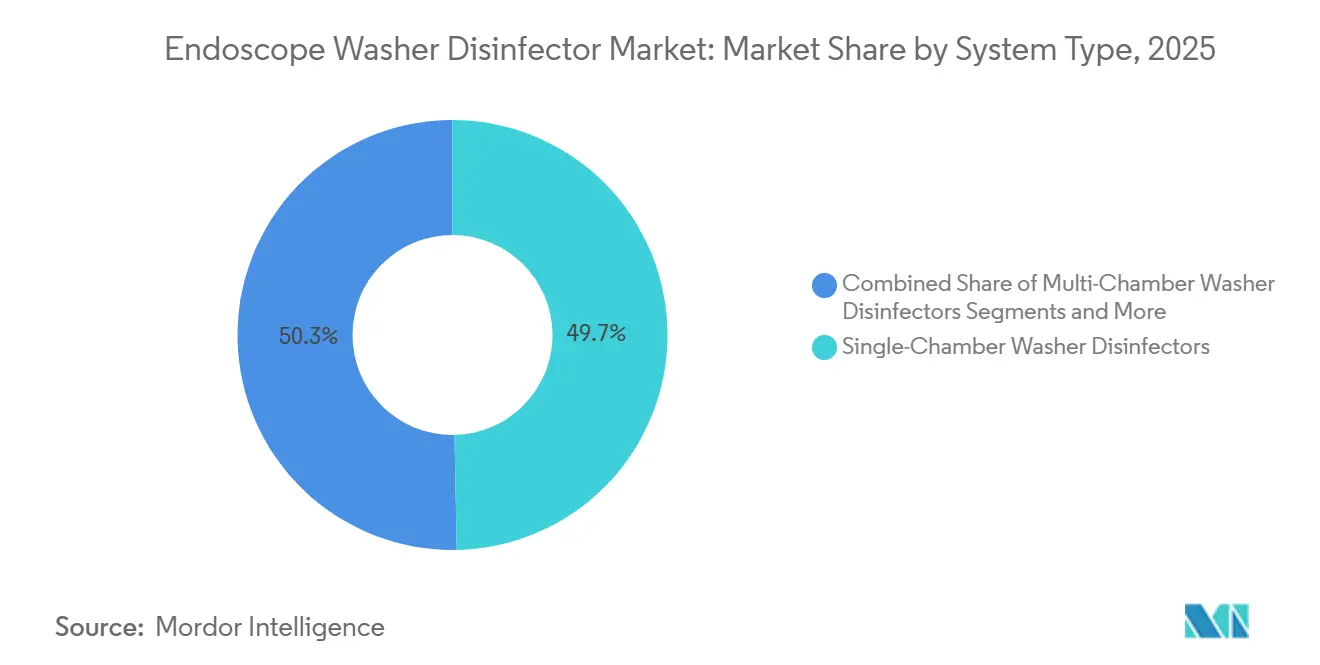

- By system type, single-chamber units led with 49.68% revenue share in 2025, while multi-chamber units are projected to rise at a 9.38% CAGR through 2031.

- By modality, automated washer-disinfectors captured 69.35% of 2025 revenue and are advancing at a 10.57% CAGR to 2031.

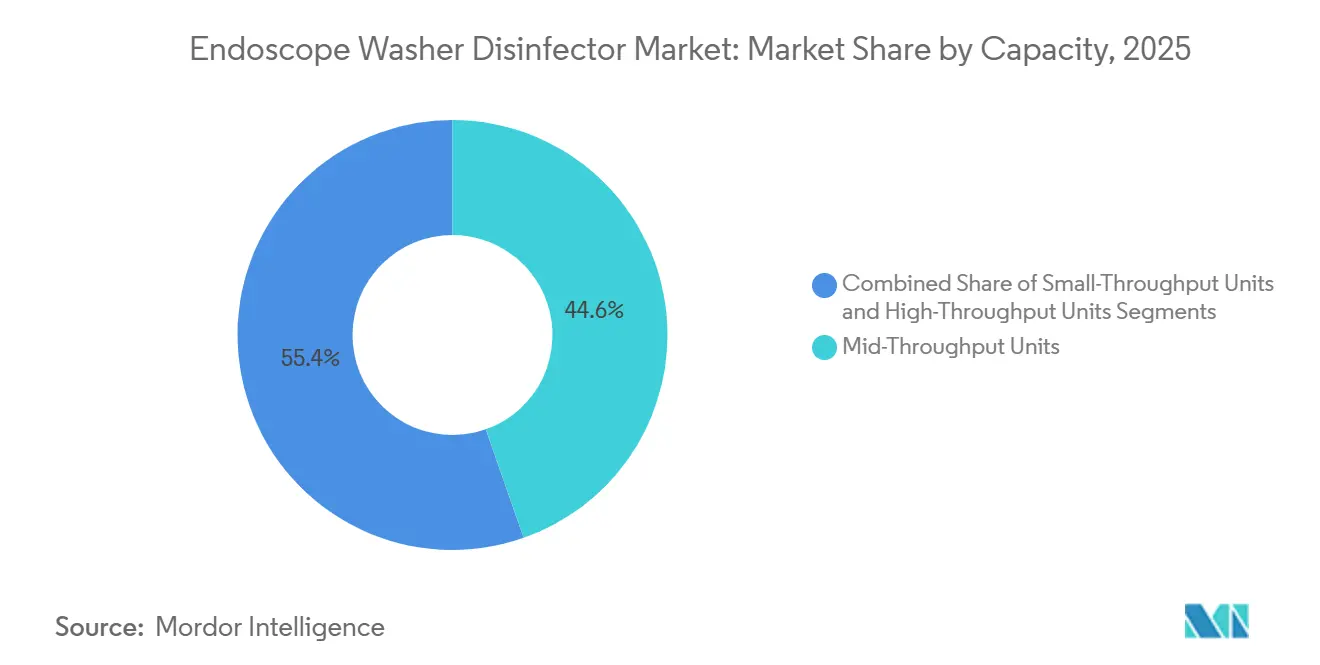

- By capacity, mid-throughput systems accounted for 44.62% of 2025 sales; high-throughput models record the fastest growth at a 9.32% CAGR.

- By endoscope compatibility, flexible scopes delivered 59.77% of 2025 revenue, whereas single-use and hybrid modules show an 8.46% CAGR outlook.

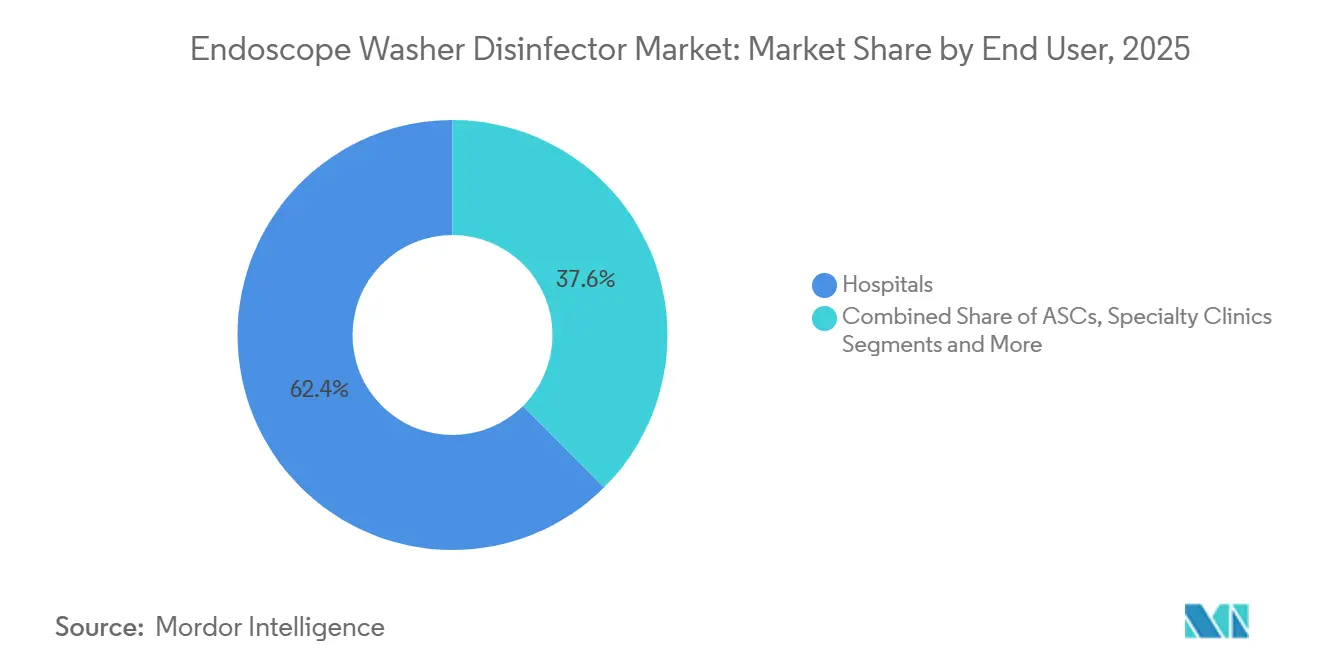

- By end-user, hospitals held 62.44% share in 2025, while ambulatory surgery centers are expanding at an 8.89% CAGR through 2031.

- By geography, North America generated 34.77% of 2025 revenue, yet Asia-Pacific leads growth with a 9.01% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endoscope Washer Disinfector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Number of Endoscopic Procedures | +1.5% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Stricter Infection-Control & Reprocessing Regulations | +1.3% | North America, Europe | Short term (≤2 years) |

| Rapid Adoption of Automated Washer-Disinfectors | +1.2% | North America, Europe, tier-1 APAC cities | Medium term (2-4 years) |

| Expansion of Ambulatory Surgery Centers | +0.9% | North America, Europe, metro APAC | Long term (≥4 years) |

| IoT-Enabled Traceability & Audit Compliance | +0.8% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Tariff-Driven Localization in the Americas | +0.6% | United States, Mexico, Canada | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Number of Endoscopic Procedures

Global procedure counts are climbing as colorectal screening begins at age 45 and bariatric therapies shift to endoluminal techniques. The lower screening age added about 19 million eligible U.S. adults by 2025 and created 3–4 million extra colonoscopies each year. Japan recorded an 8% year-on-year jump in upper-GI endoscopies in 2024 thanks to Helicobacter pylori eradication efforts. Each additional case squeezes reprocessing turnaround times; older single-chamber units that cannot meet a 24-minute median cycle are being replaced . India’s Apollo Hospitals added 3,512 beds in fiscal 2025, allocating 12–15% of procedural capacity to endoscopy suites, which links bed growth directly to washer-disinfector demand.

Stricter Infection-Control & Reprocessing Regulations

Outbreaks tied to contaminated duodenoscopes spurred new oversight. In August 2024, the U.S. FDA ordered microbiological cultures on 5% of high-risk scopes each month, plus electronic logs for traceability. The NHS rolled out its NETB 2.0 framework in 2025, making IDSc-aligned training mandatory for all decontamination staff.[3]NHS England, “National Endoscopy Training and Benchmarking Framework Version 2.0,” NHS England, england.nhs.ukTaiwan’s ST91:2021 rule added USD 52–68 per cycle in consumables and extended reprocessing by 24 minutes, driving multi-chamber adoption to overlap stages. An ISO 15883 update slated for 2027 will mandate real-time sensor logging, rendering pre-2020 models obsolete.

Rapid Adoption of Automated Washer-Disinfectors

Automation reduces operator variation and plugs labor shortages. A 2024 Cleveland Clinic survey showed 40% of technicians find manual instructions impractical, pushing facilities toward programmable washer-disinfectors. Automated units dispense detergents precisely, ramp temperatures, and archive every parameter for audits. Getinge recorded a 6.2% organic rise in infection-control orders in the Americas during Q3 2024 as hospitals prioritized compliance investments. With sterile-processing vacancies running 15–20%, automation acts as a workforce multiplier.

Expansion of Ambulatory Surgery Centers

The CMS decision to reimburse 357 additional endoscopic procedures in ASCs opened a new equipment cycle. Typical ASCs run 8–15 scopes daily across two to four rooms, favoring mid-capacity washer-disinfectors priced USD 40,000–70,000. The NHS earmarked GBP 4.1 billion for Integrated Care Boards in 2024–2025 to reach 3.5 endoscopy rooms per 100,000 population, an expansion that needs 180–200 new suites and compact reprocessors. Ireland’s HSE reserved EUR 86.25 million for equipment upgrades in 2025, further lifting demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operating Costs | −0.7% | Emerging markets, rural hospitals | Short term (≤2 years) |

| Complex Protocols & Training Burden | −0.5% | Global, especially high-turnover regions | Medium term (2-4 years) |

| Rising Use of Single-Use Endoscopes | −0.4% | North America, Western Europe, Japan | Long term (≥4 years) |

| Water-Scarcity & Eco-Compliance Pressures | −0.3% | California, Middle East, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Costs

Multi-chamber systems cost USD 80,000–150,000 up-front, while annual consumables and maintenance add USD 15,000–25,000. Taiwan’s ST91:2021 standard tacks on mandatory borescopes and drying cabinets, inflating suite costs by USD 16,000–20,000. In India a complete endoscopy suite can reach USD 200,000–300,000, stretching procurement cycles to 18 months despite hospital expansion.

Complex Protocols & Training Burden

Reprocessing involves up to 20 steps, each with precise chemical concentrations and dwell times. Forty percent of staff rate current instructions as unworkable under real-world conditions. The NHS requires IDSc-certified technicians, adding six to twelve months of coursework. Training a single technician costs USD 5,000 annually, creating a recurring expense small facilities struggle to absorb

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Multi-Chamber Platforms Rise in High-Volume Centers

Single-chamber units owned 49.68% of 2025 sales, yet multi-chamber configurations are growing at 9.38% as facilities plan parallel workflows that shrink scope-turnover times. ASC throughput of 8–12 scopes per shift is pushing mid-priced dual-chamber models, whereas community hospitals still favor the capital-light single-chamber alternative. STERIS’ 2024 acquisition of Integrated Medical Systems added compact reprocessors that fit decentralized care footprints. The endoscope washer disinfector market size for multi-chamber units is projected to climb from USD x million in 2026 to USD y million in 2031 at the stated CAGR.

Portable and benchtop units are carving out niches in mobile OR vans and rural clinics where budgets cap at USD 50,000 and space is scarce. Taiwan’s integration of borescope checks and drying cabinets in ST91:2021 favors all-in-one multi-chamber solutions, further eroding single-chamber dominance in regulated markets. NHS funding to reach 3.5 procedure rooms per 100,000 people fuels demand for scalable, modular systems.

By Modality: Automation Becomes the Norm

Automated models captured 69.35% of 2025 revenue and will add another 10.57% annually through 2031, propelled by labor shortages and mandatory electronic logs. Semi-automated formats remain interim options for facilities upgrading from manual processes. Manual washers survive mainly in low-resource settings but face obsolescence as ISO 15883 adds real-time data logging. The endoscope washer disinfector market share for automated solutions could surpass 75% by 2028 as compliance deadlines approach.

Getinge’s Q3 2024 report flagged infection-control gear as its fastest-growing U.S. line item, mirroring broader hospital priorities. With staff deficits at 15–20%, machines that cut technician steps are no longer optional

By Capacity: High-Throughput Systems Supply Academic Medical Centers

High-throughput units that handle 20–30 scopes per shift are expanding 9.32% yearly, serving tertiary hospitals where multiple endoscopy rooms operate in parallel. Apollo Hospitals’ expansion obliges large-capacity washer-disinfectors to prevent procedure delays. Ireland’s capital budget mirrors this need at Cork, St. James’s, and Galway hospitals. Mid-throughput formats dominate community settings with ≤15 daily scopes and offer the best return at USD 50,000–80,000 upfront. Small systems support single-specialty clinics yet may be consolidated at regional hubs once full ST91:2021 compliance costs are tallied

By Endoscope Compatibility: Flexible Scopes Remain the Workhorse

Flexible scopes drove 59.77% of 2025 demand thanks to rising GI and pulmonary case volumes. U.S. screening changes alone added 3–4 million colonoscopies a year. Japan’s H. pylori initiative swelled upper-GI procedures by 8% in 2024. Complex channel geometry keeps washer-disinfectors indispensable despite the rise of disposable scopes. Rigid scopes can often be cycled through general instrument washers, lowering their share.

Single-use modules are gaining traction in high-risk cases and carry an 8.46% CAGR outlook. Hybrid reprocessors that accommodate both disposable and reusable inventories are emerging as a hedge against rapid shifts in scope mix

By End-User: Hospitals Still Dominate, ASCs Accelerate

Hospitals generated 62.44% of revenue in 2025 owing to 24-hour emergency capability and complex case loads. Even with shrinking cash reserves—days cash on hand fell 28.3% between 2019 and 2024—facilities cannot postpone washer upgrades once units fail microbiological tests. ASCs, however, are the fastest-growing buyers at 8.89% CAGR after CMS expanded payable procedures. Footprint-constrained specialty clinics may outsource reprocessing where ST91-type rules make in-house compliance uneconomical.

Geography Analysis

North America accounted for 34.77% of 2025 sales, supported by high screening volumes, FDA surveillance culture mandates, and tariff incentives that favor domestic assembly. Hospitals accelerated orders by 6.7% in April 2025 to beat future tariff risks. Europe benefits from universal coverage and ISO-based rules; the NHS allocated GBP 4.1 billion to lift endoscopy capacity, and HSE Ireland set aside EUR 86.25 million for equipment renewals. Belimed posted 7.3% organic hospital-segment growth in Q3 2024, underscoring regional momentum.

Asia-Pacific is the growth engine at 9.01% CAGR. India’s 34,000-bed expansion and Japan’s intensified GI screening underpin strong demand. Domestic suppliers like Shinva compete on price yet face quality-perception hurdles in premium hospitals. Australia and South Korea are early adopters of IoT traceability, riding Olympus’ Hytrack launch.

The Middle East and Africa show uneven uptake. GCC nations fund medical mega-projects but must reconcile high-water consumption with looming conservation laws. South America’s growth centers on Brazil, where ANVISA harmonized reprocessing rules with ISO 15883 in 2024, pushing hospitals toward automated systems.

Competitive Landscape

The market is moderately concentrated. STERIS’ USD 275 million acquisition of Integrated Medical Systems in December 2024 folds drying cabinets and storage into a seamless chain-of-custody suite. Getinge’s Life Science division logged robust 6.2% organic growth in Q3 2024 on infection-control demand. Olympus differentiates via RFID-enabled Hytrack, essential as regulators demand electronic audit trails. Meanwhile, benchtop specialists court outpatient clinics locked out by large vendors’ price points. Data-aggregating software such as Nanosonics’ AuditPro and Censis’ ScopetraC is emerging as a competitive lever, because FDA’s 2024 guidance effectively makes digital traceability mandatory. Disposables from Boston Scientific and Ambu represent the long-term disruptive threat, though cost keeps penetration in single digits today

Endoscope Washer Disinfector Industry Leaders

Belimed AG

Getinge AB

Steelco S.p.A.

STERIS plc

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Steelco unveiled Steri Case, a closed system for washing and sterilizing endoscopes that maintains continuous leak testing to support just-in-time turnaround in units with limited instrument inventories.

- September 2025: Serchem acquired Serve Medical, combining chemical manufacturing expertise with validation and servicing capabilities for hospital decontamination units.

Global Endoscope Washer Disinfector Market Report Scope

An endoscope washer-disinfector is an automated device that cleans, disinfects, and dries flexible endoscopes to ensure high-level decontamination and prevent cross-contamination.

The Endoscope Washer Disinfector Market Report is segmented by System Type, Modality, Capacity, Endoscope Compatibility, End User, and Geography. By System Type, the market is segmented into Single-Chamber, Multi-Chamber, and Portable/Benchtop Units. By Modality, the market is segmented into Automated, Semi-Automated, and Manual. By Capacity, the market is segmented into Small, Mid, and High-Throughput Units. By Endoscope Compatibility, the market is segmented into Flexible, Rigid, and Single-Use/Hybrid Modules. By End User, the market is segmented into Hospitals, ASCs, Specialty Clinics, Labs, and Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Single-Chamber Washer Disinfectors |

| Multi-Chamber Washer Disinfectors |

| Portable/Benchtop Units |

| Automated Washer Disinfectors |

| Semi-Automated Systems |

| Manual Washer Disinfectors |

| Small-Throughput Units |

| Mid-Throughput Units |

| High-Throughput / Large-Capacity Units |

| Flexible Endoscopes |

| Rigid Endoscopes |

| Single-Use / Hybrid Handling Modules |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Laboratories & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By System Type | Single-Chamber Washer Disinfectors | |

| Multi-Chamber Washer Disinfectors | ||

| Portable/Benchtop Units | ||

| By Modality | Automated Washer Disinfectors | |

| Semi-Automated Systems | ||

| Manual Washer Disinfectors | ||

| By Capacity | Small-Throughput Units | |

| Mid-Throughput Units | ||

| High-Throughput / Large-Capacity Units | ||

| By Endoscope Compatibility | Flexible Endoscopes | |

| Rigid Endoscopes | ||

| Single-Use / Hybrid Handling Modules | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Laboratories & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the endoscope washer disinfector market in 2031?

The market is expected to reach USD 772.30 million by 2031, growing at a 6.82% CAGR.

Which segment will grow the fastest through 2031?

Multi-chamber washer-disinfectors lead growth at a 9.38% CAGR as high-throughput sites seek parallel processing.

How are single-use endoscopes affecting reprocessor demand?

Disposables handle fewer than 5% of cases today, but could trim washer-disinfector utilization if payer pilots lift penetration toward 20% by 2031.

Why are ASCs investing in new washer-disinfectors?

CMS approved 357 additional outpatient endoscopic procedures in 2025, driving ASC demand for mid-capacity automated units.

Which regions show the highest growth potential?

Asia-Pacific leads with a 9.01% CAGR, fueled by large-scale hospital expansions in India and rising screening volumes in Japan.

What role does IoT play in modern reprocessing?

RFID and cloud dashboards automate traceability, now essential for complying with FDA and ISO audit requirements and for quickly flagging non-compliant cycles.

Page last updated on: