Antiseptics And Disinfectants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

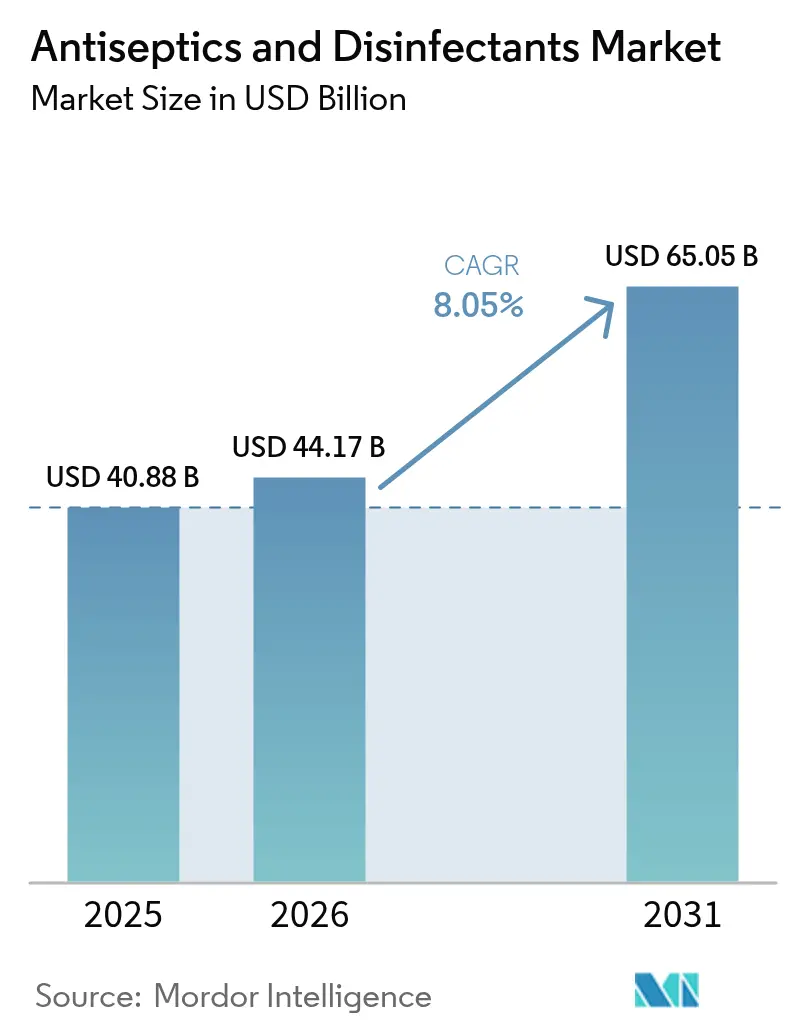

| Market Size (2026) | USD 44.17 Billion |

| Market Size (2031) | USD 65.05 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

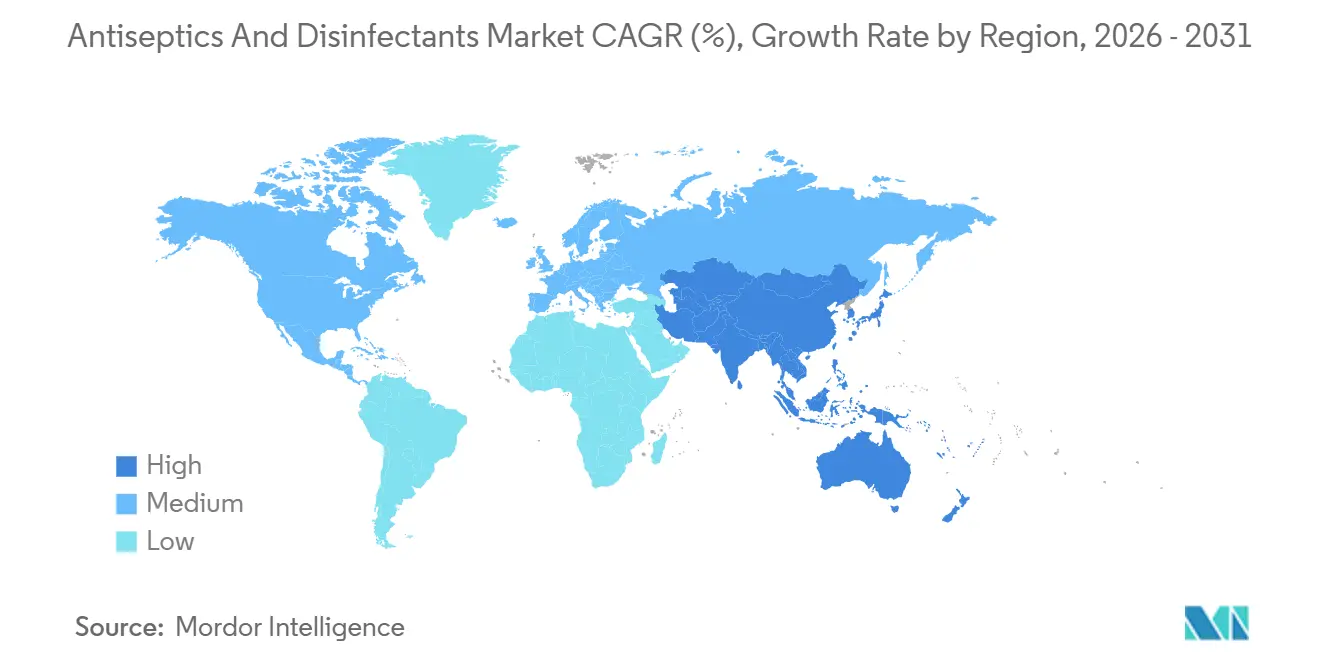

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antiseptics And Disinfectants Market Analysis by Mordor Intelligence

The Antiseptics And Disinfectants Market size is expected to increase from USD 40.88 billion in 2025 to USD 44.17 billion in 2026 and reach USD 65.05 billion by 2031, growing at a CAGR of 8.05% over 2026-2031.

Growth in the Asia-Pacific region is being driven by a steady increase in surgical volumes, adherence to post-pandemic hygiene protocols, and the rapid expansion of acute-care infrastructure. Outpatient migration is influencing purchasing decisions, with ambulatory centers prioritizing rapid-turnaround wipes and enzymatic cleaners to achieve same-day discharge goals. Stricter regulatory oversight, including new residue testing methods for quaternary ammonium compounds, is pushing procurement teams to select validated brands that can manage compliance costs effectively. The competitive landscape is evolving, with vendors focusing on integrated service contracts that combine dispensing hardware, chemical refills, and digital compliance dashboards, ensuring multi-year account retention.

Key Report Takeaways

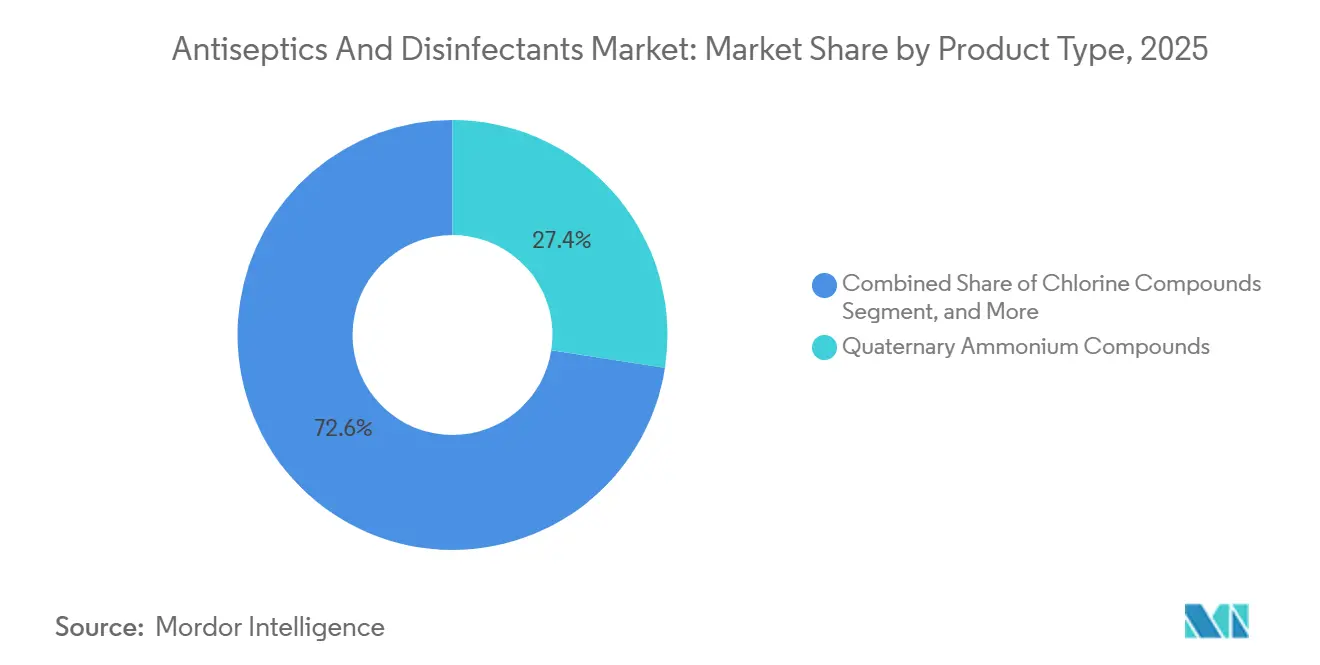

- By product type, quaternary ammonium compounds captured 27.43% of the Antiseptics and Disinfectants market share in 2025.

- By formulation, liquids accounted for 51.25% of the Antiseptics and Disinfectants market size in 2025, while wipes are expanding at a 10.78% CAGR through 2031.

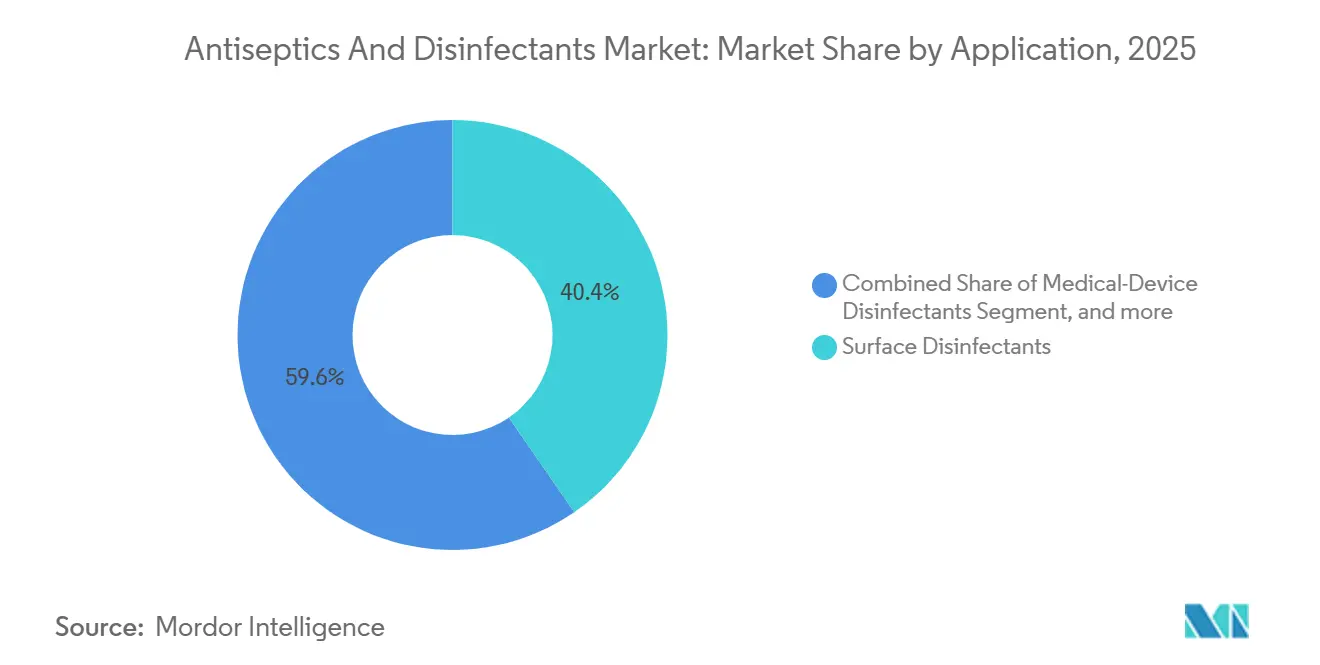

- By application, surface disinfectants led with a 40.43% revenue share of the Antiseptics and Disinfectants market in 2025; enzymatic cleaners are projected to grow at a 11.55% CAGR through 2031.

- By end user, hospitals and clinics accounted for 60.23% of 2025 revenue, but ambulatory centers are growing fastest at a 11.43% CAGR.

- By geography, North America accounted for 42.32% of 2025 revenue, while Asia-Pacific is forecast to lead growth with a 9.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antiseptics And Disinfectants Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating burden of healthcare-associated infections | +1.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Post-pandemic institutional hygiene protocols | +1.5% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Rising surgical procedure volumes and complex device reprocessing | +1.3% | Global, fastest uptake in Asia-Pacific | Medium term (2-4 years) |

| Rapid expansion of hospitals and ambulatory infrastructure | +1.2% | Asia-Pacific core, spill-over to Middle East & Africa | Long term (≥ 4 years) |

| Stringent occupational-safety regulations | +0.9% | North America and Europe | Medium term (2-4 years) |

| Growing consumer shift toward preventive self-care antiseptics | +0.7% | Global, led by urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Burden of Healthcare-Associated Infections Worldwide

Healthcare-associated infections (HAIs) affect 1 in 31 inpatients on any given day, adding millions of preventable cases each year. Declines in central-line and catheter infections between 2023 and 2024 have been offset by rising abdominal-hysterectomy site infections, exposing gaps in protocol adherence. Cost studies show that a single central-line bloodstream infection can cost up to USD 99,900 in care, compared with USD 8,500 for uninfected patients, pressing hospitals to adopt advanced surface and device disinfectants[1]. Reimbursement penalties under the U.S. Hospital-Acquired Condition Reduction Program amplify this financial urgency. A divergence between acute-care and long-term-care settings creates white-space for turnkey disinfection-as-a-service offerings that blend training, dosing hardware, and compliance analytics.

Post-Pandemic Institutional Hygiene Protocols Becoming Permanent

COVID-19 elevated cleaning frequencies that have now crystallized into formal operating procedures across healthcare and commercial real estate. Canada’s Biocides Regulations, effective May 2025, codify higher efficacy and safety standards that mirror the pandemic era[2]Health Canada, “Biocides Regulations Guidance 2025,” canada.ca. EPA approval of Reckitt’s Lysol Air Sanitizer—the first agent cleared for airborne pathogen claims—illustrates how regulatory novelty opens adjacent categories and drives brand premium. Landlords increasingly include disinfection cadence in lease covenants, shifting spend from ad hoc janitorial supplies to multi-year service contracts. Ecolab’s Institutional segment logged 6% organic growth in Q4 2024 by selling IoT-linked dispensers that auto-reorder refills, turning hygiene compliance into a managed service.

Rising Surgical Procedure Volumes and Complex Device Reprocessing

Roughly 310 million operations are performed each year; 70% of U.S. procedures now occur in outpatient settings. As total joint replacements in ambulatory centers surpass 50% by 2026, the speed of turnover is paramount. Enzymatic cleaners that dissolve biofilm within 10 minutes are replacing overnight soaks and support higher case throughput. FDA guidance notes that reprocessed single-use devices saved USD 465 million in 2023, pushing health systems toward validated disinfectants that safeguard device warranties. STERIS’s consumables revenue climbed 9.1% year-on-year to USD 452 million in Q2 FY2026, reflecting demand for bundled sterilant and detergent contracts.

Rapid Expansion of Hospitals and Ambulatory Care Infrastructure

China added 130,000 hospital beds in 2024, raising capacity to 7.67 million beds and occupancy to 81.4%. India aims to lift bed strength from 1.3 million in 2023 to 1.9 million by 2027 under Ayushman Bharat and PM-ABHIM programs. Each new bed consumes an estimated 12-15 liters of disinfectant per year, translating into an incremental demand of up to 9 million liters annually in India alone. Japan’s 8,200 hospitals are retrofitting automated hydrogen peroxide and UV-C systems to meet revised infection control guidelines issued in 2024. Private-chain dominance in India—74% of beds—favors multinational suppliers with ISO 13485 certificates and digital stock dashboards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-region chemical registration requirements | -0.8% | Global, acute in Europe and North America | Medium term (2-4 years) |

| Material compatibility limits with advanced devices | -0.6% | Global, concentrated in robotic-surgery facilities | Short term (≤ 2 years) |

| Volatility in key raw-material prices | -0.7% | Global, intense in import-dependent regions | Short term (≤ 2 years) |

| Emergence of disinfectant-resistant microorganisms | -0.5% | Global, most visible in high-acuity hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Chemical Registration Requirements

The European Chemicals Agency’s review of ethanol, opened in 2024, is likely to extend into 2026, freezing product launches across 27 member states[3]. The U.S. EPA’s June 2024 residue test methods add USD 50,000-100,000 in validation costs per SKU. California’s Department of Toxic Substances Control may list quaternary ammonium compounds as a Priority Product, forcing safer-alternative analyses that ripple through 400 hospitals. Canada’s three-tier Biocides Regulations can require up to 24 months of review for novel actives, lengthening time-to-market. Small manufacturers lack the regulatory staff to navigate simultaneous dossiers, ceding share to multinationals that amortize compliance across global portfolios.

Material Compatibility Limitations with Advanced Medical Devices

Hydrogen peroxide vapor and peracetic acid mandated by EU cleanroom rules can corrode stainless-steel ports and cloud polycarbonate lenses. Robotic-surgery suppliers stipulate non-aldehyde, pH-neutral enzymatic cleaners to maintain warranty coverage. A single damaged endoscope can cost up to USD 30,000 to replace and must be reported as a device malfunction under FDA rules, making ASCs risk-averse to switching chemistries. STERIS bought Becton Dickinson’s sterilization assets for USD 539.8 million to pair capital equipment with validated low-residue detergents, ensuring compatibility and recurring revenue. Facilities now stock multiple disinfectant classes and run staff training programs that add labor overhead, tempering aggressive product substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enzymatic Cleaners Gain Ground Despite QAC Dominance

Quaternary ammonium compounds accounted for 27.43% of 2025 revenue in the Antiseptics and Disinfectants market, benefiting from a broad spectrum of microbicidal activity and low per-dose cost. Yet enzymatic cleaners are growing at 10.43% CAGR through 2031, fueled by the need to break down biofilms on complex arthroscopic shavers and robotic instruments without corrosion. The Antiseptics and Disinfectants market size for enzymatic formulations is projected to expand from USD 6.1 billion in 2026 to USD 11.1 billion by 2031. Hospitals adopting ISO 14644 rotation protocols now cycle enzymatic, oxidizing, and quaternary products each quarter to blunt microbial adaptation. Pharmaceutical cleanrooms, where residue tolerance is minimal, contributed double-digit gains to Ecolab’s Life Sciences sales in 2024.

Chlorine compounds remain staples for water-system disinfection, while aldehydes and phenolics retreat under regulatory scrutiny from California’s DTSC. Alcohols dominate hand antisepsis but face input cost swings as isopropyl prices hover between USD 1,300-1,600 per ton into 2025. Povidone-iodine intranasal swabs that deliver 99.7% microbial reduction in 10 minutes illustrate how niche delivery systems can command premium pricing. The Antiseptics and Disinfectants market continues to reward suppliers that certify material compatibility with robotic-surgery metals and polymers, reducing risk for operating-room managers.

By Formulation: Wipes Surge on Point-of-Care Convenience

Bulk liquids delivered 51.25% of formulation revenue in 2025, driven by floor-cleaning and instrument-soak applications in the Antiseptics and Disinfectants market. Wipes, however, are growing at a 10.78% CAGR, as outpatient centers prefer single-use formats that eliminate dilution errors. Sani-Cloth leads the U.S. clinical wipe segment with a fabric that retains quaternary actives throughout the full contact time, a feature validated by the EPA. Each pre-saturated canister commands 30-40% higher gross margin than an equivalent liter of concentrate, giving manufacturers a profit motive to push conversion.

Sprays and aerosols, such as Lysol Air Sanitizer, validate new delivery vectors for antimicrobials after securing EPA approval for airborne claims. Gels and foams, especially 70% alcohol formulations that meet WHO standards, gain traction for surgical-scrub applications where drip control matters. Because wipes ship disinfectant, applicator, and dose in a single SKU, procurement officers can simplify inventory management, thereby furthering adoption. The Antiseptics and Disinfectants market benefits from wipes, which shorten turnover times in crowded ASC schedules.

By Application: Enzymatic Cleaners Lead Growth Amid Surface Disinfectant Maturity

Surface disinfectants still dominate, accounting for 40.43% of 2025 application revenue in the Antiseptics and Disinfectants market. Yet enzymatic cleaners are forecast to post an 11.55% CAGR to 2031, reflecting mandatory pre-cleaning for semi-critical devices under Spaulding classification. STERIS logged consumables growth of 9.1% to USD 452 million in Q2 FY2026 as hospitals bundle detergents with capital sterilizers. Automated washer-disinfectors that dose enzymatic solutions reduce labor costs by up to 25% and extend instrument life by minimizing abrasive brushes.

Medical-device disinfectants remain indispensable for endoscope and dialysis-machine circuits, relying on ortho-phthalaldehyde or peracetic acid with high-level kill claims. Skin and wound antiseptics ride the uptrend in surgical volume, lowering infection odds by up to 50% when paired with antibiotic prophylaxis. Future demand will hinge on balancing sporicidal potency with polymer compatibility as hospitals adopt more heat-sensitive equipment.

By End User: Ambulatory Centers Outpace Hospitals on Surgical Migration

Hospitals and clinics accounted for 60.23% of 2025 revenue in the Antiseptics and Disinfectants market, supported by centralized infection-prevention units and group purchasing power. Ambulatory surgery centers are advancing at 11.43% CAGR, driven by payers steering elective procedures to lower-cost sites. These centers favor wipes with two-minute kill times and enzymatic detergents that free instruments in under 10 minutes, allowing room staff to double procedure counts per day.

Long-term care facilities face chronic staffing gaps; ready-to-use, no-rinse formulations reduce training loads and error risk. Pharmaceutical and biotech plants represent a smaller end-user slice yet demand the most rigorous validation, including three-log reductions and residue-free finishes mandated by FDA 21 CFR 211 and EU GMP Annex 1. Ecolab’s Life Sciences division grew at double digits in 2024, thanks to single-use bioreactor adoption that requires connector sanitization between batches.

Geography Analysis

North America, with 42.32% of 2025 revenue, remains the largest Antiseptics and Disinfectants market owing to strict Medicare penalties for hospital-acquired conditions and mature infection-control staffing models. The region’s mature infrastructure favors premium service bundles that reduce nursing workload and electronically document compliance. Raw-material pricing pressure, notably volatility in isopropyl alcohol, continues to squeeze formularies and elevate the appeal of concentrated wipes that reduce shipment weight.

Asia-Pacific is projected to lead growth at 9.43% CAGR through 2031, underpinned by China’s 130,000 new beds added in 2024 and India’s planned 600,000 beds by 2027. High bed-occupancy rates are driving the construction of new isolation wards, each fitted with automated disinfectant dosing systems. Multinationals with ISO 13485 certification and cloud-based stock controls win tenders from private hospital chains dominating India’s market.

Europe’s performance is tempered by the complexity of biocide regulation. The ethanol review under EU BPR, opened in 2024, has paused product launches but will ultimately harmonize efficacy criteria across 27 member states. The Middle East and Africa enjoy a steady pipeline of specialty hospitals aimed at medical tourists, spurring demand for EPA-registered and CE-marked disinfectants. South America sees slower unit growth; Brazil’s Unified Health System procures through centralized tenders that emphasize the lowest bid, encouraging local toll blending.

Competitive Landscape

Market concentration is moderate; the five leading vendors—Ecolab, STERIS, Reckitt, Diversey, and Solventum—collectively hold about 35-40% of global revenue in the Antiseptics and Disinfectants market. Strategy centers on integrated service contracts that include IoT-enabled dispensers, refill cartridges, and cloud dashboards, locking in accounts for three to five years. Ecolab’s One Ecolab restructuring targets USD 334 million in savings by 2027 and accelerates cross-selling of digital hygiene services. STERIS’s USD 539.8 million purchase of BD’s sterilization assets extends its consumable bundle and secures a captive installed base.

Regulatory differentiation proves a viable disruptor path; Reckitt’s Lysol Air Sanitizer captured 8.4% of the U.S. instant-action category within 15 months of launch after winning the first EPA airborne claim. Technology adoption is bifurcated: large health systems deploy hydrogen-peroxide vapor robots costing USD 20,000-100,000, whereas smaller hospitals stick to manual wipes. The USPTO granted 127 disinfectant patents in 2024, with clusters in sustained-release coatings and probiotic surface colonizers. ISO 13485 and ISO 14644 compliance increasingly functions as a moat in pharmaceutical and biotech segments, where validation files exceed 500 pages and require annual audits.

Antiseptics And Disinfectants Industry Leaders

Reckitt Benckiser Group plc

Steris PLC

Becton, Dickinson and Company

The Clorox Company

Solventum Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ecolab expanded its One Ecolab restructuring, budgeting USD 334 million to unify global sales teams and roll out IoT-linked dispensers

- September 2025: GermStopSQ has been issued a Drug Identification Number by Health Canada, making it Canada's first and only approved residual disinfectant. Unlike other products on the market, a single application of GermStopSQ provides 24 hours of continuous hospital-grade disinfection.

- July 2024: Ecolab launched disinfectant 1 wipe, the first EPA-registered 100% plastic-free degradable disinfectant wipe complete with 1-minute hospital disinfection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the antiseptics and disinfectants market as the worldwide sale of chemical and enzymatic preparations formulated to eliminate or inactivate microorganisms; antiseptics are intended for living tissue, while disinfectants target hard, non-living surfaces in healthcare, institutional, and selected commercial settings.

Scope exclusion: products developed solely for agricultural crop protection, municipal water treatment, or large-scale industrial sanitation fall outside this assessment.

Segmentation Overview

- By Product Type

- Quaternary Ammonium Compounds

- Chlorine Compounds

- Alcohols & Aldehydes

- Biguanides & Iodine Derivatives

- Enzymes

- Phenolics & Others

- By Formulation

- Liquids

- Sprays & Aerosols

- Wipes

- Gels & Foams

- By Application

- Surface Disinfectants

- Medical-Device Disinfectants

- Enzymatic Cleaners

- Skin & Wound Antiseptics

- By End User

- Hospitals & Clinics

- Ambulatory & Day-Surgery Centers

- Long-Term Care Facilities

- Pharma & Biotech Manufacturing

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with infection-control nurses, central-sterilization managers, facility procurement leads, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. Interviews validated hospital-level consumption rates, emerging enzymatic cleaner adoption, and average transfer prices, thereby closing gaps spotted during desk work.

Desk Research

We began with ministry of health surveillance portals, the World Health Organization's Global Health Observatory, and infection-control advisories from agencies such as the US CDC and European ECDC. Trade flows for quaternary ammonium compounds and chlorine derivatives were parsed from UN Comtrade, while EPA List N registrations clarified active-ingredient prevalence. Financials from D&B Hoovers and news archives on Dow Jones Factiva helped size leading suppliers, and hospital bed statistics were drawn from OECD and national statistical bureaus. These sources illustrate the range consulted; many additional public and subscription references informed our base data.

Market-Sizing & Forecasting

Our model blends top-down and bottom-up views. A top-down reconstruction uses hospital bed stock, surgical procedure counts, outpatient visit volumes, and recommended disinfectant dosage guidelines to build demand pools that are then cross-checked with supplier revenue roll-ups and sampled average selling prices. Variables such as healthcare expenditure growth, EPA/FDA regulatory updates, packaging-size mix shifts, and infection-incidence alerts feed a multivariate regression that drives the 2025-2030 forecast. Where supplier disclosures lack regional splits, ratios derived from customs data and expert input bridge the gaps.

Data Validation & Update Cycle

Outputs pass variance checks against historical consumption ratios and external alert signals; anomalies trigger analyst re-contact rounds before sign-off. Reports refresh annually, with interim flashes after material regulatory or epidemiological events, and a last-minute data sweep is completed just before delivery to clients.

Why Mordor's Antiseptics And Disinfectants Market Baseline Commands Proven Reliability

Published estimates often diverge because firms choose different product baskets, inflation adjustments, and refresh cadences.

Key gap drivers include divergent inclusion of consumer household cleaners, varied treatment of antiseptics applied to skin, disparate currency bases, and the cadence at which emerging enzymatic formulations are folded into models.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.88 B (2025) | Mordor Intelligence | - |

| USD 31.4 B (2023) | Global Consultancy A | Narrower product scope and constant-2023 dollars delay inflation capture |

| USD 53.89 B (2024) | Industry Portal B | Includes household surface cleaners and retail OTC antiseptic gels |

| USD 35 B (2024) | Regional Tracker C | Excludes antiseptics for living tissue and omits Asia Pacific distributor sales |

In sum, Mordor's disciplined scope selection, live FX conversion, and yearly refresh deliver a balanced baseline that stakeholders can trace to transparent variables and repeatable steps, giving decision-makers high confidence in our numbers.

Key Questions Answered in the Report

How large is the antiseptics and disinfectants market in 2026?

The antiseptics and disinfectants market size reached USD 44.17 billion in 2026 and is projected to rise steadily through 2031.

What is the expected growth rate for Antiseptics and Disinfectants between 2026-2031?

The market is forecast to record an 8.05% CAGR over 2026-2031 as hygiene protocols persist and surgical volumes climb.

Why are enzymatic cleaners gaining traction in Antiseptics and Disinfectants?

Enzymatic cleaners dissolve biofilm quickly and protect heat-sensitive instruments, driving a forecast 11.55% CAGR in this application.

How are regulations influencing Antiseptics and Disinfectants purchasing decisions?

New residue test methods and multi-tier registration rules raise compliance costs, pushing buyers toward validated, brand-name products that can document safety and efficacy.

Which end-user group is expanding fastest in Antiseptics and Disinfectants?

Ambulatory surgery centers lead growth at 11.43% CAGR as more procedures shift to outpatient settings requiring rapid-turnaround disinfection.

Page last updated on: