Infection Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

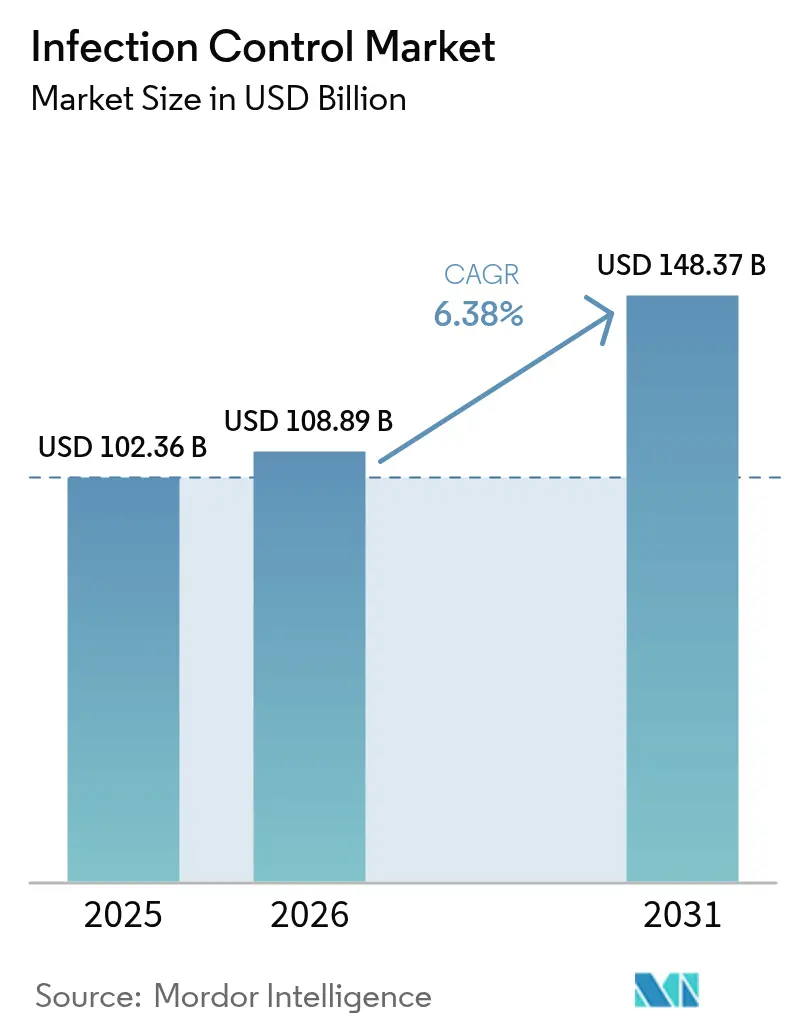

| Market Size (2026) | USD 108.89 Billion |

| Market Size (2031) | USD 148.37 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infection Control Market Analysis by Mordor Intelligence

The infection control market size is expected to grow from USD 102.36 billion in 2025 to USD 108.89 billion in 2026 and is forecast to reach USD 148.37 billion by 2031 at 6.38% CAGR over 2026-2031. Rising reimbursement penalties tied to hospital-acquired infections (HAIs), rapid hospital adoption of low-temperature sterilizers, and sustained demand for single-use protective products underpin this growth. Healthcare providers are reallocating capital toward advanced sterilization platforms as the EPA tightens ethylene oxide (EtO) emission limits. Artificial-intelligence surveillance systems further accelerate preventive strategies by predicting infection clusters in real time, while contract sterilization outsourcing expands because specialist operators can amortize new compliance costs across multiple clients. Asia-Pacific, supported by the ongoing scale-up of Chinese healthcare spending, contributes the largest incremental revenue through 2030.

Key Report Takeaways

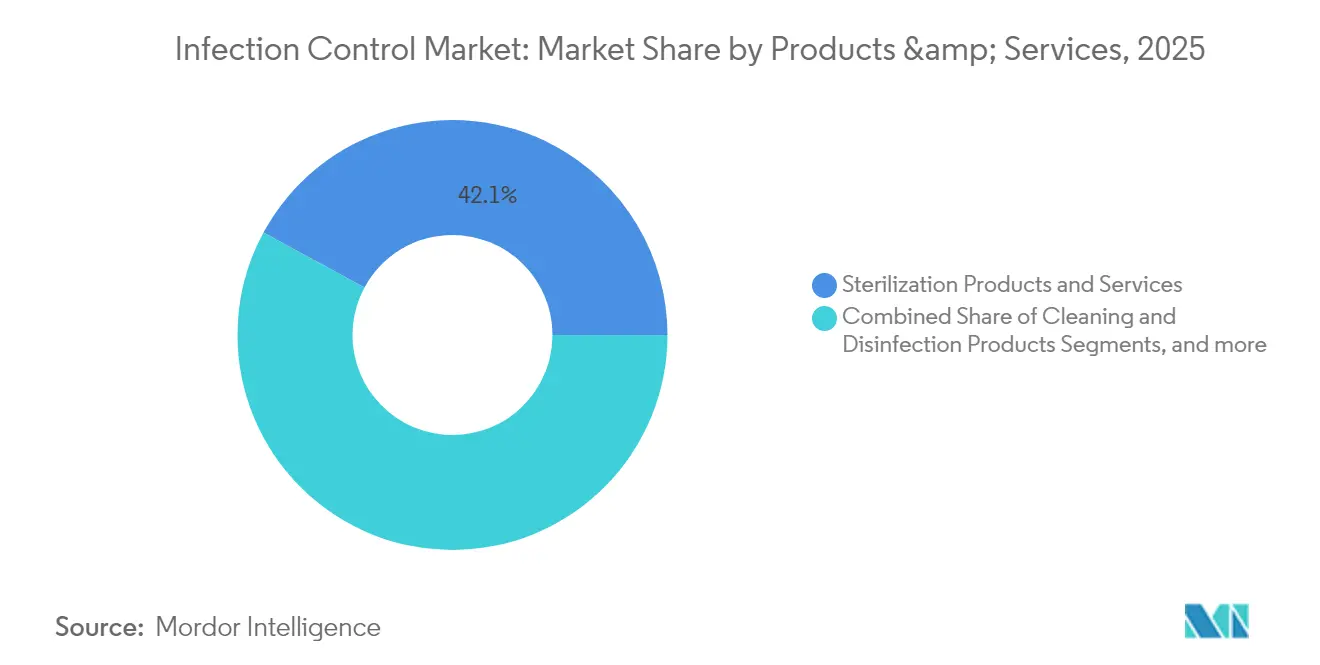

- By products & services, sterilization products and services led with 42.10% of infection control market share in 2025; protective barriers are projected to expand at a 6.66% CAGR to 2031.

- By service delivery mode, in-house programs held 53.40% of the infection control market in 2025, while contract services record the highest projected CAGR at 6.62% through 2031.

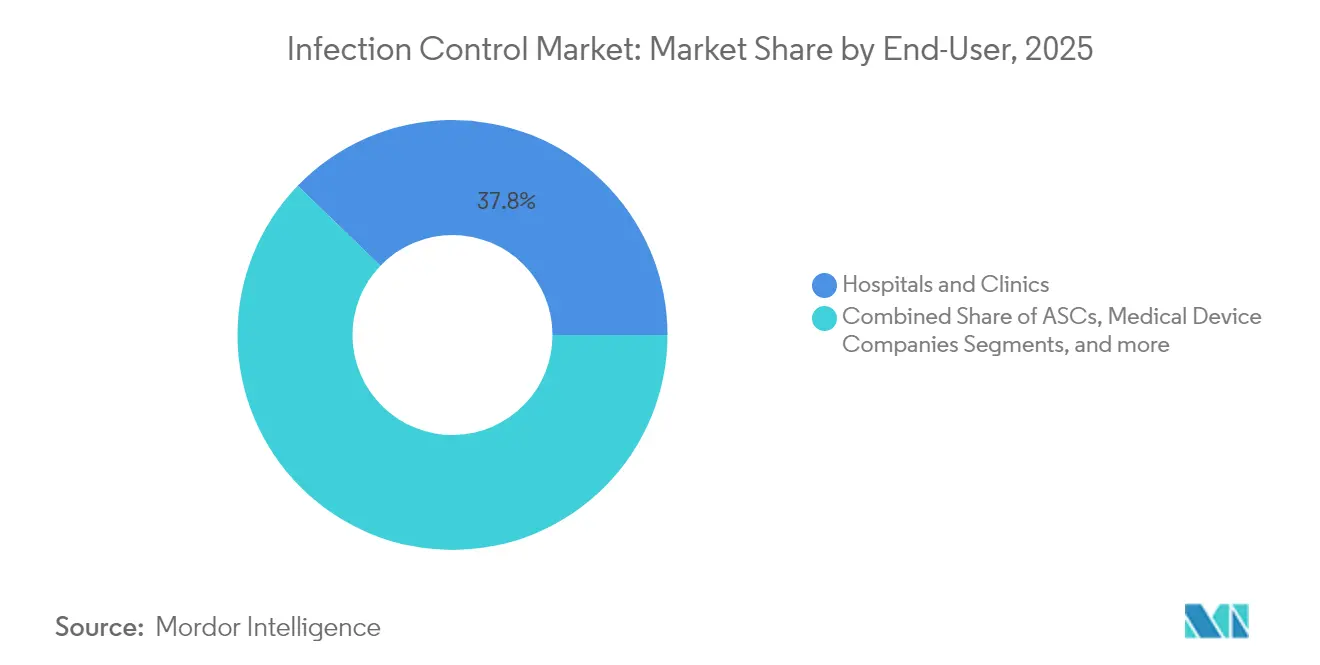

- By end-user, hospitals and clinics commanded 37.80% share of the infection control market size in 2025; ambulatory surgery centers are advancing at a 6.74% CAGR through 2031.

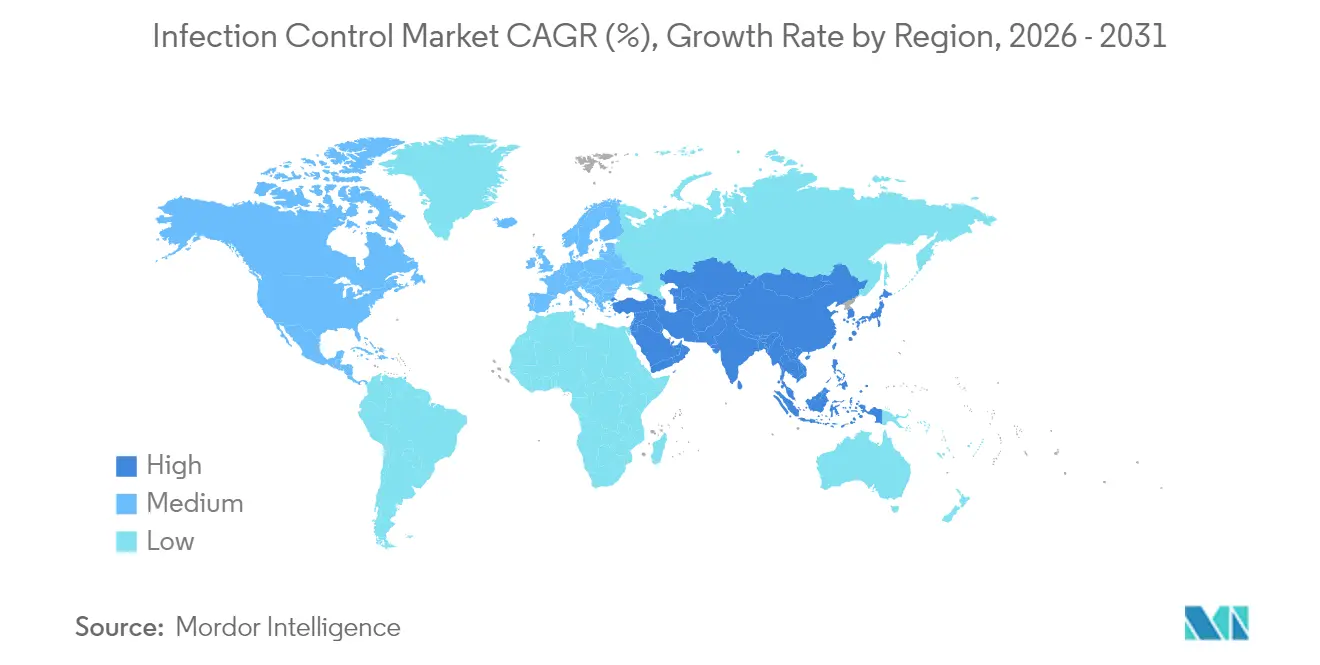

- By geography, North America occupied 38.95% of infection control market revenue in 2025, whereas Asia-Pacific is scaling at a 6.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infection Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global HAI-reduction targets & reimbursement penalties | +1.2% | Global, with strongest impact in North America & EU | Medium term (2-4 years) |

| Procedure volume surge from chronic & geriatric disease burden | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Outsourcing boom in contract sterilization services | +0.8% | North America & EU primary, expanding to APAC | Medium term (2-4 years) |

| Rapid adoption of low-temperature & plasma sterilizers | +0.9% | Global, led by North America & EU | Short term (≤ 2 years) |

| AI-driven infection-surveillance platforms winning hospital RFPs | +0.7% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Green-chemistry mandates favouring ozone & peracetic-acid systems | +0.6% | EU leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global HAI-Reduction Targets & Reimbursement Penalties

CMS value-based purchasing now links reimbursements to infection metrics, including catheter-associated urinary tract infections and central line-associated bloodstream infections. California and other states mirror these incentives, prompting hospital boards to budget for new sterilizers and data-analytics tools. Facilities that fell short during the COVID-19 disruption report a renewed focus on policy-compliant equipment upgrades. Medium-term pressure remains elevated as the Transforming Episode Accountability Model begins in 2026, making infection control performance essential for revenue integrity.

Procedure Volume Surge From Chronic & Geriatric Disease Burden

Inpatient discharges are projected to climb to 31 million while outpatient volumes rise to 5.82 billion procedures by 2034. Orthopedic, spine, and gastroenterology procedures increasingly migrate to ambulatory centers, requiring advanced sterilizers capable of rapid cycles. China’s pathway toward RMB 205 trillion in health outlays by 2030 mirrors this structural procedure expansion. Longer life expectancy and multimorbidity raise infection risk, reinforcing the commercial case for predictive surveillance platforms that identify high-risk patients pre-operatively.

Outsourcing Boom in Contract Sterilization Services

Sterigenics alone manages 48 sites across 13 countries, serving more than 2,000 clients. New EtO ventilation and monitoring rules cost facilities up to USD 900 million; outsourcing enables hospitals to avoid these capital charges while securing regulatory expertise. Specialist providers adopt vaporized hydrogen peroxide lines approved by the FDA, tempering EtO reliance and shortening turnover times. Small facilities leverage these partnerships to keep surgical blocks open without major capital allocations.

Rapid Adoption of Low-Temperature & Plasma Sterilizers

Hydrogen-peroxide gas-plasma cycles sterilize 95% of test materials in 75 minutes and leave no toxic residue. STERIS and ASP earned clearances for complex duodenoscope processing, pushing uptake in high-risk endoscopy suites. Electromagnetic-seal containers and cold plasma units extend sterilization to heat-sensitive instruments, lowering device repair costs while reducing surgical-site infections.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety & liability concerns around reprocessed instruments | -0.9% | Global, particularly North America & EU | Medium term (2-4 years) |

| Capital-intensive nature of advanced sterilization equipment | -0.7% | Global, more pronounced in emerging markets | Long term (≥ 4 years) |

| Increasing antimicrobial-resistance reduces disinfectant efficacy | -1.1% | Global, critical in hospital settings | Short term (≤ 2 years) |

| ESG pressure against single-use protective barriers | -0.5% | EU leading, North America & APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety & Liability Concerns Around Reprocessed Instruments

Complex lumened devices are prone to incomplete decontamination, raising malpractice exposure. Multidrug-resistant Klebsiella strains with biocide tolerance have already surfaced in hospital outbreaks. Updated ANSI/AAMI ST24 guidance demands rigorous performance validation, yet many facilities delay upgrades for budget reasons, sustaining litigation risk.

Capital-Intensive Nature of Advanced Sterilization Equipment

Compliance with the revised EtO rule costs smaller hospitals millions, diverting funds from other patient-care technologies. Low-temperature units require separate HVAC loops, advanced monitoring, and specialized staff training, stretching payback periods beyond traditional board approval thresholds—particularly in volatile emerging-market currencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products & Services: Sterilization Dominance Drives Technology Innovation

Sterilization products and services controlled 42.10% infection control market share in 2025. Heat sterilizers continue to anchor budgets because of entrenched staff familiarity, yet low-temperature hydrogen-peroxide plasma units are posting double-digit placement growth within tertiary centers. The infection control market size for this segment is forecast to reach USD 62.47 billion by 2031, advancing at a pace aligned with overall industry CAGR. Contract sterilization providers, leveraging scale, invest in multi-modal processing lines that individual hospitals struggle to fund. Protective barriers, the fastest-growing area, increasingly incorporate compostable substrates to satisfy ESG audits, even as hospitals audit glove and gown burn rates to ensure pandemic-era stockpiles remain current.

Cleaning chemicals face potent headwinds from antimicrobial resistance. Laboratories confirm that 80% of multidrug-resistant Pseudomonas isolates defeat standard QAC solutions, prompting formulators to explore quaternary phosphonium molecules with broader kill spectrums. Automated endoscope reprocessors with leak-testing and traceability modules are gaining mindshare because manual flushing cannot consistently navigate intricate device channels. Overall, product strategists are prioritizing sterilization throughput, eco-toxicity, and real-time compliance analytics.

By Service Delivery Mode: Contract Services Gain Momentum

Hospitals retained 53.40% control over infection-control tasks in 2025, yet rising environmental and worker-safety rules accelerate the shift toward outsourcing. The infection control market size for contract services is projected to post a 6.62% CAGR to 2031 as provider networks weigh total cost of ownership against outsourcing fees. Centralized vendors distribute EtO and vaporized hydrogen peroxide capacity across multisite networks, offering surge coverage when in-house units undergo maintenance. Third-party operators also manage record-keeping and validation, limiting liability under CMS audits.

In urgent-care chains and ambulatory centers, contract partners deliver pick-up and return cycles aligned to procedural scheduling, removing the need for on-site sterilization bays that consume scarce square footage. In Asia-Pacific, capacity additions cluster around export-oriented device manufacturers, creating dual revenue streams from hospital instruments and original-equipment processing.

By End-User: ASCs Drive Outpatient Infection Control Growth

Hospitals and clinics represented 37.80% infection control market revenue in 2025, yet ambulatory surgery centers posted the strongest trajectory at a 6.74% CAGR. Infection control market size for ASCs is expected to touch USD 13.58 billion by 2031 as orthopedics, ENT, and gastroenterology cases migrate from inpatient wings. ASC executives prioritize compact low-temperature cabinets that achieve 60-minute room turnaround, sustaining high case volumes.

Medical-device firms depend on contract sterilizers for product throughput, with EtO services covering roughly half of all device SKUs. Pharmaceutical plants under EU GMP Annex 1 now feature integrated vaporized hydrogen peroxide tunnels to validate fill-finish lines. Veterinary clinics and research labs round out secondary demand, seeking miniaturized plasma units suited to lower instrument loads without compromising sterility assurance levels.

Geography Analysis

North America accounted for 38.95% infection control market revenue in 2025. The region adopts innovations early, spurred by CMS reimbursement structures and a dense network of ASC facilities needing fast sterilizer cycles. U.S. policy shifts, such as the FY 2025 IPPS rule, embed infection metrics into broader quality reporting, intensifying hospital spending on predictive analytics platforms.

Europe follows closely, guided by medical-device directives that integrate carbon-footprint scoring into product approvals. Hospitals weigh reusable barrier programs against infection risk, leading to pilot projects pairing reusable gowns with plasma sterilization cabinets to maintain efficacy. Infection control market size in Europe is expected to approach USD 39.1 billion by 2031.

Asia-Pacific delivers the fastest 6.85% CAGR. China’s pathway toward RMB 205 trillion in health spending drives new hospital construction and bulk procurement of EtO and hydrogen-peroxide lines. India’s National Quality Assurance Standards now mandate central sterile services departments in district hospitals, stimulating equipment tenders. Japan’s aging population pushes device reprocessing volumes, while South-East Asian private hospital chains outsource sterilization to regional hubs.

The Middle East and Africa invest in flagship medical cities with central sterile processing designed to Joint Commission standards, though fragmented smaller clinics still rely on tabletop autoclaves. In South America, public-sector infection-control budgets grow alongside universal-health-coverage rollouts, creating mixed demand for premium and mid-tier equipment.

Competitive Landscape

Industry concentration is moderate. Ecolab divested its surgical-solutions unit to Medline for USD 950 million in 2024, showing portfolio refocus toward core chemistry platforms[1]Health Exec, “Ecolab Sells Surgical Solutions Unit,” healthexec.com. 3M’s healthcare spinoff, Solventum, is now an USD 8.2 billion infection-control pure-play, enabling targeted R&D on low-temperature sterilization catalysts[2]3M, “Completion of Solventum Spin-Off,” news.3m.com.

Metall Zug and Miele merged Belimed and Steelco into a EUR 423 million joint venture, pooling engineering resources across washer-disinfectors and steam sterilizers[3]Metall Zug AG, “Steelco-Belimed Joint Venture Announcement,” metallzug.ch.

Technology differentiation now leans on real-time analytics and eco-friendly sterilants. Solventum’s 2025 launch of a pre-assembled vaporized hydrogen-peroxide test pack simplifies routine biological monitoring, cutting technician labor. STERIS pilots plasma chambers with integrated AI dashboards that auto-adjust dwell times based on load geometry. Start-ups exploit white space in UV-C and cold-plasma disinfection, targeting rapid device turnarounds without chemical residues.

Infection Control Industry Leaders

Fortive (Advanced Sterilization Products)

3M Company

Getinge AB

Steris PLC

Cantel Medical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Solventum reported 2.6% sales growth and introduced a pre-assembled VH₂O₂ test pack with dual performance indicators.

- January 2025: EPA released its interim EtO decision, reducing exposure limits to 0.1 ppm by 2035.

- November 2024: FDA issued a transitional policy covering EtO facility changes for Class III devices.

- September 2024: Chronos UV-C probe disinfection device gained first-in-class FDA De Novo clearance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, our study defines the infection control market as the full range of products and contracted services that destroy, remove, or prevent the spread of microorganisms in hospitals, ambulatory centers, medical-device and pharmaceutical plants, life-science laboratories, and food-processing facilities. In scope are sterilization equipment, contract sterilization, cleaning and disinfection consumables, protective barriers, and endoscope reprocessing solutions.

(Scope exclusions) We explicitly exclude diagnostic test kits, wound-care dressings, and systemic anti-infective drugs.

Segmentation Overview

- By Products & Services

- Sterilization Products & Services

- Sterilization Equipment

- Heat Sterilization Equipment

- Low-Temperature Sterilization Equipment

- Radiation Sterilization Equipment

- Chemical Sterilization Equipment

- UV & Ozone Sterilization Equipment

- Contract Sterilization Services

- Consumables & Accessories

- Sterilization Equipment

- Cleaning & Disinfection Products

- Disinfectants

- Hand Disinfectants

- Surface Disinfectants

- Skin Disinfectants

- Instrument Disinfectants

- Cleaning & Disinfection Equipment

- Consumables & Accessories

- Disinfectants

- Protective Barriers

- Surgical Drapes

- Surgical Gowns

- Gloves

- Masks & Respirators

- Other Protective Barriers

- Other Infection Control Products

- Sterilization Products & Services

- By Service Delivery Mode

- In-house Infection Control

- Contract Infection Control

- By End-User

- Hospitals and Clinics

- Ambulatory Surgery Centers

- Medical Device Companies

- Pharmaceutical and Biologics Manufacturers

- Life-Science and Food-Processing Facilities

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with infection-prevention nurses, sterile-processing managers, contract sterilization executives, and consumable distributors across North America, Europe, Asia-Pacific, and Latin America. These interviews verified price corridors, replenishment cycles, and adoption triggers that secondary data only hinted at.

Desk Research

We began by pairing WHO Global Health Observatory, CDC NHSN, Eurostat surgical discharge files, Japan MHLW inpatient statistics, and UN Comtrade trade grids to size demand and map trade flows. Annual reports, 10-Ks, and device registration lists enriched supplier counts and average selling prices.

The next pass used tier-one journals such as the American Journal of Infection Control, APIC and AAMI portals, plus Dow Jones Factiva and D&B Hoovers for curated news and financial splits, giving early warning of price or capacity shifts. The sources cited are illustrative; many additional databases and publications informed data collection and validation.

Market-Sizing & Forecasting

We implement a top-down construct that starts with regional surgical volumes and HAI incidence, converts these to product demand through penetration and price ratios, and then corroborates results with supplier roll-ups and channel checks. Key variables like operating-room counts, installed low-temperature sterilizer base, contract irradiation capacity, PPE sets per bed, and new regulatory mandates feed a multivariate regression that shapes 2025-2030 trajectories. Data gaps are bridged with interpolation anchored to verified trend pivots.

Data Validation & Update Cycle

Our outputs undergo three-layer reviews; variance flags trigger re-contact with respondents before sign-off. Reports refresh annually, with mid-cycle updates for recalls, pandemics, or major regulatory shifts. This is where Mordor Intelligence differentiates, ensuring clients always receive the latest vetted view.

Why Our Infection Control Baseline Earns Trust

Published estimates diverge because firms vary scope, input depth, and refresh cadence.

By anchoring variables to real infection drivers and updating every year, we give decision-makers a transparent, reproducible baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 102.36 B (2025) | Mordor Intelligence | - |

| USD 57.31 B (2025) | Global Consultancy A | Narrower product basket and biennial updates |

| USD 52.38 B (2024) | Trade Journal B | Bundles wound-care items and applies straight CAGR extrapolation |

The comparison highlights how wider scope selection, fresher primary inputs, and cross-method validation let Mordor Intelligence set a balanced, dependable baseline for the infection control space.

Key Questions Answered in the Report

What is the current size of the infection control market?

The infection control market is valued at USD 108.89 billion in 2026 and is projected to reach USD 148.37 billion by 2031.

Which product category holds the largest infection control market share today?

Sterilization products and services lead with 42.10% share, reflecting sustained demand for terminal-sterilization solutions.

Why are ambulatory surgery centers important for future infection control revenue?

Procedure migration out of hospitals pushes ASC volumes to 44 million by 2034, driving rapid uptake of compact low-temperature sterilizers.

How will new EPA ethylene oxide rules affect hospitals?

Facilities must invest in upgraded ventilation and monitoring or outsource sterilization, as exposure limits fall to 0.1 ppm by 2035.

What role does artificial intelligence play in infection prevention?

AI platforms analyze patient data in real time, flagging infection risks early and enabling hospitals to cut HAI rates while lowering cost penalties.

Page last updated on: