Dental Infection Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

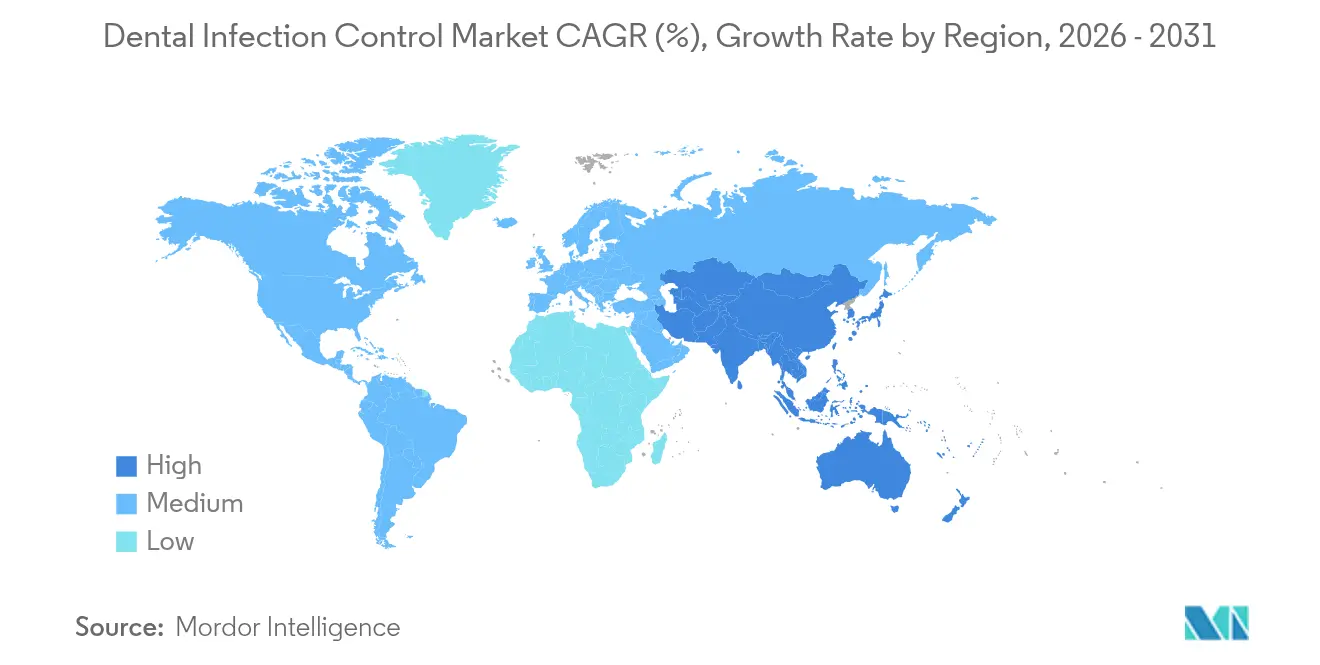

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

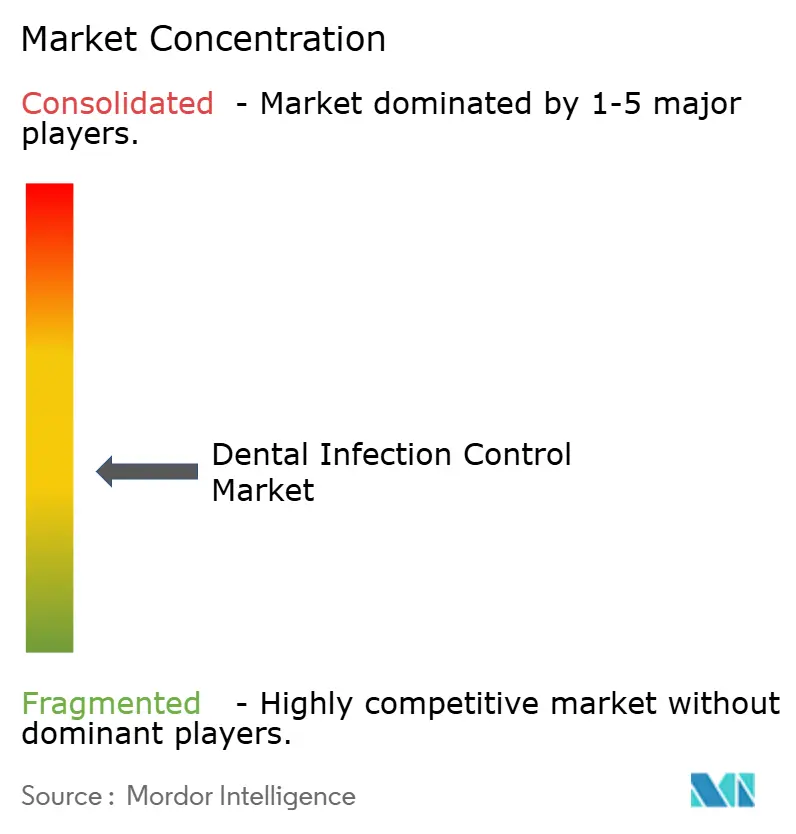

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Infection Control Market Analysis by Mordor Intelligence

The dental infection control market size was valued at USD 1.65 billion in 2025 and estimated to grow from USD 1.76 billion in 2026 to reach USD 2.39 billion by 2031, at a CAGR of 6.38% during the forecast period (2026-2031). Expansion is propelled by stricter safety regulations, rapid post-pandemic procedure growth, and integration of IoT-enabled compliance software that turns manual tasks into continuous digital workflows. Heightened patient awareness has shifted purchasing from basic autoclaves to fully validated ecosystems that bundle tracking sensors, cloud reporting, and predictive maintenance. Mid-tier manufacturers are moving quickly to fill portfolio gaps left by recent divestitures, while premium clinics are leveraging visible infection-control tech as a marketing edge to medical tourists. Supply-chain resilience and sustainability now rank alongside sterilization efficacy in procurement decisions, prompting investments in energy-efficient benchtop steam units and reusable barrier systems.

Key Report Takeaways

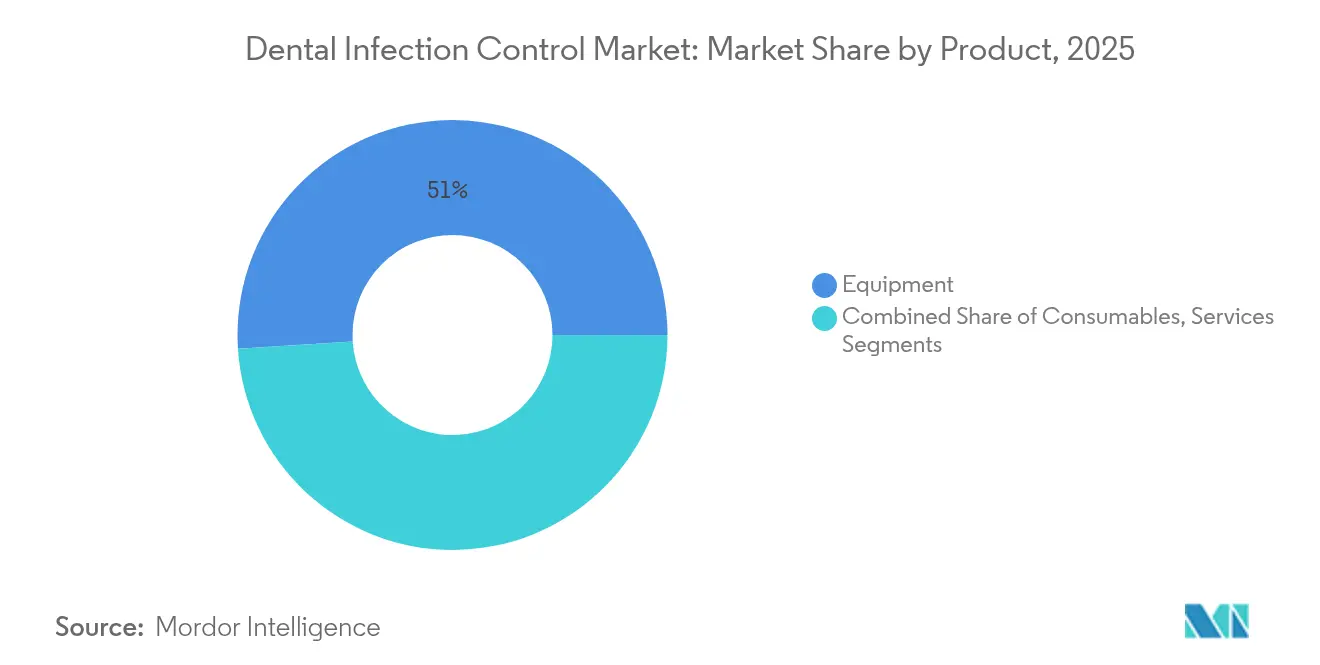

- By product type, equipment led with a 51.02% market share in 2025 for dental infection control; consumables are projected to expand at a 9.02% CAGR to 2031.

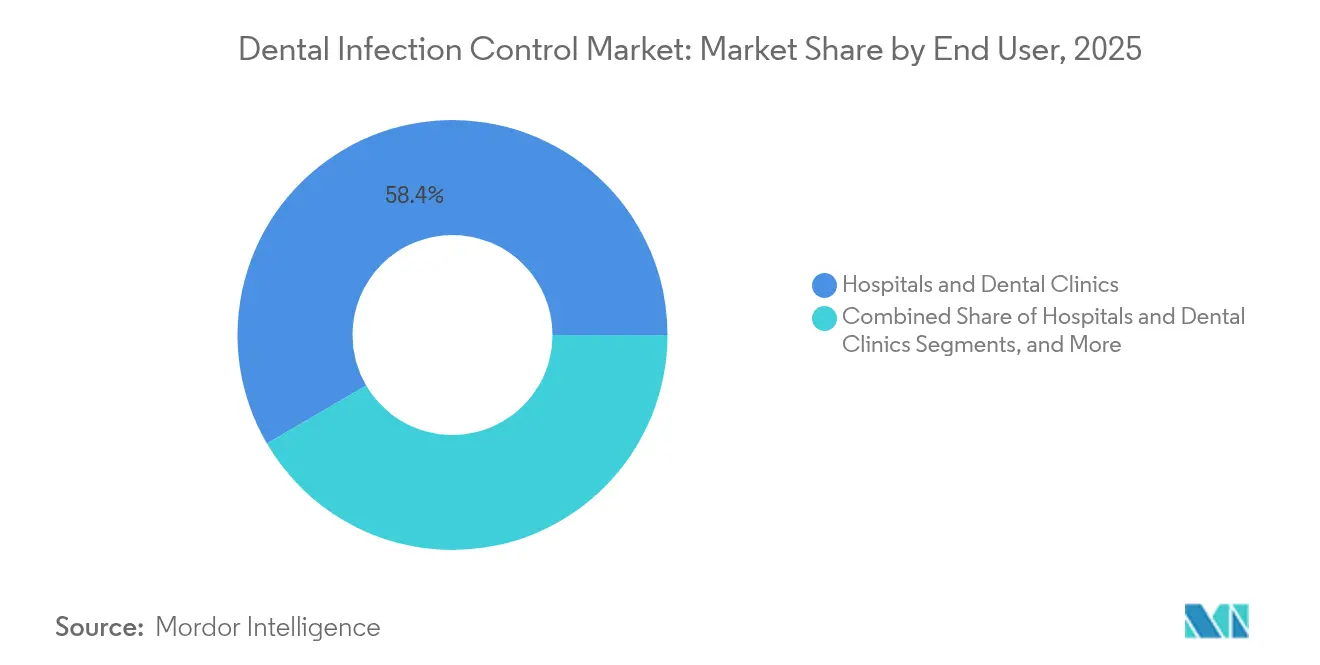

- By end user, hospital & dental clinics held 58.42% revenue share in 2025, whereas dental laboratories registered the fastest 7.78% CAGR through 2031.

- By geography, North America dominated with a 30.15% share of the dental infection control market size in 2025, while Asia-Pacific is forecast to grow at an 7.76% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Infection Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Dental Ailments & Surgeries | +1.80% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Technological Advances In Sterilization & Disinfection | +1.50% | North America & EU leading, APAC adoption accelerating | Long term (≥ 4 years) |

| Stricter Infection-Control Accreditation Standards | +1.20% | Global, with regulatory harmonization in developed markets | Short term (≤ 2 years) |

| Expansion Of Dental Clinics & Medical Tourism | +1.00% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| AI-Enabled Sterilization Tracking & IoT Compliance | +0.90% | North America & EU early adoption, APAC following | Long term (≥ 4 years) |

| Sustainability Push For Reusable Barriers & Plastics Bans | +0.80% | EU leading, North America selective adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Ailments & Surgeries

Complex implant and periodontal procedures are increasing instrument loads and turnaround frequency, forcing clinics to invest in advanced processing units that can sterilize intricate geometries without damage. Aging populations in North America and Europe continue to fuel high-value surgeries that require validated traceability, pushing demand for barcode-scanning autoclaves and biological indicator monitoring systems. Updated CDC guidelines classify bone-involving interventions as high-risk, giving practices a compliance imperative to replace legacy benchtop sterilizers with higher-capacity vacuum units.[1]Centers for Disease Control and Prevention, “Summary of Infection Prevention Practices in Dental Settings,” cdc.gov

Technological Advances in Sterilization & Disinfection

UV-C LED arrays now achieve 99.9999% inactivation of resistant fungi at 270 nm, providing an airborne safeguard that complements steam sterilization without breaking room occupancy rules. Solventum’s 2025 eBowie-Dick system digitizes daily test records, eliminating hand-written logs and cutting audit prep time. IoT sensors embedded in chamber gaskets feed maintenance data to the cloud, letting service teams intervene before a cycle failure can disrupt patient flow, although data-security hurdles still stall adoption among smaller offices.

Stricter Infection-Control Accreditation Standards

State-level mandates, such as Georgia’s quarterly waterline testing and five-year record retention, require robust documentation platforms that interface with laboratory portals. England’s updated HTM 0701 now reclassifies most chairside waste, lowering disposal fees yet expanding audit files that prove segregation accuracy.[2]BDJ In Practice, “HTM 0701 Waste Classification Changes,” nature.com Divergent federal-state rules in the United States force multi-site dental service organizations to adopt the toughest common denominator, raising administrative overhead for chain operators.

Expansion of Dental Clinics & Medical Tourism

Destinations from Kuala Lumpur to Phuket advertise glass-walled sterilization rooms where UV-C towers run visibly between appointments, turning infection control into a trust-building spectacle. Malaysia’s private clinics, which hold 70% domestic share, cite sterilization tech in marketing aimed at overseas patients seeking implant packages, and seasonal procedure surges are straining consumables supply chains.[3]International Trade Administration, “Malaysia – Healthcare Services,” trade.gov Fragmented oversight across APAC markets still leaves travelers facing uneven standards despite similar promotional claims, underlining the advantage held by facilities with internationally accredited protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost Of Advanced Equipment & Consumables | -1.40% | Global, with highest impact on emerging markets | Short term (≤ 2 years) |

| Stringent Multi-Jurisdictional Regulatory Approvals | -0.80% | North America & EU regulatory complexity | Medium term (2-4 years) |

| Tariff-Driven Supply-Chain Disruption | -0.60% | US-China trade routes, EU-Asia corridors | Short term (≤ 2 years) |

| Shortage Of Trained Sterile-Processing Technicians | -0.40% | North America & developed APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Equipment & Consumables

Midmark’s 2024 steam sterilizers boast 25,000-cycle lifespans but command premium prices that place them beyond many solo practices, especially in regions where reimbursement remains flat. Rising single-use product volumes also escalate recurring expenses, and leasing programs often bundle proprietary consumables that prevent cost-saving substitutions. Consequently, funding constraints delay upgrades in locations where infection-risk profiles are actually highest.

Stringent Multi-Jurisdictional Regulatory Approvals

The FDA’s evolving 510(k) guidance for curing lights adds new performance-test protocols, multiplying time-to-market expenses for manufacturers who must file different dossiers for CE marking and UKCA registration. Smaller labs are overwhelmed by quality-system paperwork, spurring consolidation into networks that can spread compliance overhead. Separate state directives overlay federal mandates, obliging multi-state DSOs to engineer location-specific checklists that sap managerial bandwidth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Anchors Grow While Consumables Accelerate

Equipment captured 51.02% of 2025 revenue, reflecting the capital-intensive backbone of the dental infection control market. High-capacity pre-vacuum autoclaves fitted with RFID-tracked cassettes generate long amortization cycles, and UV-C LED cabinets are emerging to address aerosol contamination previously unmanaged by steam technology. Consumables, however, are expanding at a 9.02% CAGR on the back of heightened cycle frequency, increased biological indicator usage, and single-use sheathing for handpieces. This twin-track dynamic balances predictable equipment replacement budgets against the recurring outflow for test packs and chemical integrators.

Consumables’ momentum underscores a procedural shift toward safety-first workflows that depend on validated indicators for every load rather than random sampling. Elevated PPE norms post-2024 have steadied but remain above pre-pandemic baselines, locking in higher quarterly supply spending. Meanwhile, the services niche outsourced instrument reprocessing and regulated waste management grows as urban clinics seek to free chair-time by subcontracting back-office sterilization. However, its share of the dental infection control market is still minor.

By End User: Laboratories Outpace Aggregated Clinic Base

Dental clinics accounted for 58.42% of revenue in 2025, yet laboratories are advancing at 7.78% CAGR, fueled by digital impression workflows that demand contamination-free milling hubs. The labs’ need for sterile 3-D-printed components accelerates the adoption of tabletop plasma and low-temperature vaporized H₂O₂ units that can safely process resins. Academic centers pursue flexible chambers capable of toggling between research prototypes and clinical instruments, consolidating purchasing around modular racks and programmable cycles.

Hospital dental suites must align with wider hospital infection-control committees, prompting acquisitions of large-chamber pass-through sterilizers that exceed the typical dental practice capacity. Mobile dentistry and teledentistry support teams represent an “Others” micro-segment, requiring compact, battery-friendly sterilizers that meet the same cycle-validation benchmarks demanded by fixed sites. Cross-segment, digital traceability is turning into a universal procurement prerequisite, mainly where dental infection control market share battles occur among chains vying for accreditation points.

Geography Analysis

North America generated 30.15% of the total 2025 revenue, leveraging mature reimbursement schemes and entrenched accreditation bodies that enforce rigorous sterilization audits. Growth is now tempered as replacement, not expansion, dominates purchase cycles. Clinics face staff shortages that limit throughput gains, and proposed tariffs on dental imports threaten supply cost spikes, pushing dealers to explore near-shore sourcing.

Asia-Pacific stands as the fastest mover with an 7.76% CAGR through 2031. Tipping factors include government-led oral-health campaigns and the rebound of dental tourism corridors in Thailand, Malaysia, and South Korea. Malaysia’s dental services market alone is projected to hit USD 2.8 billion by 2027, spurring private clinics to advertise sterilization transparency to win international patients. Nonetheless, disparate approval pathways across ASEAN create onboarding delays for imported equipment, prompting regional distributors to hold higher safety stocks.

Europe shows consistent mid-single-digit growth anchored by sustainability directives such as HTM 0701 that encourage low-energy sterilizers and reusable textiles. Practices benefit from waste-classification revisions that cut disposal fees, freeing capital for software that automates documentation. Southern Europe, with its strong outbound dental-tourism flows, now invests in infection-control upgrades to reclaim domestic patient loyalty.

Emerging markets in the Middle East & Africa and South America lag but register rising tender volumes tied to public-sector clinic modernization. Currency volatility and limited technician pools continue to hamper uptake, yet multilateral health-fund grants are seeding first-time purchases of Class B sterilizers. Vendors entering these regions must combine maintenance training with sales, or risk under-utilization of sophisticated systems.

Competitive Landscape

The dental infection control market shows moderate consolidation, with the top five suppliers controlling an estimated 48%, leaving ample room for nimble specialists. Steris Corporation’s USD 787.5 million spin-off of its dental portfolio in 2024 signals a trend toward segment-focused operators that can iterate quickly without conglomerate overhead. Peak Rock Capital now steers the former Steris dental assets, eyeing bolt-on acquisitions of UV-C innovators to complete its platform.

Dentsply Sirona remains a heavyweight but reported flat organic growth amid compliance costs and shipping disruptions that pinched operating margins. HuFriedyGroup bolstered its portfolio with the SS White Dental acquisition, weaving burs with reprocessing cassettes to offer a cradle-to-grave instrument solution. Meanwhile, Henry Schein leverages its distribution muscle to promote drill-free remineralization products that reduce instrument-sterilization demand, indirectly shifting autoclaveloan volumes.

Competitive advantage is drifting toward firms that blend hardware with SaaS dashboards. Vendors able to verify every cycle digitally and deliver cloud-stored PDFs at audit time enjoy pull-through sales among multi-site DSOs. UV-C LED specialists enter with disruptive form factors—over-chair light bars and in-duct modules—prompting legacy autoclave makers to partner rather than build in-house. Sustainability is the next advantage: suppliers tout recyclable indicator strips and low-water-use chambers to meet European procurement criteria.

Dental Infection Control Industry Leaders

DentsplySirona

COLETENE Group

3M

Steris

Danaher Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Solventum launched the Attest eBowie-Dick Test System, an electronic card and auto-reader that automates daily steam-penetration verification.

- November 2024: Midmark Corporation unveiled next-generation M9 and M11 Steam Sterilizers with 25,000-cycle lifespans and touch-screen compliance tracking.

- October 2024: HuFriedyGroup acquired SS White Dental, expanding its infection-prevention catalog across 100 countries.

- September 2024: Henry Schein secured exclusive US distribution of Curodont Repair Fluoride Plus to large DSOs, reducing invasive drilling and related sterilization loads.

Global Dental Infection Control Market Report Scope

As per the scope of the report, dental infections are infections that originate at the tooth or its supporting structures and can spread to the surrounding tissue. Dental infections also affect gums causing gingivitis, which later causes periodontal disease. There are mainly two routes of transmission of infection viz direct or indirect. The direct route of transmission of dental infection involves contact with an infected body fluid such as blood, saliva, or direct contact with the affected lesion. The indirect route of transmission involves contact with the contaminated equipment or instrument. It is also caused by tissue debris during intraoral procedures. The dental infection control market is segmented by Product Type (Equipment and Consumables), End User (Hospitals and Clinics, Pharmaceutical and Biotechnology Companies, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Equipment | Sterilization Equipment |

| Cleaning & Disinfection Equipment | |

| Packaging Equipment | |

| UV-C LED Disinfection Units | |

| Consumables | Surface Disinfectants |

| Sterilization Indicators & Biological Monitors | |

| Hand-hygiene Products | |

| Personal Protective Equipment (Masks, Gloves, Barriers) | |

| Services | Sterilization Services |

| Regulated Waste-disposal Services |

| Hospitals & Dental Clinics |

| Dental Laboratories |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Equipment | Sterilization Equipment |

| Cleaning & Disinfection Equipment | ||

| Packaging Equipment | ||

| UV-C LED Disinfection Units | ||

| Consumables | Surface Disinfectants | |

| Sterilization Indicators & Biological Monitors | ||

| Hand-hygiene Products | ||

| Personal Protective Equipment (Masks, Gloves, Barriers) | ||

| Services | Sterilization Services | |

| Regulated Waste-disposal Services | ||

| By End User | Hospitals & Dental Clinics | |

| Dental Laboratories | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of the dental infection control market?

The market is valued at USD 1.76 billion in 2026.

What compound annual growth rate (CAGR) is forecast between 2026 and 2031?

The market is projected to grow at a 6.38% CAGR through 2031.

Which product segment currently generates the largest revenue?

Equipment leads, accounting for 51.02% of 2025 revenue.

Which geographic region is expected to expand most rapidly?

Asia-Pacific is forecast to register the fastest 7.76% CAGR through 2031.

How are UV-C LED systems influencing infection-control practices?

UV-C LED units provide continuous air and surface disinfection, achieving 6-log pathogen reductions and complementing traditional steam cycles.

Why are dental laboratories increasing their sterilization spending?

Laboratories are modernizing to support digital CAD/CAM workflows, driving an 7.78% CAGR as they require contamination-free environments for milling and 3-D printing.

Page last updated on: