United Kingdom Payment Gateway Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

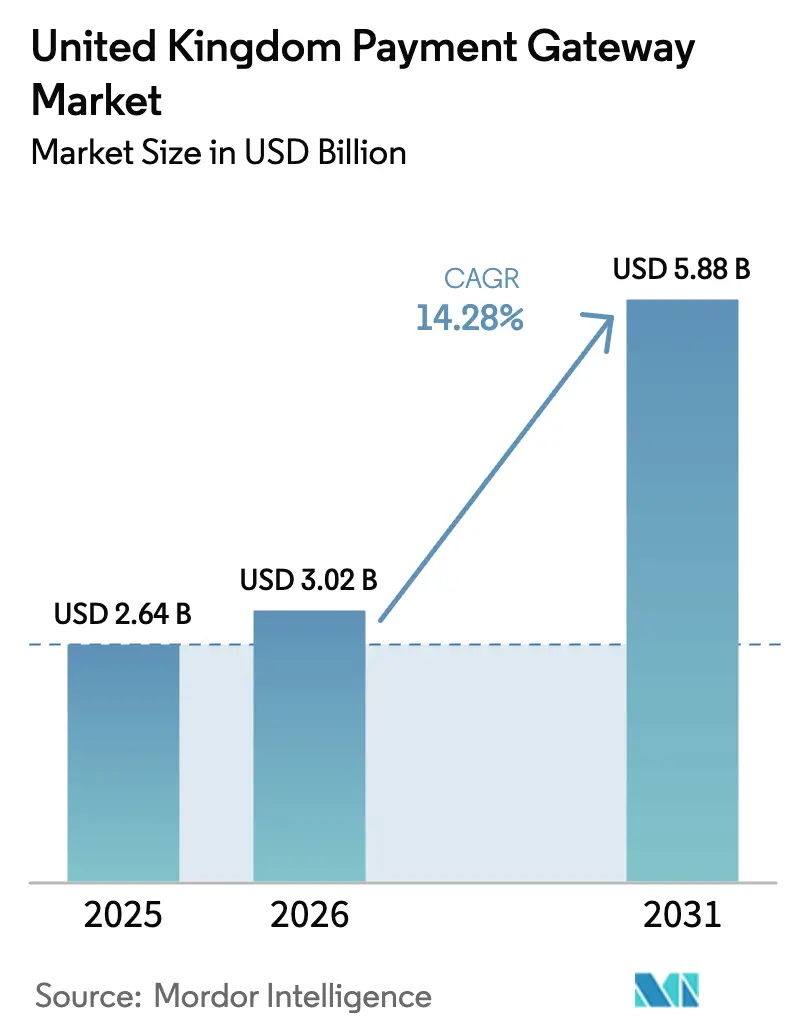

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 3.02 Billion |

| Market Size (2031) | USD 5.88 Billion |

| Growth Rate (2026 - 2031) | 14.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Payment Gateway Market Analysis by Mordor Intelligence

The United Kingdom Payment Gateway Market size in 2026 is estimated at USD 3.02 billion, growing from 2025 value of USD 2.64 billion with 2031 projections showing USD 5.88 billion, growing at 14.28% CAGR over 2026-2031. Sustained consumer preference for online and mobile shopping, the rapid roll-out of Open Banking rails and strong investor backing all align to keep expansion above 20% a year. Banks, retailers and fintechs continue to migrate to application-programming-interface (API)-based platforms that cut costs, speed settlement and improve data insights. Traditional acquirers are responding with omnichannel propositions designed to defend share against agile digital-native entrants. Risk management models are also evolving, as providers factor in compulsory reimbursement rules for Authorised Push Payment (APP) fraud and step-up investment in machine-learning fraud analytics.

Key Report Takeaways

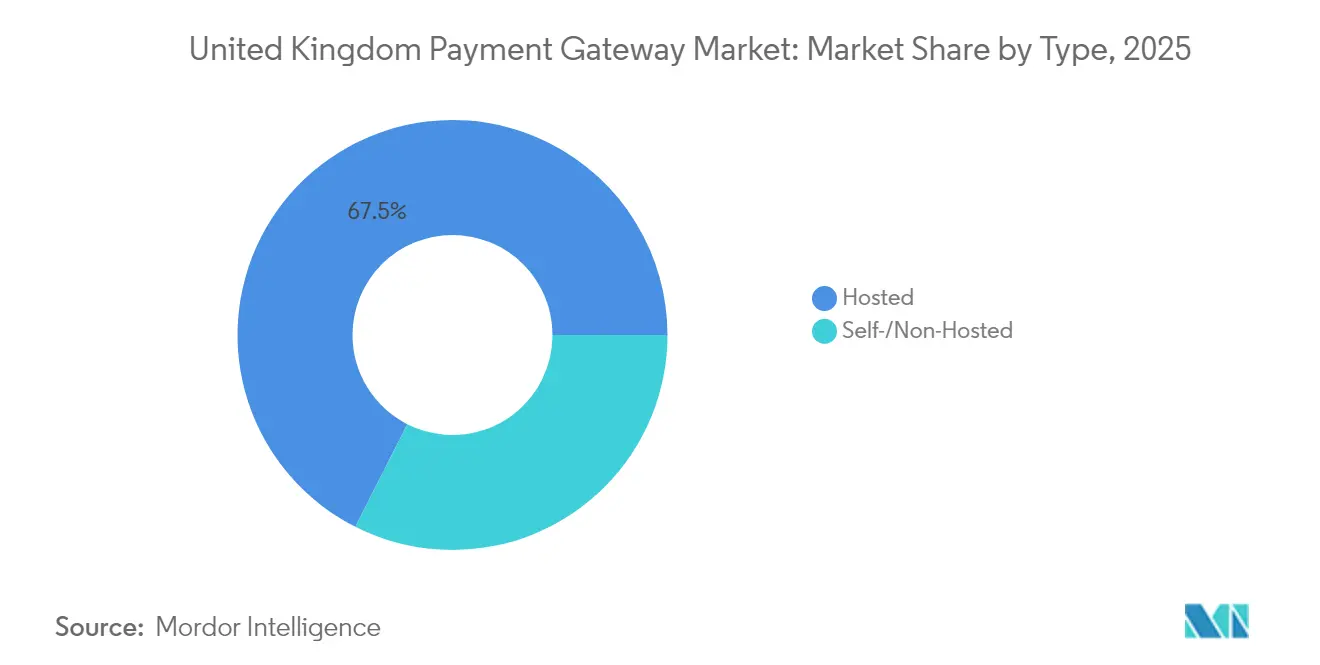

- By type, hosted solutions led with 67.54% of the UK payment gateway market share in 2025; self-hosted/non-hosted offerings post the fastest 14.32% CAGR through 2031.

- By enterprise size, large enterprises held 56.81% of the UK payment gateway market size in 2025, while the SME segment records a 12.02% CAGR to 2031.

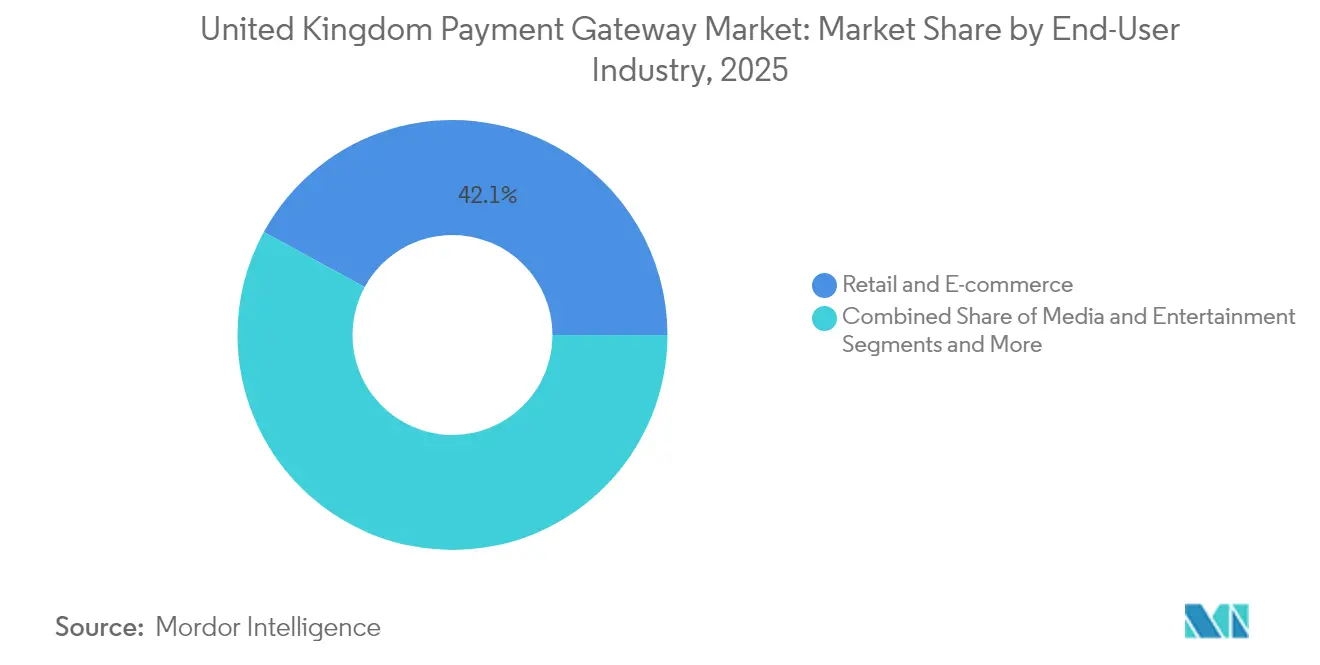

- By end-user industry, retail & e-commerce commanded 42.05% revenue share in 2025; media & entertainment expands at 15.58% CAGR over the forecast period.

- By channel, web transactions captured 54.67% of the UK payment gateway market in 2025; mobile in-app payments accelerate at 15.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Payment Gateway Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming UK E-commerce Volume Fuelled by High Broadband & 5G Adoption | +8.7% | UK-wide, with concentration in urban centers | Medium term (2-4 years) |

| Surge in Mobile-First Checkout & Digital Wallet Penetration Across Millennials | +7.6% | UK-wide, higher impact in metropolitan areas | Short term (≤ 2 years) |

| Open-Banking APIs Unlocking Low-Cost Account-to-Account Payments | +6.5% | UK-wide, with early adoption in London and major financial centers | Medium term (2-4 years) |

| Retailers' Pivot to Omnichannel & Click-and-Collect Driving Gateway Upgrades | +5.5% | UK-wide, with higher impact in retail-dense regions | Short term (≤ 2 years) |

| Growing FinTech VC Funding Creating Innovative Niche Gateways | +4.4% | Concentrated in London, Manchester, and Edinburgh | Medium term (2-4 years) |

| Increase in Contactless-Spend Limit Accelerating Card-Not-Present Transactions | +3.3% | UK-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Booming UK E-commerce Volume Fueled by High Broadband & 5G Adoption

E-commerce users in the UK are set to reach 62.1 million in 2025, and online trade already accounts for 27.9% of retail sales. Fast fibre and 5G coverage underpin user expectations for one-click, latency-free checkout, pushing merchants toward advanced gateway stacks. Eighty-four percent of citizens now shop online, spending an average EUR 4,115 (USD 4,700) annually.[1]J.P. Morgan, “2021 E-commerce Payments Trends Report: UK Country Insights,” jpmorgan.com Digital retailers in sectors such as entertainment have capitalised, with ITVX recording a 12% jump in streaming hours in 2024. As volumes shift online, merchants demand gateways that combine tokenisation, real-time fraud scoring and unified reporting to secure higher conversion.

Surge in Mobile-First Checkout & Digital Wallet Penetration Across Millennials

Half of UK adults now hold at least one mobile wallet, and proximity payments reached 14 million regular users in 2023.[2]UK Finance, “One Third of UK Adults Now Use Mobile Contactless Payments,” ukfinance.org.uk Wallets accounted for 28% of e-commerce payments in 2024, a share forecast to hit 50% by 2027. Millennials lead adoption, valuing biometric authentication and in-app loyalty integration. Payment gateways that embed token-on-file, network tokenisation and push-provisioning APIs are gaining merchant preference because they shorten checkout flows and cut chargeback risk. Heightened wallet use also amplifies data streams, letting gateways refine behavioural analytics for approval optimisation across issuers.

Open-Banking APIs Unlocking Low-Cost Account-to-Account Payments

Open Banking now serves more than 10 million active UK users, with over 600,000 new joiners each month.[3]Token.io, “Revolutionising UK Payments: 6-Year Journey of Open Banking,” token.io Account-to-account (A2A) payment requests lower merchant costs by sidestepping interchange, typically settling within seconds. The Joint Regulatory Oversight Committee has prioritised variable recurring payments, which will allow gateways to rival card-on-file subscription models for gyms, gaming and media services. Providers that integrate Open Banking rails into their orchestration layer can route transactions dynamically between A2A and cards, balancing cost efficiency, risk and customer preference at checkout.

Retailers’ Pivot to Omnichannel & Click-and-Collect Driving Gateway Upgrades

UK grocery, apparel and home-improvement chains now treat payments as a differentiator in unified commerce. ASDA’s deployment of Worldline’s platform illustrates the shift toward one back-end for store, web and mobile orders, supporting 800,000 weekly deliveries. Click-and-collect adds complexity because inventory, loyalty and refunds must synchronise in real time. Gateways that expose microservices for token vaults, installment offers and multi-acquirer routing help retailers reduce abandonment, increase acceptance and surface rich data across channels. As omnichannel interactions rise, gateways that fail to provide modular APIs risk displacement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sophisticated Fraud & Chargeback Costs Raising Gateway Compliance Spend | -5.5% | UK-wide, with higher impact in high-transaction-volume regions | Medium term (2-4 years) |

| Intensifying Price Competition Compressing Merchant Discount Rates | -4.4% | UK-wide | Medium term (2-4 years) |

| Brexit-Driven Cross-Border Fee & Scheme Rule Uncertainties | -3.3% | UK-wide, with higher impact on businesses with EU customer base | Medium term (2-4 years) |

| Consumer Data-Privacy Regulation (UK-GDPR & PSD2 SCA) Increasing Friction | -2.2% | UK-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sophisticated Fraud & Chargeback Costs Raising Gateway Compliance Spend

APP fraud generated 207,000 incidents and losses of GBP 485.2 million in 2022. From October 2024, providers must reimburse eligible victims within five days, up to GBP 85,000. Gateways now deploy layered controls device fingerprinting, behavioural biometrics and adaptive authentication to meet stricter liability while maintaining frictionless flows. The additional investment lifts unit costs and forces smaller processors to outsource risk management or partner with specialist fraud-deterrence vendors.

Intensifying Price Competition Compressing Merchant Discount Rates

Dozens of acquirers and payment service providers now vie for UK merchants, and published tariffs are converging downward. Stripe’s UK website shows card fees as low as 1.5% plus GBP 0.20. Larger retailers wield volume to negotiate custom blended rates, shrinking gateway margins further. As price becomes less of a differentiator, providers compete on value-added services such as advanced reconciliation, payout scheduling and multicurrency settlement. Smaller gateways that lack scale or niche specialisation risk margin erosion and potential consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hosted Solutions Remain Dominant While Self-Hosted Gains Momentum

Hosted gateways held 67.54% of the UK payment gateway market share in 2025, a lead founded on simplicity, outsourced PCI compliance and quick plug-in availability. Stripe, PayPal and Checkout.com collectively service tens of thousands of UK storefronts, offering embedded fraud screening, dispute handling and network tokenisation. As a result, hosted platforms captured a significant slice of the UK payment gateway market size for SMEs, which prize cost-effective onboarding and minimal maintenance.

Hosted providers are broadening value propositions with low-code terminal applications, pay-by-link and subscription management modules. Conversely, self-hosted/non-hosted solutions are scaling at a 14.32% CAGR, driven by large merchants seeking brand-controlled checkout and direct data ownership. Retail chains, airlines and subscription video platforms leverage self-hosted models to embed one-click upsell flows and to switch acquirers instantly for cost or redundancy reasons. High in-house engineering capability and the rise of cloud-native payments frameworks give these enterprises confidence to shoulder security and compliance responsibilities.

By Enterprise Size: Large Enterprises Lead While SMEs Accelerate

Large corporations accounted for 56.81% of the UK payment gateway market in 2025, reflecting their complex multi-channel infrastructures and higher average transaction values. They routinely negotiate bespoke pricing and mandate fail-over routing across multiple acquirers to minimise downtime. For these clients, gateways integrate directly into ERP, inventory and tax systems, creating data-rich dashboards that support strategic pricing decisions.

The SME cohort is expanding faster, registering a 12.02% CAGR through 2031. Government initiatives such as the British Business Bank’s finance programmes are improving digital literacy and working-capital access. Gateways that supply pre-configured plug-ins for popular web-shop builders and offer instant onboarding gain traction. The growing micro-merchant segment values blended acquiring-plus-lending bundles that turn payment data into automated cash-flow underwriting, lowering credit-risk premiums and fostering loyalty.

By End-User Industry: Retail & E-Commerce Dominates While Media & Entertainment Surges

Retail & e-commerce retained 42.05% of revenue in 2025, making it the single largest vertical in the UK payment gateway market. Fashion remains the top online retail category at 28.4% of spend, followed by electronics and groceries. Merchant appetite for seamless buy-online-pickup-in-store (BOPIS) workflows has pushed gateways to support partial authorisations, split payments and real-time inventory synchronisation. Loyalty card integration and embedded financing options such as pay-in-three increase basket conversion and average spend.

Media & entertainment leads growth at a 15.58% CAGR as UK consumers stream more content and adopt subscription bundles across music, film and gaming. ITV boosted digital ad revenue 15% in 2024, underlining the need for high-throughput, low-latency micro-payment processing. Gateways optimised for recurring billing, in-app purchases and cross-border settlement are securing long-term contracts with publishers and game studios. As creators experiment with token-gated experiences and virtual item sales, payment processors must adapt to usage-based and metered charging models.

By Channel: Web Transactions Lead While Mobile In-App Accelerates

Web-based checkouts represented 54.67% of the UK payment gateway market in 2025. Desktop and mobile browsers remain preferred for high-ticket retail, travel and B2B orders because of screen real estate and established security cues. Gateways offering server-to-server token exchanges and three-domain secure (3-DS) optimisation tools help merchants sustain high approval rates while meeting SCA mandates.

Mobile in-app flows are expanding at 15.26% CAGR, underpinned by biometric authentication and deep integration into social commerce. In-app payments already constitute 63% of total UK mobile commerce transactions. Gateways that expose software development kits (SDKs) for wallet push provisioning, instant payout and card-on-file renewal benefit from superior merchant adoption. Rich in-app data also enables granular cohort analysis, powering churn reduction and personalised offers.

Geography Analysis

London and the South-East dominate transaction value and innovation, with the capital securing 94% of UK fintech funding in Q1 2025. Access to skilled software talent and proximity to global financial institutions make the region fertile for Open Banking start-ups, account-to-account payment specialists and compliance-as-a-service providers. The concentration of venture capital accelerates the emergence of challenger gateways that focus on embedded payments for software platforms.

Northern England’s Manchester, Leeds and Newcastle form an increasingly vibrant cluster of payment technology firms. Government investment under the Northern Powerhouse initiative and lower operating costs attract companies looking to scale outside London. These hubs prioritise job creation in product engineering and client success, helping to distribute innovation geographically and increase resilience in the UK payment gateway market.

Scotland, anchored by Edinburgh, leverages its long-standing financial-services heritage to build secure, regulation-compliant gateway offerings targeting wealth management, gaming and insurance verticals. Local universities’ expertise in cryptography and data science feeds a talent pipeline for advanced fraud-detection solutions. In contrast, rural areas progress more slowly as connectivity gaps persist, though the Smart Data Roadmap promises to extend infrastructure and open data initiatives nationwide.

Competitive Landscape

The UK payment gateway market balances established acquirers and fast-growing fintech disruptors, resulting in moderate concentration. Worldpay, Barclaycard Payments and Global Payments retain extensive merchant bases, yet digital-native processors such as Stripe, Adyen and Checkout.com capture share via faster integration, transparent pricing and developer-centric tooling. In response, incumbents modernise technology stacks, launch unified commerce suites and deepen value-added services around analytics and working-capital lending.

Consolidation continues as scale becomes critical for risk investment, network negotiation and cross-border coverage. Large players form strategic alliances with cloud providers to accelerate platform migrations, while mid-tier gateways explore mergers to gain distribution or specialised capabilities in sectors like gaming or hospitality. Open Banking specialists partner with card processors to offer blended rails that dynamically route for lowest cost and highest acceptance.

Competitive intensity also derives from embedded finance, with software-as-a-service (SaaS) vendors integrating proprietary payment modules to capture margin and lock-in users. Banks counter by opening payment APIs and white-label acquiring solutions for fintech intermediaries. As new entrants exploit niches, sustained product innovation, compliance leadership and multi-rail orchestration will determine long-term positioning in the UK payment gateway market.

United Kingdom Payment Gateway Industry Leaders

PayPal Payments Private Limited

Stripe, Inc.

Amazon Payments, Inc

Mastercard, Inc.

Worldpay, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Global Payments announced a proposed acquisition of Worldpay, aiming to create the largest merchant acquirer globally, handling USD 3.5 trillion in payments.

- March 2025: Barclays initiated a major restructuring of Barclaycard Payments, allocating GBP 400 million to modernise its technology stack and partnering with Brookfield to accelerate execution.

- February 2025: The Financial Conduct Authority published a feedback statement on digital wallets, noting growth from 8% of card transactions in 2019 to 29% in 2023 and outlining potential competition remedies.

- January 2025: The Bank of England released a progress update on the digital pound, highlighting plans to support interoperable retail payments in a tokenised economy.

United Kingdom Payment Gateway Market Report Scope

A payment gateway is a technology that facilitates the processing of online transactions between customers and businesses. It acts as a bridge between the merchant’s website or app and the financial institutions involved in the transaction. Payment gateway companies in India are innovating with blockchain and Artificial Intelligence (AI) to enhance online transaction security and efficiency. Regional analysis shows a strong market presence across India, with certain areas leading due to a thriving e-commerce industry and supportive policies. This evolving landscape offers a promising future for secure and convenient online payment solutions, catering to a wide range of enterprises.

United Kingdom payment gateway market is segmented by type (hosted, non-hosted), by enterprise (small and medium enterprise (SME), large enterprise) and by end-user (travel, retail, BFSI, media and entertainment). The report offers market forecasts and size in value (USD) for all the above segments

| Hosted |

| Self-/Non-Hosted |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| Online / Web |

| Mobile In-App |

| In-store POS (Omnichannel) |

| Retail and E-commerce |

| Travel and Hospitality |

| Banking, Financial Services and Insurance (BFSI) |

| Media and Entertainment |

| Other End-user Industries |

| By Type | Hosted |

| Self-/Non-Hosted | |

| By Enterprise Size | Small and Medium Enterprises (SME) |

| Large Enterprises | |

| By Channel | Online / Web |

| Mobile In-App | |

| In-store POS (Omnichannel) | |

| By End-User Industry | Retail and E-commerce |

| Travel and Hospitality | |

| Banking, Financial Services and Insurance (BFSI) | |

| Media and Entertainment | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the UK payment gateway market?

The market is valued at USD 3.02 billion in 2026 and is forecast to reach USD 5.88 billion by 2031.

Which segment holds the largest share of UK payment gateways?

Hosted solutions lead with 67.54% market share in 2025 due to turnkey integration and outsourced compliance benefits.

How fast are mobile in-app payments growing in the UK?

Mobile in-app transactions are expanding at a 15.26% CAGR between 2026 and 2031, driven by biometric authentication and social-commerce integration.

Why is Open Banking important for UK payment gateways?

Open-Banking APIs enable low-cost account-to-account payments, helping merchants reduce interchange fees and improve settlement speed while enhancing customer choice.

What regulatory change most affects fraud management costs?

The October 2024 mandatory reimbursement scheme for APP fraud obliges payment service providers to refund victims within five days, increasing investment in fraud-prevention technology.

Are SMEs a significant growth opportunity for gateways?

Yes, the SME segment is forecast to expand at 12.02% CAGR as simplified onboarding, government finance initiatives and data-driven credit solutions boost digital payment adoption.

Page last updated on: