Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

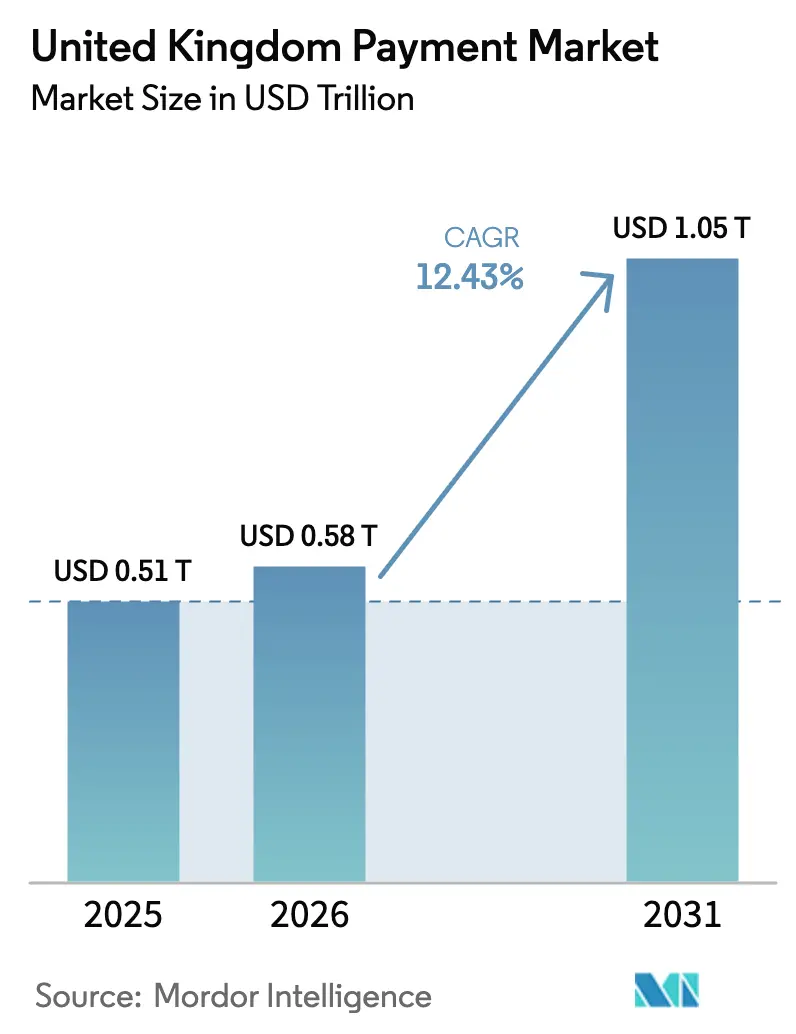

| Base Year Market Size (2025) | USD 0.51 Trillion |

| Market Size (2026) | USD 0.58 Trillion |

| Market Size (2031) | USD 1.05 Trillion |

| Growth Rate (2026 - 2031) | 12.43% CAGR |

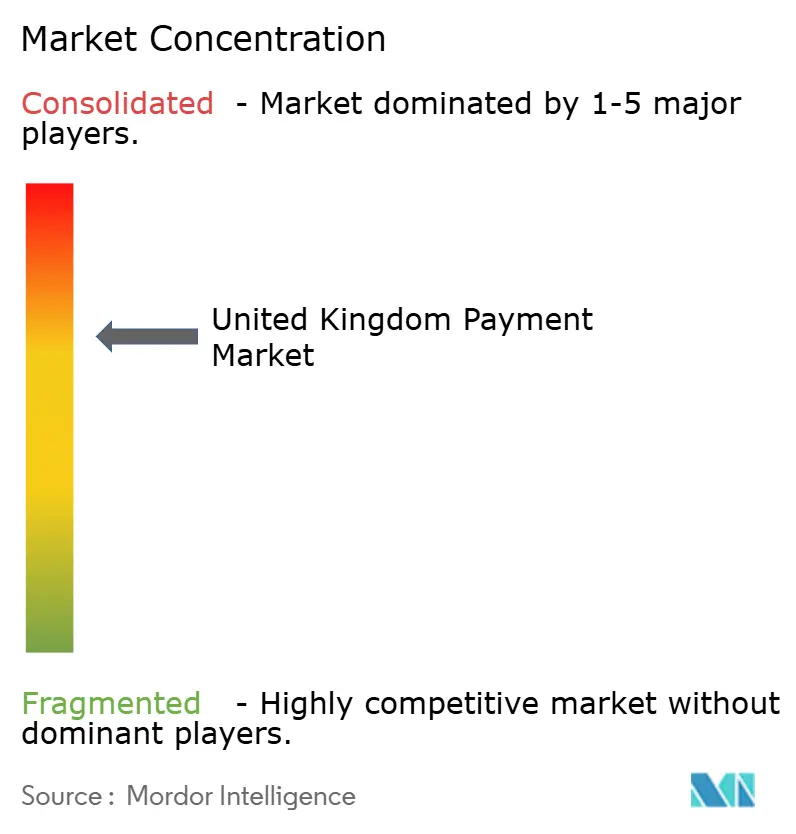

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Payment Market Analysis by Mordor Intelligence

The United Kingdom Payment Market size is projected to be USD 0.51 trillion in 2025, USD 0.58 trillion in 2026, and reach USD 1.05 trillion by 2031, growing at a CAGR of 12.43% from 2026 to 2031.

Growth rests on the steady migration from card-scheme rails to real-time account-to-account frameworks, rapid merchant adoption of embedded-finance checkouts, and sizable infrastructure spending that accompanies the potential launch of a digital pound. Instant payments already move high-value e-commerce baskets without interchange, while stricter authentication standards are driving tokenized and biometric solutions that streamline approval times. Venture capital continues to fund specialist fintechs that package credit and payment functionality into vertical software, putting competitive pressure on incumbent processors. At the same time, mandatory reimbursement rules for authorized push-payment fraud are rewriting risk-pricing models and bringing fraud-prevention tooling to the fore.

Key Report Takeaways

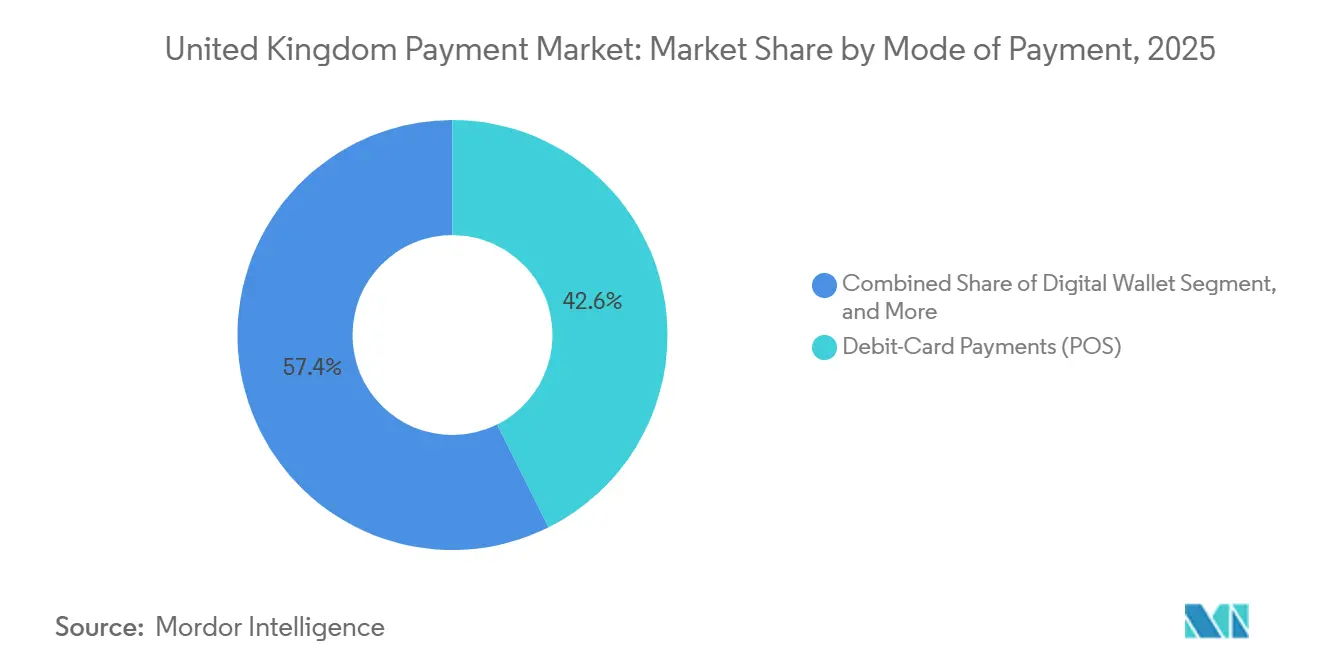

- By mode of payment, debit cards (PoS) led with a 42.62% revenue share in 2025 of the United Kingdom payment market, whereas account-to-account online payments are projected to advance at a 13.63% CAGR to 2031.

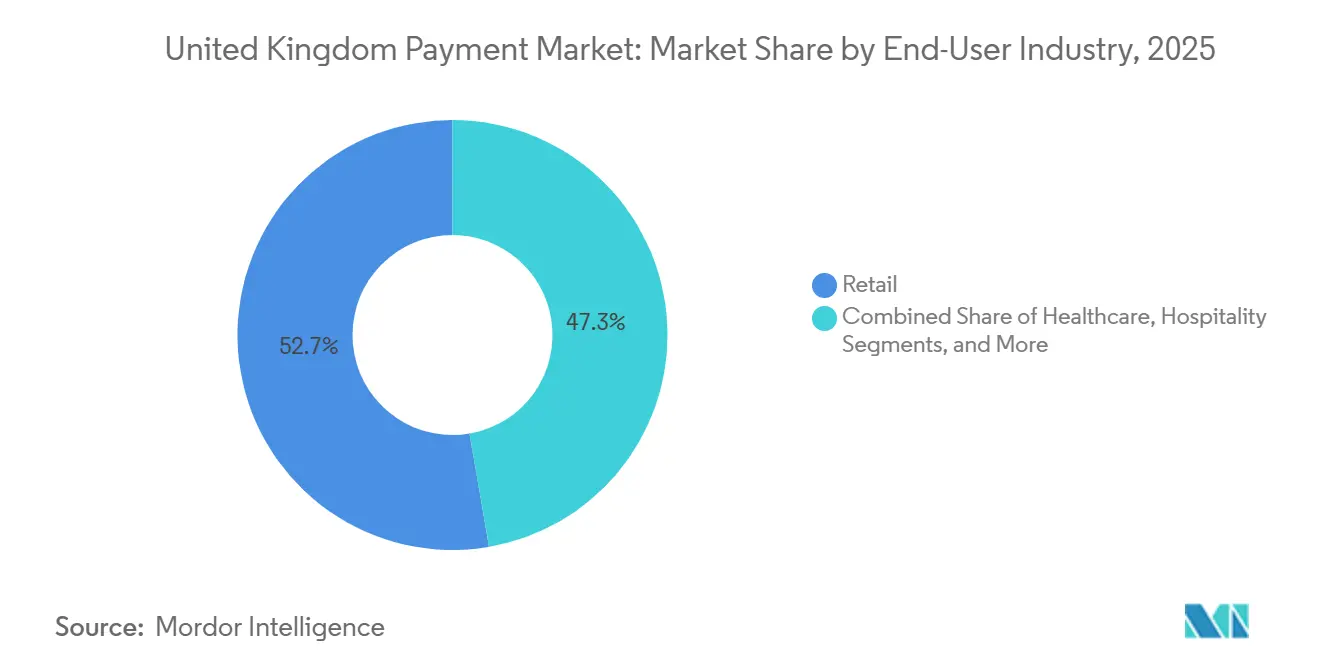

- By end-user industry, retail held 52.72% of the United Kingdom payment market share in 2025, while healthcare is expanding at a 13.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Payment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open-banking-enabled A2A instant payments | +3.2% | National, concentrated in London and Manchester | Medium term (2-4 years) |

| Strong Customer Authentication accelerating tokenized and biometric solutions | +2.1% | National, EU spillover compliance | Short term (≤2 years) |

| FinTech funding boom enabling BNPL and embedded-finance expansion | +2.4% | National, London-centric venture activity | Medium term (2-4 years) |

| Digital-pound CBDC consultation catalyzing infrastructure investment | +1.8% | National, early pilots in fintech hubs | Long term (≥4 years) |

| Raised contactless limit boosting NFC penetration | +1.5% | National, higher adoption in urban centers | Short term (≤2 years) |

| Omnichannel retail demand for unified-commerce platforms | +1.5% | National, led by grocery and fashion retailers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Open-Banking-Enabled A2A Instant Payments

Merchants are embracing open-banking rails to sidestep interchange fees, and more than 7 million consumers had granted at least one consent by 2025.[1]Financial Conduct Authority, “Open Banking Adoption 2025,” fca.org.uk Variable recurring payments are particularly useful for subscription billing, cutting involuntary churn tied to card-on-file failures. GoCardless processed 68% more A2A volume year over year in 2025, with average basket sizes running 22% above card equivalents. Regulatory confirmation that overlay service providers face lighter capital requirements than traditional institutions has lowered market entry barriers and accelerated product rollout.[2]Payment Systems Regulator, “Overlay Services Framework 2025,” psr.org.uk

Strong Customer Authentication Accelerating Tokenized and Biometric Solutions

Reinforced SCA standards obliged issuers to reject static-CVV e-commerce transactions from January 2024. Tokenized credentials already secure more than 60% of U.K. web card payments, but they can slow checkout flows. Mastercard’s biometric pilot with NatWest combined device-binding tokens and on-device fingerprint or facial verification, trimming approval times to 1.8 seconds while keeping fraud below 0.02%.[3]Mastercard, “Biometric Authentication Pilot 2025,” mastercard.com This performance advantage is driving issuers toward pervasive device-binding strategies.

FinTech Funding Boom Enabling BNPL and Embedded-Finance Expansion

UK fintech fund-raising reached GBP 8.1 billion (USD 10.3 billion) in 2024 as venture investors chased installment-lending and embedded-finance platforms. Klarna used its Series F extension to roll out QR-code BNPL in 12,000 stores, challenging point-of-sale credit cards. FCA affordability rules, including a 30-day cooling-off period, now favor well-capitalized lenders, accelerating consolidation while reinforcing growth prospects for market leaders.

Digital-Pound CBDC Consultation Catalyzing Infrastructure Investment

Although issuance remains undecided, the Bank of England consultation has already unlocked processor outlays on programmable money. Worldpay earmarked GBP 45 million (USD 57 million) in 2025 to code smart-contract modules compatible with distributed-ledger architectures. Treasury guidance clarified that a digital pound would coexist with bank deposits, reducing existential risk but rewarding early adopters able to orchestrate conditional payments at launch.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating APP fraud and reimbursement costs under new PSR rules | -1.9% | National, acute in digital-banking channels | Short term (≤2 years) |

| Legacy core-banking systems limiting real-time settlement | -1.3% | National, concentrated in tier-2 banks | Long term (≥4 years) |

| Post-Brexit interchange-fee uplift increasing merchant costs | -0.8% | National, cross-border merchants most affected | Medium term (2-4 years) |

| Cost-of-living crisis curtailing transaction values | -1.1% | National, pronounced in discretionary retail | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Escalating APP Fraud and Reimbursement Costs Under New PSR Rules

APP fraud losses reached GBP 485 million in 2024, forcing banks to reimburse most victims within five business days. Extra provisions, exceeding GBP 200 million, diverted capital from product innovation and raised the cost of instant payments. Lloyds reduced APP fraud by 34% after deploying confirmation-of-payee checks, but the fix added just over two seconds to each transfer. This friction threatens to push low-value transfers to nonbank channels.

Legacy Core-Banking Systems Limiting Real-Time Settlement

While the Faster Payments Service processed more than four billion transfers in 2024, many tier-2 banks still post funds in hourly or bi-hourly batches. Starling’s GBP 18 million (USD 23 million) cloud-native core migration delivers sub-second finality, but legacy banks face costs five to seven times higher due to technical debt. The resulting two-speed market hampers ubiquity of the United Kingdom payment market’s real-time promise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: A2A Rails Reshape Channel Economics

Account-to-account online payments are projected to expand at a 13.63% CAGR from 2026 to 2031, the fastest trajectory among all modes. Debit cards held a 42.62% United Kingdom payment market share in 2025, but growth has plateaued as merchants prefer real-time rails to avoid interchange fees. The United Kingdom payment market size for credit-card transactions is pressured by new affordability checks that extend issuance timelines. Digital wallets continue to gain ground in both e-commerce and physical venues, buoyed by integrations into small-merchant platforms.

Cash has fallen below 15% of retail payment volumes, reflecting branch and ATM closures. Cash-on-delivery for online purchases is now restricted to specific electronics categories, and even there platform rules are shrinking its use. Direct debits and invoice settlements remain common in B2B, yet they add little to consumer volumes. A regulator estimate pegs the annual subsidy required to preserve universal cash acceptance at GBP 2 billion, making an accelerated transition toward digital-only commerce likely.

By End-User Industry: Healthcare Digitization Unlocks Payment Innovation

Retail accounted for 52.72% of 2025 transaction value, yet its growth is moderating as online grocery nears maturity. Healthcare is forecast to advance at a 13.82% CAGR through 2031, supported by unified patient-payment portals. The National Health Service mandate that all trusts adopt open-banking gateways by March 2027 has spurred procurement spending worth roughly GBP 120 million.

Private providers adopted embedded checkouts faster still; Bupa’s deployment of payment links lowered patient collection times from 14 days to two hours and cut back-office costs by 35%. Hospitality venues are experimenting with QR-code pay-at-table solutions that shave eight minutes off peak service times, underscoring how vertical software adds operating leverage while expanding the United Kingdom payment market.

Geography Analysis

London and the South East account for 48% of the United Kingdom payment market, driven by higher smartphone penetration and a dense merchant network. Scotland and Wales are catching up, with 5G coverage reaching 78% of the population in 2025, enabling seamless mobile authentication even in formerly low-signal regions. Northern Ireland merchants handle dual-currency flows, with euro-denominated cards representing 31% of transactions in border towns, driving demand for multi-currency processors.

A regulator mandate requiring 95% of citizens to live within one mile of a cash point has proven difficult in rural areas, accelerating the take-up of cash-back-at-POS services that charge GBP 0.50–GBP 1.00 per withdrawal. Urban retailers are increasingly cashless as 22% of London merchants no longer accept physical currency, citing an average handling cost of 1.8%. Regional adoption curves therefore hinge on broadband availability, smartphone usage, and cost-of-cash economics.

Despite a single legal framework, payment behavior varies with local demographics. Affluent commuter belts around London show the highest penetration of biometric-authenticated transactions, while university towns such as Oxford and Cambridge observe early adoption of BNPL for tuition-adjacent services. Coastal tourist hubs depend heavily on point-of-sale QR wallets that cater to transient visitors unfamiliar with local bank-link schemes. These nuances underscore the geographic granularity embedded in the United Kingdom payment market size forecasts.

Competitive Landscape

The top five merchant acquirers, Worldpay, Barclays Payments, Adyen, Checkout.com, and Lloyds Cardnet, collectively controlled most of the processing value in 2025. No single operator exceeded a major share, creating a moderately concentrated structure where merchants routinely multihome. The 2024 ban on exclusivity clauses in contracts longer than 12 months further lowered switching costs, prompting processors to differentiate on vertical software and real-time data.

Adyen’s unified-commerce contracts with Burberry and JD Sports proved that consolidated data can shrink finance headcount by one-fifth, while Revolut processed GBP 1.2 billion in its first quarter of merchant acquiring, signaling rapid scale potential for challenger banks. Toast’s September 2025 entry emphasized the power of embedded payments inside specialized workflow software.

Cross-border services remain a white-space opportunity. Checkout.com’s Singapore license enables U.K. merchants to settle in 18 Asian currencies, eliminating 2-3 percentage-point FX margins. Meanwhile, processors are racing to integrate variable recurring payments once the legal framework is finalized, as early movers expect to capture subscription-economy merchants dissatisfied with legacy mandate mechanics. The United Kingdom payment industry therefore balances scale incumbents with agile disruptors, each pursuing technology-led differentiation.

United Kingdom Payment Industry Leaders

Stripe, Inc.

PayPal Holdings, Inc.

Worldpay Group Limited (Fidelity National Information Services, Inc.)

Amazon Payments, Inc.

Mastercard Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Visa invested GBP 200 million (USD 254 million) to expand its London data center, lifting capacity to 100,000 transactions per second and cutting cross-border latency by 40%.

- December 2025: Mastercard and NatWest launched a biometric card pilot for 10,000 customers, raising average tap-payment values by 27%.

- November 2025: Revolut obtained a U.K. banking license, unlocking deposit insurance and direct Bank of England settlement access.

- October 2025: Adyen acquired a minority stake in Banked, integrating instant A2A transfers into its platform.

United Kingdom Payment Market Report Scope

The United Kingdom Payments Market Report is Segmented by Mode of Payment (Point of Sale [Debit Card, Credit Card, Account-to-Account, Digital Wallet, Cash, and More], Online Sale [Debit Card, Credit Card, Account-to-Account, Digital Wallet, Cash-on-Delivery, and More]), and End-User Industry (Retail, Entertainment, Hospitality, Healthcare, Other). Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| Point-of-Sale | Debit-Card Payments |

| Credit-Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash | |

| Other Point-of-Sale Payment Mode | |

| Online Sale | Debit-Card Payments |

| Credit-Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online-Sales Payment Mode |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Other End-User Industries |

| By Mode of Payment | Point-of-Sale | Debit-Card Payments |

| Credit-Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point-of-Sale Payment Mode | ||

| Online Sale | Debit-Card Payments | |

| Credit-Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online-Sales Payment Mode | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the United Kingdom payment market in 2026?

The market stands at USD 0.58 billion in 2026 and is forecast to reach USD 1.05 billion by 2031, growing at a 12.43% CAGR through the forecast period.

Which payment mode is expanding fastest?

Account-to-account online transfers are projected to grow at a 13.63% CAGR between 2026 and 2031.

Which end-user sector shows the highest growth?

Healthcare payments are advancing at a 13.82% CAGR through 2031 on the back of unified patient-payment portals.

How concentrated is the processing landscape?

The top five acquirers hold most of the volume, indicating moderate concentration with room for challenger growth.

What regulatory change most affects fraud liability?

Mandatory reimbursement rules for authorized push-payment fraud introduced in October 2024 shift liability to sending institutions, raising compliance costs.

Page last updated on: