Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

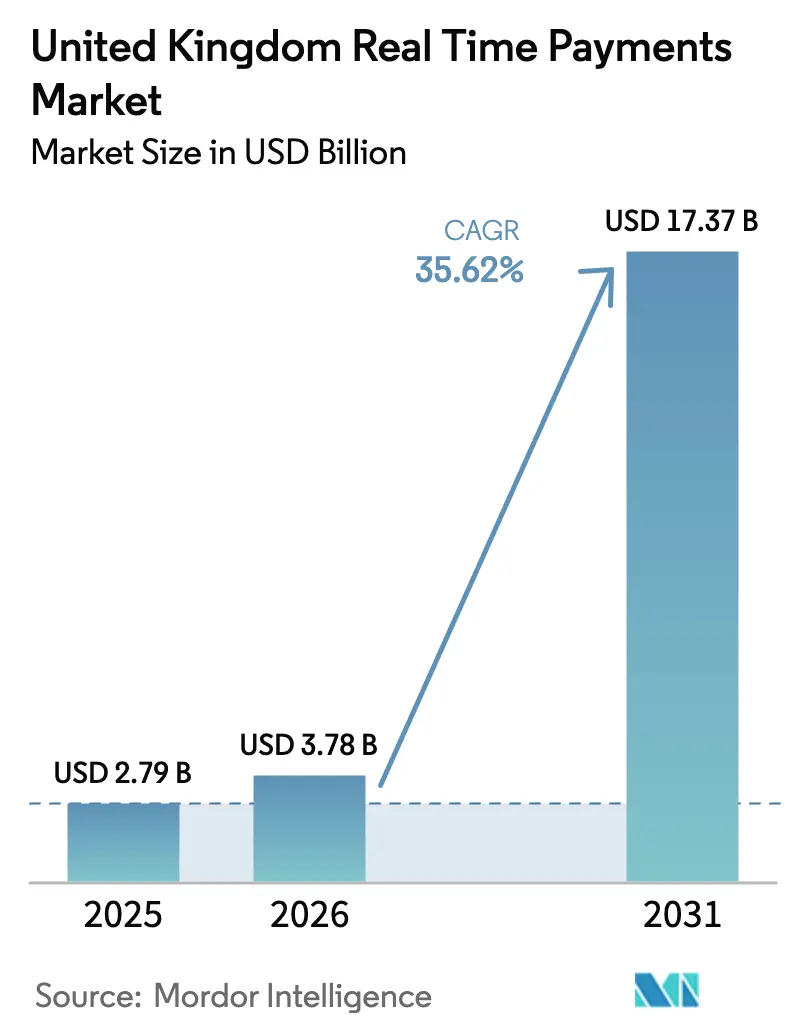

| Base Year Market Size (2025) | USD 2.79 Billion |

| Market Size (2026) | USD 3.78 Billion |

| Market Size (2031) | USD 17.37 Billion |

| Growth Rate (2026 - 2031) | 35.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Real Time Payments Market Analysis by Mordor Intelligence

The United Kingdom real time payments market size in 2026 is estimated at USD 3.78 billion, growing from 2025 value of USD 2.79 billion with 2031 projections showing USD 17.37 billion, growing at 35.62% CAGR over 2026-2031. Momentum comes from the Faster Payments Service (FPS), which processed more than 5 billion transactions in 2024. The recently unveiled National Payments Vision promises simplified regulation and fresh infrastructure investments that aim to accelerate adoption. Cloud-first deployments, mandatory fraud-reimbursement rules, and the arrival of Variable Recurring Payments (VRPs) are reshaping business models, while ISO 20022 and the New Payments Architecture open new data-driven revenue streams. Fintech challengers, incumbent banks, and global technology providers are rapidly expanding partnerships to differentiate on speed, resilience, and user experience.

Key Report Takeaways

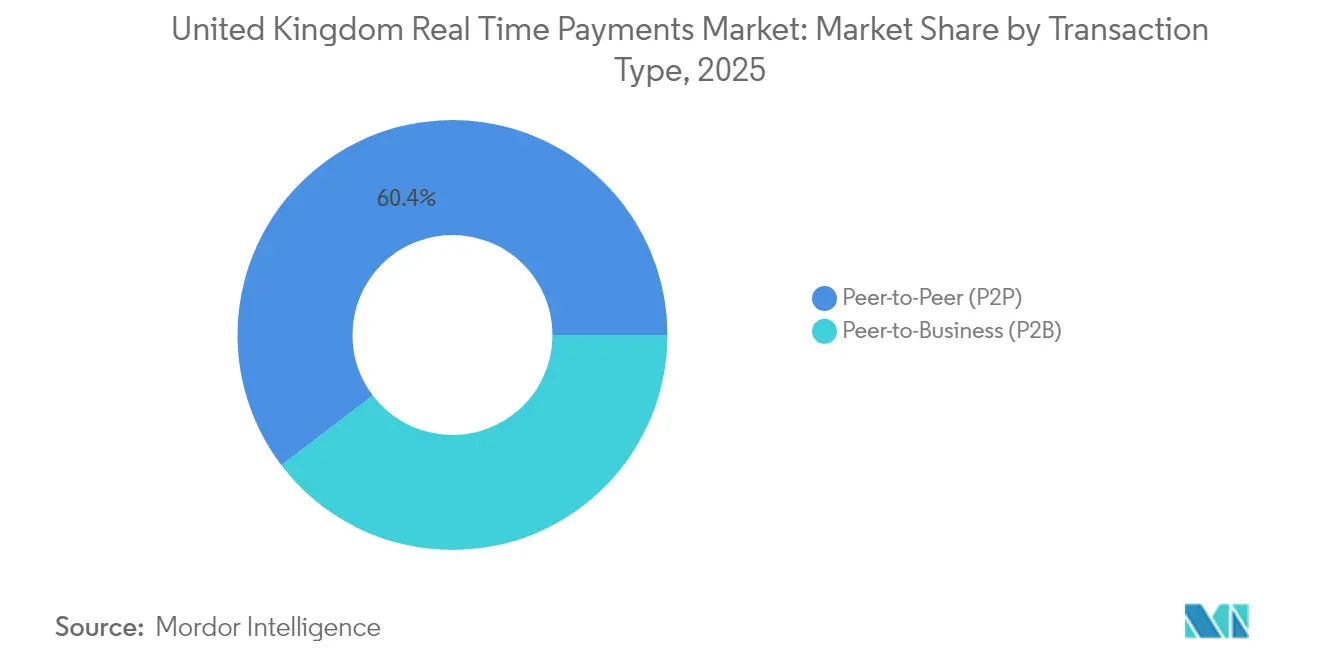

- By transaction type, P2P held 60.35% of the United Kingdom real time payments market share in 2025 while P2B is projected to expand at a 37.15% CAGR through 2031.

- By component, platform and solution offerings accounted for 70.25% share of the United Kingdom real time payments market size in 2025, whereas services are set to grow at 36.05% CAGR to 2031.

- By deployment mode, cloud captured 74.10% share of the United Kingdom real time payments market size in 2025 and is projected to advance at a 38.7% CAGR through 2031.

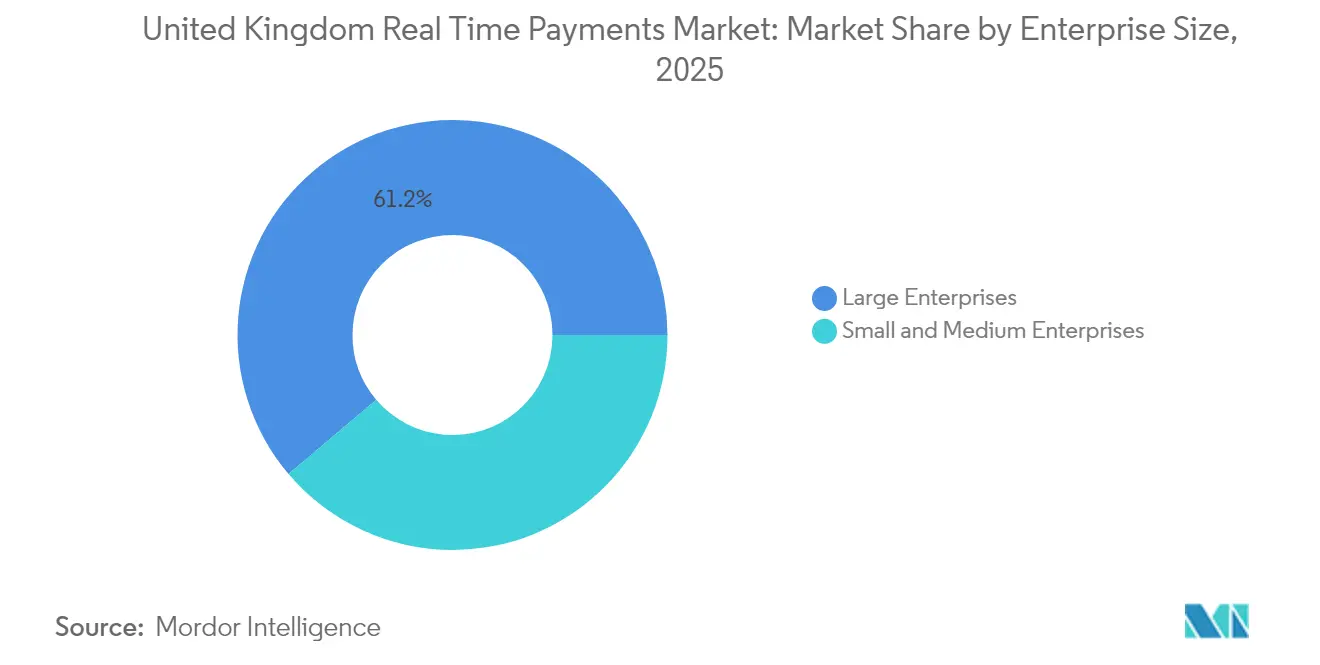

- By enterprise size, large enterprises led with 61.20% share in 2025, but SMEs are forecast to post the fastest 36.4% CAGR to 2031.

- By end-user industry, retail and e-commerce commanded 41.35% of the United Kingdom real time payments market in 2025, while the government and public sector is expected to grow at a 43.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Faster-Payments infrastructure maturity | +11.0% | National, with spillover effects to international payment corridors | Medium term (2-4 years) |

| Rising mobile-internet penetration | +9.2% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| Decline of cash & cheques drives the market | +7.3% | National, with pronounced effect in retail and service sectors | Medium term (2-4 years) |

| Open-Banking variable-recurring-payments (VRP) rollout | +5.5% | National, with initial concentration in financial services and utilities | Short term (≤ 2 years) |

| Gen-Z uptake of bank-branded social-payment apps | +3.7% | National, with higher concentration in metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Faster-Payments Infrastructure Maturity Accelerates Market Growth

Transactions settle within seconds instead of days, with 5 billion processed in 2024, a 15% annual rise. Reliability reached 99.9% uptime that year, encouraging overlay innovations such as Request to Pay and Confirmation of Payee. Raising the single-payment ceiling to GBP 1 million (USD 1.27 million) in 2024 expanded business-to-business use cases. Network effects amplify adoption as every new participant increases overall utility.

Rising Mobile-Internet Penetration Creates Payment Behaviour Shift

Eighty-seven percent of UK adults bank online. Digital-wallet share of card transactions rose from 8% in 2019 to 29% in 2023. Banks are enhancing mobile apps to integrate FPS, while higher contactless limits raise expectations for instant settlement. As merchants align checkout options with consumer demands, momentum feeds compound growth.

Decline of Cash and Cheques Creates Digital Payment Opportunity

Cash use fell from 51% of all payments in 2013 to 12% in 2023. Cheque volumes shrink more than 15% annually. A digital pound is being explored to keep central bank money relevant. [1]Bank of England, “Progress update: The digital pound and the payments landscape,” bankofengland.co.uk As businesses migrate from physical instruments, real-time payments offer the immediacy of cash without handling risks.

Open-Banking Variable-Recurring-Payments Revolutionise Subscription Economy

The Payment Systems Regulator will extend VRPs to regulated services, utilities, and government entities in Q3 2024. [2]Payment Systems Regulator, “RP24/1 Expanding VRP response to call for views,” psr.org.uk Consumers can authorise variable amounts and frequencies, improving flexibility over direct debits. Thirty-one firms already back the initiative. Coupled with ISO 20022 data richness, VRPs create new revenue opportunities around usage-based billing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating authorised push-payment fraud | -5.5% | National, with higher impact in metropolitan areas | Short term (≤ 2 years) |

| Legacy-core modernisation delays at Tier-2 banks | -3.7% | National, with concentration in regional banking centers | Medium term (2-4 years) |

| Slow ISO 20022 migration among indirect FPS participants | -1.8% | National, with greater impact on smaller financial institutions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Authorised Push-Payment Fraud Undermines Consumer Confidence

APP fraud losses hit GBP 459.7 million (USD 584 million) across 232,429 cases in 2023. [3]UK Finance, “Authorised Push Payment Fraud Information,” ukfinance.org.uk Mandatory reimbursement, effective October 2024, caps refunds at GBP 85,000 (USD 108,000). While the rule protects victims, compliance costs may slow provider innovation.

Legacy-Core Modernisation Delays Create Competitive Disadvantage

Replacing core systems costs Tier-2 banks GBP 50–150 million (USD 63–190 million), prompting project deferrals. The gap widens as ISO 20022 and the New Payments Architecture demand real-time readiness that legacy stacks cannot easily provide. Customers of agile institutions enjoy features unavailable to lagging competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2P Dominates While P2B Accelerates

P2P accounted for 60.35% of the United Kingdom real time payments market in 2025. The segment benefits from mobile-first lifestyle shifts, chat-embedded transfers, and zero-cost settlement. Banking brands cultivate loyalty by pairing social features with bank-grade security, translating engagement into multi-product cross-sell opportunities. Gen-Z adoption and rising digital-wallet penetration reinforce network effects that keep P2P in a leadership position.

P2B is forecast to compound at 37.15% between 2026 and 2031, outpacing every other segment. Visa A2A and expanding VRPs lower acceptance costs compared with cards, creating fresh value for merchants. E-commerce platforms integrating account-to-account checkout anticipate higher conversion rates, fewer chargebacks, and next-day cash availability. As billers migrate from direct debit to VRP, payment failures fall, supporting working-capital optimisation.

By Component: Solutions Lead While Services Gain Momentum

Platform and solution offerings held 70.25% share of the United Kingdom real time payments market size in 2025. Banks invest heavily in clearing engines, fraud analytics, and open-API layers that permit real-time orchestration. ISO 20022 compliance demands richer structured data, incentivising upgrades of message hubs and data warehouses.

Services are predicted to grow 36.05% CAGR to 2031, reflecting rising demand for implementation, migration, and managed-operations expertise. Institutions outsourcing transformation de-risk projects and accelerate time-to-value. Providers differentiate on reference architectures, sandbox testing, and post-go-live optimisation support.

By Deployment Mode: Cloud Dominance Reshapes Infrastructure Strategy

Cloud deployments accounted for 74.10% of the United Kingdom real time payments market share in 2025. Elastic capacity smooths peak traffic spikes and shortens innovation cycles. Continuous integration pipelines allow rapid iteration on fraud models and customer-experience features without service downtime. The United Kingdom real time payments market size tied to cloud solutions is projected to expand at 38.7% CAGR, aligning with board-level mandates to convert fixed hardware costs into variable operating expenditure.

On-premise systems persist where data-sovereignty demands prevail, yet hybrid models increasingly offload reporting, analytics, and disaster-recovery workloads to public cloud zones. Cloud providers attain a growing portfolio of financial-services certifications, mitigating earlier reservations about multitenancy security.

By Enterprise Size: Large Enterprises Lead While SMEs Rapidly Adopt

Large enterprises maintained 61.20% of overall value in 2025, using real-time payments to optimise treasury and shrink days-sales-outstanding. Straight-through bulk payments and intra-day liquidity dashboards allow corporates to refine working-capital cycles and negotiate early-payment discounts.

SMEs will post a 36.4% CAGR from 2026 to 2031 as platform providers democratise access through low-code integrations and transparent pay-per-use pricing. Switching from cheques to instant settlement saves the average small business around USD 4,500 annually, an amount immediately visible on the bottom line. The United Kingdom real time payments industry ecosystem is therefore targeting differentiated bundles such as accounting-software plug-ins and real-time invoice reconciliation.

By End-User Industry: Retail Leads While Government Sector Surges

Retail and e-commerce captured 41.35% share in 2025. Account-to-account checkout reduces card-scheme fees, while instant refunds lift customer satisfaction. Loyalty apps embed instant payout vouchers for returns, encouraging repurchase.

The government and public sector is forecast to grow at 43.6% CAGR, propelled by the digital-service roadmap that targets at least 50 high-volume services reaching a “great” standard by 2025. Immediate disbursement of welfare and emergency relief improves citizen outcomes. Rich ISO 20022 data supports automated reconciliation in tax and licensing workflows, streamlining back-office processing.

Geography Analysis

The United Kingdom real time payments market continues to benefit from a mature national clearing layer. FPS handled 5 billion transactions in 2024, supported by 24/7 availability and a GBP 1 million limit. However, Finastra projects the UK will slip from 9th to 17th globally in account-to-account volumes by 2027, highlighting intensifying international competition. The National Payments Vision seeks to counteract this trajectory with a Payments Vision Delivery Committee that will publish an integrated roadmap by Q2 2025.

London anchors ecosystem collaboration among fintechs, regulators, and incumbent banks. The Bank of England’s move to ISO 20022 for RTGS/CHAPS in 2023 extended richer data across high-value payment rails. Regional adoption is now broadly uniform, aided by ubiquitous mobile-banking coverage. Exploration of a retail central-bank digital currency could introduce programmable features that complement, rather than cannibalise, existing real-time rails.

Looking north, Scotland’s fintech cluster collaborates with local universities on risk-analytics engines tuned for instant payment fraud patterns. Wales promotes open-banking accelerators that help rural SMEs link real-time receipts to cash-flow forecasting dashboards. Northern Ireland leverages UK Fintech Growth Programme grants to pilot cross-border instant payments with Ireland, an approach that might mitigate post-Brexit settlement frictions.

Forward-looking public infrastructure, including a planned overlay directory for confirming payee and a national QR standard, aims to keep the United Kingdom real time payments market competitive despite aggressive rollouts elsewhere in Europe and Asia.

Competitive Landscape

The United Kingdom real time payments market is moderately concentrated. Legacy banks command sizeable customer bases, yet challengers capture share through digital user journeys and fee-light propositions. Revolut reported USD 1 billion profit in 2024 and is preparing to launch a UK bank, adding lending and mortgage products. Monzo, Starling, and Tide leverage open-banking APIs for embedded-finance propositions that appeal to freelancers and small traders.

Strategic moves centre on four levers:

1. Partnership: Barclays joined a multi-bank initiative to standardise pain.001 request-for-transfer messages, easing ISO 20022 rollouts.

2. Platform extension: Visa will release Visa A2A to support account-to-account retail payments in early 2025.

3. Fraud deterrence: PSPs enhance behavioural analytics to comply with the mandatory APP reimbursement scheme without eroding margins.

4. Ecosystem play: Stripe launched Pay-by-Bank powered by UK Open Banking, reducing merchant costs and accelerating settlement.

White-space opportunities involve value-added data layers such as instant invoice creation, liquidity dashboards, and credit-scoring engines that ingest ISO 20022 enriched messages. Providers able to aggregate these services around real-time rails are positioned to capture premium yield as commoditisation pressures grow on core processing fees.

United Kingdom Real Time Payments Industry Leaders

ACI Worldwide Inc.

Fiserv Inc.

PayPal Holdings Inc.

Mastercard Inc. (Vocalink)

Google LLC (Google Pay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Revolut reported USD 1 billion profit for 2024 and is progressing toward a full UK banking licence, enabling loans, overdrafts, and mortgages, thus broadening its revenue base and intensifying competition with universal banks.

- April 2025: The Bank of England published analysis on artificial intelligence in payments, urging robust risk-management frameworks so institutions can harness productivity gains without compromising system stability.

- March 2025: Barclays coordinated industry efforts to simplify ISO 20022 adoption through a new request-for-transfer rulebook that clarifies legal liabilities for pain.001 messages, reducing ambiguity for indirect participants.

- January 2025: The Financial Conduct Authority and Payment Systems Regulator outlined next steps for VRPs, reinforcing consumer control and aiming for 2025 availability across utilities, government, and financial services.

United Kingdom Real Time Payments Market Report Scope

Real-time payments are instant or immediate payments and are defined by the Euro Retail Payments Board (ERPB) as electronic retail payment solutions that are available 24/7/365. Immediate payments enable businesses and consumers to make and receive payments in real-time, providing convenience, speed, and faster availability of funds.

The UK real-time payments market is Segmented by Transaction Types (P2B, B2B, and P2P)

By Transaction Type

| Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) |

By Component

| Platform / Solution |

| Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-User Industry

| Retail and E-Commerce |

| BFSI |

| Utilities and Telecom |

| Healthcare |

| Government and Public Sector |

| Other End-user Industries |

| By Transaction Type | Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) | |

| By Component | Platform / Solution |

| Services | |

| By Deployment Mode | Cloud |

| On-Premise | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Utilities and Telecom | |

| Healthcare | |

| Government and Public Sector | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the United Kingdom real time payments market?

The market is valued at USD 3.78 billion in 2026 and is projected to reach USD 17.37 billion by 2031.

Which transaction type leads the market?

Peer-to-Peer transfers lead with 60.35% share in 2025, driven by widespread mobile-app adoption.

How fast is cloud deployment growing in UK real-time payments?

Cloud-based solutions are expected to advance at a 38.7% CAGR over 2026-2031.

Why are Variable Recurring Payments important?

VRPs enable flexible subscription payments beyond fixed direct debits, opening new revenue models for utilities, fintechs, and government.

What regulation protects consumers from APP fraud losses?

A mandatory reimbursement scheme effective October 2024 requires sending PSPs to refund victims up to GBP 85,000, sharing costs with receiving PSPs.

Which industry segment shows the fastest growth outlook to 2031?

The government and public sector segment is forecast to expand at a 43.6% CAGR over 2026-2031 due to digital-service initiatives and instant benefit disbursement.

Page last updated on: