Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

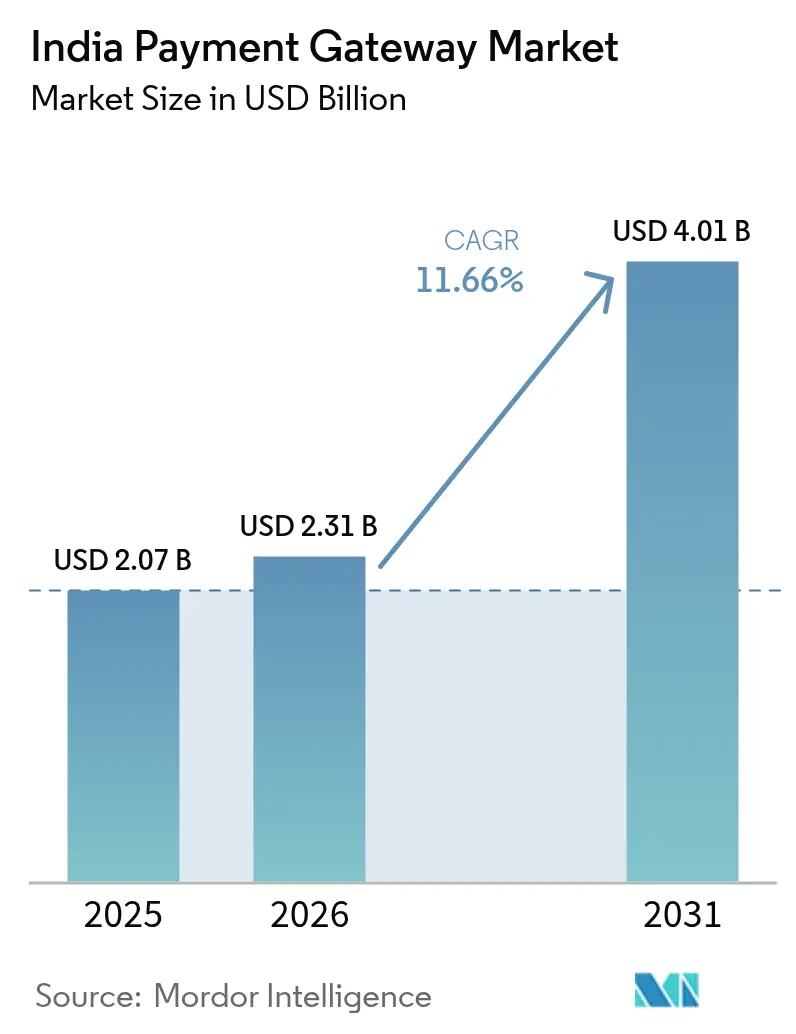

| Base Year Market Size (2025) | USD 2.07 Billion |

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 4.01 Billion |

| Growth Rate (2026 - 2031) | 11.66% CAGR |

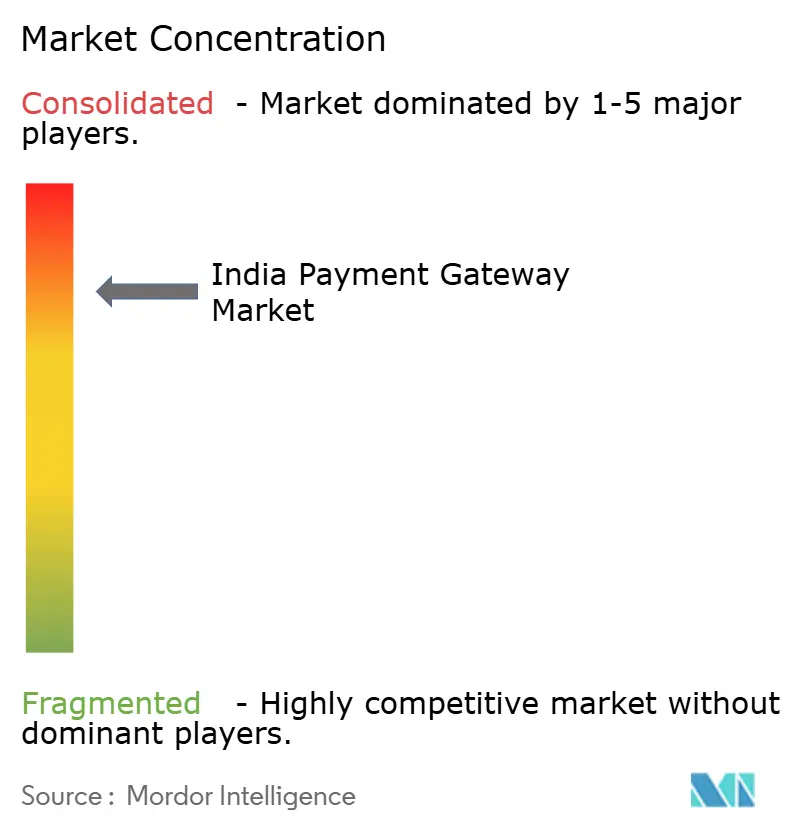

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Payment Gateway Market Analysis by Mordor Intelligence

The India payment gateway market size was valued at USD 2.07 billion in 2025 and estimated to grow from USD 2.31 billion in 2026 to reach USD 4.01 billion by 2031, at a CAGR of 11.66% during the forecast period (2026-2031). This expansion aligns with the Reserve Bank of India’s (RBI) Payment Digitization Index, which quadrupled to 417.88 between March 2018 and September 2023, signaling deep-rooted digital infrastructure maturity. Robust real-time payments growth, cloud-native technology adoption, and government-backed digital public infrastructure collectively underpin sustained transaction volume acceleration. Payment gateway providers are embedding value-added services-merchant lending, analytics, and cross-border payout orchestration offset zero-MDR pressures and unlock fresh revenue streams. Intensifying regulatory oversight is simultaneously raising compliance costs while fostering confidence among larger enterprises seeking resilient partners. International expansion of Unified Payments Interface (UPI) rails is further widening the total addressable pool for the India payment gateway market by integrating remittance corridors at materially lower costs.

Key Report Takeaways

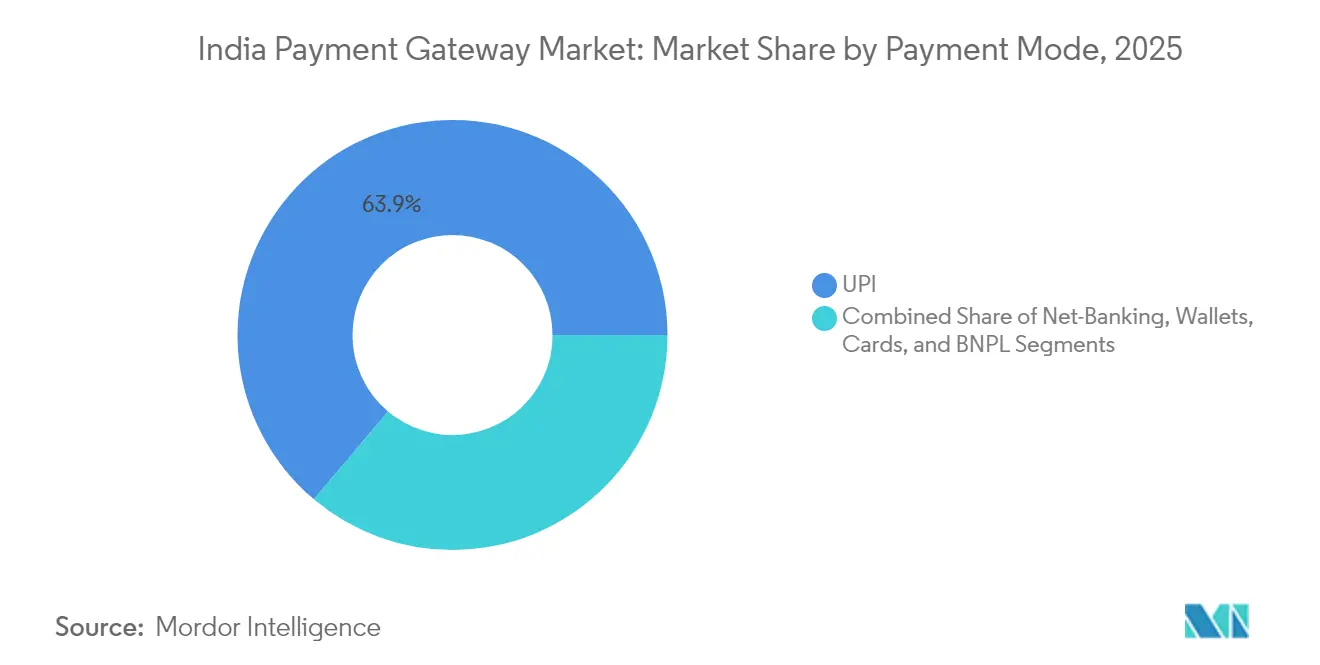

- By payment mode, UPI accounted for 63.85% of India payment gateway market share in 2025; buy-now-pay-later is forecast to post the highest 11.75% CAGR through 2031.

- By organization size, large enterprises held 57.40% of the India payment gateway market size in 2025, while small and medium enterprises are projected to expand at a 12.58% CAGR during 2026-2031.

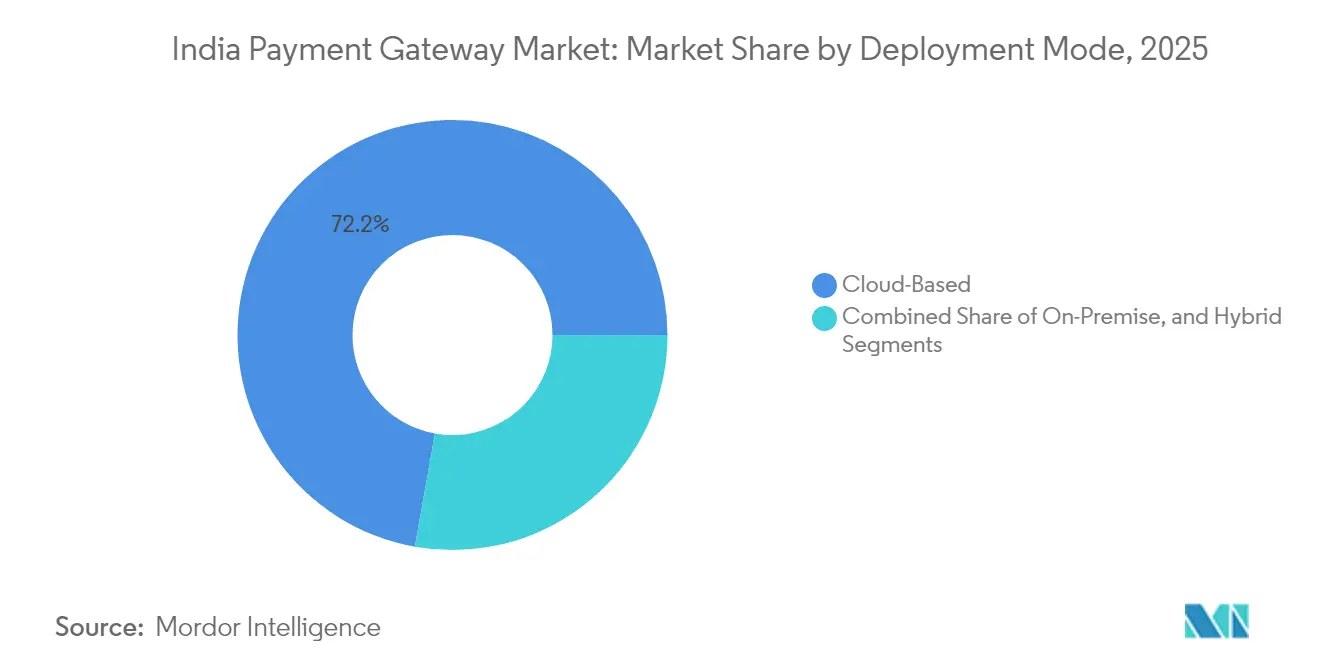

- By deployment mode, cloud-based models captured 72.20% share of the India payment gateway market size in 2025 and are anticipated to grow at a 12.08% CAGR to 2031.

- By end-user industry, e-commerce and marketplaces led with 43.50% of the India payment gateway market share in 2025; healthcare and pharmaceuticals exhibit the fastest 11.85% CAGR outlook to 2031.

- By region, West India commanded 31.60% of the India payment gateway market size in 2025, whereas East and Northeast India are on track for a 11.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Payment Gateway Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-Commerce and D2C Transactions | +2.8% | Global, with early gains in Mumbai, Delhi, Bangalore | Medium term (2-4 years) |

| Explosive UPI Adoption and International Expansion | +3.2% | Global, spill-over to Singapore, UAE, France | Short term (≤ 2 years) |

| Government-Backed Digital Public Infrastructure | +2.1% | National, with concentrated impact in tier-2/3 cities | Long term (≥ 4 years) |

| MSME Digital On-Boarding Incentives (PIDF, ONDC) | +1.9% | National, with early gains in Gujarat, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| API-First Open Finance and Embedded Payments | +1.4% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Rapid Growth of Credit-on-UPI and BNPL | +1.7% | North America and EU, National adoption patterns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive UPI Adoption and International Expansion

UPI processed more than 14 billion transactions in September 2025 alone, equal to roughly 50% of all real-time payments executed worldwide.[1]National Payments Corporation of India, “UPI-PayNow Corridor FAQs,” npci.org.in Bilateral linkages such as UPI-PayNow enable instant cross-border transfers to Singapore at sub-minute settlement windows and materially lower fees, attracting gateway partnerships with major remittance providers. NPCI’s “UPI Circle” feature now permits a primary user to delegate payments to up to five secondary profiles, extending real-time rails into underserved demographic cohorts and new merchant categories.

Government-Backed Digital Public Infrastructure

API Setu hosts more than 6,000 live government APIs, while DigiLocker supports 43 crore user wallets, creating standardized KYC layers that compress merchant onboarding cycles for gateways to a few minutes.[2]Ministry of Electronics and Information Technology, “Annual Report 2024-2025,” meity.gov.in The Public Financial Management System clears billions of subsidy payments monthly, pushing certified gateways to integrate at scale with direct benefit workflows.

MSME Digital Onboarding Incentives (PIDF, ONDC)

The Payments Infrastructure Development Fund subsidizes acceptance hardware in rural and semi-urban zones, bringing more than 12 lakh new merchants online in FY 2025.[3]Reserve Bank of India, “Draft Master Directions on Payment Aggregators April 2024,” rbi.org.in Parallelly, the Open Network for Digital Commerce (ONDC) pilot featuring nine lending service providers has reduced small-ticket loan approval times to six minutes, embedding gateway APIs into checkout and repayment flows.

API-First Open Finance and Embedded Payments

Account Aggregator (AA) consents surpassed 100 million in August 2024, with 420 regulated financial institutions live on the framework. Payment gateways are capitalizing by bundling underwriting engines into their checkout SDKs, thereby enabling instant credit-on-UPI across travel, healthcare, and education verticals without redirecting users outside merchant apps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-MDR Economics Pressure on Gateways | -1.8% | National, concentrated in UPI-dominant markets | Short term (≤ 2 years) |

| Intensifying RBI Compliance and PA Licensing Costs | -1.2% | National, affecting smaller providers disproportionately | Medium term (2-4 years) |

| Rising Fraud, Cyber-Risk and Outage Incidents | -0.9% | National, with higher impact in metro and tier-1 cities | Short term (≤ 2 years) |

| Merchant Concentration Among Top UPI Apps | -0.7% | National, with concentrated impact in West and South India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Zero-MDR Economics Pressure on Gateways

The RBI-mandated zero-merchant discount rate for UPI transactions eliminates the traditional ad-valorem revenue line for payment aggregators. Funding to private payment gateway startups contracted sharply in 2024, forcing providers to prioritize subscription-based analytics, cross-border collections, and lending partnerships to remain solvent.

Intensifying RBI Compliance and PA Licensing Costs

Draft guidelines compel non-bank payment aggregators to maintain a net worth of INR 25 crore by March 2028 and purge all card-on-file tokens by August 2025. Point-of-sale providers must obtain separate authorization by May 2025 or cease operations by July 2025, increasing compliance technology spend and favoring incumbents with larger balance sheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Mode: UPI Leads Structural Transformation

UPI accounted for 63.85% of India payment gateway market share in 2025, clearing over 240 billion USD-equivalent annually via real-time rails. Cards continue to dominate high-value retail outlays, particularly credit cards linked to RuPay rails that have doubled transaction value year-on-year. Buy-now-pay-later, tightly coupled with credit-on-UPI and Account Aggregator data pipes, is projected to deliver a 11.75% CAGR, the fastest among all modes. Net-banking retains significance for corporate bulk disbursements through NEFT and RTGS, whereas standalone wallet usage is receding as UPI interoperability becomes ubiquitous.

The India payment gateway market size tied to delegated UPI payments is set to grow sharply because “UPI Circle” allows limits of INR 15,000 per linked user each month. Simultaneously, NPCI’s plan to spin RuPay and Credit-on-UPI into dedicated subsidiaries signals a strategic focus on specialized rails that can accommodate cross-border flows.

By Organization Size: SMEs Accelerate Digital Uptake

Large organizations made up 57.40% of the India payment gateway market size in 2025 as banks, insurers, and multinationals sought multi-rail orchestration. However, SME adoption is surging at a forecast 12.58% CAGR through 2031, fuelled by ONDC’s standardized catalogs, PIDF hardware subsidies, and AA-enabled zero-paper onboarding. BharatPe’s merchant base grew 77% month-on-month in early 2024 as Tier-III and beyond cities embraced QR-based acceptance.

Payment gateways serving SMEs now bundle reconciliation dashboards and instant settlement to tackle working-capital pain points. The India payment gateway market share held by hybrid cloud dashboards catering to kirana stores is therefore expected to widen markedly.

By Deployment Mode: Cloud-Native Dominance

Cloud deployments commanded 72.20% of the India payment gateway market share in 2025, a reflection of scale requirements around peak festive seasons. National Informatics Center’s MeghRaj cloud hosts more than 21,000 virtual servers handling government payment workloads, underscoring statewide confidence in public-sector cloud security. Hybrid architectures are gaining favor among banks that run sensitive token vaults on-premise while bursting analytics to the cloud.

Regulatory sandboxes now insist on API-first submissions, encouraging start-ups to adopt containerized microservices from day one. As RBI’s “MuleHunter” fraud-monitoring engine taps transactional data inside cloud lakes, providers see compliance cost declines on automated rule engines, sustaining the 12.08% CAGR outlook for cloud-centric models.

By End-User Industry: Healthcare Emerges as Fastest Riser

E-commerce and online marketplaces retained a 43.50% share of the India payment gateway market in 2025, driven by a 141% annual uplift in UPI volumes. Yet healthcare and pharmaceuticals are forecast to expand at an 11.85% CAGR through 2031, owing to the National Health Claims Exchange (NHCX), which uses FHIR standards to automate insurer-provider settlements within minutes. AIIMS-SBI smart cards link patient IDs to prepaid wallets, further embedding gateway APIs in outpatient billing.

Banking, financial services, and insurance platforms integrate embedded payments for instant loan disbursement, with AA data streams curbing KYC drop-offs. In education, UMANG’s 2,101 live government services showcase zero-touch fee payments, whereas travel merchants adopt SoftPOS to accept tap-to-phone transactions on 20 million smartphones.

Geography Analysis

West India governed 31.60% of the India payment gateway market size in 2025 on the back of Maharashtra’s financial hub and Gujarat’s manufacturing corridors. High smartphone penetration, advanced supply-chain digitization, and Mumbai-based fintech HQs such as Razorpay anchor adoption. South India follows closely, buoyed by Bengaluru’s start-up density and Tamil Nadu’s early experiments on ONDC credit rails. North India benefits from Delhi-NCR’s concentration of enterprise clients and central-government payment backbones like PFMS, making it a crucial region for high-value bulk payouts. Central India exhibits consistent growth supported by government procurement portals that standardize QR acceptance in agricultural mandis.

East and Northeast India post the steepest growth trajectory at 11.95% CAGR through 2031. Digital Naari’s empowerment campaign already enables 60,000 women entrepreneurs across 10,000 PIN codes to earn INR 3,000-5,000 monthly through gateway-settled sales. Rural usage now constitutes one-third of nationwide digital payment users, a milestone that flips earlier patterns of metro dominance. QR code distribution surpasses 200 million nationally, and 7.3 million active POS terminals extend reach into tea gardens of Assam and coffee estates of Coorg alike.

Regulatory Landscape

The Reserve Bank of India (RBI) remains the primary regulator for payment gateways and payment aggregators under the Payment and Settlement Systems Act, 2007, with compliance increasingly centered on the consolidated Master Direction on Regulation of Payment Aggregators issued on September 15, 2025. The framework formally categorizes payment aggregators into PA-Online (PA-O), PA-Cross Border (PA-CB), and PA-Physical (PA-P), bringing physical aggregation into a unified authorization and compliance perimeter alongside escrow, governance, and cybersecurity requirements.

The consolidation tightened operational readiness for non-bank payment aggregators. Entities operating only PA-P were required to apply for authorization by December 31, 2025, and those that did not comply had to wind up operations by February 28, 2026. Payment aggregators were also directed to align merchant due diligence with CKYCR as the primary source, while ensuring merchants onboarded by December 31, 2025 meet the updated due diligence requirements by September 15, 2026. Separately, the RBI issued the Digital Payments E-mandate Framework, 2026 on April 21, 2026, consolidating recurring transaction rules across cards, PPI, and UPI, including a common AFA threshold (no AFA up to INR 15,000 per transaction, with higher limits up to INR 1,00,000 for specified categories).

Value Chain Analysis

India's payment gateway value chain is anchored by regulators and rail operators. The RBI sets authorization, escrow, KYC, and security requirements, while the National Payments Corporation of India (NPCI) operates key rails such as UPI and Bharat BillPay (Bharat Connect). Payment gateways focus on the checkout stack, including routing, tokenization, risk, and developer APIs. Payment aggregators sit closer to merchant contracting and settlement, connecting merchants to acquiring banks and card networks while orchestrating reconciliation, refunds, chargebacks, and dispute handling.

Downstream, merchants (including e-commerce and marketplaces, BFSI platforms, healthcare, education, and SMEs) consume gateway SDKs, plugins, and orchestration layers, supported by banks and networks that provide acquiring, settlement, and credential infrastructure. The September 15, 2025 consolidated Payment Aggregator Directions formalized PA-O, PA-CB, and PA-P categories, tightening merchant due diligence and escrow discipline across online and offline acceptance. That, in turn, increases demand for compliant onboarding and monitoring utilities integrated into gateway platforms. At the infrastructure layer, NPCI scale is a key operating variable for gateways, with UPI reporting 22.7 billion transactions in June 2026, pushing gateways to invest in cloud capacity, observability, and fraud controls to maintain uptime through peak loads and high-frequency merchant flows.

Competitive Landscape

Competitive intensity has risen as zero-MDR mandates compress fee-derived margins. Market leaders Razorpay, PayU, and Paytm diversify toward merchant cash-advance, payroll, and FX payout services. API-first enablers Juspay and M2P supply card tokenization, risk scoring, and payment orchestration layers to both incumbents and neo-banks.

Strategic alliances shape positioning: PayU’s tie-up with an omni-channel platform Fynd embeds checkout SDKs inside social-commerce storefronts, while HDFC Bank teams with ToneTag to offer sound-wave-based offline UPI acceptance. Compliance readiness provides a moat—players meeting the INR 25 crore net-worth bar gain early RBI approval, whereas sub-scale aggregators face exit or acquisition.

Healthcare and B2B credit present large white spaces. NHCX accreditation allows selected gateways to settle hospital claims in near real time, and ONDC’s lending rails create a multi-billion-dollar addressable base in SME working-capital finance. Cross-border corridors to Singapore, the UAE, and France open additional fee-bearing revenue lines that remain outside zero-MDR purview.

India Payment Gateway Industry Leaders

PayU Payments Private Limited

Razorpay Software Private Limited

One 97 Communications Limited (Paytm Payments Gateway)

CCAvenue - Infibeam Avenues Limited

IndiaIdeas.com Limited (BillDesk)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Recurring payments, subscription commerce, and large-ticket digital collections create monetization whitespace as the RBI's Digital Payments E-mandate Framework, 2026 (April 21, 2026) consolidates recurring mandate rules across cards, PPI, and UPI with a harmonized AFA structure. With that regulatory clarity, gateways can build mandate lifecycle management (registration, pre-debit notifications, retries, and dispute flows) into merchant toolkits for categories such as utilities, OTT and software subscriptions, and insurance and bill payments, rather than relying only on per-transaction pricing.

Cross-border UPI enablement and FX settlement capabilities also broaden the set of fee-bearing use cases beyond zero-MDR domestic UPI acceptance. NPCI's partnership with HSBC India (July 2026) to provide real-time foreign exchange settlement for international UPI payments via direct API integration creates an integration pathway for gateways serving travel merchants, global D2C brands, and inbound acceptance corridors, where FX, reconciliation, and compliance reporting can be packaged as value-added services. In parallel, NPCI's collaboration with NVIDIA (February 2026) to advance sovereign AI capabilities for the payments ecosystem, alongside UPI's transaction scale (22.71 billion transactions worth INR 28.92 trillion in June 2026), supports opportunities for gateway providers to productize AI-assisted fraud controls, operational analytics, and developer productivity layers that reduce integration time and incident-response overhead for merchants.

Recent Industry Developments

- July 2026: NPCI partnered with HSBC India to provide real-time foreign exchange settlement for international UPI payments through direct API integration. The move streamlines cross-border acceptance and settlement workflows for merchants that receive UPI-linked payments from international corridors, opening a clearer product lane for gateways to bundle FX, reconciliation, and compliance reporting as chargeable services.

- June 2026: Razorpay partnered with NPCI Bharat BillPay Limited (NBBL) to launch Banking Connect to standardize NetBanking integrations through a unified rail. By reducing fragmentation across bank-specific netbanking setups, the initiative lowers integration and maintenance load for merchants and strengthens the role of gateway-led orchestration across multiple payment modes.

- May 2025: PayU received final authorization from the Reserve Bank of India (RBI) to operate as an online payment aggregator. The approval strengthens PayU's ability to onboard and retain larger merchants that prioritize regulated partners, and it raises the competitive bar for smaller providers facing higher compliance and governance requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the India payment gateway market is defined as revenues earned from providing online payment acceptance and transaction processing for merchants in India, including gateway-related software and services that enable digital payments across major rails.

Scope exclusions: We exclude pure consumer payment apps and bank-to-bank payment rails where no payment gateway service is monetized, along with unrelated core banking infrastructure.

Segmentation Overview

- By Payment Mode

- UPI

- Cards

- Net-Banking

- Wallets

- BNPL

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

- By End-User Industry

- E-Commerce and Marketplaces

- Retail and FMCG

- BFSI and FinTech Platforms

- Healthcare and Pharmaceuticals

- Education and Ed-Tech

- Travel and Hospitality

- By Region

- North India

- West India

- South India

- East and Northeast India

- Central India

Data Sources, Market Sizing, and Validation

Desk Research

We start by building a clean view of how digital payment acceptance is expanding in India and which rails are driving it, and then we translate that into addressable gateway revenues. Public sources are used to anchor the demand pool, such as RBI publications (including payment system indicators and Payment Digitization Index), NPCI releases on UPI, RuPay and related trends, and Ministry of Electronics and Information Technology updates that describe major digital payment programs.

To keep assumptions realistic, we also scan regulatory and compliance notes from RBI (for example, notes that touch payment aggregators and data storage), along with industry-facing references such as NASSCOM or similar association writeups, and select peer-reviewed papers that discuss online merchant payments and fraud trends. Company annual reports, investor decks, and credible business press are reviewed to understand revenue mix and pricing direction. Paid subscriptions for company financials and patent databases are used selectively where private-company disclosures are limited. The desk sources listed here are illustrative, and other public references were used for cross-checks and clarification.

Primary Interviews and Surveys

We validate the model through interviews and structured surveys with payment gateway executives, product and risk leaders, merchant operations teams, and ecosystem experts such as PSP partners and consultants. Respondent input helped confirm the effective split between gateway processing and adjacent services, and it also clarified how metro versus non-metro merchant adoption affects the mix of UPI versus cards, which in turn feeds MDR and platform fee assumptions for the final numbers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | |

| Mid tier: 49% | Functional/Unit leaders: 42% | |

| Smaller Players: 16% | Managers: 43% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build where payment acceptance activity in India is reconstructed from published transaction growth signals and merchant digitization trends, and then filtered to the share that typically runs through gateways. To avoid over-counting, the demand pool is adjusted by payment mode mix (UPI, cards, wallets, and BNPL), online versus in-app versus POS routing patterns, and how much of enterprise volume is processed through in-house stacks.

The output is then corroborated using selective bottom-up approximations, such as sampled pricing checks (effective take rates), a volume-by-merchant cohort sanity check, and limited supplier roll-ups where financial disclosures allow it. Key inputs used in the model include RBI and NPCI transaction trajectories, the pace of online merchant onboarding, effective MDR and platform fee progression, gateway-led value-added service attach rates (for example, analytics or fraud tools), and policy-linked changes that influence net yields.

For forecasting, we rely on scenario analysis supported by simple time-series smoothing on stable drivers, then we adjust the curve using expert views on UPI share shifts, compliance cost pass-through, and e-commerce growth expectations. Where smaller private players have limited transparency, gaps are handled through conservative revenue ranges and then narrowed using primary checks on typical merchant acquisition and pricing behavior.

Data Validation & Update Cycle

We run multi-step validation so the market totals remain consistent with independent signals. Model outputs are checked against transaction growth, payment mode shares, and implied net take rates, and any sharp deviations are reviewed before sign-off. When a figure looks unusual, we revisit the driver assumptions and re-contact relevant respondents to confirm whether the change is real or a data artifact.

Each report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, pricing resets, or structural shifts in payment mode mix. Before delivery, a final analyst pass is completed so the estimates reflect the latest public releases and verified market feedback.

Mordor Intelligence's India Payment Gateway Market Size Compared With Other Published Estimates

Published market numbers for payment gateways in India often do not match because researchers count different revenue lines, use different years, and sometimes mix payment gateways with broader payments processing. Currency conversion timing and whether figures are reported gross or net of incentives can also shift the total.

The main gap comes from whether UPI-led flows are valued using full transaction value or only the gateway and platform fees earned on that flow, and Mordor Intelligence treats the market as the monetized gateway revenue pool tied to merchant payment acceptance, rather than the underlying payment transaction value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.07 B (2025) | |

| Regional Consultancy A | USD 1.90 B (2024) | Uses an earlier base year and often assumes a flatter take-rate path, which can understate revenue uplift from value-added services and newer merchant cohorts. |

| Trade Journal B | USD 16.20 B (2024) | Appears to blend gateway revenues with a wider digital payments value pool, which inflates totals when transaction value is counted instead of the fee-based revenue captured by gateways. |

The spread across the table is largely explained by what is being counted and how net monetization is translated from payment activity. By tying the total to observable payment adoption signals and then stress-testing yields with primary checks, the estimate stays traceable to clear variables that can be updated in a repeatable way.

Key Questions Answered in the Report

How large is the India payment gateway market in 2026?

The India payment gateway market size stands at USD 2.31 billion in 2026 and is projected to grow at an 11.66% CAGR through 2031.

Which payment mode dominates Indian online transactions?

UPI leads with 63.85% India payment gateway market share, processing more than 14 billion monthly real-time transactions.

Why are cloud deployments preferred by Indian payment gateways?

Cloud delivers scalable capacity for festive peaks, supports API-first innovation, and aligns with RBI sandbox guidelines, capturing 72.20% share in 2025.

What is driving SME adoption of payment gateways?

Government incentives like PIDF hardware subsidies and ONDC’s standardized catalogs enable rapid onboarding, propelling a 12.58% SME CAGR outlook.

How are gateways offsetting zero-MDR revenue loss?

Providers are launching subscription-based analytics, merchant lending, and cross-border payout services that lie outside zero-MDR mandates.

Which region is growing fastest for payment gateway adoption?

East and Northeast India exhibit the highest growth at a 11.95% CAGR, aided by rising internet penetration and targeted inclusion schemes.

Page last updated on: