Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

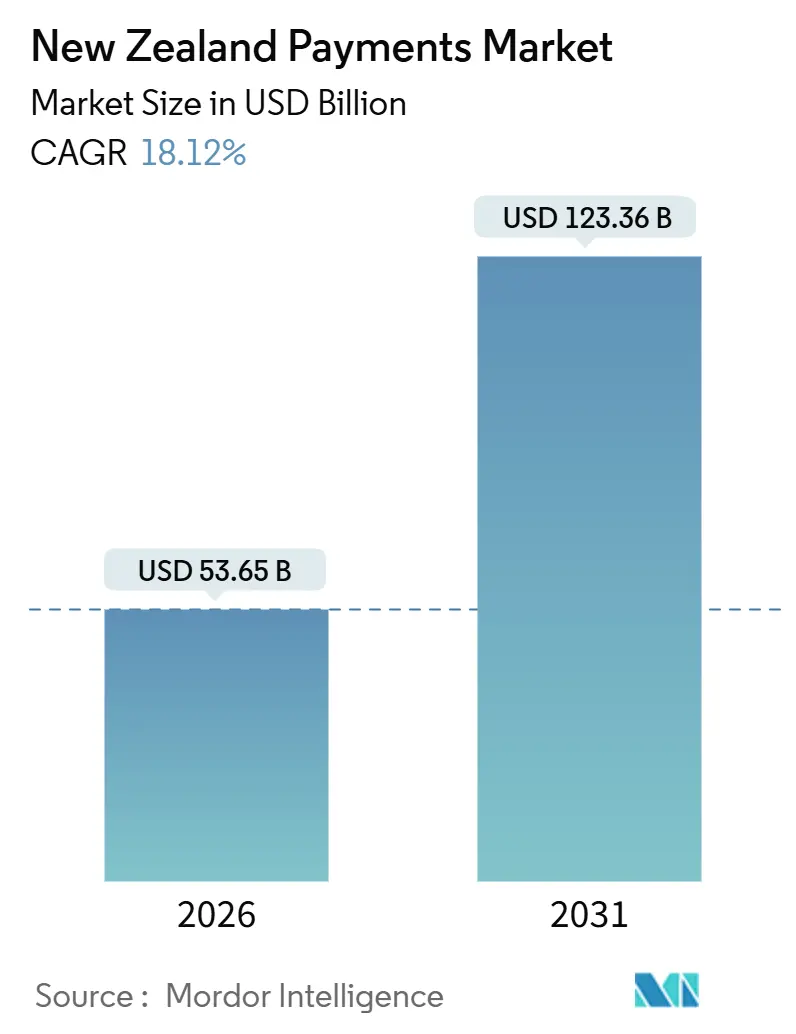

| Market Size (2026) | USD 53.65 Billion |

| Market Size (2031) | USD 123.36 Billion |

| Growth Rate (2026 - 2031) | 18.12% CAGR |

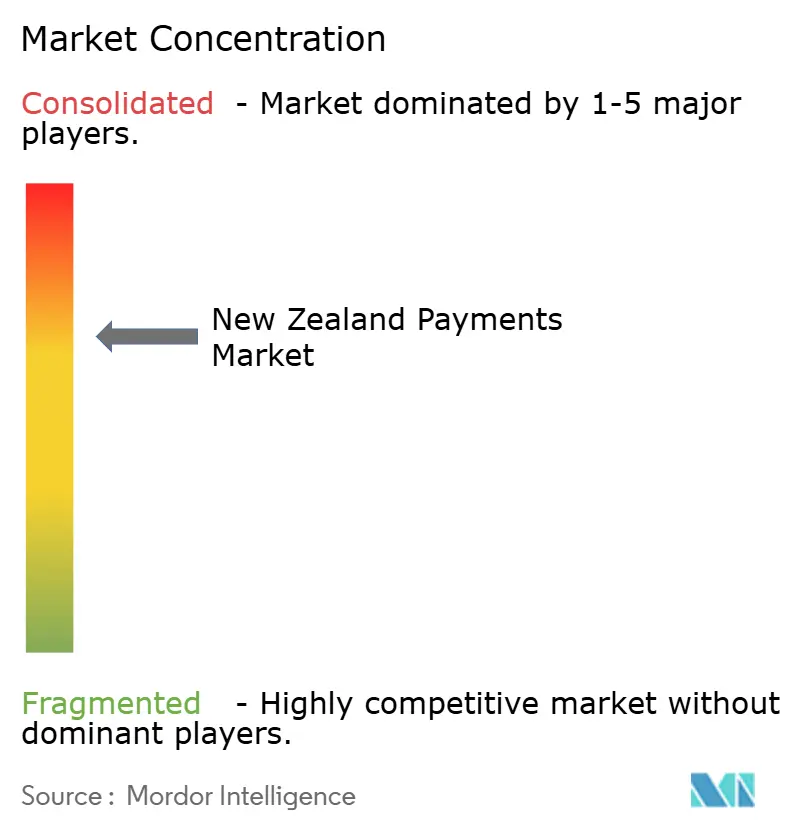

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand Payments Market Analysis by Mordor Intelligence

The New Zealand payments market size stands at USD 53.65 billion in 2026 and is projected to reach USD 123.36 billion by 2031, reflecting an 18.12% CAGR. Lower interchange fees, rapid real-time infrastructure deployment, and sustained contactless enthusiasm are steering volume from cash and batch settlement toward digital rails. Incumbent banks lean on open-banking APIs to shield deposits from wallet providers, while global processors court micro-merchants with software-only acceptance that trims hardware costs. Cross-border specialists use transparent foreign-exchange pricing to win exporters dissatisfied with bank spreads, and buy-now-pay-later platforms remain resilient despite stricter credit checks. The New Zealand payments market is therefore shaped by regulatory nudges that compress pricing yet stimulate usage, demographic cohorts native to mobile commerce, and infrastructure moves that compress settlement times from overnight to real time.

Key Report Takeaways

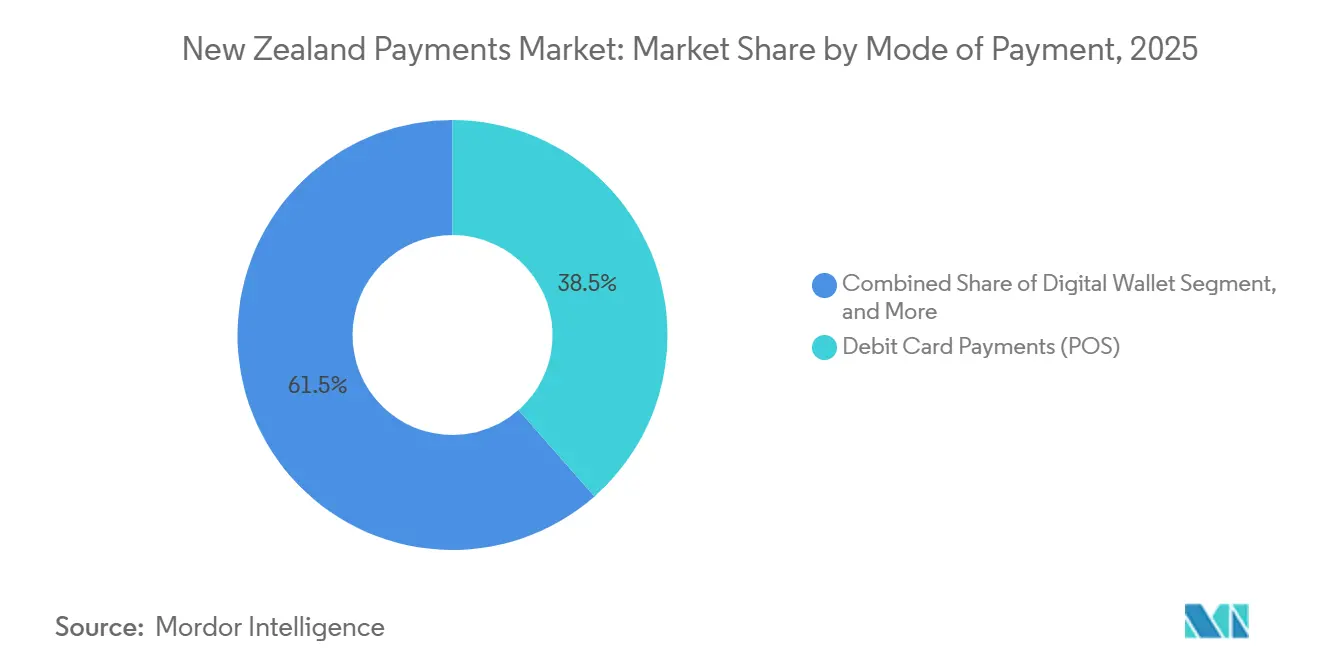

- By mode of payment, debit card transactions held 38.52% of the New Zealand payments market share in 2025. Digital wallets posted the fastest expansion at a 19.62% CAGR through 2031.

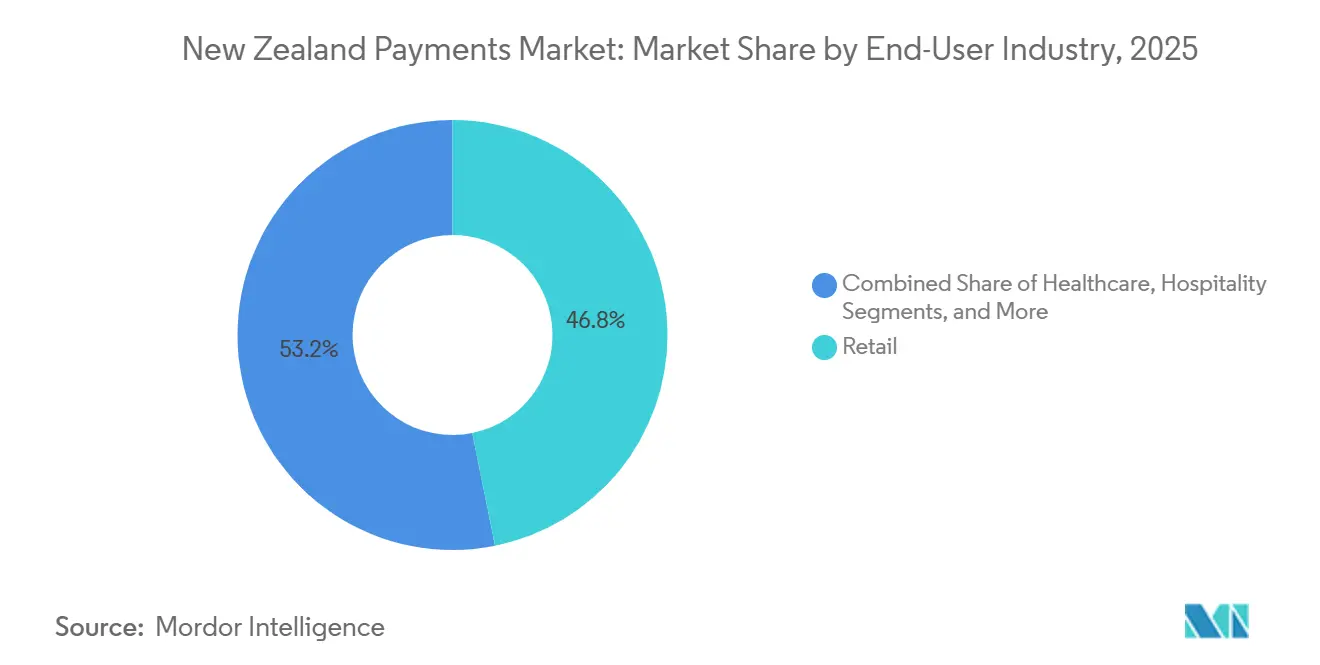

- By end-user industry, retail accounted for 46.83% of the New Zealand payments market size in 2025. Hospitality is tracking a 19.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

New Zealand Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated contactless-card limits boosting tap-and-go usage | +3.2% | National, especially Auckland, Wellington, Christchurch | Short term (≤ 2 years) |

| Rapid uptake of real-time payments infrastructure by domestic banks | +4.1% | National | Medium term (2-4 years) |

| Surge in buy-now-pay-later adoption among Millennials and Gen Z | +2.8% | Urban centers nationwide | Medium term (2-4 years) |

| Cross-border e-commerce growth fueling FX payment services | +2.3% | Export-oriented SMEs in Canterbury and Otago | Medium term (2-4 years) |

| Māori and Pasifika digital-inclusion initiatives unlocking underserved merchants | +1.6% | North Island communities, South Auckland, Porirua | Long term (≥ 4 years) |

| Carbon-neutral payment offerings gaining merchant preference | +1.1% | Early adoption in Wellington and Auckland CBD | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Contactless-Card Limits Boosting Tap-and-Go Usage

Permanent retention of the NZD 200 tap limit introduced during the pandemic has entrenched near-universal contactless behavior, with 72% of residents tapping at least weekly.[1]Payments NZ, “Contactless Payment Statistics,” paymentsnz.co.nz Apple’s Tap to Pay on iPhone, live since November 2024, extends acceptance to sole traders unwilling to rent terminals.[2]Apple Inc., “Tap to Pay on iPhone Launches in New Zealand,” apple.com Worldline’s Tap on Mobile counters this disruption by transforming Android phones into EFTPOS devices. Competition has trimmed blended merchant discount rates below 1% in grocery and fuel, reinforcing card acceptance rather than cannibalizing it. The behavioral lock-in of tap-and-go therefore sustains transaction growth even as interchange revenue compresses.

Rapid Uptake of Real-Time Payments Infrastructure by Domestic Banks

The Reserve Bank’s November 2025 decision to fund a national instant-payment rail will eliminate NZD 100 million (USD 60 million) in annual float and reconciliation costs by 2027. BNZ previewed the benefits with Payap, a QR-based account-to-account option settling in seconds at a 0.39% merchant fee. Payment Initiation API v2.3, enabled in May 2025, supports recurring debits that shift utilities and subscriptions off card rails.[3]Commerce Commission, “Retail Payment Systems,” comcom.govt.nz As real-time rails mature, Visa and Mastercard face declining domestic interchange pools, while banks seek ancillary revenue from data analytics and fraud services. The resulting competitive realignment accelerates the digital shift in the New Zealand payments market.

Surge in Buy-Now-Pay-Later Adoption Among Millennials and Gen Z

Despite mandatory credit checks imposed from September 2024, buy-now-pay-later outstandings reached NZD 2.7 billion (USD 1.63 billion) in 2026, expanding at 16.7% CAGR. Klarna’s 2024 acquisition of Laybuy consolidated 500,000 local accounts under a single underwriting engine. OneChoice’s 2025 research found 63% of consumers attribute impulse spending to cashless plans, yet merchants still enjoy 20% uplift in conversion when installments appear at checkout. Higher compliance barriers weed out under-capitalized entrants, cementing a triopoly and stabilizing default rates. The segment’s stickiness underscores consumer appetite for short-term credit alternatives in the New Zealand payments market.

Cross-Border E-Commerce Growth Fueling FX Payment Services

Wise quantified NZD 667 million (USD 400.2 million) in hidden FX spreads borne by New Zealand SMEs each year. Airwallex and Revolut responded with multi-currency accounts that allow exporters to receive USD, EUR, or GBP without forced conversions. Corpay’s August 2025 partnership with New Zealand Football showcased demand for transparent FX even among non-profits. Publishing real-time mid-market rates has become a competitive signal, pushing banks to disclose spreads or risk outflows. As cross-border volume climbs, FX transparency will remain an incremental growth lever for the New Zealand payments market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interchange fees deterring small merchants | -2.4% | National, especially rural and low-margin retail | Short term (≤ 2 years) |

| Stringent AML/CFT compliance costs for fintechs | -1.8% | National, heavier burden on startups | Medium term (2-4 years) |

| Limited rural broadband coverage impeding QR and app payments | -1.3% | Northland, East Coast, South Island interior | Medium term (2-4 years) |

| Rising consumer data-sovereignty concerns | -1.1% | Privacy-conscious urban segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Interchange Fees Deterring Small Merchants

Although the July 2025 cap pushed domestic credit interchange down to 0.30%, total acceptance costs for micro-merchants still reach 1.5%-2.5% once acquirer and scheme fees are added. Cafés in Queenstown and bookshops in Dunedin operate on sub-5% margins and view these fees as a revenue tax. A proposed 2025 surcharge ban, intended to save consumers NZD 45-65 million (USD 27-39 million) annually, prevents merchants from passing costs onward, nudging some toward cash-only signage. Account-to-account options like Payap offer cheaper rails, yet consumer unfamiliarity with QR workflows slows migration. Persistently high blended fees therefore restrain electronic penetration in the tail of the New Zealand payments market.

Stringent AML/CFT Compliance Costs for Fintechs

Phased AML and CFT rules introduced between 2023 and 2025 lifted onboarding costs to NZD 15-40 per customer, a level that erodes unit economics for high-volume, low-value payment apps. Laybuy’s 2024 receivership was partly blamed on compliance overheads that outpaced revenue. Credit check mandates for buy-now-pay-later further raised cost structures. Well-capitalized players absorb these expenses, but startups either pivot to B2B niches or exit, trimming competitive diversity in the New Zealand payments industry. The compliance drag slows innovation by diverting resources from product development to regulatory tooling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Open Banking Chips Away at Card Dominance

Debit cards generated 38.52% of total 2025 volume, underscoring a cultural bias toward immediate settlement and decades of Reserve Bank advocacy for low-cost rails. Digital wallets, growing at a 19.62% CAGR, gained momentum after Apple’s Tap to Pay on iPhone enabled small traders to accept near-field transactions without hardware outlay. Credit cards face flattening spend, as the interchange cap trims issuer economics and merchants steer patrons to cheaper alternatives. Early adopters of BNZ’s Payap illustrate the future such as a QR scan triggers instant account-to-account settlement for a 0.39% fee, compared with the 1.5% merchant discount rate typical on credit lines.

The New Zealand payments market size for account-to-account transactions is expected to expand quickly once the national instant rail goes live, closing the convenience gap with cards. Cash continues to decline in single digits each year, confined to rural pockets where broadband gaps limit QR reliability. Open-banking payments reached 15% of eligible customers in early 2025, and Westpac’s fee-free POLi campaign aims to accelerate merchant integration. As consumer familiarity grows, the New Zealand payments market will likely transition to a three-pillar structure with cards for rewards, wallets for online ease, and open-banking rails for price-sensitive merchants.

By End-User Industry: Hospitality Overtakes in Growth

Retail retained 46.83% of 2025 value, but hospitality logged a 19.74% CAGR that now outpaces every other vertical. Tourist inflows and a shift to mobile ordering lifted hospitality card spending to NZD 14.8 billion (USD 8.88 billion) for the year ended March 2025. Tap to Pay on iPhone allows staff to settle bills tableside, increasing table turnover and tip capture. Healthcare, fueled by a 10-year digital plan, is digitizing co-payments and prescription fees, demanding PCI-compliant, audit-ready rails.

Entertainment merchants harness Payment Initiation API v2.3’s recurring-debit support to streamline subscriptions, while government entities embrace Peppol e-invoicing to cut manual reconciliations. The New Zealand payments market size linked to utility and education flows grows steadily as agencies enforce digital engagement mandates. Providers able to tailor vertical-specific features, tip pooling for restaurants, multi-currency invoicing for exporters, or HIPAA-grade encryption for telehealth, gain an edge in the diversified New Zealand payments industry.

Geography Analysis

Urban centers dominate digital adoption. Auckland, Wellington, and Christchurch generate the bulk of wallet and contactless volume, aided by dense broadband coverage and affluent demographics. In contrast, Northland, the East Coast, and large portions of the South Island still rely on patchy connectivity that impedes QR reliability. Government data show one in five residents lacks foundational digital skills, a figure higher in rural districts. Without targeted training, the rollout of real-time payments could entrench, rather than bridge, the digital divide.

Māori and Pasifika communities face compounded barriers of credit access and digital literacy. Studies from September 2024 found that households without basic transaction accounts are less likely to participate in government e-transfer programs. BNZ’s NZD 0.6 million (USD 0.36 million) grant for skills training offers a template but lacks national reach. Payment providers can spur inclusion by embedding voice prompts, pictograms, and SMS receipts to lower cognitive load.

Export-oriented Canterbury and Otago favor platforms publishing live mid-market FX rates. Wise’s advocacy for transparent pricing and Airwallex’s API settlement resonate with wineries, dairy exporters, and tech outsourcers wary of hidden spreads. Corpay’s football partnership highlights that even sporting bodies are professionalizing treasury flows to capture basis-point savings. The regional picture therefore blends urban fintech concentration with rural cash persistence, demanding nuanced go-to-market strategies across the New Zealand payments market.

Competitive Landscape

Legacy banks still hold current accounts and EFTPOS rails, but global processors encroach on merchant relationships. Worldline’s 27 billion annual transactions hinge on a terminal rental model now challenged by software-only acceptance. Stripe bundles treasury, stablecoin, and global payout features into a single API, reducing reliance on correspondent networks. Visa’s Scan to Pay QR launch aims to capture offline-to-online flows, particularly among Asia-Pacific tourists spending in New Zealand.

BNZ’s Payap exemplifies defensive innovation, charging a sub-0.5% fee that undercuts card networks. Akahu offers payment initiation that bypasses schemes entirely, while Dosh migrates issuance to Pismo to gain speed and feature parity. Regulatory oversight remains intense as the Commerce Commission retains the power to cap fees and require access to essential infrastructure, limiting any player's ability to monopolize.

White-space opportunities include merchants with small baskets that cannot absorb 2% fees, rural operators seeking low-bandwidth solutions, and exporters needing real-time FX. The moderate fragmentation and steady consolidation around compliance-able incumbents shape a dynamic yet balanced New Zealand payments market.

New Zealand Payments Industry Leaders

Worldline New Zealand Limited

Fidelity National Information Services, Inc.

Visa Inc.

Mastercard Incorporated

American Express Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Stripe enabled automatic NZD-to-stablecoin conversion for New Zealand merchants settling global payouts.

- November 2025: The Reserve Bank unveiled a real-time rail expected to save NZD 100 million (USD 60 million) in float costs by 2027.

- February 2025: The Reserve Bank cut the Official Cash Rate to 3.25%, easing financing costs and potentially lifting discretionary spend, which can feed volume growth across the New Zealand payments market.

- November 2025: The Ministry of Health published a decade-long digital investment blueprint mandating secure payment flows in telehealth.

- November 2025: Visa extended Scan to Pay QR across Asia-Pacific, partnering with Samsung Wallet and LINE Pay.

New Zealand Payments Market Report Scope

Payments are increasingly becoming cashless, and the industry's role in fostering inclusion has become a top priority. Payments contribute to developing digital economies and drive innovation, all while serving as a stable backbone around the world.

The payments market is divided into two segments: POS and e-commerce. E-commerce payments include online purchases of both goods and services, such as purchases made on e-commerce websites and online travel and hospitality bookings. In terms of POS, all transactions that take place at a physical point of sale are included in the market's scope.

By Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash | |

| Other Point-of-Sale Payment Mode | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sales Payment Mode |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Other End-User Industries |

| By Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point-of-Sale Payment Mode | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sales Payment Mode | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large will electronic payments reach in New Zealand by 2031?

The New Zealand payments market is forecast to reach USD 123.36 billion by 2031, more than doubling the 2026 value.

Which segment is growing fastest within consumer payments?

Digital wallets lead with a 19.62% CAGR through 2031, driven by software-only acceptance and mobile-native consumers.

Why are interchange fees still a barrier despite regulatory caps?

Caps cut scheme fees, yet acquirer margins and terminal rental keep all-in costs near 2% for micro-merchants, limiting acceptance.

What impact will the real-time rail have on businesses?

Instant settlement is projected to save USD 60 million in float costs by 2027 and accelerate working-capital cycles.

Who benefits from transparent FX pricing?

Export-oriented SMEs in Canterbury and Otago save on hidden spreads by using platforms such as Wise, Airwallex, and Revolut.

Page last updated on: