Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 154.44 Billion |

| Market Size (2026) | USD 163.06 Billion |

| Market Size (2031) | USD 213.93 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Payments Market Analysis by Mordor Intelligence

The Hong Kong payments market size is expected to grow from USD 154.44 billion in 2025 to USD 163.06 billion in 2026 and is forecast to reach USD 213.93 billion by 2031 at 5.58% CAGR over 2026-2031. Strengthening real-time infrastructure through the Faster Payment System (FPS), surging cross-border wallet usage, and a rebound in tourism receipts are combining to sustain robust transaction value expansion in the Hong Kong payments market. Merchant appetite for unified QR acceptance and the growing profitability of virtual banks are stimulating competitive fee dynamics, while government pilots with the digital yuan position the city as a regional testbed for central-bank digital currency (CBDC) interoperability. Counterbalancing these positives, escalating cyber-fraud and persistently high interchange fees on international card rails are prompting service providers to funnel additional resources into security and merchant-acquiring innovation. Nevertheless, the underlying mix of stringent regulation, dense network effects, and geographic proximity to Mainland China reinforces long-term resilience for the Hong Kong payments market.

Key Report Takeaways

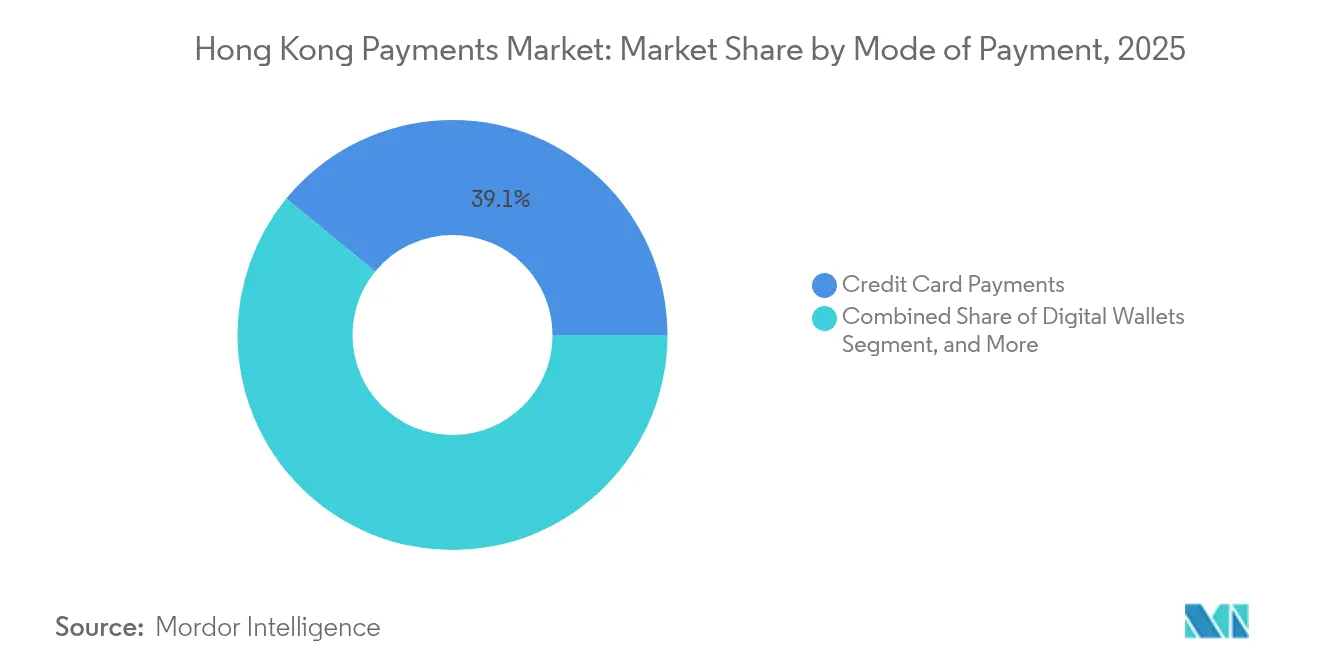

- By mode of payment, credit cards led with 39.06% of the Hong Kong payments market share in 2025, while Account-to-Account transfers are forecast to advance at a 6.08% CAGR through 2031.

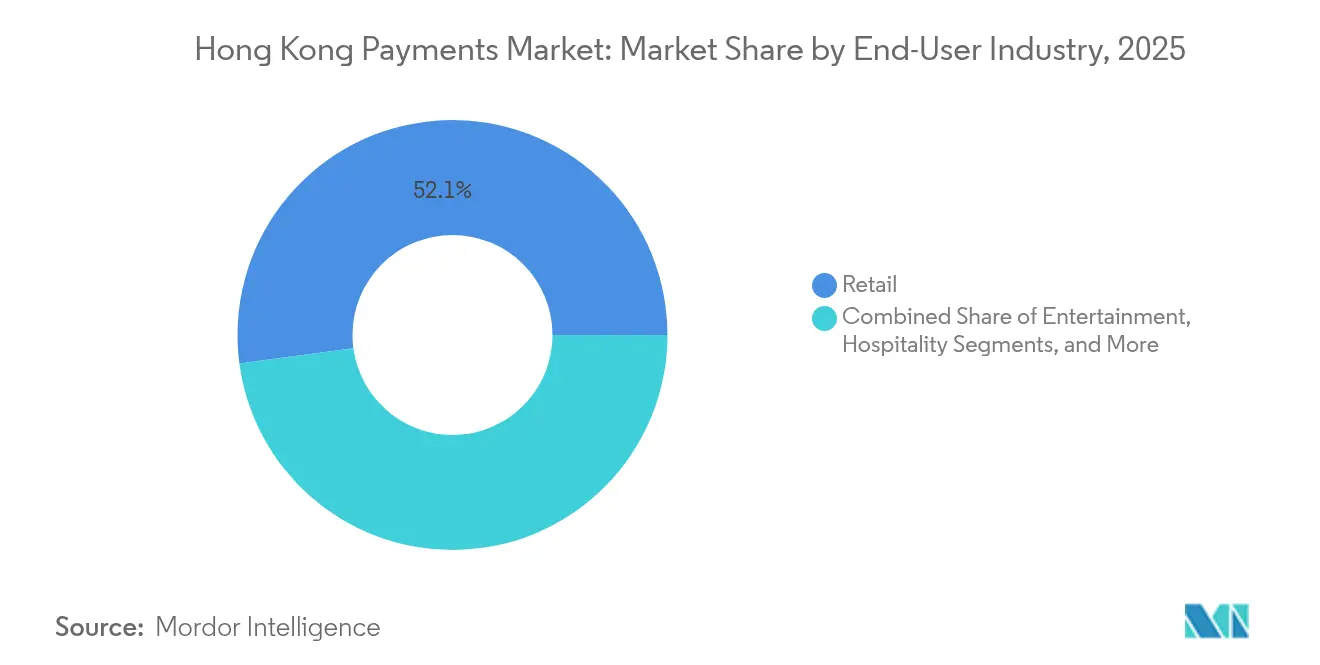

- By end-user industry, retail accounted for 52.12% share of the Hong Kong payments market size in 2025, whereas healthcare is projected to expand at a 6.49% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led Faster Payment System (FPS) enhancements | +1.2% | Hong Kong, with cross-border spillover to Mainland China | Medium term (2-4 years) |

| Rapid merchant adoption of QR-Code Unified Scheme | +0.8% | Hong Kong, with tourist acceptance benefits | Short term (≤ 2 years) |

| Cross-border e-CNY pilot integration with HK wallets | +0.7% | Hong Kong and Greater Bay Area | Medium term (2-4 years) |

| Rise of virtual banks targeting SME payment needs | +0.6% | Hong Kong, with potential regional expansion | Long term (≥ 4 years) |

| Growth of buy-now-pay-later (BNPL) embedded in wallets | +0.4% | Hong Kong, with cross-border e-commerce applications | Short term (≤ 2 years) |

| Shift of Mainland tourists to mobile wallets vs cash | +0.3% | Hong Kong, concentrated in retail and hospitality zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-led Faster Payment System Enhancements

Regular upgrades to FPS are catalyzing network effects in the Hong Kong payments market. Technical alignment with Mainland China’s Internet Banking Payment System, scheduled for mid-2025, will allow residents to move funds cross-border in real time using mobile numbers. Bilateral coordination completed in December 2024 already underpins multilateral QR linkages such as the PromptPay connection with Thailand, placing Hong Kong third worldwide for cross-border QR volumes in January 2024.[1]Press Office, “LCQ4: Link for cross-border QR payment between Hong Kong and Thailand,” HKSAR Government, info.gov.hk ISO 20022 migration and an Interbank Account Data Sharing platform launched in April 2025 extend real-time data utilities to participating banks, improving fraud analytics and onboarding speed.[2]Editorial Team, “Hong Kong Monetary Authority - Interbank Account Data Sharing,” Hong Kong Monetary Authority, hkma.gov.hk Regulators insist that all enhancements meet strict resilience thresholds, ensuring that service uptime and liquidity management remain robust even as transaction velocity increases. Collectively, these factors elevate instant transfer adoption and widen revenue streams from value-added overlay services across the Hong Kong payments market.

Rapid Merchant Adoption of the Unified QR Code Scheme

A common QR standard is reshaping point-of-sale economics. Octopus integrated PayMe in December 2024, rolling out zero-fee acceptance across 27,000 taxis and converting cash-heavy routes to digital collection.[3]Corporate Affairs, “Press Release 23 December 2024,” Octopus Cards Limited, octopus.com.hk Alipay+ imported 14 foreign e-wallets in April 2024, letting visitors spend through home-country apps at the majority of outlets. Unified QR rails settle via FPS, giving merchants same-day liquidity and bypassing interchange fees that can top 1.5% on international cards. Small retailers particularly value the simplified hardware and the ability to toggle among wallets within a single code, driving swift penetration of cash-lite acceptance terminals. As participation grows, network externalities further entrench QR as a low-cost, high-reach front end in the Hong Kong payments market.

Cross-border e-CNY Pilot Integration with Hong Kong Wallets

Since May 2024, residents and tourists have been able to top up digital-yuan balances through FPS rails. Octopus extended the function to Tourist Mobile Octopus in February 2025; during Chinese New Year week, mainland visitors spent HKD 100 million using the feature, up 10% year over year. The pilot now covers healthcare vouchers redeemable in Nansha and Dongguan, reducing currency friction for elderly residents seeking cross-border medical services. Successful technical implementation illustrates CBDC-private wallet interoperability at commercial scale, reinforcing Hong Kong’s status as a laboratory for next-generation settlement. Banks and PSPs are already designing treasury tools and programmable payments tied to digital-yuan flows, broadening the addressable base of the Hong Kong payments market.

Rise of Virtual Banks Targeting SME Payment Needs

Virtual banks moved from scale to profitability when ZA Bank posted its first positive monthly net income in August 2024. These branch-less lenders bundle instant transfers, merchant acquiring, and BNPL credit within a single mobile interface, solving pain points for SMEs that previously juggled multiple providers. Fusion Bank, through WeBank technology, extended HKD 50 million in unsecured “GoGlobal” loans to GBA affiliates by end-2024. Integrated cash-flow analytics and straight-through settlement reduce working-capital gaps, while competitive fee structures intensify pricing pressure on legacy acquirers. As more SMEs migrate, virtual banks enlarge their share of transaction volumes in the Hong Kong payments market and reinforce digital-first behavior among suppliers and staff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interchange fees on international card rails | -0.9% | Hong Kong, with spillover effects on cross-border commerce | Medium term (2-4 years) |

| Cyber-fraud surge undermining consumer trust | -1.1% | Hong Kong, with particular impact on elderly demographics | Short term (≤ 2 years) |

| Limited interoperability with Greater Bay Area wallets | -0.5% | Hong Kong and Greater Bay Area | Medium term (2-4 years) |

| Ageing population reluctant to adopt digital wallets | -0.3% | Hong Kong, concentrated in traditional retail sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-fraud Surge Undermining Consumer Trust

Scam losses hit HKD 9 billion in 2023, equal to 0.3% of GDP, and phishing attacks on banks jumped 108% in 2024. Criminals now deploy AI-generated deepfakes, including a February 2024 video-conference spoof that siphoned HKD 200 million from a multinational. Surveys show 73% of local enterprises suffered cyber incidents in 2024, with 96% reporting phishing vectors. To stem damage, the Anti-Deception Alliance cut bank intercept times by 70%, but PSPs continue to raise security spend, squeezing operating margins. Persistent headlines risk nudging consumers back to cash, placing a drag on transaction growth in the Hong Kong payments market.

High Interchange Fees on International Card Rails

Unlike Australia or the EU, Hong Kong sets no interchange caps, leaving merchants to shoulder fees that often exceed 1.5% of ticket value. DBS polling in mid-2024 found that 31% of SMEs view long settlement cycles as a pain point tied to card acceptance. Some merchants restrict card usage or encourage alternative wallets, curbing revenue from higher-spending overseas customers. While American Express teamed with KPay in June 2024 to widen local acceptance, industry observers expect regulatory scrutiny if costs remain sticky. In the interim, expensive card rails weigh on overall margins, slightly tempering expansion of the Hong Kong payments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Credit Cards Dominate While A2A Gains Momentum

By online sales, credit cards generated 39.06% of the Hong Kong payments market share in 2025, underpinned by affluent consumer segments that prize rewards and installment flexibility. Account-to-Account transfers, however, are projected to register a 6.08% CAGR to 2031, making them the fastest-expanding component of the Hong Kong payments market size. The rapid uptake stems from FPS’s 24/7 settlement, lower merchant fees, and straightforward onboarding for both individuals and corporates. Digital wallets straddle both rails, giving users a choice between stored value, linked debit, or FPS push-pay, thereby blurring historical mode distinctions and amplifying multi-rail transaction growth.

Debit cards hold steady due to payroll linkages and habitual ATM withdrawals, yet they increasingly serve as funding sources for wallets rather than direct point-of-sale instruments. Cash-on-delivery persists mainly for big-ticket e-commerce items where consumers want physical inspection before payment. Meanwhile, the September 2022 HKMA guidelines on BNPL transparency spurred platforms like livi PayLater to cap interest and embed credit checks, lifting consumer confidence. As integrated super-apps normalize cross-rail switching within a single checkout, the Hong Kong payments market gains both depth and diversity across payment modes.

By End-User Industry: Retail Leads While Healthcare Accelerates

Retail commanded 52.12% of the Hong Kong payments market size in 2025, buoyed by tourist inflows that spent HKD 100 million via Octopus during Lunar New Year 2025. Recovery in visitor arrivals compensates for lower per-capita spending, sustaining transaction frequency across department stores and duty-free outlets. Healthcare, on the other hand, is forecast to post a 6.49% CAGR, the quickest among verticals, following the March 2025 Hospital Authority fee reform that introduced tiered pricing and a HKD 10,000 annual cap on patient outlay. Hospitals and clinics now demand integrated bill-presentment, insurance adjudication, and cross-border voucher acceptance, opening white space for fintech-enabled healthcare PSPs.

Entertainment venues and hospitality providers leverage Alipay+ and WeChat Pay to cater to multi-wallet tourists, while professional-services firms embrace digital invoicing to expedite overseas receipts. Government agencies also digitize disbursements, though adoption trails the private sector due to legacy IT constraints. Over time, industry-specific wallet features such as medical installment plans and tax-deductible e-receipts will further segment solution design, yet all verticals collectively reinforce transaction velocity within the Hong Kong payments market.

Geography Analysis

Hong Kong’s compact urban footprint and Special Administrative Region status create payment flows that outsize its 1,114 km² land mass. FPS registered 14.95 million users by July 2024, double the working-age population, reflecting deep domestic penetration. At the same time, 85 million Hong Kong resident trips to Mainland China in the first ten months of 2024 underpin a steady back-and-forth corridor for remittances and consumer spend. The forthcoming mid-2025 FPS-IBPS bridge will allow instant renminbi transfers, a functionality absent in peer hubs like Singapore or Tokyo, strengthening the Hong Kong payments market’s cross-border appeal.

Mainland tourists increasingly tap wallets over cash; same-day visitor per-capita spend slid from HKD 2,400 in 2018 to HKD 1,300 in H1 2024, yet total electronic transactions rose thanks to user growth. Hong Kong’s linkage with Thailand’s PromptPay since December 2023 elevated the city to third globally for cross-border QR volume within a month. Such interconnections diversify corridor risk and embed the Hong Kong payments market inside a lattice of regional fast-payment systems.

Internally, Octopus boasts 98% household penetration and roughly 190,000 acceptance points, ensuring friction-less ubiquity even in wet-markets and minibuses. Virtual banks reach younger demographics: ZA Bank claims 25% Generation-Z penetration across its 800,000 customers. High smartphone density, mature 5G coverage, and bilingual interfaces further eliminate frictions that slow rollout in larger geographies. The result is a payments laboratory where new rails scale rapidly, reinforcing Hong Kong as a gateway node in wider Asia-Pacific commerce and cementing the geographic moat of the Hong Kong payments market.

Competitive Landscape

Traditional majors such as HSBC and Bank of China (Hong Kong) still process the bulk of corporate volumes, but fee pressure and UX innovation are shifting transaction share toward fintechs. Eight licensed virtual banks exploit cloud-native cost structures; ZA Bank reached profitability in just five years, demonstrating viable economics at sub-HKD 1 billion revenue scale. Fintech-incumbent alliances crystallize this race: the March 2025 PingPong-Octopus deal opens Octopus’ 190,000 touchpoints to global merchants selling into Hong Kong, while leveraging PingPong’s cross-border e-commerce pipeline from China.

American Express’ June 2024 pact with KPay sought to offset lagging SME acceptance by tapping KPay’s point-of-sale footprint, yet interchange concerns still hamper card uptake. Meanwhile, the April 2025 Hong Kong Investment Corporation equity stake in WeLab underscores public-sector resolve to anchor advanced AI capability at home, with WeLab pledging to reskill all employees on AI tools by 2025. Regulatory policy continues to shape the field: HKMA’s October 2024 e-banking risk manual demands end-to-end encryption and continuous threat modeling, advantaging players already compliant with rigorous cybersecurity regimes.

Cross-border capabilities now define the moat. Providers integrating e-CNY, FPS, and third-country QR rails stand to capture accelerating tourist and SME corridors. Smaller PSPs specialize in niche verticals such as healthcare claims or logistics cash-on-delivery, carving defensible territory through domain expertise. Collectively, these dynamics render the Hong Kong payments market a moderately concentrated but fiercely innovative arena where scale economies coexist with specialization.

Hong Kong Payments Industry Leaders

The Bank of East Asia Limited (BEA)

Standard Chartered Bank (HK) Limited

The Hongkong and Shanghai Banking Corporation Limited

Bank of China (Hong Kong) Limited

Citibank (Hong Kong) Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hong Kong Investment Corporation partnered with WeLab to boost AI-driven fintech solutions, committing to upskill all staff by 2025 and eyeing 500 million users by 2032.

- March 2025: Hospital Authority rolled out tiered healthcare pricing, capping annual public-hospital spend at HKD 10,000 for 1.4 million residents.

- March 2025: PingPong and Octopus agreed to integrate global PSP rails with Hong Kong’s dominant wallet infrastructure, targeting cross-border merchants.

- January 2025: Fusion Bank signed a technology pact with WeBank to scale its GoGlobal SME loan program, which disbursed HKD 50 million by end-2024.

Hong Kong Payments Market Report Scope

The point of sale is the time and location where a transaction is completed. A point-of-sale (POS) system is a combination of computer hardware and software that manages transactions during the sale of a product or service. It helps to store, capture, share, and report data related to sales transactions. It eases the shopping experience and helps expedite the checkout process, resulting in customer satisfaction. Inventory management, stock in hand, availability of a product, and pricing information are the primary data acquired from the systems.

The Hong Kong Payment Market is segmented by mode of payment (point of sale (card payments, digital wallet, cash), online sale (card payments, digital wallet)) by end-user industry (retail, entertainment, healthcare, hospitality). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash | |

| Other Point-of-Sale Payment Mode | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sales Payment Mode |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Other End-User Industries |

| By Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point-of-Sale Payment Mode | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sales Payment Mode | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the Hong Kong payments market in 2026?

The Hong Kong payments market size is USD 163.06 billion in 2026 and is projected to reach USD 213.93 billion by 2031.

What is driving real-time Account-to-Account adoption?

FPS upgrades, lower merchant fees, and instant settlement underpin the 6.08% CAGR forecast for A2A transactions.

Which industry vertical is expanding fastest in electronic payments?

Healthcare leads with a 6.49% CAGR as fee reforms and cross-border voucher schemes digitize patient billing.

How are virtual banks affecting the competitive landscape?

Profit-making virtual banks bundle payments, lending, and BNPL, pressuring incumbent fee structures while servicing SME gaps.

What are the biggest risks facing digital payments in Hong Kong?

Cyber-fraud, especially AI-driven phishing and deepfakes, and high international card interchange fees remain key headwinds.

Page last updated on: