South Korea NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

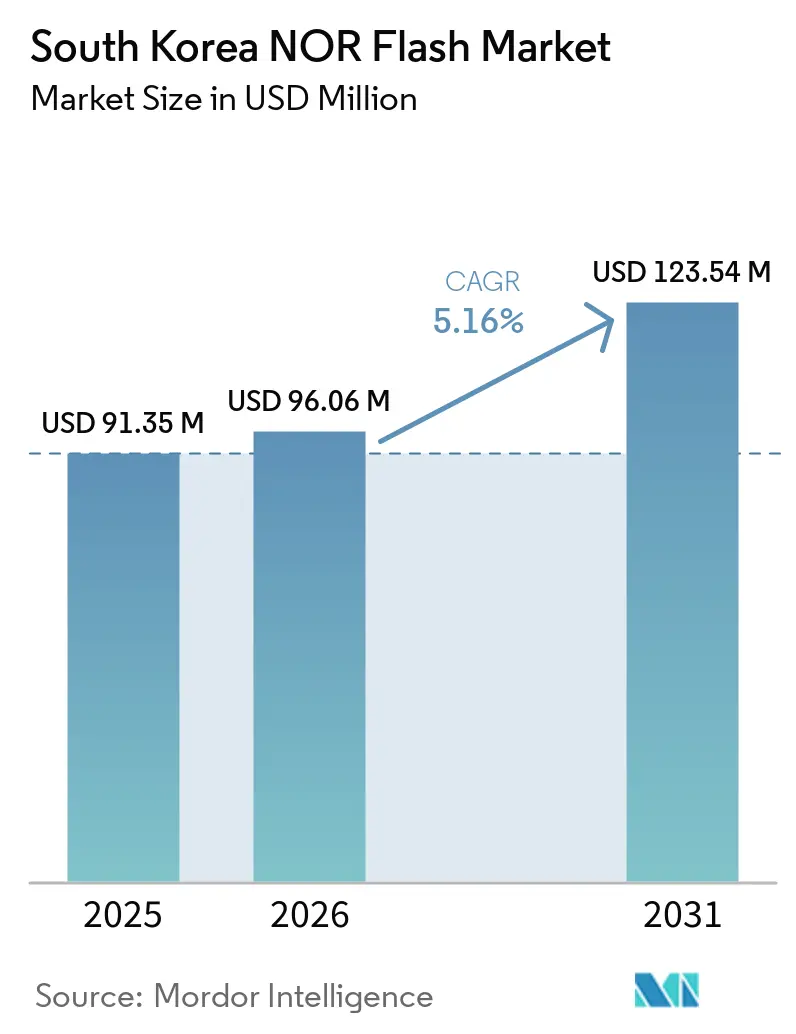

| Base Year Market Size (2025) | USD 91.35 Million |

| Market Size (2026) | USD 96.06 Million |

| Market Size (2031) | USD 123.54 Million |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea NOR Flash Market Analysis by Mordor Intelligence

The South Korea NOR Flash market was valued at USD 91.35 million in 2025 and estimated to grow from USD 96.06 million in 2026 to reach USD 123.54 million by 2031, at a CAGR of 5.2% during the forecast period 2026-2031. The market entered a steadier demand phase in 2026, supported by automotive electronics, 5G-enabled edge infrastructure, and rising AI-linked server requirements across domestic electronics and communication systems. South Korea remains one of the most important electronics manufacturing locations in Asia, so demand comes from a dense base of automotive OEMs, semiconductor fabs, equipment makers, and communication device suppliers. The country’s large 5G subscriber base and strong device ecosystem are widening the use of NOR Flash in edge nodes, communication SoCs, and firmware-heavy embedded systems. Supply conditions have also turned tighter than past cycles because AI server hardware is absorbing more NOR content per system, while automotive and industrial qualifications keep the approved supplier pool limited. This leaves the South Korea NOR Flash market with clear room in automotive-grade, higher-density, and higher-bandwidth products, even as foundry competition and memory substitution remain the main checks on growth.

Key Report Takeaways

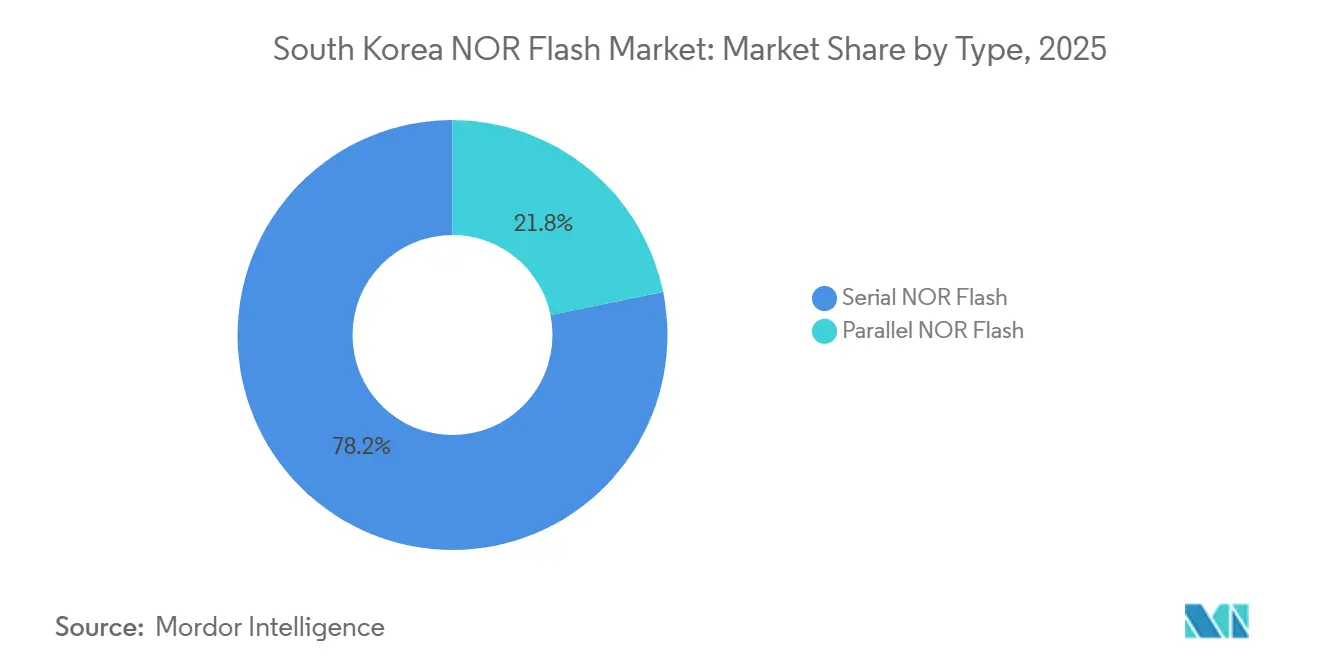

- By type, Serial NOR Flash held 78.2% share in 2025, while Parallel NOR Flash remained concentrated in legacy industrial and communication niches, and no separate fastest-growth CAGR for type was stated in the source draft.

- By interface, Quad SPI held 46.1% share in 2025, while Octal and xSPI devices are projected to expand at 9.7% CAGR through 2031.

- By density, the 16 Mb (greater than 8 Mb) NOR tier held a 27.4% share in 2025, while the 128 Mb (greater than 64 Mb) NOR tier is projected to grow at a 7.1% CAGR through 2031.

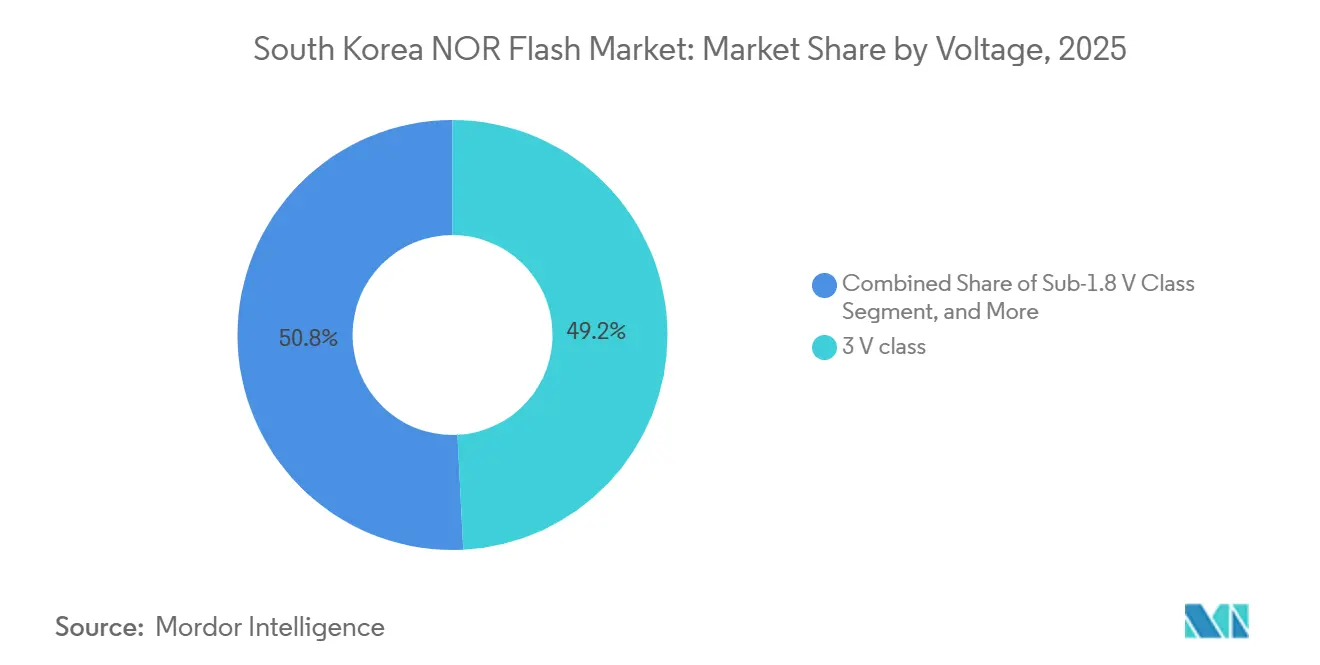

- By voltage, the 3 V class held 49.2% share in 2025, while the Sub-1.8 V class is forecast to expand at 8.6% CAGR through 2031.

- By end-user application, automotive held a 34.1% share in 2025 and had the strongest growth outlook in the source draft, though no separate CAGR figure was provided.

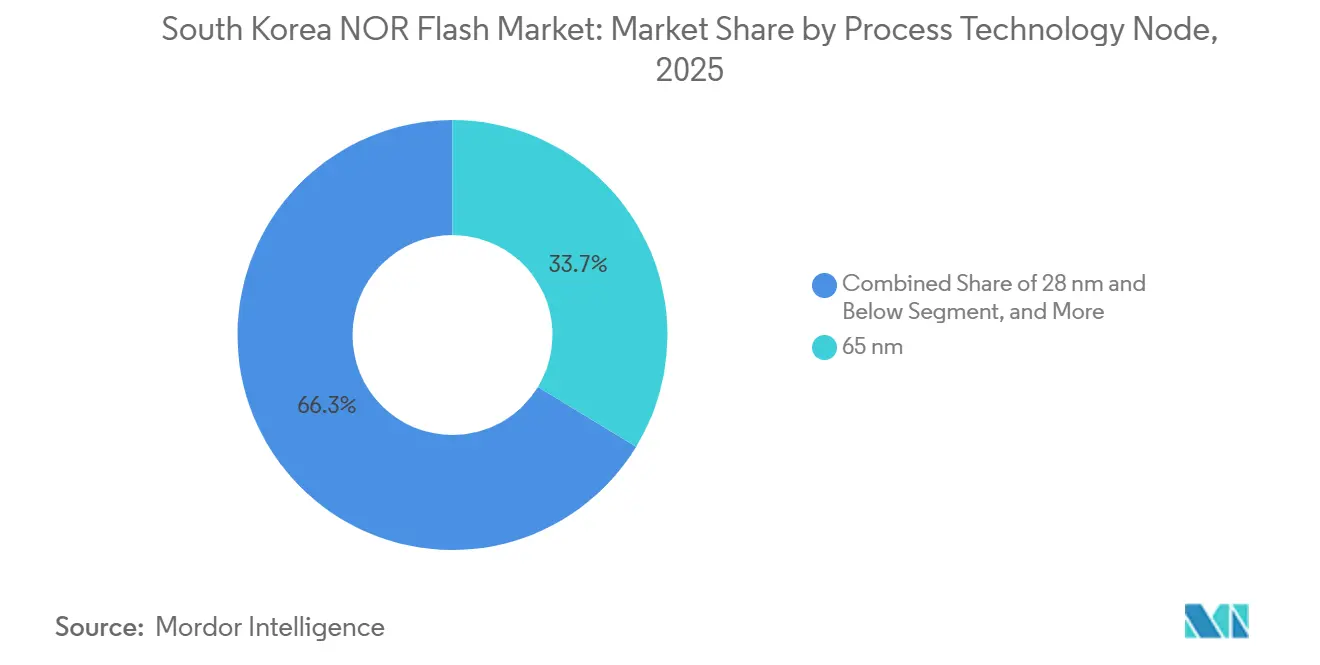

- By process technology node, 65 nm held 33.7% share in 2025, while the 28 nm and below tier is projected to grow at 8.4% CAGR through 2031.

- By packaging type, BGA and FBGA held 41.6% share in 2025, while WLCSP and CSP formats are projected to grow at 6.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South korea participates in a competitive field that extends beyond its own borders. The market landscape in the global nor flash industry outlined by Mordor Intelligence covers that wider structure.

South Korea NOR Flash Market Trends and Insights

Driver Imapct Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Digitalization and Data-Centric Applications | +1.2% | Global, with South Korea as a core APAC hub | Short term (≤ 2 years) |

| Expansion of 5G-Enabled IoT Edge Nodes | +1.0% | South Korea, APAC core | Short term (≤ 2 years) |

| Rapid ADAS and Smart-Vehicle Adoption | +0.9% | South Korea and North America and EU | Medium term (2-4 years) |

| Government Incentives for Domestic Chip Supply Chain | +0.6% | South Korea-specific, spillover to APAC | Medium term (2-4 years) |

| Wafer-Level CSP Uptake in Wearable Medical Devices | +0.4% | Global, concentrated in Asia-Pacific and EU | Medium term (2-4 years) |

| Rise of Chiplet-Based Heterogeneous Integration Requiring Code-Storage Die | +0.3% | Global, with concentration in East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Digitalization and Data-Centric Applications

AI-linked server systems are pulling, NOR Flash demand far beyond its older consumer and industrial base, and that shift is now shaping the South Korea NOR Flash market as well. EE Times reported that each Nvidia GB200 NVL72 rack requires more than 30 NOR Flash devices, up from 3 to 5 in earlier AI server generations, while NOR content per rack exceeded USD 600 and is expected to approach USD 900 within 2 years. That pull matters in South Korea because domestic OEMs, electronics manufacturers, and infrastructure buyers are procuring more AI compute systems for local deployment and export-linked programs. NOR Flash still handles secure boot, firmware initialization, and XiP functions that NAND does not serve well in latency-sensitive operations, so it remains embedded in the control layer of these systems. The supply effect is already visible, with Winbond indicating its NOR Flash capacity was fully booked through 2026 and 2027, which keeps allocation tight for automotive, IoT, and industrial buyers.[1]Winbond, “Winbond Announces 2025 Full Year Business Results,” Winbond, winbond.com

Expansion of 5G-Enabled IoT Edge Nodes

The South Korea NOR Flash market is also benefiting from the country’s highly advanced 5G base, as firmware-heavy gateways, routers, and edge modules depend on reliable code storage. South Korea had 33 million 5G subscribers in early 2024 across SK Telecom, KT, and LG U+, which keeps the installed base for firmware-driven connected devices unusually large. These devices require reliable XiP behavior and fast boot response, which help NOR Flash maintain its position in fixed wireless access units, industrial controllers, and smart-city systems. A 2025 product case from Bivocom showed 5G IoT routers shipping with 64 MB of NOR Flash to support dual firmware partitions and zero-downtime OTA updates, reflecting the direction of connected edge design. As eRedCap, 5G NR variants, and local edge AI modules spread more widely, the South Korean NOR Flash market is likely to add volume through connected endpoints rather than a single flagship device category.

Rapid ADAS and Smart-Vehicle Adoption

Automotive electronics remain one of the strongest growth engines for the South Korean NOR Flash market, as code storage requirements are rising rapidly in ADAS, digital cockpits, and zonal control systems. Infineon’s SEMPER family received ASIL-D certification from SGS-TÜV in May 2025, a certification level that reflects the strong shift in automotive memory requirements toward functional safety and high-reliability boot memory. Winbond’s W35T Octal NOR line supports up to 400 MB/s continuous read throughput over JEDEC xSPI, which fits the need for immediate code access in next-generation vehicle controllers. Firmware images are also getting larger as vehicles move toward centralized compute and software-defined features, which is pushing adoption toward 128 Mb to 256 Mb devices rather than the older 16 Mb to 64 Mb range. AEC-Q100 Grade 1 and ISO 26262 requirements screen out weaker suppliers and support the position of established vendors with proven automotive portfolios in the South Korea NOR Flash market.

Government Incentives for Domestic Chip Supply Chain

Policy support is strengthening the operating backdrop for the South Korea NOR Flash market, even though most direct investment still targets broader semiconductor capacity rather than stand-alone NOR capacity. Businesskorea reported that the amended K-Chips Act raised facility investment tax credits to 20% for large and medium enterprises and 30% for SMEs, and extended semiconductor R&D tax credits through 2031. The Korea Times also reported a KRW 26 trillion (USD 19 billion) investment covering finance, infrastructure, and R&D to strengthen domestic semiconductor capabilities. Yonhap said the Yongin semiconductor cluster was designated a national industrial complex in December 2024, and that Samsung Electronics and SK Hynix committed a combined KRW 1,000 trillion (USD 750 billion) across the cluster. The more immediate benefit for NOR Flash demand is likely to come from stronger local design, testing, packaging, and procurement ecosystems rather than from a near-term jump in dedicated NOR wafer starts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D And Fab-Conversion Costs | -1.2% | Global, with higher relative impact on APAC-based suppliers | Long term (≥ 4 years) |

| Availability Of Substitutes, SLC NAND And MRAM | -0.9% | Global | Medium term (2-4 years) |

| Stringent Automotive AEC-Q100 Reliability Hurdles | -0.5% | South Korea and EU and North America | Medium term (2-4 years) |

| Tight Foundry Capacity At Advanced Nodes | -0.4% | APAC core, spillover to North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High R&D and Fab-Conversion Costs

Advanced-node NOR manufacturing remains expensive because the additional process steps do not deliver density gains on the same scale as in other memory categories. EE Times reported that Macronix redirected capacity toward MLC NAND in 2025-2026 and delayed 3D NOR mass production to 2027 because node conversion remained highly capital-intensive. A 2025 IEDM paper showed that Gb-density NOR Flash chiplets require Cu hybrid bonding and advanced CMOS integration, keeping the technical bar high even before commercial-scale-up begins.[2]Hang-Ting Lue et al., “Architecture Design And Simulation Of A Novel 3D Stackable Split-Gate 1.5T NOR Flash For Gb-Density Embedded Flash Chiplets With Low Latency And Low Power Sensing,” IEEE, ieee.orgMicrochip and UMC said their 28 nm SuperFlash Gen 4 automotive platform required specialized process adaptation beyond standard CMOS flows, underscoring why newer NOR nodes do not expand as quickly as demand would suggest.[3]Microchip Technology, “SST And UMC Announce Availability Of 28nm SuperFlash Gen 4 Auto Grade 1 Platform,” Microchip Technology, microchip.com These economics keep supply concentrated among a few integrated vendors and can slow the pace at which the South Korea NOR Flash market receives additional qualified supply.

Availability of Substitutes, SLC NAND And MRAM

The South Korea NOR Flash market also faces substitution pressure in applications where storage density, endurance, or cost matter more than byte-addressable XiP. SLC NAND is gaining room in telematics and data-logging systems because firmware can be shadowed into DRAM at boot, which reduces the value of direct execution in those use cases. Microsoft Research noted in HotOS 2025 that STT-MRAM and RRAM are credible alternatives for AI edge workloads and can be integrated with advanced-node CMOS, which keeps pressure on future non-volatile memory choices. Winbond’s 2025 product guide included the W35N-JW Octal NAND line with 240 MB/s read throughput and much faster erase behavior, directly targeting OTA firmware update workloads that often overlap with NOR Flash design slots. NOR Flash still keeps a defensible position in secure boot, ADAS code storage, and safety-critical firmware, but the addressable volume in non-XiP applications is under steady pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serial NOR Dominance Deepens Across Platforms

Serial NOR Flash accounted for 78.2% of the South Korea NOR Flash market in 2025, which kept it far ahead of parallel NOR across automotive, consumer, industrial, and communication designs. The segment’s strength lies in its fit with compact SoC layouts, lower pin count, and simpler board design, all of which matter in space-constrained electronics. That advantage is especially relevant in wearables, IoT sensors, communication modules, and automotive controllers, where board area and routing simplicity affect both cost and qualification cycles. Parallel NOR Flash still serves a smaller installed base in legacy industrial control systems and communication equipment, where deterministic access behavior remains important for older architectures. Even with those niches intact, the South Korean NOR Flash industry is now clearly centered on serial products, as most new platforms are designed around SPI-based interfaces rather than wide parallel buses.

Winbond’s February 2026 update to its W25Q-RV series added on-chip ECC and checksum functions for automotive ISO 26262-oriented designs within a standard serial form factor, demonstrating how quickly serial products are adopting features once tied to more specialized solutions. That trend weakens one of the parallel NORs ’ remaining advantages in safety-conscious applications, since error management and functional support are increasingly built into serial families. The AI server cycle also supports serial share gains because management controllers, NICs, and board-level firmware modules now favor higher-density serial devices over bulkier parallel alternatives. Macronix reported combined net sales of NTD 6.047 billion (USD 184 million) for January and February 2026, up 55.6% year on year, with recovery led mainly by serial NOR demand in automotive and communication channels. That mix leaves serial NOR positioned to extend its lead through 2031 as the South Korea NOR Flash market moves toward denser, faster, and more software-heavy end systems.

By Interface: Octal xSPI Redefines Bandwidth Expectations

Quad SPI held 46.1% of South Korea NOR Flash market share in 2025, which reflects its broad installed base across mainstream IoT, consumer, and communication SoCs. At the same time, Octal and xSPI products are projected to grow at 9.7% CAGR through 2031, making them the fastest-growing interface tier in the South Korea NOR Flash market. That shift is being driven by zonal automotive ECUs, AI edge processors, and more complex communication hardware that need much faster boot-code access than older Quad SPI links can provide. Buyers are not only seeking speed, they are also seeking standardization, because next-generation vehicle and industrial platforms want predictable firmware behavior across suppliers. This is pushing the market toward JEDEC-aligned xSPI devices with higher throughput and lower integration friction.

Winbond’s W35T Octal NOR family delivers up to 400 MB/s continuous read throughput using JEDEC xSPI with DDR operation at 200 MHz, which is far above the bandwidth of its earlier Quad SPI line. GigaDevice’s GD25NX series, launched in November 2025, followed the same path with a dual-voltage design, 400 MB/s throughput, and lower read current for systems built around 1.2 V host logic.[4]GigaDevice, “GD25/55 Automotive SPI NOR Flash, AEC-Q100 Grade 1, 2Mb-2Gb,” GigaDevice, gigadevice.com Quad SPI will still hold large volumes in cost-sensitive equipment that refreshes on a slower cycle, especially in networking, home electronics, and mid-range IoT modules. Even so, the South Korea NOR Flash industry is moving toward a two-speed interface structure, where Quad SPI stays important for value segments while Octal and xSPI capture the performance tier.

By Density: Higher-Density Devices Are Pulled By ADAS Firmware Growth

The 16 Mb (greater than 8 Mb) tier accounted for 27.4% of the South Korea NOR Flash market in 2025, indicating that demand still comes from communication SoCs, IoT nodes, and entry-level embedded control products. The fastest-growing density band is 128 Mb (greater than 64 Mb), which is projected to advance at 7.1% CAGR through 2031 as firmware images continue to expand. In automotive systems, the reason is clear: domain controllers and digital cockpit platforms now need space for multi-image firmware, cryptographic boot loaders, rollback protection, and safety monitors within a single code-storage plan. The same pattern is appearing in AI servers and high-end network hardware, where management firmware, security layers, and board initialization stacks are growing more complex. This makes the density mix of the South Korean NOR Flash market more favorable to mid- to high-density products than in earlier cycles.

Lower-density tiers such as 2 Mb, 4 Mb, and 8 Mb still have a role, but they face pressure from embedded EEPROM, small OTP solutions, and lower-cost alternatives in simple sensors. At the other end of the range, 256 Mb and above are gaining traction for FPGA configuration, AI accelerator support, and server management. Winbond’s 2025 product guide introduced the W25Q-NE 1.2 V series up to 256 Mb, aimed at AI accelerators and high-performance NIC boot applications, which shows how the upper density bands are moving into mainstream compute hardware. A 2025 Nature paper also demonstrated a full-featured 2D NOR Flash chip built through system integration above a commercial CMOS die, with 20 ns program and erase timing and 94.3% full-chip yield, which points to a longer-term path for higher-density code storage beyond traditional scaling limits. These trends suggest that density growth in the South Korea NOR Flash market will come less from simple unit volume and more from richer firmware content per device.

By Voltage: Sub-1.8 V Class Gains Momentum In AI And Wearable Nodes

The 3V class held a 49.2% share in 2025, indicating it still anchors large portions of the South Korean NOR Flash market in industrial, communication, and mainstream consumer designs. The fastest-growing voltage tier is the Sub-1.8 V class, which is projected to expand at 8.6% CAGR through 2031 as host processors move to more advanced logic nodes. This shift matters because newer AI, wearable, and edge platforms are designed around lower I/O voltages, and external level shifting adds both cost and design complexity. As a result, low-voltage NOR is no longer a niche option tied only to a few power-sensitive devices. It is becoming a practical requirement for more advanced system architectures, especially where thermal budgets and board space are tight.

GigaDevice expanded its GD25UF family in March 2026 to cover 8 Mb to 256 Mb at 1.14 V to 1.26 V, with stated power savings of 50% to 70% compared to conventional 1.8 V Flash. Winbond also positioned its 1.2 V SpiFlash line toward AI accelerators, high-compute NIC cards, and wearable devices, showing that low-voltage NOR now serves both power-sensitive and performance-heavy designs. The 1.8 V class remains relevant for mid-range mobile and IoT systems because it balances efficiency with broad compatibility across mixed-voltage boards. Wide-voltage products also keep a useful role in wearables and medical monitors, since one qualified part can bridge multiple system power configurations and simplify procurement for the South Korea NOR Flash market.

By End-User Application: Automotive Keeps Leadership As Firmware Loads Rise

Automotive accounted for 34.1% of South Korea NOR Flash market share in 2025, and it also carried the strongest growth outlook among application segments in the source draft. That leadership comes from rising ADAS content, over-the-air update needs, secure boot requirements, and the shift toward software-defined vehicle architecture. Automotive memory demand is not only growing in unit terms, it is also moving toward higher densities, faster interfaces, and stricter qualification thresholds. That change favors suppliers with AEC-Q100 Grade 1 readiness, ISO 26262 alignment, and proven support across zonal control, cockpit, and gateway platforms. For the South Korea NOR Flash market, this means the automotive segment is shaping both product mix and vendor selection more strongly than any other end-user group.

Infineon’s SEMPER family covers 256 MB to 2 GB and carries ASIL-D certification, while GigaDevice’s automotive NOR portfolio spans 2 MB to 2 GB, with Grade 1 positioning and support for high-throughput interfaces. Consumer electronics still contribute meaningful volumes through devices such as TWS earbuds, smart TVs, cameras, and home networking products, but growth is slower because density per device is maturing in several mass categories. Communication equipment, including 5G routers, optical network gear, and access infrastructure, remains important because these systems depend on reliable firmware memory for boot and management tasks. Industrial and medical applications are smaller than automotive in volume, but they continue to support premiumization through long-life, ruggedized, and miniaturized designs, which broadens the value capture of the South Korea NOR Flash industry.

By Process Technology Node: Advanced Nodes Drive Performance

The 65 nm node held 33.7% share in 2025, which kept it as the largest single process tier in the South Korea NOR Flash market because mature-node production still suits cost-sensitive applications. Even so, the 28 nm and below tier is projected to grow at 8.4% CAGR through 2031, making it the fastest-growing node range in the source draft. The driver is not simple shrink for its own sake. It is the need for lower-voltage operation, higher endurance, faster access, and better fit with advanced host logic in automotive and AI systems. This shift does not remove the value of mature nodes, but it does increase the importance of selective migration where performance or integration benefits justify the extra process effort.

Microchip and UMC announced immediate production availability of the 28 nm SuperFlash Gen 4 Automotive Grade 1 platform in January 2026, with AEC-Q100 Grade 1 qualification, read access below 12.5 ns, and more than 100,000 endurance cycles. Winbond manufactures its W35T Octal NOR on a 58 nm process, showing that the 55 nm to 58 nm range still plays a central role in high-performance automotive code storage. A 2025 paper in Electronics showed that embedded NOR Flash on 55 nm CMOS with a NORD cell structure reached 2.5 million program and erase cycles, which suggests there is still room to improve mature-node endurance without a full move to smaller nodes. The South Korea NOR Flash market therefore appears set to use a layered node strategy, with 28 nm and below growing fastest while 65 nm and 55 nm remain central for cost, supply continuity, and long-life applications.

By Packaging Type: WLCSP And CSP Gain Ground In Miniaturized Designs

BGA and FBGA held 41.6% share in 2025, which made them the largest packaging class in the South Korea NOR Flash market by packaging type. Their lead reflects the needs of higher-density automotive and industrial products, where signal integrity, routing flexibility, and thermal behavior all carry more weight than ultra-small footprint alone. WLCSP and CSP are the fastest-growing formats, with a projected 6.7% CAGR through 2031, because wearable, medical, and edge sensor designs continue to shrink in size. That growth is not only about smaller packages. It is also about reducing stack height, board occupation, and package-related power overhead in compact electronics. This packaging shift matters because it changes where value is created, from wafer processing and package engineering to test capability and yield control.

GigaDevice’s WLCSP offering for SPI NOR and NAND is aimed directly at wearables and IoT, and the company positions these packages for space-limited designs that cannot absorb traditional plastic package overhead. The GD25NX 128 Mb xSPI NOR family is available in both TFBGA24 and WLCSP, which lets OEMs use the same die across board-mounted and chip-scale layouts depending on design priorities. QFN and SOIC still hold a durable place in home appliances, industrial sensors, and mid-range IoT controllers because they are easier to assemble, inspect, and rework. The remaining packaging group, including TSOP and specialized ceramic options, stays limited in volume but supports high-value niches such as defense, aerospace, and long-life industrial hardware in the South Korea NOR Flash market.

Geography Analysis

The South Korea NOR Flash market size stood at USD 96.1 million in 2026, and the country remains one of the more strategically important demand centers for code-storage memory in Asia because it combines automotive, communication, and advanced electronics activity in one market. SK Hynix broke ground on the first fab in the Yongin cluster in February 2025, and the investment for that first fab was raised to KRW 31 trillion, or USD 21.7 billion, by February 2026, with the first cleanroom targeted for February 2027. Samsung Electronics is also investing KRW 20 trillion, or USD 14 billion, in next-generation R&D infrastructure at the adjacent Giheung advanced system semiconductor complex by 2030. The Korea Herald reported that close to 90 materials and equipment firms planned to locate in Yongin by early 2026, which points to a denser domestic semiconductor support network. This ecosystem matters for NOR Flash because better local packaging, test, and component support can shorten procurement cycles even when finished chips are sourced from overseas vendors.

Within South Korea, demand clusters most heavily around the Seoul-Gyeonggi corridor and the Chungcheong industrial zone, where electronics manufacturing, automotive electronics development, and module design are most concentrated. Cheongju adds a smaller but relevant domestic supply link because SK Hynix System IC operates a 110 nm eFlash foundry for logic and embedded non-volatile memory applications, with positioning that reaches wearable, IoT, and selected automotive uses. South Korea’s 33 million 5G subscribers in early 2024, including 15.9 million on SK Telecom alone, support a wide installed base of routers, gateways, and connected devices that depend on stable boot memory. The result is a domestic demand map shaped less by broad regional spread and more by a dense set of electronics, telecom, and automotive nodes concentrated in a few industrial belts.

In a wider APAC comparison, South Korea has a more premium end-application mix than many neighboring markets because automotive and communication electronics account for a larger portion of demand than low-cost mass consumer devices. That raises the importance of qualified supply, safety certification, and high-bandwidth interfaces in local buying decisions. South Korea also benefits from the K-Chips Act changes passed in February 2025, which raised tax incentives and extended semiconductor R&D support to 2031. Those measures improve the economics of local chip design, validation, and test operations, and they should help shorten the path from product design to qualification in the South Korea NOR Flash market. Even when final assembly happens abroad, demand is often counted at the Korean design and sourcing stage because vehicles, appliances, and communication systems are specified and qualified through domestic OEM and Tier-1 programs.

Mordor Intelligence provides coverage of the nor flash market across other key regional markets, including Europe and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India, Japan, Italy, China, United Kingdom, Germany, and Mexico incorporating local coverage and market participation, as required.

Competitive Landscape

The South Korea NOR Flash market is supplied by a relatively concentrated global vendor group, with Winbond holding 23% of global NOR share and GigaDevice holding 18.5% in 2024, followed by Macronix, Infineon, ISSI, Renesas, and Microchip Technology. Competition is now splitting into two clear paths, one focused on automotive-grade qualification and performance interfaces, and another focused on cost, density coverage, and faster commercialization in consumer and IoT slots. GigaDevice strengthened its expansion capacity through a January 2026 Hong Kong listing that raised HKD 4.68 billion, or USD 600 million, with 40% of proceeds allocated to R&D capability enhancement. That move matters because automotive-grade NOR development requires both capital and long validation cycles, and the stronger balance sheet improves GigaDevice’s ability to compete for Korean design wins.

Infineon represents the premium qualification strategy well, because its SEMPER portfolio covers 256 Mb to 2 GB and gained ASIL-D certification in May 2025 for use in ADAS, zone control, and digital cockpit systems. Winbond is pushing both interface performance and security, with its Octal NOR family targeting high-throughput automotive and compute designs and its secure flash approach aimed at firmware integrity and protected boot paths. Macronix is pursuing a technology repositioning through 3D NOR, with contribution to operations expected in 2026 and mass production targeted for 2027, which could change the density economics of high-end code storage if execution remains on track. Smaller vendors such as Zbit Semiconductor, Puya Semiconductor, and Giantec are more active where price sensitivity is higher, especially in lower-density consumer and IoT products. That creates margin pressure in the lower end of the market, but it does not fully break the hold of larger suppliers in automotive and safety-critical applications.

Another competitive filter is the growing importance of standards and qualification depth, because Korean OEMs increasingly want proven AEC-Q100, ISO 26262, and JEDEC xSPI alignment rather than only low purchase cost. Microchip and UMC’s 28 nm automotive platform, GigaDevice’s dual-voltage xSPI products, and Winbond’s advanced Octal NOR lines all show that technical readiness has become a practical entry barrier in the South Korea NOR Flash market. For Korean buyers, the best-positioned suppliers are those that combine long product life, broad package options, secure firmware features, and enough capacity discipline to serve both automotive and AI-linked demand. This keeps the competitive field open enough for product differentiation, but not open enough for unqualified new entrants to scale quickly.

South Korea NOR Flash Industry Leaders

Winbond Electronics Corporation

Macronix International Co. Ltd

GigaDevice Semiconductor Inc.

Infineon Technologies AG

Microchip Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GigaDevice expanded its GD25UF series 1.2 V ultra-low-power SPI NOR Flash to a full density range of 8 Mb through 256 Mb, all in mass production with SOP8, WSON8, USON8, and WLCSP packages. The devices target AI computing, wearables, hearables, and medical IoT applications.

- February 2026: Winbond announced record capital expenditure of NTD 42.1 billion (USD 1.33 billion) for 2026, targeting a 30% to 40% year-on-year increase in NOR and NAND flash shipments and expanding its Kaohsiung fab from 15,000 to 24,000 wafers per month by end-2026.

- January 2026: Winbond's W35T-NW Octal NOR Flash in 1 Gb and 2 Gb densities entered sampling status, delivering 400 MB/s continuous read throughput, built-in ECC, ASIL-D compliance, and AEC-Q100 Grade 2 automotive qualification.

- January 2026: SST, a Microchip Technology subsidiary, and UMC announced immediate production availability of the 28 nm SuperFlash Gen 4 Automotive Grade 1 platform on UMC's 28HPC+ process, achieving AEC-Q100 Grade 1 qualification with read access times below 12.5 ns and over 100,000 endurance cycles.

South Korea NOR Flash Market Report Scope

The NOR Flash Market in South Korea refers to the segment of non-volatile memory used in Korean electronics, automotive, industrial, and consumer device applications for fast code storage and reliable boot-up. It is typically driven by demand in automotive, consumer electronics, and industrial applications, where quick read access and high reliability are important.

The South Korea NOR Flash Market Report is Segmented by Type (Serial NOR, and Parallel NOR), Interface (SPI Single / Dual, Quad SPI, and More), Density (2 Mb and Less NOR, 4 Mb (less than 2 Mb) NOR, 8 Mb (greater than 4 Mb) NOR, 16 Mb (greater than 8 Mb) NOR, 32 Mb (greater than 16 Mb) NOR, 64 Mb (greater than 32 Mb) NOR, 128 Mb (greater than 64 Mb) NOR, 256 Mb (greater than 128 Mb) NOR, and Greater Than 256 Mb), Voltage (3 V Class, 1.8 V Class, Wide-Voltage (1.65 V - 3.6 V), and Sub-1.8 V Class, 1.2 V and Similar), Application (Consumer Electronics, Communication, and Industrial), Process Node (90 Nm and Older, 65 nm, 55 nm (Including 58 nm), 45 nm, and 28 nm and Below), and Packaging (WLCSP/CSP, QFN / SOIC, and BGA / FBGA). The Market Forecasts are Provided in Terms of Value (USD).

| Serial NOR Flash |

| Parallel NOR Flash |

| SPI Single / Dual |

| Quad SPI |

| Octal and xSPI |

| 2 Mb and Less NOR |

| 4 Mb (less than 2 Mb) NOR |

| 8 Mb (greater than 4 Mb) NOR |

| 16 Mb (greater than 8 Mb) NOR |

| 32 Mb (greater than 16 Mb) NOR |

| 64 Mb (greater than 32 Mb) NOR |

| 128 Mb (greater than 64 Mb) NOR |

| 256 Mb (greater than 128 Mb) NOR |

| Greater Than 256 Mb |

| 3 V Class |

| 1.8 V Class |

| Wide-Voltage (1.65 V - 3.6 V) |

| Sub-1.8 V Class, 1.2 V and Similar |

| Consumer Electronics |

| Communication |

| Automotive |

| Industrial |

| Rest of Applications |

| 90 nm and Older |

| 65 nm |

| 55 nm (Including 58 nm) |

| 45 nm |

| 28 nm and Below |

| WLCSP / CSP |

| QFN / SOIC |

| BGA / FBGA |

| Rest of Packaging Types |

| By Type (Value, Volume) | Serial NOR Flash |

| Parallel NOR Flash | |

| By Interface (Value) | SPI Single / Dual |

| Quad SPI | |

| Octal and xSPI | |

| By Density (Value) | 2 Mb and Less NOR |

| 4 Mb (less than 2 Mb) NOR | |

| 8 Mb (greater than 4 Mb) NOR | |

| 16 Mb (greater than 8 Mb) NOR | |

| 32 Mb (greater than 16 Mb) NOR | |

| 64 Mb (greater than 32 Mb) NOR | |

| 128 Mb (greater than 64 Mb) NOR | |

| 256 Mb (greater than 128 Mb) NOR | |

| Greater Than 256 Mb | |

| By Voltage (Value) | 3 V Class |

| 1.8 V Class | |

| Wide-Voltage (1.65 V - 3.6 V) | |

| Sub-1.8 V Class, 1.2 V and Similar | |

| By End-User Application (Value, Volume) | Consumer Electronics |

| Communication | |

| Automotive | |

| Industrial | |

| Rest of Applications | |

| By Process Technology Node (Value) | 90 nm and Older |

| 65 nm | |

| 55 nm (Including 58 nm) | |

| 45 nm | |

| 28 nm and Below | |

| By Packaging Type (Value) | WLCSP / CSP |

| QFN / SOIC | |

| BGA / FBGA | |

| Rest of Packaging Types |

Key Questions Answered in the Report

What is the 2026 size and 2031 outlook for South Korea NOR Flash?

The South Korea NOR Flash market stands at USD 96.06 million in 2026 and is projected to reach USD 123.54 million by 2031 at a 5.16% CAGR.

Which application leads demand in South Korea NOR Flash?

Automotive led with 34.1% share in 2025, supported by ADAS growth, secure boot needs, and software-defined vehicle architecture.

Why are Octal and xSPI devices gaining traction in South Korea?

They are the fastest-growing interface tier at 9.7% CAGR because automotive SoCs and AI edge processors need faster boot-code access than Quad SPI can provide.

Which density range is expanding the fastest?

The 128 Mb (greater than 64 Mb) tier is projected to grow at 7.1% CAGR, mainly because ADAS, digital cockpit, and AI server firmware loads are increasing.

What is driving low-voltage NOR adoption in South Korea?

Sub-1.8 V products are growing at 8.6% CAGR as host processors shift to advanced logic nodes and designers try to avoid level shifters and reduce power draw.

What is the biggest supply-side risk for buyers?

The main risk is tight advanced-node capacity and high conversion cost, which keep supply concentrated among a few qualified vendors and can extend allocation pressure.

Page last updated on: