France NOR Flash Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

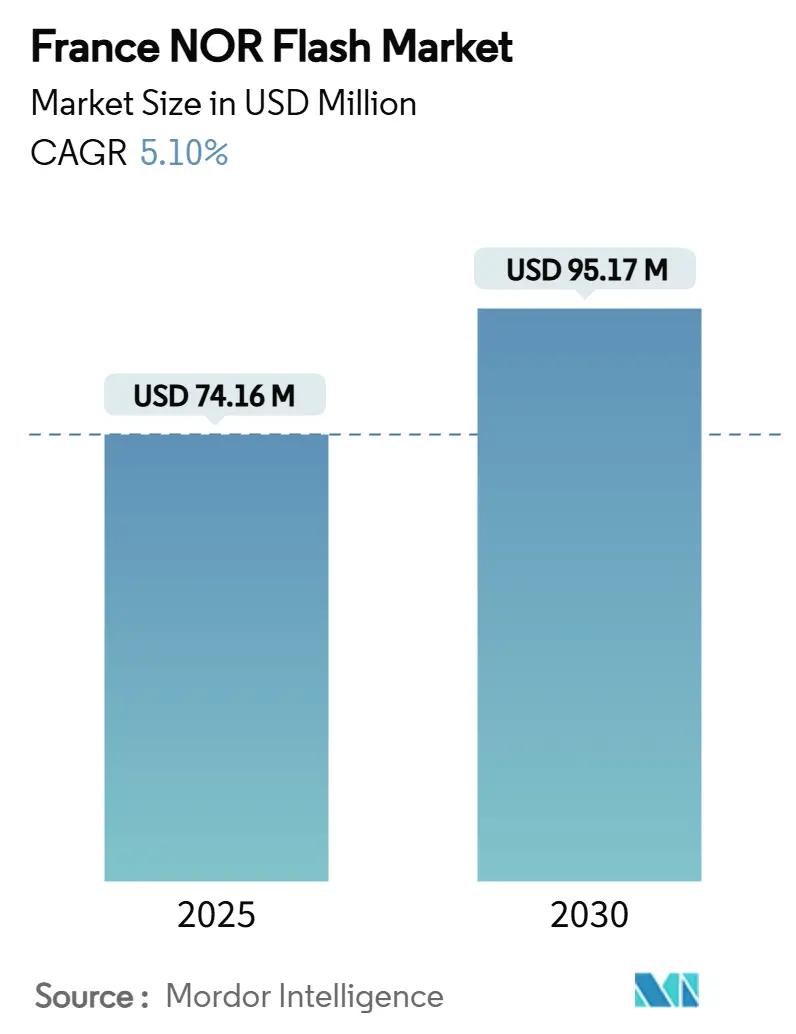

| Market Size (2025) | USD 74.16 Million |

| Market Size (2030) | USD 95.17 Million |

| Growth Rate (2025 - 2030) | 5.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France NOR Flash Market Analysis by Mordor Intelligence

The France NOR flash market size is estimated at USD 74.16 million in 2025, and is expected to reach USD 95.17 million by 2030, at a CAGR of 5.10% during the forecast period. This expansion is primarily linked to the accelerated deployment of advanced driver-assistance systems in French vehicle production, a steep rise in IoT endpoints across residential and industrial settings, and strong governmental support for semiconductor sovereignty under the France 2030 initiative[1]European Commission, “A Chips Act for Europe,” European Commission, January 18, 2024, europa.eu. . Moreover, national cybersecurity directives are compelling critical-infrastructure suppliers to specify execute-in-place (XIP) NOR parts with secure-boot features, while energy-efficiency goals are steering new designs toward 1.8 V and, increasingly, 1.2 V devices [2]European Commission, “France 2030 Investment Plan,” European Commission, October 12, 2024, europa.eu. . Consequently, memory manufacturers are localising assembly and test activity in innovation clusters such as Grenoble and Sophia Antipolis to shorten logistics lead times and meet regional qualification standards [3]Infineon Technologies, “SEMPER NOR Flash Achieves ASIL-D Certification,” Infineon Technologies Newsroom, May 02, 2025, infineon.com. . Nevertheless, Europe’s 7% share of front-end wafer fabrication constrains near-term supply resilience, prompting policymakers to accelerate incentives under the European Chips Act [4]GigaDevice, “GD25/55 SPI NOR Flash Receives ISO 26262 ASIL-D,” GigaDevice Newsroom, February 06, 2025, gigadevice.com. .

Key Report Takeaways

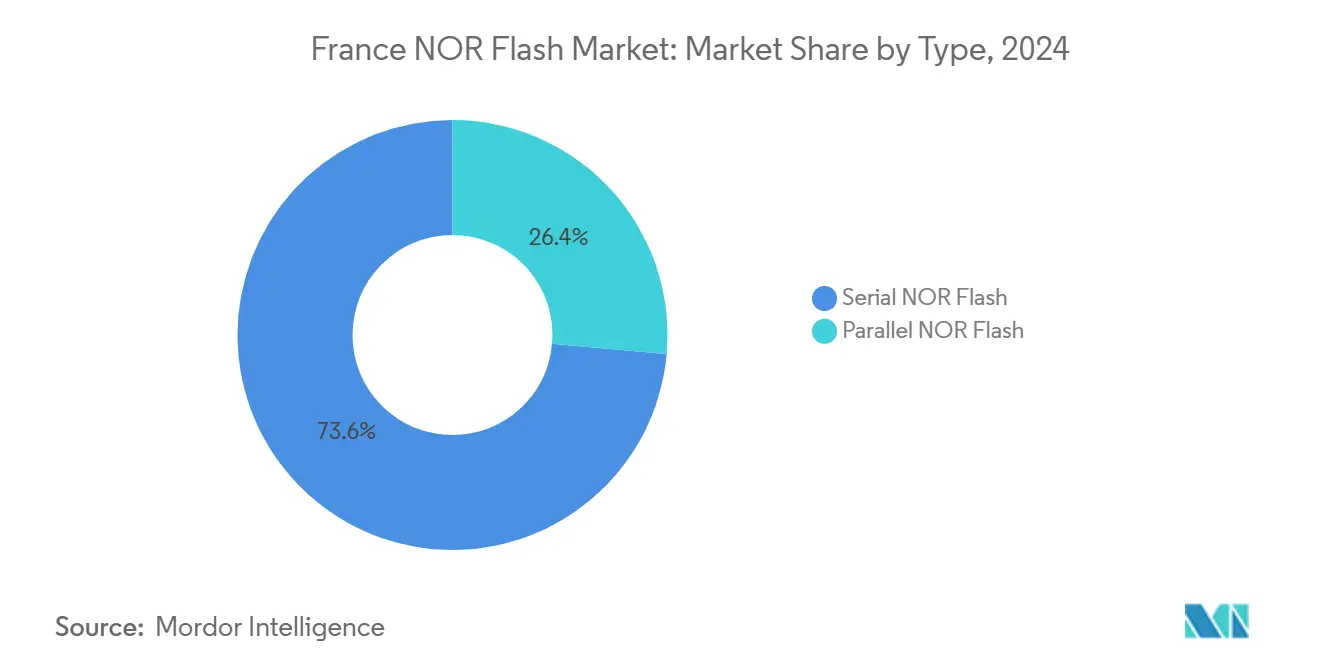

- By type, Serial NOR Flash captured 73.6% of France NOR flash market share in 2024; Parallel NOR holds the remainder while registering slower expansion.

- By interface, SPI Single/Dual led with 45.9% revenue share in 2024, whereas Octal/xSPI is forecast to grow at 5.5% CAGR through 2030.

- By density, the 64–128 Mbit tier accounted for 31.1% of France NOR flash market size in 2024; devices above 256 Mbit exhibit the fastest 5.8% CAGR between 2025–2030.

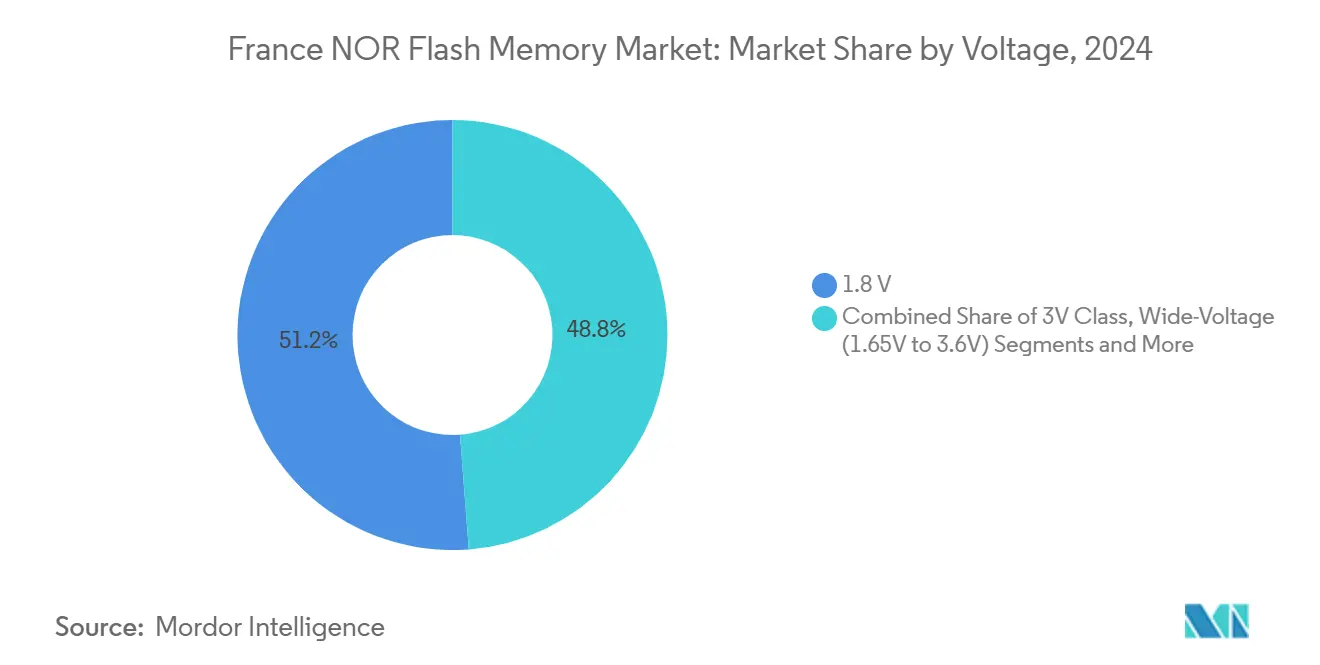

- By voltage, 1.8 V products contributed 51.2% share in 2024 and remain the highest-growing class at 6.8% CAGR.

- By end-user application, consumer electronics delivered 38.7% of 2024 revenue; automotive electronics is advancing at a 7.3% CAGR owing to e-mobility roll-outs.

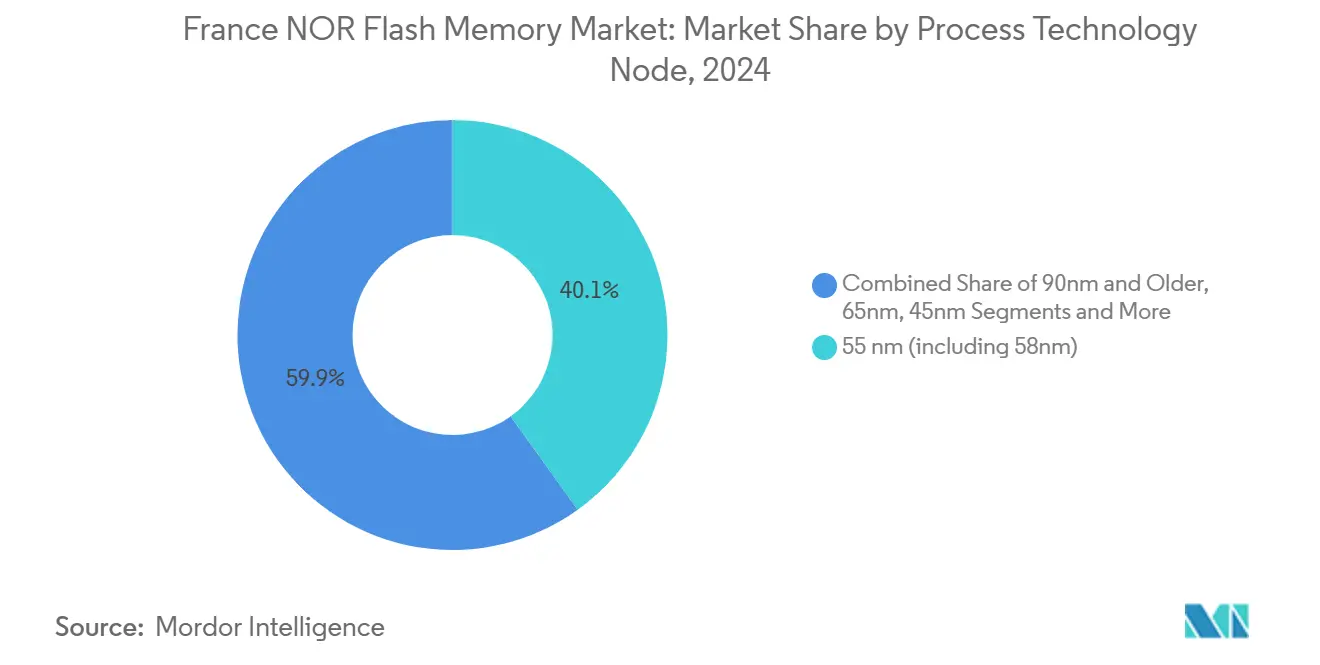

- By process node, 55 nm technology dominated with 40.1% share in 2024, although sub-28 nm solutions are scaling at 5.9% CAGR.

- By packaging, WLCSP/CSP devices commanded 46.3% share in 2024 and record a 7.3% CAGR to 2030.

France contributes to a system defined not by any single country or region but by the interaction of many. The global nor flash market data by Mordor Intelligence represents that combined structure.

France NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in High-Density Storage Demand Across French Consumer Electronics | +1.20% | National, with concentration in manufacturing hubs of Paris, Lyon, and Grenoble | Medium term (2-4 years) |

| Proliferation of IoT and Embedded Systems Leveraging Serial-NOR in Smart-Home and Industrial 4.0 | +1.40% | National, with early adoption in urban centers | Medium term (2-4 years) |

| Rapid ADAS and E-Mobility Adoption Among French OEMs Requiring XIP-Friendly NOR | +1.60% | National, with concentration in automotive manufacturing regions | Long term (≥ 4 years) |

| France 2030 Semiconductor Incentive Scheme Boosting Local NOR Assembly Partnerships | +0.80% | National, with focus on innovation clusters in Grenoble and Sophia Antipolis | Medium term (2-4 years) |

| Cyber-Security Mandates for Critical Infrastructure Driving Secure NOR with Execute-In-Place (XIP) | +0.60% | National, with emphasis on energy and transportation sectors | Short term (≤ 2 years) |

| Linky 2.0 Smart-Meter Roll-out Elevating Endurance-Focused Serial-NOR Volumes | +0.70% | National, with uniform deployment across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in High-Density Storage Demand Across French Consumer Electronics

Premium smartphones, smart televisions, and wearables demand NOR capacities above 128 Mbit for richer firmware, biometric security, and instant-boot requirements. France’s smartphone penetration of 77.5% in 2025 sustains repeat design cycles and favours dual-interface NOR that combines secure-boot with high throughput, thereby strengthening the consumer-electronics contribution to the France NOR flash market[2]European Commission, “France 2030 Investment Plan,” European Commission, October 12, 2024, europa.eu. .

Proliferation of IoT and Embedded Systems Leveraging Serial NOR in Smart-Home and Industrial 4.0

Nationwide smart-meter rollouts, predictive-maintenance sensors, and edge controllers are filling factories and homes with embedded nodes that mandate fail-safe code storage. Serial NOR’s low pin count, low power draw, and execute-in-place capability position it as the default boot memory. Density requirements cluster between 64-128 Mbit, a sweet spot that balances cost and firmware budgets for many sensors and gateways. Industrial integrators favor SPI Single/Dual for backward compatibility with microcontrollers already qualified in long-life machinery [3]Infineon Technologies, “SEMPER NOR Flash Achieves ASIL-D Certification,” Infineon Technologies Newsroom, May 02, 2025, infineon.com. . These use cases underpin the sustained volume core of the France NOR flash market.

Rapid ADAS and E-Mobility Adoption Among French OEMs Requiring XIP-Friendly NOR

Automotive electronics content per vehicle continues to climb as domestic OEMs add Level 2+ driver assistance, digital cockpits, and battery-management systems. Safety-critical code must execute directly from flash, and Serial NOR’s XIP architecture supplies deterministic latency that DDR-based alternatives lack. Design‐in specifications now often exceed 256 Mbit to accommodate complex software stacks and over-the-air update partitions. NOR suppliers with AEC-Q100 grade-1 and ASIL-D certificates gain selection priority, reinforcing automotive pull in the France NOR flash market[5]Kioxia Corporation, “Kioxia and Western Digital Present New 3D Flash Memory Technology,” IEEE ISSCC Proceedings, February 20, 2025, kioxia.com. .

France 2030 Semiconductor Incentive Scheme Boosting Local NOR Assembly Partnerships

Public-private funding pools enhance domestic back-end capacity, encouraging global memory vendors to co-locate assembly and test lines with French EMS partners. Localized packaging shortens logistics lead times, facilitates custom temperature screenings, and expands workforce skill depth in advanced chip-scale packaging [1]European Commission, “A Chips Act for Europe,” European Commission, January 18, 2024, europa.eu. . Knowledge transfer is spurring pilot runs of ruggedized WLCSP tailored for harsh industrial and automotive deployment, anchoring more of the NOR value chain inside national borders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ASPs of Advanced-Node (28 nm & Below) NOR Versus eMMC/eUFS Alternatives | -0.90% | National, with greater impact on consumer electronics manufacturing | Medium term (2-4 years) |

| Fragmented Domestic Semiconductor Ecosystem Limiting Large-Scale NOR Fabrication | -0.70% | National, with concentration in semiconductor manufacturing regions | Long term (≥ 4 years) |

| Stringent EU RoHS and REACH Compliance Increasing Low-Density NOR Qualification Costs | -0.50% | EU-wide, with uniform impact across France | Short term (≤ 2 years) |

| Constrained 28 nm Foundry Capacity in Europe Triggering Supply Volatility | -0.80% | EU-wide, with particular impact on French high-tech manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High ASPs of Advanced-Node NOR Versus eMMC/eUFS Alternatives

At 28 nm and below, per-bit costs of NOR can run 30-40% higher than high-capacity eMMC or eUFS, stressing bill-of-materials targets in mass-market phones and tablets. OEMs respond with hybrid architectures that reserve NOR only for boot code while shifting bulk data to cheaper NAND. The pricing gap is most acute in mid-tier handsets where tight retail price points dominate component choices [6]Winbond Electronics, “Ultra-Low-Voltage 1.2 V NOR Flash Product Brief,” Winbond Technical Journal, March 14, 2025, winbond.com. . Unless wafer supply rises or yields improve, premium pricing will temper how fast the France NOR flash market penetrates cost-sensitive consumer lines

Fragmented Domestic Semiconductor Ecosystem Limiting Large-Scale NOR Fabrication

France hosts world-class R&D centers but lacks an integrated foundry ecosystem dedicated to volume NOR production. Specialized niche fabs and design-houses must coordinate across borders for front-end wafers, extending cycle times and complicating customization. Dependence on Asian contract fabs exposes local OEMs to allocation risks during global shortages [4]GigaDevice, “GD25/55 SPI NOR Flash Receives ISO 26262 ASIL-D,” GigaDevice Newsroom, February 06, 2025, gigadevice.com. . While the European Chips Act targets a doubling of regional capacity by 2030, near-term fragmentation still caps domestic scale economies for the France NOR flash market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serial NOR Dominates with XIP Advantage

Serial NOR held 73.6% of France NOR flash market size in 2024. Its low-pin-count and execute-in-place functions align with ADAS controllers and industrial PLCs, which demand deterministic read latency over parallel bandwidth [5]. Conversely, Parallel NOR, serving legacy telecom and industrial control units, is gradually ceding design-ins as boards migrate toward compact Serial interfaces.

Serial NOR’s leadership is further cemented by automotive qualification milestones. Infineon achieved ISO 26262 ASIL-D status for its SEMPER line, while GigaDevice secured identical certification for GD25/55, jointly signaling supplier commitment to safety-critical applications [5]Kioxia Corporation, “Kioxia and Western Digital Present New 3D Flash Memory Technology,” IEEE ISSCC Proceedings, February 20, 2025, kioxia.com. . Consequently, automotive and industrial sectors will continue to reinforce Serial NOR’s dominance within the France NOR flash market.

By Interface: Quad SPI Balances Performance and Compatibility

SPI Single/Dual formats contributed 45.9% of France NOR flash market share in 2024, underpinned by widespread MCU support and long-established driver stacks. Nevertheless, Octal/xSPI is expanding at 5.5% CAGR, enabling bandwidth-intensive infotainment and graphical HMI systems without sacrificing pin efficiency. Quad SPI remains the transitional choice for mid-performance designs that require moderate speed improvements without a hardware overhaul.

Supplier portfolios demonstrate adaptive strategy: STMicroelectronics offers a graduated ladder from Single SPI to Octal with unified software flows, thereby reducing OEM switching costs [7]STMicroelectronics, “Automotive-Grade NOR Flash Portfolio Expansion,” STMicroelectronics Press Corner, September 27, 2024, st.com. . This measured evolution sustains broad interface adoption while facilitating progressive performance migration.

By Density: Higher Capacities Enable Complex Applications

The 64–128 Mbit bracket held 31.1% of France's NOR flash market size in 2024, providing sufficient headroom for RTOS images and fail-safe partitions in industrial gateways. However, demand for greater than 256 Mbit parts is rising at 5.8% CAGR as software-defined vehicles and edge-AI modules embed larger codebases and richer sensor-fusion algorithms.

Emerging 1.2 V devices bolster high-density roadmaps by curbing active power budgets; Winbond’s recent 128 Mbit and 256 Mbit low-voltage range exemplifies this design pivot[8]. Therefore, production-volume split will gradually tilt towards multi-die high-density offerings as embedded firmware footprints expand.

By Voltage: 1.8 V Class Leads Energy-Efficient Designs

Devices rated at 1.8 V commanded 51.2% France NOR flash market share in 2024, owing to compatibility with low-core-voltage SoCs and superior energy efficiency. Process shrinks at 55 nm and 40 nm nodes favour this rail, reinforcing its relevance across battery-operated IoT and in-vehicle modules.

Nonetheless, the advent of 1.2 V products—currently unique to Winbond’s portfolio—signals an industry shift toward ultra-low-power variants, particularly for wearables and medical sensors where battery runtime is paramount [8]ASML, “Annual Report 2025,” ASML Investor Relations, February 13, 2025, asml.com. . Wider adoption of 1.2 V standards could accelerate voltage migration trends beyond 2027.

By End-User Application: Automotive Growth Challenges Consumer Electronics Lead

Consumer electronics represented 38.7% of 2024 revenue, powered by high smartphone penetration and a robust domestic assembly base for smart TVs and set-top boxes. NOR’s instant-boot traits remain indispensable for premium user-interface responsiveness.

Conversely, automotive electronics constitutes the fastest-growing end-market at 7.3% CAGR. Electric-powertrain control, zonal architectures, and Level 2+ autonomy necessitate deterministic NOR boot memory with robust functional-safety credentials, ensuring sustained procurement from French OEMs and Tier-1 suppliers [2]European Commission, “France 2030 Investment Plan,” European Commission, October 12, 2024, europa.eu. .

By Process Technology Node: 55 nm Dominates While 28 nm Advances

The mature 55 nm node captured 40.1% of revenue during 2024 by balancing endurance, cost, and field-reliability metrics. OEMs in factory automation and railway signaling continue to value their proven track record.

Sub-28 nm nodes, enabled by EUV lithography, are expanding at 5.9% CAGR, offering superior density and read-bandwidth for connected infotainment clusters and edge analytics hardware. ASML forecasts compound semiconductor-sector growth of 9% through 2030, driven partly by advanced nodes applied to high-performance memory [6]Winbond Electronics, “Ultra-Low-Voltage 1.2 V NOR Flash Product Brief,” Winbond Technical Journal, March 14, 2025, winbond.com. .

By Packaging Type: WLCSP Enables Compact Designs

WLCSP/CSP solutions delivered 46.3% of revenue in 2024 and maintain the highest 7.3% CAGR. Elimination of wire-bond substrate shrinks footprint to die size, a critical benefit for ultra-thin smartphones and wearables.

QFN and SOIC formats retain favour within harsh-environment industrial and automotive settings that demand robust solder joints and reworkability. STMicroelectronics, for instance, offers parallel QSPI NOR variants in QFN packages rated for −40 °C to +125 °C to address under-hood automotive deployments [7]STMicroelectronics, “Automotive-Grade NOR Flash Portfolio Expansion,” STMicroelectronics Press Corner, September 27, 2024, st.com. .

Geography Analysis

Paris and its surrounding Île-de-France corridor account for roughly 40% of national NOR consumption, anchored by a dense cluster of embedded design studios, automotive Tier-1 engineering centers, and research laboratories. Proximity to investor funding and talent pipelines propels rapid prototype-to-volume cycles, ensuring regular demand pulsing through the France NOR flash market [1]European Commission, “A Chips Act for Europe,” European Commission, January 18, 2024, europa.eu. .

Grenoble and the wider Auvergne-Rhône-Alpes region form the second pole of activity, leveraging world-renowned microelectronics institutes and a strong supplier network centered on STMicroelectronics' fabs and packaging lines. Local OEMs emphasize industrial automation and smart-energy projects that rely on ruggedized Serial NOR for deterministic real-time control [3]Infineon Technologies, “SEMPER NOR Flash Achieves ASIL-D Certification,” Infineon Technologies Newsroom, May 02, 2025, infineon.com. .

Northern automotive corridors such as Hauts-de-France and Grand Est now surge as EV platforms scale. High-reliability ASIL-D flash migrates into digital clusters, battery-management units, and sensor fusion ECUs. Southern regions around Sophia Antipolis and Toulouse round out demand, installing secure NOR inside aerospace avionics, satellite payloads, and defense communication systems. Together these hubs diffuse technology adoption yet maintain a unified pull for advanced process nodes, underpinning balanced regional growth of the France NOR flash market [8]ASML, “Annual Report 2025,” ASML Investor Relations, February 13, 2025, asml.com. .

The nor flash market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe and Asia. This is complemented by country-specific insights for United Kingdom, Germany, Japan, China, India, Italy, and South Korea, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Roughly 65% of France NOR flash market revenue rests with the top five suppliers, indicating moderate concentration that nevertheless leaves space for niche specialists. STMicroelectronics leverages domestic fabs plus longstanding Tier-1 relationships to anchor automotive and industrial sockets. Winbond, Macronix, and GigaDevice strengthen footprints through joint design centers and localized technical-support teams that customize reference code and security overlays for French OEMs.

Strategic alliances are multiplying. Memory vendors bundle development kits, secure-boot stacks, and ASIL-ready driver software to shorten customer time to market. Infineon pairs its SEMPER NOR with power-management ICs in turnkey ADAS boards, while Micron offers long-term supply guarantees matched to automotive production schedules. White-space plays include edge-AI accelerators that need larger XIP images, medical-imaging consoles demanding radiation-tolerant flash, and Industry 4.0 gateways calling for extended endurance cycles.

Supply-chain resilience influences competitive edge. Firms integrating back-end assembly in France can commit shorter lead times during global wafer scarcity. Packaging know-how in WLCSP and QFN tailored to European automotive qualification distinguishes suppliers willing to co-invest alongside local EMS partners. As the European Chips Act funnels incentives into regional fabs, leadership hinges on aligning technology roadmaps with France’s domestic sovereignty ambitions, firmly tying company strategy to the trajectory of the France NOR Flash market.

France NOR Flash Industry Leaders

Winbond Electronics Corporation

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

Micron Technology Inc.

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon Technologies’ SEMPER NOR family obtained ISO 26262:2018 ASIL-D certification, enabling French carmakers to design safety-critical ADAS systems with verified functional-safety flash memory.

- February 2025: GigaDevice’s GD25/55 Automotive-Grade SPI NOR series achieved ISO 26262:2018 ASIL-D, covering 2 Mb-2 Gb densities at up to 400 MB/s, supporting France’s rapidly expanding automotive electronics landscape.

- February 2025: Kioxia and SanDisk showcased next-generation 3D flash technology at ISSCC 2025, introducing 4.8 Gb/s interfaces that could shape future NOR architectures for performance-centric French applications.

- November 2024: Infineon unveiled a radiation-hardened 512 Mbit QSPI NOR chip, specifically designed to withstand the harsh conditions of space environments. This innovation addresses the critical need for reliable memory solutions in aerospace applications, ensuring durability and performance in extreme radiation and temperature conditions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the France NOR flash memory market as revenues generated within the country from stand-alone serial or parallel NOR chips and embedded NOR blocks shipped on discrete microcontrollers and system-in-package devices that deliver execute-in-place, secure-boot, and code-storage functions across consumer, automotive, industrial, and network equipment. The boundary follows the transaction point between the component maker and the immediate systems customer, expressed in USD value.

Scope exclusions include removable USB drives, eMMC, eUFS, NAND flash, and DRAM products that are left out.

Segmentation Overview

- By Type (Value and Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit And Less NOR

- 4 Megabit And Less-NOR (greater than 2mb) NOR

- 8 Megabit And Less (greater than 4mb) NOR

- 16 Megabit And Less (greater than 8mb) NOR

- 32 Megabit And Less (greater than 16mb) NOR

- 64 Megabit And Less (greater than 32mb) NOR

- 128 Megabit and Less (greater than 64MB) NOR

- 256 Megabit and Less (greater than 128MB) NOR

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V – 3.6 V)

- Others - 1.2V Class (and similar sub-1.8V) (2.5V, 5V, etc.)

- By End-User Application (Value and Volume)

- Consumer Electronics

- Communication Equipment

- Automotive

- Industrial

- Other Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls with French fabless designers, European wafer foundries, memory distributors, Tier-1 automotive electronics integrators, and IoT module makers. These dialogues clarified local ASP spreads, density mix shifts, and upcoming qualification cycles, letting us benchmark desk findings and refine near-term outlooks across Île-de-France, Occitanie, and Auvergne-Rhône-Alpes clusters.

Desk Research

We mapped domestic demand using open data sets such as INSEE's electronic component production tables, Eurostat PRODCOM export-import lines for 85423295, patent filings filtered through Questel, and shipment disclosures from the French Directorate General for Enterprises. Trade association briefs from SEMI, automotive homologation releases, and company 10-Ks archived in Dow Jones Factiva filled pricing and channel gaps. The sources listed illustrate the breadth; many other public and paid references informed intermediate checks.

Market-Sizing & Forecasting

A top-down reconstruction from France's microcontroller and electronic assembly output, adjusted for NOR penetration and import-export balances, sets the baseline before selective supplier roll-ups validate density and interface splits. Key model drivers include average megabit price erosion, vehicle ADAS installation rates, quarterly smart-meter deployments, MCU wafer starts, and SPI-to-parallel migration ratios. Multivariate regression links these variables to historical revenue, while scenario analysis captures macro swings in manufacturing PMI and exchange rates. Where bottom-up estimates left gaps, sales channel interviews provided corrective factors that were iterated until variance sat within a 5% tolerance.

Data Validation & Update Cycle

Outputs pass a two-step peer review, followed by variance checks against customs data and quarterly vendor disclosures. We refresh the file each year and trigger interim updates when material events, such as capacity additions, trade bans, or step-change ASP moves, occur, so clients receive the latest vetted view.

Why Our France NOR Flash Baseline Commands Reliability

Published estimates often diverge because firms mix geographies, bundle adjacent memory types, or assume uniform pricing.

Key gap drivers include wider European roll-ups reported by some publishers, global snapshots that overstate local cyber-security incentives, and models that extrapolate generic NAND price curves instead of France-specific NOR ASP ladders updated yearly by Mordor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 74.16 M (2025) | Mordor Intelligence | |

| USD 568 M (2021) | Regional Consultancy A | Europe aggregate, excludes import parity adjustments, mixes NOR with specialty EEPROM |

| USD 3.22 B (2025) | Global Consultancy B | Global roll-up, assumes uniform 6% CAGR for all regions, lacks density-level ASP splits |

| USD 5.27 B (2025) | Trade Journal C | Bundles NAND and NOR, applies aggressive IoT unit forecasts, no customs cross-check |

These contrasts show why Mordor's disciplined France-only scope, variable-specific regression, and annual refresh cadence provide a balanced, transparent baseline that decision makers can trace directly to publicly auditable inputs and on-ground expert insight.

Key Questions Answered in the Report

What is the current size of the France NOR flash market?

The France NOR flash market stands at USD 74.16 million in 2025 and is projected to reach USD 95.17 million by 2030.

Which segment holds the largest share by type?

Serial NOR Flash dominates with 73.6% share, reflecting its execute-in-place advantages in embedded and automotive systems.

Why is automotive electronics the fastest-growing end-user segment?

Rising electric-vehicle production and the rollout of ADAS features demand high-reliability, XIP-ready NOR Flash, driving a 7.3% CAGR in automotive applications

How are government initiatives influencing the market?

The France 2030 program and the European Chips Act provide incentives for local assembly and test expansion, strengthening supply-chain resilience for NOR devices.

What technology trend is most affecting power consumption?

Migration to 1.8 V and, recently, 1.2 V operating voltages cuts active and standby power, a key requirement for wearables and battery-powered IoT nodes.

Which interface is growing fastest?

Octal/xSPI posts a 5.5% CAGR as data-intensive applications seek up to 8× bandwidth compared to standard SPI lines, especially in infotainment and advanced HMIs.

Page last updated on: