Netherlands Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

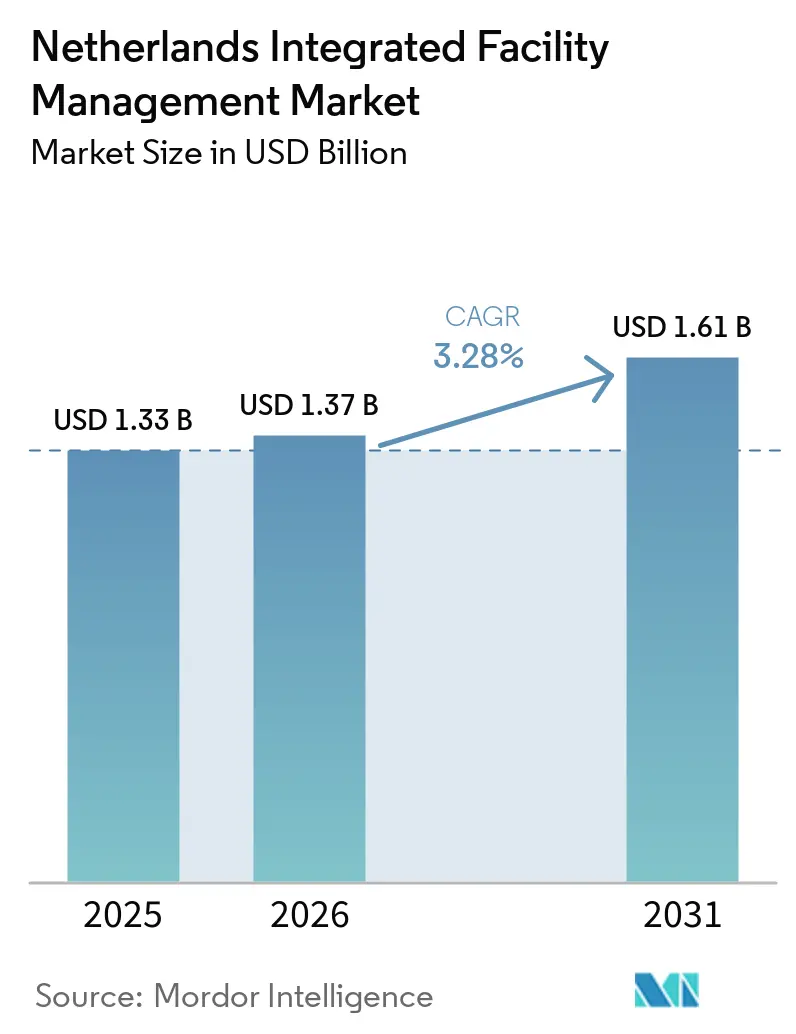

| Base Year Market Size (2025) | USD 1.33 Billion |

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Integrated Facility Management Market Analysis by Mordor Intelligence

The Netherlands integrated facility management market size was valued at USD 1.33 billion in 2025 and USD 1.37 billion in 2026 to USD 1.61 billion by 2031, registering a CAGR of 3.28% between 2026 to 2031. The Netherlands integrated facility management (IFM) market is moving forward through deeper service integration, because clients now expect one provider to combine technical upkeep, compliance work, workplace support, and reporting within a single operating model. The 2026 implementation cycle for EPBD IV, the new energy label requirements effective from May 29, 2026, and the July 2026 BACS mandate for larger utility buildings are pushing the Netherlands integrated facility management market toward compliance-led asset management rather than reactive maintenance alone. The Netherlands integrated facility management (IFM) market is also being reshaped by sustainability reporting needs, because occupiers and asset owners are writing energy, water, waste, and emissions tracking into service agreements and tender criteria, which raises switching costs and favors providers with auditable delivery systems. While soft services still account for most current contract value, the Netherlands integrated facility management market is seeing stronger pull for technical scopes such as HVAC upgrades, fire safety work, automation integration, and lifecycle maintenance planning in older commercial buildings. Competition in the Netherlands IFM market is separating into large global platforms for complex national contracts and regional specialists for local execution, while labor tightness remains a clear operating constraint for both groups.

Key Report Takeaways

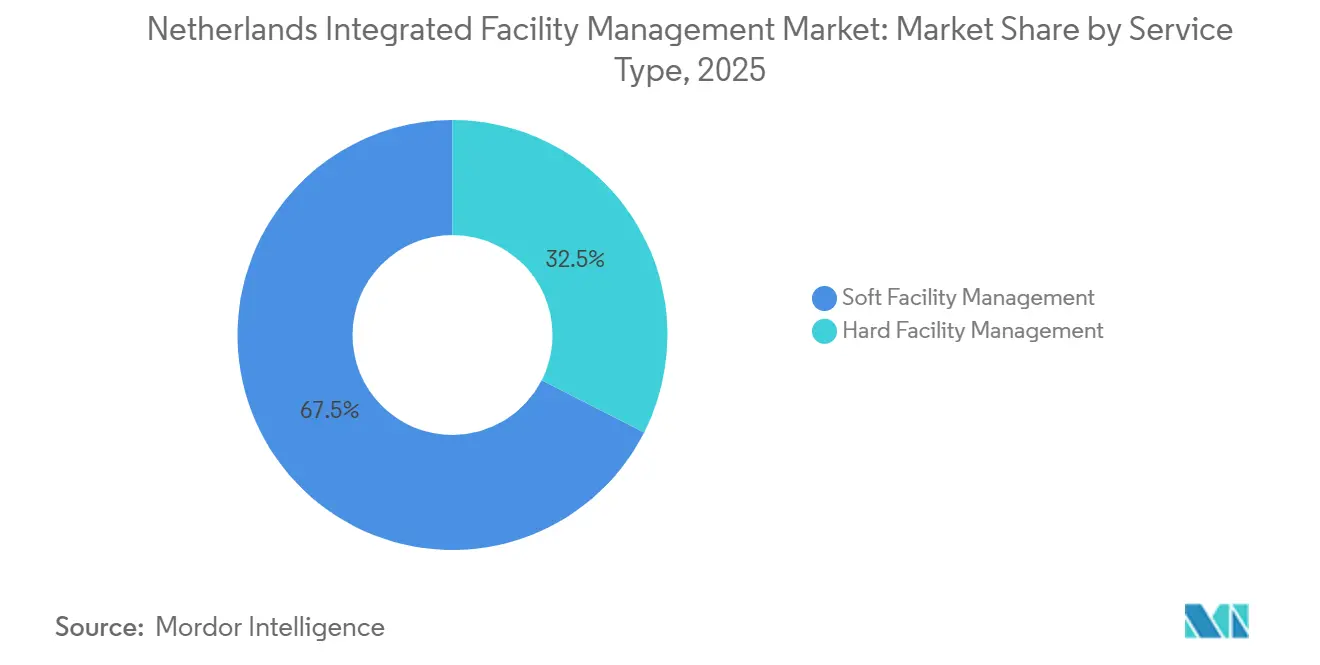

- By service type, Soft Facility Management (Soft FM) held 67.51% of the Netherlands integrated facility management market share in 2025, while Hard Facility Management (Hard FM) is forecast to expand at a 3.83% CAGR through 2031.

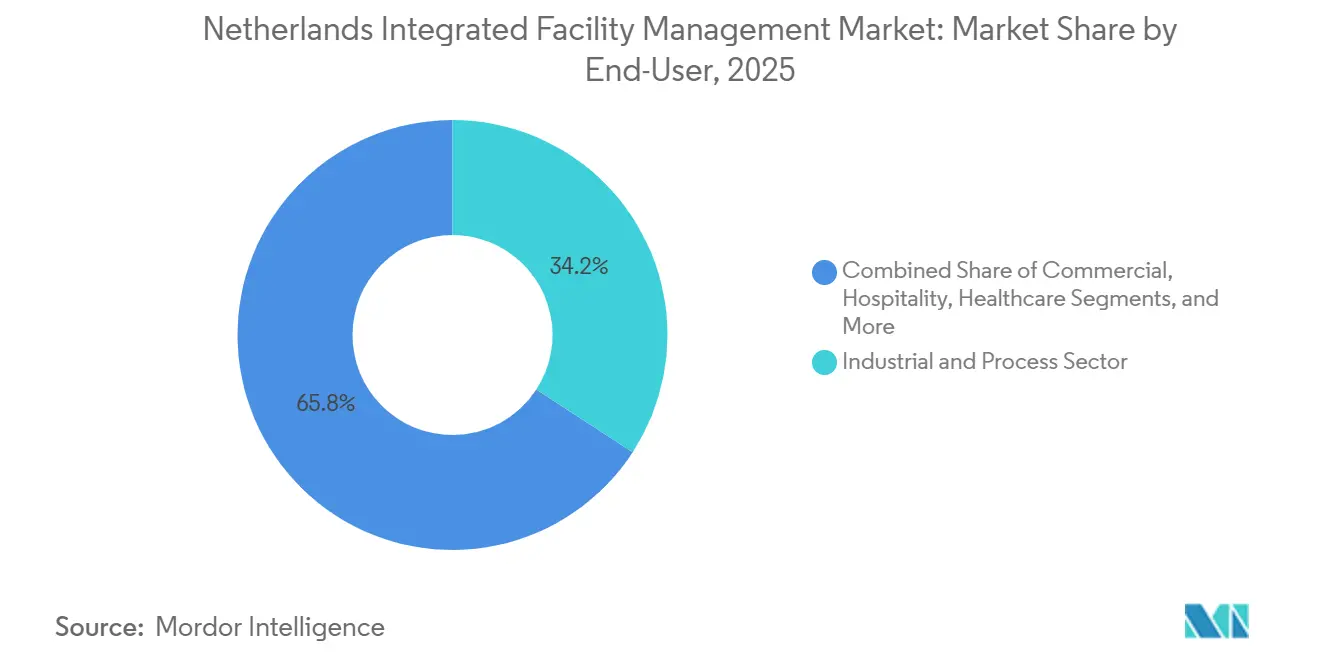

- By end-user, the Industrial and Process Sector held 34.19% of the Netherlands IFM market share in 2025, while Commercial end-users are projected to record the fastest CAGR of 4.19% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Buildings And Operations | +0.9% | National, concentrated in Amsterdam, Rotterdam, The Hague, Utrecht, extended to Eindhoven industrial clusters | Medium term (2-4 years) |

| IoT Networks And Aging Physical Infrastructure | +0.7% | National, with highest urgency in pre-1980 commercial building stock in urban centers | Medium term (2-4 years) |

| Outsourcing Trend Among Dutch Corporations | +0.6% | National, with strongest momentum in Randstad corporate real estate and the Brainport industrial corridor | Short term (≤ 2 years) |

| Digital Transformation Through IT And Smart Buildings | +0.5% | National, led by Amsterdam and Utrecht commercial districts, with Eindhoven high-tech campus concentration | Medium term (2-4 years) |

| Stronger Workplace Health And Safety Regulations | +0.3% | National, with stronger enforcement in industrial zones such as Rotterdam and Chemelot Limburg | Short term (≤ 2 years) |

| Rise Of Tenant And Logistics Needs Requiring IFM | +0.2% | Rotterdam logistics and port corridor, Amsterdam distribution and data center clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Buildings and Operations

The Dutch building base is moving into a period where energy performance compliance is becoming part of everyday facility operations instead of a one-time retrofit cycle. Offices above 100 m² have already been operating under the Energy Label C requirement, and the next layer of policy now adds stronger monitoring and control obligations through BACS for larger utility buildings from July 2026. That shift expands the service scope for integrated providers, because building systems now need continuous optimization, documented performance tracking, and technical coordination across multiple service lines instead of isolated maintenance visits. The Dutch Climate Agreement target for a 49% CO₂ reduction by 2030 against 1990 levels keeps sustainability work tied to long-duration building programs, which supports recurring service demand rather than short project spikes. For the Netherlands integrated facility management market, this means providers with verifiable energy, maintenance, and reporting capabilities are in a stronger position as client procurement becomes more compliance focused and less price only.

IoT Networks and Aging Physical Infrastructure

A large share of Dutch commercial buildings still reflects older physical infrastructure, and that makes technical modernization a practical operating need across offices, public facilities, and industrial sites. In this setting, IoT-enabled maintenance is gaining ground because continuous equipment data allows providers to detect faults earlier, schedule interventions with fewer disruptions, and reduce emergency work in buildings with aging MEP systems. The Rijksvastgoedbedrijf provided a clear reference point in November 2025 when it replaced six maintenance platforms with one intelligent maintenance system covering more than 410,000 assets and more than 300,000 maintenance activities.[1]Rijksvastgoedbedrijf, “Intelligent Maintenance Management System Implementation,” Rijksvastgoedbedrijf, rijksvastgoedbedrijf.nl Institutional programs such as Utrecht University’s BIM-led property digitization also show that clients are moving toward asset data structures that support predictive maintenance, lifecycle planning, and better tender transparency. The Netherlands integrated facility management (IFM) market is therefore being pulled toward providers that can combine physical service delivery with data integration and digital asset oversight rather than field labor alone.

Outsourcing Trend Among Dutch Corporations

The move toward outsourcing in Dutch facility services is no longer just a staffing decision, because occupiers are now using integrated models to simplify vendor oversight, compliance reporting, and workplace coordination under one contract. This trend is favoring single-provider structures over fragmented multi-vendor arrangements, especially where clients need one partner to manage technical, cleaning, food, space, and reporting requirements with shared accountability. Alliander’s long-running combined IFM and integrated security management model is important in this context, because it shows how Dutch clients are reducing supplier complexity while still improving control and compliance across distributed sites. Once service integration reaches that level, contract value tends to rise not only because more tasks are outsourced, but also because the provider is taking on a larger governance role within day-to-day building operations. For the Netherlands IFM market, this outsourcing pattern supports longer relationships and broader contract scope, especially in large corporate real estate portfolios and technically demanding sites.

Digital Transformation Through IT and Smart Buildings

Digital adoption is becoming a core operating requirement as building owners seek real-time visibility into occupancy, equipment status, cleaning needs, and energy performance.[2]Planon, “IT Leaders and Building Digitization Survey,” Planon, planonsoftware.com Survey results cited in the user draft showed that building digitization is already widespread and that IT leaders are now directly involved in FM software buying decisions, which means platform compatibility has become a procurement issue rather than an optional add-on. In the Dutch context, this is accelerating demand for IWMS, CAFM, sensors, and analytics tools that can connect maintenance, space, and sustainability information into one auditable workflow. As more public and private portfolios adopt digital baselines, providers are being evaluated on their ability to convert building data into measurable outcomes such as uptime, energy control, and occupancy-based service scheduling. The Netherlands integrated facility management (IFM) market is therefore moving toward outcome-linked service models, because data-rich buildings make activity-based billing less persuasive than verified performance delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Costs Amid Talent And Skills Gaps | -0.7% | National, most acute in Amsterdam, Rotterdam, Utrecht, and surrounding labor-scarce regions | Short term (≤ 2 years) |

| Highly Fragmented Contractor Landscape Leading To Price Wars | -0.5% | National, with strongest fragmentation pressure in Randstad commercial districts and smaller regional markets | Medium term (2-4 years) |

| Volatility And Price Changes Affecting Costs And Budgets | -0.4% | National, with highest sensitivity among energy-intensive industrial clients in Zeeland and Rotterdam | Short term (≤ 2 years) |

| Limited Scalability For Small Firm Providers | -0.2% | National, especially in peripheral regions where large IFM providers have limited physical presence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Labor Costs Amid Talent and Skills Gaps

Labor availability remains one of the clearest operating constraints in Dutch facility services, because the national labor market stayed exceptionally tight at the end of 2024 with 108 job openings for every 100 unemployed people.[3]De Nederlandsche Bank, “Labor Market Tightness in the Netherlands,” De Nederlandsche Bank, dnb.nl The shortage is especially relevant for technical FM delivery, since electricians, installers, and other skilled support roles are central to HVAC upgrades, automation work, and compliance-led maintenance programs. On the soft services side, ING reported strong revenue growth in Dutch cleaning during H1 2025 that was driven mainly by pricing rather than volume, which shows how wage pressure is being passed through to clients while still squeezing execution capacity. Providers are responding with robotics, task redesign, and more structured support models, and the Hanze University study on task shifting in hospitals points to one route for easing pressure in labor-intensive environments. Even so, the Netherlands IFM market will continue to face margin pressure when client expectations rise faster than the available supply of trained workers.

Highly Fragmented Contractor Landscape Leading to Price Wars

The Dutch FM contractor base is still broad and uneven, which keeps price competition intense even as service requirements become more technical and compliance heavy. This creates a difficult balance for providers, because clients continue to push for savings while collective labor agreement increases and tighter compliance obligations make low-price delivery harder to sustain. The updated Working Conditions Act obligations from July 1, 2025 add another cost layer for providers operating across multiple client sites, and those requirements are often harder for smaller operators to absorb. At the same time, larger integrated tenders now demand stronger reporting, automation awareness, and wider geographic execution, which narrows access for single-service firms even if they remain competitive on unit price. The result is a market where fragmentation remains high at the subcontracting level, while the largest integrated opportunities increasingly flow toward a smaller set of better-capitalized providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Gains Momentum in Compliance-Driven Renovation

Soft Facility Management (Soft FM) held 67.51% of Netherlands integrated facility management market share in 2025, while Hard Facility Management (Hard FM) is projected to grow at a 3.83% CAGR through 2031 as compliance work and technical upgrades gain weight in total contracts. Hard FM is benefiting from a clear shift in client priorities, because HVAC renewal, fire safety upgrades, automation controls, and lifecycle planning now sit closer to regulatory compliance than discretionary improvement work. The July 2026 BACS requirement for larger utility buildings strengthens that shift by making automation capability a baseline requirement in more technical contracts. The Netherlands integrated facility management (IFM) market also shows stronger demand for asset intelligence within Hard FM, because public-sector digitization programs have raised expectations around BIM-linked maintenance schedules, equipment histories, and predictive service planning.

Soft FM remains the revenue anchor in the Netherlands integrated facility management industry because cleaning, catering, front-of-house support, and routine workplace services still carry higher billing frequency and broader site coverage than technical interventions. Even so, the content of Soft FM contracts is changing as hybrid work patterns push providers toward occupancy-based cleaning, more flexible support schedules, and tighter waste and food management standards. Sodexo Nederland’s WasteWatch results in 2025 showed that measurable waste reduction can now be embedded into service delivery and client reporting, which makes Soft FM more relevant to sustainability programs than it was in older contract models. That is why the Netherlands IFM market is not shifting away from Soft FM, but rather redefining it through data, circularity, and labor-saving delivery methods that fit larger integrated contracts.

By End-User: Commercial Growth Builds on an Industrial Base

The industrial and process sector held 34.19% of Netherlands integrated facility management market share in 2025, which reflects the structural weight of manufacturing, chemicals, logistics, and complex technical sites in Dutch demand. These facilities require more technical density than many office assets, because MEP reliability, safety systems, industrial cleaning, and specialized maintenance are critical to uptime and compliance in port, production, and high-tech environments. Rotterdam, Zeeland, and the Brainport corridor remain central to this pattern, with large industrial and logistics concentrations creating steady need for integrated technical support and site services. This industrial base gives the Netherlands integrated facility management (IFM) market a stable operational core even while newer growth is appearing in office and institutional portfolios.

Commercial end-users are projected to record the fastest 4.19% CAGR in Netherlands IFM market size through 2031, supported by hybrid workplace adaptation, sustainability reporting needs, and continued investment in better managed office environments. Healthcare adds another layer of demand, and the Domus Valuas agreement with CBRE shows how care providers are moving toward national integrated coverage with preventive maintenance, technical support, and compliance-driven service continuity across multiple locations. Public and education assets are also moving in this direction as digital building programs create longer tender pipelines for providers that can connect maintenance work with data and reporting systems. In housing-related assets, renovation targets and energy label improvement plans support a gradual expansion of service scope, which keeps the Netherlands integrated facility management industry exposed to a wider set of occupier types than office-led narratives usually suggest.

Geography Analysis

The Randstad cluster accounts for more than two-thirds of Netherlands integrated facility management market size, which keeps Amsterdam, Rotterdam, The Hague, and Utrecht at the center of national contract activity. Amsterdam remains the main commercial hub because it concentrates multinational occupiers, financial institutions, and sustainability-led real estate investors that demand broader reporting and workplace coordination within FM contracts. This makes the city a strong base for contracts that combine occupancy management, energy tracking, front-of-house services, and technical support within one operating framework. The Hague continues to matter for public-sector demand, as central government property programs and standardized maintenance systems influence how integrated technical requirements are written into public tenders.

Rotterdam anchors the industrial side of the Netherlands integrated facility management (IFM) market because the port and nearby petrochemical and logistics assets create sustained need for technical maintenance, safety work, and operational support across large sites. Eindhoven and the wider Brainport corridor are the strongest growth pocket within the country, supported by the concentration of high-tech manufacturing, electronics, and specialized production environments that demand more advanced FM capability. The Brainport Industries Campus example is especially important because one campus already brings together 54 tenants under a service environment that includes regular cleaning, specialized cleaning, and sustainability-led operating tools. Utrecht adds a mixed commercial and institutional profile, with office activity, education assets, and centrally located corporate occupiers supporting a steady flow of integrated service demand. Across these urban clusters, digital building programs and stricter compliance duties are lifting the technical standard expected from providers, which strengthens the role of larger and more system-oriented contractors.

Peripheral regions such as Zeeland, Limburg, and Drenthe face a more difficult operating context because labor availability is tighter and service networks are thinner than in the western urban core. That makes fully local staffing models harder to maintain for smaller operators, especially when contracts require more technical response capability and compliance documentation. Providers serving those areas are more likely to rely on centralized coordination, mobile technical teams, and remote monitoring support than on dense site-based staffing alone. As a result, geography in the Netherlands IFM market is not just about where demand sits today, but also about where providers can sustain labor, technology, and compliance capability at an acceptable cost.

Competitive Landscape

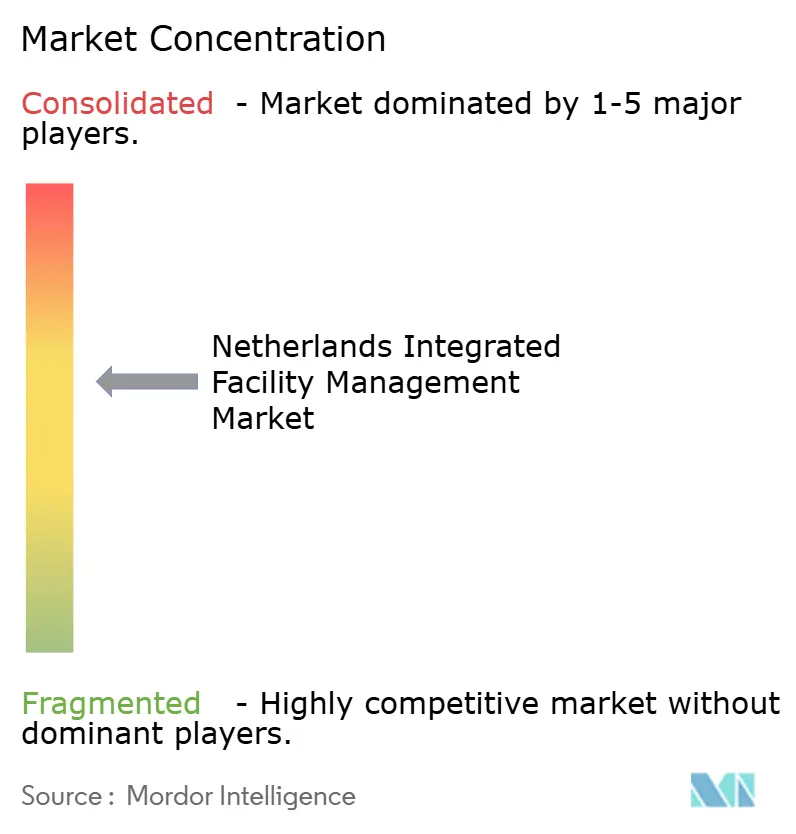

The Netherlands integrated facility management market is moderately concentrated in large national and multi-site contracts, but it remains fragmented across local and mid-sized accounts where regional providers still hold meaningful operational relevance. ISS, Sodexo, CBRE GWS, Compass Group, and other international platforms are strongest where clients want ESG reporting, digital integration, and broad service bundling under one governance structure. Regional specialists such as Facilicom, Vebego, and Unica continue to compete where local density, sector familiarity, and relationship continuity matter more than a pan-European delivery model. This split means that the competitive field is not defined by scale alone, because contract complexity and reporting capability now determine where large global players can widen their advantage.

Strategic moves in 2025 and 2026 show that providers are trying to lock in higher-value positions before compliance and digital requirements move further upstream in procurement. Compass Group’s completed acquisition of Vermaat Groep in December 2025 strengthened its position in premium hospitality and facility services, and it also signaled that Dutch contract platforms hold strategic value at the European level. ISS then deepened the market’s move toward outcome-led contracting in April 2026 through its Vested agreement with Heineken, which replaced a more traditional SLA structure with a model built on shared goals and shared accountability. CBRE is differentiating in another way through Lean Six Sigma standards, technology-led service delivery, and analytics capability, which fits the direction of more complex corporate and institutional tenders. Together, these moves show that the Netherlands integrated facility management (IFM) market is rewarding providers that can combine execution scale with measurable outcomes rather than basic bundled labor alone.

Technology overlay capabilities are also becoming more relevant to competition because smart building tools can now sit on top of traditional maintenance and workplace services rather than beside them. That raises the barrier for smaller firms that may still be strong in cleaning, catering, or local technical work but lack the systems needed for integrated reporting and digital asset visibility. It also explains why labor pressure does not automatically level the field, because clients facing compliance and reporting demands are often willing to consolidate around fewer providers if those providers reduce oversight complexity. In that setting, the Netherlands IFM market is likely to remain mixed, with concentrated competition at the top end and dispersed rivalry across subcontracting and specialist local service niches.

Netherlands Integrated Facility Management Industry Leaders

Sodexo S.A.

ENGIE Cofely

VINCI Facilities

ISS A/S

Bouygues Energies & Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ISS Facility Services and Heineken signed the first Production Based Vested IFM contract in the Netherlands, merging two existing Heineken International and Heineken Nederland FM agreements into a single future-proof contract with shared accountability. This marks a structural innovation in Dutch IFM contract design, shifting from penalty-based KPIs to shared outcome metrics across workplace and facility management scope.

- December 2025: Compass Group completed the acquisition of Vermaat Groep B.V. for approximately EUR 1.5 billion (approximately USD 1.70 billion) following regulatory approval. Vermaat, the Netherlands' premium catering and hospitality market leader with over 700 locations and approximately EUR 700 million (USD 810 million) expected 2025 revenues, continues operating independently within the Compass Group structure; Compass Nederland became part of the Vermaat Group operational organization.

- November 2025: The Rijksvastgoedbedrijf (Central Government Real Estate Agency) implemented a unified intelligent maintenance management system (i-OMS) from Planon, replacing six legacy maintenance platforms. The new system standardizes 410,000+ assets and 300,000+ maintenance activities, with 800+ RVB employees and 800+ supplier staff migrated to the platform, establishing a digitized baseline for Dutch public-building FM procurement.

- June 2025: ISS signed a new 5-year global partnership with VELUX Group covering facility services, cleaning, waste management, catering, reception, and outdoor maintenance, across 12 countries including the Netherlands, with Netherlands mobilization commencing January 1, 2026.

Netherlands Integrated Facility Management Market Report Scope

The Netherlands Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the current size of the Netherlands integrated facility management market?

The Netherlands integrated facility management market was valued at USD 1.33 billion in 2025 and is forecast to reach USD 1.61 billion by 2031 at a 3.28% CAGR.

Which service type leads facility management demand in the Netherlands?

Soft FM led with 67.51% share in 2025, supported by cleaning, catering, and workplace support contracts, while Hard FM is growing faster through 2031.

Why is Hard FM growing faster in the Netherlands?

Hard FM is being lifted by HVAC modernization, fire safety upgrades, automation integration, and building compliance requirements such as BACS from July 2026.

Which end-user group creates the largest demand in the Netherlands?

Industrial and process facilities held 34.19% share in 2025, reflecting the weight of logistics, manufacturing, chemicals, and technically demanding sites.

Which customer group is expected to grow the fastest through 2031?

Commercial end-users are projected to post the highest CAGR at 4.19%, supported by hybrid office upgrades, sustainability reporting needs, and better managed workplace environments.

Page last updated on: