United Kingdom Healthcare Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

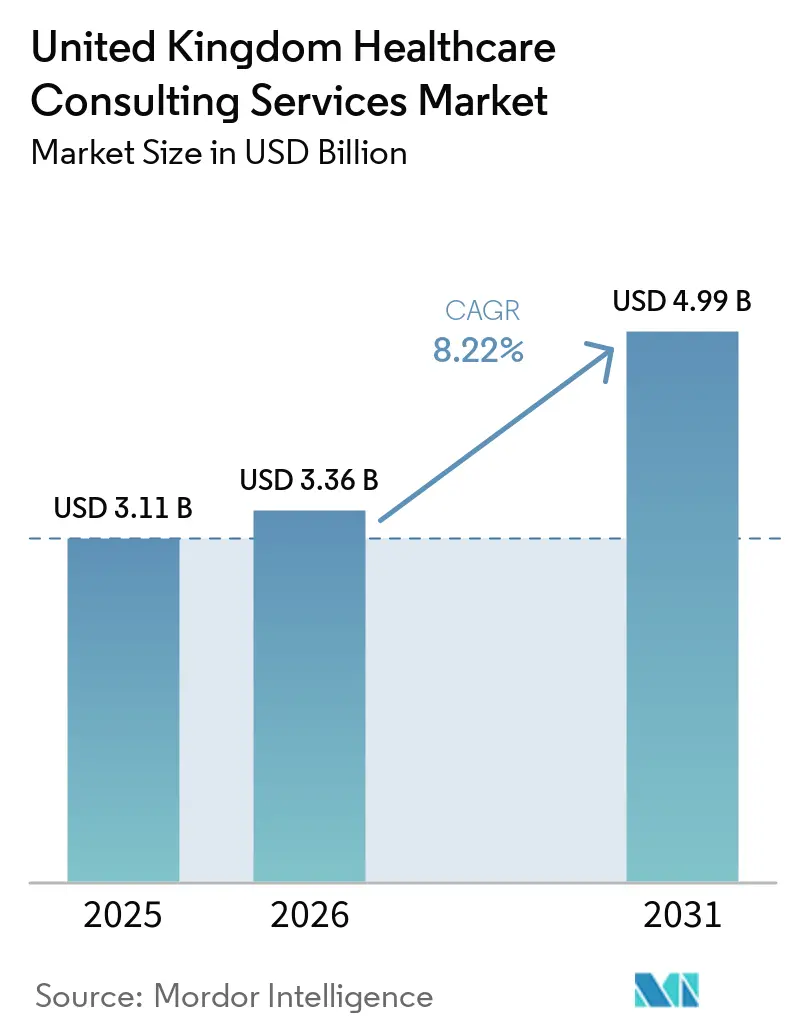

| Base Year Market Size (2025) | USD 3.11 Billion |

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 4.99 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Healthcare Consulting Services Market Analysis by Mordor Intelligence

The United Kingdom Healthcare Consulting Services Market size is expected to grow from USD 3.11 billion in 2025 to USD 3.36 billion in 2026 and is forecast to reach USD 4.99 billion by 2031 at 8.22% CAGR over 2026-2031.

The United Kingdom (UK) healthcare consulting services market is being shaped by the merger of NHS England into the Department of Health and Social Care in 2026, which is reducing internal transition capacity while widening the need for external advisory support across IT migration, workforce redesign, and governance restructuring. The March 2026 Population Health Delivery Models blueprint also extends the workload horizon for the UK healthcare consulting services market because IHO contracts will require multi-year redesign of payment flows, accountability, and population-based care models across ICBs and provider collaboratives. Digital modernization remains another core growth base for the UK healthcare consulting services market as NHS organizations continue to invest in frontline digitization, connected care records, AI-enabled workflows, and post-EPR optimization. Competitive conditions remain moderate to high because framework access favors large multidisciplinary firms, yet the market still contains a long tail of accredited suppliers that compete for specialist and mid-scale work. The main constraint on the UK healthcare consulting services market is provider finance pressure, since NHS bodies still need to justify visible operational return on every advisory engagement while many organizations remain in deficit.

Key Report Takeaways

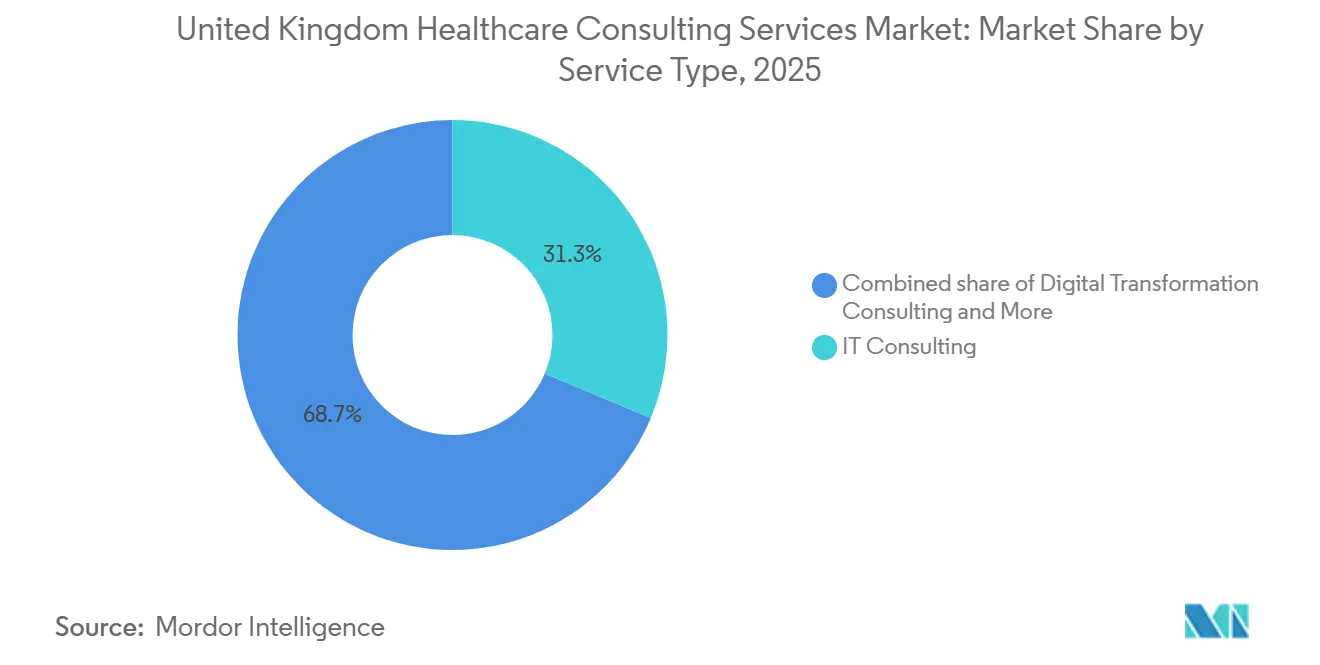

- By service type, IT Consulting held 31.31% share in 2025, while Digital Transformation Consulting is forecast to expand at an 11.38% CAGR through 2031.

- By end user, Healthcare Providers held 28.24% share in 2025, while Government Agencies are projected to record the fastest growth at a 10.52% CAGR through 2031.

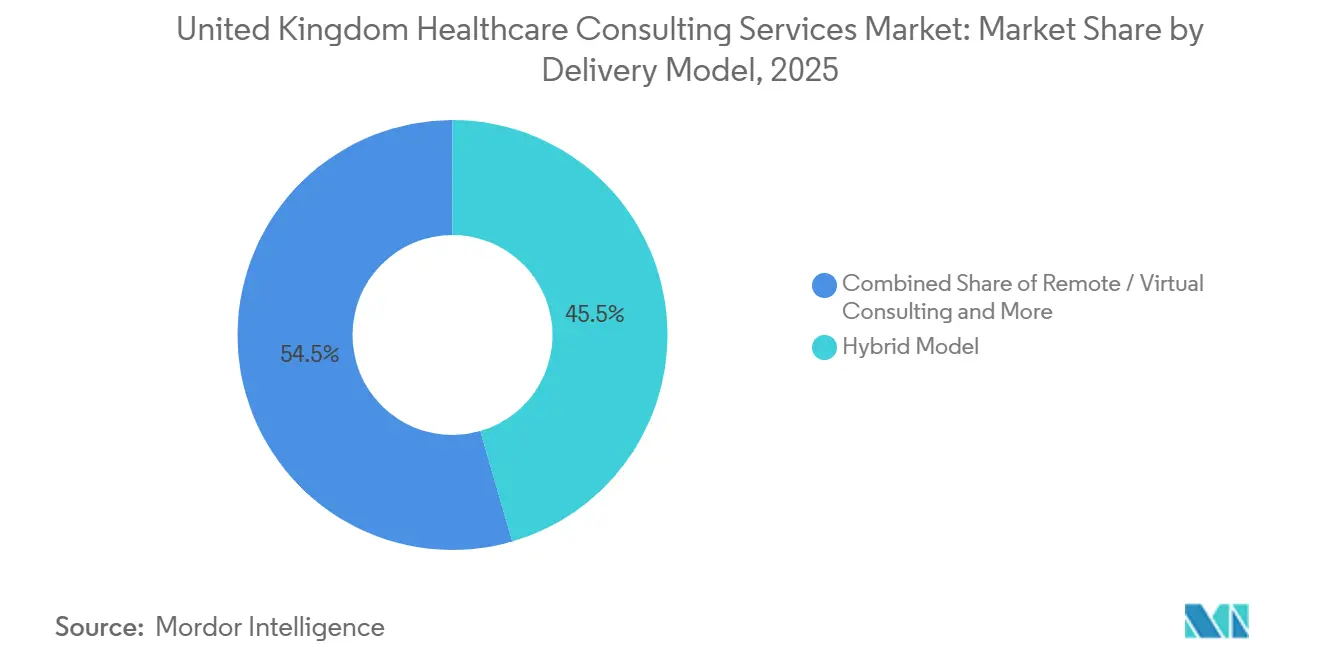

- By delivery model, Hybrid delivery accounted for 45.52% share in 2025, while Remote/Virtual Consulting is expected to grow at a 10.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Healthcare Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift to Value-Based Care Models | +1.6% | England-led, with spill-over to Scotland and Wales under devolved ICS equivalents | Long term (≥ 4 years) |

| Surging Demand for Digital-First Patient Engagement Platforms | +1.4% | England dominant, Scotland and Wales secondary | Medium term (2-4 years) |

| Heightened Cyber-Threat Environment Driving Security Consulting | +1.1% | UK-wide, concentrated in NHS England acute and mental health trusts | Short term (≤ 2 years) |

| Regulatory Push for Healthcare Price-Transparency Compliance | +0.8% | England primarily, NHS Payment Scheme compliance obligations | Medium term (2-4 years) |

| Generative AI Advisory for Clinical Decision Support | +1.3% | England leading via NHS AVT guidance, Scotland adopting through NSS digital programs | Medium term (2-4 years) |

| Climate-Resilience Planning for Hospital Infrastructure | +0.7% | UK-wide, with Welsh Health Building Notes and NHS England climate adaptation activity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Value-Based Care Models

The UK healthcare consulting services market is gaining sustained support from the NHS move toward population-based delivery and value-linked contracting. NHS Confederation noted in March 2026 that the Population Health Delivery Models blueprint moved IHO, SNP, and MNP contracts into an operating framework rather than a long-range policy discussion. This change matters because systems now need outside support to redesign payment rules, care pathways, and accountability structures around population outcomes instead of activity volumes. NHS England also sought external expertise to help manage GBP 7.5 billion (USD 9.5 billion) in all-age continuing care spend under a no saving, no payment model, which pushes consulting work into direct performance and risk-sharing territory. The pressure is stronger because the 2025/26 operating plan identified a GBP 4.4 billion (USD 5.6 billion) planning gap across systems, leaving limited room for internally funded trial and error during redesign work. Thames Valley ICB’s program with University of Oxford researchers shows that consulting teams are already being embedded into governance design and value measurement, which extends the demand base for the UK healthcare consulting services market well beyond short-term policy support[1]University of Oxford NIHR ARC OxTV, “Helping Thames Valley ICB Spend £5.6 Billion More Wisely,” University of Oxford, phc.ox.ac.uk.

Surging Demand for Digital-First Patient Engagement Platforms

The UK healthcare consulting services market is also benefiting from a wider move toward digital-first patient access, interoperability, and post-implementation optimization. NHS trust IT spend reached GBP 4.1 billion (USD 5.2 billion) in 2024/25, and that expansion created a larger installed base that now needs advisory support for integration, workflow redesign, and patient-facing service upgrades. The spending pattern is shifting because once EPR adoption nears saturation, consulting work moves from software deployment toward optimization, interoperability, and digital front-door design. A Royal College of Physicians review published in January 2026 found that 68% of 548 surveyed members disagreed that the NHS had the right digital infrastructure for widespread AI adoption, which points to an ongoing readiness gap rather than a completed transformation story. The government’s GBP 600 million (USD 802 million) investment in Frontline Digitisation and Connecting Care Records for 2025/26 gives this demand a funded pathway rather than a purely aspirational one. That funding environment favors firms in the UK healthcare consulting services market that can combine technology advisory with delivery assurance, NHS standards knowledge, and patient engagement design.

Heightened Cyber-Threat Environment Driving Security Consulting

Cyber risk is now a direct operating issue for the UK healthcare consulting services market rather than a narrow IT concern. After the June 2024 Synnovis ransomware incident disrupted transfusions and appointments across London trusts, NHS England described ransomware as endemic and required suppliers to align with an eight-step cybersecurity charter. NHS England then retained IBM on a GBP 7 million (USD 9 million) cyber security operations center monitoring contract in June 2025, showing that security monitoring and resilience support are now part of routine national procurement. The larger consulting need sits in supplier assurance, vulnerability management, contractual security schedules, and maturity reviews, because many NHS bodies do not have enough specialist internal capacity to standardize these controls at scale. Cybersecurity demand is also spreading beyond England, as Public Contracts Scotland recorded a competitively procured ransomware readiness review covering NHS Scotland boards in 2025. This broadening footprint means the UK healthcare consulting services market is seeing security advisory work become a recurring service line rather than a one-off incident response task.

Regulatory Push for Healthcare Price-Transparency Compliance

The UK healthcare consulting services market is drawing additional work from changes to pricing rules, tariff consultation, and value-based procurement. NHS England’s consultations on the 2025/26 and 2026/27 NHS Payment Scheme are reshaping how elective activity, best practice tariffs, and urgent care are priced and administered across the system. The removal of proposed payment limits for elective services after consultation feedback created planning uncertainty, and that uncertainty itself supports demand for advisory work in pricing, financial modeling, and scenario design. At the same time, the NHS expanded value-based procurement for medtech through pilots across 13 trusts in 2025 and a broader rollout path into 2026, which increases the need for consulting support on clinical effectiveness review and procurement design. Aligned Payment and Incentive frameworks and Best Practice Tariff guidance also require finance teams to interpret new rules while managing limited staff capacity. That combination keeps the UK healthcare consulting services market closely linked to payment reform, not just to digital or strategy work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Shortage and Soaring Bill Rates | -1.4% | UK-wide, with London and South East premium most acute | Short term (≤ 2 years) |

| Prolonged Provider Margin Squeeze Curbing Discretionary Spend | -1.1% | England-wide, worst in financially distressed ICB systems | Medium term (2-4 years) |

| Data-Ownership Disputes in Multi-Party Analytics Ecosystems | -0.7% | UK-wide, most acute in multi-ICB analytics consortia | Medium term (2-4 years) |

| Rising Carbon-Footprint Scrutiny of Consultants' Travel | -0.3% | UK-wide, with EU compliance spill-over for cross-border firms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage and Soaring Bill Rates

The UK healthcare consulting services market faces a clear staffing constraint because projects increasingly require people who understand clinical pathways, digital systems, data governance, and NHS procurement at the same time. Rising consultant day rates are making it harder for buyers to approve advisory spend on routine terms, especially when projects need senior healthcare specialists rather than general business teams. The pressure is stronger because NHS staffing shortages also affect the pool from which consulting firms recruit clinical subject matter experts, which reduces bench depth for transformation work. Smaller firms are especially exposed because they cannot always absorb wage inflation, retention bonuses, and IR35-related pricing pressure as easily as large multidisciplinary competitors. This keeps the UK healthcare consulting services market open to demand growth, but it also raises delivery costs and lengthens staffing cycles on complex engagements.

Prolonged Provider Margin Squeeze Curbing Discretionary Spend

Financial pressure on providers remains the clearest spending restraint for the UK healthcare consulting services market. NHS England reported a collective provider deficit of GBP 553 million (USD 700 million) in 2024/25, and 53% of providers remained in deficit even after improvement from the prior year[2]NHS England, “Consolidated NHS Provider Accounts 2024/25,” NHS England, england.nhs.uk. Nuffield Trust also highlighted an underlying structural gap of at least GBP 4.5 billion (USD 6 billion) once non-recurring support is excluded, which shows that balance sheet pressure is not a one-year issue. The King’s Fund noted that NHS organizations face a 2% productivity improvement requirement while also being pushed to reduce agency and bank staffing costs, which can limit willingness to fund advisory work unless it shows measurable operational return. That is why more contracts in the UK healthcare consulting services market are moving toward outcome-based and risk-sharing models that shift commercial pressure onto suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: IT Consulting Dominant but Digital Transformation Accelerating

IT Consulting held 31.31% of the UK healthcare consulting services market share in 2025, making it the largest service category as NHS organizations continued to modernize core systems, data flows, and infrastructure. This leadership position reflected continued trust spending on digital estate, EPR programs, interoperability, and system integration work across provider settings. Digital Transformation Consulting is projected to expand at an 11.38% CAGR through 2031, supported by the move from initial deployment into optimization, workflow redesign, and connected care implementation. The GBP 600 million (USD 802 million) Frontline Digitisation and Connecting Care Records funding path for 2025/26 gives these mandates a formal spending route inside the UK healthcare consulting services industry rather than leaving them dependent on isolated trust-level budgets.

Strategy Consulting is regaining weight because IHO contract design, population health planning, and the NHS England to DHSC transition all require organization-wide design work that cannot be solved by software implementation alone. Operations Consulting is benefiting from recurring productivity pressure as provider and DHSC bodies are pushed to redesign workflows, reduce waste, and improve service throughput. Financial Consulting is also seeing steady demand because tariff reform, value-based procurement, and planning uncertainty require stronger modeling and commercial support. HR and Talent Consulting is gaining relevance as ICS and ICB structures continue to reshape workforce models and leadership design. Across the UK healthcare consulting services industry, DTAC, DCB, and procurement framework requirements are raising entry barriers and rewarding firms that can cover multiple service lines under a single compliant delivery model.

By End User: Healthcare Providers Largest, Government Agencies Fastest-Growing

Healthcare Providers accounted for 28.24% of the UK healthcare consulting services market in 2025, which kept trusts, foundation trusts, and primary care organizations at the center of advisory demand. This group continues to need support on EPR implementation, financial recovery, integrated care redesign, and clinical operations improvement. The scale of provider-side need remains high because care delivery bodies are absorbing digital modernization, tariff adjustment, workforce redesign, and tighter performance expectations at the same time. That keeps providers as the anchor client base even while funding pressure forces stronger scrutiny of consulting outcomes.

Government Agencies are the fastest-growing end-user group, with a projected 10.52% CAGR through 2031. The main driver is the widening scope of central and commissioning-level transformation linked to the NHSE-DHSC merger, digital operating model redesign, and IHO framework rollout. Life sciences companies remain an important secondary client group because they need support on real-world evidence, market access, and NICE-related work, while IQVIA’s NHS solutions position shows how data-linked consulting can differentiate this part of the UK healthcare consulting services market. Healthcare payers, healthcare IT vendors, and medtech start-ups are also expanding their advisory use as DTAC, MHRA, and post-Brexit medical device compliance create a growing need for specialist regulatory and commercialization support. The client mix will continue to broaden as more care shifts toward neighborhood and community settings after 2026, which should rebalance future work away from a purely acute provider focus.

By Delivery Model: Hybrid Leads but Remote Growth Outpaces

Hybrid delivery accounted for 45.52% of the UK healthcare consulting services market in 2025, which shows that buyers still want a blend of in-person support and flexible remote execution. This format fits NHS work well because it allows consultants to handle workshops, governance sessions, and site-sensitive activity on location while completing analytics, design, and project management tasks virtually. Hybrid delivery also aligns with the spread of consulting demand across integrated care systems and devolved health systems, where a fully on-site model is often too costly and slow. That is why the UK healthcare consulting services market continues to treat hybrid working as the default model for many transformation engagements.

Remote or Virtual Consulting is projected to grow at a 10.25% CAGR through 2031, making it the fastest-expanding delivery model. NHS procurement is placing more weight on social value and carbon reduction, which discourages high-travel delivery structures and supports remote execution where appropriate. The new NHS SBS framework environment under the Procurement Act 2023 also reinforces flexibility in how consulting work is delivered, which supports broader acceptance of remote and blended formats. On-site Consulting remains necessary for sensitive work such as pathway redesign, leadership development, and cyber incident response, so remote growth will expand the mix rather than replace physical engagement. This balance is opening room in the UK healthcare consulting services market for smaller regional specialists that can compete nationally without carrying the cost base of a large office network.

Geography Analysis

England held the dominant position in the UK healthcare consulting services market in 2025, supported by 87% of local NHS trust IT spend and by the presence of 42 integrated care systems that shape most large consulting mandates. The NHSE-DHSC merger, the rollout of IHO contracts, and frontline digitization funding together create the densest pipeline of strategy, operations, and digital work anywhere in the country. London and the South East carry an added premium because they combine large trust budgets, central NHS institutions, and the highest concentration of framework-led procurement activity. Guy’s and St Thomas’ NHS Foundation Trust alone reported GBP 109 million (USD 138.2 million) in IT spend for 2024/25, which illustrates the scale of addressable digital advisory work in the capital area.

Scotland is the second-largest geography in the UK healthcare consulting services market. NHS National Services Scotland is driving major procurement activity, including the 2025 selection of an integrated cloud finance, HR, and procurement system valued at GBP 206 million (USD 261 million). Scotland is also building a more distinct cybersecurity advisory base, as shown by the national ransomware readiness review commissioned across NHS Scotland boards. The separate procurement regime and devolved governance structure mean firms cannot simply reuse England-facing methods without adapting to Scotland-specific compliance and buyer requirements. Welsh health estate standards also keep resilience and infrastructure planning on the agenda, which supports specialist advisory work beyond digital transformation.

Northern Ireland and other UK territories make up a smaller part of the UK healthcare consulting services market, but they still offer room for expansion as transformation and modernization work continues under Health and Social Care trust structures. Procurement is less standardized there than in England, which can slow repeatable framework-led growth but also leaves room for firms that can help shape more formal buying routes. Across the wider UK, the spread of DTAC, MHRA, cybersecurity, and value-based care requirements means consulting demand is no longer confined to one region or one client type. The geographic pattern remains England-heavy, but devolved systems are becoming more important for specialist mandates where local regulation and operating models create clear barriers to entry.

Competitive Landscape

The UK healthcare consulting services market is moderately concentrated at the top. A handful of large firms such as Deloitte, Accenture, PwC, KPMG, and McKinsey continue to capture a disproportionate share of high-value NHS transformation work, yet more than 163 accredited suppliers compete through NHS framework structures for mid-tier and specialist mandates[3]NHS Shared Business Services, “Consultancy and Advisory Services for Health Framework Agreement SBS10197,” NHS Shared Business Services, sbs.nhs.uk. This means scale matters most where clients want national coverage, integrated delivery, and procurement certainty. Framework placement is therefore one of the strongest competitive advantages in the UK healthcare consulting services market because it lowers buyer friction and narrows the field before technical evaluation even begins. Firms without access to NHS SBS, CCS, or equivalent compliant routes remain less visible for major public contracts.

Digital and data capability is the next clear dividing line. IQVIA has strengthened its position by tying consulting work to data access and NHS-facing solutions, including partnerships that cover 95% of NHS trusts. Accenture also showed the value of combining digital delivery with consulting when it secured a 30-month NHS digital capability contract from January 2025 and a separate Appointments and Patient Choice award with a ceiling value of up to GBP 124 million (USD 165 million). Deloitte remains well placed in cyber and transformation work, supported by NHS awards covering incident response, board improvement, and digital consultancy activity. Cognizant’s DHSC support role for the new NHS England IT landscape also shows that suppliers with execution depth can win work tied directly to structural system change.

Specialist space remains open in three areas. Outcome-based advisory gives firms with operational delivery DNA an edge because buyers increasingly want savings-linked or performance-backed contracts rather than pure time-and-materials work. Climate and estate resilience consulting is also becoming more competitive, with engineering and infrastructure specialists able to challenge traditional management consultancies on hospital planning mandates. A third opening sits in AI and digital medical device assurance, where smaller firms with DTAC, DCB, and MHRA experience can displace larger rivals on cost and speed. So while leading firms still dominate the top end of the UK healthcare consulting services market, the structure remains far from closed and continues to reward niche capability that maps closely to NHS compliance and delivery needs.

United Kingdom Healthcare Consulting Services Industry Leaders

Accenture

Deloitte

PwC

KPMG

EY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NHS England published its Towards Population Health Delivery Models blueprint, formally establishing the operating framework for IHO, SNP, and MNP contracts and designating spring 2026 as the start date for the first IHO contract wave. This policy milestone is expected to generate multi-year strategy and financial redesign consulting mandates across all 42 ICBs.

- April 2025: Mace Consult and Turner & Townsend, in a joint venture with Deloitte as a key subcontractor, were awarded a GBP 307 million (USD 389 million) Programme Delivery Partner contract for the NHS New Hospital Programme, the largest hospital infrastructure consulting mandate in a generation.

United Kingdom Healthcare Consulting Services Market Report Scope

As per the scope of the report, healthcare consulting services refer to specialized professional services provided to healthcare organizations, providers, and stakeholders to improve their operational efficiency, clinical outcomes, compliance, financial performance, and overall management.

The segmentation for the United Kingdom healthcare consulting services market is categorized by service type, end user, and delivery model. By service type, it includes IT consulting, strategy consulting, operations consulting, digital transformation consulting, financial consulting, and HR and talent consulting. By end user, it covers healthcare providers, healthcare payers, life sciences companies, government agencies, healthcare IT vendors, and MedTech start-ups. By delivery model, it is segmented into on-site consulting, remote/virtual consulting, and hybrid model. For each segment, the market size and forecast are provided in terms of value (USD).

| IT Consulting |

| Strategy Consulting |

| Operations Consulting |

| Digital Transformation Consulting |

| Financial Consulting |

| HR and Talent Consulting |

| Healthcare Providers |

| Healthcare Payers |

| Life Sciences Companies |

| Government Agencies |

| Healthcare IT Vendors |

| MedTech Start-Ups |

| On-Site Consulting |

| Remote / Virtual Consulting |

| Hybrid Model |

| By Service Type | IT Consulting |

| Strategy Consulting | |

| Operations Consulting | |

| Digital Transformation Consulting | |

| Financial Consulting | |

| HR and Talent Consulting | |

| By End User | Healthcare Providers |

| Healthcare Payers | |

| Life Sciences Companies | |

| Government Agencies | |

| Healthcare IT Vendors | |

| MedTech Start-Ups | |

| By Delivery Model | On-Site Consulting |

| Remote / Virtual Consulting | |

| Hybrid Model |

Key Questions Answered in the Report

What is the current size of the UK healthcare consulting services market?

The UK healthcare consulting services market stands at USD 3.36 billion in 2026 and is projected to reach USD 4.99 billion by 2031 at an 8.22% CAGR.

What is driving demand for consulting services across the UK healthcare system?

The main demand drivers are the NHSE-DHSC merger, IHO contract rollout, digital modernization, cybersecurity pressure, and growing AI governance needs.

Which service segment leads consulting demand in the UK healthcare sector?

IT Consulting led with a 31.31% share in 2025, supported by ongoing NHS digital modernization, EPR work, and interoperability needs.

Which client group is expanding the fastest in this space?

Government Agencies are projected to grow at a 10.52% CAGR through 2031 as central transformation, commissioning redesign, and operating model changes widen advisory demand.

How are consulting delivery models changing in the UK healthcare field?

Hybrid delivery led with 45.52% share in 2025, while Remote or Virtual Consulting is forecast to grow fastest at 10.25% CAGR as buyers weigh cost, flexibility, and carbon reduction.

Why does England remain the main geography for consulting activity?

England holds the largest share because it combines 42 integrated care systems, the NHSE-DHSC transition, major digitization funding, and the broadest set of NHS compliance mandates.

Page last updated on: