United Kingdom Digital Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

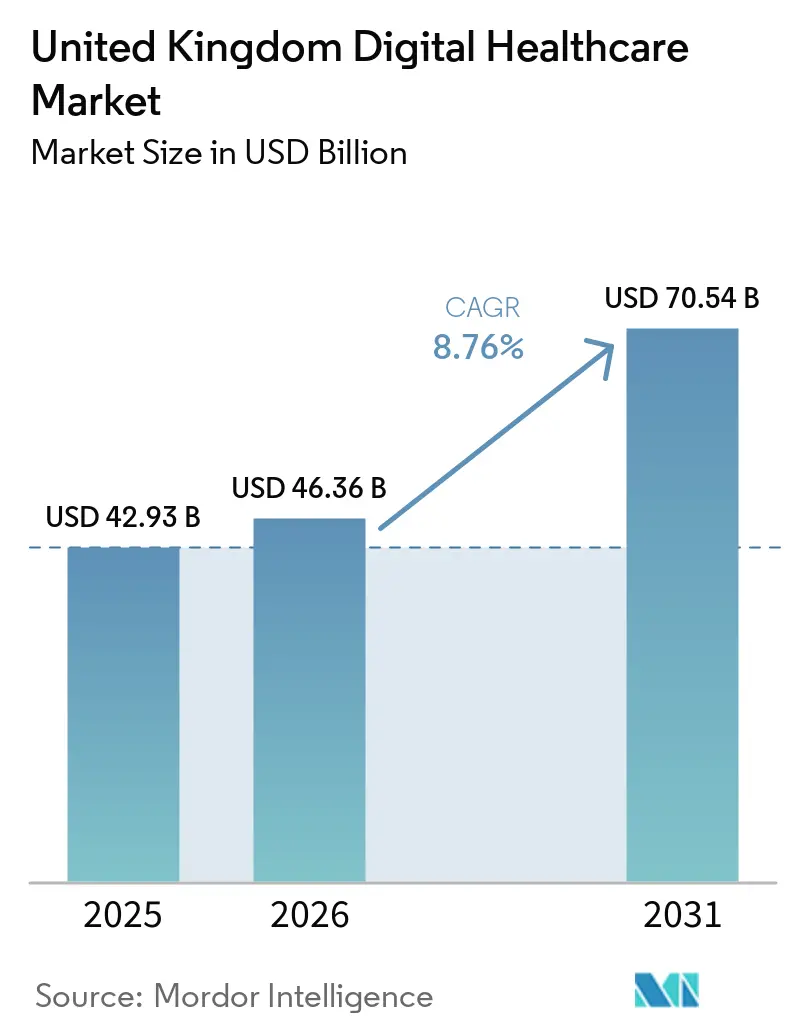

| Base Year Market Size (2025) | USD 42.93 Billion |

| Market Size (2026) | USD 46.36 Billion |

| Market Size (2031) | USD 70.54 Billion |

| Growth Rate (2026 - 2031) | 8.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Digital Healthcare Market Analysis by Mordor Intelligence

The United Kingdom Digital Healthcare Market size is projected to expand from USD 42.93 billion in 2025 and USD 46.36 billion in 2026 to USD 70.54 billion by 2031, registering a CAGR of 8.76% between 2026 to 2031.

Growth in the UK digital healthcare market is tied to a clear shift in NHS procurement, with the Department of Health and Social Care and NHS England planning GBP 7.4 billion, or USD 9.3 billion, in technology, digital, and data investment between 2026 and 2030. The 2025 Spending Review added GBP 10 billion, or USD 12.6 billion, for NHS technology and digital transformation through 2028/29, which lifted annual capital well above the prior financial year and gave suppliers stronger visibility on future program pipelines. NHS trusts also increased IT spending by 9% to GBP 4.1 billion, or USD 5.2 billion, in 2024/25 as EPR deployments, cloud migration, and AI-enabled workflow tools moved from isolated projects into core delivery plans. Adoption in the UK digital healthcare market is now moving from emergency digitization toward connected care, patient self-service, and workflow automation, helped by the NHS App rollout, remote monitoring expansion, and the goal of making hospitals fully AI-enabled within the life of the NHS 10 Year Health Plan. Competitive positioning in the UK digital healthcare market is increasingly shaped by interoperability readiness, managed service depth, cybersecurity assurance, and the ability to operate within a future single patient record environment that will speed up data sharing across NHS providers.

Key Report Takeaways

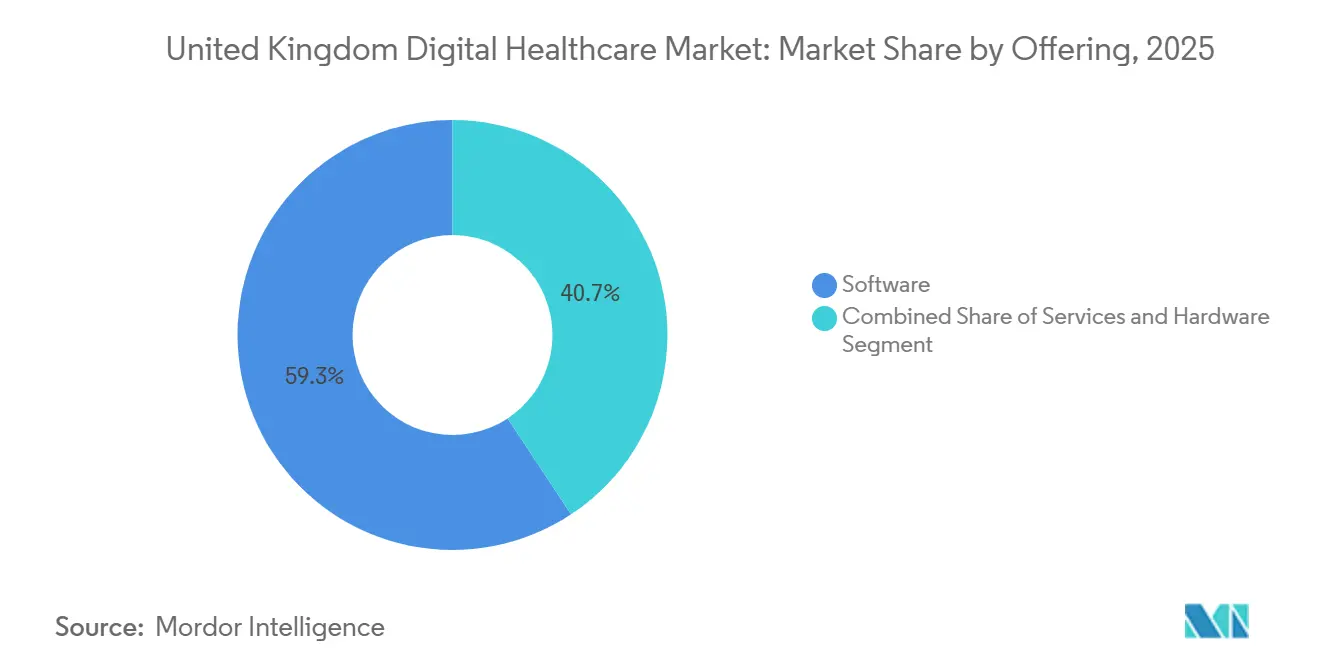

- By offering, software held 59.27% of the UK digital healthcare market share in 2025, while services are projected to grow at a 9.08% CAGR through 2031.

- By technology, telehealth and telemedicine accounted for 35.79% of revenue in 2025, while healthcare analytics and AI are forecast to expand at an 8.98% CAGR through 2031.

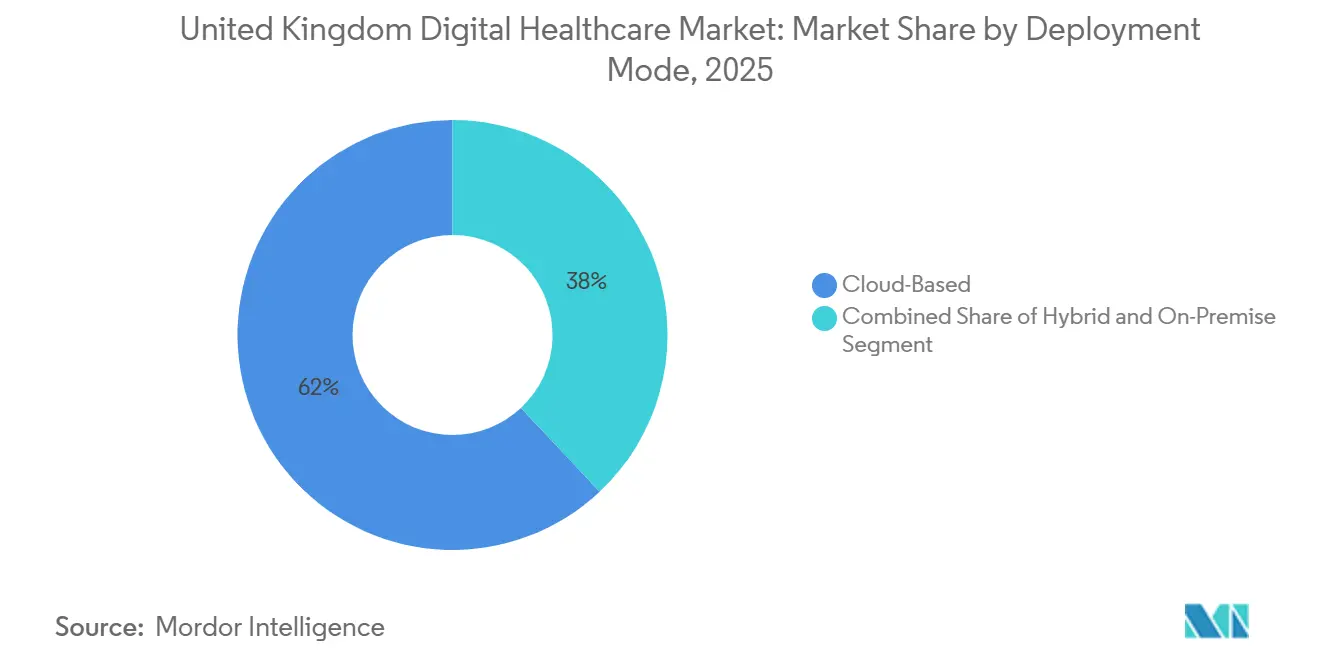

- By deployment mode, cloud-based systems represented 62.02% of the UK digital healthcare market size in 2025, while hybrid deployment is expected to advance at a 9.96% CAGR through 2031.

- By application, chronic disease management captured 42.82% of revenue in 2025, while diagnostics and decision support are set to grow at a 10.49% CAGR through 2031.

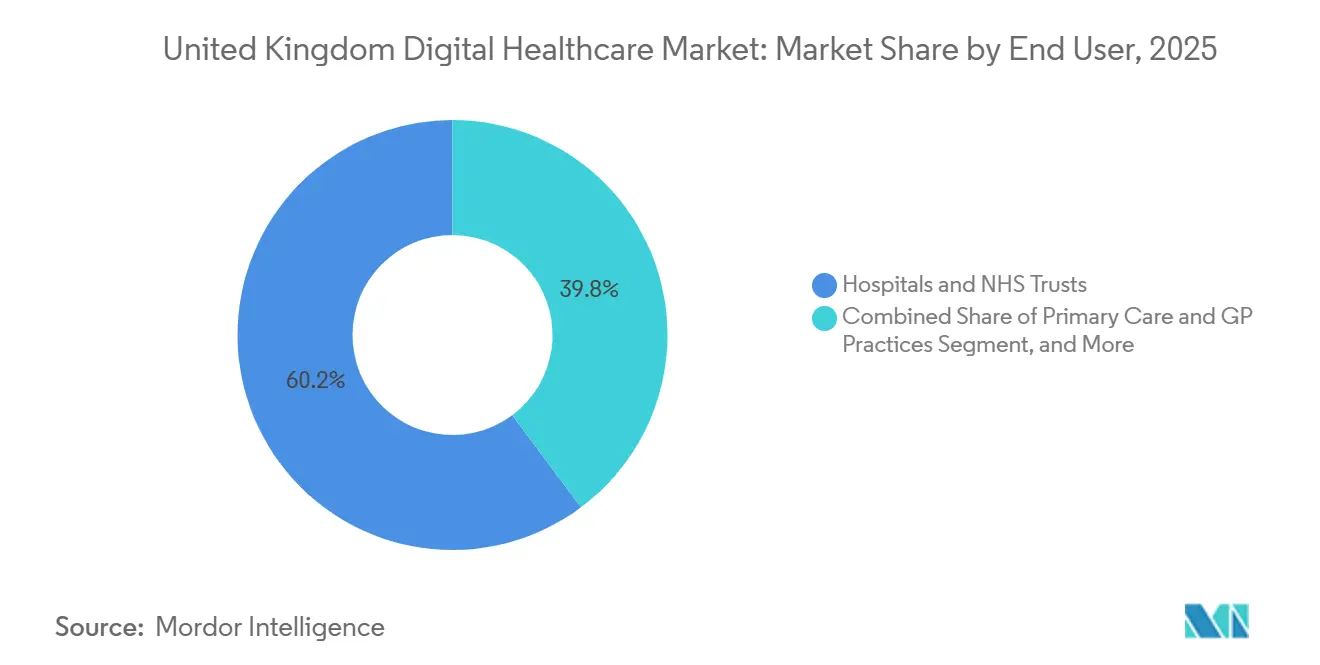

- By end user, hospitals and NHS trusts contributed 60.23% of spending in 2025, while patients and home-care settings are projected to expand at a 10.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Digital Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NHS Electronic Patient Record Rollouts | +2.0% | England primarily, with parallel adoption in Scotland and Wales | Short term (≤ 2 years) |

| Virtual Ward Expansion Beyond Acute Settings | +1.5% | National, with concentration in NHS England ICBs and NHS Scotland Hospital at Home | Medium term (2-4 years) |

| NHS App as a National Digital Front Door | +1.5% | England primary focus, with NHS Wales and NHS Scotland building parallel capability | Medium term (2-4 years) |

| AI-Enabled Clinical Workflow Automation | +1.8% | UK wide, with stronger early adoption in major NHS trusts and primary care | Medium term (2-4 years) |

| Community Care Digitization and Home Monitoring | +1.2% | National, with faster uptake in areas with high chronic disease burden | Long term (≥ 4 years) |

| FHIR-Based Interoperability Standardization | +0.8% | National, aligned with NHS England’s UK Core FHIR R4 implementation standard | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NHS Electronic Patient Record Rollouts Reach Critical Mass

As of the 2025 Digital Maturity Assessment, 93% of NHS providers had a live EPR, yet only 30% had integrated bi-directional data flows, which means the current wave centers on optimization rather than first-time installation. NHS England expects 97% of acute trusts to have EPR coverage by the end of 2026, so rollout work is still feeding demand across the UK digital healthcare market. Local NHS IT spending is projected to rise from GBP 4.9 billion, or USD 6.2 billion, in 2025/26 to GBP 6.8 billion, or USD 8.6 billion, by 2028/29, which gives platform vendors and service partners a longer runway for implementation and support work. The important commercial change is that revenue funding is now being used for EPR optimization, training, and workflow redesign through the NHS Frontline Productivity Programme, which widens spend beyond initial software licensing. This change keeps managed services, integration support, user training, and post-go-live consulting active even in trusts that have already completed major deployments, and it supports recurring rather than one-off contract value.

Virtual Ward Expansion Beyond Acute Settings

NHS England operated 12,825 virtual ward beds in March 2025, and the South East alone recorded more than 85,000 virtual ward admissions in 2024, which was 18% above the 2023 level.[1]NHS England South East, “Growth of Virtual Wards in the South East Sees More Patients Benefitting from Care at Home,” NHS England, england.nhs.uk The NHS 10 Year Health Plan committed to a national procurement route for a proactive planned care platform, and it linked incentives more directly to community-based urgent care activity. One NHS-commissioned trial found Hospital at Home care to be less expensive than inpatient treatment, with average savings of GBP 2,265, or USD 2,860, per patient episode, and that figure is now shaping local business cases. Pathways for COPD, heart failure, and frailty are now being designed as virtual-first services rather than as add-on pilots, which changes where remote monitoring vendors sit in care delivery. That shift strengthens demand in the UK digital healthcare market for connected devices, workflow platforms, and home-setting data integration that can work within routine NHS operations.

NHS App as a National Digital Front Door

The NHS App now has 41 million registered users, it is connected to every hospital trust in England, and it recorded 15 million logins in March 2026, which was 33% above the prior year. Since July 2024, the app has prevented 1.5 million missed hospital appointments and saved 5.7 million staff hours, which gives NHS leadership a direct productivity case for continued investment. The NHS Medium-Term Planning Framework targets 95% of post-triage appointments to be bookable through the app by 2028/29, and an AI-enabled smart triage tool has already reached more than 1 million patients across 200-plus GP practices. This turns the NHS App into more than an access channel because it is also becoming a route for digital therapeutics, remote monitoring enrollment, and clinically approved digital tools. As a result, the UK digital healthcare market is gaining a stronger patient-facing distribution layer that did not exist in earlier NHS procurement cycles.

AI-Enabled Clinical Workflow Automation

AI-scribing tools have reached large-scale NHS deployment faster than earlier waves of clinical technology, with Accurx Scribe reaching 200,000 existing NHS users across 98% of GP practices that use the Accurx platform by April 2025.[2]Accurx, “Accurx and Tandem Health Partner to Bring AI Scribing to the Whole NHS,” Accurx, accurx.com Oracle Health launched its Clinical AI Agent across the UK in February 2026 after pilots at Barts Health, Imperial College Healthcare, and Milton Keynes University Hospital. A GOSH-led trial across 9 NHS London sites and more than 17,000 patient encounters found that the TORTUS AI-scribing tool delivered transformative benefits for clinicians and patients. NHS procurement is also becoming more structured, with vendor scrutiny tied to data protection, clinical integration, and deployment standards, which raises entry barriers for smaller suppliers. This favors vendors in the UK digital healthcare market that can combine strong governance with proven write-back capability into core clinical systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Interoperability Debt Across NHS Estates | -1.5% | National, with stronger pressure in systems spanning acute, community, and mental health care | Medium term (2-4 years) |

| Cybersecurity and Clinical Safety Compliance Burden | -1.2% | National, with high impact in London and large academic trusts with complex estates | Short term (≤ 2 years) |

| Long Validation Cycles for Regulated Software and AI Tools | -0.7% | National, with MHRA regulation affecting all digital health applications | Long term (≥ 4 years) |

| Shortage of Clinical Informatics and Health Data Talent | -0.5% | National, with stronger pressure in systems adopting advanced analytics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Interoperability Debt Across NHS Estates

The 2025 Digital Maturity Assessment showed that only 30% of EPR-equipped NHS providers had integrated bi-directional data flows, and this remains one of the clearest limits on connected care growth. NHS England’s Frontline Productivity Programme and the NHS Canonical Data Model are intended to narrow this gap, yet the board has stated that full benefits from the Single Patient Record program are not expected to be realized until 2030. Regions that still rely on incompatible systems face slower care pathway redesign, slower data exchange, and more expensive integration work, particularly where acute, community, and mental health services need to coordinate. This delay matters for the UK digital healthcare market because revenue tied to remote monitoring, shared care, and decision support depends on reliable data exchange between settings. Vendors that can demonstrate compliance with FHIR UK Core R4 and NHS GP Connect standards, therefore, have a clearer commercial advantage than those that still depend on bespoke links.[3]HL7 UK, “Interweave FHIR Health and Social Care Data Sharing Use Case,” HL7 UK, hl7.org.uk

Cybersecurity and Clinical Safety Compliance Burden

The Synnovis ransomware attack in June 2024 disrupted services across major London trusts, canceled more than 10,000 appointments, and was later estimated to have cost GBP 32.7 million, or USD 41.3 million. One death was linked to the attack, which showed that cyber incidents in NHS settings can cause direct clinical harm as well as financial damage. By late 2025 and into 2026, NHS networks also faced threats related to Oracle zero-day vulnerabilities, with Barts Health and NHS England named by ransomware groups. For suppliers in the UK digital healthcare market, MHRA clinical safety rules, NHS Data Security and Protection Toolkit obligations, and ICO reporting duties lengthen procurement cycles and raise implementation costs. The burden falls most heavily on smaller vendors that have innovative products but limited compliance resources, which slows their ability to compete for large NHS contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Growth Signals NHS’s Shift from Deployment to Value Realisation

Software held 59.27% of the UK digital healthcare market share in 2025, supported by EPR licensing, SaaS-based clinical platforms, and the fast commercial expansion of ambient voice and analytics tools. This leadership reflects structural demand rather than short-term momentum because NHS standardization around a limited set of EPR vendors and app ecosystems creates a large renewal base. The software layer also benefits from the fact that cloud-native clinical platforms are now being treated as long-term operating infrastructure rather than stand-alone projects. That makes procurement less episodic and more tied to multiyear transformation plans across trusts and integrated care systems. It also keeps software deeply embedded in the broader UK digital healthcare industry as trusts seek fewer systems with stronger clinical and administrative coverage.

Services is the fastest-growing segment, with the UK digital healthcare market size for services expected to expand at a 9.08% CAGR from 2026 to 2031. NHS organizations are shifting more budget toward managed services, implementation support, optimization work, and AI-as-a-service after major go-lives. EPR usability surveys showed only 34% of NHS staff felt their EPR made them more efficient, which helps explain why trusts are spending more on training, workflow redesign, and post-implementation support. Hardware remains smaller, but it still matters because virtual ward kits, connected wearables, and remote monitoring devices are central to home-based care models. The planned GBP 2 billion, or USD 2.5 billion, Clinical Digital Health Systems 2.0 framework also shows that NHS contracting is moving toward bundled software and service delivery rather than stand-alone product purchasing.

By Technology: AI Outpaces Telehealth as the Primary Incremental Investment Category

Telehealth and telemedicine held 35.79% of revenue in 2025, which kept them as the largest technology category in the UK digital healthcare market. Their lead still reflects the long aftereffects of pandemic-era adoption, especially in urgent access, follow-up visits, and pathway redesign for chronic care. Remote patient monitoring is also expanding under this technology base because virtual ward models continue to rely on connected devices, alert systems, and clinician dashboards. mHealth applications are benefiting from the wider function set of the NHS App, which increasingly supports forms, messaging, appointment management, and chronic care interactions. Digital health systems are consolidating around fewer platform providers, which keeps the technology stack more integrated across the UK digital healthcare industry.

Healthcare analytics and AI are the fastest-growing technology segments at an 8.98% CAGR through 2031, driven by predictive operations, decision support, and ambient voice documentation. The NHS Federated Data Platform and related AI safety programs are helping turn data infrastructure into a direct enabler of clinical and operational applications. OECD analysis identified the UK as a leading example of scalable cloud adoption in health and pointed to AI diagnostics procurement as a benchmark for public sector deployment. Digital therapeutics are also growing, but they remain more constrained because NICE evidence pathways still require long validation cycles before broad commissioning support builds. This leaves AI and analytics as the main incremental spending category because they can improve documentation, throughput, triage, and capacity management without always waiting for entirely new care pathways.

By Deployment Mode: Hybrid Models Capture the Gap Between Cloud Promise and On-Premise Reality

Cloud-based deployment accounted for 62.02% of the UK digital healthcare market size in 2025, reflecting NHS cloud-first policy and the move of communications, analytics, and clinical platforms toward SaaS models. This position was strengthened by the fact that cloud delivery reduces the burden of local upgrades and speeds the release cycle for new functions. Trusts also see cloud platforms as a way to support wider data exchange, shared records, and mobile access without maintaining as much local infrastructure. At the same time, many NHS estates still carry critical on-premise systems that cannot be replaced in a single cycle. That is why cloud leadership in the UK digital healthcare market has not eliminated the need for mixed operating environments.

Hybrid deployment is the fastest-growing mode at 9.96% CAGR through 2031 because trusts are increasingly linking cloud-native modules to on-premise EPR cores. This model is especially common in acute settings where data residency, security, and clinical workflow sensitivity still favor retaining parts of the core environment on site. On-premise deployments therefore remain relevant in radiology archives, genomics systems, and high-security mental health settings where replacement paths are slower. East Sussex Healthcare NHS Trust’s 2026 EmPoweR EPR go-live showed how cloud migration can support faster patient flow updates and easier optimization after deployment. Oracle’s planned USD 5 billion investment in UK cloud infrastructure over five years also supports continued hybrid migration momentum because suppliers and trusts both gain more local capacity for regulated workloads.

By Application: Diagnostics AI Disrupts the Established Chronic Disease Spending Hierarchy

Chronic disease management held 42.82% of application revenue in 2025, which made it the largest use case in the UK digital healthcare market. This base was anchored in primary care registers, long-term condition pathways, and virtual ward programs for heart failure, COPD, and respiratory disease. The segment also benefited from the fact that chronic care is where the NHS has some of its clearest volume pressures and strongest need for continuous patient contact. Patient monitoring, messaging, scheduling, and care coordination tools, therefore, continue to find great and repeatable demand in this area. That gives chronic care a stable core role even as newer AI-enabled applications gain visibility.

Diagnostics and decision support is the fastest-growing application at a 10.49% CAGR through 2031 as triage, imaging analysis, and predictive deterioration tools move from pilot projects into broader deployment. The Respiratory Transformation Partnership, valued at more than GBP 10 million, or USD 12.6 million, shows how NHS bodies and pharmaceutical companies are co-investing in digital diagnostics infrastructure to improve care closer to home. Mental health tools, preventive care, and administration workflow products are also expanding as the NHS seeks better self-management, documentation, and throughput improvement. NICE’s Evidence Standards Framework remains an important gateway for these products because commissioner confidence still depends on formal evaluation paths. The result is that diagnostics and decision support are now changing spending priorities within the UK digital healthcare market without displacing the large chronic care base that still dominates present revenue.

By End User: Patient-Side Platforms Outpace Hospital Spend Growth

Hospitals and NHS trusts accounted for 60.23% of spending in 2025, which kept them as the largest end-user group in the UK digital healthcare market. This position reflects EPR licenses, major managed service contracts, enterprise communications tools, and hospital-grade AI deployments. Acute providers also remain the first destination for many large digital transformation budgets because their estates are complex and their workforce pressures are immediate. Primary care and GP practices still represent a major installed base, but procurement there is increasingly shaped by platform renewal and competitive change rather than by first-time digitization. That leaves hospitals as the revenue anchor even as newer care settings expand.

Patients and home-care settings are the fastest-growing end-user segment at a 10.17% CAGR through 2031, driven by virtual wards, home monitoring pilots, and wider use of patient-facing digital tools. NHS England’s remote monitoring pilots are expected to free 500,000 appointments annually once fully operational, which gives this channel a strong service efficiency case. Cera’s AI fall-prediction tool already processes more than 2 million home care visits per month, which shows the scale that home-based analytics can reach when linked to NHS pathways. Primary care is also changing because Medicus became the first serious GP IT challenger in 25 years, and TPG’s 2026 acquisition of Optum UK brought private equity ownership into a core data-rich part of the UK digital healthcare industry. Pharmaceutical and life sciences companies are also becoming more active end users and partners as they co-develop digital diagnostics and evidence platforms around NHS care delivery.

Geography Analysis

England remains the clear center of the UK digital healthcare market in 2025 because the NHS App, the Federated Data Platform, and the EPR rollout program are all being driven through NHS England at a national scale. The 2025 Spending Review committed GBP 10 billion, or USD 12.6 billion, to NHS technology, and much of that spending is being directed through England’s health system priorities. England also benefits from the strongest policy push on digital-first GP access, wider appointment booking through the NHS App, and the long-term goal of full AI enablement in hospitals. The DHSC’s planning case for digital investment includes large productivity gains over both four-year and ten-year periods, which has increased urgency in ICB procurement and vendor engagement. Within England, the South East stands out because it has more than 2,000 virtual ward beds and more than 85,000 virtual ward admissions in 2024, which makes it an early market for remote monitoring vendors.

London is also a distinct part of the UK digital healthcare market because its concentration of academic NHS trusts supports earlier validation and deployment of AI documentation, ambient voice, and diagnostic tools. Scotland is smaller in absolute spend, but it is moving quickly through Hospital at Home expansion and stronger virtual care deployment. NHS Greater Glasgow and Clyde’s plan for 1,000 virtual ward beds under a three-year program starting in 2025 marked the largest single virtual care deployment in Scotland. Scotland’s target of at least 2,000 Hospital at Home beds by the end of 2026 adds a clear policy signal that supports faster platform adoption in community settings. This gives Scotland a sharper profile in home-based digital care, even though England still dominates the national spending base.

Wales and Northern Ireland are smaller digital healthcare segments, but they remain important because each operates through its own health system structure and digital strategy. NHS Wales is building patient-facing digital capability in parallel with England, while Welsh policy places stronger emphasis on community care and local accessibility needs. Northern Ireland’s Health and Social Care system also creates room for cross-border data-sharing opportunities with the Republic of Ireland, which can matter for vendors with interoperability strengths. Across all four nations, MHRA clinical safety expectations and data governance requirements apply consistently, so suppliers still need a common compliance foundation even when procurement paths differ.

Competitive Landscape

The UK digital healthcare market has a mixed competitive structure because acute EPR and primary care systems are concentrated, while AI scribing, remote monitoring, virtual care, and digital therapeutics remain fragmented. In acute EPR, Oracle Health led with a 25% share among NHS trusts in early 2025, while Epic held 9.7%, and System C remained one of the core incumbents. In primary care, EMIS and TPP together covered more than 89% of GP practices, which kept infrastructure-layer competition tight even as newer challengers began to appear. The June 2025 approval of Medicus under NHS England’s Tech Innovation Framework was the first serious attempt to break that longstanding duopoly in a quarter century. This creates a market where a few vendors control the core records layer, while many smaller suppliers compete around workflow, engagement, monitoring, and analytics.

Recent strategy has centered on acquiring installed bases, deepening NHS integration, and building compliant AI capabilities. TPG’s March 2026 acquisition of Optum UK, which owns EMIS Health, showed the value investors place on sticky NHS revenue streams in core systems. Oracle Health’s UK launch of Clinical AI Agent after NHS pilots showed how incumbent EPR providers are using AI to protect and deepen existing trust relationships. Accurx has sustained its advantage in GP communications by enabling write-back into both EMIS Web and SystmOne, while Huma used its Hi Scribe product and Google Cloud partnership to reach 870 UK practices covering 10 million patients. In-home care and remote monitoring, Cera and Doccla have expanded through fundraising, partnerships, and platform rollouts that align closely with virtual ward and community care priorities.

Open space remains strongest in areas where current systems do not yet connect well or where care is shifting away from hospitals. Interoperability middleware between mental health and acute EPRs remains underdeveloped, which leaves room for vendors that can simplify data exchange without large replacement projects. AI-powered care coordination for home care workers is another opening, and Cera’s 2026 AI Lab launch showed one route toward building tools that can be licensed beyond the UK. Pharmaceutical and NHS co-development programs also remain a viable route for suppliers that can support diagnostics, prevention, and real-world evidence generation. At the same time, framework structures such as the Clinical Digital Health Systems program give existing approved suppliers a procurement advantage, which means new entrants still need strong compliance and integration credentials before price alone becomes decisive.

United Kingdom Digital Healthcare Industry Leaders

Accurx

athenahealth

Epic Systems Corporation

Oracle Health

Veradigm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The UK government introduced the NHS Modernisation Bill mandating single patient record sharing across all NHS providers in England, requiring hospitals, GP practices, and community services to make patient health data accessible to authorised clinicians nationally. This legislation, expected to benefit specialties including maternity and frailty from 2027, will structurally reshape data infrastructure requirements for every NHS EPR and interoperability vendor.

- April 2026: Cera launched what it described as the world’s first dedicated AI lab for the care sector, targeting workforce productivity, hospital admission prevention, and global licensing of AI tools. The lab builds on Cera’s partnerships with two-thirds of NHS care regions and more than 100 local governments, providing a deployment network for at-scale AI validation.

- March 2026: US private equity firm TPG closed its acquisition of Optum UK, owner of EMIS Health, completing the transition of the GP IT system covering 55% of English GP practices into private equity ownership. The deal coincided with rising competition from Doctolib’s acquisition of Medicus Health and the emergence of cloud-native GP systems.

- March 2026: University Hospitals of Leicester and University Hospitals of Northamptonshire jointly awarded Accurx a GBP 1.9 million, or USD 2.4 million, four-year contract to deploy Accurx Scribe across 10,000 clinicians and 2.5 million outpatient appointments annually.

United Kingdom Digital Healthcare Market Report Scope

The United Kingdom digital healthcare market refers to the integration of digital technologies such as mobile apps, telehealth, artificial intelligence, and electronic health records into the UK healthcare system. Its primary goal is to improve clinical outcomes, increase access to care, and drive operational efficiencies, largely driven by the publicly funded National Health Service (NHS) and private healthcare providers.

The United Kingdom Digital Healthcare Market is segmented by offering, technology, deployment mode, application, and end user. By offering, it encompasses software, services, and hardware solutions. By technology, the market includes telehealth and telemedicine, remote patient monitoring, mHealth applications, healthcare analytics and AI, digital health systems, and digital therapeutics. By deployment mode, solutions are delivered through cloud‑based, hybrid, and on‑premise models. By application, digital healthcare supports chronic disease management, diagnostics and decision support, mental health, preventive and wellness care, and administration and workflow automation. Finally, by end user, adoption is seen across hospitals and NHS Trusts, primary care and GP practices, patients and home‑care settings, payers and commissioners, and pharmaceutical and life sciences companies.

| Software |

| Services |

| Hardware |

| Telehealth and Telemedicine |

| Remote Patient Monitoring |

| mHealth Applications |

| Healthcare Analytics and AI |

| Digital Health Systems |

| Digital Therapeutics |

| Cloud-Based |

| Hybrid |

| On-Premise |

| Chronic Disease Management |

| Diagnostics and Decision Support |

| Mental Health |

| Preventive and Wellness Care |

| Administration and Workflow Automation |

| Hospitals and NHS Trusts |

| Primary Care and GP Practices |

| Patients and Home-Care Settings |

| Payers and Commissioners |

| Pharmaceutical and Life Sciences Companies |

| By Offering | Software |

| Services | |

| Hardware | |

| By Technology | Telehealth and Telemedicine |

| Remote Patient Monitoring | |

| mHealth Applications | |

| Healthcare Analytics and AI | |

| Digital Health Systems | |

| Digital Therapeutics | |

| By Deployment Mode | Cloud-Based |

| Hybrid | |

| On-Premise | |

| By Application | Chronic Disease Management |

| Diagnostics and Decision Support | |

| Mental Health | |

| Preventive and Wellness Care | |

| Administration and Workflow Automation | |

| By End User | Hospitals and NHS Trusts |

| Primary Care and GP Practices | |

| Patients and Home-Care Settings | |

| Payers and Commissioners | |

| Pharmaceutical and Life Sciences Companies |

Key Questions Answered in the Report

What is the expected value of the UK digital healthcare market by 2031?

The UK digital healthcare market is forecast to reach USD 70.54 billion by 2031, rising from USD 42.93 billion in 2025 at an 8.76% CAGR.

Which product category leads spending in the UK digital healthcare space?

Software leads spending with 59.27% of revenue in 2025, supported by EPR platforms, SaaS clinical tools, and analytics adoption.

Which technology area is growing fastest across the NHS digital ecosystem?

Healthcare analytics and AI is the fastest-growing technology segment, with an 8.98% CAGR through 2031, as trusts expand decision support and workflow automation.

Why are patient and home-care platforms gaining traction in the United Kingdom?

Remote monitoring, virtual wards, and NHS home-care programs are pushing patient and home-care settings to a 10.17% CAGR, helped by programs expected to free 500,000 appointments annually.

What is driving demand for hybrid deployment models in UK healthcare IT?

Hybrid deployment is growing at 9.96% CAGR because many trusts are connecting cloud-native tools to on-premise EPR cores instead of replacing legacy systems in one step.

Which part of healthcare delivery spends the most on digital tools in the UK?

Hospitals and NHS trusts remain the largest end users, accounting for 60.23% of spending in 2025 due to EPR licenses, managed services, and enterprise AI deployments.

Page last updated on: