Value-based Healthcare Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

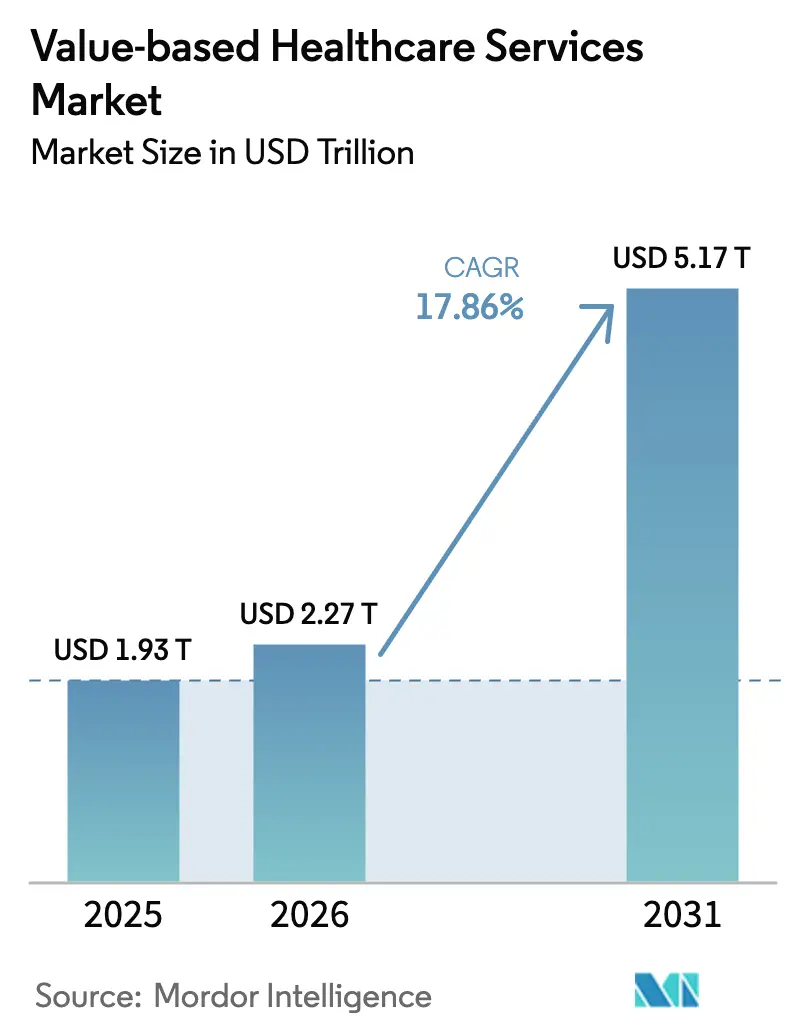

| Market Size (2026) | USD 2.27 Trillion |

| Market Size (2031) | USD 5.17 Trillion |

| Growth Rate (2026 - 2031) | 17.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Value-based Healthcare Services Market Analysis by Mordor Intelligence

Value-based Healthcare Services market size in 2026 is estimated at USD 2.27 trillion, growing from 2025 value of USD 1.93 trillion with 2031 projections showing USD 5.17 trillion, growing at 17.86% CAGR over 2026-2031.

Momentum stems from shifting reimbursement incentives that reward measurable patient outcomes, accelerated enrollment in managed Medicare options, and payer–provider alignment around integrated care delivery. A growing base of seniors managing multiple chronic conditions increases demand for continuous, coordinated services. Simultaneously, employers seek predictable medical spending, encouraging direct contracts anchored in performance guarantees. Technology adoption, notably AI-driven risk stratification, further supports proactive population management while telehealth expands access for dispersed communities. Consolidation among hospital systems and payers underpins investment capacity for analytic infrastructure and downstream care assets, reinforcing transition velocity.

Key Report Takeaways

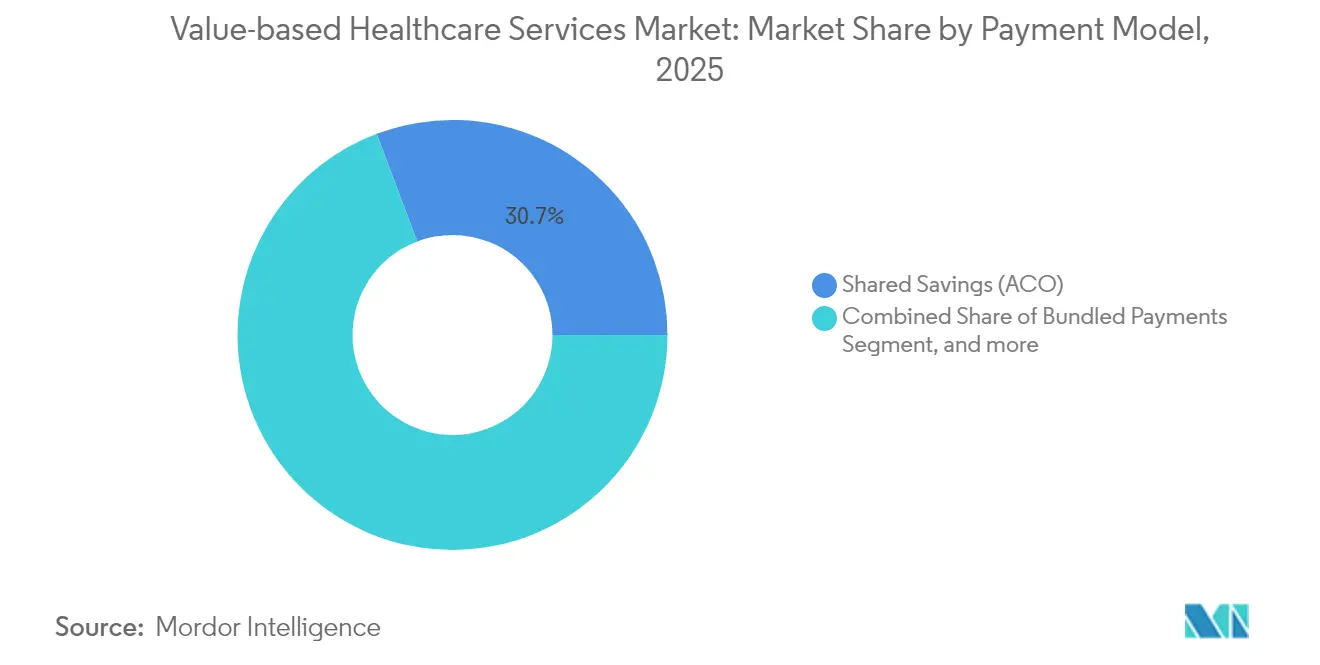

- By payment model, shared savings programs led with 30.74% revenue share in 2025, whereas capitation/global budgets are projected to post the quickest expansion at a 19.02% CAGR through 2031.

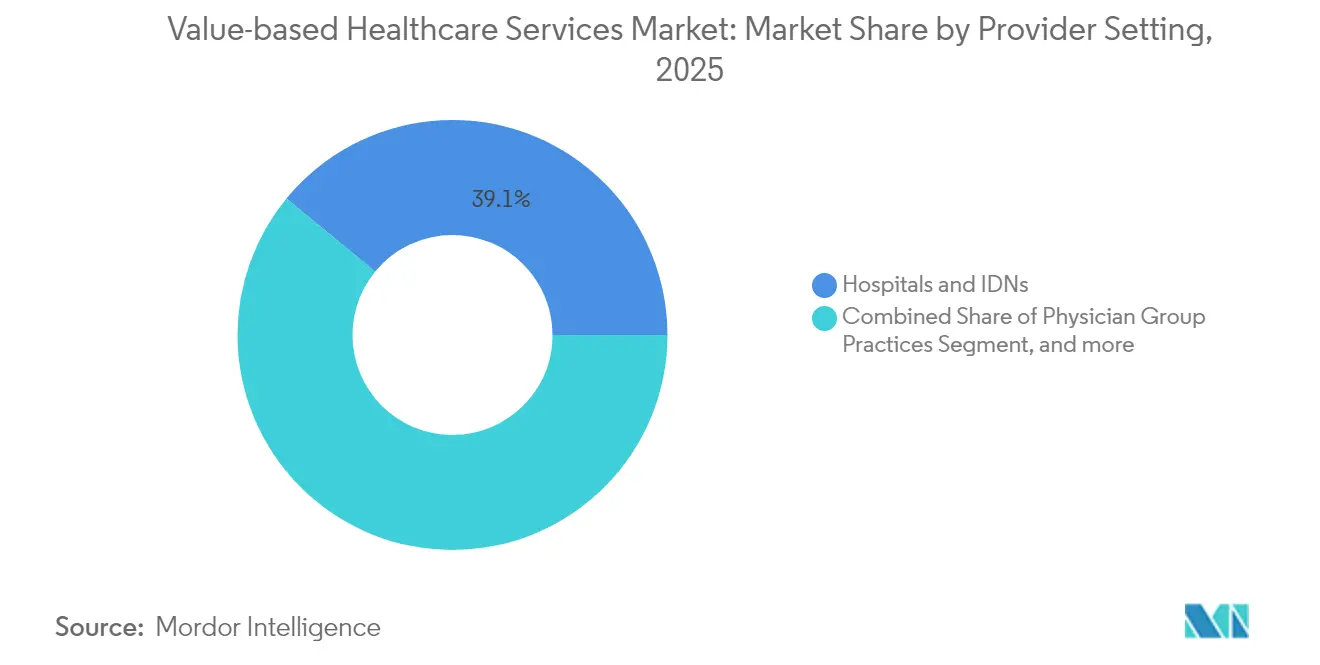

- By provider setting, hospitals and IDNs held 39.05% of the value-based healthcare services market share in 2025; virtual/telehealth providers are on track for a 23.10% CAGR between 2026 and 2031.

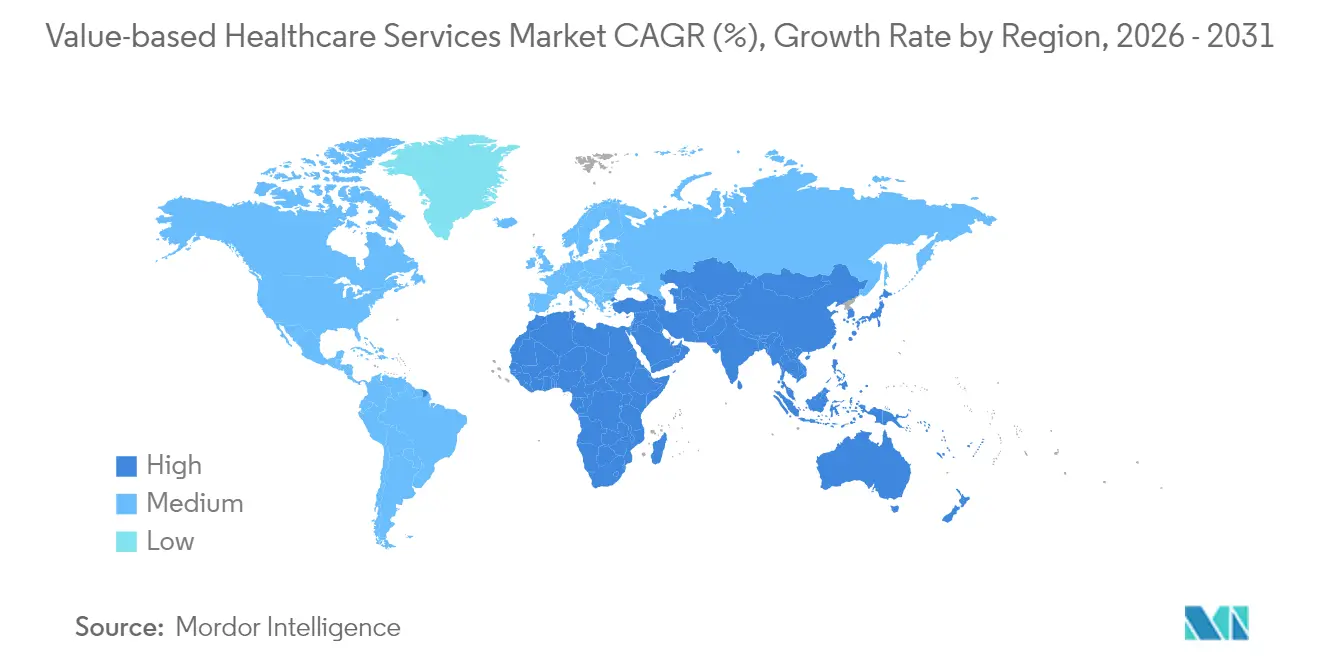

- By geography, North America dominated at 45.90% share during 2025, while Asia Pacific is expected to record a 25.20% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Value-based Healthcare Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases and aging population | +4.2% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Government-led shift toward alternative payment models | +3.8% | North America, expanding to APAC and Europe | Medium term (2-4 years) |

| Payer–provider push for integrated, longitudinal care | +3.1% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Expansion of Medicare Advantage and risk-based ACO programs | +2.9% | North America with spillover elsewhere | Short term (≤ 2 years) |

| AI-enabled risk stratification and predictive analytics | +2.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Employer-funded value-based contracts for cost containment | +1.9% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases & Aging Population

Adults aged 65 and older will number 73 million in the United States by 2030, with 85% living with at least one chronic ailment and 60% managing multiple conditions.[1]Vizient, “Demographic Shifts and Chronic Disease Prevalence,” vizientinc.com This cohort already drives over half of hospital admissions and pushes healthcare costs upward. The value-based healthcare services market incentivizes coordinated management through shared savings arrangements that encourage preventive interventions and reduce avoidable hospitalizations. Providers leverage longitudinal data, home-based monitoring, and multidisciplinary care teams to address complex needs, generating measurable quality gains and cost offsets.

Government-Led Shift Toward Alternative Payment Models

Policy is a decisive catalyst. The CMS Innovation Center has retired programs that failed to save money while rolling out mandatory episode bundles such as the Transforming Episode Accountability Model, which will involve 741 hospitals from January 2026.[2]American Journal of Managed Care Editorial, “CMS TEAM Model Details,” ajmc.com Internationally, nations like the Netherlands have adopted bundled payments that improve care protocol adherence without raising total spend. Such mandates hasten provider migration away from fee-for-service toward risk-bearing arrangements.

Payer-Provider Push for Integrated, Longitudinal Care

Vertically integrated entities now combine insurance, primary care, specialty services, pharmacy, and analytics within one operating platform. Optum already manages 4.7 million patients under value-based contracts, while Kaiser Permanente’s Risant Health adds Geisinger and Cone Health assets to expand its regional footprint.[3]UnitedHealth Group, “Optum Investor Presentation 2025,” unitedhealthgroup.com These structures facilitate real-time data exchange and shared clinical governance, enabling seamless hand-offs across the continuum and aligning incentives around total-cost-of-care metrics.

Expansion of Medicare Advantage & Risk-Based ACO Programs

Medicare Advantage enrollment is projected to reach 35.7 million members in 2025, equaling 51% of all Medicare beneficiaries, while average monthly premiums continue to fall. The Medicare Shared Savings Program delivered USD 2.1 billion in net savings during 2023, proving that upside-and-downside models can balance cost and quality. New policy elements such as Health Equity Benchmark Adjustments aim to widen participation among providers serving historically underserved populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dual revenue-cycle complexity (FFS versus VBC) | -2.1% | Global, acute in transition markets | Medium term (2-4 years) |

| Limited readiness for downside-risk exposure | -1.8% | North America and Europe, emerging in APAC | Short term (≤ 2 years) |

| Interoperability gaps across community-based providers | -1.4% | Global with regional variation | Long term (≥ 4 years) |

| Physician burnout from quality-reporting demands | -1.2% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dual Revenue-Cycle Complexity (FFS vs VBC)

Running parallel billing systems for fee-for-service and value contracts strains finance departments, particularly in smaller organizations lacking enterprise IT resources. Staff must reconcile divergent coding, documentation, and reporting rules, diverting time and increasing administrative overhead. Until a tipping point of revenue shifts under value models, back-office duplication will remain a drag on operational efficiency.

Limited Readiness for Downside-Risk Exposure

Many providers hesitate to accept full capitation because actuarial skills, reserve capital, and population-health infrastructure remain unevenly distributed. Previous instances of inadequate risk adjustment foster distrust among organizations caring for socio-economically complex populations, slowing contract uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Model: Maturation Drives Growth Beyond Shared Savings

Shared savings programs controlled 30.74% of the value-based healthcare services market in 2025, acting as an accessible on-ramp because they initially shield participants from downside exposure. They serve 11 million beneficiaries within Medicare alone and delivered USD 2.1 billion in savings during 2023. The value-based healthcare services market size for capitation/global budgets is forecast to expand at a 19.02% CAGR through 2031 as payers prefer predictable cost envelopes and providers bolster actuarial and care-management capabilities. Bundled Payments gain traction via the mandatory TEAM model covering surgical episodes, while Pay-for-Performance contracts refine quality metrics to include equity components. Patient-Centered Medical Home frameworks increasingly integrate inside broader ACO structures, and episode-based terms now encompass chronic disease cycles, reflecting rising sophistication in defining outcomes. Niche models such as specialty bundles and employer direct contracting add further optionality, illustrating the continuous evolution of payment design in the value-based healthcare services market.

Growing confidence in capitation accelerates investment in care coordination platforms, remote monitoring, and community-based partnerships. Organizations that master population-health analytics can align provider incentives, adjust panel risk, and capture shared savings while maintaining high consumer satisfaction. Those lacking scale gravitate toward collaborative contracting networks that pool actuarial exposure.

By Provider Setting: Digital Expansion Redefines Care Continuum

Hospitals and IDNs held 39.05% of the value-based healthcare services market share in 2025, leveraging integrated specialty lines, tertiary care capacity, and enterprise analytics. They deploy centralized command centers and care-at-home programs that shift lower acuity cases outside inpatient walls, preserving margin under capitated payments. Yet virtual providers represent the fastest-growing cohort, forecast at a 23.10% CAGR to 2031, as asynchronous communication, home diagnostics, and remote patient monitoring fulfill continuous engagement requirements. The value-based healthcare services market size attached to virtual modalities is poised for exponential expansion once tele-enabled episodes become core to official risk arrangements.

Physician group practices remain nimble, adopting niche geriatrics and chronic-disease contracts. Home health agencies benefit from preference for post-acute recovery at lower cost points. Ambulatory surgical centers join bundled payment tracks, and specialty clinics explore organ-specific global budgets, demonstrating the widening ecosystem within the value-based healthcare services market.

Geography Analysis

North America retained 45.90% share in 2025 because Medicare, Medicaid, and employer adoption set mature precedents for outcome-oriented clauses. Federal alignment towards accountable care is slated to place every traditional Medicare beneficiary within a risk-sharing relationship by 2030. Canada pilots province-based outcome incentives and Mexico links public-sector payment to quality metrics.

Asia Pacific exhibits the steepest trajectory at 25.20% CAGR through 2031, underpinned by large-scale public reform and rapid digital uptake. China experiments with bundled oncology payments across tier-one cities, Japan adjusts its fee schedule to reward prevention among seniors, and India’s Ayushman Bharat Digital Mission provides a backbone for claimless electronic reimbursement. Australia’s statewide program demonstrates reductions in hospital length of stay via standardized pathways, signaling regional proof of concept.

Europe maintains steady uptake, led by the Netherlands’ diabetes bundles that unite primary and specialty teams on shared budgets. Germany integrates quality thresholds into hospital financing. The United Kingdom tests population-based payments within Integrated Care Systems. Southern European states pilot outcome contracts in selected regions. Middle East and Africa display nascent initiatives, with Gulf Cooperation Council members investing in digital registries and South Africa’s National Health Insurance Bill incorporating performance clauses. In South America, Brazil’s private insurers adopt capitated oncology products and Argentina trials episode payments in public hospitals.

Competitive Landscape

Market consolidation positions diversified giants and regional systems to capture contracting opportunities. Optum invested USD 31 billion in acquisitions across two years, assembling clinics, technology, and home-health assets that let it control the full care loop. Kaiser Permanente’s Risant Health absorbed Geisinger and Cone Health, transforming disparate community systems into a multi-state platform with USD 3 billion earmarked for capital upgrades. CVS Health’s purchase of Oak Street Health provides 600 primary-care centers geared toward capitated Medicare Advantage risk.

Payers extend influence downstream, while technology specialists embed analytics and engagement tools into provider workflows. Start-ups with AI-powered population-health solutions target predictive coding automation and social determinant flagging. International players scout joint ventures in Asia Pacific, where policy momentum and digital infrastructure present first-mover opportunities in the value-based healthcare services market.

Competitive strategies revolve around building dense physician networks, augmenting virtual capacity, and integrating pharmacy and behavioral services to control total cost of care. Companies employ device-agnostic remote monitoring, patient-reported outcome measures, and closed-loop referral management to ensure accountability. The market rewards those that can align actuarial expertise with consumer-centric service models.

Value-based Healthcare Services Industry Leaders

MVP Health Care

Cigna Healthcare

UnitedHealth Group (Optum)

Humana Inc.

Blue Cross Blue Shield

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sanford Health and Marshfield Clinic Health System completed their merger, creating a USD 10 billion organization with 56 hospitals and 4,500 providers across the Midwest, aimed at enhancing patient-centered care and expanding value-based services in rural communities.

- December 2024: Kaiser Permanente's Risant Health closed its acquisition of Cone Health, adding four acute care hospitals and an accountable care organization serving nearly 200,000 patients, with USD 1 billion in capital committed over five years to support value-based care transition.

- November 2024: Astrana Health announced its acquisition of Prospect Health for USD 745 million, including Prospect Health Plan and several medical groups across multiple states, aimed at enhancing provider networks and improving access to value-based care for approximately 1.7 million members.

- April 2024: Risant Health completed its acquisition of Geisinger Health, marking the first health system to join Kaiser Permanente's value-based care expansion initiative, with at least USD 2 billion allocated for capital improvements and expanded health plan offerings.

Global Value-based Healthcare Services Market Report Scope

Value-based care is a medical services model in which practitioners and providers are paid based on the quality of their care.

The value-based healthcare services market is segmented by models, providers, and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). By models, the market is segmented into bundled payments, pay for performance, patient-centered medical home, shared savings, and other models. By providers, the market is segmented into home health care, hospital therapy, and other providers. The report also covers the market sizes and forecasts for the value-based healthcare services market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Bundled Payments |

| Shared Savings (ACO) |

| Pay-for-Performance |

| Patient-Centred Medical Home (PCMH) |

| Capitation/Global Budgets |

| Episode-based Payments |

| Other Emerging Models |

| Hospitals & IDNs |

| Physician Group Practices |

| Home Health & Post-Acute Care |

| Ambulatory Surgical Centres |

| Virtual/Tele-health Providers |

| Other Provider Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Payment Model | Bundled Payments | |

| Shared Savings (ACO) | ||

| Pay-for-Performance | ||

| Patient-Centred Medical Home (PCMH) | ||

| Capitation/Global Budgets | ||

| Episode-based Payments | ||

| Other Emerging Models | ||

| By Provider Setting | Hospitals & IDNs | |

| Physician Group Practices | ||

| Home Health & Post-Acute Care | ||

| Ambulatory Surgical Centres | ||

| Virtual/Tele-health Providers | ||

| Other Provider Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value-based healthcare services market size?

The value-based healthcare services market size reached USD 2.27 trillion in 2026 and is projected to grow to USD 5.17 trillion by 2031.

Which payment model is largest today?

Shared savings accountable care organization programs hold the leading position with 30.74% revenue share as of 2025.

Which region is expanding fastest?

Asia Pacific shows the highest growth outlook, forecast at a 25.20% CAGR from 2026 to 2031 due to policy reform and digital health investments.

Why are virtual providers gaining traction?

Telehealth platforms support continuous monitoring and lower-cost interactions that align with outcome-based reimbursement, driving a projected 23.10% CAGR for virtual providers.

How does artificial intelligence influence value-based care?

AI enhances risk stratification, enabling earlier interventions that prevent expensive acute episodes and support shared savings performance.

What challenges slow adoption of downside risk contracts?

Providers often lack actuarial expertise and sufficient financial reserves, making them cautious about accepting full capitation until risk adjustment methods mature.

Page last updated on: