Healthcare Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

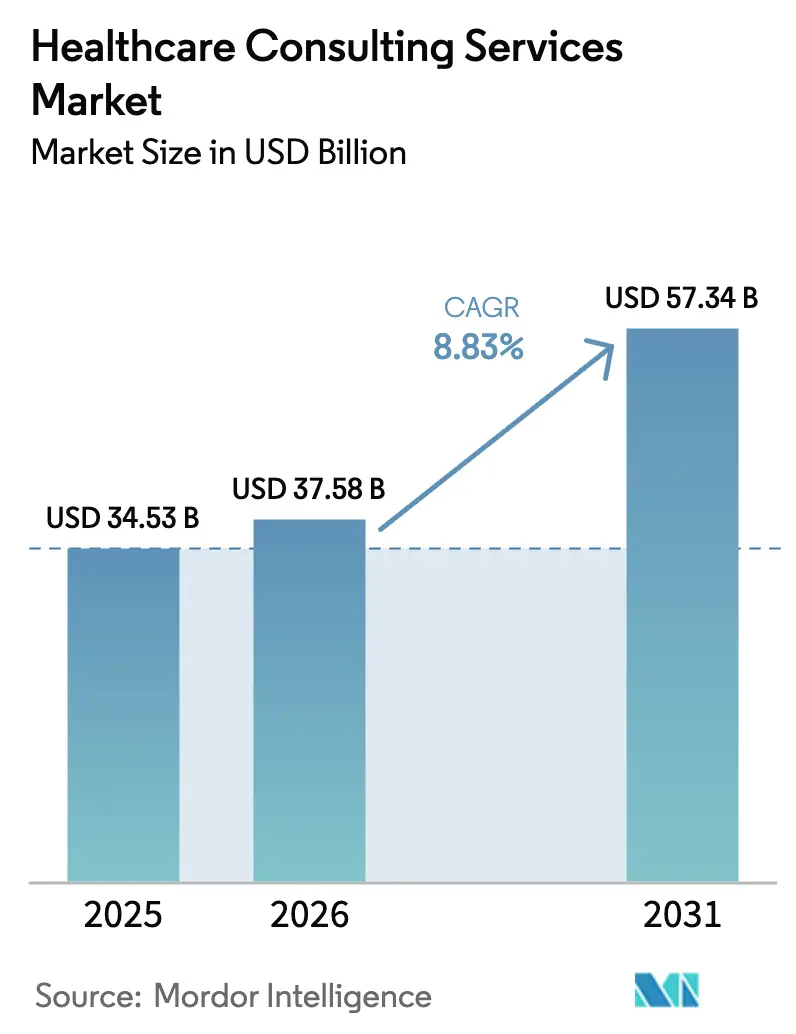

| Market Size (2026) | USD 37.58 Billion |

| Market Size (2031) | USD 57.34 Billion |

| Growth Rate (2026 - 2031) | 8.83% CAGR |

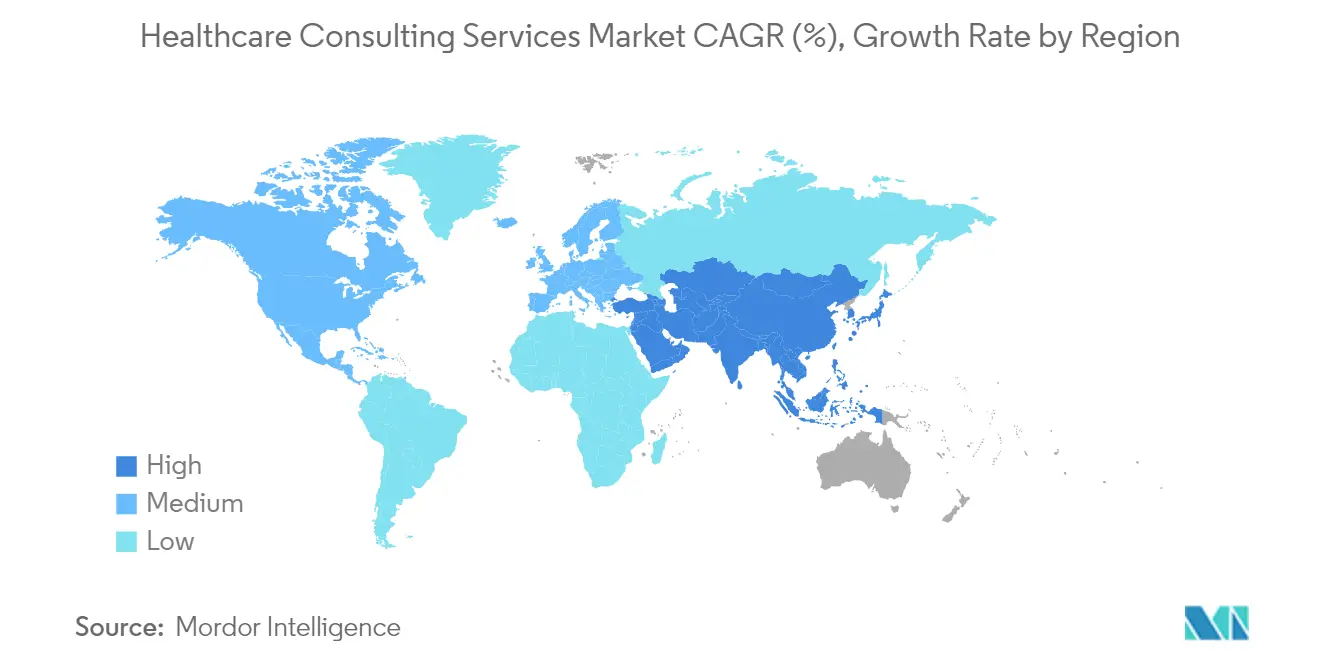

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Consulting Services Market Analysis by Mordor Intelligence

The Healthcare consulting services market size was valued at USD 34.53 billion in 2025 and estimated to grow from USD 37.58 billion in 2026 to reach USD 57.34 billion by 2031, at a CAGR of 8.83% during the forecast period (2026-2031). Growth reflects the sector’s role in guiding healthcare’s digital reinvention, with 90% of C-suite leaders expecting greater reliance on digital tools. Momentum is fuelled by wider adoption of value-based care, escalating cybersecurity threats, and stricter price-transparency rules. North America commands early adoption advantages, whereas Asia-Pacific registers double-digit expansion on the back of demographic ageing and rising private health spend. Demand concentrates on IT consulting for cloud migration, EHR optimisation, and secure device connectivity, while remote delivery models gain traction as clients pursue cost efficiency and ready access to scarce expertise.

Key Report Takeaways

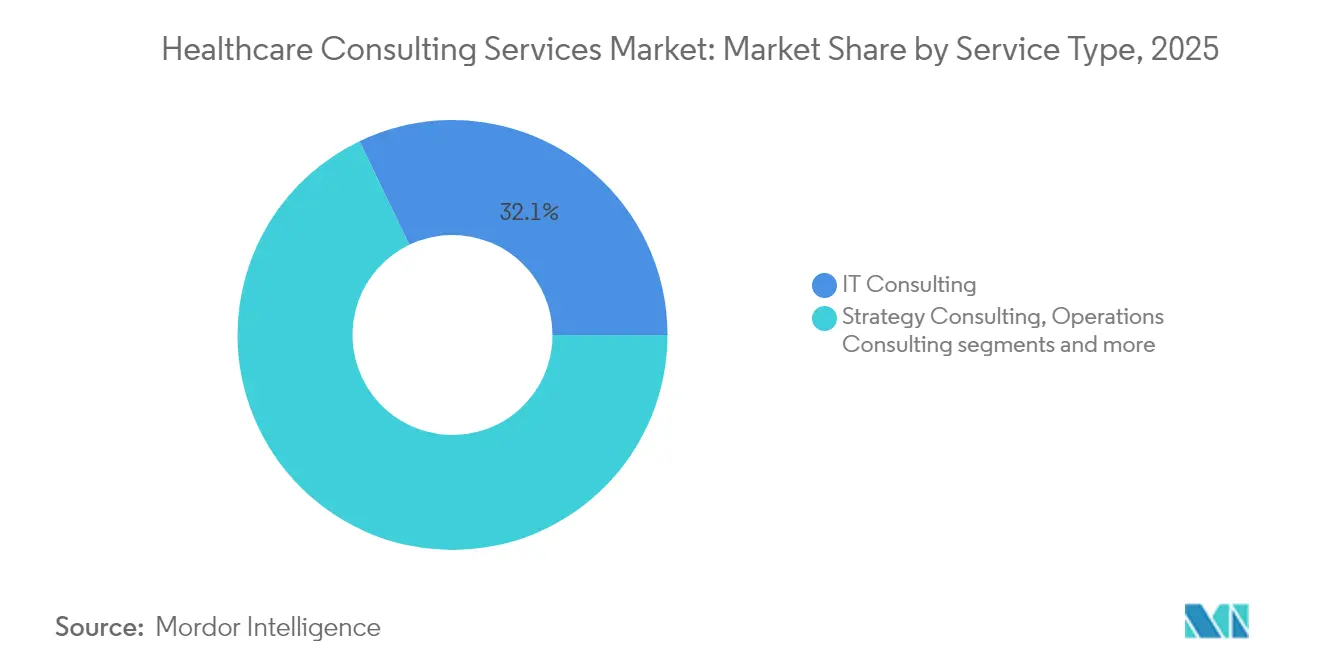

- By service type, IT consulting led with 32.12% revenue share in 2025; digital transformation consulting is forecast to expand at a 10.24% CAGR through 2031.

- By end user, healthcare providers held 46.68% of the Healthcare consulting services market share in 2025, while government agencies are projected to grow at an 11.02% CAGR to 2031.

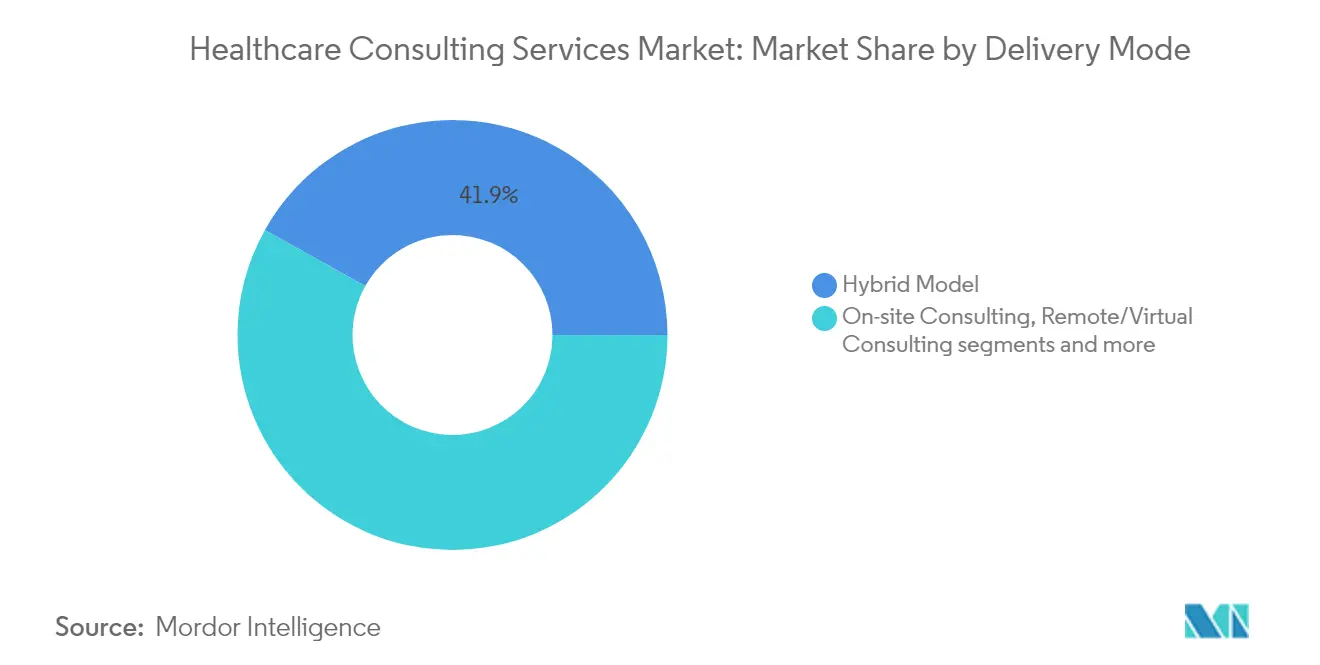

- By delivery model, on-site consulting accounted for 41.87% of the Healthcare consulting services market size in 2025; remote consulting is advancing at a 11.85% CAGR from 2026-2031.

- By geography, North America represented 39.02% of the Healthcare consulting services market size in 2025 and Asia-Pacific is progressing at a 12.55% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated shift to value-based care models | +2.1% | Global, with North America leading adoption | Medium term (2-4 years) |

| Surging demand for digital-first patient engagement platforms | +1.8% | Global, with APAC showing highest growth | Short term (≤ 2 years) |

| Heightened cyber-threat environment driving security consulting | +1.5% | Global, with North America & EU priority focus | Short term (≤ 2 years) |

| Regulatory push for healthcare price-transparency compliance | +1.2% | North America primary, EU emerging | Medium term (2-4 years) |

| Generative-AI advisory for clinical decision support | +0.9% | Global, with developed markets leading | Long term (≥ 4 years) |

| Climate-resilience planning for hospital infrastructure | +0.7% | Global, with EU and North America emphasis | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Value-Based Care Models

Advanced Alternative Payment Models are steering providers toward risk-based reimbursement, with 90 million lives expected in value-based arrangements by 2027. Consultants supply analytics, contract design, and patient-engagement workflows that undergird the shift. Engagement intensity is strongest in the United States, yet private insurers across urban Asia adopt similar schemes. As blended payment structures evolve, external expertise remains vital to balance clinical performance with financial sustainability.

Surging Demand for Digital-First Patient Engagement Platforms

Eighty-eight percent of health systems rank virtual and connected care among their 2025 priorities. Projects encompass omnichannel communication, AI chatbots, and wearable integration to meet consumer expectations for convenience. Advisory needs centre on workflow redesign, cloud enablement, and reimbursement alignment to translate engagement gains into measurable outcomes.

Heightened Cyber-Threat Environment Driving Security Consulting

Eighty-seven percent of executives cite cyber-risk escalation as a leading challenge for 2025 beckershospitalreview.com. Legacy infrastructure and IoT devices expose sensitive data to ransomware. Consulting scopes cover zero-trust architectures and HIPAA-aligned incident response. Regulatory scrutiny in the United States and Europe intensifies focus on breach-reporting readiness, spurring continuous investment in specialist security support.

Regulatory Push for Healthcare Price-Transparency Compliance

The Hospital Price Transparency Rule obliges US hospitals to disclose standard charges via machine-readable files; enhanced elements became mandatory in July 2024[1]Source: U.S. Department of Health & Human Services, “Hospital Price Transparency Rule,” hhs.gov . Roughly 30% of facilities entered 2025 non-compliant, creating advisory openings in data normalisation, consumer-friendly displays, and internal governance. Health systems increasingly regard compliance as a competitive signal of value, bolstering consulting demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage & soaring bill-rates | -1.9% | Global, with North America & EU most affected | Short term (≤ 2 years) |

| Prolonged provider margin squeeze curbing discretionary spend | -1.4% | Global, with rural and mid-size providers priority | Medium term (2-4 years) |

| Data-ownership disputes in multi-party analytics ecosystems | -0.8% | Global, with North America & EU leading adoption | Medium term (2-4 years) |

| Rising carbon-footprint scrutiny of consultants' travel | -0.5% | Global, with EU and North America emphasis | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage & Soaring Bill-Rates

A 10 million-person global health-worker shortfall looms by 2030, while wages are climbing 6.1% annually. Consulting firms face elevated attrition and premium salary demands for staff with both clinical and tech fluency, constraining project capacity and pushing day-rates higher.

Prolonged Provider Margin Squeeze Curbing Discretionary Spend

Twenty-seven percent of US health systems failed to meet operating-margin targets in 2024 as inflation and labor costs outpaced reimbursement [2]Source: American Hospital Association, “Financial and Workforce Pressures on Hospitals,” aha.org . Rural and community hospitals defer non-essential transformation projects, trimming discretionary consulting budgets. Consolidation continues as facilities seek scale efficiencies, potentially reducing the absolute number of buyers in the healthcare consulting market. Expectations for a 7% EBITDA CAGR through 2027 signal medium-term recovery, yet near-term caution persists as boards prioritize capital allocation to core service delivery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: IT Consulting Maintains Lead in Digital Modernisation

IT consulting captured 32.12% of 2025 revenue within the Healthcare consulting services market. Engagements cover EHR optimisation, cloud migration, cybersecurity fortification, and AI deployment. Digital transformation consulting, although smaller, is scaling at a 10.24% CAGR to 2031 as health systems pilot generative-AI scribes, virtual nursing, and automated coding solutions. Strategy and operations work continues through merger integration and throughput improvement mandates. Financial advisory projects focus on transparency rules, while HR & talent engagements rise amid clinician-burnout challenges.

The service mix shows health-system preference for integrated engagements that blend technology, clinical workflow, and financial risk. Consultants offering platform-based accelerators shorten implementation cycles, underpinning sustained expansion of the Healthcare consulting services market.

By End User: Providers Dominate While Government Spend Accelerates

Healthcare providers controlled 46.68% of 2025 spend, confirming their primacy in the Healthcare consulting services market share. Projects range from workforce optimisation to revenue-cycle overhaul. Government agencies form the briskest growth segment at 11.02% CAGR, propelled by federal digital programmes and cybersecurity mandates. Large NIH, CMS, and VA contracts amplify volume. Payers commission advisory work for claims automation and value-based architecture, whereas life-sciences companies focus on regulatory compliance and decentralised trials.

MedTech startups rely on boutique consultancies for market access and device approval. The broad end-user mix buffers the Healthcare consulting services market against sector-specific slowdowns

By Delivery Model: Virtual Engagement Gains Momentum

On-site engagements held 41.87% of 2025 revenue, reflecting the hands-on nature of clinical redesign. Virtual consulting, however, records a 11.85% CAGR to 2031 as collaboration platforms mature. Clients realise travel-cost savings and access specialised skills regardless of geography. Hybrid approaches—combining periodic in-person workshops with always-on remote support—dominate multi-year transformations, reinforcing flexibility in the Healthcare consulting services market

Geography Analysis

North America retained 39.02% of 2025 revenue, giving the region the largest Healthcare consulting services market size, driven by complex reimbursement frameworks and strong AI, telehealth, and cybersecurity spending. Consolidation among hospital networks, Medicare Advantage expansion, and price-transparency mandates sustain advisory demand. Canada invests in provincial EHR upgrades, whereas Mexico’s private-hospital construction lifts operational-consulting volumes.

Asia-Pacific shows the quickest ascent with a 12.55% CAGR through 2031, underpinned by ageing populations and rising disposable income. China funds digital-hospital pilots, India expands Ayushman Bharat coverage, and Japan advances robotics for elder care. ASEAN markets address physician shortages via tele-ICU roll-outs, generating fresh advisory work. Private-equity attention boosts transaction-support engagements, embedding long-term growth into the Healthcare consulting services market.

Europe remains steady amid workforce gaps estimated at 1 million clinicians. Germany drives projects linked to hospital-finance reform and data interoperability, the United Kingdom escalates NHS digitisation, and France extends telemedicine into rural regions. EU-wide data-governance rules underpin compliance consulting. South America and the Middle East & Africa stay emerging yet promising: Brazil facilitates private-insurance expansion, while Gulf states commission smart-hospital campuses requiring imported expertise

Competitive Landscape

The Healthcare consulting services market is moderately fragmented. Global multi-practice firms—Accenture, PwC, KPMG, and EY—deploy cross-sector toolkits but face mounting competition from specialised advisories such as Huron and Chartis. Consolidation persists: Blackstone’s 2024 majority stake in Chartis and Huron’s 2025 Eclipse Insights purchase expand capability breadth. Technology remains the prime differentiator; Accenture’s cloud partnerships with hyperscalers simplify migration, whereas Optum leverages claims datasets to embed advanced analytics.

Boutiques win assignments through deep clinical focus in oncology, cardiovascular care, and behavioural health. Digital natives offer AI-powered benchmarking and outcome-based pricing, resonating with cost-constrained providers. Talent acquisition is fierce as firms vie for data-science skillsets, catalysing partnerships with academic centres. White-space opportunities in climate-resilience planning and health-equity analytics invite new entrants, ensuring brisk competitive evolution within the Healthcare consulting services market.

Healthcare Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

McKinsey and Company

Cognizant

Ernst and Young

The Boston Consulting Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Huron Consulting Group acquired Eclipse Insights to enhance revenue-cycle optimisation capabilities

- June 2025: Net Health purchased Limber Health, adding outpatient EHR workflow tools

- April 2025: Centauri Health Solutions bought MedAllies, bolstering health-information exchange services

Global Healthcare Consulting Services Market Report Scope

As per the scope of this report, healthcare consultancy service providers advise government bodies, hospitals, life science companies, research institutes, and insurance companies about business strategies. Financial consulting, strategy consulting, digital consulting, and operations consultancy are the key areas where biotechnology, pharmaceutical, and medical device companies and hospitals ask for assistance. Healthcare consultancy firms examine the organization's profit-loss ratio, efficiency, and structure and then offer their industry analysis and suggestions for improvement.

The healthcare consulting services market is segmented by service type, component, application, end user, and geography. By service type, the market is segmented into digital consulting and IT consulting. By component type, the market is segmented into services and solutions. By application type, the market is segmented into financial, operations management, and population health. By end user, the market is segmented into hospitals, clinics, and life science companies. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.

| IT Consulting |

| Strategy Consulting |

| Operations Consulting |

| Digital Transformation Consulting |

| Financial Consulting |

| HR & Talent Consulting |

| Healthcare Providers |

| Healthcare Payers |

| Life Sciences Companies |

| Government Agencies |

| Healthcare IT Vendors |

| MedTech Start-ups |

| On-site Consulting |

| Remote / Virtual Consulting |

| Hybrid Model |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | IT Consulting | |

| Strategy Consulting | ||

| Operations Consulting | ||

| Digital Transformation Consulting | ||

| Financial Consulting | ||

| HR & Talent Consulting | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Life Sciences Companies | ||

| Government Agencies | ||

| Healthcare IT Vendors | ||

| MedTech Start-ups | ||

| By Delivery Model | On-site Consulting | |

| Remote / Virtual Consulting | ||

| Hybrid Model | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Healthcare consulting services market?

The market stands at USD 37.58 billion in 2026 and is forecast to reach USD 57.34 billion by 2031.

Which service category leads revenue contribution?

IT consulting generates the largest share at 32.12% of 2025 revenue.

Which region is expanding the fastest?

Asia-Pacific advances at a 12.55% CAGR through 2031.

Why is virtual consulting growing quickly?

Remote models cut travel expenses and widen access to niche expertise, supporting a 11.85% CAGR.

Page last updated on: