Private Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

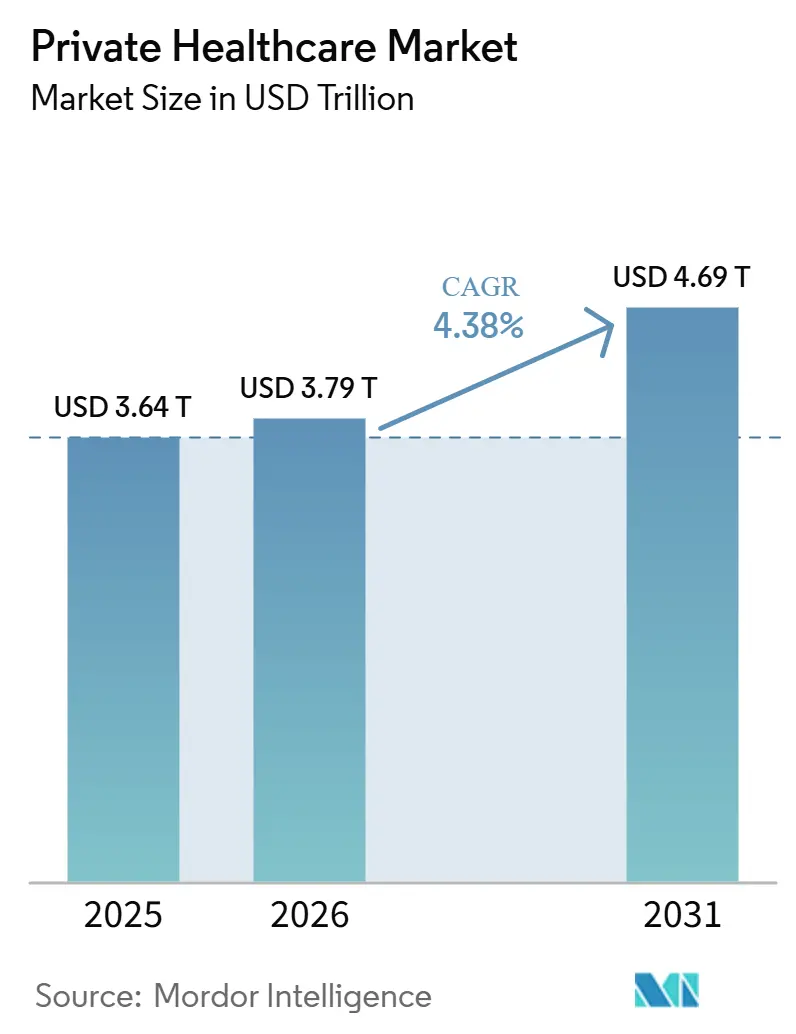

| Market Size (2026) | USD 3.79 Trillion |

| Market Size (2031) | USD 4.69 Trillion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

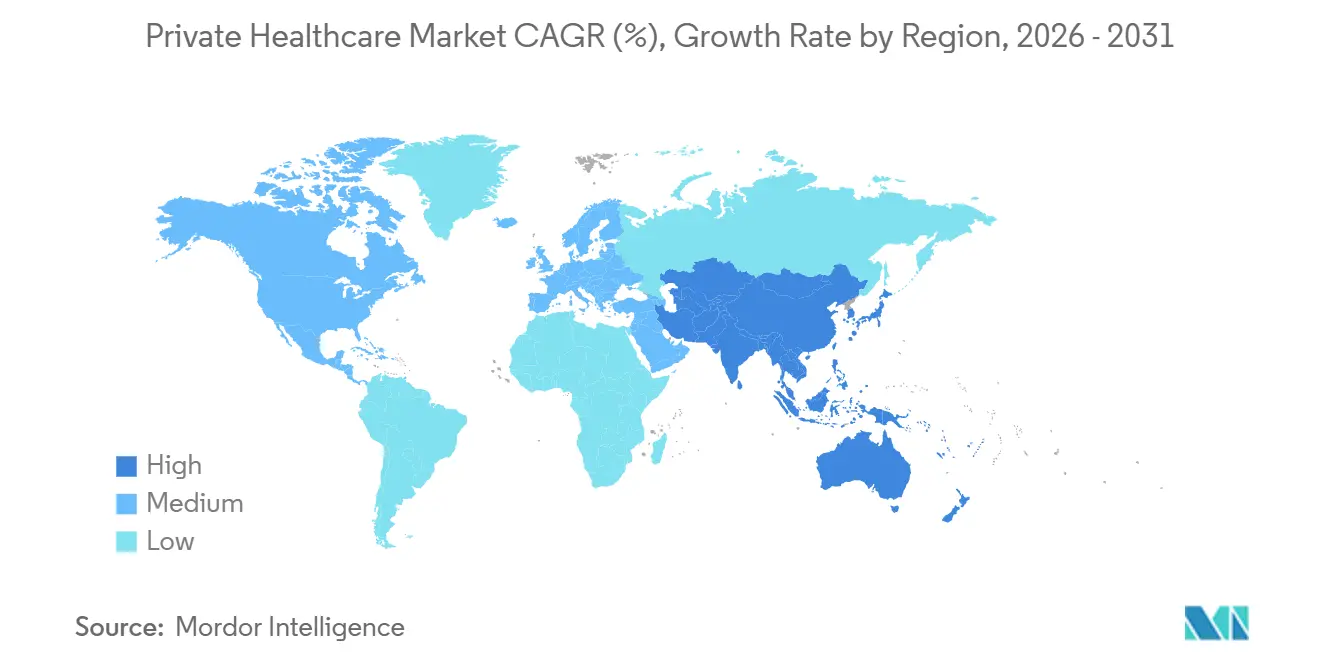

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

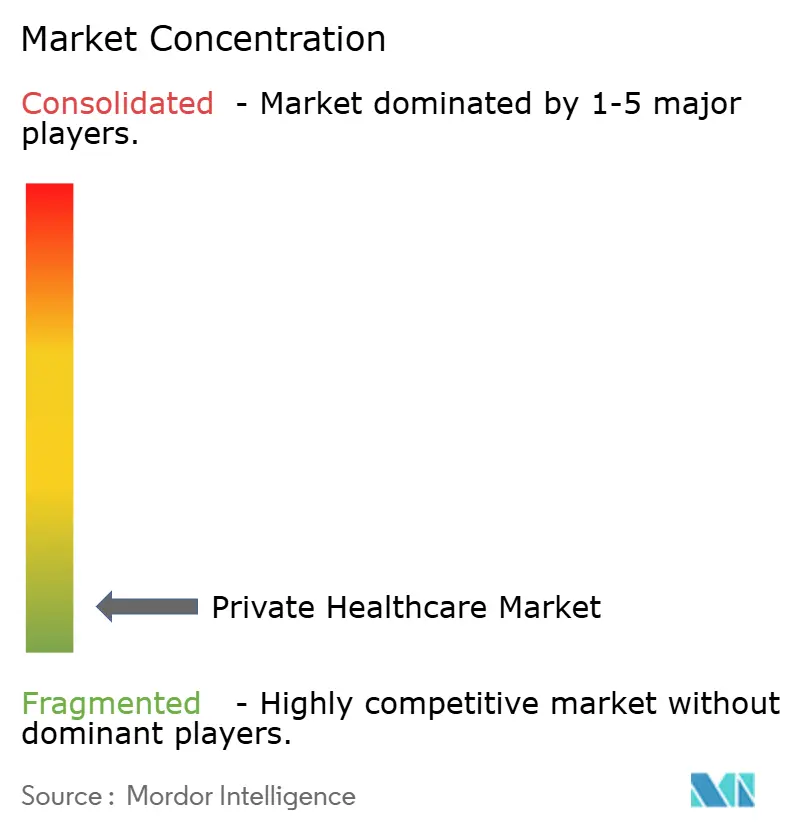

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Private Healthcare Market Analysis by Mordor Intelligence

The Private Healthcare Market size is projected to expand from USD 3.64 trillion in 2025 and USD 3.79 trillion in 2026 to USD 4.69 trillion by 2031, registering a CAGR of 4.38% between 2026 to 2031.

Growth is being supported by rising demand for quicker access to surgery, diagnostics, and specialist consultations when public systems cannot respond at the same pace. Chronic disease treatment is also pushing more patients toward private oncology, cardiology, and neurology pathways because these cases need repeat visits, faster diagnosis, and more coordinated follow-up care. Employer-sponsored coverage is expanding the addressable patient base, and this is reinforcing insured demand across both mature and upper-middle-income economies. Large operators are responding by adding outpatient sites, tightening referral pathways, and shifting capital toward higher-acuity ambulatory care, where patient conversion is faster, and asset productivity is stronger. Competition remains dispersed at the global level, but the regional scale is increasing through expansion, leases, and portfolio transactions that free up capital for further clinical investment.

Key Report Takeaways

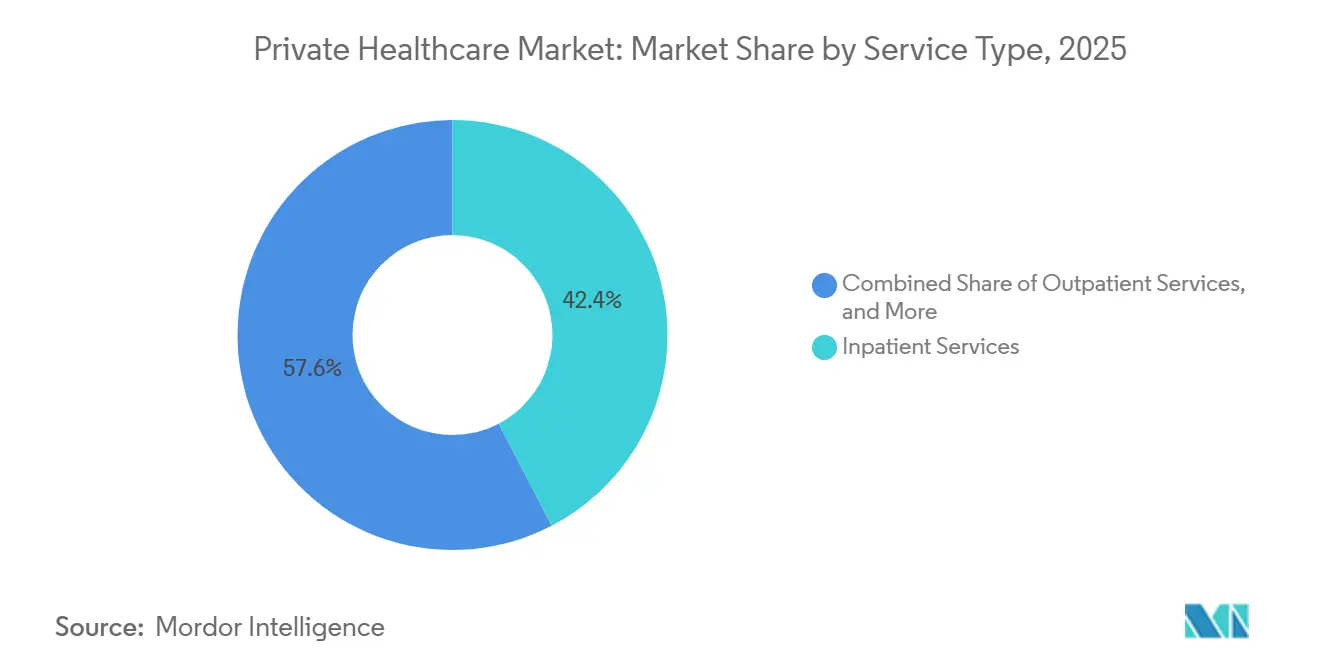

- By service type, inpatient services held 42.36% of the private healthcare market size in 2025, while outpatient services are forecast to expand at a 4.98% CAGR through 2031.

- By healthcare facility, private hospitals held 53.68% of the private healthcare market share in 2025, while specialty hospitals are projected to grow at a 5.63% CAGR through 2031.

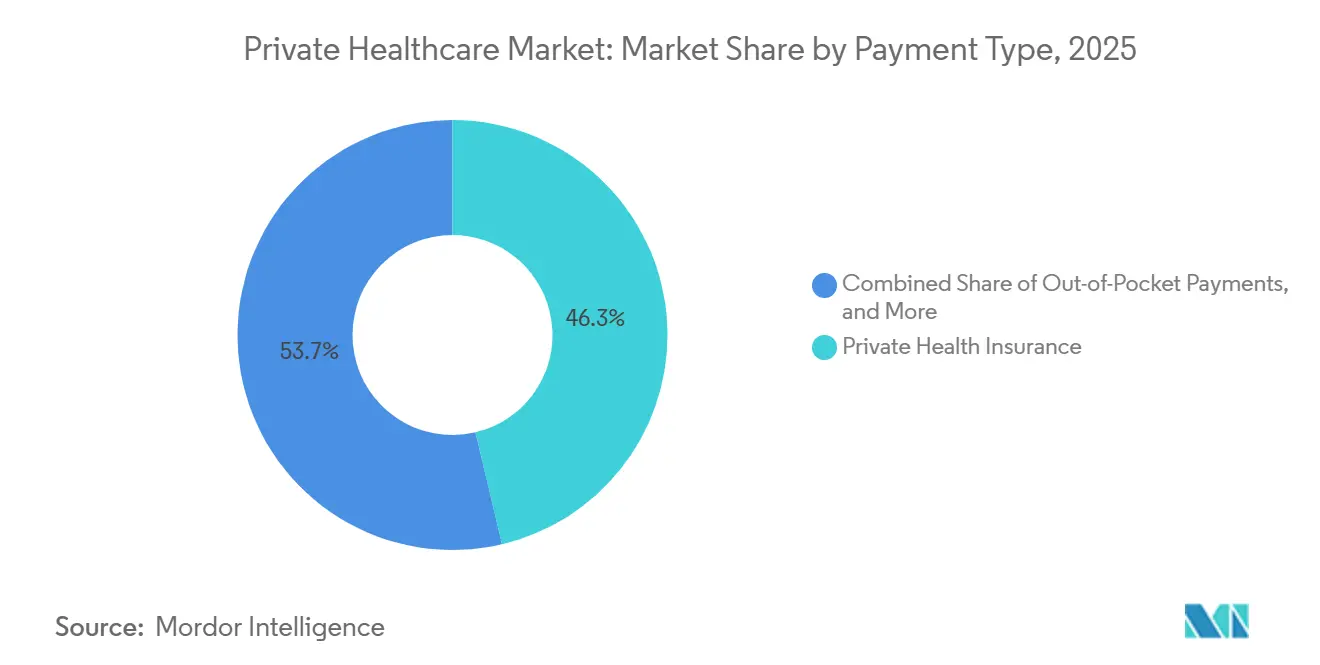

- By payment type, private health insurance accounted for 46.31% of the market in 2025, while out-of-pocket payments are expected to rise at a 6.22% CAGR through 2031 in the private healthcare market.

- By specialty, general medicine captured 28.41% of the market in 2025, while oncology is set to grow at a 6.89% CAGR through 2031.

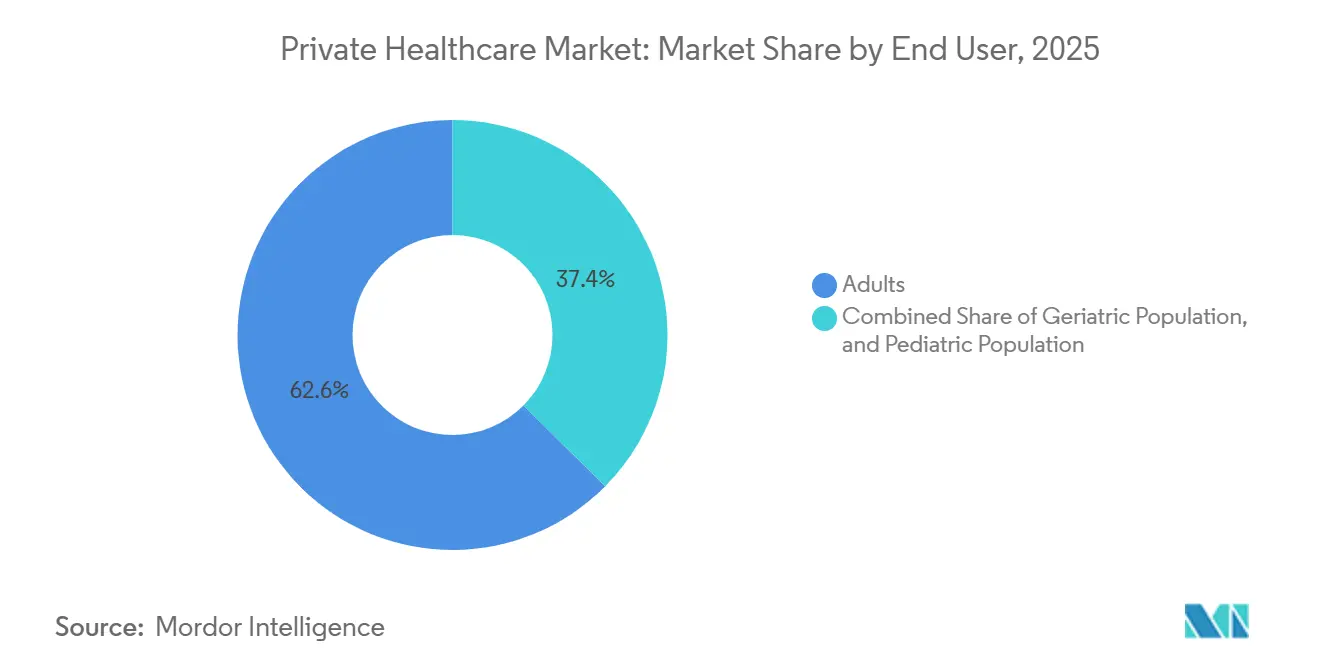

- By end user, adults represented 62.57% of the market in 2025, while the geriatric segment is forecast to expand at a 7.41% CAGR through 2031.

- By geography, North America commanded 38.24% of the private healthcare market share in 2025, whereas Asia-Pacific is projected to expand at a 8.79% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Private Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Faster, Higher-Acuity Care Access | +1.1% | Global, concentrated in North America, UK, GCC | Short term (≤ 2 years) |

| Employer-Led Private Medical Insurance Expansion | +0.9% | North America, Western Europe, GCC, spill-over to APAC | Medium term (2-4 years) |

| Rising Chronic Disease Load and Elective Backlog Migration | +0.8% | Global, strongest in India, UK, Brazil, South Africa | Long term (≥ 4 years) |

| Capacity Expansion through Private Equity and Asset-Light Hospital Models | +0.6% | India, APAC, GCC, South America | Medium term (2-4 years) |

| Digitally Enabled Diagnostics, Triage, and Appointment Conversion | +0.4% | Global, accelerated in UAE, India, Southeast Asia, UK | Short term (≤ 2 years) |

| Rising Demand for Private-Day Surgery and Short-Stay Care | +0.4% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Faster, Higher-Acuity Care Access

Patients are moving toward private care when they believe speed matters as much as treatment quality. This is especially visible in procedures, imaging, and specialist consultations where waiting can worsen outcomes or delay recovery. Operators are adjusting quickly by adding ambulatory sites that can handle more referrals outside large hospital campuses. HCA Healthcare added nearly 100 outpatient facilities in 2025 and now enters 2026 with additional expansion capital in place, which shows that provider networks are being built around access and convenience as much as around bed capacity. The private healthcare market is benefiting because faster access improves patient conversion, repeat utilization, and payer confidence in private pathways. Providers that combine clinical depth with scheduling tools and broad outpatient footprints are in a stronger position to capture this demand than operators that rely only on large inpatient assets.

Employer-Led Private Medical Insurance Expansion

Employer-backed health coverage is becoming a more important route into the private healthcare market because companies are using medical benefits to improve retention and workforce stability. UnitedHealthcare’s 2026 Health Trends Report said medical trend is expected to grow 8.5%, while pharmacy costs rose 11% in 2025, which is pushing large employers to review care access, provider choice, and direct contracting more closely. In Germany, private health coverage reached nearly 41 million in 2025, up by 0.9 million, which points to continued uptake despite a higher-cost operating setting.[1]“PKV Bleibt Stabilitätsanker Im Demografischen Wandel,” In Colombia, voluntary private health plans reached COP 14.65 trillion, equal to USD 3.49 billion, in 2025 and grew 13.2%, which shows that supplementary private coverage is gaining traction beyond high-income countries. This pattern supports stronger insured volumes, a broader payer mix, and a more stable revenue base for private operators. It also favors providers that can serve employer contracts, insurers, and self-pay patients without relying too heavily on one funding source.

Rising Chronic Disease Load And Elective Backlog Migration

Chronic disease is increasing the amount of complex care that flows into the private healthcare market. Business Group on Health identified cancer as the top employer health cost driver in the United States for the fourth straight year in 2025, which underlines how large oncology demand has become in funded care systems.[2]“Manipal Health Expands Bengaluru Presence Adds 245 Lakh Sq Ft in Yelahanka at 816 Crore Long-Term Deal,” These cases are important because they usually need diagnostics, surgery, infusion, follow-up visits, and other specialist services over a longer treatment cycle. In Brazil, the private oncology segment generates BRL 100 billion, equal to USD 18.5 billion, each year, and is projected to reach BRL 210 billion, equal to USD 38.9 billion, by 2030 as aging and treatment intensity increase. The private healthcare market is therefore not only getting more patient volume, but it is also getting a higher share of revenue-rich, specialty-led care episodes. That supports continued investment in oncology, cardiac care, neurology, and integrated diagnostics, where private providers can offer faster treatment pathways.

Capacity Expansion Through Private Equity And Asset-Light Hospital Models

Capital is becoming more flexible across the private healthcare market, and this is helping operators expand without carrying all property costs on their own balance sheets. Asset-light structures such as long leases, management contracts, and sale-leaseback arrangements let providers open or upgrade facilities while preserving cash for medical equipment, specialist hiring, and digital systems. Manipal Health’s long-term lease for a 245,000 sq ft facility in Bengaluru shows how hospital groups are using real estate structures to widen their reach in large urban catchments. Blue Owl Capital’s acquisition of a portfolio of 12 Spire Healthcare hospitals in the UK through a sale-leaseback structure shows the same logic at portfolio scale, with the transaction releasing capital for clinical reinvestment while preserving operating continuity. This approach helps private operators enter growth corridors faster and gives investors access to long-duration healthcare assets. It also encourages consolidation because expansion can happen through transactions and partnerships rather than only through new hospital construction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Cost Across Fragmented Clinical Systems | -1.8% | Global, acute in North America | Short term (≤ 2 years) |

| Data Privacy, Consent Management, and Cybersecurity Exposure | -1.4% | Global | Medium term (2–4 years) |

| Workflow Adoption Resistance Among Clinicians and Front-Desk Staff | -1.0% | Global | Medium term (2–4 years) |

| Limited ROI Visibility for Smaller Provider Organizations | -0.7% | North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Affordability Pressure

Out-of-pocket dependence continues to limit how fast the private healthcare market can grow in many emerging economies. When self-pay remains the main route into care, providers face a ceiling because tariff increases can quickly reduce procedure volumes. This effect is visible even in established private systems when medical scheme pressure or household budget stress reduces treatment uptake. Life Healthcare reported that paid patient days declined 0.4% in the six months to March 2026, which shows how financial strain can affect utilization even when broader revenue remains resilient.[3]“Life Healthcare to Add More Beds at Hospitals and Recruit 140 Specialists,” The private healthcare market, therefore, gains from self-pay demand, but it also remains exposed when affordability weakens, or patients delay non-urgent procedures. Providers that add installment options, clear price communication, and simpler digital cost estimates are better placed to protect volumes in this environment.

Licensing, Reimbursement, And Medical Staff Constraint Complexity

Regulation and staffing costs are slowing parts of the private healthcare market, even where patient demand remains healthy. Tariff updates do not always keep pace with inflation, and this weakens profitability on funded procedures. In the UK, Spire Healthcare said the proposed NHS annual tariff uplift for 2026-27 was well below prevailing inflation, which increases pressure on private operators handling publicly commissioned activity.[4]“UK Private Hospital Provider Spire in Talks on Sale to Private Equity,” Staffing adds a second layer of pressure because specialist shortages raise recruitment costs, training requirements, and the time needed to activate new beds. Life Healthcare is recruiting 140 specialists in FY2026 while also expanding acute and rehabilitation bed capacity, which shows how labor availability can become a real operating bottleneck. Compliance standards still improve care quality, but they also increase the cost and complexity of scaling hospital networks across multiple jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Outpatient Migration Redefines Revenue Architecture

Inpatient services held 42.36% of the private healthcare market size in 2025, which kept this segment in the lead because surgery, multi-specialty admissions, and intensive care still depend on hospital-based delivery. These services remain central to revenue because complex procedures carry larger bills and use more specialist resources per episode. At the same time, the private healthcare market is seeing a clear shift in where many procedures are being delivered. Outpatient services are forecast to grow at a 4.98% CAGR through 2031 as minimally invasive techniques and payer cost pressure keep moving cases away from full inpatient admission.

This migration is no longer limited to low-acuity care, because a larger share of procedural work is now being organized through ambulatory settings. U.S. ambulatory surgery center revenue reached an estimated USD 45.6 billion in late 2025, and more than 80% of surgeries were performed in outpatient settings, which shows how strong the site-of-care shift has become. Tenet Healthcare’s USPI division operated 556 ambulatory surgery centers in 2025 and invested USD 125 million in Q1 2026 to acquire 7 more centers, reinforcing the view that outpatient expansion is a major capital priority. This does not reduce the role of inpatient care, but it does change the revenue mix of the private healthcare industry by directing more profitable, shorter-stay episodes toward lower-cost settings. Emergency care remains the smallest and most operationally demanding service category because it requires round-the-clock staffing, faster triage, and closer regulatory oversight.

By Healthcare Facility: Specialty Hospitals Capitalize On Complexity Premium

Private hospitals accounted for 53.68% of the private healthcare market share in 2025, which reflects their central role in general acute care, inpatient surgery, and insured referral networks. Large hospitals still anchor most private systems because they can offer broad service lines, advanced operating theaters, and stronger payer contracting leverage. This gives them a durable position in markets where care pathways still begin with physician referral and move through high-acuity hospital settings. However, specialty hospitals are projected to expand at a 5.63% CAGR through 2031, which makes them the fastest-growing facility type in the private healthcare market.

The reason is straightforward, because specialty centers can focus on higher-value clinical pathways such as oncology, cardiology, and orthopedics while building deeper physician alignment. Apollo Hospitals reported in May 2026 that it commissioned 4 new hospitals, adding 855 beds, and still had a capex pipeline of INR 5,100 crore, equal to USD 608 million, which signals continued investment in scaled private capacity. Life Healthcare also confirmed plans in FY2026 to add acute and rehabilitation beds plus new catheterization and vascular laboratory capacity, which points to ongoing investment in focused clinical infrastructure. Day hospitals, urgent care centers, and rehabilitation facilities are also gaining relevance because they help large groups reduce emergency room pressure and extend care beyond the main campus. The private healthcare market is therefore moving toward a layered facility model where general hospitals provide scale, while specialty and short-stay sites support margin quality and referral depth.

By Payment Type: OOP Growth Signals Coverage Gap Opportunity

Private health insurance commanded 46.31% of the private healthcare market size in 2025, making it the largest funding route across the sector. Insurance remains the backbone of organized private demand because it improves affordability, steadies cash flow, and supports broader use of specialist and elective services. This is especially important in higher-cost procedures where individuals often defer treatment without some form of risk pooling. The private healthcare market also benefits when insurers and employers steer patients toward curated provider networks with better speed and lower downstream claims costs.

Employer-backed insurance growth continues to support this segment. UnitedHealthcare’s 2026 Health Trends Report showed that medical and pharmacy cost pressure is prompting employers to rethink how care is purchased, which strengthens the role of managed private access. Germany’s private coverage base reached nearly 41 million in 2025, which confirms that insured participation continued to expand even in a mature market. At the same time, out-of-pocket payments are forecast to grow at a 6.22% CAGR through 2031, showing that the private healthcare market is also growing in places where formal insurance still has gaps. Colombia’s voluntary private health plans rose 13.2% to COP 14.65 trillion, equal to USD 3.49 billion, in 2025, which illustrates how supplementary coverage and self-pay demand can deepen together. This mix creates opportunity, but it also means providers must balance tariff discipline, insurance relationships, and transparent self-pay pricing more carefully.

By Specialty: Oncology Anchors Next Growth Phase

General medicine held 28.41% of the market in 2025, which reflects its role as the main access point into the broader private healthcare market. It remains important because it captures routine consultations, referral traffic, repeat visits, and the first stage of diagnosis for many chronic conditions. Yet the strongest expansion is happening in higher-acuity specialties where speed, continuity, and clinical coordination matter more. Oncology is projected to grow at a 6.89% CAGR through 2031, which makes it the fastest-growing specialty segment.

Cancer care is expanding because treatment pathways are longer and more resource-intensive than most general medicine episodes. Business Group on Health said cancer remained the largest employer health cost driver in the United States in 2025, which reflects how deeply it is shaping care utilization and insurance spending. In Brazil, the private oncology segment is projected to reach BRL 210 billion, equal to USD 38.9 billion, by 2030, underscoring the scale of future specialty demand. Bupa and Spire Healthcare also expanded their oncology and musculoskeletal pathways under a four-year agreement in 2025, which shows how insurers and providers are deepening specialist capacity together. Cardiology and obstetrics & gynecology remain important regional revenue lines, but oncology is setting the pace because it also pulls diagnostics, pathology, imaging, and mental health support into the same care pathway. This makes specialty growth central to how the private healthcare market will allocate future capital and specialist staffing.

By End User: Geriatric Demand Reshapes Service Mix Beyond Bed Count

Adults represented 62.57% of the market in 2025, which kept them as the largest end-user group in the private healthcare market. This reflects the long-established role of working-age consumers, employer coverage, and self-pay demand in shaping private utilization. Adult patients still drive a large share of surgical, diagnostic, maternity-adjacent, and chronic disease activity across most regions. However, the geriatric segment is expected to grow at a 7.41% CAGR through 2031, which makes it the fastest-growing end-user category.

This change matters because older patients usually require more repeat visits, longer stays, and a wider mix of specialist services. Malaysia entered aging status in 2025, and people aged 65 and above accounted for 8% of the population, with healthcare use shifting from episodic care toward recurring and higher-intensity demand. In India, the elderly population aged 60 and above stands at 142 million and is projected to reach 193.4 million by 2031, while the senior care bed supply remains limited at only 20,000 beds. Pediatric demand remains relevant in higher-birth-rate markets, and Cloudnine’s acquisition of Apollo Cradle and Apollo Fertility shows active private platform building around maternal and child care. The private healthcare market is therefore shifting toward older and more clinically complex patients, even while younger family-oriented service lines still support stable throughput. Providers that align bed mix, rehabilitation services, and chronic care coordination to this aging profile are likely to improve revenue per patient more effectively than those that only expand general bed capacity.

Geography Analysis

North America accounted for 38.24% of the private healthcare market share in 2025, giving it the largest regional position in the global private healthcare market. The region benefits from deep insurance penetration, strong for-profit hospital systems, and a large base of employer-sponsored care funding. HCA Healthcare reported USD 75.6 billion in revenue for 2025 and guides to USD 76.5 billion to USD 80 billion in 2026, which reflects continued volume growth and outpatient network expansion. Employer health premiums are also projected to rise nearly 5% in 2027, which suggests that employer purchasing decisions will continue to shape demand, access design, and provider selection. Canada and Mexico remain meaningful private capacity opportunities, but their growth remains more moderate because public systems still carry a larger share of care delivery.

Europe remains a large but mixed private healthcare market where funding models and the private-public balance vary widely by country. Germany provides one of the clearest signs of ongoing private participation, with private health coverage reaching nearly 41 million in 2025. The UK is still seeing active strategic interest in private hospital assets, and Spire Healthcare drew private equity attention in early 2026 while operators also managed pressure from NHS commissioning reform and tariff uncertainty. Across the region, private providers are trying to balance insured growth, self-pay demand, and publicly commissioned activity without allowing reimbursement pressure to weaken returns too sharply.

Asia-Pacific is forecast to grow at an 8.79% CAGR through 2031, making it the fastest-growing regional block in the private healthcare market. India remains a major expansion market because hospital groups are adding beds, raising capital, and widening specialist capacity across both major metros and selected tier-2 cities. The GCC also remains a high-priority growth zone because governments are pushing more private participation and operators continue to invest in accredited hospital and specialty capacity. South Africa continues to have strong private hospital groups, but utilization still faces pressure from medical scheme affordability and specialist staffing constraints. In South America, Brazil stands out through the scale of private oncology expansion, while Colombia shows that voluntary health plan adoption is widening the customer base for formal private care. This mix leaves Asia-Pacific as the main growth engine, while North America and Europe continue to anchor scale, capital, and payer sophistication in the private healthcare market.

Competitive Landscape

The private healthcare market remains fragmented at the global level, and no single provider controls more than a low single-digit share worldwide. Scale matters far more within regions, where hospital density, insurer relationships, and specialist networks create meaningful barriers to entry. In the United States, HCA Healthcare, Tenet, and other large systems keep reinforcing local density through outpatient buildouts, urgent care additions, and tighter care pathway control. HCA Healthcare’s net income rose 17.8% in 2025 to USD 6.8 billion, which shows how size, case mix, and broad network reach continue to support earnings in mature private systems. Tenet’s continued investment in USPI also shows that the ambulatory scale is now one of the clearest competitive levers in the private healthcare market.

Competition across Asia, the Middle East, and parts of Africa is following a different pattern because providers are still building platforms rather than defending already saturated national footprints. Manipal Health received approval in July 2026 to move ahead with its proposed IPO of INR 8,000 crore, equal to USD 952 million, and the company operated 49 hospitals with 12,631 licensed beds as of December 2025, which points to continued consolidation and capital market interest. Max Healthcare also plans to lift bed capacity from 6,500 to more than 10,000 by FY30, backed by INR 6,000 crore, equal to USD 714 million, in investment. Apollo Hospitals added 4 new hospitals in FY26 and continues to invest across healthcare services, diagnostics, and digital health, which shows that leading Indian groups are building broader care ecosystems rather than only adding beds. This means competition is increasingly shaped by who can combine physical expansion, specialist recruitment, and capital access most effectively.

Strategic moves are also changing ownership and funding structures inside the private healthcare market. Blue Owl Capital and Moor Park Capital Partners completed the acquisition of a portfolio of 12 Spire Healthcare hospitals in July 2026 through a sale-leaseback structure, giving Spire more room for clinical reinvestment while separating the real estate from operations. HCA Healthcare acquired 17 urgent care clinics in the Carolinas in June 2026 while also moving to divest home health and hospice agencies, which shows a sharper focus on higher-acuity outpatient care within its network. Remgro’s restructuring to take full control of Mediclinic further signals that regional hospital portfolios are still attractive when operators can align assets, management, and capital across markets. The private healthcare market is therefore becoming more organized regionally, even if it remains fragmented globally. Providers with strong balance sheets, dense clinical networks, and the ability to recycle capital into specialty growth are likely to keep widening their advantage over smaller standalone hospitals.

Private Healthcare Industry Leaders

Apollo Hospitals Enterprise Limited

Bupa

Fortis Healthcare

IHH Healthcare

Manipal Hospitals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Blue Owl Capital, together with Moor Park Capital Partners, completed the acquisition of a portfolio of 12 acute-care hospitals operated by Spire Healthcare Group plc in the UK. The transaction, structured as a sale-leaseback arrangement, accelerates Blue Owl's European Net Lease strategy and releases capital within Spire for clinical reinvestment.

- July 2026: Manipal Health Enterprises received SEBI approval to proceed with its proposed IPO of approximately INR 8,000 crore (approximately USD 952 million at 2026 rate), with proceeds earmarked primarily to repay subsidiary borrowings and acquire a minority stake in Sahyadri Hospitals. As of December 2025, Manipal operated 49 hospitals with 12,631 licensed beds across 14 states.

- June 2026: HCA Healthcare acquired 17 urgent care clinics from Urgent Care Group across the Carolinas, extending its HCA CareNow ambulatory brand. The company is separately in the process of divesting 31 home health and hospice agencies to Deaconess Associations, reflecting a strategic focus on higher-acuity outpatient care.

- May 2026: Apollo Hospitals reported FY26 net profit growth of 34% to INR 1,942 crore (approximately USD 232 million at 2025 rate), driven by growth across healthcare services, diagnostics, and digital health. Apollo commissioned 4 new hospitals adding approximately 855 beds and has a remaining capex pipeline of approximately INR 5,100 crore (approximately USD 608 million).

Global Private Healthcare Market Report Scope

As per the scope of the report, private healthcare comprises healthcare services delivered by privately owned and privately operated providers, including private hospitals, specialty hospitals, multi-specialty clinics, ambulatory care centers, diagnostic centers, rehabilitation centers, and home healthcare providers. The market serves patients through self-pay, private insurance, employer-sponsored insurance, and public-private partnership (PPP) reimbursement models.

The private healthcare market is segmented by service type, healthcare facility, payment type, specialty, end user, and geography. By service type, the market is segmented into inpatient services, outpatient services, diagnostic services, emergency care services, and others. By healthcare facility, the market is segmented into private hospitals, specialty hospitals, ambulatory surgical centers, and others. By payment type, the market is segmented into private health insurance, out-of-pocket payments, public-private partnerships (PPP), and others. By specialty, the market is segmented into general medicine, cardiology, oncology, obstetrics & gynecology, and others. By end user, the market is segmented into adults, the geriatric population, and the pediatric population. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Inpatient Services |

| Outpatient Services |

| Diagnostic Services |

| Emergency Care Services |

| Others |

| Private Hospitals |

| Specialty Hospitals |

| Ambulatory Surgical Centers |

| Others |

| Private Health Insurance |

| Out-of-Pocket Payments |

| Public-Private Partnerships (PPP) |

| Others |

| General Medicine |

| Cardiology |

| Oncology |

| Obstetrics & Gynecology |

| Others |

| Adults |

| Geriatric Population |

| Pediatric Population |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Inpatient Services | |

| Outpatient Services | ||

| Diagnostic Services | ||

| Emergency Care Services | ||

| Others | ||

| By Healthcare Facility | Private Hospitals | |

| Specialty Hospitals | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Payment Type | Private Health Insurance | |

| Out-of-Pocket Payments | ||

| Public-Private Partnerships (PPP) | ||

| Others | ||

| By Specialty | General Medicine | |

| Cardiology | ||

| Oncology | ||

| Obstetrics & Gynecology | ||

| Others | ||

| By End User | Adults | |

| Geriatric Population | ||

| Pediatric Population | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of private healthcare by 2031?

The private healthcare market is projected to reach USD 4.69 trillion by 2031 from USD 3.79 trillion in 2026, rising at a 4.38% CAGR over 2026 to 2031.

Which service area is growing fastest in private care delivery?

Outpatient services are growing fastest by service type, with a projected 4.98% CAGR through 2031 as more procedures move to ambulatory and short-stay settings.

Which facility format leads revenue today?

Private hospitals remain the largest facility type, holding 53.68% share in 2025 because they still anchor acute care, surgery, and insured referral pathways.

Why is oncology becoming so important for providers?

Oncology is projected to grow at a 6.89% CAGR through 2031 because cancer care requires longer treatment cycles, faster diagnostics, and coordinated specialty services.

Which patient group is changing demand patterns the most?

The geriatric segment is forecast to grow at a 7.41% CAGR through 2031, which is pushing providers to rethink bed mix, rehabilitation, and chronic care coordination.

Which region offers the strongest growth outlook?

Asia-Pacific is the fastest-growing region with an 8.79% CAGR through 2031, supported by hospital expansion, specialty investment, and broader private participation.

Page last updated on: