United Arab Emirates Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

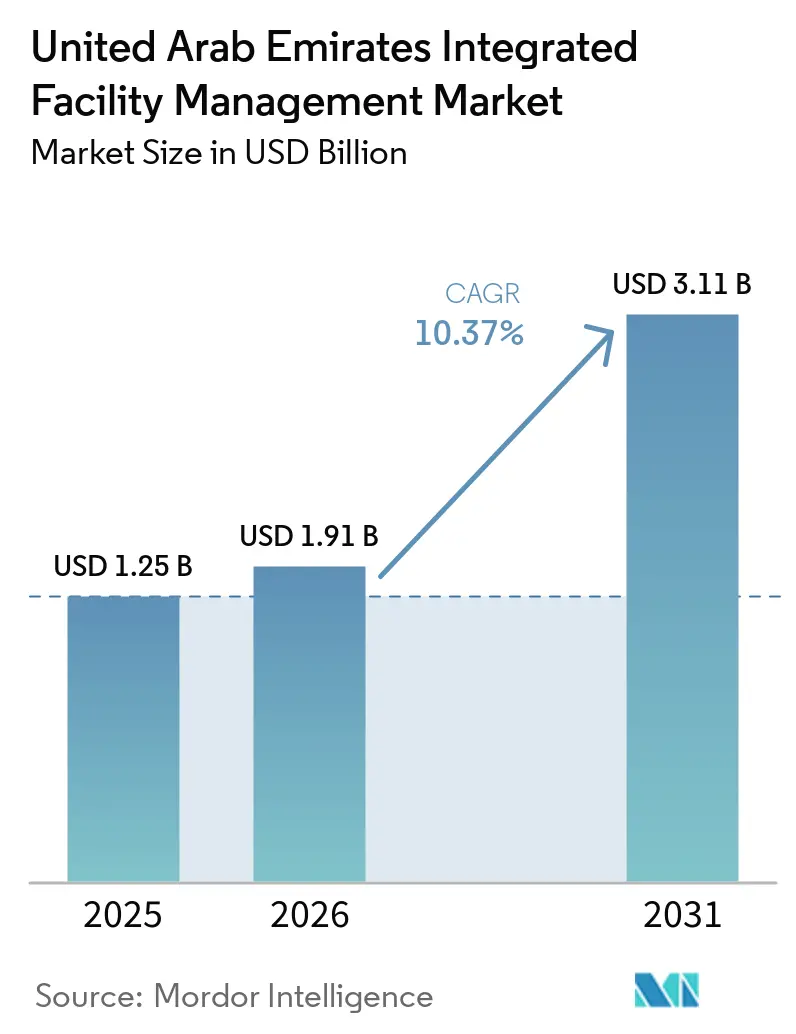

| Base Year Market Size (2025) | USD 1.25 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 3.11 Billion |

| Growth Rate (2026 - 2031) | 10.37% CAGR |

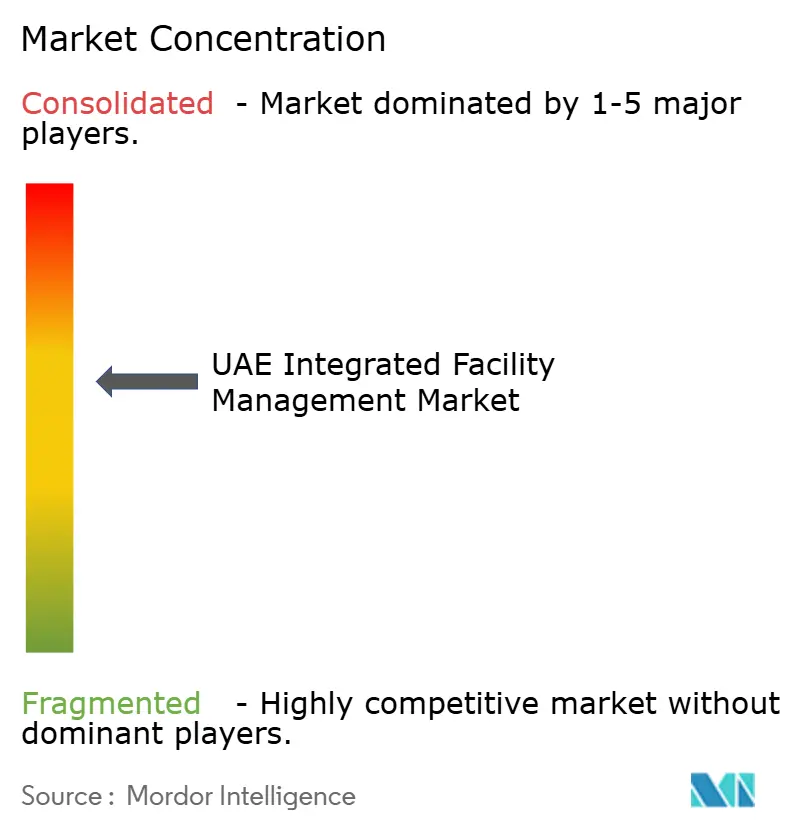

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Integrated Facility Management Market Analysis by Mordor Intelligence

The United Arab Emirates integrated facility management market size was valued at USD 1.25 billion in 2025 and estimated to grow from USD 1.91 billion in 2026 to reach USD 3.11 billion by 2031, at a CAGR of 10.37% during the forecast period (2026-2031). The United Arab Emirates integrated facility management (IFM) market is expanding as urban development continues at scale, owners shift toward consolidated service delivery, and occupiers demand stronger service consistency across commercial, hospitality, and industrial assets. Construction output reached USD 107.2 billion in 2024 and is projected to reach USD 130.8 billion by 2029, which keeps adding new buildings that will move into long-term operating and maintenance cycles. Dubai alone has 8.2 million sq ft of office space under construction for delivery by 2028, which supports a visible forward pipeline for integrated FM contracts. The United Arab Emirates IFM market also benefits from Soft FM’s broad daily-use demand, while commercial assets are lifting contract volumes and industrial facilities are raising contract complexity and average contract value. Competition remains intense, but contract wins are moving toward providers with digital tools, certified technical capability, and the scale to manage labor and compliance costs across multiple sectors.

Key Report Takeaways

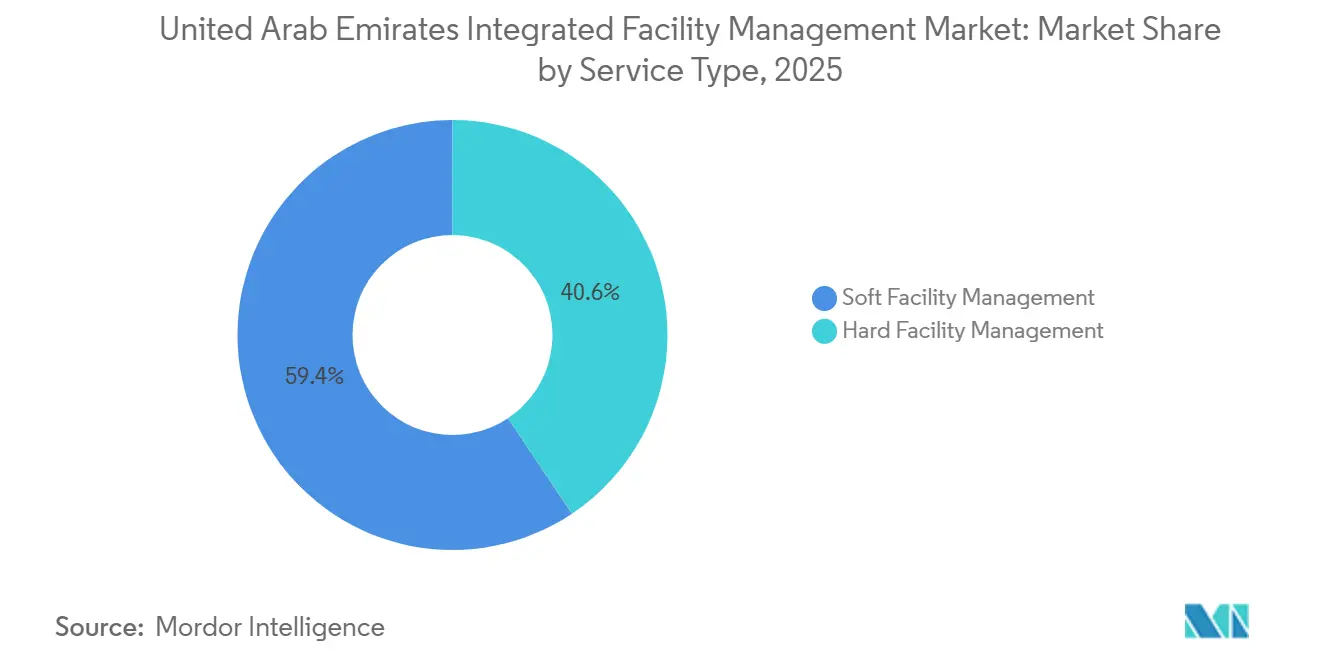

- By service type, soft facility management commanded 59.38% share of the United Arab Emirates integrated facility management market in 2025, while hard facility management is forecast to expand at a 11.01% CAGR through 2031.

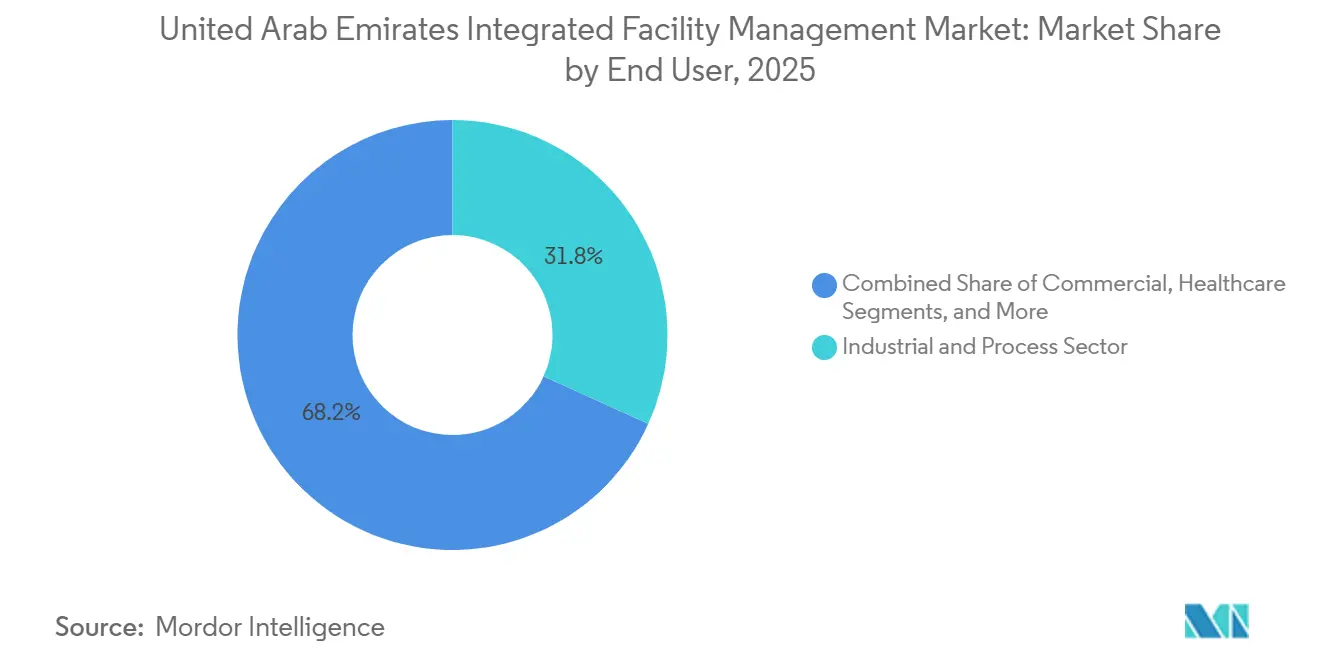

- By end user, the industrial and process segment held a 31.78% share of the UAE integrated facility management (IFM) market in 2025, while the commercial segment recorded the highest projected CAGR at 10.79% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Commercial Real Estate and Economy | +3.5% | Dubai and Abu Dhabi core, spill-over across all emirates | Short term (≤ 2 years) |

| Outsourcing Trend for Cost Optimisation | +2.8% | Global, across all UAE emirates and sectors | Medium term (2-4 years) |

| Regulatory Push for Green Buildings and Energy Efficiency | +2.2% | Dubai and Abu Dhabi core, spill-over to Sharjah and Northern Emirates | Medium term (2-4 years) |

| Adoption of Integrated Digital FM and IoT Platforms | +1.8% | Global, with early adoption concentrated in Dubai, Abu Dhabi, and Sharjah smart city clusters | Long term (≥ 4 years) |

| Public-Private Build-to-Operate Models | +1.2% | Abu Dhabi and Ras Al Khaimah primarily | Long term (≥ 4 years) |

| Mega Cultural and Sports Events Driving FM Demand | +0.8% | Abu Dhabi and Dubai, with event infrastructure spanning all emirates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Commercial Real Estate and Economy

Dubai’s office market tightened sharply in 2025 as multinational firms expanded regional headquarters activity and absorbed premium space at a faster pace. Commercial property sales in Dubai reached AED 30.38 billion (USD 8.3 billion) in Q3 2025, while the office segment recorded AED 3.1 billion (USD 844.1 million) across 1,153 units, which shows how quickly commercial stock is moving into operation.[1]CRC, "The Pulse of Dubai's Commercial Real Estate Market Report 2025," www.crcproperty.com/en/insights/market-reports That matters for the United Arab Emirates integrated facility management market because new office deliveries usually convert into multi-year FM contracts that cover technical services, cleaning, security, and workplace support. The development pipeline is also widening into hospitality and data centers, and data centers already account for 9% of the active pipeline by project type, which raises the value of FM scopes beyond standard building upkeep. ESG-compliant towers add another layer of demand because certified assets need operating models that can sustain energy, air quality, and system performance over time.

Outsourcing Trend for Cost Optimization

Across the private sector, outsourcing has moved beyond a short-term cost response and become a more permanent operating model. In the UAE integrated facility management (IFM) market, this shift supports third-party providers that can spread labor pools, compliance systems, and technology investment across many clients instead of one balance sheet. Farnek secured AED 690 million (USD 187.9 million) in new contracts during 2024 across aviation, healthcare, and retail in the UAE and Saudi Arabia, which shows that buyers continue to move large scopes to providers with broad delivery capability.[2]Farnek, “2024 New Contract Wins Across Aviation, Healthcare, and Retail,” Farnek, farnek.comThe contract structure is also changing because clients increasingly want outcome-based agreements tied to verified service levels rather than billed labor hours alone. That change benefits operators that can measure performance clearly, manage workforce compliance consistently, and absorb operational risk without weakening service quality.

Regulatory Push for Green Buildings and Energy Efficiency

Energy and sustainability rules are turning building operations into a more regulated part of the service model. In February 2025, the Dubai Supreme Council of Energy accredited 5 FM companies under the BEMAS framework to manage more than 700 buildings covering over 13 million m² across the UAE, which narrowed access to a growing pool of energy-sensitive contracts for certified operators.[3]Dubai Electricity and Water Authority, “Building Energy Management Accreditation Scheme Accreditation Announcement,” Dubai Electricity and Water Authority, dewa.gov.aeDubai’s green building rules require sub-metering for larger assets, HVAC compliance testing, periodic recommissioning for major buildings, and indoor air quality testing for hotels, malls, hospitals, and government buildings. These are recurring operating requirements, so they create repeat FM revenue rather than one-time project work. Within the UAE IFM market, this is pushing more value toward BEMAS-accredited and ISO-certified providers that can document compliance and deliver measurable efficiency outcomes.

Adoption of Integrated Digital FM and IoT Platforms

Digital building systems and IoT-enabled maintenance platforms are now moving into core contract requirements, especially in complex commercial and industrial assets. The performance case is clear because predictive maintenance can reduce machine downtime by 30-50% and extend equipment life by 20-40%, which gives owners a direct reason to specify digital capability in tenders. Johnson Controls launched OpenBlue Workplace in the Middle East from Dubai in June 2025 and reported up to 10% energy savings, a 67% reduction in chiller maintenance costs, and a 155% return on investment with payback periods as short as 8 months. Khansaheb Facilities Management then announced full Digital Twin integration across its 2,000+ property portfolio in February 2026, raising the service benchmark for large local operators. For the UAE IFM market, digital investment is no longer just a differentiator because it is becoming a cost of entry for premium contracts that require transparency, predictive capability, and remote monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Cost Inflation From Visa Reforms | -1.0% | Global, concentrated in labor-intensive Soft FM segments across all emirates | Short term (≤ 2 years) |

| Price-Based Competition Squeezing Margins | -0.7% | Global, concentrated in commoditized cleaning and security segments | Medium term (2-4 years) |

| In-House FM Adoption in Sensitive Government Sectors | -0.5% | Abu Dhabi and Dubai government building portfolios | Medium term (2-4 years) |

| Supply-Chain Disruption for Specialised Equipment and Services | -0.4% | APAC core, with spill-over effects on UAE and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Cost Inflation from Visa Reforms

Labor remains the largest single input cost in FM delivery, so regulatory changes have an immediate effect on margins. Employer costs in Dubai exceeded base salary by 15-20% in 2025 when work permit fees, health insurance obligations, and end-of-service gratuity accruals were included. Work permit fees alone stood at AED 3,500-5,500 per hire, (USD 953-1,497), which is meaningful for operators hiring at scale. Emiratization penalties rose to AED 120,000 per unfilled Emirati position (USD 32,675 per position) from 2026, and mandatory health insurance for all private-sector employees from January 2026 adds another fixed layer to workforce cost.[4]Ministry of Human Resources and Emiratisation, “Private-Sector Employment Rules and Emiratisation Penalties,” Ministry of Human Resources and Emiratisation, mohre.gov.ae In the UAE integrated facility management (IFM) market, providers with stronger technical revenue and multi-sector contract books are better placed to absorb this pressure than firms that depend heavily on labor-intensive Soft FM lines.

Price-Based Competition Squeezing Margins

The United Arab Emirates integrated facility management market still has a fragmented mid-tier where many local and regional operators compete for similar building portfolios. That structure keeps pricing pressure high, especially in cleaning and security, where service scopes are easier for clients to compare. Adeeb Group noted in 2025 that competitive pressure and payment delays remained an issue even as it secured and renewed more than 700 contracts, which shows that volume growth does not automatically improve profitability. Clients are responding by adding certification thresholds, technology requirements, and performance-linked payment terms into tenders, but these measures mainly help larger providers that already have the needed systems in place. Smaller firms that cannot differentiate through sector expertise, verified outcomes, or digital transparency will find it harder to defend margins even as contract demand rises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Acceleration Challenges Soft Facility Management's Structural Lead

Soft facility management (FM) held 59.38% of the United Arab Emirates integrated facility management market share in 2025, while Hard facility management is projected to expand at 11.01% CAGR through 2031. Soft FM remained the larger service line because cleaning, catering, security, and office support are required at high frequency across the UAE’s commercial, hospitality, and residential building stock. Buyers also prefer bundled ancillary services because they reduce vendor coordination and help control site-level operating costs in a competitive occupier environment. Hard FM is growing faster because new-generation assets use more complex building systems and owners are shifting from reactive repairs toward preventive and predictive maintenance. Within the UAE IFM industry, that transition is steadily increasing the value of MEP, HVAC, asset management, and system analytics scopes.

The strongest uplift inside hard facility management comes from areas where regulation and technical complexity intersect. Dubai’s green building rules require HVAC compliance testing and periodic recommissioning, which converts specialist technical work into recurring revenue instead of one-time intervention. Fire systems and safety remain protected niches because Dubai Civil Defence’s A+ contractor certification limits competition to a smaller qualified pool, and Imdaad’s Vision Safety unit is one of the operators that benefits from that structure. The refrigerant transition under Federal Decree-Law No. 11 of 2024 adds another multi-year workstream because FM providers need to manage retrofits, legacy refrigerant inventories, and future compliance planning before the 2028 freeze date. At the same time, Soft FM cleaning and catering are facing higher labor costs and greater automation needs, which is pushing providers in the United Arab Emirates IFM market toward robotics, smart dispatch, and outcome-based pricing to protect margins.

By End User: Industrial Sector Anchors Share While Commercial Segment Leads Growth

The commercial segment is projected to grow at 10.79% CAGR through 2031, which is the fastest pace within the United Arab Emirates IFM market size, while the industrial and process segment remained the largest end-user category accounts for 31.78% share in 2025. Commercial demand is rising because office absorption is strong in Dubai’s premium towers and retail activity is benefitting from the city’s 12.4 million international visitors in the first 9 months of 2025. Industrial and process facilities still anchor the largest share because they need 24/7 uptime, specialist MEP support, hazardous waste management, and tightly controlled maintenance programs across manufacturing, oil and gas, and logistics sites. Farnek’s 2024 contract portfolio included the Barakah Nuclear Power Plant and Etihad Airways Engineering in Abu Dhabi, with a combined value of AED 240 million (USD 65.4 million), which illustrates the higher ticket size available in industrial accounts. Within the United Arab Emirates IFM industry, this means commercial assets are expanding contract volumes while industrial facilities keep raising contract complexity and revenue per site.

Hospitality is becoming a sharper growth pocket because new mixed-use and tourism-led assets are buying more advanced service bundles than legacy hotels. Emrill reported AED 73 million (USD 19.9 million) in hospitality contracts as a major contributor to its 9% revenue growth in 2025, and its One Za'abeel mandate includes drone façade inspections and energy modeling for a 530,000 m² LEED Gold certified development. Healthcare is also strengthening because hospital expansion brings stricter infection control, clean room maintenance, and zero-downtime standards that favor experienced providers with regulated operating models. Institutional and public-sector demand is widening as Dubai Police tendered integrated FM across its buildings in December 2025, while Farnek’s flexible model for education clients, supported by CAFMTEK AI Predictive Maintenance and IoT Remote Monitoring, reported 20-55% monthly savings versus conventional fixed contracts.

Geography Analysis

Dubai and Abu Dhabi accounted for the clear majority of United Arab Emirates integrated facility management market demand in 2025 because they dominate the country’s commercial, institutional, and industrial built environment. Dubai’s commercial property market remained active, with sales reaching AED 30.38 billion (USD 8.3 billion) in Q3 2025, and that strength is supported by 8.2 million sq ft of office supply under construction for delivery by 2028. Each major office, retail, hospitality, or mixed-use delivery in Dubai usually creates a multi-year FM mandate, so today’s construction pipeline feeds tomorrow’s recurring service backlog. Abu Dhabi has a different demand profile because government, public-sector, and institutional clients carry a larger share of FM spend there. Adeeb Group secured and renewed more than 700 contracts in 2025, including mandates with Abu Dhabi Police and the Central Bank of the UAE, while the Abu Dhabi Masters Games 2026 activated 38 venues across Abu Dhabi, Al Ain, and Al Dhafra and lifted both event-linked and baseline maintenance demand.

Sharjah is emerging as a third operating node in the UAE IFM market because its commercial and government real estate base continues to expand. Apleona’s joint venture with Sharjah Asset Management already supports government buildings, commercial properties, and healthcare facilities, including the 37,000 m² Souq Al Jubail market, which shows that integrated FM demand is becoming more established outside Dubai and Abu Dhabi. Sharjah’s lower rental levels also attract cost-sensitive occupiers, and that encourages bundled service models that combine technical and soft scopes under one contract at a controlled price point. Ras Al Khaimah and the Northern Emirates remain less penetrated, but infrastructure and hospitality investment is broadening the long-term addressable base for operators that can move beyond the two main metropolitan centers.

These geographic spread matters because each emirate is creating a different contract mix inside the United Arab Emirates IFM market. Dubai favors high-spec office, retail, and hospitality mandates with strong digital and sustainability requirements, while Abu Dhabi offers larger institutional and public-sector contracts with long tenure and stricter compliance expectations. Sharjah provides room for value-oriented integrated models, and Ras Al Khaimah is opening a new lane through utility, tourism, and build-own-operate-transfer projects with long operating horizons. Operators that already have delivery depth in Dubai are well placed to follow hospitality and infrastructure demand into the Northern Emirates, especially where luxury resorts and utility assets need the same technical discipline seen in top-tier urban portfolios.

Competitive Landscape

The UAE integrated facility management market is moderately consolidated at the top and fragmented through the middle and lower tiers. Imdaad and Transguard Group anchor the domestic field, while Farnek, Serco, Emrill, Adeeb, Khansaheb, Apleona, and other multi-service or specialist firms compete across overlapping contract pools. Transguard reported AED 3.2 billion (USD 871.3 million) in annual revenue for FY24/25, achieved ISO 41001:2018 certification, and deployed a new CAFM system during the year, which shows how leading operators are building process depth and system control. The same report also disclosed a partnership with the DIFC Innovation Hub and sustainability collaboration with Emirates Flight Catering, which reflects a broader push to create institutional and technology linkages that smaller firms struggle to match. This structure keeps the UAE integrated facility management market competitive, but it also rewards scale, certifications, and cross-sector operating history more than low pricing alone.

Global operators still compete selectively for major public and institutional mandates where long-term service models and technology platforms matter. Serco Middle East secured an AED 495 million (USD 134.8 million) contract extension with Dubai Airports in June 2025, extending a major airport services relationship through December 2030. Johnson Controls and Al-Futtaim Technologies also launched OpenBlue Workplace in the UAE in June 2025, bringing a digital offer that reported 155% ROI and a 67% reduction in chiller maintenance costs at adopter sites. These moves show why premium contracts are increasingly shaped by digital performance, energy outcomes, and trusted public-sector relationships rather than by labor scale alone.

Three strategies are clearly working in the UAE IFM market, scale-and-integrate, tech-and-certify, and sector-specialize. Scale-and-integrate helps large operators spread compliance costs and offer bundled services across wider client bases. Tech-and-certify supports premium pricing because clients now value predictive maintenance, transparent reporting, and recognized operating standards. Sector specialization still matters in healthcare, aviation, nuclear, and other regulated environments, while the Serco-Solutions+ partnership to build Khadamat Facilities Management and Presight’s AI-led work with Khazna Data Centers show that consolidation and digital unbundling are both starting to reshape the upper end of the market.

United Arab Emirates Integrated Facility Management Industry Leaders

-

Emrill Services LLC

-

EFS Facilities Services Group

-

Imdaad LLC

-

Farnek Services LLC

-

Khidmah LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cleanco Group signed an agreement with YAEMCO Facilities Management to acquire YAEMCO’s Hard FM operations, strengthening its integrated facility management (IFM) capabilities across the UAE. The deal expands Cleanco’s technical FM, MEP, HVAC, and compliance services, supporting rising demand from healthcare, commercial, and government sectors.

- February 2026: Khazna Data Centers signed a long-term, commercially significant contract with Presight for an AI-optimised facility management platform at its UAE hyperscale data center operations. The platform integrates OT and facility data into a centralized intelligence layer for predictive maintenance, ESG reporting, and a Meta-Intelligence Digital Twin for 3D infrastructure simulation.

- January 2026: Transguard Group signed a memorandum of understanding with FAAC Technologies Middle East at Intersec 2026 to jointly develop access control and automation solutions for UAE commercial and institutional built environments.

- June 2025: Serco and Solutions+ expanded their partnership to strengthen Khadamat Facilities Management as a national integrated facility management (IFM) platform in the UAE. Under the agreement, both companies will consolidate IFM service contracts into Khadamat, combining Solutions+’ digital transformation expertise with Serco’s FM capabilities across infrastructure, healthcare, transport, and real estate to support operational efficiency, sustainability, and Emiratization goals.

United Arab Emirates Integrated Facility Management Market Report Scope

The United Arab Emirates Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is driving demand for the United Arab Emirates integrated facility management services?

Demand is being lifted by large construction handovers, stronger outsourcing by occupiers, green building compliance, and wider use of digital maintenance platforms. The market is projected to grow from USD 1.91 billion in 2026 to USD 3.11 billion by 2031 at a 10.37% CAGR.

Which service type leads the UAE integrated facility management market?

Soft facility management led in 2025 with 59.38% share because cleaning, security, catering, and workplace support are recurring needs across large building portfolios.

Why is Hard FM growing faster than the overall sector?

Hard facility management is forecast to grow at 11.01% CAGR through 2031 because newer assets need more technical maintenance, HVAC compliance work, predictive maintenance, and specialist engineering support.

Which end-user group is expanding the fastest in the United Arab Emirates?

The commercial segment is the fastest-growing end-user group, with a 10.79% CAGR through 2031, supported by office absorption, tourism-linked retail demand, and premium mixed-use developments.

Why do industrial and process facilities remain important for FM providers?

They remain the largest end-user category because they require 24/7 uptime, hazardous waste management, specialist MEP maintenance, and higher-value service scopes than standard commercial sites.

How competitive is the UAE IFM market?

The market is competitive and only moderately consolidated at the top. Large firms have advantages in digital tools, certifications, and public-sector relationships, but dozens of mid-tier and specialist operators still keep pricing pressure high.

Page last updated on: