Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

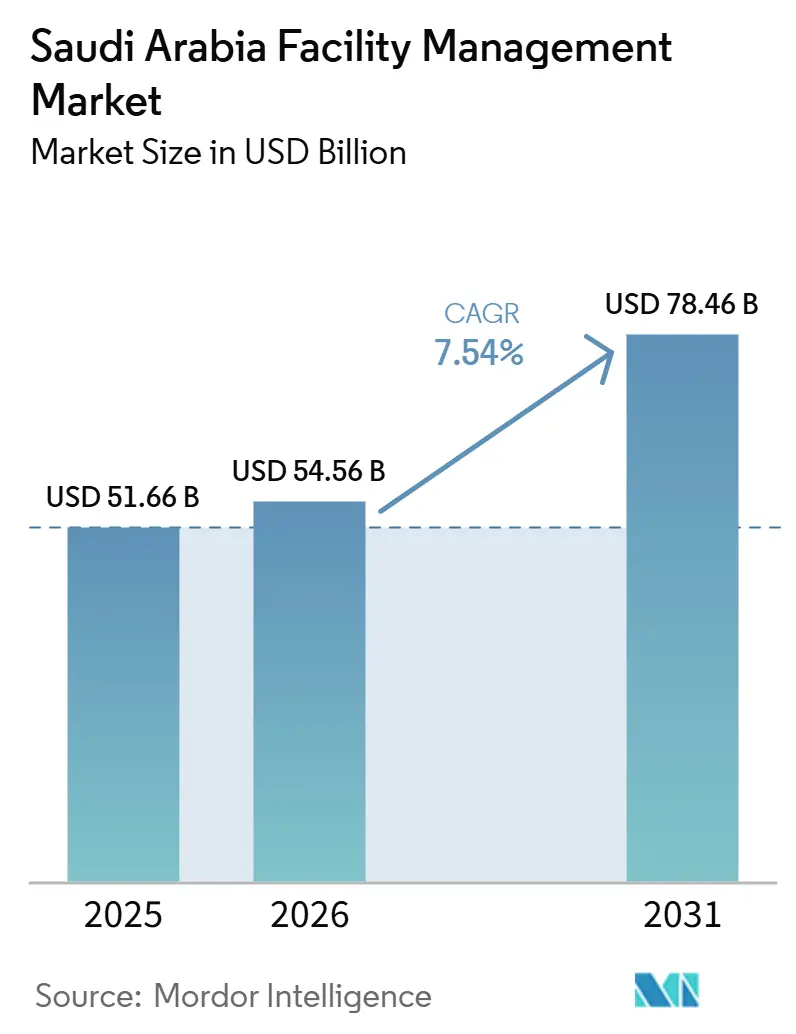

| Base Year Market Size (2025) | USD 51.66 Billion |

| Market Size (2026) | USD 54.56 Billion |

| Market Size (2031) | USD 78.46 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

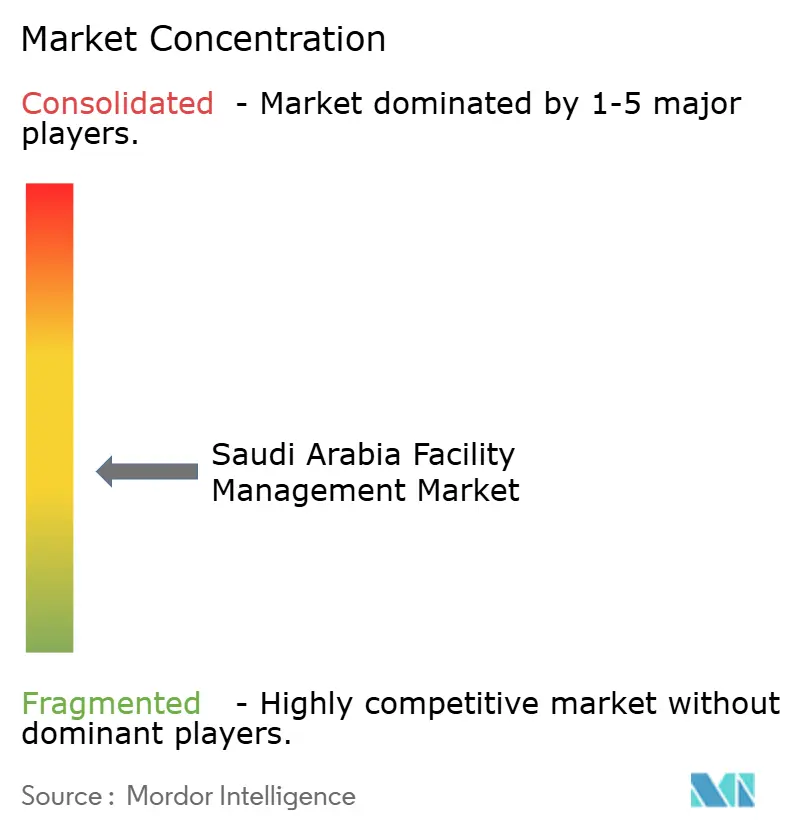

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Facility Management Market Analysis by Mordor Intelligence

The Saudi Arabia Facility Management Market size is projected to be USD 51.66 billion in 2025, USD 54.56 billion in 2026, and reach USD 78.46 billion by 2031, growing at a CAGR of 7.54% from 2026 to 2031. Surging capital expenditure on giga-projects, the rollout of Special Economic Zones with 5% corporate tax for two decades, and an increasingly liberalized services sector are together propelling the Saudi Arabia facility management market toward double-digit growth. Large mixed-use developments such as NEOM, Red Sea Global and Qiddiya now insist on integrated contracts that cover hard, soft and sustainability services under single governance structures, a demand pattern that favors providers with scale, digital platforms and ESG credentials.[1]TradeArabia News Service, “Saudi Vision 2030 real estate, infra projects top $1.1trn,” tradearabia.com Government privatization of 38 agencies has simultaneously opened core municipal and utility assets to private operators, boosting the pipeline of long-term outsourcing tenders and fueling the Saudi Arabia facility management market’s transition from in-house models to specialist providers. At the same time, rising IoT adoption is embedding predictive maintenance and energy analytics into everyday operations, cutting unplanned downtime by up to 70% and lowering lifecycle costs, which in turn strengthens the business case for outsourced, data-driven service agreements.[2]International Journal of Information and Education Technology, “Predictive Maintenance Using IoT,” ijiet.org Finally, mandated compliance with the Mostadam rating system and the Green Building Code is pushing ESG from voluntary practice to contractual obligation, anchoring sustainability as a core revenue stream for facility managers.

Key Report Takeaways

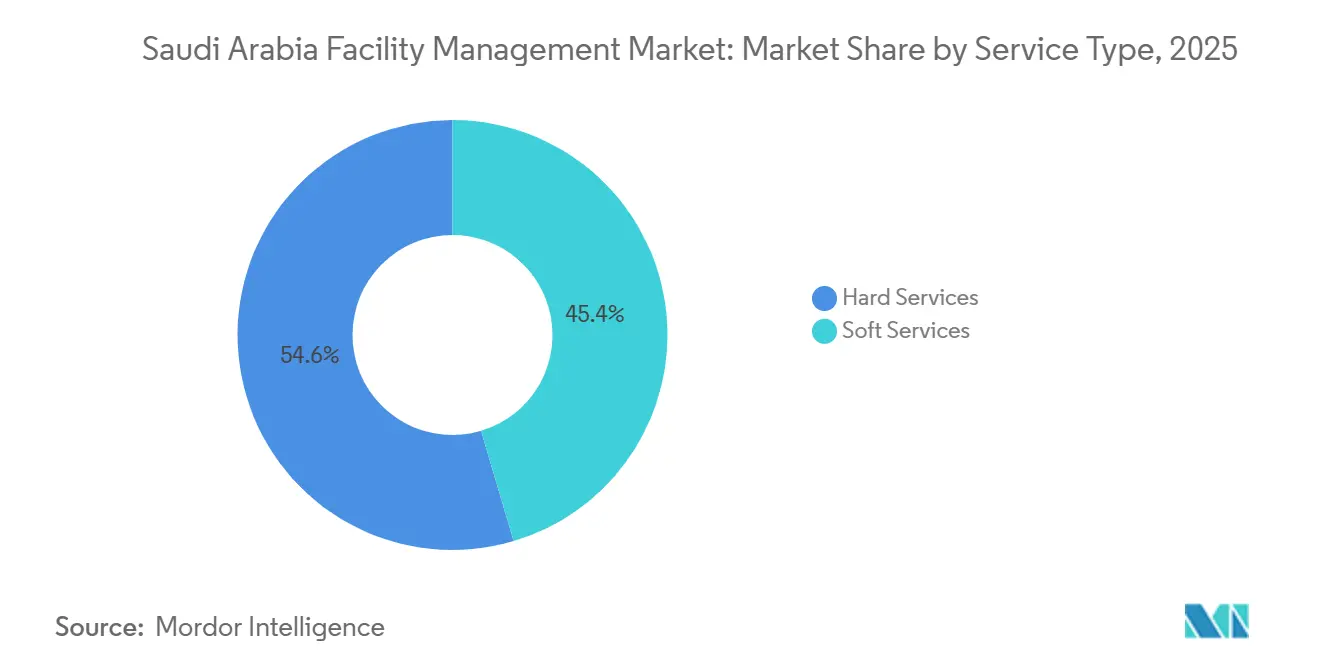

- By service type, Hard Services held 54.59% of the Saudi Arabia facility management market share in 2025, while Soft Services are forecast to post a 8.12% CAGR through 2031.

- By offering type, the Outsourced segment accounted for 59.36% of the Saudi Arabia facility management market size in 2025 and is projected to grow at a 8.34% CAGR to 2031.

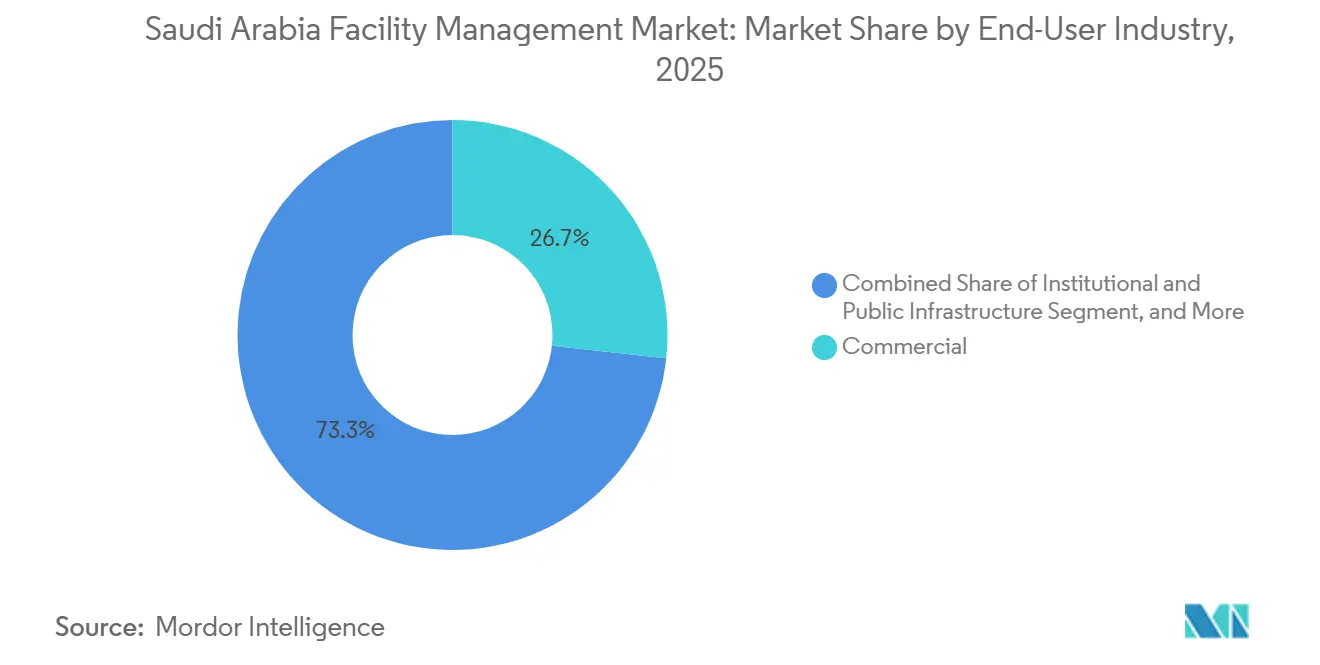

- By end-user industry, Commercial facilities led with 26.73% revenue share in 2025; healthcare is set to record the fastest expansion at a 9.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 infrastructure expansion | +2.8% | Riyadh, NEOM, Red Sea | Long term (≥ 4 years) |

| Technology adoption in building management | +1.9% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Outsourcing and service integration | +2.1% | National, strong in commercial hubs | Medium term (2-4 years) |

| Sustainability and ESG compliance | +1.4% | National, pronounced in giga-projects and SEZs | Long term (≥ 4 years) |

| Giga-projects driving integrated FM demand | +2.6% | NEOM, Red Sea, Qiddiya, KAEC | Long term (≥ 4 years) |

| Government-led privatization of services | +1.7% | Pilot programs in major municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Infrastructure Expansion

Mega-projects valued at more than USD 1.1 trillion have re-defined the Saudi Arabia facility management market by replacing ad-hoc maintenance with lifecycle-oriented contracts that blend asset uptime, energy optimization and sustainability reporting. NEOM alone spans 26,500 km² and demands single-provider solutions across linear cities, floating industries and luxury resorts. Dussmann Group’s joint venture with Ajlan & Bros created more than 4,000 jobs to service these assets and plans to double its workforce, signaling the volume of integrated work coming to market. Outcome-based contracting is becoming common, transferring performance risk to suppliers yet raising revenue visibility. With the Kingdom committed to net-zero emissions by 2060, carbon-reduction metrics are embedded in all new project tender documents, cementing long-term demand for ESG-aligned services.[3]Red Sea Global, “Recognized as Real Estate Industry Leader in Sustainability Assessment,” redseaglobal.com

Technology Adoption in Building Management

IoT sensors, AI analytics and digital twins are pushing the Saudi Arabia facility management market toward data-centric operations. Field tests show maintenance costs falling 25-30% and breakdowns declining up to 75% after predictive programs are deployed. Saudi Aramco’s facilities saved 40% in energy costs once predictive maintenance and automated controls went live, establishing an industrial benchmark. The King Abdullah Financial District runs 100,000 assets through an IBM Maximo platform and achieves 95% occupant satisfaction, proving that enterprise asset management can scale in extreme climates.[4]IBM, “King Abdullah Financial District Case Study,” ibm.com Smaller domestic providers struggle to reach similar digital maturity, giving international firms a competitive edge. Government initiatives such as the Future Factories Program, which targets 4,000 automated plants by 2027, will widen the customer base for tech-enabled providers and drive further consolidation..

Outsourcing and Service Integration

The Private Sector Participation Law authorizes decade-long concessions and allows private entities to collect user fees, materially reducing counterparty risk and fueling the Saudi Arabia facility management market’s shift to outsourced models. National Water Company’s SAR 198 million contract with a Saur-led consortium exemplifies this move toward private-sector efficiency in utility operations. Clients increasingly demand bundled or fully integrated packages that cover maintenance, cleaning, security and energy services under unified key-performance indicators. Musanadah now retains 98% of its clients after adopting integrated delivery platforms, underscoring the sticky economics of single-provider models]. In regulated environments such as hospitals, integration extends to infection-control cleaning protocols, reinforcing the need for specialist expertise.

Sustainability and ESG Compliance

Mostadam and the Saudi Green Building Code require documented, measurable savings in water, waste and energy. Red Sea Global scored 91/100 in the 2023 GRESB audit, positioning ESG as a differentiator among operators seeking premium tourism clientele. Green bond issuance rose eight-fold between 2019 and 2023, providing inexpensive capital to operators that can prove carbon reductions, which drives additional outsourced demand for energy retrofits and zero-waste programs. The Saudi green building market is projected to double to USD 33 billion by 2030, setting a sizeable revenue pool for sustainability-focused service lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortages linked to Saudization | -1.8% | National, acute in technical roles | Medium term (2-4 years) |

| Contract stability and working-capital pressure | -1.3% | National, heavy in public contracts | Short term (≤ 2 years) |

| Low digital readiness among small providers | -0.9% | Secondary cities | Medium term (2-4 years) |

| Delays in public-sector payments | -1.1% | Projects tied to construction ministries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled-labor Shortages Linked to Saudization

Expanded Saudization targets cover 269 professions, inflating payroll costs and shrinking the technical talent pool that keeps complex MEP systems operational.[5]Harvard University, “Labor Market Outcomes and Saudization,” growthlab.hks.harvard.edu Healthcare facilities illustrate the pressure: the sector will need 100,000 additional positions by 2030 while maintaining rigorous compliance regimes. Many contractors face salary delays under the financial strain, a factor that tightens working capital and raises execution risk. Larger providers are offsetting the gap by investing in in-house academies; Solutions by stc already reports a 65.5% Saudi workforce after three years of structured upskilling.

Contract Stability and Working-Capital Pressure

Historic payment lags average 335 days in government work, forcing small firms to self-finance operations and triggering sector-wide consolidation. The state injected USD 26.7 billion in 2024 to clear arrears, yet advance payments on new contracts fell from 20% to 5%, leaving liquidity gaps unresolved . PPP structures promise better payment certainty but impose higher financial-qualification thresholds, narrowing the bidder universe to capital-strong entities. While the Private Sector Participation Law grants compensation for early termination, it does not solve recurring cash-flow volatility that constrains aggressive expansion plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Large-Scale Builds Sustain Hard Services Dominance

Hard Services controlled 54.59% of the Saudi Arabia facility management market in 2025 as mega-airports, high-speed rail links and new city blocks required constant upkeep of HVAC, power distribution and fire systems. The King Salman International Airport alone commands a USD 7.2 billion package for six runways and anticipates 120 million passengers a year, ensuring long-run demand for MEP monitoring and asset-management platforms. Within this category, Asset Management contracts now integrate predictive analytics to meet uptime targets, mimicking the 100,000-asset IBM Maximo installation at the King Abdullah Financial District. On the flip side, Soft Services are accelerating at a 8.12% CAGR through 2031, mirroring the shift toward hospitality, retail and corporate offices inside Special Economic Zones. Cleaning and security have evolved into regulated disciplines, particularly in healthcare, where Musanadah’s ISSA accreditation attests to enhanced infection-control standards.

The Saudi Arabia facility management market size tied to Soft Services is set to expand quickly as SEZ-based multinationals insist on global-grade concierge, help-desk and workplace-strategy offerings. Security and lobby services are also scaling because giga-projects attract international events and VIP clientele. Red Sea Global’s hospitality program alone will require support for 50 resorts and 8,000 rooms, showcasing the scale of non-technical services coming downstream.

By Offering Type: Outsourcing Gains Ground on Efficiency Needs

Outsourced contracts accounted for 59.36% of the Saudi Arabia facility management market size in 2025, affirming that specialized expertise and technology platforms outperform internal departments on cost and risk mitigation. Integrated FM now outpaces single-service models as clients consolidate procurement to reduce overhead and capture data synergies. National Water Company’s SAR 198 million concession exemplifies the move toward multi-decade utility outsourcing, placing performance accountability squarely on private operators. At 8.34% CAGR, Outsourced FM is the fastest-growing option through 2031, driven by bundled energy-management clauses that link contractor remuneration to kWh reductions, thereby aligning incentives.

In-house teams persist among select government agencies but face pressure to modernize. Without predictive maintenance tools and ESG dashboards, their costs rise and availability metrics slip, nudging agencies toward competitive tenders. Consequently, the Saudi Arabia facility management market industry sees a steady pipeline of first-time outsourcing conversions across ministries and state-owned enterprises.

By End-User Industry: Services-Led Economy Raises Commercial Demand

Commercial properties generated 26.73% of 2025 revenue as corporate relocations to Riyadh and Jeddah spurred fresh demand for premium workplace solutions. Retail complexes such as Arabian Centres’ Jawharat developments roll together shopping, entertainment and warehouses inside one footprint, raising complexity and boosting FM ticket sizes. The Saudi Arabia facility management market share for Commercial buildings is expected to hold steady even as Industrial sites accelerate.

Healthcare facilities are projected to post a 9.68% CAGR through 2031. Saudi Aramco’s USD 25 billion Jafurah gas program and USD 9 billion of local EPC awards are all dependent on rigorous maintenance regimes. Manufacturing gains momentum through joint ventures like TK Elevator’s EUR 160 million local plant, which will require on-site monitoring, logistics support, and safety services.

Geography Analysis

The Western region anchors the Saudi Arabia facility management market, supported by Jeddah’s multimodal port, the Haramain rail link and Red Sea Global’s sustainable tourism cluster. ESG-driven procurement rules, highlighted by a 91/100 GRESB score, amplify demand for zero-carbon operations across 50 resorts and related marinas]. Providers must navigate luxury hospitality standards alongside Mostadam requirements, magnifying opportunities for those with hotel-grade housekeeping, marine maintenance and waste-to-energy capabilities.

The Eastern Province is the nation’s industrial epicenter. Saudi Aramco’s unconventional gas extraction at Jafurah needs predictive maintenance, pipeline monitoring and camp facilities, tasks that raise the region’s contract volume; energy savings already hit 40% after digitization of major plants. Municipal modernization schemes in Dammam add non-oil opportunities, particularly water PPPs and smart-city initiatives that demand integrated IT-OT frameworks.

Riyadh in the Central region experiences the fastest structural change. International firms rushed to set up regional headquarters after SEZ incentives took effect, swelling demand for corporate campuses and data-center management. The King Salman International Airport extension, the capital’s metro and financial district all rely on advanced FM dashboards that ensure 24×7 asset visibility. Collectively, these trends ensure that the Saudi Arabia facility management market maintains geographic diversity, cushioning providers from single-city exposure risk.

Competitive Landscape

The Saudi Arabia facility management market remains moderately fragmented but shows rapid consolidation around technology leaders. Dussmann Group, ENGIE Solutions and Emcor leverage global procurement and IoT platforms tosecure multi-asset contracts, while Musanadah, SETE Energy Saudia and Almajal G4S defend share via localized expertise and high Saudization ratios. International entrants draw strength from predictive analytics, energy dashboards and ESG reporting toolsets that smaller domestic competitors cannot yet replicate. Privatization of 38 government agencies and rising preference for outcome-based agreements redirect procurement toward bidders with robust balance sheets and performance guarantees, accelerating merger activity among mid-tier firms.

White-space niches appear in healthcare, smart logistics hubs and renewable-powered campuses, where specialized certifications provide defensible barriers. Musanadah’s ISSA membership for hospital cleaning signals credentials increasingly decisive in contract wins. IoT pure-plays offering cloud-native CMMS solutions are early disruptors but must partner with heavyweights to navigate working-capital cycles and Saudization rules. As top five players move toward 50% combined revenue by 2030, differentiation hinges on scaling local talent pipelines, integrating AI-driven analytics and demonstrating hard ESG outcomes.

Saudi Arabia Facility Management Industry Leaders

SETE Energy Saudia for Industrial Projects Ltd (SETE Saudia)

ZOMCO (Zamil Operations and Maintenance)

Almajal G4S

Initial Saudi Group

EFSIM Facilities Management Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TK Elevator and Alat unveiled a EUR 160 million venture to localize elevator and escalator production, backing large mixed-use projects in the Kingdom.

- January 2025: Saudi Aramco issued USD 9 billion in locally executed contracts, expanding the addressable industrial facilities base for FM providers.

- January 2025: NEOM awarded a SAR 20 billion dam package at Trojena, underscoring the scale of future maintenance demand within the mountainous resort zone.

Saudi Arabia Facility Management Market Report Scope

Facility management services involve building upkeep, utilities, maintenance operations, waste services, and security. These services are divided into hard and soft facility management services. Hard services comprise mechanical and electrical maintenance, fire safety and emergency services, building management system controls, elevator and lift maintenance, and conveyor maintenance. Soft services include cleaning, recycling, security, pest control, handyperson services, ground maintenance, and waste disposal.

The Saudi Arabia facility management market is segmented by service type (hard service (asset management, MEP and HVAC services, fire systems and safety, and other hard FM services), soft services (office support and security, cleaning services, catering services, and other soft FM services)), offering type (in-house, outsourced [single FM, bundled FM, integrated FM]), and end-user industry (commercial and retail and restaurants, manufacturing and industrial, government, infrastructure and public entities, institutional, and other end-user industries), region (Riyadh, Makkah, Eastern Province, Rest of Saudi Arabia). The Report Offers the Market Size in Value Terms in USD for all the Abovementioned Segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size and projected value of the Saudi Arabia facility management market?

The Saudi Arabia facility management market size is USD 54.56 billion in 2026 and is forecast to reach USD 78.46 billion by 2031, reflecting a 7.54% CAGR.

Which service category holds the largest share today?

Hard services lead with 54.59% of 2025 revenue, underpinned by the Kingdom’s extensive infrastructure and MEP requirements.

Which service segment is expanding the fastest?

Soft services are growing at a 8.12% CAGR through 2031 as clients prioritize premium cleaning, security and workplace support across new commercial hubs.

How dominant is outsourcing in this market?

Outsourced agreements capture 59.36% of 2025 revenue and are rising at a 8.34% CAGR, propelled by PPP legislation and demand for integrated, single-provider contracts.

What technology capabilities most influence contract awards?

IoT-enabled predictive maintenance and enterprise asset-management platforms illustrated by the 100,000-asset IBM Maximo deployment in Riyadh now play a decisive role in winning large-scale tenders.

Page last updated on: