Middle East Facility Management Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

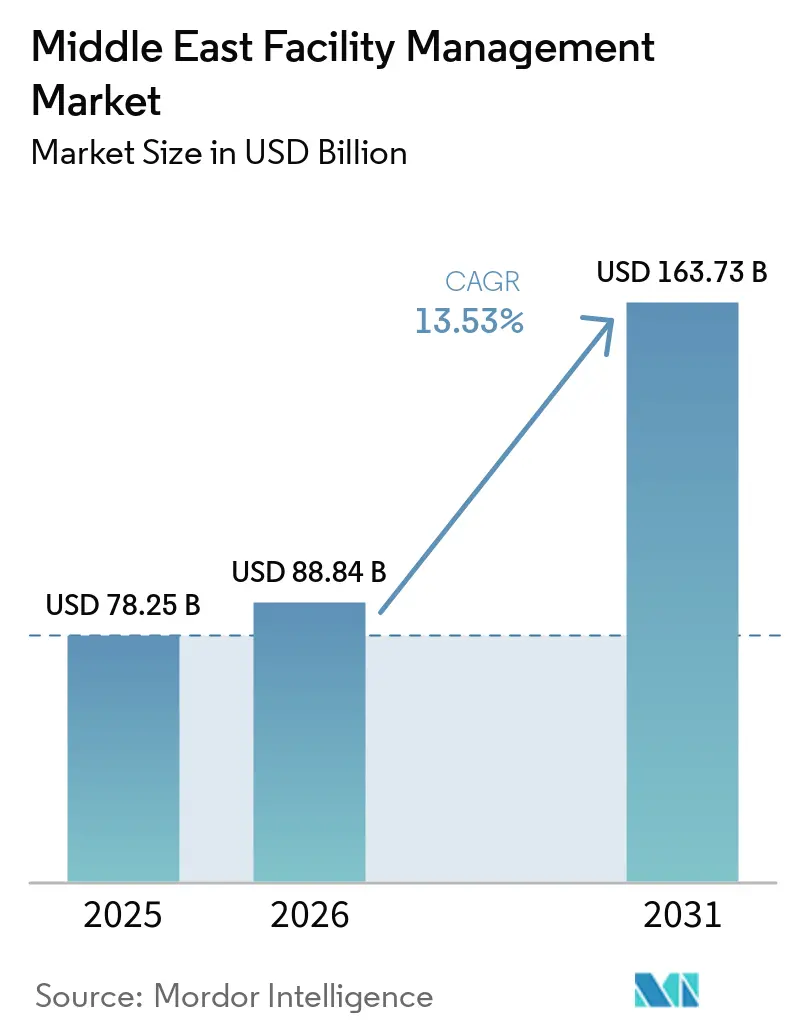

| Base Year Market Size (2025) | USD 78.25 Billion |

| Market Size (2026) | USD 88.84 Billion |

| Market Size (2031) | USD 163.73 Billion |

| Growth Rate (2026 - 2031) | 13.53% CAGR |

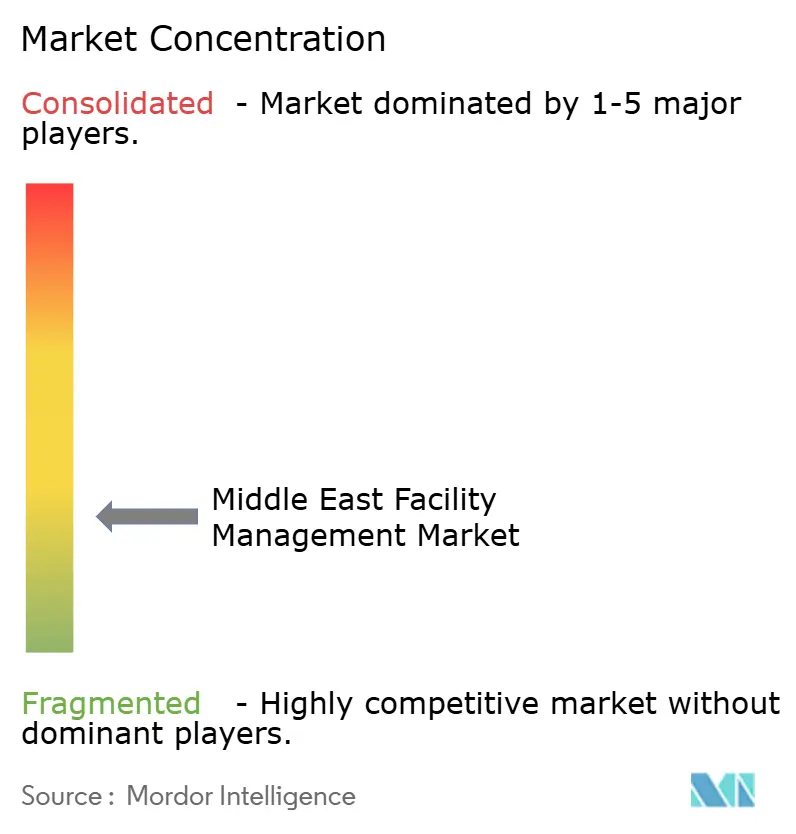

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Facility Management Market Analysis by Mordor Intelligence

The Middle East facility management market size is projected to expand from USD 78.25 billion in 2025 and USD 88.84 billion in 2026 to USD 163.73 billion by 2031, registering a CAGR of 13.53% between 2026 and 2031. The Middle East facility management market is outpacing global growth, transitioning from construction to long-term operations in sectors such as commercial, hospitality, healthcare, and public assets. Economic diversification in the Gulf is fueling this demand, as new assets in real estate, transport, utilities, and tourism now necessitate structured maintenance and lifecycle management post-handover. Developers and public entities are increasingly favoring outsourced and integrated models, seeking fewer vendors, clearer accountability, and measurable performance across their asset portfolios. ESG compliance is now integral to contract design, with owners closely monitoring emissions, energy use, and building performance in line with emerging regulations. Despite challenges such as price-driven tendering, labor shortages, and cybersecurity risks in connected buildings, the market thrives on a robust pipeline of newly operational assets and a growing appetite for tech-enabled services.

Key Report Takeaways

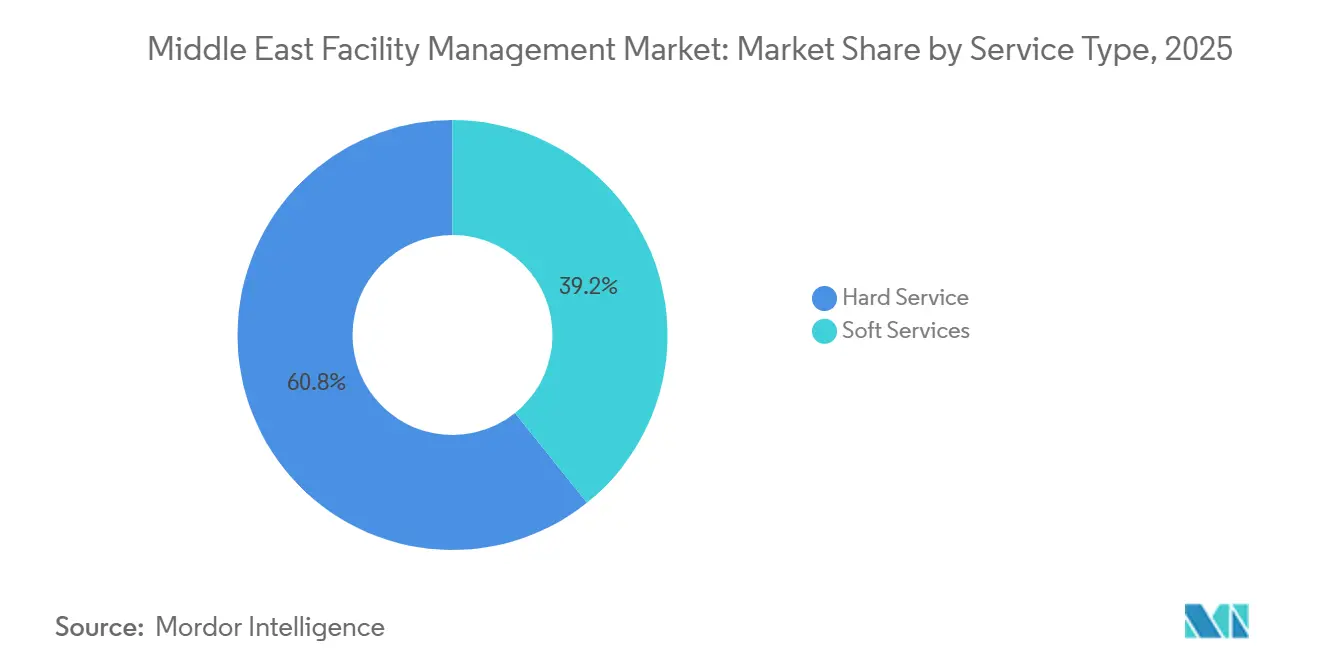

- By service type, hard services held 60.76% share of the Middle East facility management market size in 2025, while soft services are forecast to expand at a 14.76% CAGR through 2031.

- By offering type, outsourced delivery held 68.65% share of the Middle East facility management market size in 2025, while integrated facility management is forecast to grow at a 14.98% CAGR through 2031.

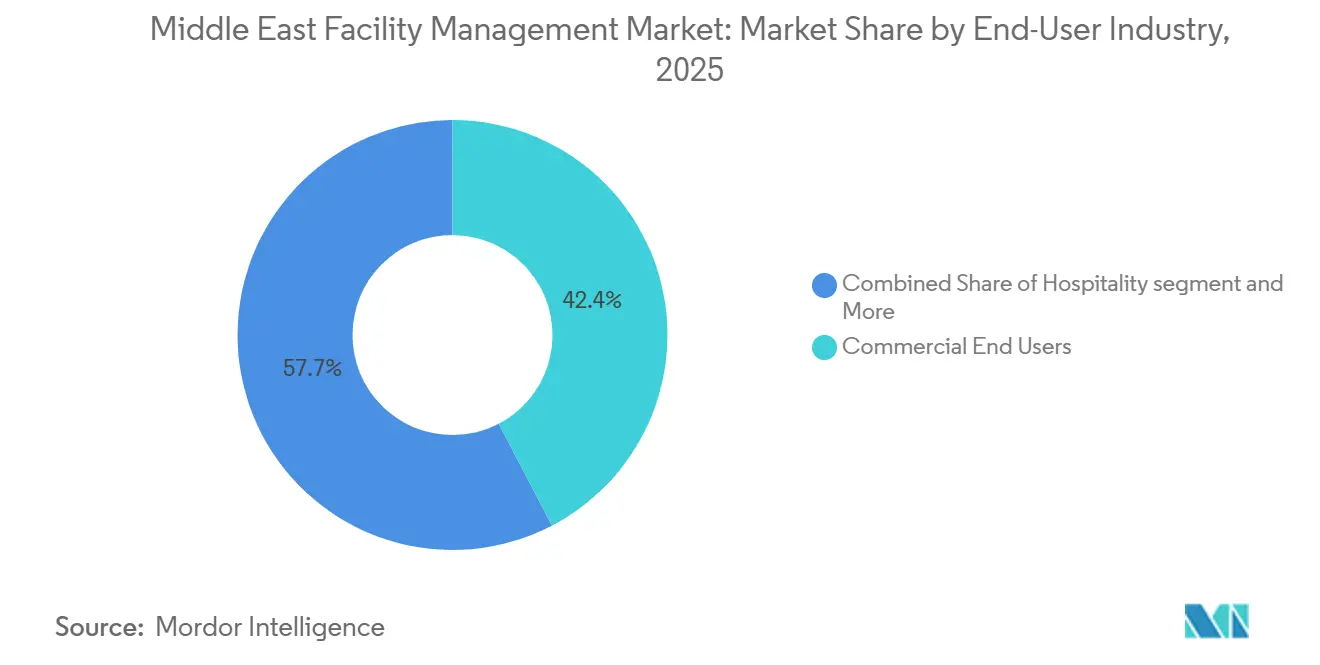

- By end-user industry, commercial assets accounted for 42.35% share of the Middle East facility management market size in 2025, while the industrial and process segment is projected to advance at a 16.85% CAGR through 2031.

- By geography, Saudi Arabia held 38.00% of the Middle East facility management market share in 2025, while Bahrain is forecast to record the fastest CAGR at 17.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 And Giga-Project Asset Handovers | +4.2% | Saudi Arabia primarily, spillover to the UAE and Bahrain | Short term (≤ 2 years) |

| Outsourcing Shift Toward Integrated And Outcome-Based Contracts | +2.8% | GCC-wide, led by Saudi Arabia and the UAE | Medium term (2-4 years) |

| Smart-Building, CAFM, And Predictive Maintenance Adoption | +2.1% | UAE core, spillover to Saudi Arabia and Bahrain | Medium term (2-4 years) |

| Energy-Efficiency And Green-Building Compliance Demand | +1.5% | UAE and Saudi Arabia primary, broader GCC secondary | Long term (≥ 4 years) |

| Mission-Critical FM Demand From Data Centers And Digital Infrastructure | +1.2% | UAE, especially Abu Dhabi and Dubai, and Saudi Arabia, especially Riyadh | Short term (≤ 2 years), Medium term (2-4 years) |

| Commissioning-To-Operations Soft-Landing Needs In Mega Developments | +0.9% | Saudi Arabia, especially NEOM, Diriyah, Red Sea, and Qiddiya | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 And Giga-Project Asset Handovers

Saudi Arabia's transition from construction to operational asset management is reshaping the Middle East's facility management landscape, particularly across its ambitious giga-projects. With a project pipeline surpassing USD 1 trillion, initiatives like NEOM, Red Sea Global, and King Salman International Airport are not just milestones but catalysts. Each handover amplifies the demand for services ranging from engineering support to lifecycle oversight.[1]International Facility Management Association, “From Reactive to Predictive,” FMJ Magazine, fmj.ifma.org This evolution underscores a pivotal shift: post-occupancy work now extends into long-term service contracts, aligning with the asset's entire lifecycle. Furthermore, as handovers occur, developer expectations evolve. There is a pronounced shift towards partners adept at managing data, ensuring uptime, and meeting performance targets. NEOM, for instance, emphasizes advanced requirements such as digital twin integration and ongoing data exchange, setting a high bar for vendors lacking robust digital capabilities. Consequently, as these projects evolve, larger, tech-savvy providers are poised to dominate the Middle East's facility management arena, reaping the rewards of their strategic positioning.

Outsourcing Shift Toward Integrated And Outcome-Based Contracts

In the Middle East, the facility management market is witnessing a notable shift. Traditionally, contracts were often fragmented, focusing on single services. However, there is a clear trend moving towards outsourced and integrated solutions. By 2025, a significant 68.65% of the market revenue was generated from outsourced deliveries, highlighting its dominance, especially for large assets in the region. What is evolving is the format of these contracts. Owners are now favoring a singular provider capable of managing everything, from hard and soft services to sustainability needs and reporting duties. This trend is particularly pronounced in mega-projects and government-linked procurements. Here, tenders are increasingly emphasizing multi-service integration, digital solutions, and tangible results, moving beyond just labor supply. As a result, contracts are not only growing in value but also in duration. There is a marked preference for providers boasting established systems and governance. Even with clients tightening their belts on costs, this shift is broadening the opportunities within the Middle East's facility management landscape.

Smart-Building, CAFM, And Predictive Maintenance Adoption

Building owners in the Middle East are increasingly adopting digital operations in facility management, transitioning from reactive maintenance to predictive service models. At King Abdullah Financial District, AI-driven fault detection and diagnostics led to a 30%-45% reduction in unplanned downtime, underscoring the tangible benefits of digital tools in operations. Imdaad integrated its Computer-Aided Facility Management (CAFM) platform with the Building Management System command center on Oracle Fusion Cloud, achieving a 50% cut in manual efforts across its portfolio. Farnek's deployment of CAFMTEK at Yas Marina Circuit resulted in a 17% decrease in manpower costs and a 30% drop in utility expenses, bolstering the argument for technology-driven service models in high-end assets. These advancements enhance uptime, boost labor productivity, and elevate reporting quality. As connected buildings gain traction and service contracts increasingly incorporate performance clauses linked to data visibility, the Middle East's facility management market is poised for broader digital adoption during the forecast period.

Energy-Efficiency And Green-Building Compliance Demand

Energy performance and green-building compliance are driving heightened demand in the Middle East's facility management market. Buildings, a significant contributor to global energy-related emissions, have seen a surge in investments. The International Energy Agency highlighted this trend, noting a global investment of USD 380 billion in 2024, focusing on building efficiency, electrification, and renewables, underscoring the potential of this burgeoning service sector. In a notable achievement, Etihad ESCO, in Dubai, executed the city's inaugural energy savings performance contract. Over six years, this initiative not only saved 35.2 GWh of electricity but also led to a reduction of nearly 1,452 tonnes of carbon dioxide. Meanwhile, in Bahrain, the Electricity and Water Authority, in 2025, broadened its Kafa’a program. Now encompassing 20 government and 14 private buildings, the program aims for an ambitious target: 308 GWh in electricity savings and a reduction of almost 154,000 tonnes of emissions by 2040. Highlighting the growing importance of regulations, the UAE’s Federal Decree-Law No. 11 of 2024 mandates significant-emission operators to monitor, report, and curtail greenhouse gas emissions. As a result, facility management contracts are evolving. They're increasingly viewed as instruments for compliance, energy monitoring, and performance evaluation, moving beyond their traditional role of mere routine maintenance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-Driven Tendering And Margin Compression | -1.5% | GCC-wide, most acute in Saudi Arabia public-sector tenders | Short term (≤ 2 years), Medium term (2-4 years) |

| Skilled Labor Shortages And Nationalization Pressures | -1.3% | Saudi Arabia, the UAE, and the wider GCC | Medium term (2-4 years), Long term (≥ 4 years) |

| Cybersecurity And System-Interoperability Risk In Connected Buildings | -0.8% | UAE, Saudi Arabia, and data center-heavy markets | Medium term (2-4 years), Long term (≥ 4 years) |

| Public-Sector Payment Delays And Multi-Agency Procurement Friction | -0.6% | Saudi Arabia, Kuwait, and broader public-sector markets across the GCC | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Driven Tendering And Margin Compression

In the Middle East facility management market, public-sector and large developer contracts often favor the lowest bid, creating a recurring pricing challenge. Mid-tier providers grapple with this issue, as they juggle labor, compliance, and technology costs while contending with aggressive pricing in standardized service lines. The immediate fallout is diminished margins, but the broader consequence is a hesitance to invest in platforms, automation, and predictive maintenance. This dynamic results in a divided market: well-capitalized operators chase premium contracts, while smaller firms find themselves anchored to labor-intensive tasks, stifling their potential for innovation. Furthermore, price-driven procurement complicates the transition to outcome-based service models, even when the benefits of long-term lifecycle savings are evident. Without a shift in procurement frameworks towards prioritizing quality, uptime, and performance metrics, the Middle East facility management market will struggle to elevate its value.

Skilled Labor Shortages And Nationalization Pressures

The Middle East facility management market also faces labor pressure as localization rules expand at the same time that technical demand rises. Saudi Arabia and the UAE are both pushing stronger national workforce participation, which raises compliance expectations for employers across engineering, technical, and support roles. That shift matters because the sector still relies heavily on expatriate labor, especially in MEP, HVAC, and other specialist maintenance disciplines. Replacing or rebalancing that workforce is not simple, since the training pipeline for certified technicians and site-ready supervisors is still catching up with the scale of new asset demand. Providers therefore face higher staffing costs, tighter recruitment conditions, and greater contract execution risk in labor-intensive mandates. Over time, this constraint will favor operators with stronger training systems, deeper bench strength, and better ability to manage workforce planning across multiple countries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Holds The Core Revenue Base While Soft Services Expand Fast

In 2025, hard services accounted for 60.76% of the Middle East's facility management market, underscoring the region's engineering-centric asset base. Gulf commercial towers, hospitals, airports, hotels, industrial sites, and mixed-use developments rely heavily on MEP systems, HVAC, fire safety, and asset performance support. Given the region's climate, there is heightened demand on cooling and mechanical systems, leading to more frequent maintenance cycles and costlier failures compared to milder climates. The specification of new projects increasingly incorporates asset data, commissioning standards, and monitoring obligations into the operating model even before occupancy. A prime example of this evolution is NEOM’s digital twin requirement, linking hard-service responsibilities with real-time asset visibility and long-term performance management.

Soft services are emerging as the quicker-growing segment of the Middle East's facility management market, boasting a projected CAGR of 14.76% through 2031. This growth is buoyed by an expanding hospitality sector, outsourcing in education and government campuses, and a broader demand for cleaning, security, catering, and workplace support. Demonstrating the industry's shift, Farnek introduced a hybrid cleaning unit that merges human teams with autonomous robotic cleaners, achieving coverage of up to 5,000 sq ft per hour. Emrill’s sustainability initiative, with 143 continuous improvement measures in 2024, successfully reduced emissions by 640 tCO2e and conserved 2.25 million liters of water, highlighting the trend of bundling soft services with environmental performance commitments rather than confining them to routine tasks.[2]Emrill Services LLC, “Emrill Announces Five-Year Achievements as Part of Its Continued Growth and Transformation Journey,” Emrill Services LLC, emrill.com

By Offering Type: Outsourcing Leads While Integrated FM Redefines Contract Value

In 2025, the Middle East's facility management market saw 68.65% of its operations shift to outsourced delivery. This marks a notable pivot from the traditional in-house model, favored by major regional asset owners. Clients are increasingly outsourcing, not merely for convenience, but to harness technical expertise, streamline vendor coordination, maintain stringent reporting standards, and expand service coverage, all without the burden of developing these capabilities internally. Among the diverse outsourcing formats, integrated facility management is leading the pack, with a projected CAGR of 14.98% through 2031. This growth is primarily due to asset owners' preference for a consolidated approach, merging hard services, soft services, compliance reporting, and energy management under a single contract. In essence, integrated FM is climbing the value hierarchy in the Middle East's facility management arena, providing clients with a singular operator for performance metrics, a cohesive tracking framework, and an efficient escalation route.

Despite the rise of integrated FM, single FM and bundled FM remain pivotal, especially for clients venturing into outsourcing or those with a service-specific procurement strategy. Retail facilities, warehouses, and certain mid-market commercial properties often take a gradual approach, incrementally adding services instead of jumping into full integration. Yet, contract designs are shifting, leaning towards providers ready to broaden their offerings as clients evolve in their outsourcing journey. This trend bolsters the competitive advantage for firms with vast operating platforms. On the other hand, the in-house segment retains its dominance in mission-critical environments, where direct oversight on uptime, resilience, and security is paramount. Highlighting this inclination, Khazna's 2026 launch of Khazna NexOps signals that some data center operators prioritize developing specialized internal capabilities, especially when asset criticality is at stake.

By End-User Industry: Commercial Assets Lead While Industrial Demand Builds Fast

In 2025, commercial end users dominated the Middle East facility management market, holding a 42.35% share. These users spanned sectors like IT and telecom, retail, warehousing, and office-led mixed-use assets. The expansion of regional headquarters in Dubai and Riyadh, coupled with a burgeoning logistics real estate sector, has bolstered the demand for high-specification maintenance, workplace support, fire safety, and energy management in commercial buildings. Warehousing and expansive logistics nodes present a unique operational profile, necessitating varied service intensities across MEP systems, fire suppression, access control, and loading infrastructure. This extensive footprint positions commercial assets at the forefront of contract volumes, driving a significant portion of recurring service revenue in the Middle East's facility management landscape. Consequently, providers boasting flexible multi-site operating models find themselves better equipped to manage portfolios spanning office, retail, and logistics sites.

Forecasted to grow at a CAGR of 16.85% through 2031, the industrial and process segment is outpacing all other end-user groups in the Middle East facility management industry. This segment demands specialized O&M capabilities, as any downtime in sectors like oil and gas, mining, logistics, and advanced manufacturing can have immediate repercussions on production and safety. As a result, the demand profile here is more technical, highly sensitive to uptime, and less forgiving of service interruptions compared to standard commercial contracts. A testament to this trend, Farnek’s HITEK subsidiary clinched a contract tied to Maaden operations in 2024, underscoring the industrial sector's preference for providers that meld technical expertise with digital monitoring capabilities. Meanwhile, healthcare and hospitality sectors are also on the rise. Hospitals are emphasizing stringent controls over sterile environments, medical gases, and infection-related systems. At the same time, hotels are expanding their focus on both guest-facing soft services and energy-conscious hard services.

Geography Analysis

In 2025, Saudi Arabia commanded a dominant 38.00% share of the Middle East's facility management market, solidifying its position as the leading national contributor to regional demand. The country's vastness mirrors the magnitude of its real estate, infrastructure, tourism, and industrial sectors, especially as its ambitious giga-projects transition from mere construction to active occupancy and operations. This shift not only extends the revenue timeline for service providers but also pivots contract focus toward uptime, lifecycle asset care, compliance, and service quality post-handover. However, the Saudi market is evolving, with heightened standards for participation in major contracts, emphasizing licensing, localization, and digital capabilities. Thus, Saudi Arabia stands as the primary driver of contract growth and a testing ground for integrated operational models in the Middle East's facility management landscape.

Meanwhile, the United Arab Emirates (UAE) has emerged as the region's frontrunner in technology-driven and sustainability-focused service delivery within the facility management arena. The UAE's stringent climate laws are forging a closer link between building operations and emissions accountability, elevating the importance of energy performance and reporting in contract negotiations. A testament to this is Dubai's inaugural energy savings performance contract, underscoring the market's capability to convert efficiency initiatives into tangible electricity savings and reduced carbon footprints at the asset level. Emrill, a key player, boasted a 9% revenue uptick in 2025, bolstered by over 70 new contracts, expanding its portfolio to 265 active contracts, a clear indicator of robust demand in hospitality and digitally managed services.[3]Emrill Services LLC, “Emrill Reports 9% Revenue Growth in 2025, Exceeding Annual Targets,” Emrill Services LLC, emrill.com Thus, the UAE cements its status as the region's premier market for platform-centric FM delivery, intelligent maintenance, and compliance-driven service design.

Bahrain is emerging as the fastest-growing market in the Middle East's facility management sector, eyeing a robust CAGR of 17.01% through 2031. This surge is fueled by a swift embrace of integrated models and a concerted policy emphasis on building efficiency and curbing emissions. Notably, the 2025 expansion of the Kafa’a program to encompass both government and private buildings offers FM providers and ESCO-linked operators a tangible avenue to enhance project pipelines centered on performance improvements. Meanwhile, other regional players are witnessing gradual growth as sustainability standards, modernization of public assets, and professional outsourcing gain traction across national markets.

Competitive Landscape

In the Middle East facility management market, while the landscape remains moderately fragmented, larger players are gaining a distinct advantage, particularly in premium integrated contracts. Major operators such as Emrill, EFS Facilities Services, Farnek, Imdaad, and state-linked platforms are effectively competing, especially where clients prioritize digital systems, multi-service execution, and robust governance. On the other hand, smaller firms, active in cleaning, security, and routine maintenance, grapple with margin pressures in labor-intensive tasks and find it challenging to invest in advanced platforms or service models. This gap is widening as larger portfolios increasingly value in-depth reporting, uptime control, sustainability tracking, and transparent contracts. Consequently, while the Middle East facility management market remains fragmented in terms of company count, it is consolidating based on capabilities.

Technology stands out as a pivotal differentiator in this competitive arena. Farnek’s HITEK platform has facilitated connected operations in thousands of buildings, and its CAFMTEK deployment at Yas Marina Circuit has yielded notable improvements in labor and utility efficiency. Emrill’s Techsphere ecosystem efficiently tracks a vast array of assets and manages maintenance digitally across its contracts. Imdaad’s integration of CAFM and BMS has reduced manual efforts by 50%, underscoring how top providers leverage software and command-center visibility for operational advantages. In this segment of the Middle East facility management market, buyers are increasingly favoring platforms over traditional service vendors.

Strategic maneuvers since 2025 highlight firms' positioning for the forthcoming competitive phase.[4]BEEAH Group, “BEEAH Launches Facilities Management Services for the Next Era,” BEEAH Group, beeahgroup.com BEEAH introduced a new FM service line, merging hard services with eco-friendly soft services, CAFM monitoring, and environmental management, steering its offerings toward net-zero-ready operations. In Saudi Arabia, OPTIMA and FMTECH's strategic alliance aims to provide technology-driven FM solutions spanning O&M, utilities, and consulting, signaling a growing appetite for structured local capabilities intertwined with digital planning. Khazna’s unveiling of NexOps in mission-critical data centers hints that such specialized environments might foster distinct service models, separate from mainstream outsourcing. These developments indicate that the future frontrunners in the Middle East facility management arena will be those adept at harmonizing local execution scale, digital oversight, and regulatory compliance.

Middle East Facility Management Industry Leaders

EFS Facilities Services Group LLC

Emrill Services LLC

Farnek Services LLC

Imdaad LLC

Khidmah LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Shalfa Facilities Management signed a contract worth SAR 52,101,511 (USD 13.9 million) for integrated FM services with the National Water Company. This agreement, covering NWC buildings in Saudi Arabia's southern sector, spans 36 months, with financial impacts anticipated from H2 2026.

- January 2026: Emrill announced a 9% revenue increase in 2025, surpassing its annual targets. This growth resulted from securing over 70 new contracts, expanding its active portfolio to over 265. The hospitality sector's expansion was identified as a key driver, and Emrill's Techsphere digital platform successfully completed over 2 million maintenance tasks.

- October 2025: BEEAH, a prominent player in the environmental sector, unveiled its new FM services. These services seamlessly blend environmental expertise with traditional offerings such as HVAC and safety infrastructure. Additionally, BEEAH emphasizes eco-friendly soft services, advanced environmental management, and utilizes cutting-edge technologies such as AI and IoT. Their operations, now net-zero-ready, span across the UAE, Saudi Arabia, and Egypt.

- August 2025: In a significant move, OPTIMA and FMTECH joined forces, forging a strategic partnership. Their collaboration aims to roll out integrated, tech-driven FM solutions throughout Saudi Arabia. By merging OPTIMA's expertise in FM strategy and data-centric operations with FMTECH's robust national infrastructure and ISO-certified systems, they cover a wide spectrum from energy management to consulting services.

- February 2025: In 2024, Farnek secured contracts valued at over AED 690 million (USD 187.9 million) across 460+ engagements. This portfolio included AED 240 million (USD 65.4 million) in new business in Abu Dhabi, with notable projects spanning Zayed Sport City, Etihad Airways Engineering, and the Barakah Nuclear Power Plant. Additionally, the company bolstered its workforce, expanding its total headcount to over 9,000 employees.

Middle East Facility Management Market Report Scope

The Middle East Facility Management Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-house, Outsourced [Single FM, Bundled FM, Integrated FM]), End-user Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Others), and Geography (Saudi Arabia, UAE, Kuwait, Bahrain, Rest of Middle East).

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| Saudi Arabia |

| United Arab Emirates |

| Kuwait |

| Bahrain |

| Rest of Middle East |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Region | Saudi Arabia | |

| United Arab Emirates | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the size of the Middle East facility management market in 2026?

The Middle East facility management market stands at USD 88.84 billion in 2026 and is forecast to reach USD 163.73 billion by 2031, growing at a CAGR of 13.53%.

Which service category leads demand in the region?

Hard services led in 2025 with 60.76% of total revenue because MEP, HVAC, fire safety, and asset management remain central across engineering-heavy properties.

Which service segment is expanding the fastest?

Soft services such as cleaning, security, and catering are growing at a 14.76% CAGR due to workplace automation and higher hygiene standards.

Which offering model is expanding the fastest across the Middle East?

Integrated facility management is the fastest-growing offering type, with a forecast CAGR of 14.98% through 2031 as owners seek single-accountability contracts.

Which end-user group is creating the strongest new growth opportunity?

The industrial and process segment is expected to grow at a 16.85% CAGR through 2031, supported by oil and gas, mining, logistics, and manufacturing facilities that require high-uptime operations.

Which country leads regional demand for facility management services?

Saudi Arabia held 38.00% of regional revenue in 2025, making it the largest country market as giga-projects move into occupancy and operations.

Why is ESG becoming more important in building operations across the Gulf?

Owners and operators are facing stronger pressure to monitor emissions, improve efficiency, and maintain post-occupancy performance, which is turning FM contracts into compliance and reporting tools as well as service agreements.

Page last updated on: