Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

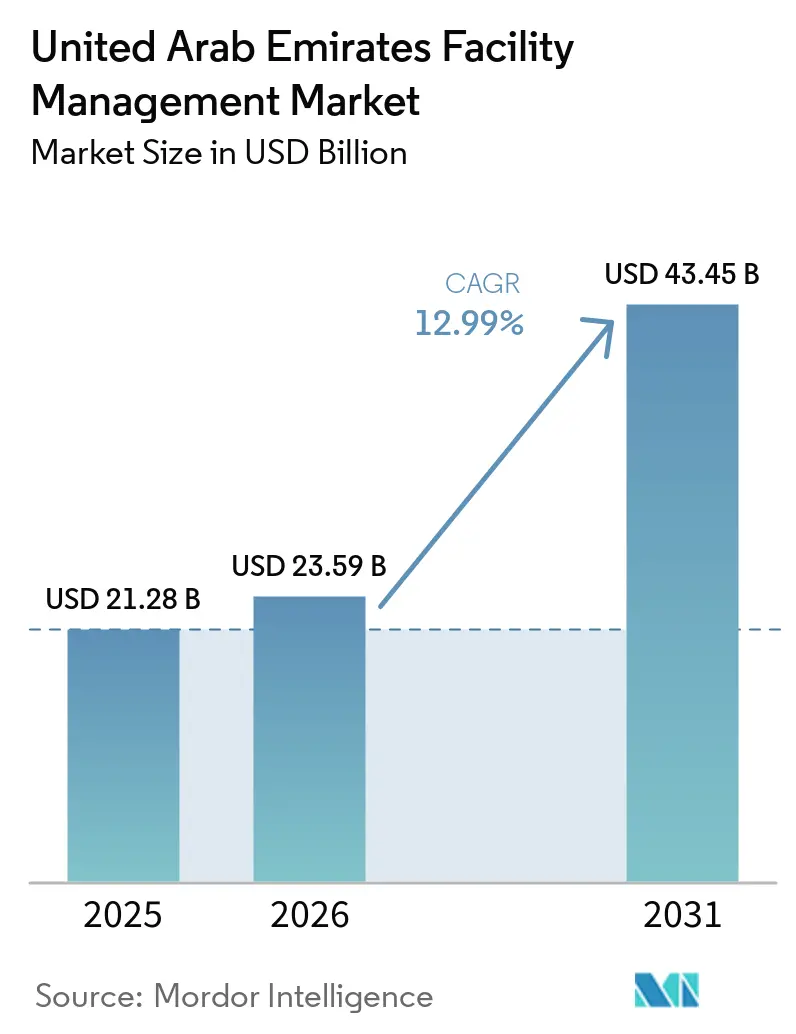

| Base Year Market Size (2025) | USD 21.28 Billion |

| Market Size (2026) | USD 23.59 Billion |

| Market Size (2031) | USD 43.45 Billion |

| Growth Rate (2026 - 2031) | 12.99% CAGR |

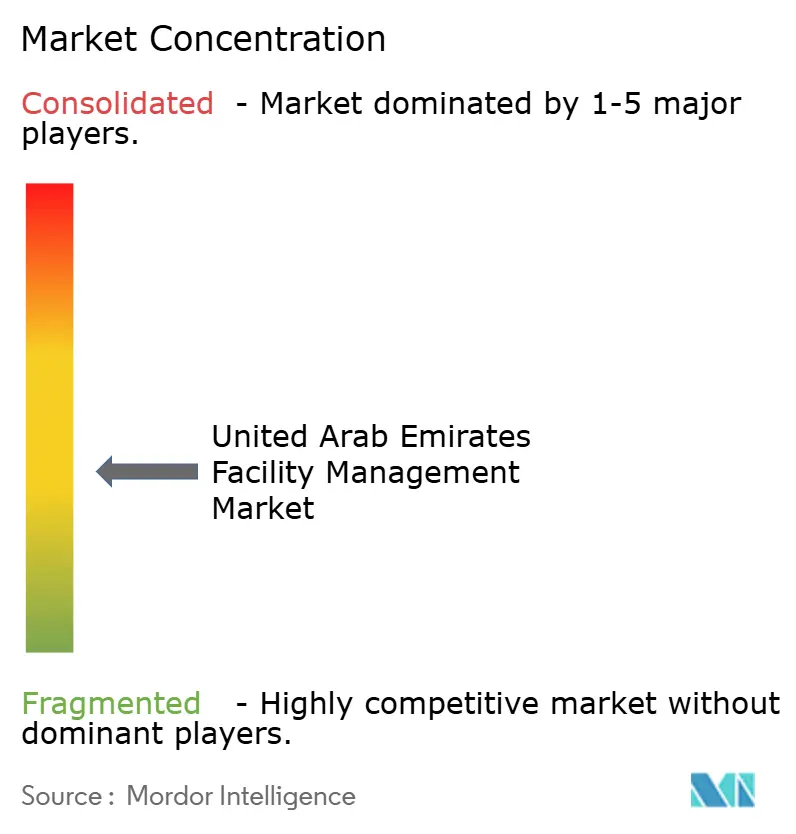

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Facility Management Market Analysis by Mordor Intelligence

The United Arab Emirates Facility Management Market size is projected to expand from USD 21.28 billion in 2025 and USD 23.59 billion in 2026 to USD 43.45 billion by 2031, registering a CAGR of 12.99% between 2026 to 2031.

This growth trajectory is underpinned by large-scale smart-city investments, mandatory sustainability codes and rapid technology adoption that collectively elevate facility management from a cost centre to a strategic pillar of the national diversification plan. The drive toward intelligent buildings is visible in flagship assets such as Burj Khalifa, where an IoT platform cut maintenance hours by 40% while pushing asset reliability close to 99.95%. Parallel advances in district cooling and energy analytics are optimising resource use, trimming operational expenditure and enabling compliance with the UAE Climate Law’s strict emissions mandates. Population growth to a projected 5.8 million in Dubai by 2040 magnifies demand for seamless building services, while an USD 100 billion national infrastructure pipeline opens new revenue pools for providers. Intensifying competition is shifting the UAE facility management market towards integrated, outsourced solutions that offer economies of scale and unified data visibility across hard and soft services.

Key Report Takeaways

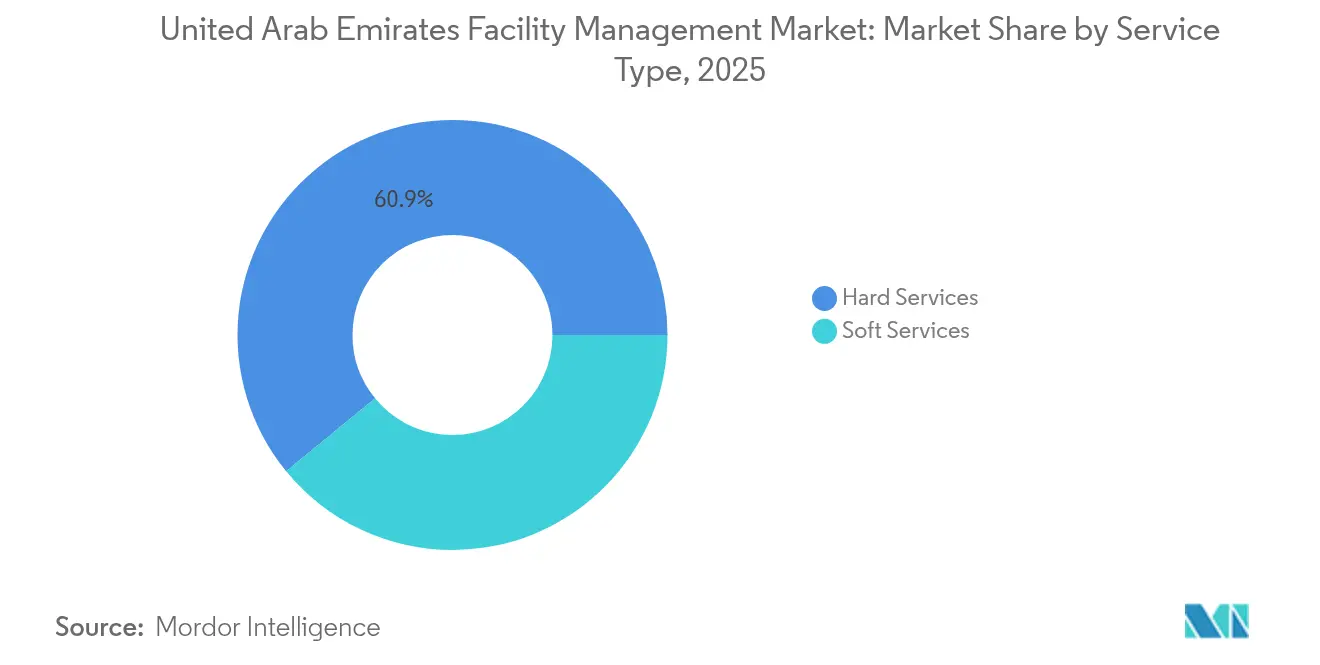

- By service type, hard services held 60.92% of the UAE facility management market share in 2025. Soft services are projected to grow at a 12.33% CAGR through 2031.

- By offering type, outsourced models controlled 64.88% of the UAE facility management market size in 2025 and are advancing at a 12.21% CAGR.

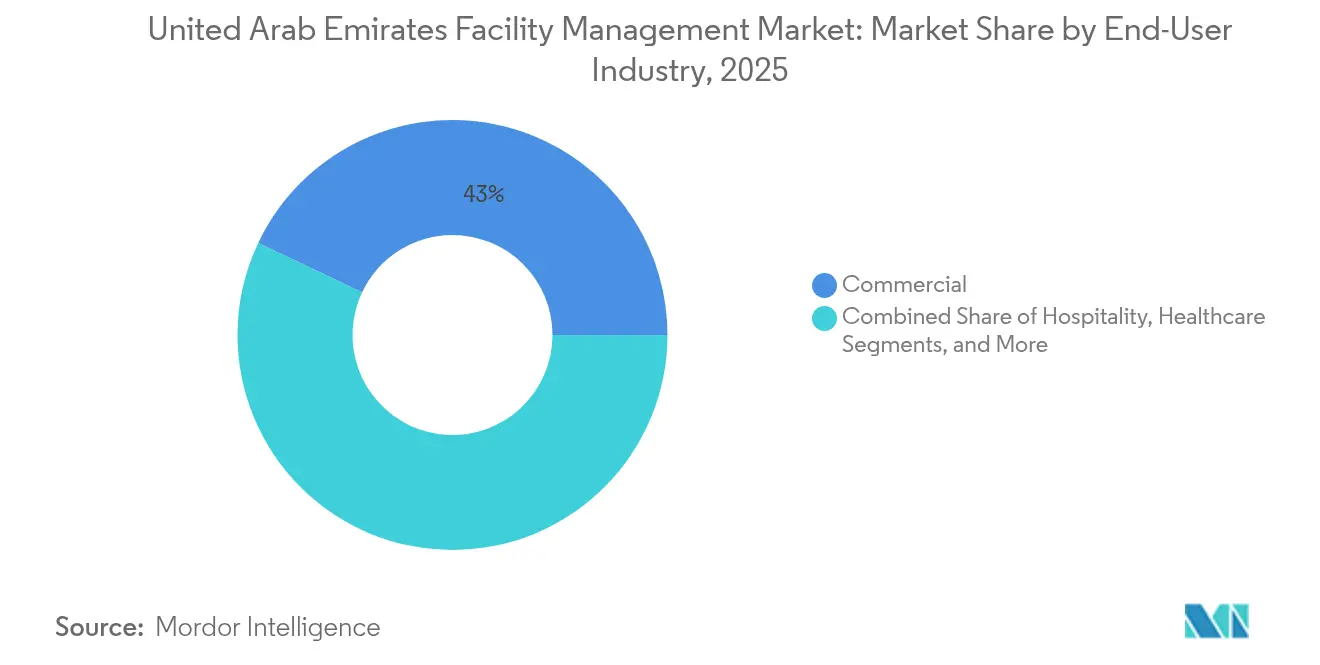

- By end-user industry, commercial facilities captured 42.96% of revenue in 2025, while healthcare is forecast to expand at a 12.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological integration: AI and IoT | +2.8% | Dubai, Abu Dhabi, spill-over to Northern Emirates | Medium term (2–4 years) |

| Sustainability initiatives and compliance | +2.1% | National, early gains in Dubai, Abu Dhabi, Sharjah | Long term (≥ 4 years) |

| Healthcare sector expansion | +1.9% | Dubai, Abu Dhabi, expansion to Sharjah | Short term (≤ 2 years) |

| Urbanisation and megaproject pipeline | +2.4% | Dubai, Abu Dhabi, secondary growth in Ajman, RAK | Medium term (2–4 years) |

| Outsourced and integrated FM adoption | +1.6% | Nationwide, business districts | Short term (≤ 2 years) |

| Mandatory energy audits and green retrofits | +1.4% | National, policy focus in Dubai, Abu Dhabi | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Technological Integration: AI and IoT Revolutionising Operations

Smart-building platforms are reshaping the UAE facility management market by embedding predictive maintenance, digital twins and real-time asset monitoring into day-to-day workflows. Enova’s AI-powered virtual assistant, built on Google Cloud’s Gemini model, automates service requests and frees teams for high-value analytics, mirroring a wider shift toward data-rich workflows across energy and facilities portfolios. [1]Enova, “AI-Powered Virtual Assistant Launch,” enova-me.comEmirates Global Aluminium recorded USD 100 million in financial gains after deploying 80 Industry 4.0 use cases that cut downtime by 50% and lifted overall equipment effectiveness by 12%. These gains demonstrate a maturing ecosystem in which facility managers move from reactive maintenance to outcome-based contracts driven by IoT telemetry and machine learning. The UAE’s National Artificial Intelligence Strategy forecasts the domestic AI economy to rise from USD 3.47 billion in 2023 to USD 46.33 billion by 2030, a tailwind that cements technology as the primary catalyst for next-generation service models.

Sustainability Initiatives: Environmental Compliance Driving Innovation

Climate-aligned regulations are accelerating the UAE facility management market toward low-carbon practices. The Federal Decree-Law 11 of 2024 mandates greenhouse-gas monitoring and imposes fines of AED 50,000–2 million (USD 13,612.94–0.54 million) for non-compliance, pushing owners toward sensor-driven energy dashboards and renewable integrations. DEWA’s Al Shera’a net-zero headquarters exemplifies the trend, with digital-twin controls delivering 66% energy and 48% water savings while qualifying for LEED Platinum certification. Complementary frameworks such as Abu Dhabi’s Pearl Rating System ensure that sustainability considerations extend from design through operations. For existing stock, modelling by academic researchers shows that green-retrofit payback periods can fall below eight years while cutting electricity demand by up to 57%, validating the commercial case for investment. [2]Ministry of Energy and Infrastructure, “Clean Energy Investments Surpass AED 45 Billion,” moei.gov.ae

Healthcare Sector Growth: Specialised FM Services in High Demand

Rapid medical-care expansion is reshaping service portfolios in the UAE facility management market. PureHealth posted a 53% jump in H1 2024 revenue to AED 12.5 billion (USD 3.40 billion), on the back of acquisitions such as Circle Health Group and Sheikh Shakhbout Medical City that multiply facility footprints. Burjeel Medical City recorded a 21.8% revenue uplift as patient throughput rose, reinforcing demand for around-the-clock critical-system monitoring and infection-control capable cleaning. Healthcare facilities impose rigorous HVAC, pharmaceutical storage and waste-handling standards, prompting providers to recruit specialised engineers and invest in ISO 41001-compliant quality systems. With a national healthcare workforce of 145,981 across 172 hospitals, scale alone is generating durable contract pipelines for integrated FM suppliers.

Urbanisation and Infrastructure Development: Expanding FM Footprint

Government megaprojects worth USD 100 billion are broadening geographic demand in the UAE facility management market. The Etihad Rail link, Al Maktoum International Airport’s 260 million-passenger capacity plan and the Dubai Metro Blue Line collectively require ongoing asset management once delivered. Dubai’s population is projected to climb from 3.8 million in 2024 to 5.8 million by 2040, stretching existing utilities and boosting requirements for high-performance MEP, security and waste-management services across new housing clusters. Logistics schemes such as Aldar Properties’ 1.55 million sq ft park with DP World further expand the scope for FM providers capable of warehouse automation and energy-efficient lighting

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour-market constraints and Emiratisation | -1.8% | National, acute in Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Price competition and margin pressure | -1.4% | Dubai, Abu Dhabi core markets | Medium term (2–4 years) |

| Rising compliance costs (ISO 41001, green) | -1.2% | National, stronger in Dubai, Abu Dhabi | Medium term (2–4 years) |

| Climate extremes and accelerated degradation | -0.9% | National, high in Northern Emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labour-Market Challenges: Workforce Availability Constraining Growth

Tight labour supply and a phased Emiratisation quota are escalating operating costs in the UAE facility management market. Firms with 50 or more staff must raise Emirati headcount by 2% each year to hit a 10% threshold by 2026 or pay AED 96,000 (USD 26,136.85) per position left vacant, a penalty that squeezes provider margins. Smaller firms with 20–49 workers now must hire one Emirati in 2024 and two in 2025 or face similar fines. [3]Rödl & Partner, “Emiratisation Priorities,” roedl.com Industry polling shows 29% of FM executives already struggle with staff shortages, while 61% expect headcount growth, highlighting a structural supply gap. The simultaneous roll-out of mandatory unemployment insurance and a new savings scheme as an alternative to end-of-service gratuity adds HR complexity for outsourced providers balancing cost optimisation with service-quality metrics.

Market Competition: Price Pressures Affecting Profitability

A fragmented competitive landscape applies downward pressure to contract pricing, particularly in Dubai where property service charges rose up to 10% in 2025, prompting owners to renegotiate FM contracts on leaner budgets. Construction costs in Dubai remain lower than Riyadh or Doha, luring foreign entrants and heightening bidding contests. In response, incumbents such as Imdaad streamline operations; its SAP-Maximo mobile workforce solution was key to winning a three-year Dubai Municipality cleaning tender staffed by 222 personnel. At the developer end, Union Properties consolidated three business units, targeting AED 7 million (USD 1.91 million) annual savings that cascade into tighter FM fee expectations. Providers are therefore compelled to differentiate on technology, sector specialism and ESG compliance rather than on rate cards alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Dominate Despite Soft-Services Momentum

Hard services commanded 60.92% of the UAE facility management market in 2025 due to asset-heavy investments in smart MEP, fire safety and predictive maintenance systems anchored by digital twins and IoT monitors. DEWA’s Al Shera’a headquarters illustrates how advanced sensors and analytics expand the scope of technical upkeep while cutting energy bills, thereby reinforcing demand for specialised engineers. The UAE facility management market size for hard services is projected to maintain a double-digit trajectory as mandatory energy audits and performance-based contracts link payments to measurable outcomes. At the same time, soft services are forecast to post a 12.33% CAGR through 2031 as employers prioritise occupant well-being, hospitality-grade cleaning and AI-enabled security patrols. This creates a convergence path where integrated providers package both service classes under a single SLA, improving cost transparency and delivering real-time KPI dashboards to clients.

The crossover is visible in corporate campuses where AI vision cameras trigger automated work orders to cleaning crews and in hospitals deploying UV-C disinfection robots to meet infection-prevention standards. As a result, soft-services vendors are re-skilling staff for data-driven workflows while hard-services teams partner with OEMs to support remote diagnostics and condition-based part replacements. By 2030, bundled contracts are expected to outpace single-service engagements, further blurring the distinction between technical and non-technical pillars and supporting sustained expansion in the UAE facility management market.

By Offering Type: Outsourced Models Accelerate Through Integrated Solutions

Outsourced service delivery captured 64.88% of the UAE facility management market share in 2025 as corporates sought specialist expertise, KPI-linked contracts and CAPEX-to-OPEX conversions. Integrated facility management is the fastest-growing cohort within outsourced offerings, riding a 12.21% CAGR as decision-makers consolidate single and bundled engagements into one-stop partnerships. Imdaad’s SAP-enabled field-force platform feeds live asset data to both client dashboards and its Maximo CMMS, improving mean-time-to-repair metrics and underpinning multi-year renewals. In-house delivery remains essential in mission-critical sites such as defence, select healthcare and data-centre assets where regulatory or confidentiality needs demand direct control. Nevertheless, hybrid governance models are gaining favour, combining on-site supervision with outsourced labour and analytics platforms that enhance operating-expense transparency.

Technology adoption differentiates outsourced leaders: Enova’s AI-driven chatbots, Farnek’s computer-vision security suite and EFS’s predictive HVAC analytics progressively raise performance benchmarks across the UAE facility management market. As ESG disclosure rules tighten, clients view third-party providers as risk-mitigation partners capable of centralising gas, water and electricity reporting into auditable formats aligned with national climate frameworks. This trend is forecast to translate into longer contract tenures and outcome-based payment structures calibrated against energy-intensity and maintenance-efficiency benchmarks.

By End-User Industry: Healthcare Outpaces Commercial Despite Share Gap

Commercial assets, encompassing office towers, warehouses and retail malls, represented 42.96% of UAE facility management market revenue in 2025 owing to the emirates’ role as a regional business hub. Majid Al Futtaim alone operates 467 Carrefour stores that require 24/7 refrigeration, supply-chain dock control and customer-footfall analytics. Yet sector growth is moderating as hybrid work compresses office utilisation, prompting landlords to re-scope SLAs toward flexible cleaning, dynamic HVAC load balancing and experience-aligned service metrics.

Healthcare facilities are closing the gap, with a projected 12.28% CAGR driven by hospital new-builds, specialist clinics and telemedicine hubs. PureHealth’s aggressive acquisition spree and Burjeel’s double-digit revenue rise exemplify the sector’s capital deployment and resultant demand for high-complexity FM protocols spanning surgical-suite sterility, negative-pressure isolation rooms and redundant power supplies. Integrated providers with healthcare sub-brands are leveraging ISO 15189 awareness and biomedical equipment maintenance competencies to secure multi-site contracts. Looking ahead, increased automation in diagnostic imaging and robotic surgeries will intensify requirements for asset integrity management and cybersecurity-enabled building-management systems, propelling sustained demand within the UAE facility management market.

Geography Analysis

Dubai and Abu Dhabi together anchor the UAE facility management market, accounting for an estimated two-thirds of contract value thanks to concentration of high-rise real estate, government campuses and industrial scale energy assets. Dubai’s 2040 Urban Master Plan channels investments across 50 megaprojects, from Etihad Rail freight stations to the world’s largest airport expansion, each requiring long-term asset care once operational. Elevated migrant inflows raise occupancy rates, heightening demand for residential community management, district cooling optimisation and advanced waste-handling solutions.

Abu Dhabi’s market is buoyed by government and defence court contracts as well as industrial clusters anchored by ADNOC and Emirates Global Aluminium. The emirate’s Pearl Rating System accelerates uptake of green-building-aligned FM services linking occupant health to energy intensity metrics. Upcoming projects such as the AI-powered Aion Sentia city and logistics-hub expansions around Khalifa Port add specialised niches for data-centre and warehouse automation expertise. Together, the two emirates set technology and compliance benchmarks subsequently adopted in Sharjah, Ajman, Ras Al Khaimah and Fujairah, gradually raising the baseline for service delivery nationwide.

Sharjah and the Northern Emirates form the emergent frontier, supported by civic-facility spending that exceeded half of the 2024 federal budget [U.AE]. Bee’ah’s AI-enabled “Office of the Future” demonstrates appetite for high-tech FM even in secondary cities, blending smart lighting, robotic cleaning and real-time carbon dashboards under one BMS. Go-forward growth in these emirates will draw on logistics corridors, free-zone warehousing and utility-scale desalination plants, collectively expanding the geographic spread of the UAE facility management market.

Competitive Landscape

The UAE facility management market is highly fragmented, with more than 50 active medium-to-large providers across hard and soft service lines. Market leaders EFS, Imdaad and Farnek leverage IoT dashboards, mobile workforce apps and sector-specific add-ons to defend share. Imdaad’s successive Dubai Municipality awards underscore scale benefits in public-sector tenders. Farnek’s January 2025 launch of an events-sector unit shows diversification into high-margin verticals, while its hospitality division expansion illustrates tactful portfolio balancing.

Disrupters focus on technology-centric value propositions. Enova’s AIEVA chatbot shortens customer response times and accelerates issue resolution through large-language-model triage, while Serco’s acquisition of sustainability consultancy Climatize deepens ESG-oriented service components. Consolidation trends are likewise evident in catering sub-segments, where ADNH’s purchase of Food Nation positions it to cross-sell FM into education accounts. Expect rising M&A as providers seek geographic coverage, certifications and specialised talent in data-centre and healthcare niches.

Overall, integrated FM capabilities and demonstrable ESG expertise are becoming the differentiators that command premium pricing and multi-year contract renewals. Providers without IoT-enabled platforms risk relegation to commoditised labour categories as clients gravitate toward partners that deliver data-backed performance reporting in line with UAE climate-law disclosure obligations.

United Arab Emirates Facility Management Industry Leaders

EFS Facilities Services Group

Imdaad LLC

Farnek Services LLC

Enova Facilities Management Services LLC

Marafeq Facilities Management LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Farnek launched a dedicated service provider for the UAE events sector

- January 2025: ADNH Catering acquired Food Nation Catering Services to serve more than 70,000 students

- December 2024: ADNH Catering agreed to raise its Compass Arabia stake to 50%

- November 2024: Empower signed 18 contracts adding 21,640 RT of district-cooling capacity

- October 2024: Enova introduced AIEVA, an AI virtual assistant built on Google Cloud

United Arab Emirates Facility Management Market Report Scope

Facility management (FM) consists of multiple disciplines that influence organizations' efficiency and productivity, including the management of building upkeep, utilities, maintenance operations, waste services, and security.

The UAE facility management market is segmented by services (hard services and soft services), type (in-house and outsourced (single, bundled, and integrated FM)), end user (commercial and retail, manufacturing and industrial, government, infrastructural and public entities, and institutional), and cities (Abu Dhabi, Dubai, and Rest of United Arab Emirates). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

How large is the UAE facility management market in 2026?

The UAE facility management market size is valued at USD 23.59 billion in 2026 and is projected to grow at a 12.99% CAGR through 2031.

Which service segment dominates current revenue?

Hard services, covering MEP, fire safety and asset management, command 60.92% of 2025 revenue.

Why is healthcare the fastest-growing end-user industry?

Acquisitions by PureHealth and expansion at Burjeel Medical City are boosting hospital floor space and driving specialised facility management needs, supporting a 12.28% CAGR.

What regulatory trend is shaping FM contracts?

Federal Decree-Law 11 of 2024 mandates emissions monitoring and heavy fines for non-compliance, making sustainability reporting a core contract requirement.

How are technology platforms impacting contract awards?

IoT-enabled platforms and AI analytics shorten maintenance cycles and provide real-time performance data, features that increasingly influence tender evaluations and renewals.

Is the market moving toward outsourced or in-house management?

Outsourced integrated solutions hold 64.88% of market share and are expanding faster than in-house delivery as corporates seek cost optimisation and single-point accountability.

Page last updated on: