Middle East and Africa Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

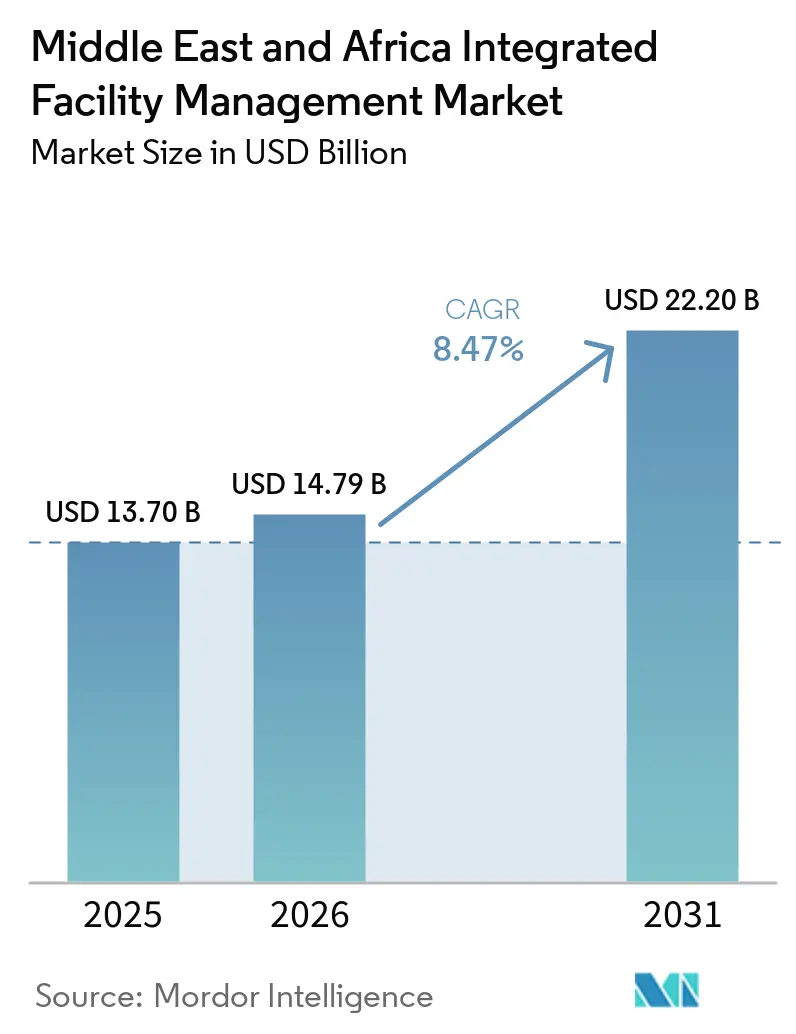

| Base Year Market Size (2025) | USD 13.70 Billion |

| Market Size (2026) | USD 14.79 Billion |

| Market Size (2031) | USD 22.20 Billion |

| Growth Rate (2026 - 2031) | 8.47% CAGR |

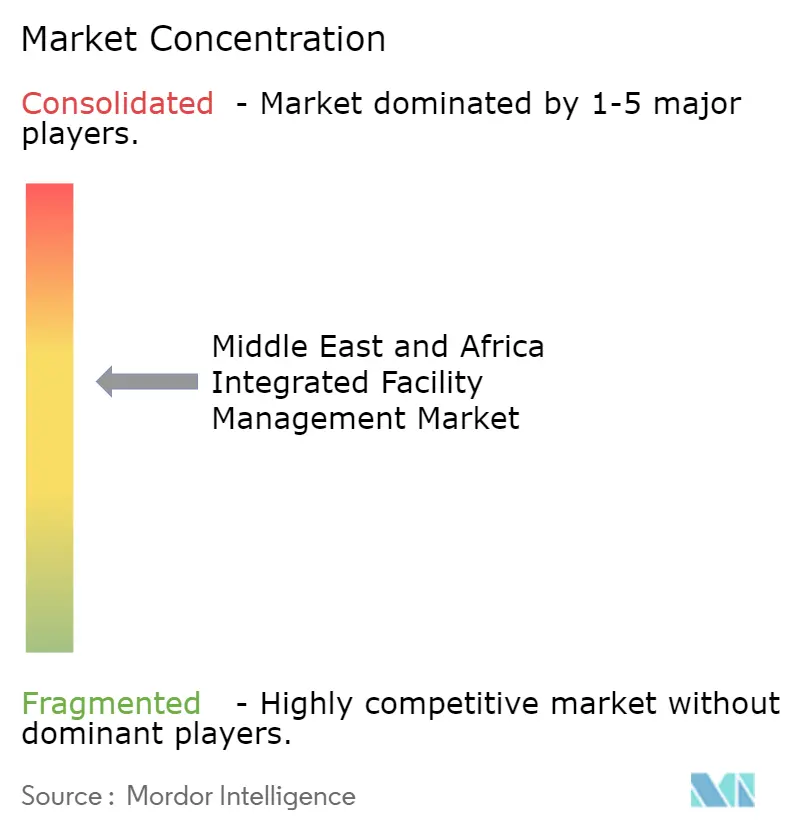

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Integrated Facility Management Market Analysis by Mordor Intelligence

The Middle East and Africa integrated facility management market size is projected to expand from USD 13.70 billion in 2025 and USD 14.79 billion in 2026 to USD 22.20 billion by 2031, registering a CAGR of 8.47% between 2026 to 2031. Asset owners across the Gulf Cooperation Council and sub-Saharan Africa are moving in-house facility teams into performance-based integrated contracts, which is shifting FM from a cost-control function to a broader asset-performance discipline. Sustainability targets, digital requirements in large projects, and wider use of outcome-based service models are making integrated delivery more central to infrastructure value preservation. The regional pattern is uneven, but both the Gulf and key African markets are moving toward bundled service contracts where uptime, compliance, and lifecycle support matter more than labor-only procurement. International platforms and regional operators are responding through technology-led delivery, localization readiness, and deeper sector specialization. Longer contract tenures in healthcare, aviation, and government portfolios are strengthening incumbent positions while leaving room for growth in commercial campuses, hospitality assets, and digital infrastructure.

Key Report Takeaways

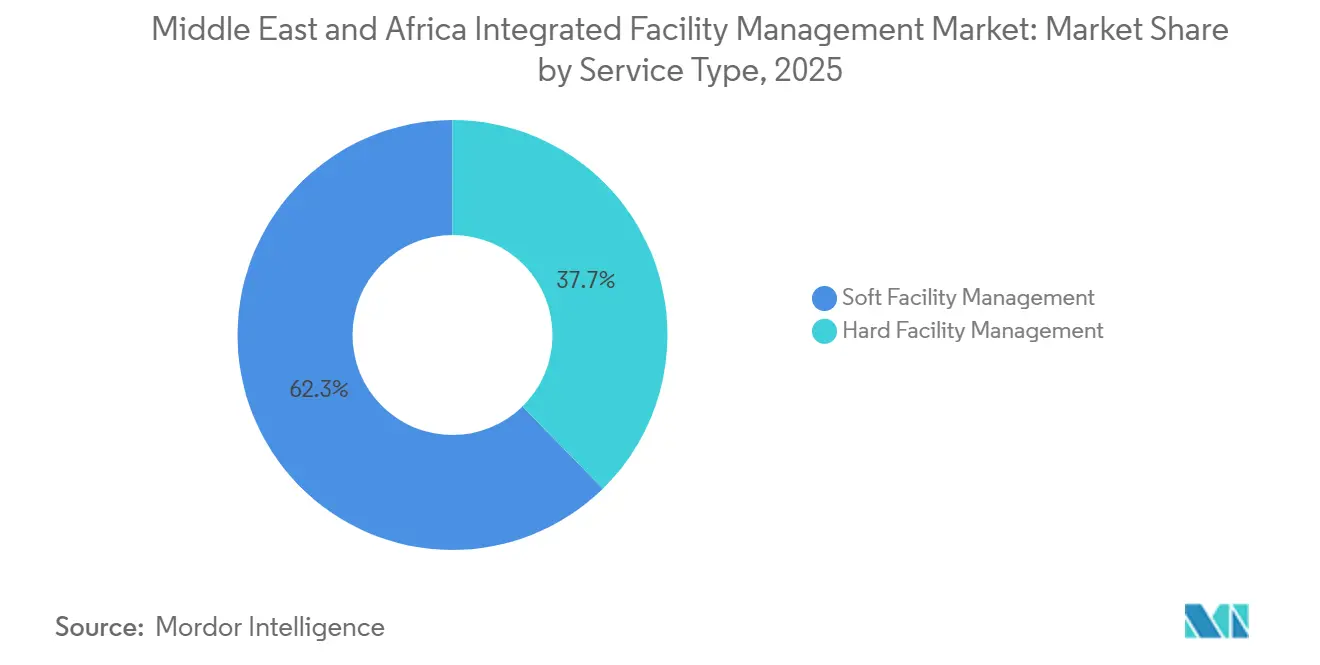

- By service type, soft facility management led with a 62.33% revenue share in 2025, while hard facility management is forecast to expand at an 8.53% CAGR through 2031.

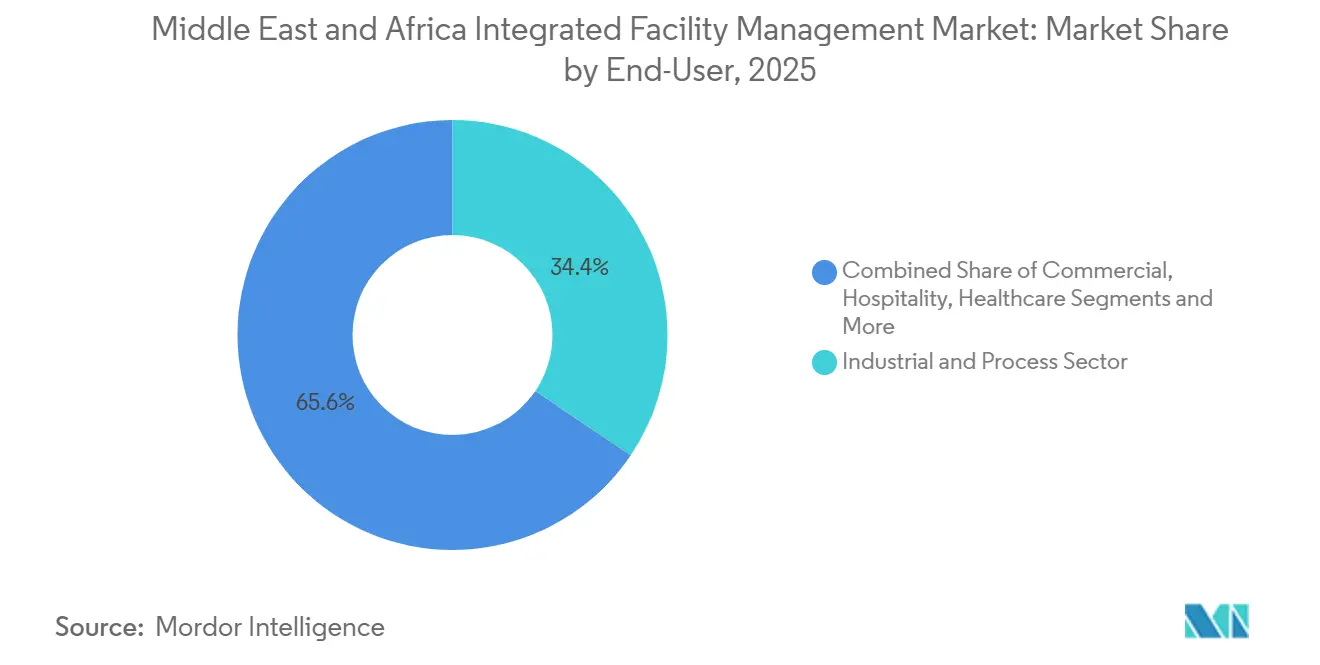

- By end user, the industrial and process sector held a 34.44% revenue share in 2025, while the commercial segment is projected to grow at a 9.12% CAGR through 2031.

- By geography, Saudi Arabia accounted for a 34.13% revenue share in 2025, while the UAE is forecast to advance at a 9.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Vision Programs Driving Smart Infrastructure | +2.8% | GCC-wide, Saudi Arabia and UAE most concentrated | Long term (≥ 4 years) |

| Rise in Energy-Efficiency Retrofits Across Commercial Real Estate | +1.5% | UAE, Saudi Arabia, spill-over to South Africa | Medium term (2-4 years) |

| Expansion of Data Centers Demanding Specialized FM Services | +1.2% | UAE and Qatar core, Saudi Arabia and Egypt emerging | Short term (≤ 2 years) |

| Increasing Adoption of IoT-Enabled Predictive Maintenance | +1.0% | Global, early gains concentrated in UAE and Saudi Arabia | Medium term (2-4 years) |

| Growing Regulatory Mandates for Building Safety Compliance | +0.7% | Saudi Arabia, UAE, Egypt | Medium term (2-4 years) |

| Upsurge in PPP Models for Social Infrastructure Upkeep | +0.5% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Vision Programs Driving Smart Infrastructure

Saudi Arabia's Vision 2030 and the UAE's long-range development frameworks are expanding the asset base that needs bundled operations, maintenance, and workplace services. In 2025, Saudi Arabia's non-oil activities made up 55.6% of real GDP, which shows how the building stock tied to tourism, services, logistics, and public infrastructure is widening beyond the hydrocarbon base.[1]Saudi Vision 2030, “Saudi Vision 2030 - 2025 Annual Report,” Saudi Vision 2030, vision2030.gov.saThe same annual report stated that tourism reached 123 million arrivals and USD 81 billion in spending in 2025, which keeps hotels, entertainment districts, transport assets, and public venues in continuous operating mode. In the Middle East and Africa integrated facility management market (MEA IFM), that shift supports larger bundled contracts because new districts and mixed-use projects need one provider to manage cleaning, security, engineering, and lifecycle performance together. The Middle East and Africa integrated facility management (MEA FM) market is also moving closer to outcome-based procurement because public clients want contractors to protect asset value, meet service levels, and support localization goals through the full operating cycle. This raises the advantage of providers that can combine technical depth, workforce scale, and digital oversight across multiple sites.

Rise in Energy-Efficiency Retrofits Across Commercial Real Estate

Energy-efficiency retrofits are turning into a recurring service line for the Middle East and Africa integrated facility management market as owners try to cut utility spend and meet sustainability targets. The IEA stated that buildings account for 40% of global energy consumption, which keeps energy performance high on the agenda for property owners and public authorities. A peer-reviewed study published in October 2025 found that residential and commercial buildings represented 39% of the UAE's national energy use, which keeps retrofit demand tied to a clear operating cost base.[2]Mahmoud Z. Mistarihi, Mohamad Kharseh, Essam M. Abo-Zahhad, Kadhim Alamara, Mohamed Elasy, and Khadija Aldhuhoori, “Energy-Efficient Strategies for Net-Zero Buildings in the UAE: A Climate-Resilient Blueprint,” Energy Conversion and Management: X, sciencedirect.com Emrill Energy stated in October 2025 that AI-driven HVAC retrofits across sites in Dubai and Sharjah delivered 14% verified electricity savings over 18 months, with average site efficiency gains of 21%. In the Middle East and Africa integrated facility management market, these retrofit programs do more than improve equipment, because they create longer monitoring, maintenance, and verification work after the first project is complete. That pattern is moving more contracts away from one-time engineering jobs and toward multi-year operating agreements tied to performance.

Expansion Of Data Centers Demanding Specialized FM Services

The Middle East and Africa integrated facility management market (IFM) is gaining a distinct mission-critical niche as data center construction accelerates across the Gulf. Microsoft and G42 announced a 200-megawatt expansion of UAE data center capacity in November 2025, with operations expected before the end of 2026, which adds major demand for specialized power, cooling, security, and uptime management. In February 2026, Iron Mountain took a minority stake in Ooredoo's MENA Digital Hub to support hyperscale and AI data center growth, reinforcing the region's direction toward larger and more complex digital infrastructure.[3]Khazna Data Centers, “Khazna Sets a New Standard for Mission-Critical Data Center Operations with Launch of Khazna NexOps,” Khazna Data Centers, khaznadatacenters.com Khazna launched NexOps in February 2026 and scaled from 20 to more than 230 specialists across over 30 UAE data centers in under 12 months, showing how fast staffing needs can rise in this part of the Middle East and Africa integrated facility management (FM) market. These sites need 24/7 command coverage and tighter control of electrical and cooling systems than standard office assets. The same buildout is also changing buyer expectations, because clients increasingly want providers that can manage operational technology, resilience, and energy performance in one service layer.

Increasing Adoption Of IoT-Enabled Predictive Maintenance

The Middle East and Africa integrated facility management (MEA FM) market is moving from reactive maintenance toward data-led asset care as connected building systems become more common. IFMA reported in January 2026 that NEOM's technical requirements mandate digital twin integration and continuous data exchange for core assets, making digital monitoring a baseline requirement in one of the region's largest project ecosystems. Emrill Energy's October 2025 results showed that AI-driven HVAC retrofits can turn operational data into measurable energy savings, giving owners a clearer basis for service-level commitments. Khazna stated that its NexOps platform uses an AI-powered command and control system built with Presight, and the company linked the model to a 2.3% improvement in power usage effectiveness from existing baselines. In the Middle East and Africa integrated facility management market (MEA IFM), this matters because verifiable output makes it easier for buyers to shift contracts from labor pricing toward uptime, efficiency, and fault-prevention targets. Providers with stronger CAFM, digital twin, and sensor integration capability are therefore gaining a better position in technically demanding tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Vendor Ecosystem Limiting Standardization | -1.5% | Africa-wide, spill-over to tier-2 Middle East markets | Medium term (2-4 years) |

| Skilled-Labor Shortages in HVAC and MEP Trades | -1.2% | Global, most acute in UAE, Saudi Arabia, and South Africa | Short term (≤ 2 years) |

| Volatile Oil-Linked Budgets Curtailing OPEX in Government Facilities | -0.8% | Saudi Arabia, Kuwait, Qatar, Bahrain | Medium term (2-4 years) |

| Cyber-Security Concerns Around Connected Building Systems | -0.6% | UAE and Saudi Arabia core, spill-over to data center markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Vendor Ecosystem Limiting Standardization

The Middle East and Africa integrated facility management market still works through dense subcontractor layers in many African and tier-2 Middle Eastern locations. This structure creates variation in service quality, staffing standards, and reporting discipline across multi-site contracts. Nigeria's commercial corridors and Nairobi's expanding office stock still attract many small operators that compete strongly on price, which makes standardized delivery harder for ISO-aligned providers. Cross-border work becomes more complex when providers must manage different building codes, safety rules, and certification practices at the same time. In the Middle East and Africa integrated facility management market, firms that deploy CAFM systems and stricter vendor qualification rules can improve consistency, but the cost of systems integration and workforce training weighs on early returns. The result is a slower scaling path for regional platforms that want to build uniform service models across several African markets.

Skilled-Labor Shortages in HVAC And MEP Trades

Skilled shortages in HVAC and MEP trades remain one of the most immediate constraints in the Middle East and Africa integrated facility management market. Farnek stated in February 2025 that it mobilized more than 1,500 additional staff across the UAE and Saudi Arabia in 2024 to deliver AED 690 million (approximately USD 187.9 million) in new and retained contracts, which shows how tight the labor base had become.[4]Farnek Services LLC, “Farnek Secures Contracts Worth Over AED 690 Million in 2024,” Farnek Services LLC, farnek.comWhen technicians are hard to source, providers face pressure on mobilization speed, renewal performance, and energy outcomes on complex sites. The Middle East and Africa integrated facility management market also faces a narrower tender pool where public and sovereign-linked projects require stronger local staffing pipelines and compliance readiness. Farnek's hybrid cleaning rollout in 2025 and 2026 shows why operators are pairing automation with human labor so teams can shift toward higher-skill technical work. This response helps at the margin, but it does not remove the need for deeper training and retention capability across the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Gains Ground as Asset Complexity Rises

Hard Facility Management (Hard FM) is the fastest-growing service type in the Middle East and Africa integrated facility management market, with a forecast CAGR of 8.53% from 2026 to 2031. The expansion reflects rising demand from data center campuses, healthcare facilities, industrial sites, and large commercial buildings that need specialist management of MEP, HVAC, and fire systems. New safety and construction compliance requirements in 2025 widened the scope of preventive maintenance and inspection activity across major urban assets, especially in technically regulated buildings. Asset management, MEP, and HVAC services remain the largest hard service anchors because giga-project operating models depend on long-duration preventive work rather than break-fix activity. In the Middle East and Africa integrated facility management market, data centers now sit at the top end of hard FM demand because they require specialist staffing, continuous oversight, and tighter environmental control than conventional commercial properties.

Soft Facility Management (Soft FM) held 62.33% of the Middle East and Africa integrated facility management market size in 2025, supported by the labor intensity of cleaning, catering, office support, and security across hospitality, healthcare, and government assets. That lead remains important because many regional portfolios still need high-headcount service delivery across large public venues, mixed-use communities, and institutional facilities. Farnek expanded its hybrid cleaning model across the UAE in September 2025, with more than 30 robotic cleaners deployed, 60 more on order, and a target of over 100 units by mid-2026, which shows how soft services are being automated without losing scale. Saudi Arabia's tourism activity also keeps catering and support services active across resorts, entertainment assets, and hospitality complexes, with the kingdom reporting 123 million tourist arrivals and USD 81 billion in spending in 2025.

By End User: Industrial and Process Sector Leads While Commercial Demand Accelerates

Industrial and process sector clients accounted for 34.44% of the Middle East and Africa integrated facility management market share in 2025, making this the largest end-user base. The segment is sustained by refinery, gas, mining, aviation engineering, and heavy industrial sites where uptime and compliance matter as much as cost control. Long-duration operating and maintenance contracts are common here because owners of high-hazard assets cannot tolerate interruptions in technical service delivery. Farnek's 2024 portfolio included work for Maaden and Etihad Airways Engineering, which reflects how industrial demand extends beyond hydrocarbons into mining and adjacent technical sectors. Large operators have built strong positions in this segment by combining technical services, compliance systems, and mobilization capacity across the GCC.

The commercial segment is the fastest-growing end user in the Middle East and Africa integrated facility management market, with a CAGR of 9.12% through 2031. Grade A offices, logistics hubs, and data center campuses in Saudi Arabia and the UAE are raising service specifications and favoring integrated contracts over fragmented single-service models. Emrill expanded its managed residential and commercial communities portfolio from 157 in 2023 to 254 by 2025, which points to the broader scale-up in community and property operations. Institutional and public infrastructure demand remains stable through long-tenure education, transport, and government contracts, and EFSIM secured a Saudi schools mandate worth more than SAR 100 million (USD 26.7 million) in March 2025. Healthcare and other public-facing assets are also becoming more specialized, which is pushing providers to build dedicated operating models rather than rely on generic service packages.

Geography Analysis

Saudi Arabia represented 34.13% of regional revenue in 2025, giving it the largest position in the Middle East and Africa integrated facility management market. The scale comes from the kingdom's large construction pipeline, sovereign-backed project portfolio, and a stronger shift toward licensed and performance-based FM delivery. Saudi Arabia's economy grew by 4.5% in 2025 and non-oil activities reached 55.6% of real GDP, which supports a broader operating base across tourism, public services, logistics, and mixed-use development. The UAE is the fastest-growing geography in the Middle East and Africa integrated facility management market, with a projected CAGR of 9.23% from 2026 to 2031. That pace is tied to commercial expansion, sustained hospitality demand, and major digital infrastructure additions such as Microsoft's planned 200-megawatt capacity expansion with G42 through Khazna.

Qatar and Kuwait form the next tier of Gulf demand, supported by energy assets, transport infrastructure, and large public building portfolios. In Qatar, corporate headquarters, airport facilities, and utility-linked assets are creating longer IFM contract cycles and higher demand for technical operations support. Kuwait's modernization agenda continues to support FM needs across ports, public services, and transport-related infrastructure, while Oman, Bahrain, and Jordan add opportunities linked to economic zones and urban development. Across this part of the Middle East and Africa integrated facility management market, buyers are steadily shifting from labor-only tenders toward bundled contracts that combine engineering, soft services, compliance, and reporting.

Africa presents a more uneven but still expanding operating environment within the Middle East and Africa integrated facility management market. South Africa remains the most mature African base because it has a stronger commercial real estate platform and a larger multinational occupier presence that values standardized service delivery. Nigeria, Kenya, and Egypt make up the clearest growth frontier as office, retail, and mixed-use assets expand and draw regional operators into longer outsourcing agreements. The Middle East and Africa integrated facility management (MEA IFM) market in Africa is still shaped by fragmented regulation and uneven infrastructure, which slows standardization and raises delivery cost across borders. Even so, ESG reporting needs, hygiene standards, and wider use of ISO-aligned contracts are creating a clearer opening for certified providers in the continent's leading urban markets.

Competitive Landscape

The Middle East and Africa integrated facility management market shows moderate concentration at the top end, where global platforms and a limited set of regional leaders win most large government, institutional, and critical infrastructure contracts. CBRE, JLL, ISS, Sodexo, and Cushman and Wakefield compete on cross-border delivery, compliance standards, and digital operating tools, while regional firms win through localization, pricing discipline, and deep client familiarity. In the Middle East and Africa integrated facility management market, the ability to manage multi-country portfolios is a strong differentiator because sovereign funds, developers, and multinational occupiers want consistent service frameworks across sites. JLL's December 2025 agreement to acquire a significant stake in FMTECH shows how competitive positioning is moving beyond advisory work and into co-owned operating platforms that can combine global systems with domestic reach. Longer contract durations in healthcare, aviation, and government assets also reinforce incumbent advantage by reducing the frequency of open rebidding.

The Middle East and Africa integrated facility management market is also seeing regional champions strengthen through technology-led operating models. Farnek expanded hybrid human-robot cleaning across UAE sites in 2025 and kept integrating AI scheduling through CAFMTEK, which helped it address labor pressure and productivity needs at the same time. Solutions+ and Serco expanded their partnership in June 2025 to consolidate IFM contracts into Khadamat Facilities Management LLC, creating a UAE-based platform that pairs local capital and digital transformation capability with international operating expertise. Emrill reported 9% revenue growth in 2025, which indicates that scale players with established client relationships and operational depth are still growing in a competitive field. This part of the Middle East and Africa integrated facility management market therefore rewards firms that can localize delivery without giving up data visibility, compliance control, or service breadth.

White-space opportunities remain strongest in Africa and in specialist categories such as data centers and healthcare, where standardized integrated delivery is still relatively scarce. Khazna's decision to build NexOps as an in-house operating organization shows that some asset owners are large enough to internalize mission-critical FM, which may narrow outsourcing volume in that niche even as total technical demand rises. The Middle East and Africa integrated facility management market is therefore competitive in 2 different ways, with intense rivalry for large sovereign and enterprise contracts and a long tail of smaller providers competing for localized work. Providers that can combine workforce scale, digital visibility, and sector-specific expertise remain best placed to defend margins as buyer expectations continue to rise.

Middle East and Africa Integrated Facility Management Industry Leaders

CBRE Group Inc.

ISS A/S

EFS Facilities Services Group

Sodexo SA

Compass Group Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Iron Mountain acquired a minority stake in Ooredoo's MENA Digital Hub, combining Iron Mountain's global infrastructure management expertise with Ooredoo's carrier-neutral regional network to address rising hyperscale and AI data center FM demand across the MENA region. The partnership positions both organizations to capture FM outsourcing contracts as regional data center capacity expands rapidly.

- February 2026: Khazna Data Centers launched Khazna NexOps, an in-house FM operations organization that scaled from 20 to over 230 specialists across more than 30 UAE data centers in under 12 months, transitioning from a vendor-driven to a fully insourced operations model. The initiative incorporated an AI-powered command and control platform built with Presight and achieved a 2.3% improvement in Power Usage Effectiveness from existing baselines.

- December 2025: JLL entered an agreement to acquire a significant stake in FMTECH, the PIF-backed Saudi Facility Management Company, with PIF retaining majority ownership. The transaction enables JLL to embed its global digital FM platforms and operating systems into FMTECH's national service framework, targeting PIF portfolio companies and broader public and private sector clients across Saudi Arabia.

- November 2025: Microsoft and G42 announced a 200-megawatt expansion of UAE data center capacity through Khazna Data Centers, as part of Microsoft's USD 15.2 billion total UAE investment commitment, with operations expected before end-2026. The expansion strengthens the UAE's position as a regional AI and cloud infrastructure hub and directly expands the FM scope for Khazna NexOps.

- October 2025: Emrill Energy completed the first phase of AI-driven HVAC retrofits across multiple sites in Dubai and Sharjah, achieving 14% total electricity savings over 18 months and verified efficiency gains averaging 21% per site, in collaboration with Green Leaf's AirNERGY solution under Dubai's RERA Energy Efficiency policy.

Middle East and Africa Integrated Facility Management Market Report Scope

The Middle East and Africa Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels),Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)), and Geography (Middle East [Saudi Arabia, United Arab Emirates, Qatar, Kuwait, and rest of Middle East], and Africa [South Africa, Nigeria, Kenya, Egypt, and rest of Africa]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Egypt | |

| Rest of Africa |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the Middle East and Africa integrated facility management market?

The Middle East and Africa integrated facility management market stands at USD 14.79 billion in 2026 and is projected to reach USD 22.2 billion by 2031, growing at an 8.47% CAGR.

Which service type leads revenue in this sector?

Soft FM led revenue with a 62.33% share in 2025, supported by cleaning, catering, office support, and security demand across hospitality, healthcare, and government facilities.

Which end-user group contributes the most revenue?

The industrial and process sector was the largest end user in 2025 with a 34.44% share, driven by refineries, gas assets, mining sites, and other high-uptime facilities.

Which country leads regional demand?

Saudi Arabia led regional revenue in 2025 with a 34.13% share, while the UAE is the fastest-growing geography with a projected 9.2% CAGR through 2031.

Why are data centers becoming important for facility management providers in the region?

Data center growth is increasing demand for mission-critical FM services such as 24/7 monitoring, power and cooling management, and tighter operational technology control, especially in the UAE.

What is the main operational challenge facing providers?

Skilled shortages in HVAC and MEP trades remain a key challenge, because technical contracts need certified staff and faster mobilization across large multi-site portfolios.

Page last updated on: