United Arab Emirates Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

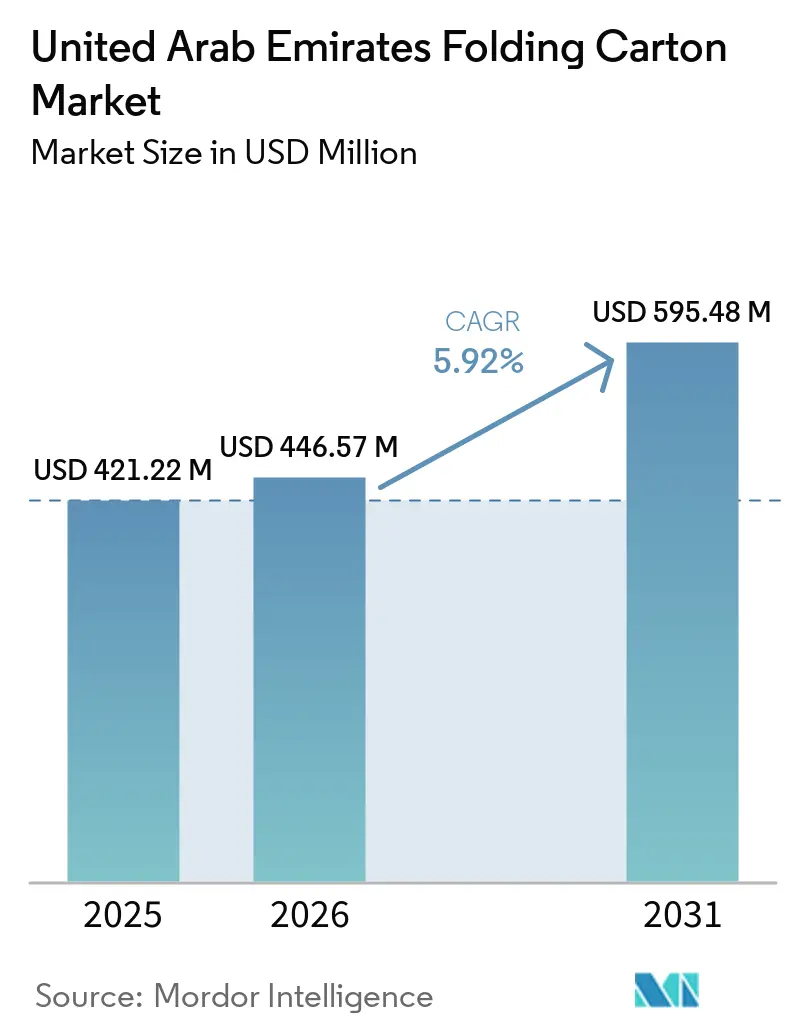

| Base Year Market Size (2025) | USD 421.22 Million |

| Market Size (2026) | USD 446.57 Million |

| Market Size (2031) | USD 595.48 Million |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

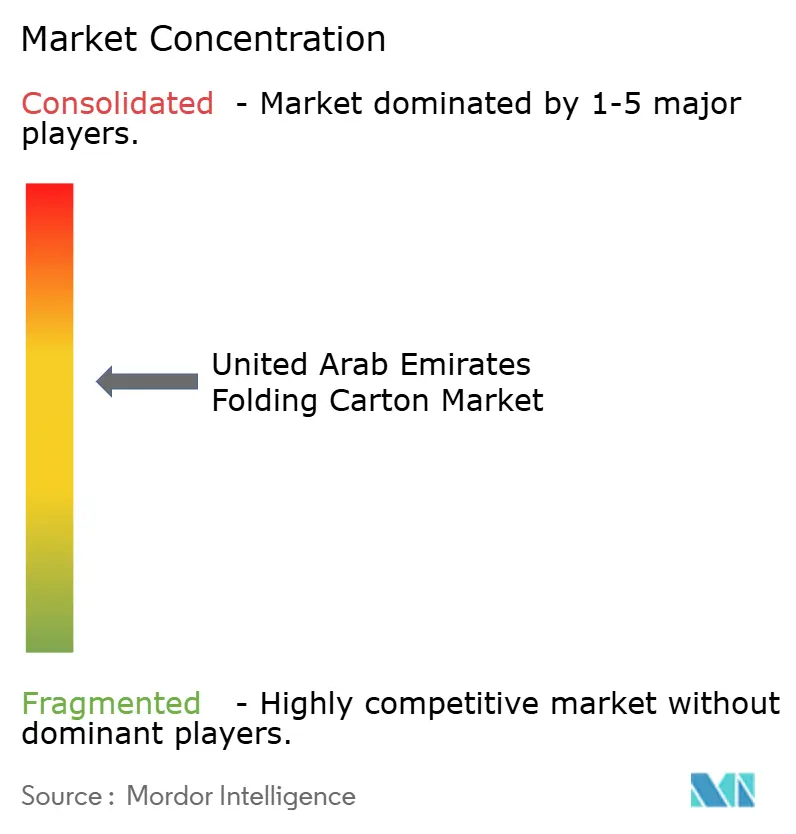

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Folding Carton Market Analysis by Mordor Intelligence

The United Arab Emirates folding carton market size is expected to increase from USD 421.22 million in 2025 to USD 446.57 million in 2026 and reach USD 595.48 million by 2031, growing at a CAGR of 5.92% over 2026-2031. Favorable sustainability regulations, double-digit travel-retail sales, and policy-driven pharmaceutical localization are driving folding-carton demand ahead of GDP growth. Material premiums for virgin-fiber grades, rapid scale-up of e-commerce fulfillment hubs, and momentum in the duty-free channel bolster pricing power while offsetting raw-material cost volatility. Converter margins remain sensitive to imported paperboard prices, yet in-country initiatives such as Star Paper Mill’s near-ready containerboard line hint at longer-term supply-chain insulation. International Paper’s EMEA spin-off and Smurfit WestRock’s USD 14 billion discretionary cash-flow roadmap signal ongoing capital deployment that can lift local converting capacity if macro tailwinds persist.

Key Report Takeaways

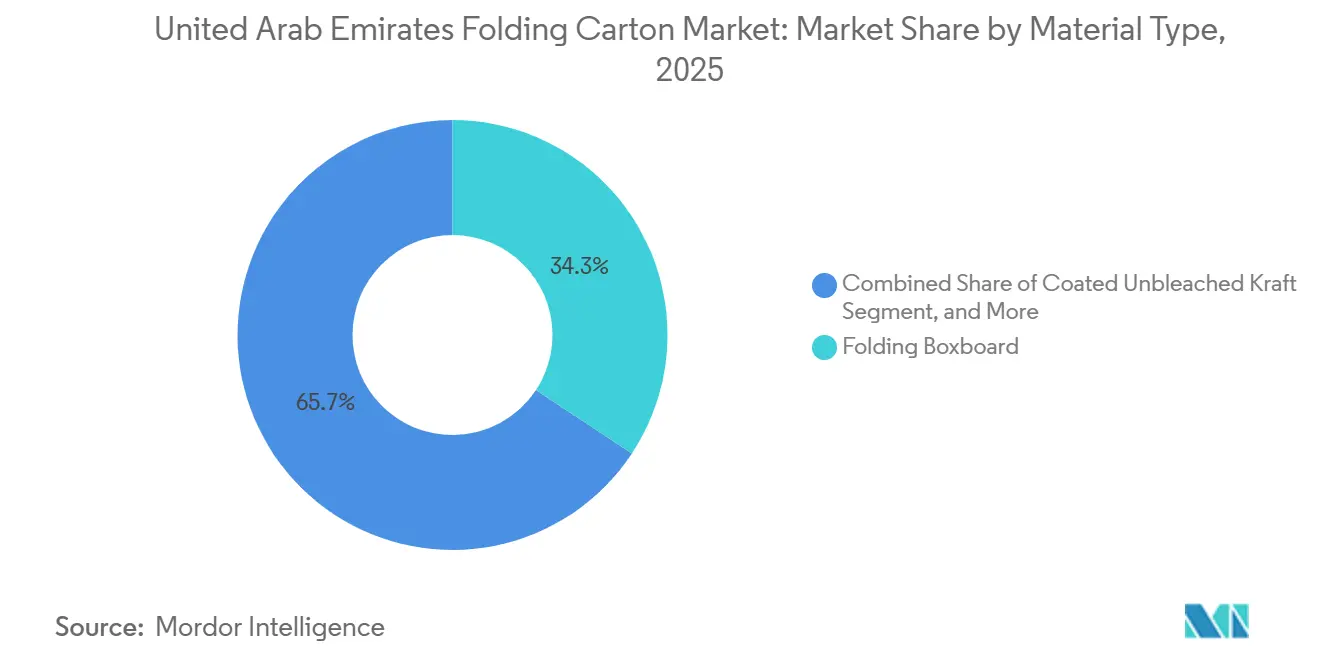

- By material type, folding boxboard captured with 34.29% of the United Arab Emirates folding carton market share in 2025.

- By printing technology, the United Arab Emirates folding carton market size for digital printing is projected to grow at a 7.89% CAGR to 2031.

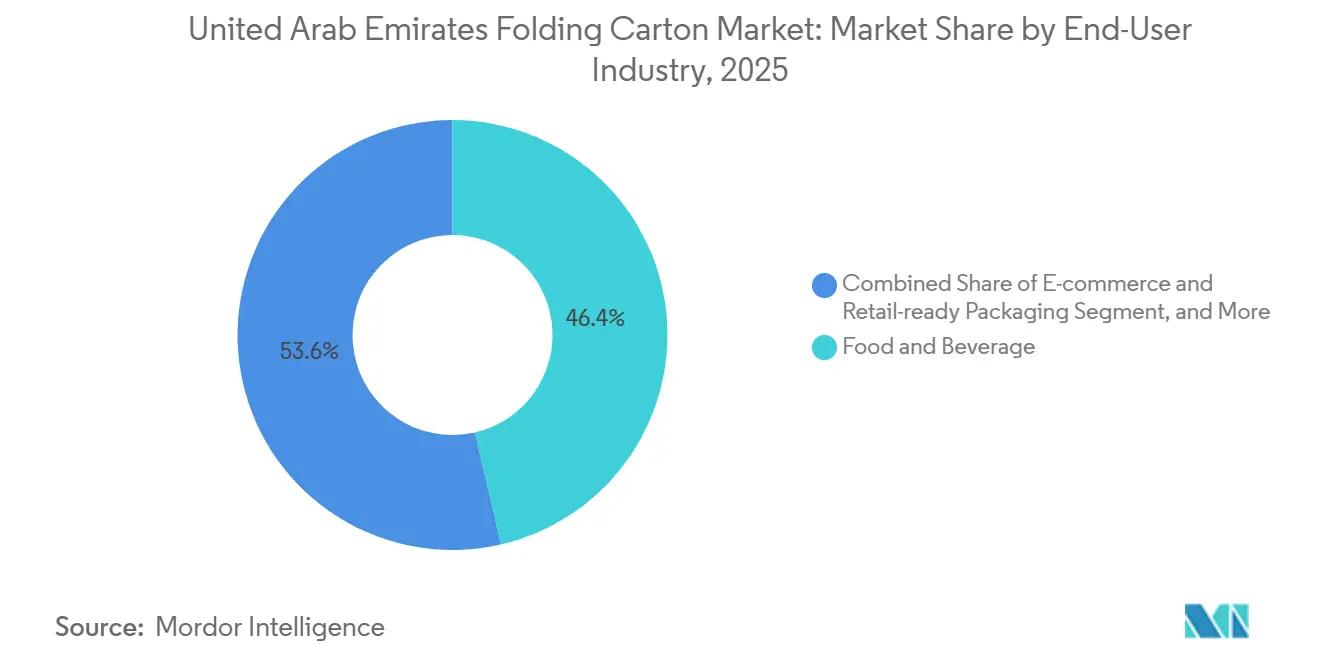

- By end-user industry, the food and beverage industry captured 46.38% of the United Arab Emirates folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of Food and Beverage Carton Demand | +1.2% | Dubai, Abu Dhabi, Sharjah retail and hospitality clusters | Medium term (2-4 years) |

| Expansion of E-commerce Fulfillment Networks | +0.9% | Dubai and Sharjah logistics zones | Short term (≤ 2 years) |

| Government Sustainability Mandates for Recyclable Packaging | +1.5% | Nationwide | Long term (≥ 4 years) |

| Rising Adoption of Digital Printing for Short-Run Jobs | +0.7% | Dubai and Abu Dhabi converters | Medium term (2-4 years) |

| Growth of Dubai Pharmaceutical Manufacturing Cluster | +1.1% | Dubai and Abu Dhabi pharma zones | Long term (≥ 4 years) |

| Surge in Duty-Free Retail Sales Boosting Carton Volumes | +0.8% | Dubai and Abu Dhabi airports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization of Food and Beverage Carton Demand

Travel-retail confectionery revenue jumped 15.35% year-on-year in January 2026, illustrating how premium chocolate brands invest in rigid, high-gloss cartons to capture impulse buys at Dubai International Airport. Sharjah’s Mleiha Dairy Factory added Tetra Top cartons to replace plastic bottles, underscoring cartons' advantages for on-the-go beverages. Brands leverage lithographic embossing, foil, and soft-touch coatings to justify price premiums, while converters stocking coated solid bleached sulfate enjoy above-average margins as shelf-ready aesthetics trump cost. The premiumization wave now spans ready-to-drink coffee, cold-pressed juice, and plant-based shakes, each seeking tactile cues and sustainable narratives unavailable with flexible film. As hypermarkets and airport concessions allocate limited shelf space, converters offering inline finishing and rapid prototyping gain share.

Expansion of E-commerce Fulfillment Networks

Same-day delivery norms in Dubai free zones are spurring demand for retail-ready folding cartons that offer crush resistance and premium unboxing appeal. Robotic pick-and-place systems in automated hubs favor cartons with predictable footprints, driving brands away from irregular flexible mailers. Digital printing enables micro-runs carrying variable data, such as recipient names or localized offers, without plate costs, aligning with fast-cycle online merchandising. UAE online logistics footprints expanded sharply in 2025, and converters combining digital presses with inline die-cutting now quote lead times in days instead of weeks, an edge that attracts direct-to-consumer electronics and cosmetics labels.

Government Sustainability Mandates for Recyclable Packaging

Phase-two enforcement of the single-use plastic ban from 1 January 2026 accelerates nationwide substitution toward fiber-based formats. The carve-out exempting locally recycled content rewards domestic converters and recycling investments, while brands face granular labeling and traceability rules that elevate compliant carton suppliers above low-cost importers. Hotpack’s recyclable H-rPET and fiber offerings illustrate the competitive advantage that comes from early alignment with Ministry guidelines. Anticipated future phases, including recycled-content quotas, make closed-loop supply chains a strategic imperative.

Rising Adoption of Digital Printing for Short-Run Jobs

SIG Group recorded 24% sales growth in 2025 for aluminum-layer-free aseptic cartons marketed on low carbon footprints, a proof point that sustainability pairs with personalization SIG.BIZ. Digital presses eliminate plate waste, enabling profitable 500-carton campaigns used by seasonal cosmetics and nutraceutical startups. Lead times shrink to 48-72 hours, letting brands pivot creative assets rapidly without over-ordering inventory. Hybrid workflows digital for micro-runs, litho for long runs anchor one-stop converter value propositions, while advances in inkjet color gamut and inline varnishing narrow the quality gap with lithography. E-commerce subscription boxes and influencer collaborations now rely on digitally printed folding cartons to embed QR codes, serialized artwork, or localized language at negligible setup cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber and Recovered Paper Prices | -0.8% | Nationwide | Short term (≤ 2 years) |

| Limited Domestic Paperboard Production Capacity | -0.6% | Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Stringent Food-Contact Compliance Costs for SMEs | -0.4% | Nationwide | Long term (≥ 4 years) |

| Substitution Threat From Flexible Packaging Formats | -0.5% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber and Recovered Paper Prices

Export OCC climbed to USD 118-130 per short ton out of U.S. ports in January 2026, squeezing UAE converters that import most fiber inputs. Brent crude rose to about USD 107 per barrel by early April, inflating diesel surcharges on waste-paper collections and inbound freight. Mondi’s Q1 2026 price hikes highlight converter exposure to upstream shocks.[1]Packaging News Team, “Mondi increases prices and shuts plants as Middle East war affects business,” packagingnews.co.uk Larger players may hedge through multi-year supply contracts or backward integration, but SMEs struggle to absorb rapid spikes, eroding competitiveness.

Limited Domestic Paperboard Production Capacity

Star Paper Mill’s USD 54 million recycled containerboard project nears completion, yet targets liner grades, not premium folding-carton substrates. The absence of in-country solid bleached sulfate mills means converters still import high-brightness board from Europe or Asia, incurring war surcharges of up to USD 3,500 per 40-foot container when Strait of Hormuz routes are disrupted. Lead-time uncertainty forces higher inventory buffers, tying up working capital. Until domestic coated board capacity emerges, local suppliers remain vulnerable to geopolitical and freight shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Solid Bleached Sulfate Accelerates on Premium and Pharma Demand

Solid bleached sulfate is forecast to record a 7.14% compound growth rate, the fastest within the United Arab Emirates folding carton market, as pharmaceutical and high-end food producers demand pristine whiteness, FDA-grade contact surfaces, and robust barrier properties. Folding boxboard still represented 34.29% of 2025 revenue, buttressed by cosmetics and electronics SKUs that balance print quality with cost efficiency, and it continues to anchor lithographic long runs. Coated unbleached kraft enjoys niche appeal among organic brands seeking a natural aesthetic, whereas white line chipboard remains confined to low-value secondary packs. Converters that pre-stock solid bleached sulfate and integrate inline foil, embossing, and window patching tap higher margins because brand owners view packaging as a marketing spend rather than a cost line.

Premium positioning in confectionery, ready-to-drink coffee, and cold-pressed juice funnels volume to virgin substrates that deliver vibrancy and tactile effects. Meanwhile, the Emirates Drug Establishment’s licensing of 37 manufacturing plants increases the use of compliant cartons for tamper-evident, serialized medicines.[2]Dubai News.Net Reporter, “Emirates Drug Establishment launches major initiative to boost UAE pharmaceutical manufacturing,” dubainews.net Over the forecast window, folding boxboard will still command the largest share of the United Arab Emirates folding carton market, yet its growth trails solid bleached sulfate as electronics slow and sustainability audits tighten traceability standards for recycled grades.

By Printing Technology: Digital Printing Captures Micro-Run Opportunity

Lithography retained 41.67% of 2025 revenue thanks to economies of scale in cosmetics, beverages, and tobacco, but digital printing is poised for a 7.89% CAGR as the go-to solution for SKU proliferation and variable data. Digital eliminates plates, trims setup waste, and enables profitable 500-unit orders, aligning with influencer collaborations and subscription boxes. Brands also leverage near-real-time artwork swaps to comply with regional labeling laws or promotional tie-ins, a flexibility that lithography cannot match at a small scale.

Hybrid converter workflows combine litho for volume and digital for customization, minimizing total system cost per brand. Flexography sustains mid-volume commodity food runs, while gravure now largely serves legacy tobacco lines facing regulatory decline. As SIG’s success with low-carbon aseptic cartons demonstrates, sustainability credentials pair naturally with inkjet and electrophotographic platforms that minimize waste. By 2031, digital’s share of the United Arab Emirates' folding carton market size could challenge lithography in high-margin personal-care and pharma niches where lot traceability and serialization are critical.

By End-User Industry: Pharma Sets the Growth Pace

Food and beverage delivered 46.38% of 2025 volume, driven by duty-free confectionery and premium dairy, with cartons showcasing for shelf presence. Nevertheless, healthcare and pharmaceuticals are expected to post the strongest CAGR of 8.38% through 2031 as national manufacturing policies reshape supply chains. ISO 15378 compliance drives demand for virgin board with high opacity, and folding cartons integrate tamper evidence, braille, and serial coding to satisfy traceability mandates.

Personal care and cosmetics leverage embossing, foil, and soft-touch finishes to justify elevated price points in travel retail, while electronics brands seek crush-resistant yet lightweight cartons for e-commerce. Tobacco, household goods, and industrial products represent incremental but slower-growing niches as anti-smoking regulations and flexible-film substitution temper momentum. The Holistic National Manufacturing Project effectively locks in carton demand within pharma clusters, raising the overall value density of the United Arab Emirates folding carton market.

Geography Analysis

Dubai, Abu Dhabi, and Sharjah dominate folding-carton consumption, reflecting their weight in travel retail, pharmaceuticals, food processing, and logistics. Dubai Duty Free’s record AED 858.21 million (USD 235 million) January 2026 sales underline Dubai’s role as the gateway for high-margin cartons serving perfumes, confectionery, and fashion. E-commerce fulfillment centers in Jebel Ali Free Zone and Dubai South rely on retail-ready cartons that withstand multiple hand-offs while maintaining brand aesthetics.

Abu Dhabi’s pharmaceutical corridor, enabled by 37 licensed plants, creates captive demand for serialized cartons produced under GMP conditions. Star Paper Mill’s containerboard site in Khalifa Economic Zones, Abu Dhabi, offers partial insulation from import shocks, although its liner grades do not directly feed premium carton lines.[3]ME Printer Staff, “Star Paper Mill to set up USD 54 m recycled containerboard mill,” meprinter.com Sharjah’s push into organic dairy, highlighted by Tetra Top installations, adds steady dairy-carton volume and reinforces the emirate’s credentials in sustainable food production.

Northern emirates, such as Ras Al Khaimah, offer cost-effective manufacturing footprints, with United Carton Industries investing AED 74 million (USD 20.2 million) to scale capacity by 2027. Re-export flows to the wider Gulf Cooperation Council and East Africa further elevate throughput at Dubai and Abu Dhabi ports, although Strait of Hormuz disruptions occasionally reroute cargo through Jeddah Islamic Port, inflating land-transport costs and highlighting geopolitical exposure.

Competitive Landscape

The United Arab Emirates folding carton market is moderately concentrated. Multinational integrators such as International Paper, Smurfit WestRock, and Mondi contest share with regional specialists Gulf Printing and Packaging, Arabian Packaging, Al Ghurair Printing and Publishing, and Emirates Printing Press. International Paper’s planned EMEA spin-off, scheduled to close within 12-15 months of its January 2026 announcement, may accelerate capital investment in localized converting lines aligned with Middle East specification requirements.

Smurfit WestRock targets USD 7 billion adjusted EBITDA by 2030 and USD 14 billion cumulative discretionary free cash flow from 2026-2030, implying ample headroom for UAE plant upgrades or bolt-on acquisitions.[4]Smurfit WestRock Investor Relations, “Medium-Term Investor Update,” smurfitwestrock.com Mondi, after reporting EUR 212 million (USD 231 million) Q1 2026 EBITDA, is uplifting prices and optimizing its European footprint, signaling a disciplined yet expansion-ready stance toward profitable regions.

Domestic disruptors include Star Paper Mill’s backward-integrated board source and Hotpack’s recyclable mono-material portfolio, both of which differentiate through sustainability. Converter strategies increasingly hinge on hybrid digital-litho workflows, ISO 14001 accreditation and pharma-grade cleanroom capabilities. Market participants able to provide variable-data cartons within 72 hours, uphold MOCCAE compliance and bundle graphic design with co-packing services secure higher wallet share as brand owners consolidate supplier bases.

United Arab Emirates Folding Carton Industry Leaders

Emirates Printing Press LLC

Gulf Printing and Packaging FZ-LLC

Tetra Pak International SA

Al Bayader International LLC

Ittihad Paper Mill LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mondi reported Q1 2026 EBITDA of EUR 212 million (USD 231 million) and confirmed price increases alongside the closure of three European converting plants to shield margins.

- March 2026: SIG Terra RecShield BD pouch earned Association of Plastic Recyclers design-for-recyclability recognition, reinforcing SIG’s sustainability positioning.

- February 2026: Emirates Drug Establishment launched the Holistic National Manufacturing Project, having licensed 37 pharmaceutical plants to date.

- February 2026: Smurfit WestRock forecast USD 7 billion EBITDA by 2030 and USD 14 billion free cash flow over 2026-2030.

United Arab Emirates Folding Carton Market Report Scope

The United Arab Emirates Folding Carton Market encompasses the production, distribution, and application of folding cartons, paper-based packaging solutions designed for a variety of consumer and industrial goods. This report includes an analysis of key market dynamics, trends, and forecasts specific to Saudi Arabia.

The United Arab Emirates Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and projected size of the United Arab Emirates folding carton market?

The market is valued at USD 446.57 million in 2026 and is forecast to reach USD 595.48 million by 2031, reflecting a 5.92% CAGR.

Which material type is expanding fastest in UAE folding cartons?

Solid bleached sulfate is projected to grow at a 7.14% CAGR to 2031, propelled by pharmaceutical and premium food demand.

How are government regulations influencing carton demand?

Nationwide plastic bans effective from 2026 favor fiber-based folding cartons and drive brand shifts toward recyclable mono-materials.

Why is digital printing gaining traction among UAE converters?

Digital printing supports micro-runs, variable data and 48-hour lead times, matching e-commerce and personalized marketing needs.

Which end-user sector will be the principal growth engine through 2031?

Healthcare and pharmaceuticals lead with an expected 8.38% CAGR, underpinned by the Emirates Drug Establishment’s localization agenda.

How concentrated is competition in the UAE folding carton space?

The top five suppliers hold just over 60% combined share, indicating moderate concentration with room for agile regional specialists.

Page last updated on: