Algeria Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

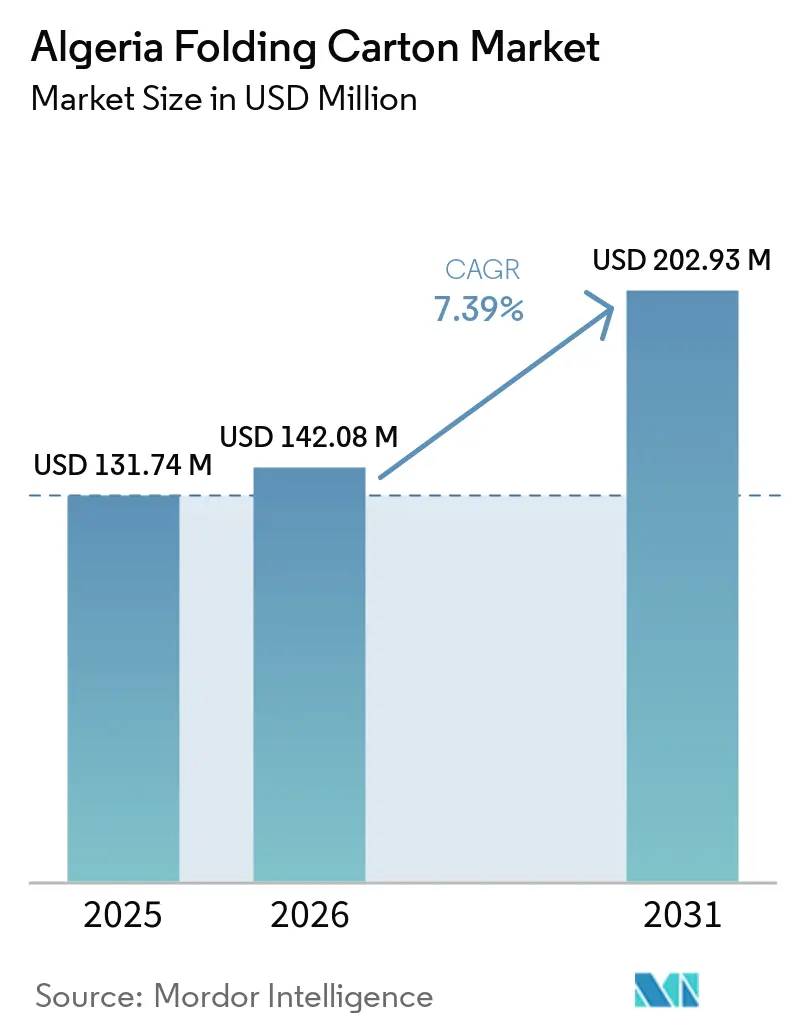

| Base Year Market Size (2025) | USD 131.74 Million |

| Market Size (2026) | USD 142.08 Million |

| Market Size (2031) | USD 202.93 Million |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

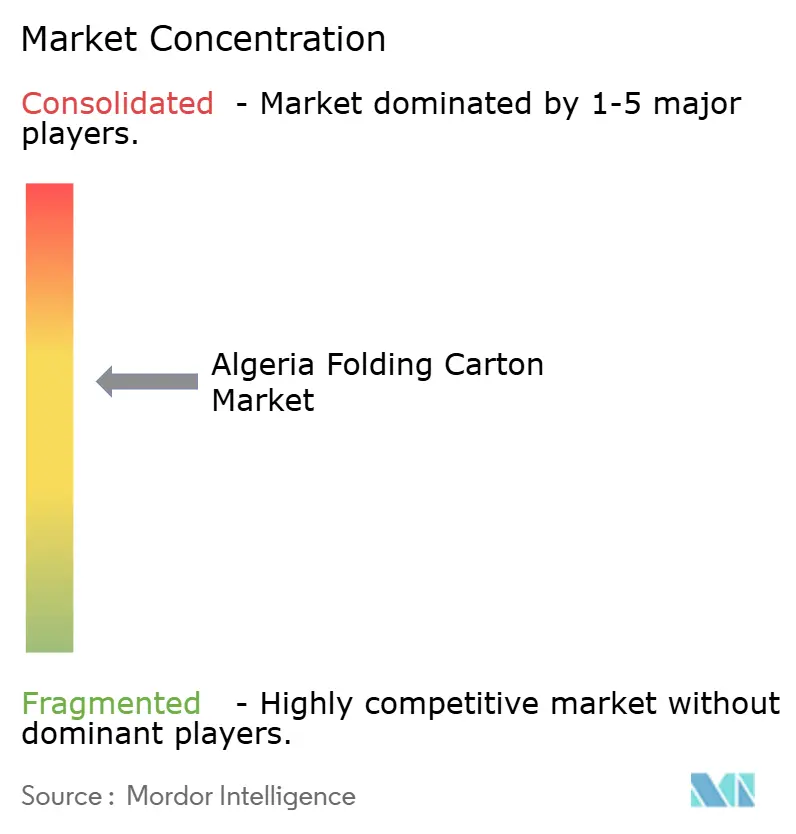

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Folding Carton Market Analysis by Mordor Intelligence

The Algeria folding carton market size is expected to increase from USD 142.08 million in 2026 to USD 202.93 million by 2031, growing at a CAGR of 7.39% over 2026-2031. Domestic production of packaged foods and medicines, a legal crackdown on single-use plastics, and the rapid rise of e-commerce are expanding folding carton demand faster than broad packaging growth. The Algeria folding carton market is benefiting from premiumization in urban grocery channels, where brand owners are adopting higher-GSM substrates and multi-color graphics to boost shelf appeal. Export ambitions for dates, olive oil, and ready-to-eat meals require ISO 22000-compliant cartons that meet European migration rules, pushing converters toward Solid Bleached Sulfate. Meanwhile, pharmaceutical self-sufficiency is deepening the need for blister-compatible cartons that meet WHO pre-qualification, EU serialization, and 40 °C stability testing requirements. Although imported board costs remain volatile, subsidized electricity, a nascent domestic fiber-recovery push, and Général Emballage’s new mill plan form a structural hedge against price spikes.

Key Report Takeaways

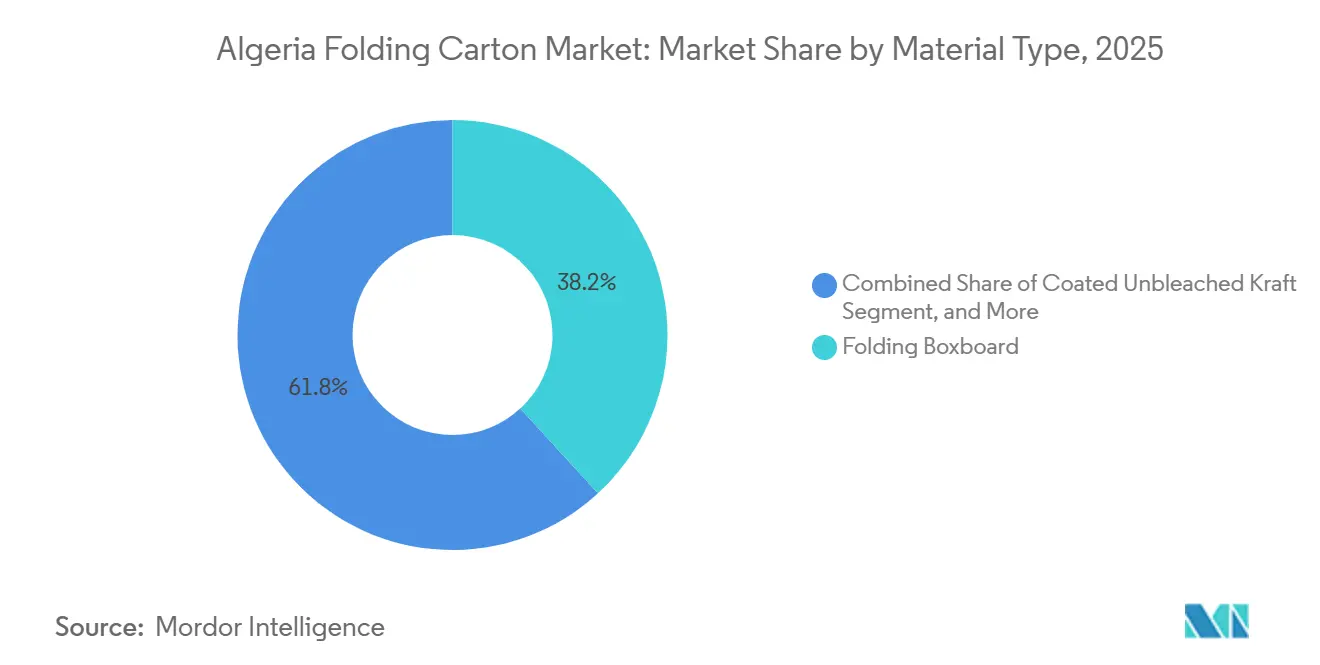

- By material type, folding boxboard captured with 38.17% of the Algeria folding carton market share in 2025.

- By printing technology, the Algeria folding carton market size for digital printing is projected to grow at a 8.51% CAGR to 2031.

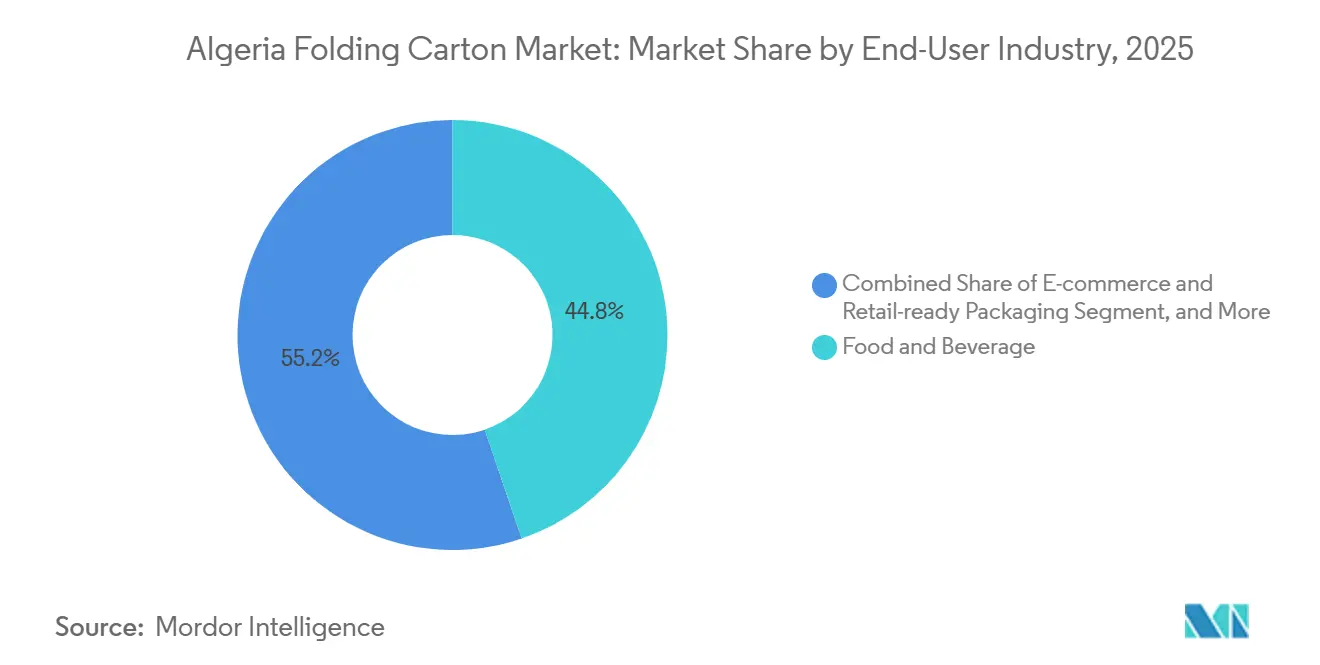

- By end-user industry, the food and beverage industry captured 44.79% of the Algeria folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Algeria Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urban Middle-Class Consumption | +1.8% | National, concentrated in Algiers, Oran, Constantine | Medium term (2-4 years) |

| Expansion of Algeria's Packaged Food Exports | +1.5% | National with export corridors to the EU, Sub-Saharan Africa, Middle East | Long term (≥ 4 years) |

| Regulatory Ban on Single-Use Plastics | +1.3% | National, enforced through Law 25-02, and municipal EPR programs | Short term (≤ 2 years) |

| Growth of Local Pharmaceutical Manufacturing | +1.1% | National, led by Algiers, Constantine, and Sétif clusters | Medium term (2-4 years) |

| On-site Digital Printing Adoption by Converters | +0.7% | National, early adopters in Algiers, Oran, Béjaïa | Medium term (2-4 years) |

| Subsidized Industrial Electricity Tariffs | +0.6% | National, benefiting energy-intensive lines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Urban Middle-Class Consumption

Urban households, already 82% of the population, are trading bulk staples for branded ready meals, detergents, and cosmetics. That shift multiplies unit packs per capita, so each new SKU feeds incremental demand in the Algerian folding carton market. Hypermarkets opened fifteen outlets in 2024-2025, each stocking 8,000-12,000 items that need secondary cartons for shelf-ready display. Modern retailers conduct ISO 9001 supply-chain audits, narrowing the supplier base to converters with color management and food safety certifications. The quality message resonates with middle-income consumers who equate rigid cartons with reliability. As disposable incomes rise further, premium designs printed on Solid Bleached Sulfate capture a greater share of the basket.

Expansion of Algeria's Packaged Food Exports

The state aims to reach USD 30 billion in non-hydrocarbon exports by 2030, and every outbound container must withstand sea humidity, heat, and customs inspections. Deglet Nour dates, olive oil, and UHT dairy pose distinct barrier requirements that Folding Boxboard alone cannot always satisfy, fostering a swing toward virgin grades. EU Regulation 1935/2004 compels migration testing, so converters upgrade to FDA-approved boards and ISO 22000 production. Cargo bound for Sub-Saharan Africa often moves through mixed-mode corridors, intensifying durability standards. As the export mix shifts from raw to processed goods, carton value per tonne shipped climbs, lifting the Algerian folding carton market.

Regulatory Ban on Single-Use Plastics

Law 25-02 lifted the plastic-bag tax to 200 dinars per kilogram and mandated extended producer responsibility.[1]Algerian Official Gazette, “Law 25-02 on Waste Management,” joradp.dz The immediate cost penalty on flexible laminates makes fiber-based formats the compliance shortcut. Personal-care brands pivot to folding cartons that list recyclability icons, gaining shelf share while avoiding plastic backlash. Early-stage curbside trials in Algiers and Oran assign QR-coded disposal instructions, and converters with dual print-data capability win tenders. As deadlines tighten, substitution spreads from bags to trays, tubes, and clamshells, accelerating Algeria folding carton market penetration in non-food aisles.

Growth of Local Pharmaceutical Manufacturing

More than 230 drug plants met 82-83% of domestic volume in 2025, and pipeline launches—insulin pens and oncology blister packs demand virgin SBS with tight tolerances. WHO pre-qualification files require evidence of tamper-evidence, serialization, and 40 °C/75 % RH stability. Each new biologic or vaccine line needs cartons that run flawlessly on high-speed cartoners, boosting per-unit board weight. Local suppliers able to document GMP-grade hygiene secure contracts displacing imported printed boxes, anchoring double-digit expansion of the Algeria folding carton market inside health care channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Imported Paperboard Prices | -1.2% | Nationwide, all converters are reliant on European and Turkish mills | Short term (≤ 2 years) |

| Limited Domestic Fiber Recovery Infrastructure | -0.9% | National, acute in interior provinces | Long term (≥ 4 years) |

| Energy Supply Interruptions Impacting Converting Lines | -0.6% | National, industrial zones with aging grids | Medium term (2-4 years) |

| Capital-Intensive Equipment Modernization Needs | -0.5% | National burden on small and mid-size converters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Imported Paperboard Prices

70% of folding-carton substrates originate in Europe and Türkiye, exposing converters to euro-dinar swings and freight spikes. Container rates through the Red Sea trebled during 2024 disruptions, and long lead times forced 60-90 day safety stocks. Quarterly price resets squeeze working capital, especially when finished-goods contracts run twelve months. Général Emballage’s DZD 40 billion (USD 296 million) mill will cover 55% of national demand by 2028, but until then, cost turbulence drains margins and tempers growth.

Limited Domestic Fiber Recovery Infrastructure

Recycling captures under 10% of post-consumer paper, so converters must import virgin pulp at premium prices. Contamination exceeds 15%, deterring food and pharma buyers who fear odor migration. Though the SNGID 2035 roadmap targets 47% valorization, funding gaps delay the construction of material-recovery facilities outside coastal cities. Until collection networks mature, recycled grades struggle to meet brightness and hygiene requirements, slowing the Algerian folding carton market’s circular transition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Grades Outpace Recycled Alternatives

Folding Boxboard delivered 38.17% of material revenue in 2025, dominating cereals, frozen foods, and dairy cartons that rely on its stiffness-to-cost ratio to protect light products. Its bright surface pairs well with CMYK litho graphics, and wax-coated variants protect dates from moisture during trips to Europe. Solid Bleached Sulfate, however, is forecast to expand at 8.73% annually, lifting its slice of the Algeria folding carton market size as pharma and cosmetics specify virgin fiber to meet migration and odor thresholds.

The Algeria folding carton market rewards SBS’s white point and ink holdout, enabling photographic reproduction, a feature prized by halal beauty brands. Pharmaceutical blister boxes also favor SBS because zero recycled content eases ICH Q1A stability filing. As WHO-prequalified vaccine ambitions grow, SBS’s share will climb despite its higher cost, helped by subsidized power that lowers conversion overhead. Coated unbleached kraft and white-line chipboard continue to serve heavy-duty detergents and tobacco, but sustainability narratives chip away at these segments.

By Printing Technology: Digital Printing Scales Personalization

Lithography accounted for 42.83% of technology revenue in 2025 and remains the backbone of six-color process work over 10,000 sheets. Heidelberg Speedmaster lines hit 18,000 sph, supporting high-volume milk and medicine cartons that anchor demand in Algeria's folding carton market. This growth highlights the increasing reliance on advanced printing technologies to meet market demands.

Digital printing is set to grow 8.51% annually as HP Indigo 100K and Xerox Iridesse platforms drive variable-data runs for e-commerce and serialized drugs. Zero plate change allows 500-unit pilot SKUs, trimming obsolescence costs. By 2028, Smithers expects digital to account for more than 23% of print volume, so converters adding hybrid inkjet-offset lines position themselves for faster artwork changeovers while keeping litho economics on flagship SKUs.

By End-User Industry: E-Commerce Spurs Fastest Growth

Food and beverage retained 44.79% of Algeria's folding carton market demand in 2025, spanning cereals, UHT dairy, sugar, and olive oil retail cases. Each hypermarket opening installs thousands of UPCs that rely on folding cartons for secondary containment, while date exporters specify extra-barrier waxed board for 30,000-tonne annual shipments.[2]Paperboard Packaging Council, “Solid Bleached Sulfate Applications,” paperboard.org The growing preference for sustainable packaging solutions is also driving the demand for folding cartons in the country.

E-commerce and retail-ready packaging will eclipse all peers, with an 8.61% CAGR, as Jumia, Ouedkniss, and Yassir scale to 15-20% yearly. Cash-on-delivery norms drive tamper-evident designs printed with QR codes, pushing digital printing adoption. Healthcare ranks second after food, underpinned by 230 local drug plants whose blister lines load SBS-compliant cartons in compliance with WHO GMP. Tobacco’s share is receding under plain-pack rules, freeing capacity that converters redeploy into growing consumer-goods niches.

Geography Analysis

The Algeria folding carton market concentrates in Algiers, Oran, and Constantine, three metros that capture roughly 65% of demand. Algiers alone bundles Saidal’s insulin pen plant, Danone’s dairy complex, and most Carrefour outlets, generating continual orders for SBS blister cartons and shelf-ready milk multipacks. Oran hosts Propacking’s 500-tonne-per-day reel line scheduled for 2026, positioning the city as a western logistics hub feeding export corrugated and carton volumes into Spain and West Africa. Constantine anchors the eastern drug cluster and links to Béjaïa’s port, where European board arrives and finished goods depart.

The Algeria folding carton market also benefits from grid reinforcement along the coast: 1,100 megawatts entered service in 2025, damping outage frequency that once crippled long litho runs. Subsidized tariffs of 4.698 dinars per kilowatt-hour remain nationwide, but the IMF warns of adjustments beyond 2027, tilting marginal economics toward energy-efficient digital presses in interior provinces. When Général Emballage’s Naâma mill starts in Q4 2028, western converters will cut freight costs and shorten replenishment cycles, redistributing share toward Oran and Tlemcen.

Interior provinces currently trail because agricultural raw materials ship out for coastal conversion, yet the state’s US 296 million mill outlay, plus SNGID curbside pilots, could trigger satellite carton plants nearer farms by 2031.[3]Algerian Ministry of Environment, “SNGID 2035 Waste Valorization Strategy,” menv.gov.dz If fiber-recovery centers meet quality targets, secondary cities will tilt from carton importers to regional suppliers, deepening Algeria folding carton market penetration across hinterlands.

Competitive Landscape

The Algeria folding carton market features moderate concentration: Général Emballage, Cevital Packaging, and Copac Algérie account for roughly half of sales, while Mondi, Smurfit WestRock, and Huhtamaki serve premium accounts via Moroccan and Tunisian hubs. Général Emballage’s backward-integration bet, the USD 296 million recycled containerboard mill, will supply 350,000 tpa and anchor low-cost substrate flows for its own converting lines and external buyers.

That leverage may compress import-dependent rivals’ margins yet widen board access for small converters. Mid-tier players are answering through technology: Propacking is ramping up capacity and adding digital presses to achieve 500 tonnes per day, while Imprimerie La Tulipe installed a Gallus Labelmaster to handle serialized pharma runs and limited-edition cosmetics. These advancements highlight the growing reliance on innovation to maintain market competitiveness.

Multinationals pursue differentiation through barrier coatings and global brand approvals rather than capacity, although Smurfit WestRock’s 2026 investor plan signals a willingness to partner if Algeria’s licensing hurdles ease.[4]Smurfit WestRock, “Medium-Term Investor Update,” smurfitwestrock.com Strategic vectors now bifurcate: Integrated firms chase upstream scale and EPR compliance, whereas specialists court short-run agility. The next 24 months will prove whether backward integration or digital agility secures faster share gains in the Algeria folding carton market.

Algeria Folding Carton Industry Leaders

Mayr-Melnhof Karton AG

Tetra Pak International S.A

Maghreb Emballage SpA

Mb Algerian Packaging Sarl

Sarl Super Pack

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Général Emballage ordered a complete recycled-containerboard line from Andritz for its Naâma mill, with 350,000 tpa capacity and Q4 2028 start-up.

- March 2026: Smurfit WestRock closed the acquisition of Cartomanabí, adding 50,000 tons of corrugated capacity to reinforce its South America reach.

- March 2026: Mondi completed its EUR 1.2 billion (USD 1.35 billion) multi-mill upgrade, including Štětí’s new machine and Polish box-plant expansions.

- February 2026: Smurfit WestRock unveiled a medium-term plan targeting USD 7 billion EBITDA by 2030, anchored by USD 2.4-2.5 billion capex in 2026.

Algeria Folding Carton Market Report Scope

The scope of the report covers the analysis of the folding carton market in Algeria, focusing on its current trends, growth drivers, challenges, and opportunities. Folding cartons are paper-based packaging solutions widely used across various industries, including food and beverage, healthcare, personal care, and others. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton market in Algeria.

The Algeria Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 Algeria folding carton market size?

The Algeria folding carton market size stands at USD 142.08 million in 2026, and Mordor Intelligence projects it will reach USD 202.93 million by 2031.

Which material type is growing the fastest in folding cartons?

Solid Bleached Sulfate is forecast to expand at an 8.73% CAGR through 2031 as pharmaceutical and cosmetics firms demand virgin-fiber purity.

How is digital printing affecting converters?

Digital printing is expected to grow 8.51% annually, enabling short-run personalization, serialization, and faster artwork changeovers that lithography cannot match at low volumes.

What impact does Law 25-02 have on packaging choices?

The law raised plastic taxes and enforced producer responsibility, leading many brand owners to switch from flexible plastics to recyclable fiber-based folding cartons.

Who are the top players in the Algeria folding carton industry?

Général Emballage, Cevital Packaging, and Copac Algérie jointly control about 50% of the market, while Mondi, Smurfit WestRock, and Huhtamaki service premium niches.

Where are growth opportunities strongest?

E-commerce and retail-ready packaging show the fastest growth at an 8.61% CAGR, driven by online platforms that need tamper-evident, shelf-ready cartons with traceable graphics.

Page last updated on: