Oman Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

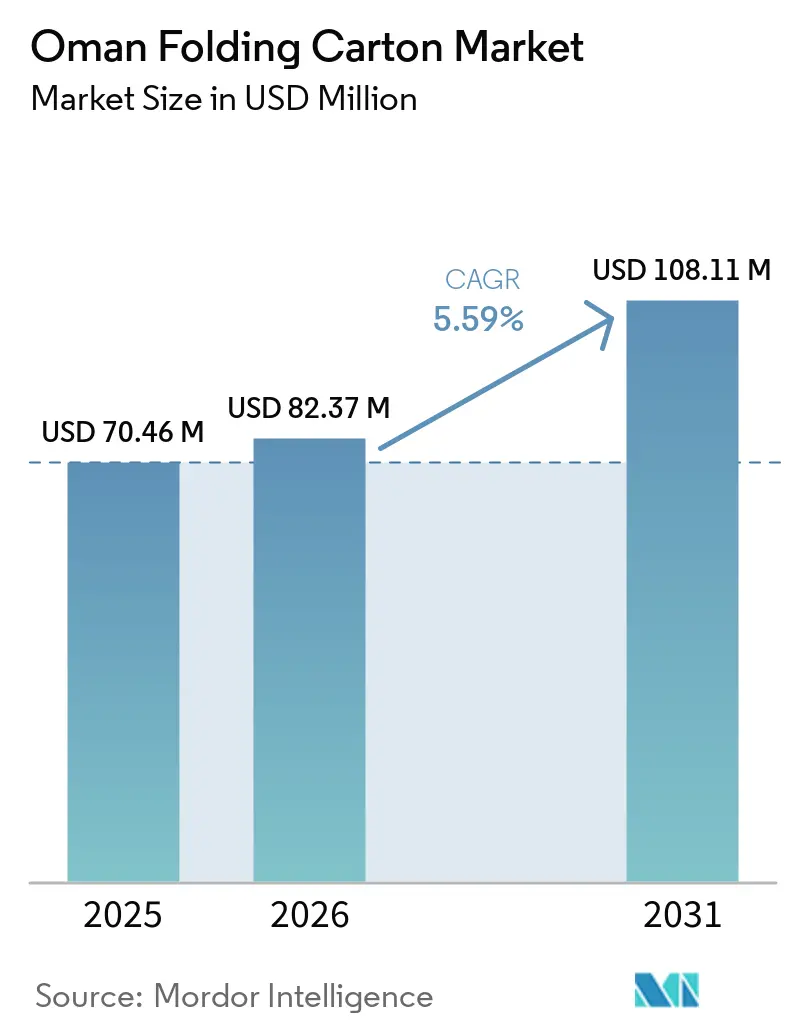

| Base Year Market Size (2025) | USD 70.46 Million |

| Market Size (2026) | USD 82.37 Million |

| Market Size (2031) | USD 108.11 Million |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Folding Carton Market Analysis by Mordor Intelligence

The Oman folding carton market size is projected to expand from USD 70.46 million in 2025 and USD 82.37 million in 2026 to USD 108.11 million by 2031, registering a CAGR of 5.59% between 2026 and 2031. A phased ban on single-use plastic bags, rapid adoption of e-commerce, onshoring of food processing, and rising serialization mandates are simultaneously widening the addressable market for paperboard formats. Retailers are replacing flexible pouches with recycled or virgin cartons to comply with plastics regulations, while brand owners are investing in shorter, personalized print runs to support online sales campaigns. Industrial incentives inside Sohar, Duqm, and Salalah free zones further lower setup costs for new converting lines, encouraging regional and local firms to localize capacity. Supply-chain challenges such as pulp price volatility and desalination-linked utilities still pinch margins, yet tax holidays and duty waivers partly offset these headwinds and sustain steady capital inflows into the Oman folding carton market.

Key Report Takeaways

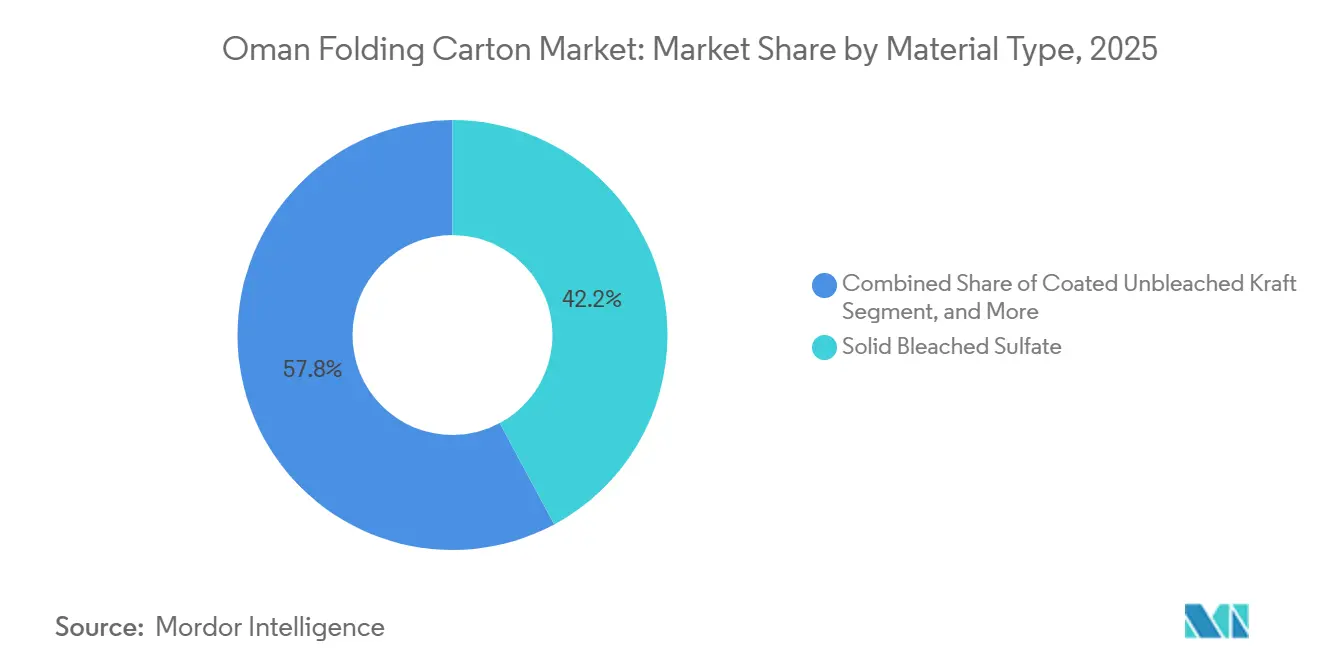

- By material type, solid bleached sulfate captured with 42.16% of the Oman folding carton market share in 2025.

- By printing technology, the Oman folding carton market size for digital printing is projected to grow at a 7.13% CAGR to 2031.

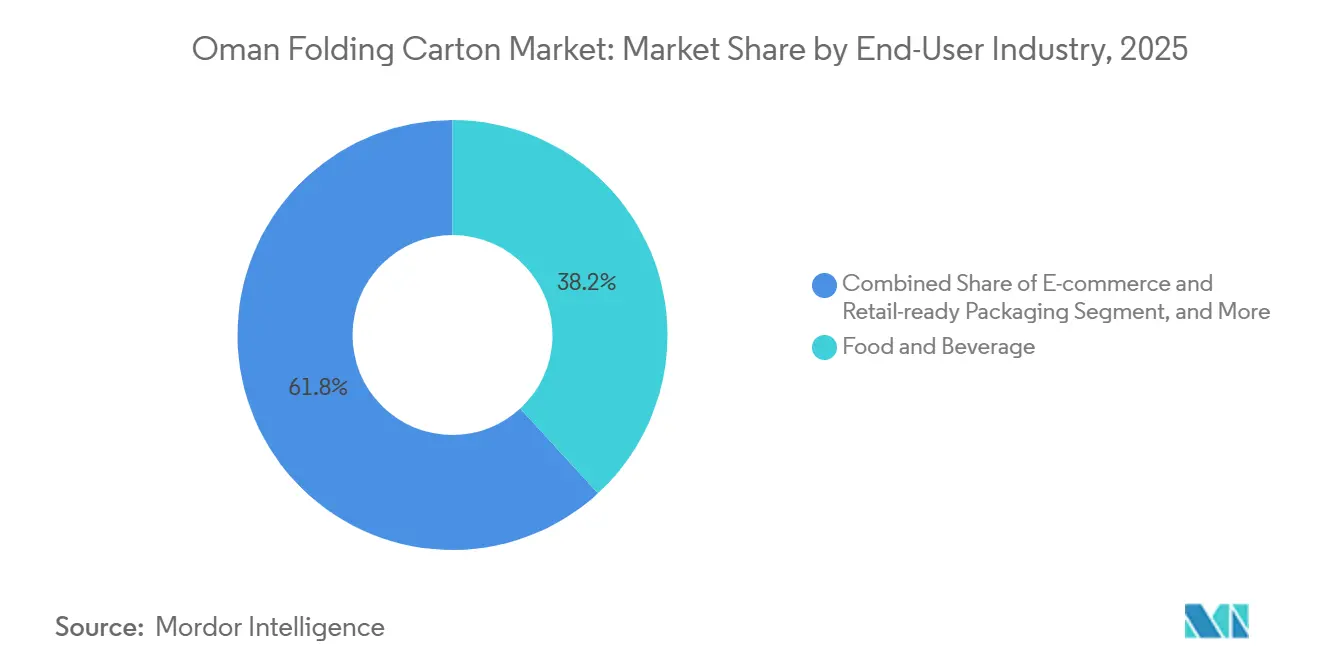

- By end-user industry, the food and beverage industry captured 38.16% of the Oman folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastics Ban Boosts Paperboard Demand | +1.2% | National, with early gains in Muscat, Sohar, Salalah governorates | Short term (≤ 2 years) |

| E-Commerce Expansion Spurs Short-Run Digital Cartons | +1.0% | National, concentrated in Muscat and Sohar logistics hubs | Medium term (2-4 years) |

| Food-Processing Onshoring Under Tanfeedh Program | +0.9% | Duqm, Sohar, Salalah industrial zones | Medium term (2-4 years) |

| Growing Healthcare Serialization Requirements | +0.7% | National, with regulatory compliance in Muscat pharmaceutical distribution | Short term (≤ 2 years) |

| Rising Premium Cosmetics Consumption | +0.5% | Muscat, Salalah tourism-linked luxury retail | Medium term (2-4 years) |

| Governorate Incentives for Manufacturing Investment | +0.6% | Sohar Free Zone, Duqm SEZ, Salalah Free Zone | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastics Ban Boosts Paperboard Demand

Phase 4 of the nationwide bag ban entered force on 1 January 2026, extending the prohibition to date vendors, water sellers, agricultural suppliers, and food stalls. Penalties that double for repeat offenses compress the substitution window and push retailers toward recyclable cartons. Local waste-paper recovery still lags at 12% of the 600,000-tonne annual potential, yet policy targets of 80% recycling by 2030 promise a future feedstock pipeline once collection improves. The regulation, therefore, drives immediate virgin-fiber demand while laying the groundwork for a longer-term circular model inside the Oman folding carton market.

E-Commerce Expansion Spurs Short-Run Digital Cartons

Online retail sales are forecast to grow from USD 660 million in 2024 to USD 1.24 billion by 2029, a trend supported by streamlined customs procedures and the Oman Business Platform’s mandatory registration for web merchants. Smaller brands need multicolor packs in batches of 1,000 units or fewer, favoring inkjet and electrophotographic presses that skip plate-making and slash makeready waste. Converters installing hybrid lines now capture premium margins on personalized gift boxes and seasonal launches, strengthening the Oman folding carton market against imported packaging alternatives.

Food-Processing Onshoring Under Tanfeedh Program

The Sea-to-Shelf initiative guarantees fish quotas of 6,000-30,000 tons per investor in Duqm, Sohar, and Salalah, provided that new plants include downstream canning and carton-packing lines.[1]Food Business Middle East and Africa, “Oman launches Sea-to-Shelf program to transform fisheries sector,” foodbusinessmea.com Tax holidays up to 10 years, subsidized power, and duty-free equipment imports cut payback periods for integrated processors. Each tonne of canned seafood shipped from Duqm requires secondary cartons for chilled export lanes, reinforcing visibility of substrate suppliers in the Oman folding carton market.

Growing Healthcare Serialization Requirements

Circular 141/2023 obliges pharmaceutical firms to embed GS1 barcodes and QR-based electronic inserts on every pack by end-2025, with digital tax stamps on excisable beverages already in effect. Variable-data printing and inspection systems become critical capabilities, steering orders to converters that can reconcile print, code, verify, and aggregate cartons at line speed. The regulation raises technical barriers that concentrate value among technology-ready suppliers in the Oman folding carton market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Virgin Pulp Import Prices | -0.8% | National, affecting all converters reliant on imported paperboard | Short term (≤ 2 years) |

| Water-Scarcity Driven Mill Operating Costs | -0.5% | National, concentrated in Sohar and Muscat industrial areas | Medium term (2-4 years) |

| Competition From Flexible Pouches in Dry Foods | -0.4% | National, particularly in snack and confectionery segments | Medium term (2-4 years) |

| Skills Gap in High-Color Carton Converting | -0.3% | National, with acute shortages in Muscat and Sohar converter clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Pulp Import Prices

Freight surcharges of USD 3,000-3,500 per 40-foot container through the Strait of Hormuz and a 223% rate jump on Asia-to-Europe lanes have inflated linerboard quotes by more than 4% in April 2026. Smaller Omani converters without long-term pulp contracts face margin compression and occasional stock-outs, forcing customers to pre-order cartons or risk service gaps within the Oman folding carton market.

Water-Scarcity Driven Mill Operating Costs

Reverse-osmosis desalination now supplies the bulk of industrial water but comes with high energy intensity and capital costs. The Barka IV plant, for example, cost USD 300 million and operates at 281,000 m³ per day, with tariffs that reflect both amortization and electricity inputs. Rising utility costs directly lift coating and wash-up expenses in Muscat and Sohar print corridors, eroding price competitiveness for some segments of the Oman folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Grades Gain on Strength Demands

Solid Bleached Sulfate held 42.16% of the Oman folding carton market share in 2025, thanks to its premium print surface and food-safe credentials. Coated Unbleached Kraft is projected to outpace overall growth at 7.38% as fisheries canning, beverage multipacks, and chilled seafood exports need high-strength, moisture-resistant cartons. The Oman folding carton market size for kraft grades is therefore expected to climb steadily as Tanfeedh-backed processors ramp new lines.

Converters balancing FSC or PEFC compliance with recycled-content ambitions must also address migration barriers for fatty foods and pharmaceuticals. Folding boxboard continues to serve confectionery and nutraceuticals, while white-lined chipboard satisfies low-cost secondary shippers. Regulated waste-recovery targets could unlock domestic recycled streams by 2030, reducing import dependency and moderating cost pressures in the Oman folding carton market.

By Printing Technology: Digital Gains Amid Offset Dominance

Lithography retained 49.53% share of the Oman folding carton market in 2025, anchoring medium-run commodity jobs. Digital is forecast to expand 7.13% annually as converters install inkjet presses with in-line die-cutting to meet sub-1,000-unit online orders. Investments in ESKO workflows and cloud-based prepress trim turnaround to hours are a critical differentiator for cosmetics and electronics sellers.

Flexography is also gaining favor for mid-volume corrugated and shelf-ready cartons, supported by regional showcases such as Gulf Print and Pack 2026.[2]Packaging MEA, “Flexo Rising: Driving packaging print into a new era,” packagingmea.com Smaller shops that delay automation risk being priced out when raw-material costs spike. The Oman folding carton market size attached to digital and hybrid presses is therefore likely to widen its share incrementally without unseating offset’s bulk-run dominance in the near term.

By End-User Industry: E-Commerce Reshapes Demand Mix

Food and beverage commanded 38.16% of demand in 2025, leveraging HACCP-certified converters for dairy, bakery, and beverage cluster projects in Sohar. Luxury fragrance sales by Amouage rose 33% domestically, stimulating premium carton finishes, foil stamping, and protective inserts. This growth highlights the increasing focus on quality and safety standards in packaging solutions.

E-commerce and retail-ready applications will register the fastest CAGR of 6.85% as online parcel volumes climb. Serialization, tamper-evidence, and consumer-engagement QR codes simplify conversion, tilting sourcing toward plants equipped with camera inspection and automated gluing. Healthcare, personal care, and electronics lines also gravitate toward short lead times, advancing structural design innovation within the Oman folding carton market.

Geography Analysis

Muscat and its satellites dominate consumption, reflecting a concentration of pharmaceutical distributors, luxury retailers, and commercial printers. Sohar Free Zone, linked to a 40-hectare food cluster and a deep-water port, underpins export-oriented seafood and sugar-refining projects that require chilled, moisture-resistant cartons.[3]Public Authority for Special Economic Zones and Free Zones, “Sohar Free Zone,” opaz.gov.om Rusayl Industrial Estate, only 45 km from the capital, offers 100% foreign ownership and five-year profit tax holidays, making it a logical node for brownfield capacity upgrades.

Duqm SEZ spans 2,000 km² and hosts the Sea-to-Shelf fisheries hub, guaranteeing raw-fish quotas that translate into predictable carton procurement cycles. Developers enjoy corporate tax exemptions up to 30 years and VAT suspension, incentives that encourage vertically integrated processors to colocate converting and filling lines. Salalah Free Zone leverages proximity to the Port of Salalah and a budding food cluster of 27 projects.

Value-added incentives attract regional brands that previously imported finished cartons, easing lead times and currency risk. Combined, these zones distribute investment and lift localized demand, reinforcing supply-chain resilience across the Oman folding carton market. Additionally, these developments are fostering a competitive environment, encouraging innovation within the market. The growing focus on sustainability is also driving the adoption of eco-friendly folding carton solutions.

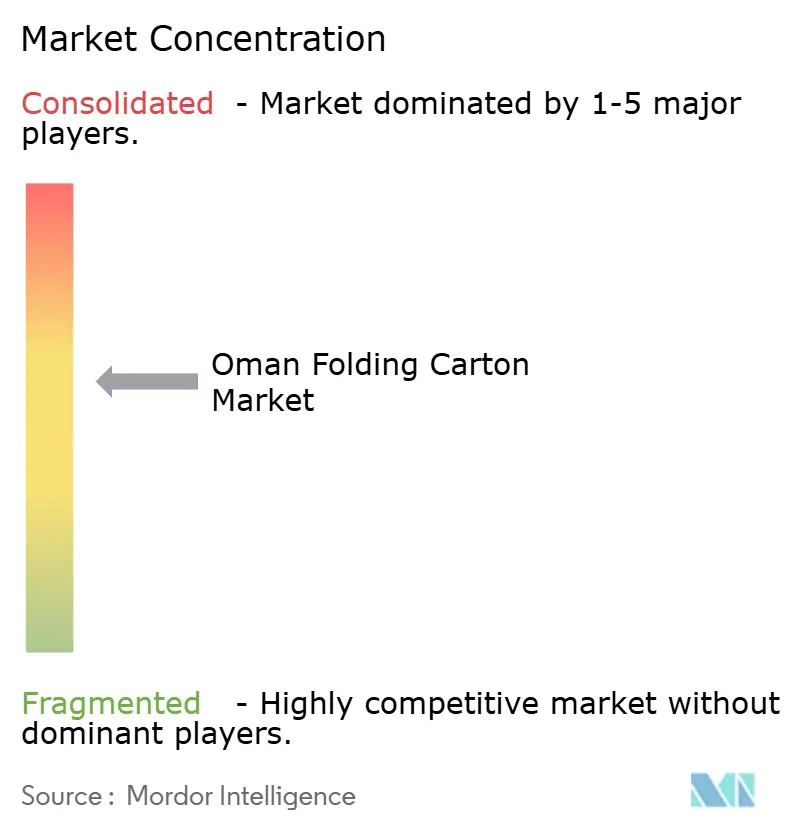

Competitive Landscape

Regional majors and agile locals share the field. United Carton Industries Company booked USD 375 million in revenue in 2025 and is expanding capacity via a USD 20 million line in Ras Al Khaimah, scheduled for completion in 2027. Napco National’s purchase of Arabian Flexible Packaging deepens its Middle East footprint and hints at future cross-border integration in board, film, and label supply.[4]ME Printer, “Napco buys Arabian Flexible Packaging,” meprinter.com Creative Graphics’ new Muscat platemaking hub shortens flexo plate lead times, raises local quality standards, and enables converters to reduce import duties.

Oman Printers and Stationers invested USD 2.6 million in a six-color Heidelberg CX 104, signaling SME appetite for carton diversification. This investment highlights the company's strategic focus on expanding its product offerings to meet evolving market demands. The move also reflects the increasing adoption of advanced printing technologies among SMEs in the region. While the Oman folding carton market faces entry barriers like ISO, HACCP, and FSC certifications, alongside escalating digital workflow demands, enticing factors such as tax holidays and affordable land rents continue to attract new investments.

Moreover, advancements in printing technology promise to boost production efficiency and quality. Companies are increasingly investing in research and development to stay competitive. Furthermore, consumer demand for eco-friendly products is shaping market strategies. The growing adoption of digital printing methods is also transforming production processes. Additionally, regulatory pressures are pushing manufacturers to adopt sustainable practices.

Oman Folding Carton Industry Leaders

United Carton Industries Company

TCPL Packaging Limited

Power Carton L.L.C

Al Bahja Group

Silver Corner Packaging LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: United Carton Industries Company reported 4.6% revenue growth to USD 375 million for FY 2025 and approved a USD 20 million expansion of its Ras Al Khaimah Packaging subsidiary, with completion slated for Q3 2027.

- March 2026: Ocean of Majan International Commercial Services, trading as Bagpak, secured Shariah-compliant working capital from Sharakah to expand woven polypropylene bag production for cement, petrochemicals, and sugar sectors.

- March 2026: Creative Graphics inaugurated its first international facility in Muscat under the Alrasm banner, installing Esko, Miraclon, and Kongsberg systems to supply flexo plates across the Middle East and North Africa.

- December 2025: OQ Group launched nine downstream plastics factories worth USD 104 million at Ladayn Polymer Park, Sohar, producing food containers, dairy films, masterbatches, and medical plastics for export to more than 80 countries.

Oman Folding Carton Market Report Scope

The report provides an in-depth analysis of the folding carton market in Oman, focusing on its current trends, growth drivers, challenges, and opportunities. It examines the market's scope, including the production, consumption, and applications of folding cartons across various industries. The study also evaluates the competitive landscape, supply chain dynamics, and key market players, providing insights into market performance during the forecast period.

The Oman Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Oman folding carton market size?

The Oman folding carton market size stood at USD 82.37 million in 2026 and is forecast to reach USD 108.11 million by 2031.

How fast is the Oman folding carton market expected to grow?

From 2026 to 2031 the market is projected to expand at a 5.59% CAGR, driven by plastics regulation, e-commerce growth, and industrial incentives.

Which material will grow the fastest in Oman’s carton segment?

Coated Unbleached Kraft is expected to record the highest growth, advancing at a 7.38% CAGR through 2031 as seafood, beverage, and frozen food lines demand moisture-resistant strength.

What printing technology is gaining momentum in Oman?

Digital printing is projected to increase at a 7.13% CAGR as brands seek variable data and short runs for online fulfillment, although lithographic presses still hold the largest installed base.

How does e-commerce influence packaging demand in Oman?

Online retail growth of more than 13% annually through 2029 is fueling demand for protective, personalized cartons, prompting converters to add automated digital lines and transit-ready structural designs.

Which free zones offer the best incentives for new folding carton plants?

Sohar Free Zone, Duqm SEZ, and Salalah Free Zone each provide long corporate tax holidays, 100% foreign ownership, and customs duty exemptions, reducing start-up costs for converters.

Page last updated on: